Office of the Auditor General of Canada’s 2023–24 Departmental Results Report

On this page

Copyright information

© His Majesty the King in Right of Canada, as represented by the Auditor General of Canada, 2024.

Catalogue Number FA1-25E-PDF

ISSN 2561-0945

Message from the Auditor General of Canada

I am pleased to present the 2023–24 Departmental Results Report for the Office of the Auditor General of Canada (OAG). This document outlines our results and significant achievements over the past fiscal year to deliver on our core mandate while providing value to Canada’s Parliament and northern legislative assemblies, Canadians, and audited organizations.

This report marks the first time we are reporting on our revised departmental results framework. Our new departmental result indicators measure federal and territorial organizations’ progress in implementing audit recommendations, thus promoting greater transparency and accountability in improving public sector programs and services.

In the 2023–24 fiscal year, we completed key actions from our 2022–24 Strategic Plan to make progress in our transformation journey. We reviewed and renewed our performance audit selection process and made steady progress on various other initiatives to increase our overall capacity to deliver timely high-quality products that bring value to Canadians, legislators, and the organizations we audit. This work is informed by important insights from our partners and interested parties on the value that our work brings and draws from our continuous efforts to meet evolving needs, improve efficiencies in our audits, and provide more impactful recommendations.

Over the past year, we presented audit reports to Parliament and territorial legislatures on a variety of topics of great interest to Canadians, such as the ArriveCAN application, forests and climate change, housing in First Nations communities, and child and family services in Nunavut. Through the delivery of our audit reports and the parliamentary committee hearings that studied them, we maintained an ongoing dialogue with legislators about accountability and improving program delivery and results in the public service.

I am grateful for the steadfast dedication, commitment, and professionalism of my OAG colleagues. It is a privilege to lead such an exceptional group of people and to together carry out our mandate and effect positive change through the delivery of improved results for Canadians.

[Original signed by]

Karen Hogan, Fellow Chartered Professional AccountantFCPA

Auditor General of Canada

12 September 2024

Results—What we achieved

Core responsibility: Legislative auditing

Description

Our audit reports provide objective, fact‑based information and advice on government programs and activities. With our audits, we assist Parliament in its authorization and oversight of government spending and operations.

Our audits also help territorial legislatures, boards of Crown corporations, and audit committees in their oversight of the management of government activities. Those charged with governance use our audit findings to hold their respective organizations to account for the handling of public funds.

Financial audits assess whether the annual financial statements of the Government of Canada, the territories, Crown corporations, and others are presented fairly, consistent with applicable accounting standards.

Performance audits assess whether government organizations manage programs with due regard for economy, efficiency, and environmental impact and measure their effectiveness. We have also incorporated the assessment of equity, diversity, and inclusion as a priority area for our performance audits.

Special examinations assess whether Crown corporation systems and practices provide reasonable assurance that assets are safeguarded and controlled, resources are managed economically and efficiently, and operations are managed effectively.

Progress on results

This section presents details on how the OAG performed to achieve results and meet targets for our core responsibility of legislative auditing.

The OAG maintains a departmental results framework for reporting corporate results in accordance with the Treasury Board’s Policy on Results. Our new framework came into effect on 1 April 2023 and was included in our 2023–24 Departmental Plan. Our new indicators measure our influence by examining the percentage of audit recommendations that have been implemented and the improvement in terms of specific measures. In the 2023–24 fiscal year, we set targets and began reporting on these new indicators. The 2023–24 results reported below will act as a baseline for reporting in future years.

Exhibit 1—Targets and results for legislative auditing

Exhibit 1 provides a summary of the target and actual results for each indicator associated with the results under legislative auditing.

Departmental result: Government acts on recommendations to improve public sector programs, service delivery, and financial management and reporting.

|

Departmental result indicators

|

Target

|

Date to achieve target

|

Actual resultsFootnote 1

|

|---|---|---|---|

|

Percentage of performance audit and special examination recommendations implemented

|

At least 85% of the recommendations have been implemented, 3 years after tabling

|

31 March 2025

|

2023–24: 84%Footnote 2

|

|

Percentage of financial audit recommendations implemented

|

At least 85% of the recommendations have been implemented, 2 years after they were issued

|

31 March 2025

|

2023–24: 91%Footnote 3

|

|

Percentage of measures examined for which progress made is assessed as “substantial improvement”

|

At least 85% of the measures have improved, 3 years after tabling

|

31 March 2025

|

2023–24: 50%Footnote 4

|

Additional information on the detailed results and performance information for the OAG’s program inventory is available on GC InfoBase.

Details on results

The following section describes the results for legislative auditing in 2023–24 compared with the planned results set out in the OAG’s departmental plan for the year.

Planned results, as reported in the OAG’s 2023–24 Departmental Plan:

Audit operations

We planned to complete 89 financial audits, 25 performance audits, and 6 special examinations of Crown corporations during the 2023–24 fiscal year, as well as a review of departmental progress in implementing sustainable development strategies, our annual commentary on our financial audit work, our annual report on environmental petitions, an audit on Export Development Canada’s Environmental and Social Review Directive, and a new web release of the Update on Past Audits searchable online tool.

Results achieved:

- We completed 95 financial audits, 22 performance audits, and 4 special examinations of Crown corporations during the 2023–24 fiscal year. We also completed a review of departmental progress in implementing sustainable development strategies (with a focus on zero‑emission vehicles), our annual commentary report on our financial audit work, our annual report on environmental petitions, and an audit report on Export Development Canada’s Environmental and Social Review Directive.

2022–24 Strategic Plan

We planned to advance initiatives in support of our 2022–24 Strategic Plan, including advancing initiatives in support of our “one office, one team, one vision” priority, trialing and implementing various aspects of our hybrid work model, developing a roadmap for our ongoing transformation journey, implementing an engagement plan and completing a value‑added analysis for our partners and interested parties, and delivering on our project to bring efficiencies to audits.

Results achieved:

- During 2023–24, we advanced initiatives in our 2022–24 Strategic Plan under our 2 strategic priorities.

Our current results: Audit operations

Our role in supporting a well-managed and accountable government is to deliver high-quality audit work in a timely manner to Parliament, the territorial legislative assemblies, and the boards of the Crown and territorial corporations we audit. We are always looking to enhance the impact and value of our audit work to better inform decision makers and those charged with oversight responsibilities.

Our system of quality management is fundamental in delivering quality in our audits. It creates an environment that enables and supports audit teams in performing quality engagements. The OAG periodically evaluates the design, implementation, and operation of all components of its system of quality management. When deficiencies are identified, we investigate the root causes; this enables appropriate actions to be taken and then monitored to ensure that deficiencies are corrected.

To assess the impact of our work on government organizations, we measure the percentage of recommendations that are implemented by the organizations we audit. This independent reporting to parliamentarians about improvements that are being made in public institutions because of our audit work promotes greater accountability and transparency in the public sector and thus contributes to improved public sector performance.

Financial audits and other engagements

The OAG conducts financial audits and related work across various jurisdictions every year, including

- the federal government’s consolidated financial statements, the results of which are published annually in the Public Accounts of Canada

- the consolidated financial statements of the governments of Nunavut, Yukon, and the Northwest Territories, which are published annually in each territory’s public accounts

- the financial statements of most Crown corporations and territorial corporations and other federal organizationsFootnote 1

During the 2023–24 fiscal year, we completed 95 financial audits. The objective of financial audits is to provide an opinion on whether an organization’s financial statements are prepared, in all material respects, in accordance with the applicable financial reporting framework. In addition, when applicable, the objective is also to provide an opinion on whether the transactions that have come to the auditor’s notice during the audit of financial statements complied with specified authorities. An unmodified audit opinion indicates that the financial statements of the organization are prepared, in all material respects, in accordance with the applicable financial reporting framework and that the transactions that we looked at during the audit of financial statements complied with specified authorities.

In the 2023–24 Departmental Plan, we had reported that we planned to complete 89 financial audits in the 2023–24 fiscal year. The difference between the number of planned financial audits for 2023–24 and the number of actual financial audits that were reported in 2023–24 derives from 2 elements: the addition of a financial audit of the Canada Growth Fund, which was approved after the 2023–24 Departmental Plan was published, and a change in the way that we report the number of financial audits completed per fiscal yearFootnote 1.

During the 2023–24 fiscal year, 94% of our financial audit opinions were issued on an unmodified basis. We modified 5 audit opinions and added 1 “other matter” paragraph to another. For 2 of the modified audit opinions, we qualified our opinions because the organizations missed their statutory deadlines for submitting their annual reports to their ministers. In another case, we qualified our opinion because the organization missed its statutory deadline for presenting the public accounts to the legislative assembly. In the fourth case, we found that in addition to missing its statutory deadline for submitting its annual report to its minister, management had not implemented reliable inventory procedures, and we were unable to satisfy ourselves concerning inventory quantities by alternative means. We qualified a fifth opinion because management had not completed all necessary analysis to determine whether an asset retirement obligation existed, and we were therefore unable to conclude on this matter. Finally, for 1 audit opinion, we added an “other matter” paragraph because an organization did not use some of its funds for their intended purpose.

As part of our financial audit work, we issue recommendations when we have identified opportunities for changes that would improve internal control systems, streamline operations, or enhance financial reporting practices. The impact and value of our audits is fully realized when our recommendations are implemented. We expect at least 85% of recommendations to have been implemented, 2 years after they are issued. From 1 April 2022 to 31 March 2024, 91% were implemented.

In addition to financial audits, we worked on more than 50 other engagements during the 2023–24 fiscal year, including agreed-on procedure engagements for First Nations groups in relation to tax administration agreements.

During 2023–24, we also presented our annual commentary on financial audits, which provides additional insights to Parliament on matters of significance raised during our financial audits of federal organizations. In the Commentary on the 2022–2023 Financial Audits, released in October 2023, we presented information on COVID‑19 benefit overpayments, gaps in IT controls, the financial situation of the Trans Mountain Corporation, and pay administration issues for government employees.

Performance audits

The OAG conducts over 20 performance audits every year of federal and territorial government departments, agencies, and other organizations. A performance audit is an independent, objective, and systematic assessment of how well the government is managing its activities, responsibilities, and resources. Performance audits may look at a single government program or activity, an area of responsibility that involves several government organizations, or an issue that affects many organizations.

Performance audits provide assurance and, when appropriate, recommendations for improvement to assist Parliament and its committees or the legislative assemblies of the territories in their scrutiny of the government’s management of resources and delivery of programs.

In the 2023–24 fiscal year, we presented 22 performance audit reports: 19 to the Parliament of Canada, 1 to the Yukon Legislative Assembly, and 2 to the Legislative Assembly of Nunavut. We also completed several other reports, such as our annual report on environmental petitions and our annual commentary on our financial audit work. Details for all these reports appear in the “List of reports” section of this report, including a reconciliation of planned and completed reports for the 2023–24 fiscal year.

In the 2023–24 Departmental Plan, we had reported that we planned to complete 25 performance audits in the 2023–24 fiscal year. The difference between the number of planned performance audits for 2023–24 and the number of actual performance audits that were reported in 2023–24 is explained by the fact that 4 audits were deferred to 2024–25, 1 audit was cancelled, and an additional audit not planned originally for 2023–24 was completed in 2023–24. We also included our annual review of departmental progress in implementing sustainable development strategies in the number of performance audits that were reported in 2023–24 because it is an audit completed to the same level of assurance as a performance audit. Details for these changes can be found in the “List of reports” section of this report.

For example, the Auditor General’s October 2023 report on antimicrobial resistance identified important gaps that persist in the federal government’s actions to address growing antimicrobial resistance and improve access to antimicrobial drugs. Filling these gaps is necessary to mitigate significant current and foreseeable effects on the health of Canadians.

The Auditor General’s October 2023 report on modernizing information technology (IT) systems within the federal government found that progress on modernizing applications and data centres had been very slow, even though it had been more than 24 years since the government first identified aging systems as a significant issue. Our audit found that at least two thirds of departments’ and agencies’ applications were reported as being in poor health and in critical need of modernization.

The Auditor General’s February 2024 report on the ArriveCAN application found that the Canada Border Services Agency repeatedly failed to follow good management practices regarding the application’s contracting, development, and implementation. As of August 2024, we have appeared 9 times to discuss our findings on ArriveCAN at parliamentary committee hearings.

The Auditor General’s March 2024 report on housing in First Nations communities found that many people living in these communities still did not have access to housing that was safe and in good condition. Since 2003, this was the fourth time that the OAG had raised concerns about housing in First Nations communities.

The Commissioner of the Environment and Sustainable Development’s 2023 report on the 2030 Emissions Reduction Plan, under the Canadian Net-Zero Emissions Accountability Act, identified concerns about the federal government’s ability to achieve meaningful progress to meet the 2030 targets in reducing greenhouse gas emissions. If fully implemented, the recommendations in this audit would provide a strong basis for Canada to meet, for the first time, its emission reduction target.

Taken as a whole, the Commissioner’s audit reports in 2023–24 included important findings related to long‑standing issues in data collection and improvements needed in decision making to support sustainable development, climate change, and sustainably managed marine resources, such as fisheries.

As noted above, all our performance audit reports include recommendations that highlight important areas where improvements are needed to enhance outcomes and services for Canadians and to ensure that government’s management practices, controls, and reporting systems are functioning as they should, on the basis of organizations’ own public administration policies and best practices. We expect at least 85% of recommendations to have been implemented, 3 years after audit reports are tabled. For performance audit recommendations (including special examinations) for which progress was examined in the 2023–24 fiscal year, 84% were implemented.

Special examinations

The OAG audits most, but not all, Crown corporations. The Financial Administration Act requires the OAG to audit federal parent Crown corporations at least once every 10 years.

Special examinations are a form of performance audit that focuses on the operations of parent federal Crown corporations. These audits examine whether a Crown corporation’s systems and practices provide reasonable assurance that its assets are safeguarded and controlled, its resources are managed economically and efficiently, and its operations are carried out effectively.

In our 2023–24 Departmental Plan, we reported that we planned to complete 6 special examinations. Of these, 4 special examinations were completed in the 2023–24 fiscal year. The fifth planned special examination, the special examination of the Pacific Pilotage Authority, is planned to be completed in 2024–25 and will be included in our 2024–25 Departmental Results Report. The sixth planned report, relating to Export Development Canada’s Environmental and Social Review Directive, is an audit report required by legislation but is not a special examination. It was completed in November 2023 and is included in the “Other reporting” table in the “List of reports” section of this report.

The 4 special examinations that we completed in the 2023–24 fiscal year were of the Canadian Museum of History, the Laurentian Pilotage Authority, the Royal Canadian Mint, and Canada Lands Company Limited. We found significant deficiencies in 2 of the Crown corporations we examined. For the Laurentian Pilotage Authority, we found a significant deficiency in the management of operations (pilotage services), specifically in the systems and practices related to pilot boarding safety measures. For the Canadian Museum of History, we found weaknesses in collections conservation that amounted to a significant deficiency.

The special examination reports included recommendations for improvements in many areas, including board independence, board oversight, performance measurement, risk management, and the management of operations.

As noted above, for performance audit recommendations (including special examinations) for which progress was measured in the 2023–24 fiscal year, 84% were implemented.

International work

The OAG maintained its active participation and contributions to the International Organization of Supreme Audit Institutions (INTOSAI) committees and working groups throughout the 2023–24 fiscal year.

Additionally, the OAG continued its collaboration with the Canadian Audit and Accountability Foundation’s International Development Program by hosting international fellows. In 2023–24, the office welcomed 3 fellows from the State Audit Office of Vietnam.

The OAG was involved in 3 peer reviews during 2023–24. We were invited to and agreed to participate in the peer review of the United StatesU.S. Government Accountability Office’s quality management system. On this mandate, we were asked specifically to provide our expertise from a financial audit perspective. We also participated in a peer review for the European Court of Auditors as the principal for the data analytics stream. This peer review is expected to conclude during 2024–25. In addition, we initiated the planning of a peer review for the Australian National Audit Office in a lead role, which is expected to conclude during 2025–26. Our peer review work, done jointly with other audit offices around the world, helps build meaningful and mutually beneficial relationships in the global audit community and contributes to the sharing of expertise and best practices within this community.

The 2023–24 fiscal year marked the end of our 6-year term as the external auditor of the United Nations Educational, Scientific and Cultural Organization (UNESCO). Over that period, we completed 30 financial audits, with specific audit work spanning 24 countries. In addition, on the basis of our audit work, we identified and recommended opportunities for changes to improve internal control systems, streamline operations, and enhance financial reporting practices.

Our current results: 2022–24 Strategic Plan

In our 2023–24 Departmental Plan, we described several initiatives to be delivered as part of our 2022–24 Strategic Plan. During the 2023–24 fiscal year, we remained focused on implementing actions in support of our 2 priorities in the strategic plan.

Priority 1: One office, one team, one vision

In 2023–24, we completed key initiatives to support this priority:

- furthered steps toward enhancing our integrated office-wide planning process at both the strategic and operational levels

- improved workspaces and technology in support of our hybrid work experience, enhanced accessibility and inclusivity, and reduced the OAG’s environmental footprint by aligning with the Government of Canada’s Office Portfolio Reduction Plan

- furthered diversity and accessibility goals, including developing our 2023–26 diversity and inclusion plan and delivering our first progress report for the 2022–25 accessibility plan; hiring an accessibility coordinator; implementing the Government of Canada Workplace Accessibility Passport; formalizing the Equity, Diversity, Inclusion, Accessibility, and Official Languages Committee; and implementing Public Service Commission of Canada guides and tools for identifying and mitigating biases and barriers in staffing assessment methods

- furthered our audit transformation initiative—we made steps toward streamlining and strengthening how we conduct and report on our audit work as part of our multi-year effort focused on meeting present-day and future needs and challenges

- advanced initiatives to transform our internal services—we streamlined many of our human resources and financial processes and services, resulting in improved reporting more informed decision making, and operational efficiencies that were reinvested in change management toward our transition to new financial and human resources systems over the next 2 fiscal years

- modernized our cybersecurity and aging IT—all but 1 of our IT systems are now fully supported, our transition plan to onboard our systems onto the Government of Canada Enterprise Architecture is underway, and we have made further progress on our data strategy and associated implementation plan

- launched a talent management initiative with the goal of strengthening our employees’ people management competencies, including training focused on developing key leadership areas (such as the courage to lead difficult and open conversations and psychological safety) and career development and accountability to nurture a diverse workforce and an inclusive workplace

Priority 2: Meaningful relationships, trusted advice

In 2023–24, we completed key initiatives to support this priority:

- held consultations with parliamentarians and other interested parties to better understand how to meet their needs and strengthen these relationships and to seek input into approaches and topics for our upcoming work

- held our first symposium with audit committee chairs in October 2023

- developed a new evergreen audit selection process, which was launched in April 2023, after a review of our existing process—these improvements will ultimately increase the value of our work for Canadians, legislators, and the organizations we audit

- updated our international engagement plan and finalized our framework on standard-setting activities

Resources required to achieve results

Exhibit 2—Snapshot of resources required for legislative auditing

Exhibit 2 provides a summary of the planned and actual spending and full-time equivalents (FTEs) required to achieve results.

|

Resource

|

Planned

|

Actual

|

|---|---|---|

|

Spending (in millions of dollars)

|

$122.6

|

$134.9

|

|

Full-time equivalents

|

765

|

780

|

Complete financial and human resources information for the OAG’s program inventory is available on GC InfoBase.

Related government-wide priorities

Gender-based analysis plus

The OAG incorporates gender-based analysis plus (GBA Plus) in its audit work to provide parliamentarians and all Canadians with information on the government’s progress toward its gender, equity, diversity, and inclusion priorities. A summary of the activities to support the advancement of Canada’s GBA Plus commitments is included in a supplementary information table accompanying this report.

United Nations’ 2030 Agenda for Sustainable Development and the Sustainable Development Goals

All of the OAG’s audits—financial audits, performance audits, and special examinations—contribute to the goal of peace, justice, and strong institutions (Sustainable Development Goal 16 of the United Nations’ 2030 Agenda for Sustainable Development). In addition, the OAG is committed to aligning its direct engagement audit work to support the agenda and the underlying 17 Sustainable Development Goals. We consider the goals when planning and reporting on this audit work. During the 2023–24 fiscal year, 9 of the goals were included in the OAG’s published performance audit and special examination reports, with the goal framework referenced in 5 reports (Exhibit 3). In addition, internally, we have committed to completing actions that contribute to the goals of reduced inequalities (Sustainable Development Goal 10), responsible consumption and production (Sustainable Development Goal 12), and climate action (Sustainable Development Goal 13) in our departmental sustainable development strategy. These actions include mandatory training on Indigenous topics, working toward meeting workforce availability percentages for employment equity groups at the OAG, and incorporating elements of the Greening Government Strategy into OAG procurement practices.

Exhibit 3—The number of United Nations’ Sustainable Development Goal references in the OAG’s direct engagements for the 2023–24 fiscal year

Notes:

- The number of references includes mentions of any of the United Nations’ Sustainable Development Goals or the 2030 Agenda for Sustainable Development in the OAG’s performance audit reports presented to Parliament and northern legislative assemblies and in the OAG’s special examination reports transmitted to Crown corporations during the period from 1 April 2023 to 31 March 2024. Note that a direct engagement report may refer to more than 1 goal.

- The source of the Sustainable Development Goal icons is the United Nations.

Text description of Exhibit 3

This image shows the number of United Nations’ Sustainable Development Goal references in the direct engagements of the Office of the Auditor General of Canada, or OAG, for the 2023–24 fiscal year.

The number of references includes mentions of any of the United Nations’ Sustainable Development Goals or the 2030 Agenda for Sustainable Development in the OAG’s performance audit reports presented to Parliament and northern legislative assemblies and in the OAG’s special examination reports transmitted to Crown corporations during the period from 1 April 2023 to 31 March 2024. Because a direct engagement report may refer to more than 1 goal, the total number of references is greater than the total number of reports presented or transmitted during the period.

The Sustainable Development Goals that are mentioned and the number of references are as follows.

| Sustainable Development Goal | Number of references |

|---|---|

| Goal 3: Good health and well-being | 1 |

| Goal 5: Gender equality | 1 |

| Goal 9: Industry, innovation and infrastructure | 2 |

| Goal 10: Reduced inequalities | 2 |

| Goal 12: Responsible consumption and production | 1 |

| Goal 13: Climate action | 7 |

| Goal 14: Life below water | 2 |

| Goal 15: Life on land | 2 |

| Goal 16: Peace, justice and strong institutions | 1 |

| No specific goal | 5 |

The exhibit includes the Sustainable Development Goal icons. The source of these icons is the United Nations.

More information on the OAG’s contributions to Canada’s Federal Implementation Plan for the 2030 Agenda and the Federal Sustainable Development Strategy can be found in our departmental sustainable development strategy.

Innovation

In the 2023–24 fiscal year, the Innovation Lab experimented with simplifying data access for the OAG’s audit work. This resulted in lessons learned in terms of testing new technologies and building skills in experimentation and user experience design. The OAG recruited an employee from the Government of Canada Digital Talent pilot program to lead the Innovation Lab for 2 years to test the suitability of a new Human Resources classification for the Chief Information Officer Group. As part of the OAG’s approach to transformation, the Innovation Lab supported the OAG in conducting an ideation workshop to encourage employees to adopt an innovation mindset, and a recommended experiment resulting from the workshop is presently being planned for 2024–25. Currently, the Innovation Lab has partnered with Human Resources to enable an experiment to improve workplace relations using artificial intelligence.

Program inventory

The OAG’s core responsibility, legislative auditing, is supported by the sole program in our program inventory:

- legislative audit

Additional information related to the program inventory for legislative auditing is available on the “Results” section of GC Infobase.

Contracts awarded to Indigenous businesses

Government of Canada departments are to meet a target of awarding at least 5% of the total value of contracts to Indigenous businesses each year. The OAG is a Phase 3 organization and is committed to achieving the minimum 5% target by the end of the 2024–25 fiscal year. To prepare the organization for meeting this target, the following supporting measure has been completed:

- In 2023–24, the OAG evaluated Indigenous business capacity and identified set-aside opportunities for major spend categories. Pre‑qualified methods of supply were identified in many areas where there is recurring contracting activity.

Recognizing that the intended outcome of this commitment is to improve socio-economic outcomes for Indigenous peoples, the following measures will be instituted to ensure that our actions contribute to the intended outcome:

- To ensure that Indigenous businesses are receiving appropriate consideration in OAG procurement activities, awareness sessions will be held with the OAG employees responsible for business units or program areas under which a procurement plan is established so that the commitment for contracts awarded to Indigenous businesses is considered at each step of our procurement planning process.

- To ensure that contracts awarded to Indigenous businesses are contributing to economic reconciliation with Indigenous peoples, any supplier that has been awarded a contract designated as set aside under the Government of Canada’s Procurement Strategy for Indigenous Business is required to demonstrate adherence to the program requirements. Compliance audits may also be leveraged to confirm that the ownership criterion, control criterion, and Indigenous content criterion, where applicable, are being satisfied.

Spending and human resources

-

In this section

Spending

This section presents an overview of the OAG’s actual and planned expenditures from 2021–22 to 2026–27.

Budgetary performance summary

Parliament provided the OAG with up to $136.5 million in parliamentary authorities, which consisted of $122.6 million in Main Estimates authorities and $13.9 million in adjustments and transfers, which, for the most part, were routine in nature—for example, carry-forward funding from the previous year and an adjustment for retroactive wage increases.

Exhibit 4—Actual 3-year spending on the core responsibility (in millions of dollars)

Exhibit 4 presents how much money the OAG spent over the past 3 years to carry out its core responsibility.

|

Core responsibility

|

2023–24 Main Estimates

|

2023–24 total authorities available for use

|

Actual spending over 3 years (authorities used)

|

|---|---|---|---|

|

Legislative auditing |

$122.6 |

$136.5 |

|

Analysis of past 3 years of spending

In the 2023–24 fiscal year, $134.9 million was charged against our total parliamentary authorities of $136.5 million. This resulted in the lapse of $1.6 million of the OAG’s parliamentary authorities provided in 2023–24. The OAG may carry forward up to 5% of its operating budget (on the basis of Main Estimates program expenditures) into the next fiscal year, subject to parliamentary approval. This carry‑forward amount of $2.7 million for 2024–25 comprises a combination of lapsed authorities ($1.6 million) and credits for certain pay-related amounts ($1.1 million) for which authorities were not provided in the current year. The actual spending (authorities used) increased from 2021–22 to 2022–23, mainly because of increased salaries for certain employee groups (newly approved economic salary increases and retroactive pay). In 2023–24, there were further increases to salaries, as other employee groups received salary increases and retroactive pay. In addition, we temporarily increased our full‑time‑equivalent count to advance our mandate, key priorities, and transformation initiative.

More financial information from previous years is available on the “Finances” section of GC Infobase.

Exhibit 5—Planned 3-year spending on the core responsibility (in millions of dollars)

Exhibit 5 presents how much money the OAG plans to spend over the next 3 years to carry out its core responsibility.

|

Core responsibility

|

2024–25 planned spending

|

2025–26 planned spending

|

2026–27 planned spending

|

|---|---|---|---|

|

Legislative auditing

|

$127.4

|

$128.1

|

$126.1

|

More detailed financial information from previous years is available on the “Finances” section of GC Infobase.

Funding

This section provides an overview of the OAG’s voted and statutory funding for its core responsibility. For further information on funding authorities, consult the Government of Canada budgets and expenditures.

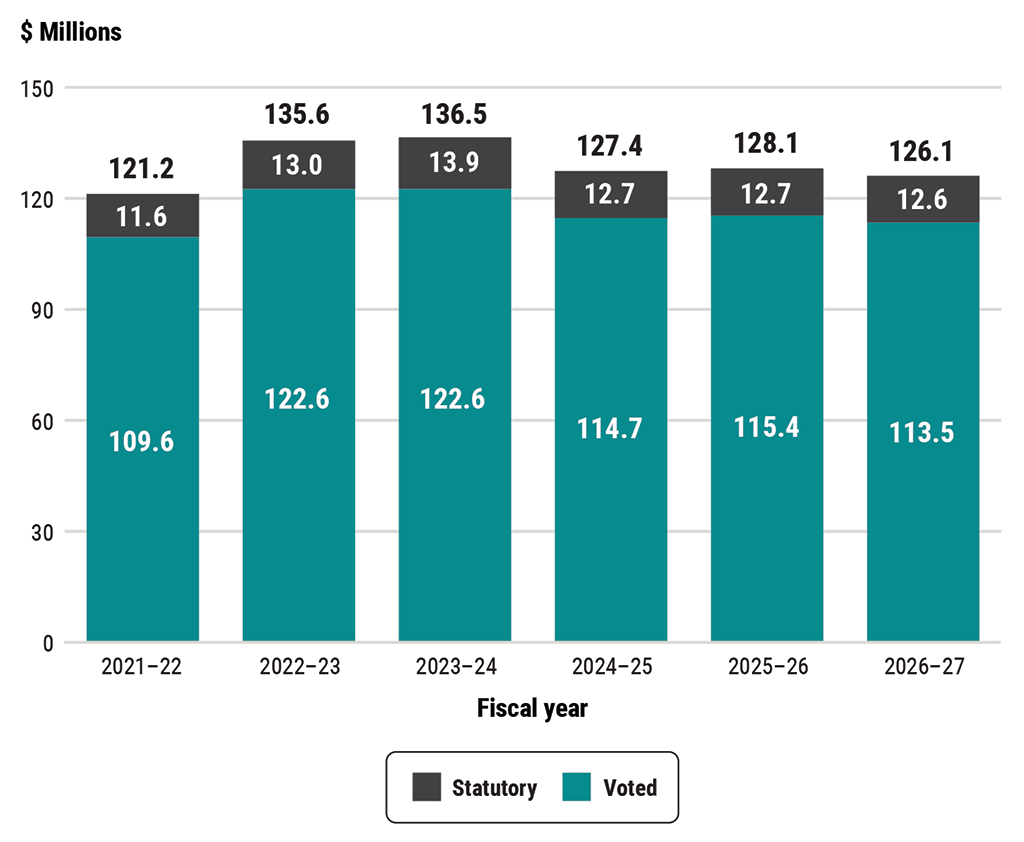

Exhibit 6—Approved funding (statutory and voted) over a 6‑year period (in millions of dollars)

Exhibit 6 summarizes the OAG’s approved voted and statutory funding from 2021–22 to 2026–27.

Text description of Exhibit 6

|

Fiscal year

|

Total

(in millions of dollars) |

Voted

(in millions of dollars) |

Statutory

(in millions of dollars) |

|---|---|---|---|

|

2021–22

|

$121.2

|

$109.6

|

$11.6

|

|

2022–23

|

$135.6

|

$122.6

|

$13.0

|

|

2023–24

|

$136.5

|

$122.6

|

$13.9

|

|

2024–25

|

$127.4

|

$114.7

|

$12.7

|

|

2025–26

|

$128.1

|

$115.4

|

$12.7

|

|

2026–27

|

$126.1

|

$113.5

|

$12.6

|

Analysis of statutory and voted spending over a 6‑year period

The authorities available for use mainly increased in the 2022–23 and 2023–24 fiscal years because of additional funding received for approved economic salary increases, including the associated statutory employee benefits. The 2024–25 and beyond amounts represent the Main Estimates and do not consider in‑year adjustments.

For further information on the OAG’s departmental voted and statutory expenditures, consult the Public Accounts of Canada.

Human resources

This section presents an overview of the OAG’s actual and planned human resources from 2021–22 to 2026–27.

Exhibit 7—Actual human resources for the core responsibility

Exhibit 7 shows a summary of human resources, in full-time equivalents, for the OAG’s core responsibility for the previous 3 fiscal years.

|

Core responsibility

|

2021–22 actual full‑time equivalents

|

2022–23 actual full‑time equivalents

|

2023–24 actual full‑time equivalents

|

|---|---|---|---|

|

Legislative auditing

|

727

|

732

|

780

|

Analysis of human resources over the last 3 years

In March 2021, the OAG received $25 million of additional permanent annual funding. With this new funding, we hired additional staff and, in the 2023–24 fiscal year, employed 780 full‑time equivalents. We also increased the number of performance audits we produce in a year from an average of 14 before receiving the increase in our funding to more than 20 in 2022–23 and 2023–24. The increase in full‑time equivalents also supported our transformation initiative.

Exhibit 8—Human resources planning summary for the core responsibility

Exhibit 8 shows information on human resources, in full‑time equivalents, planned for the next 3 years. Human resources for the current fiscal year are forecasted based on year to date.

|

Core responsibility

|

2024–25 planned full‑time equivalents

|

2025–26 planned full‑time equivalents

|

2026–27 planned full‑time equivalents

|

|---|---|---|---|

|

Legislative auditing

|

770

|

760

|

750

|

Financial statements

Statement of Management Responsibility Including Internal Control Over Financial Reporting

Management of the Office of the Auditor General of Canada (OAG) is responsible for the preparation of the accompanying financial statements for the year ended 31 March 2024 and for all information contained in these statements, in accordance with Canadian public sector accounting standards.

Management is responsible for the integrity and objectivity of the information in these financial statements. Some of the information in the financial statements is based on management’s best estimates and judgment and gives due consideration to materiality. To fulfill its accounting and reporting responsibilities, management maintains a set of accounts that provides a centralized record of the OAG’s financial transactions. Financial information submitted in the preparation of the Public Accounts of Canada, and included in the OAG’s Departmental Results Report, is consistent with these audited financial statements. In preparing the financial statements, management is responsible for assessing the OAG’s ability to continue as a going concern; disclosing matters related to going concern; and using the going concern basis of accounting, as applicable.

Management is also responsible for maintaining an effective system of internal control over financial reporting (ICFR), which is designed to provide reasonable assurance that financial information is reliable; that assets are safeguarded; and that transactions are properly authorized and recorded in accordance with the Financial Administration Act and other applicable legislation, regulations, authorities, and policies.

Management seeks to ensure the objectivity and integrity of data in its financial statements through the careful selection, training, and development of qualified staff; through organizational arrangements that provide appropriate divisions of responsibility; through communications aimed at ensuring that regulations, policies, standards, and managerial authorities are understood throughout the OAG; and through an annual assessment of the effectiveness of the system of ICFR.

The system of ICFR is designed to mitigate risks to a reasonable level and may not prevent or detect all misstatements. It is based on an ongoing process designed to identify key risks, to assess the effectiveness of associated key controls, and to make any necessary adjustments.

The effectiveness and adequacy of the OAG’s system of internal control are reviewed through the work of internal audit staff, who conduct periodic audits of different areas of the OAG’s operations. Also, financial services staff annually monitor ICFR. As a basis for recommending approval of the financial statements to the Auditor General, the OAG’s Audit Committee reviews management’s arrangements for internal controls and the accounting policies employed by the OAG for financial reporting purposes. The Audit Committee also meets independently with the OAG’s internal and external auditors to consider the results of their work.

A risk-based assessment of the system of ICFR for the year ended 31 March 2024 was completed in accordance with the Treasury Board’s Policy on Financial Management. The results and action plans are summarized in the 2023–24 Annex to the Statement of Management Responsibility Including Internal Control Over Financial Reporting.

Raymond Chabot Grant Thornton LLP Chartered Professional Accountants, Licensed Public Accountants, the independent auditor for the OAG, has expressed an opinion on the fair presentation of the financial statements of the OAG in conformity with Canadian public sector accounting standards, which does not include an audit opinion on the annual assessment of the effectiveness of the OAG’s ICFR.

[Original signed by]

Karen Hogan, Fellow Chartered Professional AccountantFCPA

Auditor General of Canada

[Original signed by]

Jean-René Drapeau, Chartered Professional AccountantCPA

Chief Financial Officer

Ottawa, Canada

8 July 2024

Independent Auditor’s Report

To the Speaker of the House of Commons:

Report on the Audit of the Financial Statements

Opinion

We have audited the financial statements of the Office of the Auditor General of Canada (the “Office”), which comprise the statement of financial position as at 31 March 2024, and the statements of operations, change in net debt and cash flow for the year then ended, and notes to the financial statements, including a summary of significant accounting policies.

In our opinion, the accompanying financial statements present fairly, in all material respects, the financial position of the Office as at 31 March 2024, and the results of its operations, the change in its net debt and its cash flows for the year then ended in accordance with Canadian public sector accounting standards.

Basis for Opinion

We conducted our audit in accordance with Canadian generally accepted auditing standards. Our responsibilities under those standards are further described in the “Auditor’s responsibilities for the audit of the financial statements” section of our report. We are independent of the Office in accordance with the ethical requirements that are relevant to our audit of the financial statements in Canada, and we have fulfilled our other ethical responsibilities in accordance with these requirements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion.

Responsibilities of Management and Those Charged with Governance for the Financial Statements

Management is responsible for the preparation and fair presentation of the financial statements in accordance with Canadian public sector accounting standards, and for such internal control as management determines is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error.

In preparing the financial statements, management is responsible for assessing the Office’s ability to continue as a going concern, disclosing, as applicable, matters related to going concern and using the going concern basis of accounting unless management either intends to liquidate the Office or to cease operations, or has no realistic alternative but to do so.

Those charged with governance are responsible for overseeing the Office’s financial reporting process.

Auditor’s Responsibilities for the Audit of the Financial Statements

Our objectives are to obtain reasonable assurance about whether the financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditor’s report that includes our opinion. Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance with Canadian generally accepted auditing standards will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of these financial statements.

As part of an audit in accordance with Canadian generally accepted auditing standards, we exercise professional judgment and maintain professional skepticism throughout the audit. We also:

- Identify and assess the risks of material misstatement of the financial statements, whether due to fraud or error, design and perform audit procedures responsive to those risks, and obtain audit evidence that is sufficient and appropriate to provide a basis for our opinion. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control;

- Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Office’s internal control;

- Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates and related disclosures made by management;

- Conclude on the appropriateness of management's use of the going concern basis of accounting and, based on the audit evidence obtained, whether a material uncertainty exists related to events or conditions that may cast significant doubt on the Office's ability to continue as a going concern. If we conclude that a material uncertainty exists, we are required to draw attention in our auditor's report to the related disclosures in the financial statements or, if such disclosures are inadequate, to modify our opinion. Our conclusions are based on the audit evidence obtained up to the date of our auditor's report. However, future events or conditions may cause the Office to cease to continue as a going concern;

- Evaluate the overall presentation, structure and content of the financial statements, including the disclosures, and whether the financial statements represent the underlying transactions and events in a manner that achieves fair presentation.

We communicate with those charged with governance regarding, among other matters, the planned scope and timing of the audit and significant audit findings, including any significant deficiencies in internal control that we identify during our audit.

Report on Compliance with Specified Authorities

Opinion

In conjunction with the audit of the financial statements, we have audited transactions of the Office coming to our notice for compliance with specified authorities. The specified authorities for which compliance was audited are the Financial Administration Act and its regulations and the Auditor General Act.

In our opinion, the transactions of the Office that came to our notice during the audit of the financial statements have complied, in all material respects, with the specified authorities referred to above.

Responsibilities of Management for Compliance with Specified Authorities

Management is responsible for the Office’s compliance with the specified authorities named above, and for such internal control as management determines is necessary to enable the Office to comply with the specified authorities.

Auditor’s Responsibilities for the Audit of Compliance with Specified Authorities

Our audit responsibilities include planning and performing procedures to provide an audit opinion and reporting on whether the transactions coming to our notice during the audit of the financial statements are in compliance with the specified authorities referred to above.

[Original signed by]

Raymond Chabot Grant Thornton Limited Liability PartnershipLLP

Chartered Professional Accountants,

Licensed Public Accountants

Ottawa, Canada

8 July 2024

Office of the Auditor General of Canada

Statement of Financial Position

as at March 31

| 2024 | 2023 | |

|---|---|---|

| Financial assets | ||

|

Due from the Consolidated Revenue Fund

|

14,590 | 14,926 |

|

Accounts receivable (note 4)

|

556 | 1,482 |

|

Accounts receivable held on behalf of the Government of Canada (note 4)

|

(125) | (203) |

| Financial assets subtotal | 15,021 | 16,205 |

| Liabilities | ||

|

Accounts payable and accrued liabilities (note 5)

|

14,471 | 15,984 |

|

Vacation pay

|

9,668 | 8,992 |

|

Sick leave benefits (note 6b)

|

2,211 | 2,441 |

|

Severance benefits (note 6c)

|

1,491 | 1,603 |

|

Maternity/parental leave benefits (note 6d)

|

469 | 422 |

| Liabilities subtotal | 28,310 | 29,442 |

| Net debt | (13,289) | (13,237) |

| Non-financial assets | ||

|

Tangible capital assets (note 7)

|

3,220 | 2,520 |

|

Prepaid expenses

|

509 | 483 |

| Non-financial assets subtotal | 3,729 | 3,003 |

| Accumulated deficit | (9,560) | (10,234) |

Contractual obligations (note 10)

The accompanying notes are an integral part of these financial statements.

Approved by

[Original signed by]

Karen Hogan, Fellow Chartered Professional AccountantFCPA

Auditor General of Canada

[Original signed by]

Jean-René Drapeau, Chartered Professional AccountantCPA

Chief Financial Officer

Ottawa, Canada

8 July 2024

Office of the Auditor General of Canada

Statement of Operations

for the year ended March 31

| 2024 | 2024 | 2023 | |

|---|---|---|---|

| Planned results (note 12) |

Actual | Actual | |

| Expenses (note 8) | |||

|

Financial audits of Crown corporations, territorial governments, and other organizations, and of the consolidated financial statements of the Government of Canada

|

65,800 | 75,135 | 67,540 |

|

Performance audits

|

55,800 | 59,922 | 58,264 |

|

Professional practices

|

9,700 | 12,531 | 12,085 |

|

Special examinations of Crown corporations

|

4,200 | 3,778 | 5,007 |

|

Sustainable development monitoring activities and environmental petitions

|

2,500 | 2,290 | 2,144 |

| Total cost of operations | 138,000 | 153,656 | 145,040 |

| Revenues | |||

|

International audits

|

1,300 | 1,270 | 1,292 |

|

Other

|

- | 190 | 227 |

|

Revenues earned on behalf of the Government of Canada

|

- | (159) | (236) |

| Net revenues | 1,300 | 1,301 | 1,283 |

| Net cost of operations before government funding and transfers | 136,700 | 152,355 | 143,757 |

| Government funding and transfers (note 3) | |||

|

Net cash provided by the Government of Canada

|

- | 135,713 | 118,770 |

|

Change in due from the Consolidated Revenue Fund

|

- | (336) | 8,307 |

|

Services provided without charge (note 9b)

|

- | 17,652 | 16,479 |

| Total government funding and transfers | 139,100 | 153,029 | 143,556 |

| Annual surplus/(deficit) | 2,400 | 674 | (201) |

| Accumulated deficit, beginning of year | (10,234) | (10,234) | (10,033) |

| Accumulated deficit, end of year | (7,834) | (9,560) | (10,234) |

The accompanying notes are an integral part of these financial statements.

Office of the Auditor General of Canada

Statement of Change in Net Debt

for the year ended March 31

| 2024 | 2024 | 2023 | |

|---|---|---|---|

| Planned results (note 12) |

Actual | Actual | |

| Annual surplus/(deficit) | 2,400 | 674 | (201) |

| Acquisition of tangible capital assets (note 7) | (2,100) | (1,792) | (997) |

| Amortization of tangible capital assets (notes 7 and 8) | 1,000 | 889 | 751 |

| Write-off of tangible capital assets | - | 203 | 723 |

| Subtotal | 1,300 | (26) | 276 |

| (Increase)/Decrease in prepaid expenses | - | (26) | 115 |

| (Increase)/Decrease in net debt, during the year | 1,300 | (52) | 391 |

| Net debt, beginning of year | (13,237) | (13,237) | (13,628) |

| Net debt, end of year | (11,937) | (13,289) | (13,237) |

The accompanying notes are an integral part of these financial statements.

Office of the Auditor General of Canada

Statement of Cash Flow

for the year ended March 31

| 2024 | 2023 | |

|---|---|---|

| Operating transactions | ||

|

Cash paid for

|

||

|

Employee salaries, wages, and benefits

|

(105,503) | (90,937) |

|

Services, transportation, communication, and other expenses

|

(19,951) | (18,886) |

|

Statutory contributions to employee benefit plans

|

(13,505) | (11,957) |

| Cash paid for operating transactions subtotal | (138,959) | (121,780) |

|

Cash received from

|

||

|

International audits

|

1,989 | 653 |

|

Sales tax recovered

|

1,818 | 1,546 |

|

Salaries and benefits recovered

|

992 | 1,155 |

|

Other

|

394 | 404 |

| Cash received from operating transactions subtotal | 5,193 | 3,758 |

|

Cash used by operating transactions

|

(133,766) | (118,022) |

| Capital transactions | ||

|

Cash used to acquire tangible capital assets

|

(1,947) | (748) |

|

Cash applied to capital transactions

|

(1,947) | (748) |

| Net cash provided by the Government of Canada (note 3c) | (135,713) | (118,770) |

The accompanying notes are an integral part of these financial statements.

Office of the Auditor General of Canada

Notes to the financial statements for the year ended 31 March 2024

1. Authority and objective

The Auditor General Act, the Financial Administration Act, and a variety of other acts and orders‑in‑council set out the duties of the Auditor General and the Commissioner of the Environment and Sustainable Development.

The core responsibility of the Office of the Auditor General of Canada (OAG) is legislative auditing and consists of performance audits of departments and agencies; the audit of the consolidated financial statements of the Government of Canada; financial audits of Crown corporations, territorial governments, and other organizations; special examinations of Crown corporations; and sustainable development monitoring activities and environmental petitions.

Pursuant to the Financial Administration Act, the OAG is a department of the Government of Canada. It is listed in Schedule I.1 of the act as a division or a branch of the federal public administration, and in Schedule V of the act as a separate agency. The OAG is not subject to income taxes under the provisions of the Income Tax Act.

2. Significant accounting policies

a) Basis of presentation

The financial statements of the OAG have been prepared by management in accordance with Canadian public sector accounting standards (PSAS).

b) Parliamentary authorities

The OAG is funded by the Government of Canada through parliamentary authorities. Financial reporting of authorities provided to the OAG does not parallel financial reporting according to PSAS, since authorities are primarily based on cash flow requirements. Consequently, items recognized in the Statement of Operations and in the Statement of Financial Position are not necessarily the same as those provided through authorities from Parliament. Note 3a provides a reconciliation between the 2 bases of reporting.

c) Revenues

Revenues are from international audits and other activities, such as audit professional services provided to members of the Canadian Council of Legislative Auditors. These revenues arise from transactions with performance obligations.

Revenues from transactions with performance obligations occur when there is an enforceable promise to transfer goods or services directly to a payer in return for promised consideration. These revenues are recognized when control of the benefits associated with the goods or services have transferred and there is no unfulfilled performance obligation.

Of those revenues, amounts that are considered to be earned on behalf of the Government of Canada are not available for discharging the OAG’s liabilities. Although the OAG is expected to maintain accounting control, it has no authority regarding the disposition of those revenues. As a result, revenues earned on behalf of the Government of Canada are presented as a reduction of the OAG’s gross revenues.

d) Net cash provided by the Government of Canada

The OAG operates within the Consolidated Revenue Fund (CRF), which is administered by the Receiver General for Canada. All cash received by the OAG is deposited to the CRF, and all cash disbursements made by the OAG are paid from the CRF. The net cash provided by the Government of Canada is the difference between all cash receipts and all cash disbursements, including transactions between departments of the Government of Canada.

e) Due from the Consolidated Revenue Fund

Amounts due from or to the CRF are the result of timing differences at year-end between when a transaction affects authorities and when it is processed through the CRF. Amounts due from the CRF represent the net amount of cash that the OAG is entitled to draw from the CRF, without further parliamentary authorities to discharge its liabilities.

f) Accounts receivable and Accounts receivable held on behalf of the Government of Canada

Accounts receivable are stated at the lower of cost and net recoverable value. A valuation allowance is recorded for accounts receivable where recovery is considered uncertain.

Accounts receivable held on behalf of the Government of Canada are presented as a reduction to the financial assets on the Statement of Financial Position because they are not available to discharge the OAG’s liabilities.

g) Tangible capital assets

By nature, tangible capital assets are normally used to provide future services.

Tangible capital assets are recorded at historical cost less accumulated amortization. The OAG capitalizes the costs associated with the development of software used internally, such as installation costs, professional service contract costs, and salary costs of employees directly associated with these projects. The costs of software maintenance, project management and administration, data conversion, and training and development are expensed in the year incurred.

When conditions indicate that a tangible capital asset no longer contributes to the OAG’s ability to provide future services, or that the value of future economic benefits associated with the tangible capital asset is less than its net book value, the cost of the tangible capital asset is reduced to reflect the decline in the asset’s value. Any write-downs of tangible capital assets are accounted for as expenses in the Statement of Operations and are not subsequently reversed.

The cost of work in progress is transferred to the applicable asset class in the year the assets are put into service.

Amortization of tangible capital assets begins when assets are put into use and is recorded using the straight-line method over the estimated useful lives of the assets as follows:

| Tangible capital asset class | Useful life |

|---|---|

| Leasehold improvements | Lesser of the remaining term of the lease or the useful life of the improvements |

| Furniture and fixtures | 10 to 25 years |

| Informatics software | 5 years |

| Informatics hardware and infrastructure | 5 years |

| Office equipment | 4 to 10 years |

| Motor vehicle | 5 years |

| Work in progress | In accordance with asset class, once in service |

Software-as-a-service arrangements

Software-as-a-service arrangements are service contracts providing the OAG with the right to access a cloud provider’s software over the term of the contract. The OAG does not generally receive an informatics software asset as a result of these services, and related costs are recognized as operating expenses in the Statement of Operations when services are received.

h) Accounts payable and accrued liabilities

Accounts payable and accrued liabilities represent obligations of the OAG for salaries and wages, for material and supply purchases, and for the cost of services rendered to the OAG.

Salary-related accrued liabilities are primarily determined using employees’ salaries at year-end. Accounts payable and accrued liabilities are measured at cost.

i) Vacation pay

Vacation pay is accrued as the benefit is earned by the employees under their respective labour contracts and conditions of employment. The liability represents all unused vacation pay benefits accruing to employees. The employees’ salaries at year-end determine the amount of these accrued vacation pay benefits.

j) Employee benefits

i) Pension benefits

All eligible employees participate in the Public Service Pension Plan, a plan administered by the Government of Canada. The OAG’s contributions are currently based on a multiple of an employee’s required contributions and may change over time, depending on the experience of the plan. The OAG’s contributions are expensed during the year in which the services are rendered and represent its total pension obligation. The OAG is not required to make contributions with respect to any actuarial deficiencies of the plan.

ii) Health and dental benefits

The Government of Canada sponsors employee benefit plans (health and dental) in which the OAG participates. Employees are entitled to health and dental benefits, as provided for under labour contracts and conditions of employment. The OAG’s contributions to the plans, which are provided without charge by the Treasury Board of Canada Secretariat, are recorded at cost based on a percentage of the salary expenses and charged to personnel expenses in the year incurred. They represent the OAG’s total obligation to the plans. Current legislation does not require the OAG to make contributions for any future unfunded liabilities of the plans.

iii) Sick leave benefits

Employees are eligible to accumulate sick leave benefits until the end of employment, according to their labour contracts and conditions of employment. Sick leave benefits are earned based on employee services rendered and are paid upon an illness or injury-related absence. These are accumulating non-vesting benefits that can be carried forward to future years but are not eligible for payment on retirement or termination nor can these be used for any other purpose. A liability is recorded for unused sick leave credits expected to be used in future years in excess of future allotments, based on an actuarial valuation using an accrued benefit method. Changes in actuarial assumptions and any variance between the expected and the actual experience of the sick leave benefit plan give rise to actuarial gains or losses. These gains or losses are amortized on a straight-line basis over the expected average remaining service life of the employees, starting in the fiscal year following the one in which they arose.

iv) Severance benefits

The accumulation of severance benefits for employees ceased in the 2012–13 fiscal year. The accrued benefit obligation is determined using employees’ salaries at year-end and the number of weeks earned but unpaid for employees who have elected to defer the receipt of their full or partial severance benefits payment.

v) Maternity/parental leave benefits

Employees are entitled to maternity/parental leave benefits as provided for under labour contracts and conditions of employment. The benefits earned are event-driven, meaning that the OAG’s obligation for the cost of the entire benefit arises upon occurrence of a specific event, being the commencement of the maternity/parental leave. The accrued benefit obligation and benefit expenses are based on management’s best estimates.

k) Related party transactions

i) Inter-entity transactions

The OAG is related as a result of common ownership to all Government of Canada departments, agencies, and Crown corporations. The OAG enters into transactions with these organizations in the normal course of business. These transactions are measured as follows:

- Inter-entity transactions are measured at the exchange amount when undertaken on similar terms and conditions to those adopted if the entities were dealing at arm’s length, or where transactions are allocated costs and recoveries.

- Common services provided without charge by other government departments are recorded as operating expenses by the OAG at the carrying amount of the providing department. A corresponding amount is reported as government funding in the Statement of Operations.

- Other inter-entity transactions are measured at the carrying amount of the providing department.

ii) Other related party transactions

Related parties include key management personnel who have the authority and responsibility for planning, directing, and controlling the activities of the OAG. Related parties also include the close family members of these personnel. The OAG has defined its key management personnel to be the Executive Committee members and parties related to them.

The OAG is also related to other organizations through its membership.

Related party transactions, other than inter-entity transactions, are recorded at the exchange amount.

l) Allocation of expenses

All direct expenses related to the delivery of audits and professional practice projects, such as salary, professional services, travel, and other associated costs, are allocated to each audit and professional practice project. All other expenses, including services provided without charge, are treated as overhead and are allocated to audits and professional practice projects on the basis of the direct staff cost charged to them.

m) Measurement uncertainty

These financial statements are prepared in accordance with PSAS. These standards require management to make estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the financial statements and the reported amounts of revenues, government funding and transfers, and expenses during the reporting period. The amount of services provided without charge, the assumptions underlying the liability calculation for sick leave benefits, and the estimated useful lives of tangible capital assets are the most significant items for which estimates are used. Actual results could differ significantly from the estimates. These estimates are reviewed annually, and as adjustments become necessary, they are recognized in the financial statements in the period in which they become known.

3. Parliamentary authorities

The OAG is funded through annual parliamentary authorities. Items recognized in the Statement of Operations in one year may be funded through parliamentary authorities in prior, current, or future years. Accordingly, the OAG has different net results of operations for the year on a government funding basis than on an accrual accounting basis. The differences are reconciled in the following tables.

a) Reconciliation of net cost of operations to current year authorities used

| 2024 | 2023 | |

|---|---|---|

| Net cost of operations before government funding and transfers | 152,355 | 143,757 |

| Adjustments for items recorded as part of net cost of operations but not affecting current year authorities: | ||

|

Services provided without charge by other government departments

|

(17,652) | (16,479) |

|

Amortization of tangible capital assets

|

(889) | (751) |

|

Write-off of tangible capital assets

|

(203) | (723) |

|

(Increase)/Decrease in liabilities not charged to authorities

|

(52) | 391 |

|

Adjustment to previous year accruals

|

11 | 61 |

| Total items recorded as part of net cost of operations but not affecting current year authorities | (18,785) | (17,501) |

| Adjustments for items not recorded as part of net cost of operations but affecting current year authorities: | ||

|

Acquisition of tangible capital assets

|

1,792 | 997 |

|

(Recoveries from prior year’s revenues) / Revenues available for spending in future years

|

(505) | 647 |

|

Increase/(Decrease) in prepaid expenses

|

26 | (115) |

|

Other

|

47 | 71 |

| Total items not recorded as part of net cost of operations but affecting current year authorities | 1,360 | 1,600 |

| Current year authorities used | 134,930 | 127,856 |

b) Authorities provided and used

| 2024 | 2023 | |

|---|---|---|

| Main Estimates | ||

|

Vote 1—Program expenditures

|

109,132 | 107,013 |

|

Statutory amounts—Contributions to employee benefit plans

|

13,418 | 12,869 |

| Total Main Estimates | 122,550 | 119,882 |

| Supplementary Estimates—Vote 1c—Program expenditures | - | - |

| Supplementary voted authorities | 8,717 | 11,282 |

| Authorities carried forward from previous year | 4,786 | 4,302 |

| Adjustment to statutory contributions to employee benefit plans | 442 | 87 |

| Statutory spending of proceeds from disposal of tangible capital assets | 3 | - |

| Current year authorities provided | 136,498 | 135,553 |

| Less: Lapsed authorities | (1,568) | (7,697) |

| Current year authorities used | 134,930 | 127,856 |

The OAG may carry forward up to 5% of its operating budget (based on Main Estimates program expenditures) into the next fiscal year, subject to parliamentary approval. The OAG expects to carry forward $2.7 million ($5.5 million in 2022–23).

c) Reconciliation of net cash provided by the Government of Canada to current year authorities used

| 2024 | 2023 | |

|---|---|---|

| Net cash provided by the Government of Canada | 135,713 | 118,770 |

| Change in due from the Consolidated Revenue Fund | ||

|

Decrease in Accounts receivable and Accounts receivable held on behalf of the Government of Canada

|

848 | 381 |

|

(Decrease)/Increase in liabilities charged to authorities

|

(1,184) | 7,926 |

| Total—Change in due from the Consolidated Revenue Fund | (336) | 8,307 |

|

(Recoveries from prior year’s revenues)/Revenues available for spending in future years

|

(505) | 647 |

|

Adjustment to previous year accruals

|

11 | 61 |

|

Other

|

47 | 71 |

| Current year authorities used | 134,930 | 127,856 |

4. Accounts receivable

The following table presents details of the OAG’s accounts receivable:

| 2024 | 2023 | |

|---|---|---|

| International audits and audit‑related professional services | 287 | 1,023 |

| Other government departments and agencies | 167 | 327 |

| Other | 102 | 132 |

| Gross accounts receivable | 556 | 1,482 |

| Accounts receivable held on behalf of the Government of Canada | (125) | (203) |

| Net accounts receivable | 431 | 1,279 |

5. Accounts payable and accrued liabilities

The following table presents details of the OAG’s accounts payable and accrued liabilities:

| 2024 | 2023 | |

|---|---|---|

| Accrued employee salaries | 11,833 | 13,376 |

| Due to others | 2,638 | 2,608 |

| Total | 14,471 | 15,984 |

6. Employee benefits

a) Pension benefits

The OAG’s eligible employees participate in the Public Service Pension Plan, which is established and governed by the Public Service Superannuation Act and sponsored and administered by the Government of Canada. Pension benefits accrue up to a maximum period of 35 years at a rate of 2% per year of pensionable service, times the average of the best 5 consecutive years of earnings. The benefits are integrated with Canada/Québec Pension Plan benefits, and they are indexed to inflation.

Both the employees and the OAG contribute to the cost of the Public Service Pension Plan. Because of the amendment of the Public Service Superannuation Act following the implementation of provisions related to Economic Action Plan 2012, employee contributors have been divided into 2 groups: Group 1 relates to existing plan members as of 31 December 2012, and Group 2 relates to members joining the Public Service Pension Plan as of 1 January 2013.Each group has a distinct contribution rate.

The 2023–24 expense amounts to $8.2 million ($8.5 million in 2022–23). For Group 1 members, the expense represents approximately 1.02 times (1.02 times in 2022–23) the employee contributions and, for Group 2 members, approximately 1.00 times (1.00 times in 2022–23) the employee contributions.

The OAG’s responsibility with regard to the Public Service Pension Plan is limited to its contributions. Actuarial surpluses or deficiencies are recognized in the financial statements of the Government of Canada, as the plan’s sponsor.

b) Sick leave benefits

Employees are credited, based on service, a maximum of 15 days annually for use as paid absences due to illness or injury. The sick leave benefit obligation is unfunded and will be paid from future parliamentary authorities.

The most recent actuarial valuation of the sick leave accrued benefit obligation performed for accounting purposes was done as at 31 March 2024. Actuarial assumptions are used to determine the obligation. They are reviewed at March 31 of each year and are management’s best estimate based on an analysis of the historical data up to the reporting date. The key assumptions used are a discount rate of 3.50% (3.05% in 2022–23), which is based on an average yield of government borrowings over the expected average remaining service life of employees of 10 years (9 years in 2022–23); a rate of salary increase of 3.75% (3.75% in 2022–23); an average turnover rate of 6% (8.3% in 2022–23); an average retirement age of 58 (58 in 2022–23) for Group 1 members and 61 (61 in 2022–23) for Group 2 members; and the excess utilization and underutilization of sick leave credits, which are based on plan experience and representative of the different groups of employees covered.

Information about the sick leave benefits as at March 31 is as follows:

| 2024 | 2023 | |

|---|---|---|

| Accrued benefit obligation, beginning of year | 2,524 | 2,666 |

|

Current year benefit costNote 1

|

521 | 537 |

|