Office of the Auditor General of Canada’s 2026–27 Departmental Plan

Contents:

Copyright information

© His Majesty the King in Right of Canada, as represented by the Auditor General of Canada, 2026

Catalogue number: FA1-24E-PDF

ISSN 2371-7661

At a glance

This departmental plan details the Office of the Auditor General of Canada’s (OAG’s) priorities, plans, and associated costs for the upcoming 3 fiscal years.

Text version

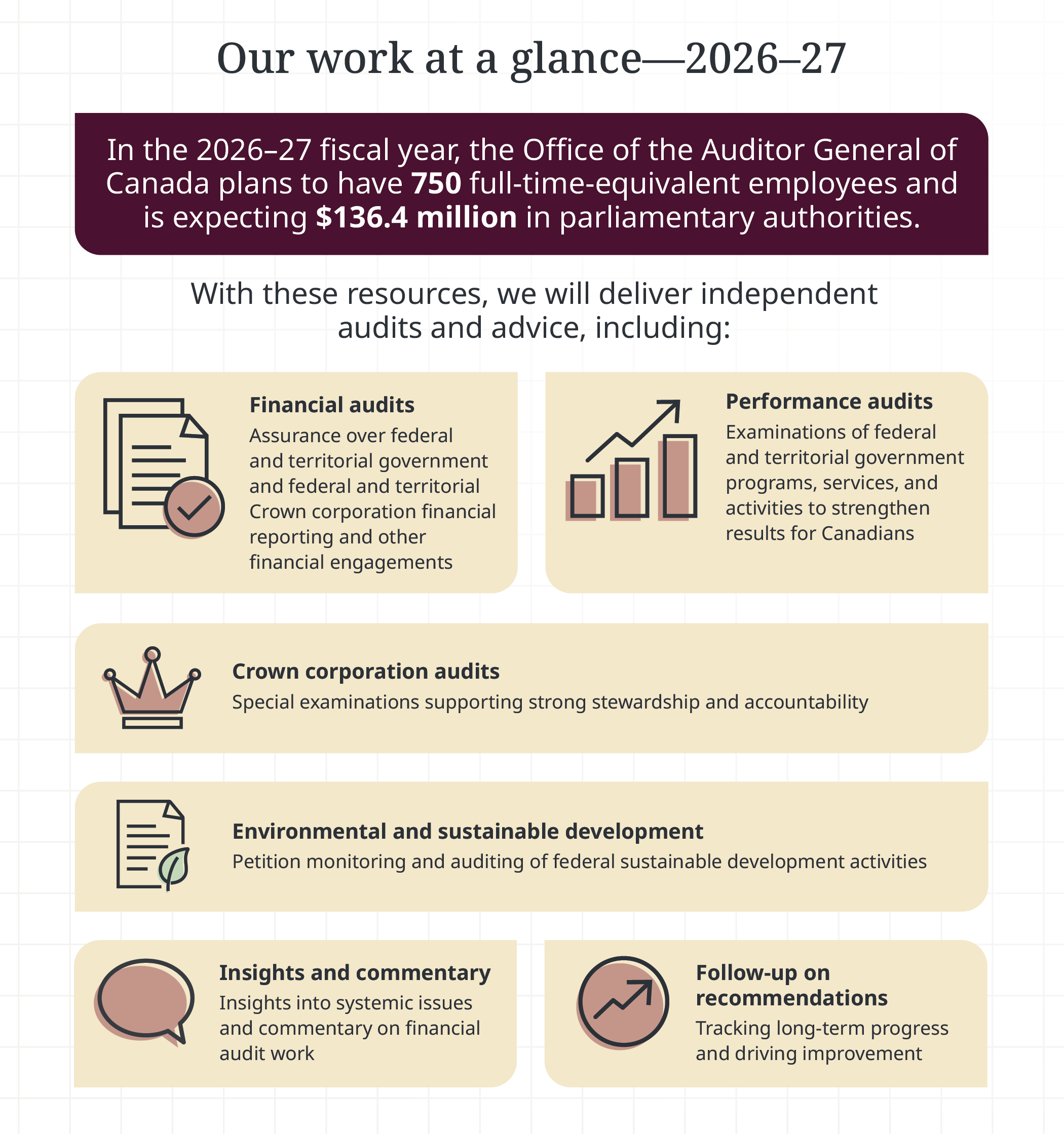

Our work at a glance—2026–27

In the 2026–27 fiscal year, the Office of the Auditor General of Canada plans to have 750 full-time-equivalent employees and is expecting $136.4 million in parliamentary authorities.

With these resources, we will deliver independent audits and advice, including:

- Financial audits. Assurance over federal and territorial government and federal and territorial Crown corporation financial reporting and other financial engagements.

- Performance audits. Examinations of federal and territorial government programs, services, and activities to strengthen results for Canadians.

- Crown corporation audits. Special examinations supporting strong stewardship and accountability.

- Environmental and sustainable development. Petition monitoring and auditing of federal sustainable development activities.

- Insights and commentary. Insights into systemic issues and commentary on financial audit work.

- Follow-up on recommendations. Tracking long-term progress and driving improvement.

Key priorities

In the 2026–27 fiscal year, the OAG will advance multiple initiatives in support of our core responsibility, legislative auditing, with a particular focus on the following priorities:

- delivering audits of the future, including enhancing our audit practices while maintaining the high level of quality work that the OAG is known for, expanding the use of innovative technologies, and implementing enhancements to audit tools and workflows

- strengthening accountability through transparency, including implementing a systematic approach for assessing and reporting on the status of the implementation of recommendations by federal departments and agencies and delivering our first annual report on this topic

- empowering a future-ready workforce, including upgrading our human resources tools and policies, modernizing our OAG workspaces, deepening our use of data to strengthen decision making, and increasing digital literacy across the organization

Comprehensive Expenditure Review

The government is committed to restraining the growth of day-to-day operational spending to make investments that will grow the economy and benefit Canadians.

The OAG was not asked to commit to planned reductions under the Comprehensive Expenditure Review.

The OAG will, however, respect the spirit of the exercise by doing the following:

- identifying opportunities to improve productivity and efficiency across the office while continuing to deliver high-quality audit work to Parliament and legislative assemblies

- leveraging digital tools and technologies, supported by training and change management, to increase our ability to plan and deliver audits

- implementing targeted expenditure reductions and reallocating resources within existing reference levels to align with strategic priorities

This departmental plan reflects these measures.

Highlights for the OAG in 2026–27

In support of the key priority for 2026–27 to strengthen accountability through transparency, the OAG will advance initiatives designed to help Canadians and parliamentarians track progress by federal departments and agencies on our audit recommendations. A key milestone will be the release of the Auditor General of Canada’s first annual report on the status of the implementation of past recommendations. We will also begin work on a public-facing online portal that consolidates information about government responses and actions taken on audit findings. Through these initiatives, the OAG will enhance accountability, reinforce trust in public institutions, and promote continuous improvement across federal organizations.

Another priority initiative for 2026–27 will be completing the workspace modernization project, which will update the Ottawa office to provide a more accessible, flexible, and digitally enabled workplace and reduce our Ottawa office space footprint. These renovations of our Ottawa office will enhance technology integration, facilitate collaboration, and improve the employee experience.

A third priority initiative, specifically tied to our multi-year digital transformation, includes piloting and adopting new tools and technologies, including artificial intelligence (AI) and automation solutions, and continuing upgrades to our information technology infrastructure.

To learn more about these initiatives, see the Our planned results: Corporate initiatives section in the full plan.

In 2026–27, total planned spending (including internal services) for the OAG is $136,428,682, and the total planned full-time-equivalent staff (including internal services) is 750.

Summary of planned results

The following provides a summary of the results that the OAG plans to achieve in 2026–27 under its main area of activity, called “core responsibility.”

Core responsibility: Legislative auditing

The OAG is the legislative audit office for the Government of Canada and the governments of the 3 northern territories. Through our audit reports, we provide assurance and recommendations to improve public sector programs, service delivery, and financial management and reporting. We plan to deliver a broad suite of performance audits at the federal and territorial levels, conduct several special examinations, complete approximately 100 financial audits, and undertake multiple other financial engagements during the 2026–27 fiscal year.

More information about legislative auditing can be found in the full plan. Planned spending: $136,428,682

Planned human resources: 750

For complete information on the OAG’s total planned spending and human resources, read the Planned spending and human resources section of the full plan.

Message from the Auditor General of Canada

Auditor General of Canada

I am pleased to present the 2026–27 Departmental Plan of the Office of the Auditor General of Canada (OAG). As we head into the next fiscal year, the OAG continues to advance its mission of strengthening accountability and trust in Canada’s public institutions. Our work, which is conducted independently and grounded in evidence, helps Parliament hold government organizations to account while encouraging improvement in how programs and services are delivered to Canadians.

At the midpoint of my mandate, and as the OAG nears its 150th anniversary, I am reminded that this institution’s strength lies in its people—their professionalism, dedication, and commitment to serving Parliament and Canadians with integrity. The same service mindset that has always guided our work continues to drive our focus today: to provide objective insights that help government perform better.

In the coming fiscal year, we plan to complete approximately 100 financial audits, conduct additional financial engagements, deliver a broad portfolio of performance audits, and carry out several special examinations of Crown corporations. We will also assess the value of our work across parliamentarians and territorial legislators, audited organizations, and other users of our audits to ensure that our work remains impactful and relevant.

Moving forward, our organizational priorities will continue to emphasize innovation, collaboration, and digital readiness, ensuring that we remain well equipped to meet the growing expectations of Canadians and the evolving challenges facing the public service. We will continue to upgrade our audit tools and methods, drawing on new technologies and approaches to enhance the quality and impact of our work. We will also launch our first annual report tracking the implementation of past audit recommendations, an important step toward greater transparency and accountability.

The current fiscal environment is a reminder that all public institutions must be disciplined in their use of resources. The OAG is committed to enhancing its productivity by pursuing increasingly efficient ways to deliver results. That means simplifying our processes, onboarding new technologies, and reallocating resources where they are best positioned to enhance the value of our core mandate activities.

As we look forward to the next fiscal year, our priorities remain clear: delivering high-quality audits that make a difference for Canadians, communicating our findings in ways that drive change, and empowering a skilled, adaptable, and future-ready workforce.

It is a privilege to work alongside the talented people at the OAG as we continue to serve Parliament and Canadians with integrity and excellence while creating opportunities to evolve how we work for a better Canada, one audit at a time.

Karen Hogan, FCPA

Auditor General of Canada

Plans to deliver on the core responsibility

Core responsibility: Legislative auditing

In this section

Description

Our audit reports provide objective, fact-based information and advice on government programs and activities. With our audits, we support Parliament in its authorization and oversight of government spending and operations.

Our audits also help territorial legislatures, boards of Crown corporations, and audit committees in their oversight of the management of government activities. Those charged with governance use our audit findings to hold their respective organizations to account for the handling of public funds.

Financial audits assess whether the annual financial statements of the Government of Canada, the territories, Crown corporations, and others are presented fairly and are consistent with applicable accounting standards.

Performance audits assess whether government organizations manage programs with due regard for economy, efficiency, and environmental impact and measure their effectiveness. We have incorporated the assessment of equity, diversity, and inclusion as a priority area for our performance audits and also consider the United Nations’ Sustainable Development Goals when planning and reporting on these audits.

Special examinations assess whether Crown corporation systems and practices provide reasonable assurance that assets are safeguarded and controlled, resources are managed economically and efficiently, and operations are managed effectively.

Quality of life impacts

As an independent agent of Parliament, the OAG indirectly contributes to the Quality of Life Framework for Canada domains, subdomains, and indicators. Our reports inform Parliament on the efficiency, effectiveness, economy, and environmental effects of government programs and financial management.

Through our legislative assurance reports, we highlight areas for improvement in government programs and services that, when acted on, can positively affect Canadians’ quality of life.

The framework’s domain, subdomain, and indicator that relate most closely to legislative auditing are as follows:

- Domain: Good governance

- Subdomain: Democracy and institutions

- Indicator: Confidence in institutions

Indicators, results, and targets

This section presents details on the OAG’s indicators, the actual results from recently reported fiscal years, and the targets and target dates for the OAG’s core responsibility of legislative auditing.

Exhibit 1—Indicators, targets, and results for legislative auditing

Exhibit 1 provides a summary of the target and actual results for each indicator associated with the results under our core responsibility, legislative auditing.

Departmental result: Government acts on recommendations to improve public sector programs, service delivery, and financial management and reporting.

| Departmental result indicators | Actual results Footnote 1 | 2026–27 target | Date to achieve target |

|---|---|---|---|

| Percentage of performance audit and special examination recommendations implemented | 2023–24: 84% 2024–25: 88% | At least 85% of the recommendations have been implemented, 3 years after tabling | March 31, 2027 |

| Percentage of financial audit recommendations implemented | 2023–24: 91% 2024–25: 88% | At least 85% of the recommendations have been implemented, 2 years after they were issued | March 31, 2027 |

Additional information on the detailed results and performance information for the OAG’s program inventory is available on GC InfoBase.

Plans to achieve results

The following section describes the planned results for the OAG’s core responsibility of legislative auditing in 2026–27.

Departmental result: Government acts on recommendations to improve public sector programs, service delivery, and financial management and reporting.

The OAG conducts independent audits that provide objective and timely information, advice, and assurance to Parliament, territorial legislatures, boards of Crown corporations, government, and Canadians. The result the OAG seeks to achieve is that the government acts on the recommendations arising from our audit work to improve public sector programs, service delivery, and financial management and reporting.

Results we plan to achieve

Our work drives continuous improvement across public sector organizations at the federal and territorial levels and supports those charged with governance in fulfilling their oversight responsibilities. Through objective, fact-based audits of the federal government and Crown corporations and of territorial governments and corporations, we help identify risks and barriers to effective program and service delivery and provide action-oriented recommendations to address root causes. By delivering high-quality audits on a timely basis, we provide insights that help Parliament and Canadians ensure that public resources are managed responsibly and that government commitments translate into meaningful results for Canadians.

Our planned results: Audit operations

Performance audits. Our federal performance audits in 2026–27 will encompass a variety of topics that hold significant interest for Canadians. In 2026–27, we plan to deliver a range of performance audit reports, including those presented to Parliament by the Commissioner of the Environment and Sustainable Development and those presented to northern legislative assemblies. Our reports will include topics such as:

- the National Emergency Strategic Stockpile inventory

- the status of the pay system in the federal public service

- whether the Royal Canadian Mounted Police is recruiting officers in a timely and effective way to meet operational requirements

- basic training in the Canadian military

- how federal assets, services, and activities are being protected against climate change on the basis of commitments made in the Greening Government Strategy

- early learning and childcare in the territories

Financial audits and engagements. Each fiscal year, the OAG conducts financial audits and related work across multiple jurisdictions and organizations of varying sizes that apply multiple accounting frameworks.

In 2026–27, we will complete approximately 100 financial audits, including the audit of the Public Accounts of Canada; audits of the 3 territorial governments, most federal Crown and territorial corporations, and many other federal organizations; and multiple other financial engagements, including engagements for First Nations groups in relation to tax administration agreements.

Special examinations. Special examinations are a form of performance audit that is conducted within parent Crown corporations. Special examinations take place at least once every 10 years. In 2026–27, the OAG plans to complete approximately 6 special examinations across a range of federal Crown corporations.

Follow-up on recommendations. Building on earlier groundwork, the OAG will launch a systematic approach for assessing and reporting on the status of the implementation of audit recommendations by departments and agencies and deliver its first annual report on the status of the implementation of past recommendations. This initiative will provide Parliament and Canadians with transparent, accessible information about government progress on audit recommendations.

International activities. In 2026–27, the OAG will continue to actively participate in and contribute to the committees and working groups of the International Organization of Supreme Audit Institutions, advancing good governance and accountability practices worldwide. We will also continue to leverage opportunities to host international fellows and support capacity building among partner supreme audit institutions. In addition, we will begin preparations for a peer review of the OAG that will be completed in 2029, reinforcing our commitment to transparency, quality, and continuous improvement.

Quality of work. Our reputation and the trust Canadians place in us are firmly grounded in the quality of the work we deliver to Parliament, territorial legislatures, and the boards of directors of Crown corporations. We are dedicated to consistently providing high-quality audits that are relevant, outcome-focused, and aligned with the needs of those we serve. In 2026–27, we will continue to prioritize quality management activities, including targeted training, to ensure our people are equipped to conduct the audits of the future while upholding established professional standards.

Our planned results: Corporate initiatives

Digital enablement. In 2026–27, the Digital Services Group’s focus will be on digital enablement across the organization.

On the auditing side, we are equipping audit teams with modern digital capabilities, platforms, and support and will continue this work in 2026–27. This includes piloting and adopting new tools and technologies, such as a new audit tool; participating in pilot projects offered by Government of Canada service providers, including AI and automation; and embedding digital expertise into audit planning and execution.

To further our plans to digitally enable our workforce in 2026–27, we will continue to focus on advancing employee digital competencies across the OAG by delivering targeted learning programs, hands-on innovations, and ongoing awareness initiatives in such areas as AI, cybersecurity, data management, and reporting. We are also focused on skills development within the Digital Services Group to support the OAG workforce to confidently adopt and maximize digital tools, platforms, and emerging technologies.

In 2026–27, we will also continue to upgrade our digital infrastructure (including continuing our onboarding to Government of Canada enterprise applications) to enable collaboration, productivity, and flexibility in our work environment. We are implementing our data strategy to ensure high-quality, actionable, and reportable data that provides insights for decision making.

Workplace modernization. In 2026–27, the OAG will complete the workplace renewal initiative to refit its Ottawa office, incorporating the latest Government of Canada workplace standards for accessibility, flexibility, and collaboration.

The project will include refined layouts, ergonomic furniture, enhanced acoustics, and inclusive design features to improve employees’ experiences and support diverse work needs. This modernization will position the OAG to operate more efficiently while promoting workforce vitality, engagement, and environmental sustainability.

Audit innovation. In 2026–27, the OAG will continue evolving its audit practices by leveraging innovative technologies and data‑driven methods to enhance audit quality, efficiency, and impact. We will pilot the use of innovative technologies, adopt new tools where appropriate, and improve our approaches to become more efficient. These initiatives will ensure that the OAG’s audits remain relevant and efficient and provide Parliament with clear, actionable insights on issues that matter to Canadians.

Skilled, inclusive, and future-ready workforce. In 2026–27, the OAG will focus on ensuring that employees are well positioned to deliver value-added work that advances our mandate. We will continue to strengthen the employee experience by supporting learning and development for the skills and competencies needed and by designing a human resources organizational structure that better supports our people and their work. We will also continue updating our human resources policies, tools, and systems to ensure they are barrier-free and responsive while fostering a workplace culture that values inclusion and removes barriers to participation for all employees.

Key risks

The OAG proactively manages risks that could impact its ability to achieve its strategic priorities and deliver on its mandate. The organization maintains a dynamic and responsive approach to risk management, continuously scanning the environment and refining mitigation strategies to ensure resilience and agility.

Key areas of focus include:

- audit quality: upholding the integrity, consistency, and high standards of excellence in audit work

- relevance: reimagining the organization’s approaches to ensure audits remain timely, impactful, and aligned with the evolving priorities of Parliament, the territorial legislatures, and the needs of Canadians

- cybersecurity: strengthening the protection of OAG systems and data against increasingly sophisticated digital and cyber threats

Planned resources to achieve results

Exhibit 2—Planned resources to achieve results for legislative auditing

Exhibit 2 provides a summary of the planned spending and full-time equivalents required to achieve results.

| Resource | Planned |

|---|---|

| Spending | $136,428,682 |

| Full-time equivalents | 750 |

Complete financial and human resources information for the OAG’s program inventory is available on GC InfoBase.

Related government priorities

Gender-based analysis plus

In 2026–27, the OAG will strengthen the integration of gender-based analysis plus (GBA Plus) across its legislative audit work and internal management practices. This work supports the OAG’s commitment to equity, diversity, inclusion, accessibility, and reconciliation while ensuring that its audit practices and workplace culture reflect these principles in a consistent and meaningful way.

In its audit work, the OAG will continue to apply GBA Plus considerations during audit planning and analysis to assess how federal organizations incorporate gender and diversity perspectives in their programs, policies, and service delivery. The OAG will further refine its audit guidance to help audit teams identify how impacts, systemic barriers, and data limitations vary across groups and affect the experiences of diverse populations. Opportunities will also be explored to enhance the collection and use of disaggregated information, where relevant to audit objectives, and to refine the way we communicate within our reports to the public.

Internally, the OAG will maintain the application of GBA Plus considerations to enhance the employee experience from recruitment to offboarding, providing a seamless, inclusive, and positive journey to all employees. This includes monitoring workforce representation; updating policies, processes, and tools; and advancing initiatives under its people management plans. Training, tools, and advisory support will continue to build employee capacity to apply GBA Plus in both audit and corporate contexts.

These efforts align with the Government of Canada’s Gender Results Framework, the Quality of Life Framework for Canada—Good Governance domain, and the United Nations’ Sustainable Development Goals, particularly the goal of gender equality (Goal 5), the goal of reduced inequalities (Goal 10), and the goal of peace, justice, and strong institutions (Goal 16). The OAG also continues to consider the Truth and Reconciliation Commission’s Calls to Action and the United Nations Declaration on the Rights of Indigenous Peoples when audit work involves Indigenous people or reconciliation-related themes.

United Nations’ 2030 Agenda for Sustainable Development and the United Nations’ Sustainable Development Goals

The OAG has committed to aligning its audit work to support the United Nations’ 2030 Agenda for Sustainable Development and the underlying 17 Sustainable Development Goals. All of the OAG’s audits—financial audits, performance audits, and special examinations—contribute to the goal of peace, justice, and strong institutions (Goal 16). In addition, we consider the other goals when planning and reporting on our audit work. For example, the OAG’s performance audits planned for the 2026–27 fiscal year will contribute to several of the goals, such as the goal of climate action (Goal 13), the goal of good health and well-being (Goal 3), and the goal of quality education (Goal 4). At an organizational level, we aim to reduce the OAG’s ecological footprint, which supports the goal of responsible consumption and production (Goal 12); to better withstand the impact of climate change, which supports the goal of climate action (Goal 13); and to ensure that we have a diverse and inclusive workforce, which supports the goal of reduced inequalities (Goal 10).

More information on how the OAG supports the 2030 Agenda and the Sustainable Development Goals, as well as our contributions to the Federal Sustainable Development Strategy, can be found in our departmental sustainable development strategy.

Artificial intelligence

The OAG’s current AI use and plans for AI use in 2026–27 are as follows:

Increase productivity. Over the next fiscal year, the OAG will continue to expand its use of AI to enhance productivity. Building on multiple AI experiments completed to date—which have demonstrated measurable time savings in tasks such as text summarization, generation, and translation and spreadsheet automation—the organization will move toward a broader, more integrated adoption of these capabilities. Planned initiatives include extending the use of AI-enabled tools to further streamline audit topic research, sentiment analysis, and code development and the use of virtual assistants in some areas.

Decrease government operating costs. We are planning to increase our experimentation and use of AI tools to find further efficiencies in our work, including leveraging some Government of Canada AI tools. For example, we plan to use AI tools hosted by Shared Services Canada to support the OAG’s annual audit selection process, improve back-office productivity, and promote innovative practices.

Improve service delivery. Although all teams are encouraged to explore the benefits of AI, 3 audits have been prioritized to use AI capabilities in the audit reporting phase to help the OAG improve service delivery and deliver on our mandate.

The value in AI adoption is assessed by comparing manual versus AI-assisted task durations, error rates, overall process efficiency, and user feedback on task efficiency and quality.

In 2026–27, the OAG will advance its AI enablement plan by delivering key initiatives that support both employee readiness and operational integration of AI. Short-term efforts will focus on publishing guidance on responsible AI use, providing additional access to AI tools, implementing training programs on using AI for specific purposes, and AI knowledge-sharing initiatives.

Program inventory

The OAG’s core responsibility is supported by the sole program in our program inventory, legislative audit.

Additional information related to the program inventory for legislative auditing is available on the Results page on GC InfoBase.

Summary of changes to reporting framework since last year

We have made the following changes to our departmental results framework for 2026–27:

- minor edits to the text for our core responsibility and program

Planning for contracts awarded to Indigenous businesses

To ensure Indigenous businesses are supported in OAG procurement activities, we continue to raise organizational awareness, particularly among those involved in procurement and contract management. Socio-economic considerations, including support for Indigenous businesses, have been incorporated as a mandatory step in our integrated procurement and contract management process. The Contracting and Procurement team provides ongoing support and a challenge function to responsible managers, helping to ensure that Indigenous businesses are consistently considered in procurement planning wherever feasible.

In 2026–27, we will continue to identify additional opportunities to procure goods and services from Indigenous businesses and enhance oversight of this procurement process. Progress will be tracked and reported on a quarterly basis, with related risks actively managed.

Finally, we will maintain set-aside opportunities for qualified Indigenous suppliers under our Audit and Related Services Supply Arrangement and leverage whole-of-government supply arrangements managed by Public Services and Procurement Canada and Shared Services Canada that include Indigenous suppliers, covering a range of equipment, furniture, support, and services.

Exhibit 3—Percentage of contracts planned and awarded to Indigenous businesses

Exhibit 3 presents the current, actual results with forecasted and planned results for the total percentage of contracts the OAG awarded to Indigenous businesses.

| 5% reporting field | 2024–25 actual result | 2025–26 forecasted result | 2026–27 planned result |

|---|---|---|---|

| Total percentage of contracts with Indigenous businesses | 8.79% | A minimum of 5% | A minimum of 5% |

Planned spending and human resources

This section provides an overview of the OAG’s planned spending and human resources for the next 3 fiscal years and of planned spending for 2026–27 with actual spending from previous years.

Spending

This section presents an overview of the OAG’s actual and planned expenditures from 2023–24 to 2028–29.

Budgetary performance summary

Exhibit 4—Three-year spending summary for core responsibility (dollars)

Exhibit 4 presents the OAG’s spending over the past 3 years to carry out its core responsibility. Amounts for the 2025–26 fiscal year are forecasted based on spending to date.

| Core responsibility | 2023–24 actual expenditures | 2024–25 actual expenditures | 2025–26 forecast spending |

|---|---|---|---|

| Legislative auditing | 134,929,754 | 132,403,257 | 133,172,562 |

Analysis of the past 3 years of spending

Actual spending for 2024–25 decreased slightly compared with 2023–24, primarily because of temporary cost reduction measures caused by funding uncertainties arising from the prorogation of Parliament. Forecast spending for 2025–26 is expected to remain consistent with 2024–25, reflecting our commitment to increasing efficiency in the current fiscal environment.

More financial information from previous years is available on the Finances section of GC Infobase.

Exhibit 5—Three-year spending on core responsibility (dollars)

Exhibit 5 presents the OAG’s planned spending over the next 3 years for its core responsibility.

| Core responsibility | 2026–27 planned spending | 2027–28 planned spending | 2028–29 planned spending |

|---|---|---|---|

| Legislative auditing | 136,428,682 | 134,628,322 | 134,637,191 |

Analysis of the next 3 years of spending

Planned spending over the next 3 fiscal years reflects a decrease to a steady state. This aligns with our long-term transformation strategy and anticipated workforce optimization to a steady state while ensuring the continued delivery of our core responsibility.

More detailed financial information on planned spending is available on the Finances section of GC InfoBase.

Funding

This section provides an overview of the OAG’s voted and statutory funding for its core responsibility. For further information on funding authorities, consult the Government of Canada budgets and expenditures.

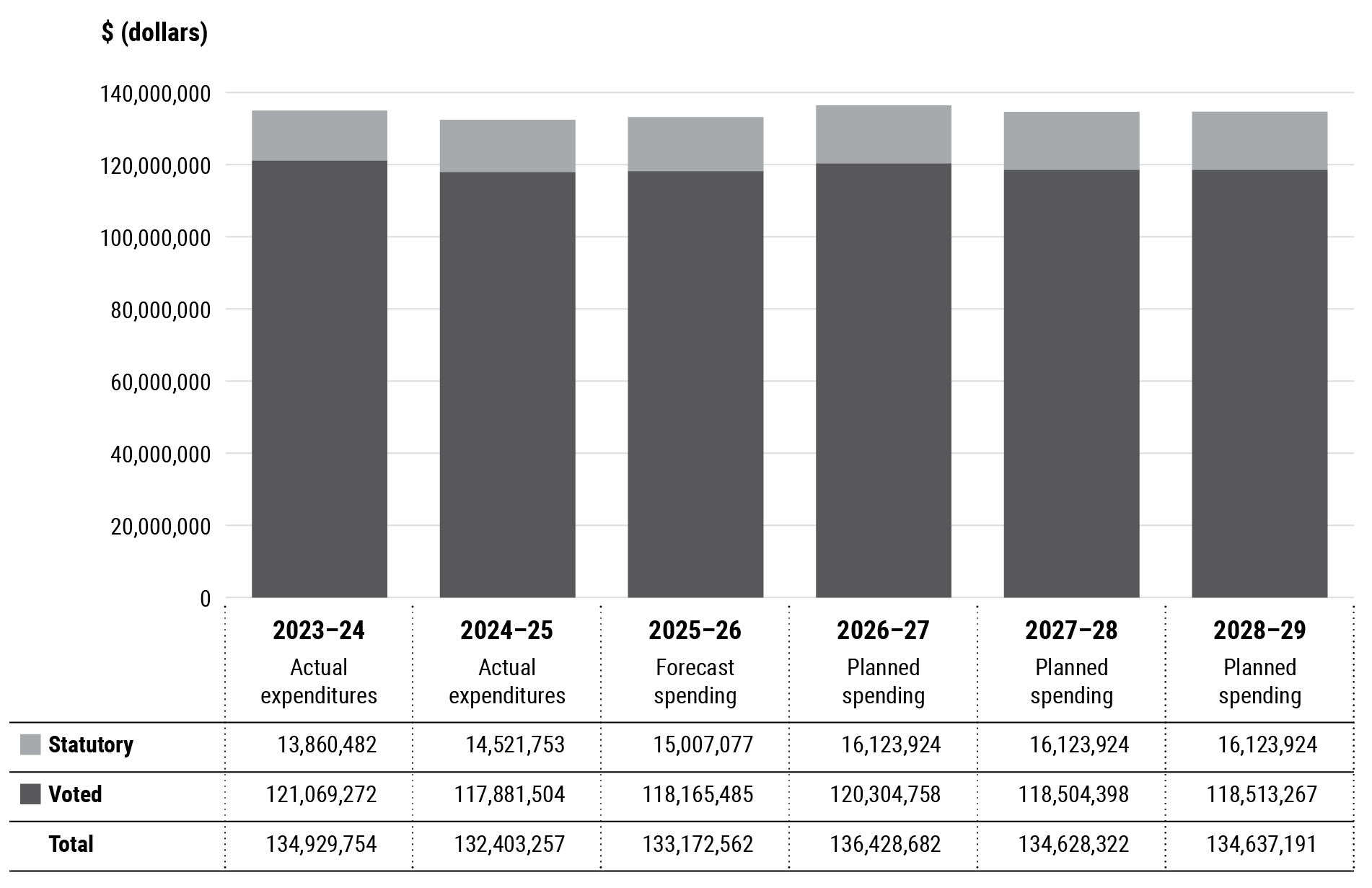

Exhibit 6—Approved funding (statutory and voted) over a 6-year period

Exhibit 6 summarizes the OAG’s approved voted and statutory funding from 2023–24 to 2028–29.

Text version

| Fiscal year | Total | Voted | Statutory |

|---|---|---|---|

| 2023–24 actual expenditures | $134,929,754 | $121,069,272 | $13,860,482 |

| 2024–25 actual expenditures | $132,403,257 | $117,881,504 | $14,521,753 |

| 2025–26 forecast spending | $133,172,562 | $118,165,485 | $15,007,077 |

| 2026–27 planned spending | $136,428,682 | $120,304,758 | $16,123,924 |

| 2027–28 planned spending | $134,628,322 | $118,504,398 | $16,123,924 |

| 2028–29 planned spending | $134,637,191 | $118,513,267 | $16,123,924 |

Analysis of statutory and voted funding over a 6-year period

The 2026–27 and beyond amounts represent the Main Estimates and do not consider in-year adjustments.

For further information on the OAG’s departmental appropriations, consult the 2026–27 Main Estimates.

Future-oriented condensed statement of operations

The future-oriented condensed statement of operations provides an overview of the OAG’s operations for 2025–26 to 2026–27.

Exhibit 7—Future-oriented condensed statement of operations for the year ended March 31, 2027 (dollars)

Exhibit 7 summarizes the expenses and revenues, which net to the cost of operations before government funding and transfers for 2025–26 to 2026–27. The forecast and planned amounts in this statement of operations were prepared on an accrual basis. The forecast and planned amounts presented in other sections of the Departmental Plan were prepared on an expenditure basis. Amounts may therefore differ.

| Financial information | 2025–26 forecast results | 2026–27 planned results |

|---|---|---|

| Financial audits of Crown corporations, territorial governments, and other organizations, and of the summary financial statements of the Government of Canada | 75,100,000 | 75,600,000 |

| Performance audits | 55,600,000 | 56,500,000 |

| Special examinations of Crown corporations | 5,700,000 | 7,500,000 |

| Sustainable development monitoring activities and environmental petitions | 2,300,000 | 2,600,000 |

| Professional practices | 12,100,000 | 13,000,000 |

| Total cost of operations | 150,800,000 | 155,200,000 |

| Total revenues | (100,000) | (100,000) |

| Net cost of operations before government funding and transfers | 150,700,000 | 155,100,000 |

Note to the future-oriented statement of operations—Parliamentary authorities

The OAG is financed by the Government of Canada through parliamentary authorities. Financial reporting of authorities provided to the OAG differs from financial reporting according to generally accepted accounting principles because authorities are based mainly on cash flow requirements. Items recognized in the future-oriented statement of operations in one year may be funded through parliamentary authorities in prior, current, or future years. Accordingly, the OAG has a different net cost of operations for the year on a government funding basis than on an accrual accounting basis. The differences are reconciled in Exhibit 8.

Exhibit 8—Reconciliation of net costs of operations to authorities forecast (dollars)

| Financial information | 2025–26 forecast results | 2026–27 planned results |

|---|---|---|

| Net cost of operations before government funding and transfers | 150,700,000 | 155,100,000 |

| Adjustments for items recorded as part of the net cost of operations but not affecting current year authorities: | | |

| Services provided without charge by other government departments | (17,874,000) | (17,991,000) |

| Amortization of tangible capital assets | (930,000) | (630,000) |

| Total items recorded as part of the net cost of operations but not affecting current year authorities | (18,804,000) | (18,621,000) |

| Adjustments for items not recorded as part of net cost of operations but affecting current year authorities: | | |

| Acquisition of tangible capital assets | 900,000 | 300,000 |

| Decrease (increase) in liabilities not previously charged to authorities | 377,000 | (304,000) |

| Total items not recorded as part of net cost of operations but affecting current year authorities | 1,277,000 | (4,000) |

| Forecast spending (authorities forecast to be used) | 133,173,000 | 136,475,000 |

| Add: Forecast lapse (authorities forecast to be lapsed) | 4,950,000 | 6,149,000 |

| Authorities forecast (authorities forecast to be requested) | 138,123,000 | 142,624,000 |

| Main Estimates | | |

| Vote 1: Program expenditures | 121,233,000 | 120,305,000 |

| Statutory amounts: Contributions to employee benefit plans | 15,007,000 | 16,124,000 |

| Total Main Estimates | 136,240,000 | 136,429,000 |

| Supplemental operating authorities | (3,733,000) | – |

| Authorities carried forward from previous year Footnote 1 | 5,616,000 | 6,195,000 |

| Authorities forecast (authorities forecast to be requested) | 138,123,000 | 142,624,000 |

Human resources

This section presents an overview of the OAG’s actual and planned human resources from 2023–24 to 2028–29.

Exhibit 9—Actual human resources for core responsibility

Exhibit 9 shows a summary of human resources, in full-time equivalents, for the OAG’s core responsibility for the previous 3 fiscal years. Human resources for the 2025–26 fiscal year are forecasted based on the year to date.

| Core responsibility | 2023–24 actual full-time equivalents | 2024–25 actual full-time equivalents | 2025–26 forecasted full-time equivalents |

|---|---|---|---|

| Legislative auditing | 780 | 752 | 730 |

Analysis of human resources over the last 3 years

In 2023–24, the OAG employed 780 full-time equivalents. As part of ongoing efforts to streamline operations and align resources with strategic priorities, the number of full-time equivalents decreased to 752 in 2024–25 and is forecasted at 730 in 2025–26. The reduction reflects our deliberate effort to reduce management positions and increase capacity at more junior levels while finding operating efficiencies. The OAG anticipates stabilizing near 750 full-time equivalents over the longer term as transformation initiatives progress.

Exhibit 10—Human resources planning summary for core responsibility

Exhibit 10 shows information on human resources, in full-time equivalents, for the OAG’s core responsibility planned for the next 3 years.

| Core responsibility | 2026–27 Planned full-time equivalents | 2027–28 Planned full-time equivalents | 2028–29 Planned full-time equivalents |

|---|---|---|---|

| Legislative auditing | 750 | 750 | 750 |

Analysis of human resources for the next 3 years

Over the planning period, the OAG expects to maintain approximately 750 full-time equivalents. This level reflects the organization’s steady-state workforce following recent transformation and realignment efforts. It represents a sustainable capacity that balances operational needs, efficiency objectives, and the ability to deliver on the OAG’s legislative auditing mandate.

Supplementary information tables

The OAG has no supplementary information tables to report for the 2026–27 fiscal year.

Information on the OAG’s sustainable development strategy can be found on the OAG’s website.

Federal tax expenditures

The OAG’s Departmental Plan does not include information on tax expenditures.

The tax system can be used to achieve public policy objectives through the application of special measures such as low tax rates, exemptions, deductions, deferrals, and credits. The Department of Finance Canada publishes cost estimates and projections for these measures each year in the Report on Federal Tax Expenditures.

This report also provides detailed background information on tax expenditures, including descriptions, objectives, historical information, and references to related federal spending programs as well as evaluations and GBA Plus of tax expenditures.

Corporate information

Organizational profile

Auditor General of Canada: Karen Hogan, FCPA

Appropriate minister: The Honourable François-Philippe Champagne, P.C., M.P., Minister of Finance and National Revenue*

Ministerial portfolio: Finance

Enabling instruments:**

- Auditor General Act

- Financial Administration Act (federal)

- Canadian Net-Zero Emissions Accountability Act

- Federal Sustainable Development Act

- Nunavut Act

- Financial Administration Act (Nunavut)

- Northwest Territories Act

- Financial Administration Act (Northwest Territories)

- Yukon Act

- Financial Administration Act (Yukon)

Year of incorporation / commencement: 1878

* The Auditor General acts independently in the execution of her audit responsibilities but reports to Parliament on expenditures through the Minister of Finance.

** Various other instruments, including acts governing some Crown corporations and other organizations, also contribute to the Auditor General’s mandate.

Organizational contact information

Mailing address:

Office of the Auditor General of Canada

240 Sparks Street

Ottawa, Ontario K1A 0G6

CANADA

Telephone: 1-888-761-5953

TTY: 613-954-8042

Fax: 613-957-0474

Email: communications@oag-bvg.gc.ca

Website: www.oag-bvg.gc.ca

Planned reports

A list of our upcoming reports can be found on the OAG’s website.

Definitions

List of terms

appropriation (crédit)

Any authority of Parliament to pay money out of the Consolidated Revenue Fund.

budgetary expenditures (dépenses budgétaires)

Operating and capital expenditures; transfer payments to other levels of government, departments or individuals; and payments to Crown corporations.

core responsibility (responsabilité essentielle)

An enduring function or role performed by a department. The intentions of the department with respect to a core responsibility are reflected in one or more related departmental results that the department seeks to contribute to or influence.

Departmental Plan (plan ministériel)

A report on the plans and expected performance of an appropriated department over a 3-year period. Departmental Plans are usually tabled in Parliament each spring.

departmental result (résultat ministériel)

A consequence or outcome that a department seeks to achieve. A departmental result is often outside departments’ immediate control, but it should be influenced by program-level outcomes.

departmental result indicator (indicateur de résultat ministériel)

A quantitative measure of progress on a departmental result.

departmental results framework (cadre ministériel des résultats)

A framework that connects the department’s core responsibilities to its departmental results and departmental result indicators.

Departmental Results Report (rapport sur les résultats ministériels)

A report on a department’s actual accomplishments against the plans, priorities, and expected results set out in the corresponding Departmental Plan.

financial audit (audit d’états financiers)

An audit that provides assurance that financial statements are presented fairly, in accordance with the applicable financial reporting framework.

full-time equivalent (équivalent temps plein)

A measure of the extent to which an employee represents a full person-year charge against a departmental budget. For a particular position, the full-time equivalent figure is the ratio of the number of hours the person actually works divided by the standard number of hours set out in the person’s collective agreement.

gender-based analysis plus (GBA Plus) (analyse comparative entre les sexes plus [ACS Plus])

Is an analytical tool used to support the development of responsive and inclusive policies, programs, and other initiatives. GBA Plus is a process for understanding who is impacted by the issue or opportunity being addressed by the initiative; identifying how the initiative could be tailored to meet diverse needs of the people most impacted; and anticipating and mitigating any barriers to accessing or benefitting from the initiative. GBA Plus is an intersectional analysis that goes beyond biological (sex) and socio-cultural (gender) differences to consider other factors, such as age, disability, education, ethnicity, economic status, geography (including rurality), language, race, religion, and sexual orientation.

Using GBA Plus involves taking a gender- and diversity-sensitive approach to our work. Considering all intersecting identity factors as part of GBA Plus, not only sex and gender, is a Government of Canada commitment.

government priorities (priorités gouvernementales)

For the purpose of the 2026–27 Departmental Plan, government priorities are the high-level themes outlining the government’s agenda in the 2025 Speech from the Throne.

horizontal initiative (initiative horizontale)

An initiative where two or more federal departments are given funding to pursue a shared outcome, often linked to a government priority.

Indigenous business (entreprise autochtones)

Requirements for verifying Indigenous businesses for the purposes of the departmental result report are available through the Indigenous Services Canada Mandatory minimum 5% Indigenous procurement target website.

non-budgetary expenditures (dépenses non budgétaires)

Non-budgetary authorities that comprise assets and liabilities transactions for loans, investments and advances, or specified purpose accounts, that have been established under specific statutes or under non-statutory authorities in the Estimates and elsewhere. Non-budgetary transactions are those expenditures and receipts related to the government’s financial claims on, and obligations to, outside parties. These consist of transactions in loans, investments and advances; in cash and accounts receivable; in public money received or collected for specified purposes; and in all other assets and liabilities. Other assets and liabilities, not specifically defined in G to P authority codes are to be recorded to an R authority code, which is the residual authority code for all other assets and liabilities.

performance (rendement)

What a department did with its resources to achieve its results, how well those results compare to what the department intended to achieve, and how well lessons learned have been identified.

performance audit (audit de performance)

An independent, objective, and systematic assessment of how well the government is managing its activities, responsibilities, and resources.

performance indicator (indicateur de rendement)

A qualitative or quantitative means of measuring an output or outcome, with the intention of gauging the performance of a department, program, policy or initiative respecting expected results.

plan (plan)

The articulation of strategic choices, which provides information on how a department intends to achieve its priorities and associated results. Generally, a plan will explain the logic behind the strategies chosen and tend to focus on actions that lead to the expected result.

planned spending (dépenses prévues)

For Departmental Plans and Departmental Results Reports, planned spending refers to those amounts presented in Main Estimates.

A department is expected to be aware of the authorities that it has sought and received. The determination of planned spending is a departmental responsibility, and departments must be able to defend the expenditure and accrual numbers presented in their Departmental Plans and Departmental Results Reports.

program (programme)

Individual or groups of services, activities or combinations thereof that are managed together within the department and focus on a specific set of outputs, outcomes or service levels.

program inventory (répertoire des programmes)

Identifies all the department’s programs and describes how resources are organized to contribute to the department’s core responsibilities and results.

result (résultat)

A consequence attributed, in part, to a department, policy, program or initiative. Results are not within the control of a single department, policy, program or initiative; instead they are within the area of the department’s influence.

special examination (examen spécial)

A form of performance audit that is conducted within Crown corporations. The scope of special examinations is set out in the Financial Administration Act. A special examination considers whether a Crown corporation’s systems and practices provide reasonable assurance that its assets are safeguarded and controlled, its resources are managed economically and efficiently, and its operations are carried out effectively.

statutory expenditures (dépenses législatives)

Expenditures that Parliament has approved through legislation other than appropriation acts. The legislation sets out the purpose of the expenditures and the terms and conditions under which they may be made.

target (cible)

A measurable performance or success level that a department, program or initiative plans to achieve within a specified time period. Targets can be either quantitative or qualitative.

voted expenditures (dépenses votées)

Expenditures that Parliament approves annually through an appropriation act. The vote wording becomes the governing conditions under which these expenditures may be made.