Audit of Low-Dollar-Value Contracting at the Treasury Board of Canada Secretariat

Table of contents

Statement of conformance

The Internal Audit and Evaluation Bureau (the Bureau) has completed an audit of low-dollar-value (LDV) contracting. This audit conforms with the Internal Auditing Standards for the Government of Canada, as supported by the results of the Bureau’s quality assurance and improvement program.

Executive summary

Background

The audit was part of the Treasury Board of Canada Secretariat’s approved Risk-Based Audit Plan for 2015 to 2018.

The Secretariat’s LDV contracts have a low materiality (approximately 4% per year); however, they represent about 40% of the Secretariat’s volume of contracting annually and can be subject to external scrutiny.

LDV contracting at the Secretariat is partially decentralized. The Procurement and Contracting Unit (P&C) is the functional group responsible for contracting goods and services in support of the Secretariat’s departmental activities. Sectors are delegated the authority to complete LDV contracting activities (for contracts below $25,000 for services and below $10,000 for goods);Footnote 1 P&C has operational oversight and support roles in providing information and advice, and in facilitating sectors in LDV contracting activities. In cases where sectors choose not to take up their delegation, their contracting is handled by P&C. During the period covered by this audit, approximately 25% of LDV contracts were processed by sectors under their delegated authority.

Objective and scope

The audit was conducted to provide assurance that the Secretariat’s LDV contracting complies with related P&C policies and procedures, and to determine whether the management and practices of such contracting are efficient and responsive to the needs of the organization.

The audit scope includes LDV contracts processed from to . LDV contracts are those that are below $25,000, as identified in the Supply Manual issued by Public Services and Procurement Canada (PSPC).

Audit results

Two themes emerged related to the challenges and opportunities that face LDV contracting at the Secretariat:

- the need for department-specific LDV contracting policies, procedures, guidance and training that support consistent and sufficiently articulated information management practices and operational compliance

- the need for a performance measurement framework and related processes that support oversight and continuous improvement

Department-specific policies, procedures, guidance and operational compliance

The Treasury Board’s Contracting Policy sets out the broad strategic direction and principles of contracting, and federal departments are responsible for developing guidelines that are specific to their own operating environment. Although the Secretariat has applied the Government of Canada’s (GC’s) policies for procurement and contracting, the audit found that the Secretariat’s internal process was not supported by a sufficiently articulated policy framework specific to LDV contracting that outlines key foundational elements. Such elements would normally include defined roles and responsibilities, as well as operational requirements for managing information and documentation, administering contracts, and managing processes for monitoring and performance.

With respect to operational compliance, contract planning was sound, as contract requirements were adequately defined and documented. However, the following areas for improvement were identified:

- contract initiation, where proper authorization was missing for some commitments

- contract administration, where there was inadequate authority documentation found in a significant number of files, insufficient tracking information, and inconsistent data entry to substantiate an audit trail

- information management, where inadequate documentation and records management limited the ability to conclude on the verification and approval of payments for contracts

Oversight and performance measurement

Strategic and operational oversight within the Secretariat for LDV contracting is limited. Although there were a few reporting and monitoring activities, there was no documentary evidence of ongoing performance measurement. There was also inconsistent understanding of roles and responsibilities for oversight and monitoring among stakeholders.

There is a need to implement an ongoing process for performance measurement and a degree of oversight that is appropriate to LDV contracting. Such a process and oversight should include clear roles and responsibilities to support continuous improvement and to measure the extent to which the LDV contracting process is efficient and responsive.

Conclusion

Because of issues with documentation and information management, the audit could not conclude on whether the LDV contracting process properly adhered to contract administration and payment requirements. In order to provide assurance that contracting authorities and segregation of duties are maintained, enhancements to the authorities verification process are needed that relate specifically to the following sections of the Financial Administration Act (FAA);

- section 32 (Expenditure Initiation and Commitments Authority)

- section 34 (Certification of Contract Performance)

- section 41 (Contracting Authority)

In addition, due to limited performance measurement and strategic oversight, the audit could not conclude on whether the management and practices of LDV contracts are efficient and responsive to the needs of the organization.

To support decentralized LDV contracting activities at the Secretariat, improvements to policies, procedures, guidance, training, documentation and information management are needed. These improvements will address the majority of contracting administration and compliance issues noted in the audit. As well, enhancements to oversight and implementation of a performance measurement framework will support continuous improvement.

Recommendations have been made in the report to address the areas for improvement.

Management response

The Secretariat has developed a management response and action plan, which is presented in Appendix C.

1. Introduction

According to the Supply Manual issued by Public Services and Procurement Canada (PSPC) (formerly Public Works and Government Services Canada), LDV contracts are those that are below $25,000.

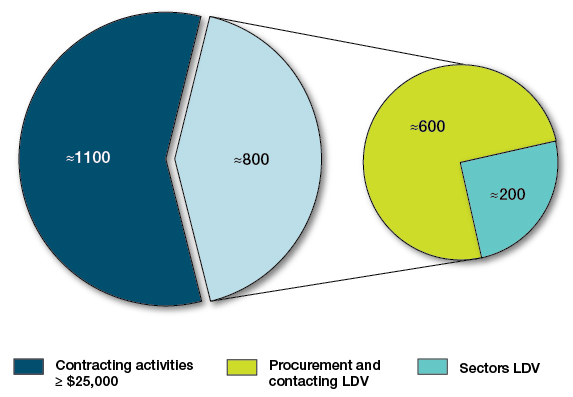

Over three years, from April 2012 to March 2015, the Treasury Board of Canada Secretariat issued approximately 1,900 contracts that had a total value of about $180 million. The approximately 800 LDV contracts issued during that period accounted for about 40% of the total number of Secretariat contracts and roughly 4% of total contract value.

Figure 1 - Text version

| Breakdown of low-dollar-value contracting activities at the Secretariat from to | Number of contracts |

|---|---|

|

Total number of contracts for $25,000 or more

|

Approximately 1,100 |

|

Total number of contracts for less than $25,000

|

Approximately 800 |

| Number of low-dollar-value contracts processed by the Procurement and Contracting Unit and by sectors and branches | |

|

Number of low-dollar-value contracts processed by the Procurement and Contracting Unit

|

Approximately 600 |

|

Number of low-dollar-value contracts processed by sectors and branches

|

Approximately 200 |

Although LDV contracts have a low materiality, they represent approximately 40% of contracting volume and can be subject to scrutiny (proactive disclosure). The audit was launched in , with audit examination starting in and completed by . The audit scope includes LDV contracts processed from to to provide an assessment on the design and operating effectiveness and efficiency of the Secretariat’s control framework over the procurement and contracting process.

LDV contracting at the Secretariat is partially decentralized through two streams:

- issuing contracts through P&C under the definition provided by PSPC’s Supply Manual

- through sectors using thresholds below $10,000 for goods and $25,000 for services

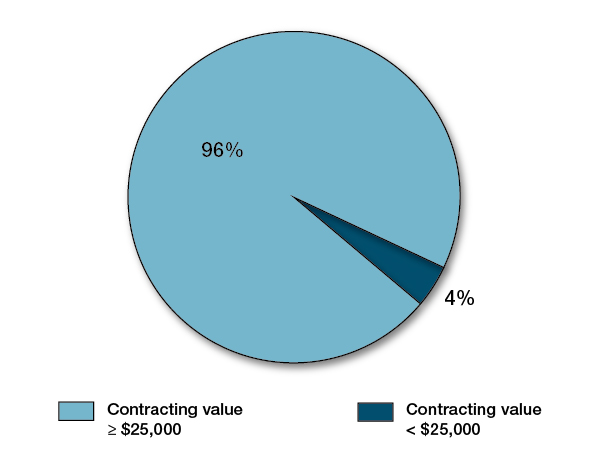

Figure 2 - Text version

| Contracting value | Proportion of contracts by value (per cent) |

|---|---|

| Contracting value above $25,000 | 96 |

| Contracting value below $25,000 | 4 |

The departmental LDV contracting delegation program, which provided managers of sector fund centres with the authority to issue contracts, was implemented at the Secretariat late in the 2011 to 2012 fiscal year to address a significant backlog of contracting requests at P&C.

Under the decentralized process, P&C, which is part of the Secretariat’s Corporate Services Sector, is the functional group responsible for contracting goods and services in support of the Secretariat’s departmental activities. Although sectors are delegated the authority to complete certain LDV contracting activities, P&C has operational oversight and support roles in providing information and advice, and in facilitating LDV contracting activities for sectors. During the period covered by the audit, P&C had significant employee turnover (discussed in subsection 3.1.1 of this report).

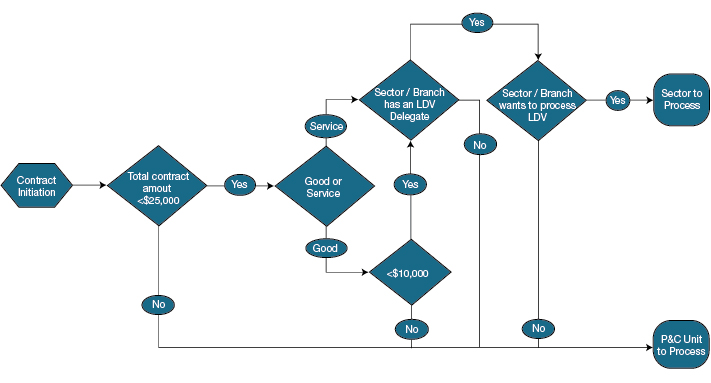

Figure 3 illustrates the processes for deciding which stream a LDV contract follows.

Figure 3 - Text version

Upon the contract’s initiation, determine whether the total amount of the contract will be for less than $25,000.

If the contract will be for less than $25,000, determine whether the contract is for a good or service. If the contract will be for $25,000 or more, the Procurement and Contracting Unit will process the contract.

If a contract for less than $25,000 is for a service, determine whether the sector or branch has a delegate for low-dollar-value contracts. If there is such a delegate, determine whether the sector or branch wants to process the contract. If it does, the sector or branch will proceed. If the sector or branch does not have a delegate for low-dollar-value contracts, the Procurement and Contracting Unit will process the contract.

If a contract for less than $25,000 is for a good, determine whether the contract will be for less than $10,000. If it is, determine whether the sector or branch has a delegate for low-dollar-value contracts. If there is such a delegate, determine whether the sector or branch wants to process the contract. If it does, it will proceed. If it does not want to process the contract, the Procurement and Contracting Unit will process the contract. If the sector or branch does not have a delegate for low-dollar-value contracts, the Procurement and Contracting Unit will process the contract.

If the contract is for a good and is for $10,000 or more, the Procurement and Contracting Unit will process the contract.

File administration relating to LDV contract responsibilities are split between contract file leads (P&C or sectors for contract administration) and the Financial Management Directorate of the Secretariat’s Corporate Services Sector (for contract payments).

1.1 Reasons for the audit

The Treasury Board’s Contracting Policy states that the objective of government procurement and contracting is to acquire goods and services in a manner that enhances access, competition and fairness, and that results in the optimal balance of overall benefits to the Crown and to Canadians.

LDV contracting activities are expected to respect these objectives. Although the materiality of LDV contracts in terms of dollar value is low, such contracts represent approximately 40% of the Secretariat’s departmental contracts processed. Regardless of the dollar value of the contract, reputational risk remains, given the organization’s role as a central agency and the scrutiny of the use of the public funds.

2. Audit details

2.1 Authority

The Audit of Low-Dollar-Value Contracting is part of the Secretariat’s approved Risk-Based Audit Plan for 2015 to 2018.

2.2 Objectives and scope

The objective of the audit was to provide assurance that the Secretariat’s contracting process for LDV contracts complies with related procurement and contracting policies and procedures, and to determine whether the management and practices of the Secretariat’s departmental LDV procurement and contracting are efficient and responsive in support of the needs of the organization.

The audit scope covers the contracting process of LDV contracts (below $25,000) to provide an assessment of the design and operating effectiveness and efficiency of the Secretariat’s control framework over the procurement and contracting process.

The audit was launched in , and audit procedures were initiated in . The audit examination was concluded in .

2.3 Scope exclusions

The audit did not address the following:

- the use of acquisition cards

- memoranda of understanding with other government departments and agencies

- confirming orders

- Task Authorizations issued under an existing contract

- low-dollar-value contracts issued by the Secretariat’s Internal Audit and Evaluation Bureau

2.4 Approach and methodology

The audit approach and methodology was risk-based and conformed with the Internal Auditing Standards for the GC. These standards require that the audit be planned and performed in a way so that obtains reasonable assurance that the audit objectives were achieved.

The audit included various tests and procedures considered necessary to provide such assurance, including interviews, documentation reviews, process walkthroughs,Footnote 2 data analysis and a survey. There was also a detailed examination and testing of selected samples, specifically, 24 files led by P&C and 26 files led by sectors.

Audit procedures were applied to a judgmental sample of contracts, and amended contracts, below $25,000 and issued between , and .

2.5 Lines of enquiry

The audit had three lines of enquiry:

- the Secretariat has in place key elements of a management control framework for LDV procurement and contracting that meets Treasury Board and departmental requirements

- LDV contracting activities are conducted in compliance with relevant GC and departmental legislation, policies and guidelines

- LDV contracting activities are conducted in an efficient manner and are responsive to the needs of the organization

Detailed audit sub-criteria for each of these audit criteria are presented in Appendix A.

3. Audit results

Two underlying themes emerged related to the challenges and opportunities that face the Secretariat’s LDV contracting:

- the need for a department-specific policy framework for LDV contracting that is supported by consistent and sufficiently articulated information management practices and that underpins operational compliance (lines of enquiry 1 and 2)

- the need for a systematic and formal oversight or performance measurement framework and processes that incorporate feedback for continuous improvement (line of enquiry 3)

3.1 Departmental policies, procedures, guidance and operational compliance regarding LDV contracting

3.1.1 Department-specific policies, procedures and guidance

The Treasury Board’s Contracting Policy sets out the broad strategic direction and principles of contracting. Federal departments are responsible for developing guidelines that are specific to their own operating environment.

To facilitate LDV contracting at the Secretariat, P&C (of the Secretariat’s Corporate Services Sector) developed tools, including guidelines and training, to support and provide information on LDV contracting activities. However, the process was not supported by a departmental policy framework that is specific to LDV contracting and that outlines key foundational elements for policies, procedures and guidance. Foundational elements would include operational requirements for the following:

- LDV contracting procedures and processes

- roles and responsibilities

- contract administration

- monitoring and reporting

- information and documentation management

The audit found that the Secretariat’s internal LDV contracting policies, procedures, guidance and training were insufficient, particularly for non-expert contracting authorities. Sector contracting authorities stated in interviews that the quantity and complexity of tools that support LDV contracting were overwhelming, and that guidance that was commensurate with some contracts’ complexity was not provided sufficiently. For example, the audit found that there were guidance gaps for contract initiation and segregation of duties. LDV contracting tools, which included training and written guidelines, were developed by P&C functional specialists. The tools, in order to be used successfully, rely on an in-depth and broad understanding of contracting concepts and rules that are complex.

Audit interviews with sector contracting authorities and results from the audit survey revealed that training was inadequate to meet their needs. Many sectors continued to rely on P&C to ensure that their contracts met requirements and complied with applicable law, regulations and policies.

The lack of clarity for non-expert contracting authorities was further complicated by a high turnover of P&C employees, which impacted P&C’s capacity to support sectors.

In the opinion of the audit team, enhancements to policies, procedures, guidance and training will address the majority of contracting administration and compliance issues noted in the audit. These issues are summarized in subsection 3.1.2.

3.1.2 LDV contracting compliance

The audit found that contract planning was generally sound, with contract requirements adequately defined and documented. However, several areas for improvement were identified with respect to contract initiation and contract administration.

The following seven findings relate to LDV operational compliance and illustrate the need for enhanced policies, procedures, guidance and training at the departmental level:

- Insufficient sole-source justification:

- The sector sample files show two sole-sourced contracts that did not contain written justification. In addition, the rationales for five other contracts were not sufficient. This lack of justification and rationale could limit the ability to justify decisions and affect the ability of decisions to withstand public scrutiny.

- Inconsistencies in the segregation of duties at the sector level:

- The same employee performed section 34 and 41 authorizations for more than half of the sectors’ 26 sample files. Improper segregation of duty increases the risk of inappropriate contracting, although none was found in the course of this audit.

- Insufficient maintenance of the list of authorized contracting authorities:

- Of the 26 sample files from sectors, 11 contracts and amendments were not signed by authorized delegates. Interviews with personnel from P&C indicate that the list of authorized contracting authorities has not been kept up to date. This could lead to mistaken authorization. In addition, properly authorized contracts could be deemed inappropriate.

- Data entry errors and inconsistencies:

- A significant number of sample files from P&C (11 of 24) and sectors (24 of 26) contain data entry errors and inconsistencies. Inconsistencies were mostly associated with contract award date, whereas errors were often related to commodity types and contracting methods. The latter occurred most frequently with sample files from sectors. Such errors and inconsistencies contribute to an increased risk of inaccurate reporting, which was evidenced through an examination of a sample of proactive disclosures, which showed several inconsistencies in what was reported.

- Contract and payment files had incomplete documentation and improper authorization in some cases:

- For P&C-led contract files, there were 14 instances of inadequate authorization relating to sections 32 and 41 of the FAA.

- There were 29 sector-level findings that included inadequate section 32 and 41 authorization and justification for sole-source contracts.

- Ten payment files administered by the Financial Management Directorate did not contain evidence of invoices on file.

The above contract administration and document management findings limit the ability of the Secretariat to provide assurance and verification that key controls are functioning as intended, particularly with regard to proper authorization of transactions.

- The Secretariat’s processes for informing Security Services about site or information access were not consistently followed:

- In 10 of 26 cases, there was no evidence of consultation or approval from Security Services on security aspects of the contract. Lack of such evidence and consultation limits the ability of the Secretariat to validate that individuals are not being exposed to information that is above their security classification level.

- The approved Security Requirements Check List (SRCL) was sometimes not on file or was not filled out properly:

- Three P&C-led contract files did not have SRCLs that were approved and signed according to requirements, and six sector contract files were either incomplete or did not have approval from Security Services. Lack of such approvals and not having complete contracts limits the ability of the Secretariat to verify that protected and classified information and assets remain secure.

Because of the gaps in documentation and information management inconsistencies that led to the above findings, the audit could not conclude on whether the LDV contracting process properly adhered to contract administration requirements, or that payments had been properly verified and approved. The audit also found that employees involved with LDV contracting did not consistently follow departmental security validation processes. Improved clarity in guidance and training, and in information management practices, would resolve many of the findings.

The Financial Management Directorate of the Secretariat’s Corporate Services Sector implemented the Account Verification Framework in to support the improvement of payment process and information management practices for contract payments. The management of P&C has expressed its intention to improve information management and documentation related to contract files.

Recommendation: establish and implement a department-specific LDV policy framework

- The Assistant Secretary, Corporate Services Sector, should develop and implement department-specific policies, procedures, guidance and training to clarify LDV contracting (for P&C and sectors). Such activities should:

- clarify roles and responsibilities, and enhance guidance for all aspects of the LDV process

- ensure that contracting activities comply with GC policies through an appropriate ongoing monitoring process

- specify consistent and sufficiently articulated information management practices

3.2 Performance measurement and oversight

The audit expected that oversight and performance measurement would be conducted to support effective and efficient contracting and strategic direction, and to support continuous improvement of contract processes. Performance measurement would identify key risks for LDV contracting and define performance measurement activities that are commensurate with their value and potential impact in order to support oversight and trend analysis of LDV contracting.

There is no systematic performance measurement process that supports strategic oversight and continuous improvement of LDV contracting. For example, the tracking of the distribution of contracting volume by user and the results of compliance testing were not routinely performed. These types of activities would have enabled P&C to analyze performance and to identify strengths and weaknesses in contracting within the Secretariat.

There is also limited departmental guidance, which has led to the following:

- confusion about the roles and responsibilities for LDV contracting oversight

- operational oversight that is inconsistently communicated and implemented

Two client satisfaction surveys were conducted by P&C (in 2014 and in 2015). However, there was no evidence that the survey results were used for process improvements. Although contracting service standards on contracts processed by P&C are published, interviews with P&C personnel indicate that those standards are not being used to measure services, and that existing performance measurement reporting activities are done on an ad hoc basis.

Recommendation: enhance oversight and performance measurement over LDV contracting

- The Assistant Secretary, Corporate Services Sector, should define an approach to overseeing LDV contracting that is informed by a formal, ongoing and documented performance measurement process that is commensurate with the risk, value and volume of LDV contracting.

- The performance measurement process should:

- identify key risks for LDV contracting activities and define performance measures, establish baselines, and develop trends analysis for these risks

- establish feedback, monitoring and reporting mechanisms to support strategic oversight

3.3 Overall conclusion

Because of documentation and information management issues, the audit could not conclude on whether the LDV contracting process properly adhered to contract administration and payment requirements. In order to provide assurance that contracting authorities and segregation of duties are maintained, enhancements to the authorities verification process are needed, specifically as they relate to the following sections of the FAA:

- section 32 (Expenditure Initiation and Commitments Authority)

- section 34 (Certification of Contract Performance)

- section 41 (Contracting Authority)

Due to limited performance measurement and strategic oversight, the audit could not conclude on whether the management and practices of LDV contracts are efficient and responsive to the needs of the organization.

To support decentralized LDV contracting activities at the Secretariat, improvements to policies, procedures, guidance, training, documentation and information management are needed. These improvements will address the majority of contracting administration and compliance issues noted in the audit. As well, enhancements to oversight and implementation of a performance measurement framework will support continuous improvement.

Recommendations have been issued in the report to address the areas for improvement.

Appendix A: Audit criteria

Line of enquiry 1: the Secretariat has in place key elements of the management control framework for low-dollar-value procurement and contracting that meet departmental and Treasury Board requirements

Audit criteria

Line of enquiry 2: low-dollar-value contracting activities are conducted in compliance with departmental and relevant GC legislation, policies and guidelines

Audit criteria

Line of enquiry 3: low-dollar-value contracting activities are conducted in an efficient manner and are responsive to the needs of the organization

Audit criteria

Appendix B: definitions

- audit trail

- The elements that allow tracking of a complete process. Elements of an audit trail include delegation of authorities’ matrices, user profiles, and the data and files required to reconstruct the sequence of events and the transactions processed.

- authority

- The right to perform certain acts or prescribe rules governing the conduct of others. Generally, under balanced schemes of management, administrative authority represents the activation of corporate policy and is coupled with responsibility and accountability.

- competitive contract

- A contract where the process used for the solicitation of bids enhances access, competition and fairness, and assures that a reasonable and representative number of suppliers are given an opportunity to bid though the options specified in the Government of Canada’s Contracting Policy.

- contract administration

- A process of systematically and efficiently managing contract development, implementation and administration for maximizing financial and operational performance and for managing inherent risk. Contract management encompasses the life cycle of a contract and involves many stakeholders, including, but not limited to, the contracting officer, the client department and the supplier.

- contract amendment

- An agreed addition, deletion, correction or modification to a contract.

- contracting authority

- The person authorized or sub-delegated to enter into a contract on behalf of Canada according to section 41 of the Financial Administration Act.

- contract planning

- The phase of the procurement life cycle that involves the activities associated with identifying, defining and planning a requirement, including the determination that procurement is the appropriate instrument, the development of specifications or statements of work, and the development of the procurement strategy.

- contractor

- One who contracts to perform work or furnish materials in accordance with a contract.

- Corporate Service Sector

- The sector of the Treasury Board of Canada Secretariat that provides internal corporate services to the Secretariat in the areas of financial management, security, information management and technology, facilities and materiel management.

- expenditure initiation authority

- The authority, according to section 32 of the Financial Administration Act, to incur an expenditure or to make an obligation to obtain goods or services that will result in the eventual expenditure of funds. Such authority includes the authority to hire staff; order supplies or services; authorize travel, relocation or hospitality; or enter into some other arrangement for program purposes.

- Financial Administration Act (FAA)

- An act to provide for the financial administration of the Government of Canada, the establishment and maintenance of the accounts of Canada, and the control of Crown corporations. The FAA provides legislative requirements for financial management of the Government of Canada.

- fund centre manager

- The individual responsible for all transactions against a fund centre according to the Delegation of Financial Signing Authorities.

- information management

- The management of information (including custodianship and documentation) within an organization, throughout the life cycle of a project or process, including planning, acquisition, systems development, distribution, and disposal or long-term preservation.

- low-dollar-value contracting

- A departmental senior management initiative to delegate low-dollar-value and low-complexity contracting authority of goods (less than $10,000) and services (less than $25,000) to fund centre managers at the Secretariat (excludes standing offers and supply arrangements).

- low-dollar-value (LDV) contracting authority

- For the purpose of this audit, those groups that avail themselves of the LDV contracting process in order to issue an LDV contract.

- non-competitive contract

- Any contract for which bids were not solicited, or, if bids were solicited, the conditions of a competitive contract that were not met.

- non-expert contracting authorities

- Authorities that have low levels of experience in the contracting process. Such authorities could include new procurement and contracting employees who have no prior experience beyond training, and authorities that have delegated authority for contracting outside the Secretariat’s Procurement and Contracting Unit.

- oversight body

- A body that monitors an organization’s performance, including progress on plans related to projects or initiatives and progress against any other set expectation, makes adjustments, and takes corrective actions to ensure that expectations are met. Continuous oversight ensures that decisions are implemented as intended, strategies are met, and delegation of authorities are appropriate to ensure effective decision making and that performance meets expectations.

- payment authority

- The authority to requisition payments according to section 33 of the Financial Administration Act.

- Security Requirements Check List (SRCL)

- A form used to identify security requirements associated with a contract that has protected or classified security requirements.

- Task Authorization (TA)

- A method of supply for services under which all the work or a portion of the work will be performed as and when requested, through predetermined conditions. Contracts that have TAs are used in situations when there is a defined need by a client to rapidly have access to one or more categories of consultants that are expected to be needed on a repetitive basis during the period of the contract.

Appendix C: management response and action plan

Overall observations of Corporate Services Sector (CSS)

In 2012, the Secretariat began to pilot decentralized low-dollar-value (LDV) contracting, where sectors were delegated the authority to complete LDV contracts (up to $25,000 for services and up to $10,000 for goods), with guidance and oversight from CSS’s Procurement and Contracting Unit (P&C).

This audit has been helpful in demonstrating the opportunities and challenges of decentralized LDV contracting, and CSS agrees with its recommendations. The management response below reflects the GC’s move toward a more centralized approach to LDV contracting and the Secretariat’s contribution to the GC working group that is developing new procurement policies for LDV.

Recommendation 1: establish and implement a department-specific LDV policy framework

- The Assistant Secretary, Corporate Services Sector, should develop and implement department-specific policies, procedures, guidance and training to clarify LDV contracting (for P&C and sectors). Such activities should:

- clarify roles and responsibilities, and enhance guidance for all aspects of the LDV process

- ensure that contracting activities comply with GC policies through an appropriate ongoing monitoring process

- specify consistent and sufficiently articulated information management practices

Priority ranking: high

Management response

CSS agrees with the recommendation.

To address this recommendation, CSS will review its policies, procedures, guidance and training relating to LDV contracting. Accordingly, it will undertake the management actions listed in the following table.

| Management action | Completion date | Action owner |

|---|---|---|

| Action A: Clarifying roles and responsibilities, and enhancing guidance needed for all aspects of the LDV process | ||

|

Corporate Administration and Security Directorate (CASD) | |

|

CASD | |

|

CASD | |

|

CASD | |

| Action B: Ensuring that contracting activities comply with GC policies through an appropriate ongoing monitoring process | ||

CSS will:

|

CASD | |

|

CASD | |

|

CASD | |

| Action C: Specifying consistent information management practices | ||

CSS will:

|

CASD, Accounting Services (AS) | |

|

CASD, AS | |

|

CASD, AS | |

Recommendation 2: enhance oversight and performance measurement over LDV contracting

- The Assistant Secretary, Corporate Services Sector, should define an approach to overseeing LDV contracting that is informed by a formal, ongoing and documented performance measurement process that is commensurate with the risk, value and volume of LDV contracting.

- The performance measurement process should:

- identify key risks for LDV contracting activities and define performance measures, establish baselines, and develop trends analysis for these risks

- establish feedback, monitoring and reporting mechanisms to support strategic oversight

Priority ranking: medium to high

Management response

CSS agrees with the recommendation.

To address this recommendation, CSS will develop an approach for the oversight of LDV contracting that is informed by a formal, ongoing and documented performance measurement process that is commensurate with the risk, value and volume of LDV contracting. As such, it will undertake the management actions listed in the following table.

| Management action | Completion date | Action owner |

|---|---|---|

| Action A: identify key risks for LDV contracting activities and define performance measures, establish baselines and develop trends analysis for these risks | ||

CSS will:

|

CASD | |

|

CASD | |

|

CASD | |

|

CASD | |

| Action B: establish feedback, monitoring and reporting mechanisms to support strategic oversight | ||

As part of the review of policies, procedures, guidance and training relating to LDV contracting (see Recommendation 1, Actions B1, B2 and B3), CSS will:

|

CASD | |

|

CASD | |

Page details

- Date modified: