Office of the Auditor General of Canada’s 2024–25 Departmental results report

On this page

- At a glance

- Message from the Auditor General of Canada

- Results—What we achieved

- Spending and human resources

- Financial statements

- Supplementary information tables

- Federal tax expenditures

- Corporate information

- Report on staffing

- List of reports

- Definitions

Copyright information

His Majesty the King in Right of Canada, as represented by the Auditor General of Canada, 2025.

ISSN 2561-0945

At a glance

This departmental results report details the Office of the Auditor General of Canada’s (OAG’s) accomplishments against the plans, priorities, and expected results outlined in its 2024–25 Departmental Plan.

Text version of At a Glance infographic

In the 2024–25 fiscal year, the Office of the Auditor General of Canada used $132.4 million in parliamentary authorities and had 752 full‑time‑equivalent employees.

With these resources, we completed the following:

- 100 financial audits of the federal government, territorial governments, Crown corporations, and other organizations, as well as more than 60 other financial engagements

- 20 performance audits of government activities and programs (17 federal and 3 territorial)

- 3 special examinations of Crown corporations

- 1 annual report on environmental petitions

- 1 annual commentary report on our financial audit work

Key priorities

In the 2024–25 fiscal year, the OAG advanced multiple initiatives in support of our core responsibility, legislative auditing, with a particular focus on the following priorities:

- Transformation. Furthering our multi‑year transformation initiative, focusing on transforming audit processes, practices, and reporting; on transforming internal service delivery and business processes; and on information technology (IT) modernization.

- Engagement with our interested parties. Engaging with parliamentarians and our other interested parties, including international peers, to build on strong relationships, gather input, and use information gathered to deliver added value and increase our relevance.

- Skilled, inclusive, and engaged workforce. Fostering a skilled, inclusive, and engaged workforce and a healthy, inclusive, and respectful work environment.

Highlights for the OAG in 2024–25

- Total actual spending: $132,403,257

- Total full-time-equivalent staff: 752

For complete information on the OAG’s total spending and human resources, read the “Spending and human resources” section of this report.

Summary of Results

The following provides a summary of the OAG’s achievements in 2024–25 under its main area of activity, called “core responsibility.”

-

Core responsibility: Legislative auditing

- Actual spending: $132,403,257

- Actual full-time equivalent staff: 752

In 2024–25, we completed 20 performance audits, 3 special examinations of Crown corporations, 100 financial audits and more than 60 additional financial engagements, and our annual environmental petitions and financial commentary reports, as detailed in the infographic above. In addition, we follow up on recommendations issued in our audits to assess whether they have been implemented, and we report on this through our departmental result indicators. We measured the percentage of audit recommendations implemented for each of the types of audits we conduct. The 2024–25 results can be found in Exhibit 1.

For more information on the OAG’s core responsibility of legislative auditing, read the “Results—What we achieved” section of this report.

Message from the Auditor General of Canada

I am proud to present the OAG’s departmental results report for 2024–25. Over the past fiscal year, we have made progress in achieving important milestones that strengthen our ability to fulfill our mandate. I am also pleased to highlight the results of our efforts to provide legislators with independent information to support their role in holding government to account for financial responsibility, well‑managed programs, and transparency in public reporting.

In this report, you will find an overview of our key initiatives, our performance results, and the impact our work has had over the past fiscal year. However, before highlighting specific achievements, I want to acknowledge that my office’s results in the most recent Public Service Employee Survey reflect that we have been an organization that has been navigating significant change over the last few years to modernize who we are and how we work. Change is challenging, and our survey results flag important concerns and areas where we must improve. Senior management remains committed to listening, learning, and taking meaningful action so that we can better support our employees through this transition. In a time of transformation like the one we are navigating, it is the strength and commitment of individuals that carry the organization forward. I am grateful for their contributions, and I will be relying on all employees as we continue to modernize our approaches, increase our efficiency, and enhance our productivity. I look forward to continuing this journey with them throughout the second half of my mandate.

This report represents the second year that we are reporting on our revised departmental results framework. Our departmental result indicators help measure the progress that audited organizations have made in implementing the actions that they committed to in response to our audit recommendations. This in turn promotes greater transparency and accountability in improving public sector programs and services. Of our 3 departmental result indicators, 2 have exceeded their targets this year.

Our legislative audit work, the core of our mandate, remains central to our efforts. The professional services contracts audit discussed good practices that all federal organizations should follow when procuring professional services on behalf of the federal government, while the audit report on cybercrime recommended several ways for Canada’s cybersecurity systems and processes to be strengthened across organizations. The follow‑up audit of child and family services in Nunavut, the fourth on this topic since 2011, found that while the territory’s Department of Family Services had taken initial actions to address previously identified failures affecting services for children, youth, and families, much work remains to be done to ensure that sufficient protection is provided under Nunavut’s Child and Family Services Act. We have committed to regular follow‑up audits on this topic because it has a significant and direct impact on the health and well‑being of children and families in Nunavut.

As part of our performance audit work, the Commissioner of the Environment and Sustainable Development provided Parliament with audit reports that focused on increasingly important issues related to climate change and sustainability and included topics such as contaminated sites in the North, advancing the government’s goal to reduce plastic waste by 2030, and protecting species at risk in Canada. The 2024–25 fiscal year also marked our second year of reporting under the Canadian Net‑Zero Emissions Accountability Act, assessing progress on climate change mitigation measures and providing recommendations to guide further action.

In 2024–25, we advanced several important internal initiatives. For example, we made key improvements to our audit processes as part of a multi‑year effort to strengthen how we select and conduct audits. We also made progress in modernizing our services and IT infrastructure, renewed several of our workspaces, and achieved key milestones in our broader workplace renewal plans.

I would like to express my deepest gratitude to everyone who has contributed to our successes this past year. I am exceptionally proud of the outstanding work delivered by our dedicated employees, who consistently uphold the highest standards of quality and integrity. And as I mentioned above, with our combined strength and commitment, together we will transform the organization to accomplish great things for a better Canada, one audit at a time.

Karen Hogan, Fellow Chartered Professional AccountantFCPA

Auditor General of Canada

Results—What we achieved

Core responsibility: Legislative auditing

In this section

Description

Our audit reports provide objective, fact‑based information and advice on government programs and activities. With our audits, we support Parliament in its authorization and oversight of government spending and operations.

Our audits also help territorial legislatures, boards of Crown corporations, and audit committees in their oversight of the management of government activities. Those charged with governance use our audit findings to hold their respective organizations to account for the handling of public funds.

Financial audits assess whether the annual financial statements of the Government of Canada, the territories, Crown corporations, and other organizations are presented fairly, consistent with applicable accounting standards.

Performance audits assess whether government organizations manage programs with due regard for economy, efficiency, and environmental impact and measure their effectiveness. We have also incorporated the assessment of equity, diversity, and inclusion as a priority area for our performance audits.

Special examinations assess whether Crown corporation systems and practices provide reasonable assurance that assets are safeguarded and controlled, resources are managed economically and efficiently, and operations are managed effectively.

Quality of life impacts

As an independent agent of Parliament, the OAG indirectly contributes to the Quality of Life Framework for Canada domains, subdomains, and indicators. Our reports inform Parliament on the efficiency, effectiveness, economy, and environmental effects of government programs and financial management.

Through our legislative assurance reports, we highlight areas for improvement in government programs and services that, when acted upon, positively affect Canadians’ quality of life.

The framework’s domain, subdomain, and indicator that relate most closely to legislative auditing are as follows:

- Domain: Good governance

- Subdomain: Democracy and institutions

- Indicator: Confidence in institutions

Progress on results

This section details the OAG’s performance against its targets for its departmental result under its core responsibility of legislative auditing.

The OAG maintains a departmental results framework for reporting corporate results in accordance with the Treasury Board’s Policy on Results. Our framework came into effect on 1 April 2023 and was included in our 2023–24 Departmental Plan. Our indicators measure our influence by examining the percentage of audit recommendations that have been implemented and the improvement in terms of specific measures.

Exhibit 1—Targets and results for legislative auditing

Exhibit 1 shows the target, the date to achieve the target, and the actual result for each indicator under legislative auditing in the last 2 fiscal years.

Departmental result: Government acts on recommendations to improve public sector programs, service delivery, and financial management and reporting.

| Departmental result indicator | Target | Date to achieve target | Actual resultFootnote 1 |

|---|---|---|---|

| Percentage of performance audit and special examination recommendations implemented | At least 85% of the recommendations have been implemented, 3 years after tabling | 31 March 2025 | 2023–24: 84% 2024–25: 88%Footnote 2 |

| Percentage of financial audit recommendations implemented | At least 85% of the recommendations have been implemented, 2 years after they were issued | 31 March 2025 | 2023–24: 91% 2024–25: 88%Footnote 3 |

| Percentage of measures examined for which progress made is assessed as “substantial improvement” | At least 85% of the measures have improved, 3 years after tabling | 31 March 2025 | 2023–24: 50% 2024–25: 55%Footnote 4 |

The “Results” section of the infographic for the OAG on GC Infobase provides additional information on results and performance related to its program inventory.

Details on results

The following section describes the results for legislative auditing in 2024–25 compared with the planned results set out in the OAG’s departmental plan for the year.

Planned results, as reported in the OAG’s 2024–25 Departmental Plan, were as follows:

Audit operations

We planned to complete more than 90 financial audits, 25 performance audits, and 3 special examinations of Crown corporations during the 2024–25 fiscal year, as well as our annual commentary on our financial audit work and our annual report on environmental petitions, and to continue work on our Update on Past Audits searchable online tool.

Results achieved:

We completed 100 financial audits, 20 performance audits, and 3 special examinations of Crown corporations during the 2024–25 fiscal year. We also completed our annual commentary report on our financial audit work and our annual report on environmental petitions. For details, see the “Our current results: Audit operations” section of this report.

Corporate initiatives

We planned to advance several internal organization‑level initiatives in 2024–25, including advancing the 3 streams of our multi‑year transformation journey—audit, service, and IT; advancing our ongoing engagement initiatives with our interested parties and using feedback from these initiatives to inform and improve our audit approach; and continuing work on various initiatives to support and foster a skilled, inclusive, and engaged workforce.

Results achieved:

We advanced several of our ongoing corporate‑level initiatives in 2024–25, including work on our transformation initiative, engagement with our interested parties, and a focus on our workforce. For details, see the “Corporate initiatives” section of this report.

Our current results: Audit operations

Our role in supporting a well‑managed and accountable government is to deliver high‑quality audit work in a timely manner to Parliament, the territorial legislative assemblies, and the boards of the Crown and territorial corporations we audit. We are always looking to enhance the impact and value of our audit work to better inform decision makers and those charged with oversight responsibilities.

To assess the impact of our work on government organizations, we measure the percentage of recommendations that are implemented by the organizations we audit. This independent reporting to parliamentarians about improvements that are being made in public institutions because of our audit work promotes greater accountability and transparency in the public sector and thus contributes to improved public sector performance.

Audit quality management

Our system of quality management is a key element in ensuring that the audits we conduct meet professional standards and deliver value to Canadians. It provides the structure and support that our audit teams need to carry out high‑quality work.

In line with professional auditing standards, we evaluate our system annually to ensure it is appropriately designed, effectively implemented, and operating as intended. Our most recent evaluation identified opportunities for improvement in the application of risk assessment procedures and in the timeliness of internal reviews of our audit work. To address these, we have taken concrete actions such as enhancing training and strengthening oversight. This ongoing work reflects our continued commitment to audit excellence and continuous improvement.

Financial audits and other engagements

The OAG conducts financial audits and related work across various jurisdictions every year, including

- the federal government’s consolidated financial statements, the results of which are published annually in the Public Accounts of Canada

- the consolidated financial statements of the governments of Nunavut, Yukon, and the Northwest Territories, which are published annually in each territory’s public accounts

- the financial statements of most Crown corporations and territorial corporations and other federal organizations

During the 2024–25 fiscal year, we completed 100 financial audits. The objective of financial audits is to provide an opinion on whether an organization’s financial statements are prepared, in all material respects, in accordance with the applicable financial reporting framework. In addition, when applicable, the objective is also to provide an opinion on whether the transactions that have come to the auditor’s notice during the audit of financial statements complied with specified authorities. An unmodified audit opinion indicates that the financial statements of the organization are prepared, in all material respects, in accordance with the applicable financial reporting framework and that the transactions that we looked at during the audit of financial statements complied with specified authorities.

In the 2024–25 Departmental Plan, we had reported that we planned to complete more than 90 financial audits in the 2024–25 fiscal year. The variance between the number of planned and reported financial audits for 2024–25 derives mainly from 2 elements:

- timing differences relating to when audits were expected to be completed and when they were actually completed

- a change in the OAG’s reporting methodology for the number of financial audits completed in a given fiscal year (beginning in the 2023–24 Departmental Results Report, we are reporting on the number of audit opinions issued instead of the number of organizations for which we have issued at least 1 audit opinion)

During the 2024–25 fiscal year, 98% of our financial audit opinions were issued on an unmodified basis. The 2 audit opinions that were modified were for territorial audits, and both relate to qualifications. The first qualification was because the organization did not present its public accounts to the legislative assembly by the required statutory deadline. The second qualification was because management had not implemented reliable inventory procedures and we were unable to validate inventory quantities by alternative means.

As part of our financial audit work, we issue recommendations when we have identified opportunities for changes that would improve internal control systems, streamline operations, or enhance financial reporting practices. The impact and value of our audits is fully realized when our recommendations are implemented. We expect at least 85% of recommendations to have been implemented, 2 years after they are issued. From 1 April 2022 to 31 March 2025, 88% were implemented.

In addition to financial audits, we worked on more than 60 other financial engagements during the 2024–25 fiscal year, including agreed‑on procedure engagements for First Nations groups in relation to tax administration agreements.

During 2024–25, we also presented our annual commentary on financial audits, which provides information to Parliament on matters of significance raised during our financial audits of federal organizations. In the Commentary on the 2023–2024 Financial Audits, released in December 2024, we presented information on the results of our federal financial audits, including our audit opinions, approvals of corporate plans for Crown corporations, and COVID‑19 benefit overpayments. Our report includes observations on the Government of Canada’s consolidated financial statements, including the preparation of the consolidated financial statements, pay administration issues for government employees, deficiencies in general controls over key government IT systems, asset retirement obligations, and issues in National Defence inventory and asset pooled items. We also included a section with additional insights on environmental, social, and governance reporting.

Performance audits

The OAG conducts many performance audits every year of federal and territorial government departments, agencies, and other organizations. A performance audit is an independent, objective, and systematic assessment of how well the government is managing its activities, responsibilities, and resources. Performance audits may look at a single government program or activity, an area of responsibility that involves several government organizations, or an issue that affects many organizations.

Performance audits provide assurance and, when appropriate, recommendations for improvement to assist Parliament and its committees or the legislative assemblies of the territories in their scrutiny of the government’s management of resources and delivery of programs.

In the 2024–25 fiscal year, we presented 20 performance audit reports: 17 to the Parliament of Canada, 1 to the Yukon Legislative Assembly, 1 to the Legislative Assembly of Nunavut, and 1 to the Northwest Territories Legislative Assembly. We also completed several other reports, such as our annual report on environmental petitions. Details for all these reports appear in the “List of reports” section of this report, including a reconciliation of planned and completed reports for the 2024–25 fiscal year.

Parliament’s prorogation in early January 2025 was the main reason for the gap between the number of performance audits we had planned for 2024–25, as reported in the 2024–25 Departmental Plan, and what we reported. Without Parliament sitting, we were not able to present our audit reports for tabling. See the “List of reports” section for details.

Our federal performance audits completed in 2024–25 include the Auditor General’s June 2024 report on professional services contracts, which found that nearly 100 contracts awarded to McKinsey & Company by 20 federal departments, agencies, and Crown corporations between 2011 and 2023 often disregarded procurement rules and failed to demonstrate value for money. This audit highlighted basic requirements and good practices that all federal organizations should follow when procuring professional services on behalf of the Government of Canada and made a recommendation, agreed on by all audited organizations, that the organizations that have not already done so should implement a proactive process to identify conflicts of interest in the procurement process.

Another June 2024 report of the Auditor General, which focused on combatting cybercrime, found breakdowns in enforcement, tracking, and analysis between and across the organizations responsible for protecting Canadians from cybercrime. The report recommended several ways for Canada’s cybersecurity workforce and systems and processes to be strengthened across organizations.

The Auditor General’s June 2024 report on Sustainable Development Technology Canada found that there were significant lapses in the foundation’s management of public funds in accordance with its legislative mandate and with contribution agreements between the foundation and the Government of Canada and that Innovation, Science and Economic Development Canada did not sufficiently monitor compliance with the contribution agreements. As of May 2025, the House of Commons Standing Committee on Public Accounts had held 18 hearings on this report. We appeared 3 times at these hearings to discuss our audit findings in the report.

The Commissioner of the Environment and Sustainable Development’s April 2024 report on contaminated sites found that sites in northern Canada had not been managed to reduce the financial liability under the Federal Contaminated Sites Action Plan and the Northern Abandoned Mine Reclamation Program. Since the launch of the action plan in 2005, the financial liability for known contaminated sites increased from $2.9 billion to $10.1 billion. Recommendations in the report aim to reduce financial liability related to contaminated sites and to lower environmental and human health risks for current and future generations.

In November 2024, the Commissioner released his second report on the 2030 Emissions Reduction Plan, under the Canadian Net‑Zero Emissions Accountability Act, which found that although the federal government had advanced a variety of mitigation measures to support progress toward a net‑zero transition, implementation of measures in the plan remained insufficient to meet Canada’s target of reducing greenhouse gas emissions by 40% to 45% below 2005 levels by 2030. Making progress on implementing federal climate change measures to reduce emissions is crucial for Canada to significantly and rapidly reduce its greenhouse gas emissions and avoid current and future severe effects of climate change.

As noted above, recommendations from our performance audits highlight important areas where improvements are needed to enhance outcomes and services for Canadians and to ensure that the government’s management practices, controls, and reporting systems are functioning as they should, on the basis of organizations’ own public administration policies and best practices. We expect at least 85% of recommendations to have been implemented, 3 years after audit reports are tabled. For performance audit recommendations (including special examinations) for which progress was examined in the 2024–25 fiscal year, 88% were implemented.

While performance audits are designed to identify areas for improvement, they also highlight where government programs are delivering meaningful results. For example, between 2019 and 2023, the Canada Summer Jobs program funded more than 460,000 jobs for youth, helping to improve their success in both current and future labour markets. Youth who participated in the program had better long‑term earnings compared with those who did not. Similarly, in the audit of Canada’s response to cybercrime, the Royal Canadian Mounted Police and Communications Security Establishment Canada were found to be well coordinated in their responses to high‑priority cases, such as attacks on Government of Canada systems and critical infrastructure. These findings reflect the government’s ongoing efforts to deliver programs that produce tangible benefits for Canadians while protecting critical systems.

Special examinations

The OAG audits most, but not all, Crown corporations. The Financial Administration Act requires the OAG to audit federal parent Crown corporations at least once every 10 years.

Special examinations are a form of audit that focuses on the operations of parent federal Crown corporations. These audits examine whether a Crown corporation’s systems and practices provide reasonable assurance that its assets are safeguarded and controlled, its resources are managed economically and efficiently, and its operations are carried out effectively.

In our 2024–25 Departmental Plan, we reported that we planned to complete 3 special examinations. As planned, we completed special examinations of Pacific Pilotage Authority Canada, the Canadian Air Transport Security Authority, and the Canadian Tourism Commission in the 2024–25 fiscal year. The Canadian Tourism Commission report did not contain any recommendations. The other 2 special examination reports included recommendations for improvements in various areas, including the management of operations, corporate governance, and risk mitigation. For 1 of these 2, the report on Pacific Pilotage Authority Canada, we also reported a significant deficiency in relation to the pilotage waiver process.

International work

The OAG maintained its active participation and contributions to the International Organization of Supreme Audit Institutions (INTOSAI) committees and working groups throughout the 2024–25 fiscal year. We also continued our collaboration with the Canadian Audit and Accountability Foundation’s International Development Program, welcoming 2 fellows from the Office of the Auditor General of Rwanda. In addition, the OAG contributed to the peer review of the European Court of Auditors, specifically in the data analytics segment.

The OAG hosted an international meeting of the INTOSAI Working Group on Financial and Economic Stability on central banking auditing. We also welcomed delegations from 6 countries and organizations, including elected officials, auditors, and representatives from the Organisation for Economic Co‑operation and Development and the Intercultural Development Inventory, to exchange knowledge, strengthen institutional relationships, and explore opportunities for collaboration.

Corporate initiatives

As outlined in our 2024–25 Departmental Plan, in addition to our core audit work, our priorities included work under several initiatives under 3 umbrellas: our ongoing transformation initiative, engagement with our interested parties, and a focus on our workforce. A new strategic plan for the second half of the Auditor General’s mandate was also approved. In the 2024–25 fiscal year, we advanced the following corporate initiatives in support of these principles.

Audit transformation

As part of our audit transformation stream, in 2024–25, we undertook several key initiatives aimed at enhancing the efficiency, relevance, and impact of our audit work.

The audit selection process was supported by a more comprehensive environment scan and analysis. The list of potential new audits was reviewed and ranked by a committee of cross‑functional staff. These improvements made the process more effective to ensure that we are focusing on the most significant and timely topics.

We also began exploring the integration of artificial intelligence (AI) into auditing to increase effectiveness, efficiency, and productivity. See the “Innovation” section for details.

We advanced our audit software upgrade project, completing the planning phase and securing expertise to migrate historical data and to train users. The new system, to be implemented in the second half of 2025–26, will strengthen our tools and support high‑quality, value‑added audits going forward.

Digital transformation: Advancing digital capabilities

In 2024–25, the OAG advanced its multi‑year digital services transformation, guided by a 3‑year integrated roadmap and digital enablement plan. The OAG embedded digital expertise across its audit and corporate services, providing targeted support in project management, business analysis, vendor management, and user experience design.

We continued to build digital literacy and competencies through tailored learning initiatives, and we advanced our data strategy by modernizing reporting tools to support integrated, evidence‑based performance reporting.

The OAG also began shifting from internally managed systems to externally hosted enterprise applications to improve reliability, security, and scalability. Key milestones included the successful configuration of and data migration to SAP in preparation for a 1 April 2025 launch of the financial system and the planning to adopt the Public Service Performance Management and the Executive Talent Management System applications. The OAG completed infrastructure upgrades to support a secure and modern hybrid work environment and enhance network communications across Government of Canada organizations, and we continued the rollout of Microsoft 365 applications and features.

Services transformation

In 2024–25, the OAG advanced its service transformation efforts with a focus on enabling better decision making, increasing transparency, and streamlining internal processes in both finance and human resources. A key achievement was developing and implementing several enterprise‑level reporting dashboards, which provide management with access to timely, transparent, and integrated data across the organization.

The OAG also made progress in laying the groundwork for future system transitions.

To support employee experience and client service, the OAG modernized several service delivery platforms. These included implementing a ticketing system for task management, launching a dynamic onboarding journey leveraging new and existing platforms, and strengthening training resources for auditors, including adding new courses and updating existing ones. Together, these initiatives reflect the OAG’s commitment to continuous improvement and its strategic shift toward providing more agile, responsive, and client‑centred internal services.

While the OAG made significant progress on several modernization and optimization initiatives, the pace of change also brought its share of challenges. There was additional effort required from internal resources to manage workload and learn new processes. The integration of new tools and technologies with existing systems proved more time‑consuming than expected. These efforts required extensive coordination across teams and revealed a growing need for stronger governance mechanisms to manage interdependencies and ensure cohesive implementation.

Engagement with our interested parties

During 2024–25, we continued our work on engaging with our interested parties, including parliamentarians and international peers. We surveyed federal parliamentarians and legislators in the 3 territorial legislatures as part of our ongoing engagement initiatives to seek feedback externally and used the information gained to inform our audit approach and reporting. The survey results were very positive. At the international level, we continued our engagement activities through the INTOSAI committees and working groups, peer reviews of other audit institutions, and collaboration with representatives from other international audit organizations. For details, see the “International work” section of this report.

Skilled, inclusive, and engaged workforce

During 2024–25, the OAG prioritized fostering a skilled, inclusive, and engaged workforce by enhancing our human resource and learning system. We delivered 5 targeted sessions on harassment prevention, equity, and heritage topics. We also conducted a thorough review of our human resource policies suite to reflect best practices for diversity, equity, accessibility, and inclusion. In tandem, we launched office‑wide training for leadership development and implemented a framework for employee resource groups.

These initiatives collectively contribute to creating a healthy, inclusive, and respectful work environment, which is essential to the ongoing success and well‑being of our workforce.

OAG FLEX—Optimization of the hybrid work environment

In 2024–25, we increased the frequency of employees coming to the office. In our Ottawa office, we are leveraging a hybrid working model in temporary, modernized workplaces while our permanent workspace is being renovated. In 2024–25, planning began for redesigning the future workspaces to Government of Canada standards, which will optimize collaboration, productivity, and wellness for employees.

Public Service Employee Survey results

While much progress has been made to transform and modernize our office over the past year, our employees have voiced a number of concerns through the 2024 Public Service Employee Survey. We have begun a comprehensive review of the feedback and are prioritizing concrete, measurable steps to address the issues raised. We recognize the importance of strong employee engagement and are committed to addressing the important issues that employees have highlighted through the survey.

Key risks

The OAG proactively manages potential events that could affect its ability to achieve its planned results. In the 2024–25 fiscal year, the OAG continued to implement a range of measures aimed at mitigating risks and supporting the delivery of audits. We continuously monitor our risk landscape, adjusting our mitigation strategies in response to changes in the business environment.

Resources required to achieve results

Exhibit 2—Snapshot of resources required for legislative auditing

Exhibit 2 provides a summary of the planned and actual spending and full‑time equivalents required to achieve results. See the “Analysis of the past 3 years of spending” section of this report for an explanation of the variance between planned and actual spending.

| Resource | Planned | Actual |

|---|---|---|

| Spending | $127,534,214 | $132,403,257 |

| Full-time equivalents | 770 | 752 |

The “Finances” section of the infographic for the OAG on GC Infobase and the “People” section of the infographic for the OAG on GC Infobase provide complete financial and human resources information related to the OAG’s program inventory.

Related government priorities

Gender-based analysis plus

The OAG incorporates gender‑based analysis plus (GBA Plus) in its internal decision making and its audit work to provide parliamentarians and all Canadians with information on the government’s progress toward its gender, equity, diversity, and inclusion priorities. A summary of the activities to support the advancement of Canada’s GBA Plus commitments is included in a supplementary information table accompanying this report. In addition, we apply a GBA Plus lens to selected internal operations (such as policies and services), which aligns with the OAG’s ongoing commitment to maintaining a healthy, safe, diverse, and inclusive workplace.

United Nations 2030 Agenda for Sustainable Development and the Sustainable Development Goals

All of the OAG’s audits—financial audits, performance audits, and special examinations—contribute to Sustainable Development Goal (SDG) 16 (Peace, Justice and Strong Institutions) of the United Nations’ 2030 Agenda for Sustainable Development. In addition, the OAG is committed to aligning its direct engagement audit work to support the agenda and the underlying 17 SDGs. We consider the goals when planning and reporting on all direct engagements. During the 2024–25 fiscal year, 13 of the goals were referenced in the OAG’s published performance audits, and the SDG framework is referenced in 2 reports (Exhibit 3). In addition, internally, we have committed to completing actions that contribute to SDG 10 (Reduced Inequalities), SDG 12 (Responsible Consumption and Production), and SDG 13 (Climate Action) in our departmental sustainable development strategy. These actions include mandatory training on Indigenous topics, working toward meeting workforce availability percentages for employment equity groups at the OAG, and incorporating elements of the Greening Government Strategy into OAG procurement practices and internal policy instruments.

In the 14 audit reports that included SDGs, some had specific audit findings related to specific goals. For example, the performance audit of programs to assist seniors found that Employment and Social Development Canada had worked with Statistics Canada to further disaggregate data collected about seniors to better understand seniors’ poverty, contributing to advancing work related to SDG 1 (No Poverty) and SDG 10 (Reduced Inequalities). In addition, the audit of agriculture and climate change mitigation found that Agriculture and Agri‑Food Canada had aligned its program indicators to SDG 2 (Zero Hunger) and SDG 13 (Climate Action) to report on its contribution to the SDGs.

Exhibit 3—The number of United Nations’ Sustainable Development Goal references in the OAG’s direct engagements for the 2024–25 fiscal year

Notes:

- The number of references includes mentions of any of the United Nations’ Sustainable Development Goals or the 2030 Agenda for Sustainable Development in the OAG’s performance audit reports presented to Parliament and northern legislative assemblies and in the OAG’s special examination reports transmitted to Crown corporations during the period from 1 April 2024 to 31 March 2025. Note that a direct engagement report may refer to more than 1 goal.

- The source of the Sustainable Development Goal icons is the United Nations.

Text version of Exhibit 3

This image shows the number of United Nations’ Sustainable Development Goal references in the direct engagements of the Office of the Auditor General of Canada (OAG) for the 2024–25 fiscal year.

The number of references includes mentions of any of the United Nations’ Sustainable Development Goals or the 2030 Agenda for Sustainable Development in the OAG’s performance audit reports presented to Parliament and northern legislative assemblies and in the OAG’s special examination reports transmitted to Crown corporations during the period from 1 April 2024 to 31 March 2025. Note that a direct engagement report may refer to more than 1 goal.

The Sustainable Development Goals that are mentioned and the number of references are as follows.

| Sustainable Development Goal | Number of references |

|---|---|

| Goal 1: No poverty | 1 |

| Goal 2: Zero hunger | 1 |

| Goal 3: Good health and well-being | 1 |

| Goal 5: Gender equality | 1 |

| Goal 6: Clean water and sanitation | 1 |

| Goal 7: Affordable and clean energy | 1 |

| Goal 8: Decent work and economic growth | 1 |

| Goal 9: Industry, innovation and infrastructure | 3 |

| Goal 10: Reduced inequalities | 3 |

| Goal 12: Responsible consumption and production | 3 |

| Goal 13: Climate action | 5 |

| Goal 14: Life below water | 1 |

| Goal 15: Life on land | 1 |

| No specific goal | 2 |

The exhibit includes the Sustainable Development Goal icons. The source of these icons is the United Nations.

More information on the OAG’s contributions to Canada’s Federal Implementation Plan for the 2030 Agenda and the Federal Sustainable Development Strategy can be found in our departmental sustainable development strategy.

Innovation

In the 2024–25 fiscal year, as part of its innovation agenda, the OAG re‑established its Innovation Lab and carried out more than 20 explorations aimed at gaining time savings, improving process efficiency, and building internal knowledge of AI.

The lab experimented with AI in several ways, including an AI coaching pilot in partnership with Human Resources and a cloud‑based sandbox, which involved using a Shared Services Canada platform to run multiple experiments (translation, speech‑to‑text, first‑draft generation). We also used generative AI tools for document summarization and the creation of preliminary findings that helped support the work for some of our reports.

The Innovation Lab also delivered 6 office‑wide learning events on AI throughout the 2024–25 fiscal year, including specific sessions on how AI prompts can be used in audit work.

Also in 2024–25, the Innovation Lab successfully experimented with a mobile audit evidence capture application. This application will be scaled up during the 2025–26 fiscal year. Furthermore, a lessons‑learned exercise informed a 2025–26 experimentation agenda that includes advanced data analytics for financial audits and the integration of disruptive technologies in upcoming performance audits.

Collectively, these achievements established the governance, skills, and technical foundations needed to scale up AI solutions office‑wide in 2025–26.

Program inventory

The OAG’s core responsibility, legislative auditing, is supported by the sole program in our program inventory:

- legislative audit

Additional information related to the program inventory for legislative auditing is available on the “Results” section of the infographic for the OAG on GC Infobase.

Contracts awarded to Indigenous businesses

Government of Canada departments are required to award at least 5% of the total value of contracts to Indigenous businesses every year.

The OAG’s results for 2024–25 are as follows.

Exhibit 4—Total value of contracts awarded to Indigenous businessesFootnote 1

As shown in Exhibit 4, the OAG awarded 8.79% of the total value of all contracts to Indigenous businesses for the fiscal year.

| Contracting performance indicators | 2024–25 results |

|---|---|

| Total value of contracts awarded to Indigenous businessesFootnote 2 (A) | $994,347 |

| Total value of contracts awarded to Indigenous and non-Indigenous businesses (B) | $11,310,011 |

| Value of exceptions approved by deputy head (C) | $0 |

| Proportion of contracts awarded to Indigenous businesses [A / (B−C) × 100] | 8.79%Footnote 3 |

In its 2024–25 Departmental Plan, the OAG estimated that it would award a minimum of 5% of the total value of its contracts to Indigenous businesses by the end of 2024–25.

To ensure Indigenous businesses receive appropriate consideration in OAG procurement activities, awareness sessions have been conducted with employees responsible for business units and program areas that establish procurement plans. This helps embed the commitment to awarding contracts to Indigenous businesses at every stage of our procurement planning process.

To support economic reconciliation with Indigenous peoples, we have reserved opportunities for qualified Indigenous suppliers for major spend categories. Pre‑qualified methods of supply were identified in many areas where there is recurring contracting activity.

We have strengthened our internal governance to enhance oversight, identify emerging opportunities for Indigenous businesses, and manage related risks. Additionally, we have implemented quarterly tracking and reporting to monitor progress.

To ensure that contracts awarded to Indigenous businesses are contributing to economic reconciliation with Indigenous peoples, any supplier that has been awarded a contract designated as set aside under the Government of Canada’s Procurement Strategy for Indigenous Business is required to demonstrate adherence to the program requirements. Compliance audits may also be leveraged to confirm that the ownership criterion, control criterion, and Indigenous content criterion, where applicable, are being satisfied.

Spending and human resources

In this section

Spending

This section presents an overview of the department’s actual and planned expenditures from 2022–23 to 2027–28.

Refocusing government spending

In Budget 2023, the government committed to reducing spending by $14.1 billion over 5 years, starting in 2023–24, and by $4.1 billion annually after that. While not officially part of this spending reduction exercise, to respect the spirit of this exercise, we proactively reduced travel expenditures by 20% of planned spending in 2023–24—exceeding our 15% target. In 2024–25, we continued to limit travel, achieving a further 21% reduction.

Budgetary performance summary

Exhibit 5—Actual 3‑year spending on core responsibility (dollars)

Exhibit 5 shows the money that the OAG spent in each of the past 3 years on its core responsibility.

| Core responsibility | 2024–25 Main Estimates | 2024–25 total authorities available for use | Actual spending over 3 years (authorities used) |

|---|---|---|---|

| Legislative auditing | $127,415,620 | $138,097,801 |

|

Analysis of the past 3 years of spending

In the 2024–25 fiscal year, the OAG spent $132.4 million of its total parliamentary authorities of $138.1 million, resulting in a lapse of $5.7 million. The OAG may carry forward up to 5% of its operating budget (on the basis of Main Estimates program expenditures) into the next fiscal year, subject to parliamentary approval. For 2024–25, the OAG expects a carry‑forward of approximately $5.6 million into the 2025–26 fiscal year.

The lower amount of actual spending in 2024–25 was primarily due to a reduction in full‑time‑equivalent staffing levels, as we continued to advance our transformation initiative and realized operational efficiencies. This aligns with our long‑term objective of building a more streamlined and agile organization while reinvesting savings into innovation and modernization. In addition, operational spending was reduced as part of a prudent financial management strategy in response to funding uncertainties.

The “Finances” section of the infographic for the OAG on GC Infobase offers more financial information from previous years.

Exhibit 6—Planned 3‑year spending on core responsibility (dollars)

Exhibit 6 shows the OAG’s planned spending for each of the next 3 years on its core responsibility.

| Core responsibility | 2025–26 planned spending | 2026–27 planned spending | 2027–28 planned spending |

|---|---|---|---|

| Legislative auditing | $136,240,285 | $134,622,488 | $132,822,128 |

Analysis of the next 3 years of spending

Planned spending over the next 3 fiscal years reflects a gradual decrease, which aligns with our long‑term transformation strategy and anticipated workforce optimization while ensuring the continued delivery of our core responsibility.

The “Finances” section of the infographic for the OAG on GC Infobase offers more detailed financial information related to future years.

Funding

This section provides an overview of the department’s voted and statutory funding for its core responsibility. Consult the Government of Canada budgets and expenditures for further information on funding authorities.

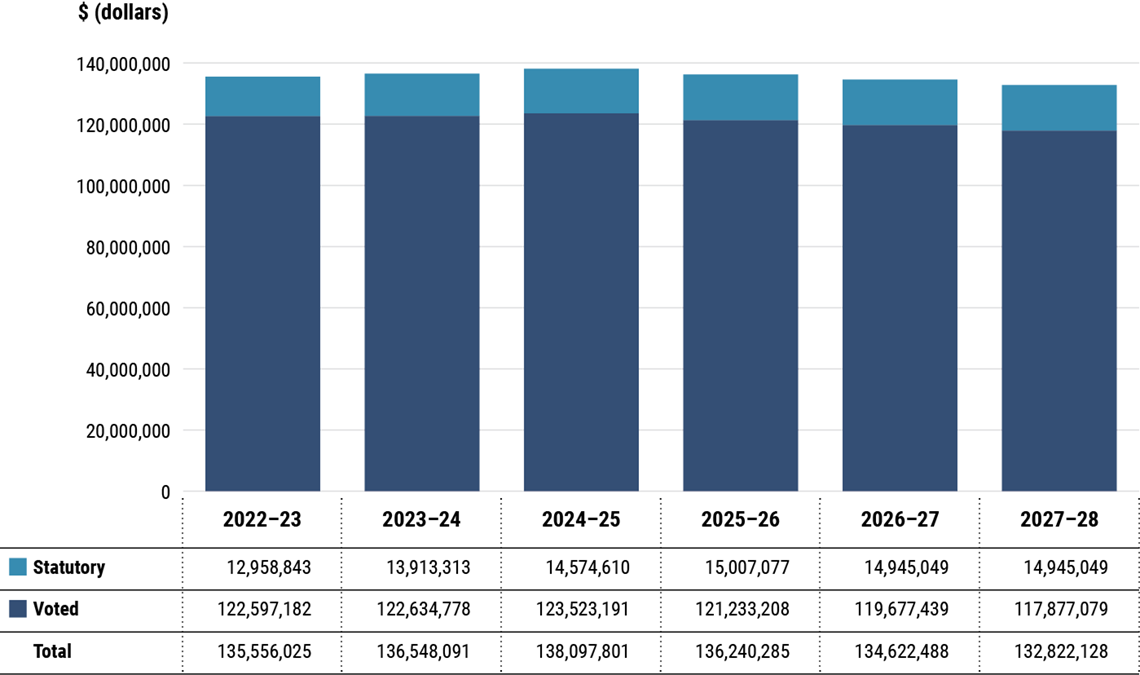

Exhibit 7—Approved funding (statutory and voted) over a 6-year period

Exhibit 7 summarizes the OAG’s approved voted and statutory funding from 2022–23 to 2027–28.

Text version of Exhibit 7

Exhibit 7 includes the following information in a bar graph:

| Fiscal year | Statutory | Voted | Total |

|---|---|---|---|

| 2022–23 | $12,958,843 | $122,597,182 | $135,556,025 |

| 2023–24 | $13,913,313 | $122,634,778 | $136,548,091 |

| 2024–25 | $14,574,610 | $123,523,191 | $138,097,801 |

| 2025–26 | $15,007,077 | $121,233,208 | $136,240,285 |

| 2026–27 | $14,945,049 | $119,677,439 | $134,622,488 |

| 2027–28 | $14,945,049 | $117,877,079 | $132,822,128 |

Analysis of statutory and voted spending over a 6‑year period

The authorities available for use mainly increased in 2023–24 and 2024–25 as a result of additional funding received for approved economic salary increases, including the associated statutory employee benefits. The 2025–26 and beyond amounts represent the Main Estimates and do not consider in year adjustments.

Consult the Public Accounts of Canada for further information on the OAG’s departmental voted and statutory expenditures.

Human resources

This section presents an overview of the OAG’s actual and planned human resources from 2022–23 to 2027–28.

Exhibit 8—Actual human resources for core responsibility

Exhibit 8 shows a summary in full-time equivalents of human resources for the OAG’s core responsibility for the previous 3 fiscal years.

| Core responsibility | 2022–23 actual full-time equivalents | 2023–24 actual full-time equivalents | 2024–25 actual full-time equivalents |

|---|---|---|---|

| Legislative auditing | 732 | 780 | 752 |

Analysis of human resources for the last 3 years

In 2024–25, as we advanced in our transformation initiative, we reduced our full-time equivalent count, aligning with our long-term vision of a more streamlined and effective organization. This has freed up additional funds for further investments in innovation and transformation.

Exhibit 9—Human resources planning summary for core responsibility

Exhibit 9 shows the planned full time equivalents for the OAG’s core responsibility for the next 3 years. Human resources for the current fiscal year are forecast on the basis of year to date.

| Core responsibility | 2025–26 planned full-time equivalents | 2026–27 planned full-time equivalents | 2027–28 planned full-time equivalents |

|---|---|---|---|

| Legislative auditing | 750 | 740 | 740 |

Financial statements

Statement of Management Responsibility Including Internal Control Over Financial Reporting

Management of the Office of the Auditor General of Canada (OAG) is responsible for the preparation of the accompanying financial statements for the year ended 31 March 2025 and for all information contained in these statements, in accordance with Canadian public sector accounting standards.

Management is responsible for the integrity and objectivity of the information in these financial statements. Some of the information in the financial statements is based on management’s best estimates and judgment and gives due consideration to materiality. To fulfill its accounting and reporting responsibilities, management maintains a set of accounts that provides a centralized record of the OAG’s financial transactions. Financial information submitted in the preparation of the Public Accounts of Canada, and included in the OAG’s Departmental Results Report, is consistent with these audited financial statements. In preparing the financial statements, management is responsible for assessing the OAG’s ability to continue as a going concern; disclosing matters related to going concern; and using the going concern basis of accounting, as applicable.

Management is also responsible for maintaining an effective system of internal control over financial reporting (ICFR), which is designed to provide reasonable assurance that financial information is reliable; that assets are safeguarded; and that transactions are properly authorized and recorded in accordance with the Financial Administration Act and other applicable legislation, regulations, authorities, and policies.

Management seeks to ensure the objectivity and integrity of data in its financial statements through the careful selection, training, and development of qualified staff; through organizational arrangements that provide appropriate divisions of responsibility; through communications aimed at ensuring that regulations, policies, standards, and managerial authorities are understood throughout the OAG; and through an annual assessment of the effectiveness of the system of ICFR.

The system of ICFR is designed to mitigate risks to a reasonable level and may not prevent or detect all misstatements. It is based on an ongoing process designed to identify key risks, to assess the effectiveness of associated key controls, and to make any necessary adjustments.

The effectiveness and adequacy of the OAG’s system of internal control are reviewed through the work of internal audit staff, who conduct periodic audits of different areas of the OAG’s operations. Also, financial services staff annually monitor ICFR. As a basis for recommending approval of the financial statements to the Auditor General, the OAG’s Audit Committee reviews management’s arrangements for internal controls and the accounting policies employed by the OAG for financial reporting purposes. The Audit Committee also meets independently with the OAG’s internal and external auditors to consider the results of their work.

A risk‑based assessment of the system of ICFR for the year ended 31 March 2025 was completed in accordance with the Treasury Board’s Policy on Financial Management. The results and action plans are summarized in the 2024–25 Annex to the Statement of Management Responsibility Including Internal Control Over Financial Reporting.

Raymond Chabot Grant Thornton Limited Liability PartnershipLLP Chartered Professional Accountants, Licensed Public Accountants, the independent auditor for the OAG, has expressed an opinion on the fair presentation of the financial statements of the OAG in conformity with Canadian public sector accounting standards, which does not include an audit opinion on the annual assessment of the effectiveness of the OAG’s ICFR.

[Original signed by]

Karen Hogan, Fellow Chartered Professional AccountantFCPA

Auditor General of Canada

[Original signed by]

Jean-René Drapeau, Chartered Professional AccountantCPA

Chief Financial Officer

Ottawa, Canada

10 July 2025

Independent Auditor’s Report

To the Speaker of the House of Commons

Report on the Audit of the Financial Statements

Opinion

We have audited the financial statements of the Office of the Auditor General of Canada (the “Office”), which comprise the statement of financial position as at 31 March 2025, and the statements of operations, change in net debt and cash flow for the year then ended, and notes to the financial statements, including a summary of significant accounting policies.

In our opinion, the accompanying financial statements present fairly, in all material respects, the financial position of the Office as at 31 March 2025, and the results of its operations, the change in its net debt and its cash flows for the year then ended in accordance with Canadian public sector accounting standards.

Basis for Opinion

We conducted our audit in accordance with Canadian generally accepted auditing standards. Our responsibilities under those standards are further described in the “Auditor’s responsibilities for the audit of the financial statements” section of our report. We are independent of the Office in accordance with the ethical requirements that are relevant to our audit of the financial statements in Canada, and we have fulfilled our other ethical responsibilities in accordance with these requirements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion.

Responsibilities of Management and Those Charged with Governance for the Financial Statements

Management is responsible for the preparation and fair presentation of the financial statements in accordance with Canadian public sector accounting standards, and for such internal control as management determines is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error.

In preparing the financial statements, management is responsible for assessing the Office’s ability to continue as a going concern, disclosing, as applicable, matters related to going concern and using the going concern basis of accounting unless management either intends to liquidate the Office or to cease operations, or has no realistic alternative but to do so.

Those charged with governance are responsible for overseeing the Office’s financial reporting process.

Auditor’s Responsibilities for the Audit of the Financial Statements

Our objectives are to obtain reasonable assurance about whether the financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditor’s report that includes our opinion. Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance with Canadian generally accepted auditing standards will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of these financial statements.

As part of an audit in accordance with Canadian generally accepted auditing standards, we exercise professional judgment and maintain professional skepticism throughout the audit. We also:

- Identify and assess the risks of material misstatement of the financial statements, whether due to fraud or error, design and perform audit procedures responsive to those risks, and obtain audit evidence that is sufficient and appropriate to provide a basis for our opinion. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control;

- Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Office’s internal control;

- Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates and related disclosures made by management;

- Conclude on the appropriateness of management’s use of the going concern basis of accounting and, based on the audit evidence obtained, whether a material uncertainty exists related to events or conditions that may cast significant doubt on the Office’s ability to continue as a going concern. If we conclude that a material uncertainty exists, we are required to draw attention in our auditor’s report to the related disclosures in the financial statements or, if such disclosures are inadequate, to modify our opinion. Our conclusions are based on the audit evidence obtained up to the date of our auditor’s report. However, future events or conditions may cause the Office to cease to continue as a going concern;

- Evaluate the overall presentation, structure and content of the financial statements, including the disclosures, and whether the financial statements represent the underlying transactions and events in a manner that achieves fair presentation.

We communicate with those charged with governance regarding, among other matters, the planned scope and timing of the audit and significant audit findings, including any significant deficiencies in internal control that we identify during our audit.

Report on Compliance with Specified Authorities

Opinion

In conjunction with the audit of the financial statements, we have audited transactions of the Office coming to our notice for compliance with specified authorities. The specified authorities for which compliance was audited are the Financial Administration Act and its regulations and the Auditor General Act.

In our opinion, the transactions of the Office that came to our notice during the audit of the financial statements have complied, in all material respects, with the specified authorities referred to above.

Responsibilities of Management for Compliance with Specified Authorities

Management is responsible for the Office’s compliance with the specified authorities named above, and for such internal control as management determines is necessary to enable the Office to comply with the specified authorities.

Auditor’s Responsibilities for the Audit of Compliance with Specified Authorities

Our audit responsibilities include planning and performing procedures to provide an audit opinion and reporting on whether the transactions coming to our notice during the audit of the financial statements are in compliance with the specified authorities referred to above.

[Original signed by]

Raymond Chabot Grant Thornton Limited Liability PartnershipLLP

Chartered Professional Accountants,

Licensed Public Accountants

Ottawa, Canada

July 10, 2025

Office of the Auditor General of Canada

Statement of Financial Position

as at March 31

| 2025 | 2024 | |

|---|---|---|

| Financial assets | ||

|

Due from the Consolidated Revenue Fund

|

9,618 | 14,590 |

|

Accounts receivable (note 4)

|

1,515 | 556 |

|

Accounts receivable held on behalf of the Government of Canada (note 4)

|

(1,380) | (125) |

| Financial assets subtotal | 9,753 | 15,021 |

| Liabilities | ||

|

Accounts payable and accrued liabilities (note 5)

|

9,340 | 14,471 |

|

Vacation pay

|

9,168 | 9,668 |

|

Sick leave benefits (note 6b)

|

1,990 | 2,211 |

|

Severance benefits (note 6c)

|

1,304 | 1,491 |

|

Maternity/parental leave benefits (note 6d)

|

626 | 469 |

| Liabilities subtotal | 22,428 | 28,310 |

| Net debt | (12,675) | (13,289) |

| Non-financial assets | ||

|

Tangible capital assets (note 7)

|

2,887 | 3,220 |

|

Prepaid expenses

|

419 | 509 |

| Non-financial assets subtotal | 3,306 | 3,729 |

| Accumulated deficit | (9,369) | (9,560) |

Contractual obligations (note 10)

The accompanying notes are an integral part of these financial statements.

Approved by

[Original signed by]

Karen Hogan, Fellow Chartered Professional AccountantFCPA

Auditor General of Canada

[Original signed by]

Jean-René Drapeau, Chartered Professional AccountantCPA

Chief Financial Officer

Ottawa, Canada

10 July 2025

Office of the Auditor General of Canada

Statement of Operations

for the year ended March 31

| 2025 | 2025 | 2024 | |

|---|---|---|---|

| Planned results (note 12) |

Actual | Actual | |

| Expenses (note 8) | |||

|

Financial audits of Crown corporations, territorial governments, and other organizations, and of the consolidated financial statements of the Government of Canada

|

69,100 | 75,535 | 75,135 |

|

Performance audits

|

59,600 | 53,669 | 59,922 |

|

Professional practices

|

11,000 | 13,337 | 12,531 |

|

Special examinations of Crown corporations

|

5,300 | 5,317 | 3,778 |

|

Sustainable development monitoring activities and environmental petitions

|

2,400 | 2,083 | 2,290 |

| Total cost of operations | 147,400 | 149,941 | 153,656 |

| Revenues | |||

|

International audits

|

600 | 402 | 1,270 |

|

Other

|

- | 120 | 190 |

|

Revenues earned on behalf of the Government of Canada

|

- | (67) | (159) |

| Net revenues | 600 | 455 | 1,301 |

| Net cost of operations before government funding and transfers | 146,800 | 149,486 | 152,355 |

| Government funding and transfers (note 3) | |||

|

Net cash provided by the Government of Canada

|

- | 137,491 | 135,713 |

|

Change in due from the Consolidated Revenue Fund

|

- | (4,972) | (336) |

|

Services provided without charge (note 9b)

|

- | 17,158 | 17,652 |

| Total government funding and transfers | 149,090 | 149,677 | 153,029 |

| Annual surplus | 2,290 | 191 | 674 |

| Accumulated deficit, beginning of year | (9,560) | (9,560) | (10,234) |

| Accumulated deficit, end of year | (7,270) | (9,369) | (9,560) |

The accompanying notes are an integral part of these financial statements.

Office of the Auditor General of Canada

Statement of Change in Net Debt

for the year ended March 31

| 2025 | 2025 | 2024 | |

|---|---|---|---|

| Planned results (note 12) |

Actual | Actual | |

| Annual surplus | 2,290 | 191 | 674 |

| Acquisition of tangible capital assets (note 7) | (2,500) | (918) | (1,792) |

| Amortization of tangible capital assets (notes 7 and 8) | 1,010 | 1,251 | 889 |

| Write-off of tangible capital assets | - | - | 203 |

| Subtotal | 800 | 524 | (26) |

| Decrease/(Increase) in prepaid expenses | - | 90 | (26) |

| Decrease/(Increase) in net debt, during the year | 800 | 614 | (52) |

| Net debt, beginning of year | (13,289) | (13,289) | (13,237) |

| Net debt, end of year | (12,489) | (12,675) | (13,289) |

The accompanying notes are an integral part of these financial statements.

Office of the Auditor General of Canada

Statement of Cash Flow

for the year ended March 31

| 2025 | 2024 | |

|---|---|---|

| Operating transactions | ||

|

Cash paid for

|

||

|

Employee salaries, wages, and benefits

|

(110,124) | (105,503) |

|

Services, transportation, communication, and other expenses

|

(15,751) | (19,951) |

|

Statutory contributions to employee benefit plans

|

(13,170) | (13,505) |

| Cash paid for operating transactions subtotal | (139,045) | (138,959) |

|

Cash received from

|

||

|

Salaries and benefits recovered

|

1,630 | 992 |

|

International audits

|

655 | 1,989 |

|

Sales tax recovered

|

184 | 1,818 |

|

Other

|

168 | 394 |

| Cash received from operating transactions subtotal | 2,637 | 5,193 |

|

Cash used by operating transactions

|

(136,408) | (133,766) |

| Capital transactions | ||

|

Cash used to acquire tangible capital assets

|

(1,083) | (1,947) |

|

Cash applied to capital transactions

|

(1,083) | (1,947) |

| Net cash provided by the Government of Canada (note 3c) | (137,491) | (135,713) |

The accompanying notes are an integral part of these financial statements.

Office of the Auditor General of Canada

Notes to the financial statements for the year ended 31 March 2025

1. Authority and objective

The Auditor General Act, the Financial Administration Act, and a variety of other acts and orders‑in‑council set out the duties of the Auditor General and the Commissioner of the Environment and Sustainable Development.

The core responsibility of the Office of the Auditor General of Canada (OAG) is legislative auditing and consists of performance audits of departments and agencies; the audit of the consolidated financial statements of the Government of Canada; financial audits of Crown corporations, territorial governments, and other organizations; special examinations of Crown corporations; and sustainable development monitoring activities and environmental petitions.

Pursuant to the Financial Administration Act, the OAG is a department of the Government of Canada. It is listed in Schedule I.1 of the act as a division or a branch of the federal public administration, and in Schedule V of the act as a separate agency. The OAG is not subject to income taxes under the provisions of the Income Tax Act.

2. Significant accounting policies

a) Basis of presentation

The financial statements of the OAG have been prepared by management in accordance with Canadian public sector accounting standards (PSAS).

b) Parliamentary authorities

The OAG is funded by the Government of Canada through parliamentary authorities. Financial reporting of authorities provided to the OAG does not parallel financial reporting according to PSAS, since authorities are primarily based on cash flow requirements. Consequently, items recognized in the Statement of Operations and in the Statement of Financial Position are not necessarily the same as those provided through authorities from Parliament. Note 3a provides a reconciliation between the 2 bases of reporting.

c) Revenues

Revenues are from international audits and other activities, such as audit professional services provided to members of the Canadian Council of Legislative Auditors. These revenues arise from transactions with performance obligations.

Revenues from transactions with performance obligations occur when there is an enforceable promise to transfer goods or services directly to a payer in return for promised consideration. These revenues are recognized when control of the benefits associated with the goods or services have transferred and there is no unfulfilled performance obligation.

Of those revenues, amounts that are considered to be earned on behalf of the Government of Canada are not available for discharging the OAG’s liabilities. Although the OAG is expected to maintain accounting control, it has no authority regarding the disposition of those revenues. As a result, revenues earned on behalf of the Government of Canada are presented as a reduction of the OAG’s gross revenues.

d) Net cash provided by the Government of Canada

The OAG operates within the Consolidated Revenue Fund (CRF), which is administered by the Receiver General for Canada. All cash received by the OAG is deposited to the CRF, and all cash disbursements made by the OAG are paid from the CRF. The net cash provided by the Government of Canada is the difference between all cash receipts and all cash disbursements, including transactions between departments of the Government of Canada.

e) Due from the Consolidated Revenue Fund

Amounts due from or to the CRF are the result of timing differences at year‑end between when a transaction affects authorities and when it is processed through the CRF. Amounts due from the CRF represent the net amount of cash that the OAG is entitled to draw from the CRF, without further parliamentary authorities to discharge its liabilities.

f) Accounts receivable and Accounts receivable held on behalf of the Government of Canada

Accounts receivable are stated at the lower of cost and net recoverable value. A valuation allowance is recorded for accounts receivable where recovery is considered uncertain.

Accounts receivable held on behalf of the Government of Canada are presented as a reduction to the financial assets on the Statement of Financial Position because they are not available to discharge the OAG’s liabilities.

g) Tangible capital assets

By nature, tangible capital assets are normally used to provide future services.

Tangible capital assets are recorded at historical cost less accumulated amortization. The OAG capitalizes the costs associated with the development of software used internally, such as installation costs, professional service contract costs, and salary costs of employees directly associated with these projects. The costs of software maintenance, project management and administration, data conversion, and training and development are expensed in the year incurred.

When conditions indicate that a tangible capital asset no longer contributes to the OAG’s ability to provide future services, or that the value of future economic benefits associated with the tangible capital asset is less than its net book value, the cost of the tangible capital asset is reduced to reflect the decline in the asset’s value. Any write‑downs of tangible capital assets are accounted for as expenses in the Statement of Operations and are not subsequently reversed.

The cost of work in progress is transferred to the applicable asset class in the year the assets are put into service.

Amortization of tangible capital assets begins when assets are put into use and is recorded using the straight‑line method over the estimated useful lives of the assets as follows:

| Tangible capital asset class | Useful life |

|---|---|

| Leasehold improvements | Lesser of the remaining term of the lease or the useful life of the improvements |

| Furniture and fixtures | 10 to 25 years |

| Informatics software | 5 years |

| Informatics hardware and infrastructure | 5 years |

| Office equipment | 4 to 10 years |

| Motor vehicle | 5 years |

| Work in progress | In accordance with asset class, once in service |

Cloud computing arrangements

Cloud computing arrangements are service contracts providing the OAG with the right to access a cloud provider’s resources over the term of the contract. The OAG does not generally receive an informatics asset as a result of these services, and related costs are recognized as operating expenses in the Statement of Operations when services are received.

h) Accounts payable and accrued liabilities

Accounts payable and accrued liabilities represent obligations of the OAG for salaries and wages, for material and supply purchases, and for the cost of services rendered to the OAG.

Salary‑related accrued liabilities are primarily determined using employees’ salaries at year‑end. Accounts payable and accrued liabilities are measured at cost.

i) Vacation pay

Vacation pay is accrued as the benefit is earned by the employees under their respective labour contracts and conditions of employment. The liability represents all unused vacation pay benefits accruing to employees. The employees’ salaries at year‑end determine the amount of these accrued vacation pay benefits.

j) Employee benefits

i) Pension benefits

All eligible employees participate in the Public Service Pension Plan, a plan administered by the Government of Canada. The OAG’s contributions are currently based on a multiple of an employee’s required contributions and may change over time, depending on the experience of the plan. The OAG’s contributions are expensed during the year in which the services are rendered and represent its total pension obligation. The OAG is not required to make contributions with respect to any actuarial deficiencies of the plan.

ii) Health and dental benefits

The Government of Canada sponsors employee benefit plans (health and dental) in which the OAG participates. Employees are entitled to health and dental benefits, as provided for under labour contracts and conditions of employment. The OAG’s contributions to the plans, which are provided without charge by the Treasury Board of Canada Secretariat, are recorded at cost based on a percentage of the salary expenses and charged to personnel expenses in the year incurred. They represent the OAG’s total obligation to the plans. Current legislation does not require the OAG to make contributions for any future unfunded liabilities of the plans.

iii) Sick leave benefits

Employees are eligible to accumulate sick leave benefits until the end of employment, according to their labour contracts and conditions of employment. Sick leave benefits are earned based on employee services rendered and are paid upon an illness or injury‑related absence. These are accumulating non‑vesting benefits that can be carried forward to future years but are not eligible for payment on retirement or termination nor can these be used for any other purpose. A liability is recorded for unused sick leave credits expected to be used in future years in excess of future allotments, based on an actuarial valuation using an accrued benefit method. Changes in actuarial assumptions and any variance between the expected and the actual experience of the sick leave benefit plan give rise to actuarial gains or losses. These gains or losses are amortized on a straight‑line basis over the expected average remaining service life of the employees, starting in the fiscal year following the one in which they arose.

iv) Severance benefits