Impact Assessment Agency of Canada Quarterly Financial Report For the quarter ended June 30, 2025

Introduction

The Impact Assessment Agency of Canada’s (IAAC) first quarterly financial statement for the period ended June 30, 2025, has been prepared by management as required by section 65.1 of the Financial Administration Act, and in the form and manner prescribed by Treasury Board under the Directive on Accounting Standards. It should be read in conjunction with the Main Estimates and Supplementary Estimates for the current year.

This report has not been subject to an external audit or review.

IAAC, led by a President who reports directly to the Minister of Environment and Climate Change, has its headquarters in Ottawa and regional offices in St. John’s, Halifax, Quebec City, Toronto, Edmonton, and Vancouver. IAAC’s activities are carried out under a single core responsibility: Impact Assessment (IA). This core responsibility encompasses two programs: Assessment Administration, Conduct and Monitoring, and Indigenous Relations and Engagement. The delivery of this core responsibility, and thereby the delivery of the two programs, is supported by Internal Services.

1. Impact Assessment

To foster sustainability, IAAC undertakes high-quality federal assessments of proposed projects based on scientific information and Indigenous Knowledge to assess health, social, economic, and environmental effects, and impacts on Indigenous Peoples and rights. These assessments help to identify and to prevent or mitigate significant adverse effects within federal jurisdiction that may be caused by major projects. IAAC conducts compliance and enforcement activities to ensure proponents adhere to the legislation, including the conditions in decision statements.Footnote 1

IAAC’s work includes:

- Leading and managing the impact assessment process for all major projects designated under the Impact Assessment Act.

- Leading Crown engagement and serving as the single point of contact for consultation and engagement with Indigenous peoples during impact assessments for designated projects.

- Providing opportunities and funding to support public participation in impact assessments.

- Working to ensure that mitigation measures are applied and are working as intended.

- Promoting uniformity and coordination of impact assessment practices across Canada through research, guidance and ongoing discussion with stakeholders and partners.

- Working with a range of international jurisdictions and organizations to exchange best practices in impact assessment.

- Working closely with other jurisdiction to achieve the goal of "one project, one review".

In delivering on its core responsibility for designated projects, IAAC collaborates with federal departments and agencies with specific expertise to provide information and advice that support the conduct of impact assessments. Where projects are associated with lifecycle regulators such as the Canada Energy Regulator, the Canadian Nuclear Safety Commission and the Offshore Petroleum Boards, IAAC works collaboratively with these partners to draw upon their expert knowledge and ensure that safety, licensing requirements, international obligations, and other key regulatory factors are considered as part of a single, integrated assessment. In accordance with the transitional provisions of Impact Assessment Act (IAA), IAAC is also responsible for continuing to manage the environmental assessment (EA) of most projects required under the former Canadian Environmental Assessment Act, 2012 (CEAA 2012).

In addition, IAAC advises and assists the Minister of Environment and Climate Change in establishing review panels and supports panels in their work. It also supports the Minister in fulfilling responsibilities under the IAA, including the development and issuance of enforceable IA decision statements.

2. Internal Services

Internal Services are resources that are required to enable program delivery and are activities provided to meet corporate obligations of IAAC. Internal Services include:

- Acquisition management services,

- Communications services,

- Financial management services,

- Human resource management services,

- Information management services,

- Information technology services,

- Legal services,

- Management and oversight services,

- Materiel management services, and

- Real property services.

IAAC has a mandate to administer four Grant and Contribution funding programs (Funding Programs):

- Participant Funding Program - to facilitate the participation of the public and Indigenous Peoples in preparing for possible IAs of designated projects, for the IA of projects by IAAC or a review panel, for the design and implementation of follow-up programs for projects, and for regional and strategic assessments.

- Policy Dialogue Program - to promote uniformity and harmonization in relation to the assessment of effects across Canada and all levels of government; promote and monitor the quality of IAs under the Act; develop policy related to the Act; and to engage with Indigenous Peoples on policy issues related to the Act.

- Research Program - to promote or conduct research on matters related to IAs that focuses on policy-relevant research on impact assessment and enabling research partnership opportunities.

- Indigenous Capacity Support Program - to promote communication and cooperation with Indigenous peoples ensuring respect for the rights of Indigenous peoples and ensuring the consideration of Indigenous knowledge.

IAAC also has federal administrative responsibilities under the environmental and social protection regimes set out in sections 22 and 23 of the 1975 James Bay and Northern Quebec Agreement to review and determine whether projects proposed under this Agreement should proceed and under which conditions. The President of IAAC is designated by Order-in-Council as the federal administrator of these processes.

Basis of Presentation

This quarterly report has been prepared by management using the expenditure basis of accounting. The accompanying Statement of Authorities includes IAAC’s spending authorities granted by Parliament and those used by IAAC consistent with the Main Estimates and Supplementary Estimates (as applicable) for the 2025-2026 fiscal year. This quarterly report has been prepared using a special purpose financial reporting framework designed to meet financial information needs with respect to the use of spending authorities.

The authority of Parliament is required before funds can be spent by the Government. Approvals are given in the form of annually approved limits through appropriation acts, or through legislation in the form of statutory spending authority for specific purposes.

When Parliament is dissolved for the purposes of a general election, section 30 of the Financial Administration Act authorizes the Governor General, under certain conditions, to issue a special warrant authorizing the Government to withdraw funds from the Consolidated Revenue Fund. A special warrant is deemed to be an appropriation for the fiscal year in which it is issued.

IAAC uses the full accrual method of accounting to prepare and present its annual financial statements that are part of the departmental results reporting process. However, the spending authorities voted by Parliament remain on an expenditure basis.

Highlights of Fiscal Quarter and Fiscal Year-to-Date (YTD) Results

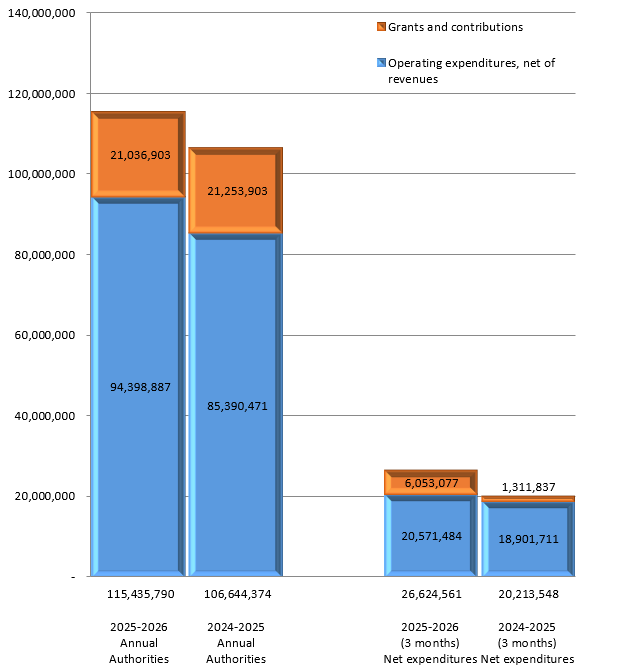

Figure 1 outlines the net budgetary authorities ($115.44M in 2025–2026 and $106.64M in 2024–2025), which represents the resources available for the year as of June 30, 2025, net of the revenue that is forecasted to be collected. IAAC’s available authorities, net of revenues, currently represent an increase of $8.80M (8.24%) from the previous year. This variance is due to new funding announced in the Fall Economic Statement 2022 (FES 2022) for IAAC to continue to implement the IAA and complete assessments started under the CEAA 2012.

Figure 1 also outlines IAAC’s first quarter year-to-date budgetary expenditures, net of revenues that have increased by $6.41 M (31.72%) from the previous year ($26.62M in 2025–2026 and $20.21M in 2024–2025). This increase is explained by the following:

- Transfer payments (grants and contributions) increased by $4.74M ($6.05M in 2025–2026 and $1.31M in 2024–2025) as a result of IAAC’s multi-year contractual obligations maturing.

- Personnel expenditures increased by $2.44M ($18.22M in 2025–2026 and $15.78M in 2024–2025) due to an increase in the number of employees hired in 2024-2025, the increase in wages, and the related cost of employee benefits.

- Other budgetary expenditures decreased by $0.64M ($2.48M in 2025–2026 and $3.12M in 2024–2025) due to expenditures being limited to routine and legally required items during the caretaker convention.

- Revenues increased by $0.13M ($0.13M in 2025–2026 and nil in 2024–2025) following the resumption of cost recovery activities once the IAA amendment took effect on June 20, 2024.

Risks and Uncertainties

IAAC’s expenditures and revenues are influenced by the number of assessments underway during a given fiscal year and are affected by the economic conditions that are outside the control of IAAC. To offset a portion of its expenditures, IAAC has vote-netted revenue authority to recover certain incurred costs from proponents in the conduct of assessments by review panels. The timing of revenue collection is uncertain and may impact IAAC’s overall financial results.

In addition, the timing of requests for grant or contribution participant funding under the four funding programs varies and is unpredictable. A contribution commitment to participant funding may be planned in one year but could be realized across multiple fiscal years depending on the progression of the assessment. Unused contribution commitments are carried forward from one year to another and are honored by IAAC as they materialize.

IAAC is also subject to litigation, the extent and costs of which are uncertain. If applicable, these costs are normally covered by IAAC’s annual appropriations.

Approval by Senior Officials

Approved by:

(the original version was signed by)

____________________________________

Patricia Brady

Acting President

Ottawa, Canada

August 29, 2025

(the original version was signed by)

____________________________________

Charles Vigneault

Acting Vice-President, Corporate Services and Chief Financial Officer

Ottawa, Canada

Statement of Authorities (unaudited)

| Total available for use for the year ending March 31, 2026 | Used during the quarter ended June 30, 2025 | Year-to-date used at quarter ended June 30, 2025 | |

|---|---|---|---|

VOTE 1 - Net operating expenditures |

84,212,146 |

18,024,799 |

18,024,799 |

VOTE 5 - Grants and contributions |

21,036,903 |

6,053,077 |

6,053,077 |

Statutory Authorities - Employee benefits |

10,186,741 |

2,546,685 |

2,546,685 |

| Total Authorities |

115,435,790 |

26,624,561 |

26,624,561 |

| Total available for use for the year ended March 31, 2025 | Used during the quarter ended June 30, 2024 | Year-to-date used at quarter ended June 30, 2024 | |

|---|---|---|---|

VOTE 1 - Net operating expenditures |

77,358,614 |

16,893,747 |

16,893,747 |

VOTE 5 - Grants and contributions |

21,253,903 |

1,311,837 |

1,311,837 |

Statutory Authorities - Employee benefits |

8,031,857 |

2,007,964 |

2,007,964 |

Total Authorities |

106,644,374 |

20,213,548 |

20,213,548 |

IAAC Budgetary Expenditures by Standard Object (unaudited)

| Planned expenditures for the year ending March 31, 2026 | Expended during the quarter ended June 30, 2025 | Year-to-date used at quarter ended June 30, 2025 | |

|---|---|---|---|

| Expenditures | |||

Personnel |

76,766,746 |

18,222,673 |

18,222,673 |

Transportation and telecommunications |

2,687,311 |

175,215 |

175,215 |

Information |

692,591 |

24,329 |

24,329 |

Professional services |

14,265,729 |

2,180,082 |

2,180,082 |

Rentals |

119,746 |

11,150 |

11,150 |

Purchased repair and maintenance |

121,569 |

23,741 |

23,741 |

Utilities, materials and supplies |

231,391 |

9,585 |

9,585 |

Acquisition of machinery and equipment |

2,684,771 |

60,470 |

60,470 |

Transfer payments |

21,036,903 |

6,053,077 |

6,053,077 |

Other expenses |

26,924 |

(672) |

(672) |

Total gross budgetary expenditures |

118,633,681 |

26,759,650 |

26,759,650 |

| Less revenues netted against expenditures |

|||

Panel reviews |

3,197,891 |

135,089 |

135,089 |

| Total net budgetary expenditures |

115,435,790 |

26,624,561 |

26,624,561 |

Note 1: IAAC has authority to collect up to $8,001,000 in vote-netted revenue.

| Planned expenditures for the year ended March 31, 2025 | Expended during the quarter ended June 30, 2024 | Year-to-date used at quarter ended June 30, 2024 | |

|---|---|---|---|

| Expenditures | |||

Personnel |

66,233,721 |

15,780,293 |

15,780,293 |

Transportation and telecommunications |

2,668,837 |

258,213 |

258,213 |

Information |

1,223,625 |

82,087 |

82,087 |

Professional services |

11,704,331 |

2,299,589 |

2,299,589 |

Rentals |

115,016 |

14,635 |

14,635 |

Purchased repair and maintenance |

631,520 |

0 |

0 |

Utilities, materials and supplies |

581,056 |

12,280 |

12,280 |

Acquisition of machinery and equipment |

2,842,058 |

455,822 |

455,822 |

Transfer payments |

21,253,903 |

1,311,837 |

1,311,837 |

Other expenses |

15,307 |

(1,208) |

(1,208) |

| Total gross budgetary expenditures |

107,269,374 |

20,213,548 |

20,213,548 |

| Less revenues netted against expenditures |

|||

Panel reviews |

625,000 |

0 |

0 |

| Total net budgetary expenditures |

106,644,374 |

20,213,548 |

20,213,548 |

Note 1: IAAC has authority to collect up to $8,001,000 in vote-netted revenue.