Below are highlights from our commentary on the 2023–2024 financial audits. For the complete commentary, download the PDF version of the document.

Commentary on the 2023–2024 Financial Audits

Report metadata

- Tabling date:

- Report type

- Commentaries on financial audits

Results of our 2023–2024 financial audits

The Office of the Auditor General of Canada provided the government with an unmodified audit opinion on its 2023–24 consolidated financial statements, which provides credibility to the government’s financial reporting.

Overall, for our other financial audits, we were satisfied with the credibility of the financial statements prepared by 68 of the 69 federal government organizations we audited.

Approval of corporate plans

The majority of Crown corporations’ corporate plans, which set out their planned activities for the next 5 years, were not approved by the government before the start of their fiscal year. Corporations can operate under existing plans but cannot make changes or undertake new activities, such as investing in major infrastructure, without an approved plan.

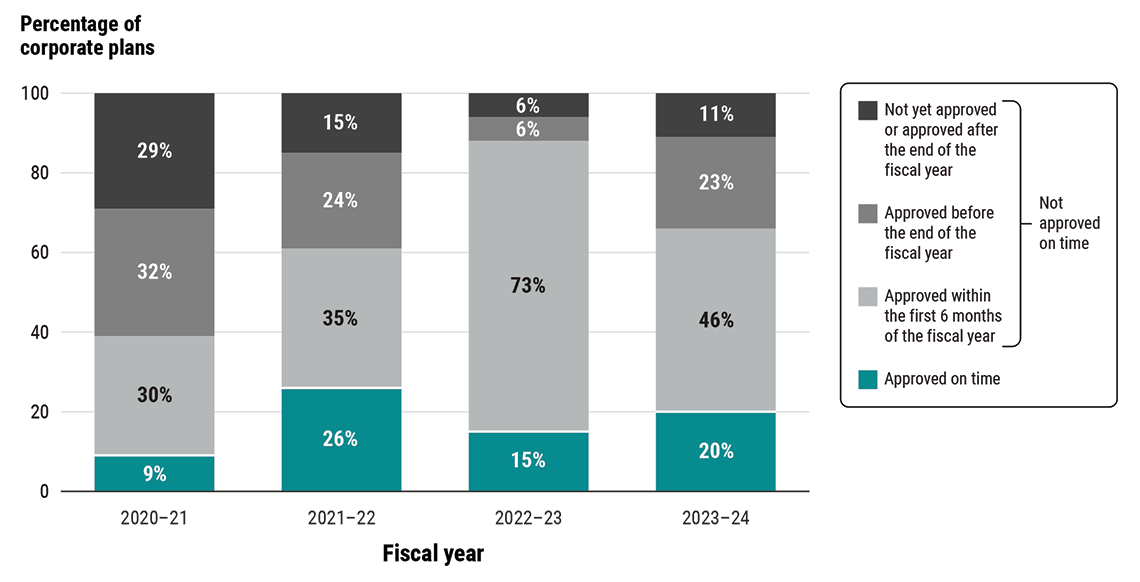

Percentage of corporate plans approved at various points

during the Crown corporation’s fiscal year

Source: Based on the Office of the Auditor General of Canada’s analysis of data on approval dates for Crown corporations’ corporate plans

Text version

This stacked bar chart shows the percentage of Crown corporation corporate plans approved on time from the 2020–21 to 2023–24 fiscal years and the percentage of corporate plans not approved on time in the same period, divided into 3 categories:

- Not yet approved or approved after the end of the fiscal year

- Approved before the end of the fiscal year

- Approved within the first 6 months of the fiscal year

Overall, the majority of the corporate plans were not approved on time.

The corporate plans that were not yet approved or approved after the end of the fiscal year decreased from 29% in 2020–21 to 15% in 2021–22 and 6% in 2022–23, then increased to 11% in 2023–24.

The corporate plans approved before the end of the fiscal year decreased from 32% in 2020–21 to 24% in 2021–22 and 6% in 2022–23, then increased to 23% in 2023–24.

The corporate plans approved within the first 6 months of the fiscal year increased from 30% in 2020–21 to 35% in 2021–22 and 73% in 2022–23, then decreased to 46% in 2023–24.

The corporate plans approved on time increased from 9% in 2020–21 to 26% in 2021–22, then decreased to 15% in 2022–23, and increased to 20% in 2023–24.

One such example was the Canada Post Corporation, which has been without an approved corporate plan since 2020. This is particularly concerning because it has been operating at a loss for the past few years.

The Canada Post Corporation stated that changes to its operations are needed to remain competitive and financially self‑sustaining. Without action from the Government of Canada, there is a risk that the corporation could run out of cash by July 2025.

COVID-19 benefits programs

Overpayments or ineligible payments

Our 2022 performance audit report Specific COVID‑19 Benefits recommended that the government update its post‑payment verification plans to identify overpayments or payments to ineligible recipients.

Through post-payment verifications, the Government of Canada has identified almost $6 billion in overpayments or payments to ineligible recipients of COVID‑19 benefits in 2023–24. This brings the amount identified over the past 4 years to a total of $17.2 billion.

The government has stated that post-payment verifications will continue for years. However, we remain concerned that it may not be investigating significant amounts of payments made to ineligible individuals or businesses, which it therefore may not identify or recover.

Repayment of Canada Emergency Business Account loans

This year, the government received repayments from Canada Emergency Business Account loan recipients and expects to receive additional repayments in coming years.

The government loaned $49.1 billion through this program. It forgave up to 33% as an incentive if the recipient repaid the required portion of the loan by an established deadline.

As at 31 March 2024, approximately $8.5 billion of the loans was still to be repaid.

The Auditor General’s observations on the Government of Canada’s 2023–24 consolidated financial statements

Preparation of the consolidated financial statements

We identified opportunities for improvement in the preparation of the consolidated financial statements of the Government of Canada.

One example was that the Office of the Comptroller General should provide more oversight of departments and agencies to ensure consistency across government for important estimates.

Pay administration

Pay errors continued for many government employees in 2023–24.

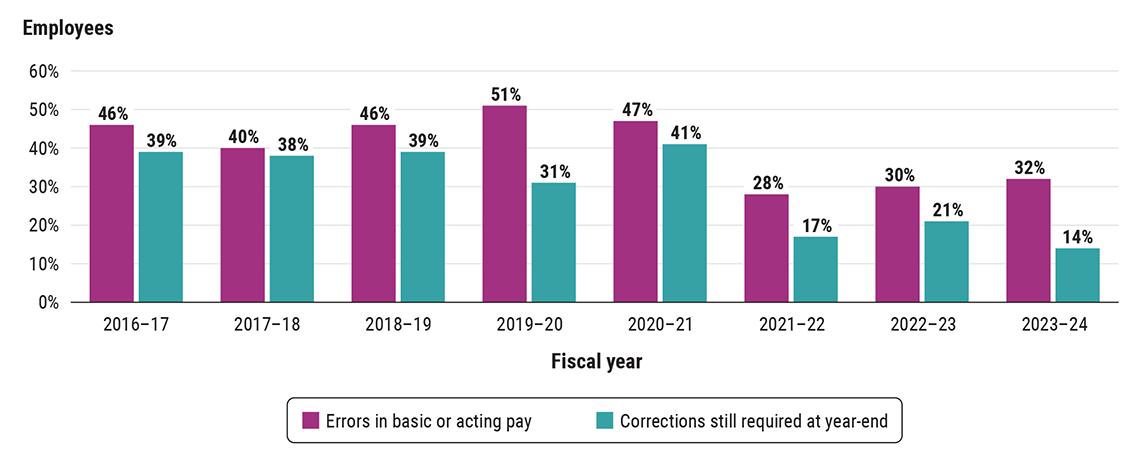

Percentage of employees in our sample with an error in basic or acting pay

and who were awaiting a correction at year‑end

Source: Based on the Office of the Auditor General’s analysis of a sample of employees’ pay transactions used in the audit of the consolidated financial statements of the Government of Canada for the 8 fiscal years ending March 31 from 2017 to 2024

Text version

This bar chart shows for each fiscal year from 2016–17 to 2023–24 the percentage of employees in our sample with an error in basic or acting pay and who were awaiting a correction at year‑end.

The chart shows that the percentage of employees in our sample who had an error in basic or acting pay during the fiscal year decreased from 46% in 2016–17 to 40% in 2017–18 and then increased to 46% in 2018–19 and to 51% in 2019–20. The percentage then decreased to 47% in 2020–21 and to 28% in 2021–22. In 2022–23, the percentage increased to 30% and increased again in 2023–24 to 32%.

The chart also shows that the percentage of employees in our sample who were awaiting a correction at year‑end was steady at either 38% or 39% for the 3 fiscal years from 2016–17 to 2018–19 and then decreased to 31% in 2019–20. The percentage then increased to 41% in 2020–21, decreased to 17% in 2021–22, and increased to 21% in 2022–23. In 2023–24, the percentage decreased to 14%.

Information technology general controls

Our audit again noted deficiencies in general controls over key government information technology (IT) systems.

IT general controls are controls over access to systems and data, how system changes are managed, and how the system operates.

We again found deficiencies in controls over access to key systems that store and process data related to payments, receipts, and accounting records. This increases the risk of fraud, privacy breaches, or other wrongdoing. Since March 2024, the government has made significant progress in addressing access risks.

Asset retirement obligations

The Government of Canada owns various assets, like buildings, equipment, and vehicles. When it is time to retire some of these assets, the government needs to take action, such as removing asbestos.

The estimated cost of retiring these assets is called an asset retirement obligation and needs to be assessed by the government as part of an accounting standard that came into effect last year.

As of 31 March 2024, the government estimated that it had asset retirement obligations of $12.5 billion. However, we noted there were data quality issues at some federal departments, which means their estimates of asset retirement obligations may not be accurate.

National defence inventory and asset pooled items

For over 2 decades, we have raised concerns about National Defence’s ability to properly account for the quantities and values of its inventory.

In our audit this year, we found errors in 20% of the items we sampled, compared with 17% the year before. In our view, these continued errors indicate that further improvements to internal controls are needed.

Also, the department has fallen further behind schedule to implement a modern scanning and barcoding system. The department projects the system will be fully operational in the 2030–31 fiscal year—a 4‑year delay from its original expected date.

Additional insights

Environmental, social, and governance reporting

The government requested that larger Crown corporations—those with $1 billion in assets or more—report on climate-related risks and opportunities as well as other sustainability matters. In 2023–2024, this applied to 17 Crown corporations whose financial statements we audit.

We reviewed a sample of the disclosures by these corporations and noted that the format of the reporting varied widely, as did the depth and breadth of what matters they viewed as relevant to their business and industry.

We also noted that some disclosures on climate-related risks were not always linked to the Crown corporation’s strategic objectives.

Find out more

Videos