Adapting the Canada Emergency Wage Subsidy to Protect Jobs and Promote Growth

Backgrounder

The Government of Canada has taken immediate, significant and decisive action to protect the health of Canadians, support Canadian workers and businesses, and stabilize the Canadian economy during the global COVID-19 outbreak.

As part of its COVID-19 Economic Response Plan, the government introduced the Canada Emergency Wage Subsidy (CEWS) to prevent further job losses, encourage employers to quickly rehire workers previously laid off as a result of COVID-19, and help better position the Canadian economy as we bridge to the other side.

Continuing to Protect Canadian Jobs

The CEWS was put in place for an initial 12-week period from March 15 to June 6, 2020, providing a 75-per-cent wage subsidy to eligible employers. On May 15, 2020 Finance Minister Bill Morneau announced that the Government of Canada would extend the CEWS by an additional 12 weeks to August 29, 2020. This announcement was part of a public consultation the government undertook to ensure the CEWS was best positioned to help get Canadians hired back quickly as provincial and territorial economies begin to reopen. The government announced on June 10, 2020 that the same eligibility criteria for the initial three 4-week periods (March 15 to June 6, 2020) would continue to apply for Period 4 (June 7 to July 4, 2020).

The government is proposing a further extension of the CEWS, until December 19, 2020, providing proposed program details until November 21, 2020, and has shared draft legislative proposals. These proposals would adapt the CEWS to support more workers and businesses, better protect jobs and promote growth, and effectively respond as the economy continues to reopen. The draft legislative proposals would also give the government some flexibility to ensure the wage subsidy can adjust to the needs of businesses if economic conditions change. The estimated total fiscal cost in 2020-21 for the CEWS program that is being announced today is $83.6 billion.

What We Heard During Consultations on the CEWS

During the consultations, we heard from many businesses and employers. They indicated that the CEWS was invaluable in keeping workers on the payroll and helping to bring workers back. Many ideas were shared on how the design of the CEWS could be made better to provide greater support to businesses and employees, as businesses reopen and continue to recover and grow. Some of these ideas are illustrated below.

- Cliff Effect: Employers are worried about the “cliff effect” caused by the elimination of support at the 30-per-cent revenue drop threshold in the current CEWS design. There are concerns that it may induce inefficient decisions, in addition to being unfair. Many suggested that an effective way to deal with this would be to provide for a gradual reduction in the CEWS rate as revenues increase.

“My ask is that the 30% threshold be lowered (at minimum) each month to allow businesses to increase their sales and still be eligible for CEWS.” – Individual stakeholder (small business owner)

- Revenue Test: Some employers find the current 30 per cent revenue decline test too stringent. They argue that businesses that experience revenue drops of less than this amount may still be heavily affected by the pandemic. This would also become more relevant as the economy reopens and activity increases but remains lower than normal for some businesses.

“Having options of a tiered support may better support those organizations that are still hit really hard by the pandemic but that have not seen a full 30% reduction in revenue. At the moment it is all or nothing, you either get 0-10% support or 75% support but have nothing for those in between.” – Individual stakeholder (tax professional)

- Extension: Many employers worry that the current 12-week extension until August 29 may not be enough to help businesses that continue to struggle given the uneven impacts across economic sectors.

“It is important to continue to help businesses to restart their activities. Otherwise, we will have to face an explosion of unemployed people and the closing of businesses and organizations. (translation)” – Sports and community association

- Highly Impacted Firms: All firms that qualify are treated the same way once they qualify for the program, while some may require more help. There is recognition among employers of a need to provide additional support for those that were particularly adversely impacted.

“The CEWS… should be adjusted to potentially target especially hard-hit sectors, such as food service…” – Food-related industry association

Ensuring Strong Subsidy Support for Those who Need It

Effective July 5, 2020, the CEWS would consist of two parts:

- a base subsidy available to all eligible employers that are experiencing a decline in revenues, with the subsidy amount varying depending on the scale of revenue decline; and

- a top-up subsidy of up to an additional 25 per cent for those employers that have been most adversely affected by the COVID-19 crisis.

The two-part CEWS would apply with respect to the remuneration of active employees. A separate CEWS rate structure would apply to furloughed employees (as described further below). In addition, a safe harbour would be available to ensure that, through August 29 (periods 5 and 6), employers would have access to a CEWS rate that is at least as generous as they would have had under the initial CEWS structure, as described further below (see Safe harbour rule for Periods 5 and 6).

Base subsidy for all employers impacted by the crisis

Effective July 5, 2020 (i.e., Period 5 and subsequent periods), employers that have been affected by the COVID-19 crisis would be eligible for a base CEWS amount for active employees. This base CEWS would be a specified rate, applied to the amount of remuneration paid to the employee for the eligibility period, on remuneration of up to $1,129 per week. The rate of the base CEWS would now vary depending on the level of revenue decline, and its application would be extended to employers with a revenue decline of less than 30 per cent (see Table 1). This expansion would mean that all eligible employers with a revenue decline would now qualify for CEWS support.

The specified rate would be determined based on the change in an eligible employer's monthly revenues, as described further below (see Reference Periods for the Drop-in-Revenues Test).

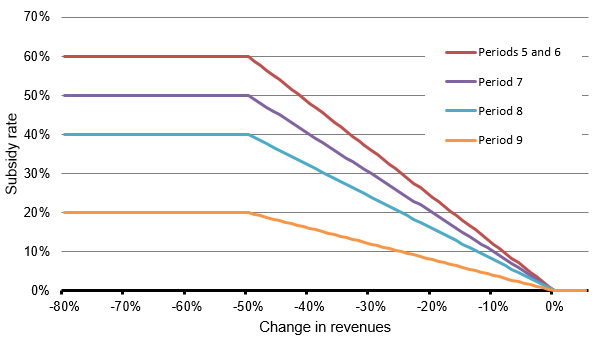

The maximum base CEWS rate would be provided to employers with a revenue drop of 50 per cent or more. Employers with a revenue drop of less than 50 per cent would be eligible for a lower base CEWS rate, as shown in Table 1. The decline in the base CEWS rate between a 50-per-cent revenue drop and zero provides a smooth phase-out so that businesses can grow and rehire without worrying about a sharp drop in support as economic activity returns.

The maximum base CEWS rate would be gradually reduced from 60 per cent in Periods 5 and 6 (July 5 to August 29) to 20 per cent in Period 9 (October 25 to November 21).

| Timing | Period 5*: July 5 – August 1 |

Period 6*: August 2 – August 29 | Period 7: August 30 – September 26 | Period 8: September 27 – October 24 | Period 9: October 25 – November 21 |

|---|---|---|---|---|---|

| Maximum weekly benefit per employee | Up to $677 | Up to $677 | Up to $565 | Up to $452 | Up to $226 |

| Revenue drop | |||||

| 50% and over | 60% | 60% | 50% | 40% | 20% |

| 0% to 49% | 1.2 x revenue drop (e.g., 1.2 x 20% revenue drop = 24% base CEWS rate) |

1.2 x revenue drop (e.g., 1.2 x 20% revenue drop = 24% base CEWS rate) |

1.0 x revenue drop (e.g., 1.0 x 20% revenue drop = 20% base CEWS rate) |

0.8 x revenue drop (e.g., 0.8 x 20% revenue drop = 16% base CEWS rate) |

0.4 x revenue drop (e.g., 0.4 x 20% revenue drop = 8% base CEWS rate) |

| * In Periods 5 and 6, employers who would have been better off in the CEWS design in Periods 1 to 4 would be eligible for a 75% wage subsidy if they have a revenue decline of 30% or more. As described further below (see Safe harbour rule for Periods 5 and 6). | |||||

Figure 1

Top-up subsidy for the most adversely affected employers

A top-up CEWS of up to 25 per cent would be available to employers that were the most adversely impacted by the pandemic. Generally, an eligible employer’s top-up CEWS would be determined based on the revenue drop experienced when comparing revenues in the preceding 3 months to the same months in the prior year. Under the alternative approach to the calculation of baseline revenues, an eligible employer’s top-up CEWS would be determined based on the revenue drop experienced when comparing average monthly revenue in the preceding 3 months to the average monthly revenue in January and February 2020.

- For example, if an employer had $600,000 in revenue between April 1 and June 30, 2019, and $210,000 in revenue between April 1 and June 30, 2020, the employer would have a 3-month revenue drop of 65 per cent.

- Under the alternative approach, if an employer had $400,000 in revenue between January 1 and February 29, 2020 (average monthly revenue of $200,000), and $210,000 in revenue between April 1 and June 30, 2020 (average monthly revenue of $70,000), the employer would have a 3-month revenue drop of 65 per cent.

Employers that have experienced a 3-month average revenue drop of more than 50 per cent would receive a top-up CEWS rate equal to 1.25 times the average revenue drop that exceeds 50 per cent, up to a maximum top-up CEWS rate of 25 per cent, which is attained at a 70‑per‑cent revenue decline. As with the base CEWS rate, the top-up CEWS rate would apply to remuneration of up to $1,129 per week. The top-up CEWS rate for selected average revenue drop levels is illustrated in Table 2 below.

| 3-month average revenue drop | Top-up CEWS rate | Top-up calculation = 1.25 x (3 month revenue drop - 50%) |

|---|---|---|

| 70% and over | 25% | 1.25 x (70%-50%) = 25% |

| 65% | 18.75% | 1.25 x (65%-50%) = 18.75% |

| 60% | 12.5% | 1.25 x (60%-50%) = 12.5% |

| 55% | 6.25% | 1.25 x (55%-50%) = 6.25% |

| 50% and under | 0.0% | 1.25 x (50%-50%) = 0.0% |

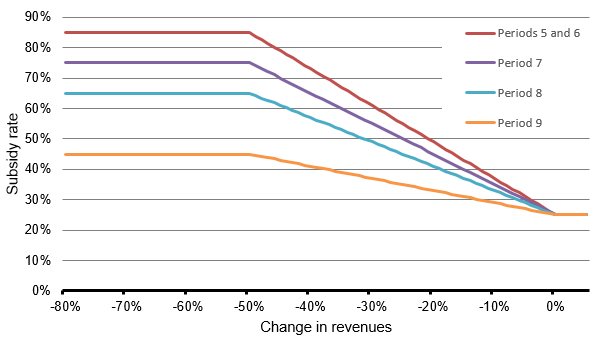

The overall CEWS rate would be equal to the top-up CEWS rate plus the base CEWS rate. Table 3 shows the combined base and top-up CEWS rates for Periods 5 to 9 for the most adversely affected employers.

| Timing | Period 5*: July 5 – August 1 | Period 6*: August 2 – August 29 | Period 7: August 30 – September 26 | Period 8: September 27 – October 24 | Period 9: October 25 – November 21 |

|---|---|---|---|---|---|

| Maximum weekly benefit per employee | Up to $960 | Up to $960 | Up to $847 | Up to $734 | Up to $508 |

| Revenue drop in the current 1-month reference period | |||||

| 50% or more | 85% (60% base CEWS + 25% top-up) |

85% (60% base CEWS + 25% top-up) |

75% (50% base CEWS + 25% top-up) |

65% (40% base CEWS + 25% top-up) |

45% (20% base CEWS + 25% top-up) |

| 0% to 49% | 1.2 x revenue drop + 25% (e.g., 1.2 x 20% revenue drop + 25% = 49% CEWS rate) | 1.2 x revenue drop + 25% (e.g., 1.2 x 20% revenue drop + 25% = 49% CEWS rate) | 1 x revenue drop + 25% (e.g., 1 x 20% revenue drop + 25% = 45% CEWS rate) | 0.8 x revenue drop + 25% (e.g., 0.8 x 20% revenue drop + 25% = 41% CEWS rate) | 0.4 x revenue drop + 25% (e.g., 0.4 x 20% revenue drop + 25% = 33% CEWS rate) |

| * In Periods 5 and 6, employers who would have been better off in the CEWS design in Periods 1 to 4 would be eligible for a 75% wage subsidy if they have a revenue decline of 30% or more. As described further below (see Safe harbour rule for Periods 5 and 6). | |||||

Table 4 illustrates the interaction of the 3-month drop in revenue test for the top-up CEWS and the month-over-month revenue test for the base CEWS for Periods 5 and 6. For example, an employer that is recovering with a revenue drop of 20 per cent in Period 5 and a preceding 3-month average revenue drop of 60 per cent would benefit from a base CEWS rate of 24 per cent and a top-up CEWS rate of 12.5 per cent, which would provide a combined CEWS rate of 36.5 per cent.

| Revenue drop in the current 1-month reference period | 70% or more | 50% to 69% | 0% to 49% |

|---|---|---|---|

| 50% or more | 85% (60% base CEWS + 25% top-up) | 60% + 1.25 x (3 month revenue drop-50%) (e.g., 60% base CEWS + 1.25 x (60% 3 month revenue drop - 50%) = 72.5% CEWS rate) |

60% (60% base CEWS + 0% top-up) |

| 0% to 49% | 1.2 x revenue drop + 25% (e.g., 1.2 x 20% revenue drop + 25% = 49% CEWS rate) |

1.2 x revenue drop + 1.25 x (3 month revenue drop-50%) (e.g., 1.2 x 20% revenue drop + 1.25 x (60% 3-month revenue drop-50%) = 36.5% CEWS rate) |

1.2 x revenue drop (e.g., 1.2 x 20% revenue drop = 24% CEWS rate) |

| No revenue drop | 25% (0% base CEWS + 25% top-up) | 1.25 x (3 month revenue drop-50%) (e.g., 1.25 x (60% 3-month revenue drop-50%) = 12.5% CEWS rate) |

nil |

| * In Periods 5 and 6, employers who would have been better off in the CEWS design in Periods 1 to 4 would be eligible for a 75% wage subsidy if they have a revenue decline of 30% or more. As described further below (see Safe harbour rule for Periods 5 and 6). | |||

Figure 2

Safe harbour rule for Periods 5 and 6

For Periods 5 and 6, an eligible employer would be entitled to a CEWS rate not lower than the rate that they would be entitled to if their entitlement were calculated under the CEWS rules that were in place for Periods 1 to 4. This means that in Periods 5 and 6, an eligible employer with a revenue decline of 30 per cent or more in the relevant reference period would receive a CEWS rate of at least 75 per cent or potentially an even higher CEWS rate using the new rules outlined above for the most adversely affected employers (up to 85 per cent).

CEWS for Furloughed Employees

For Periods 5 and 6, the subsidy calculation for a furloughed employee would remain the same as for Periods 1 to 4. It would be the greater of:

- For arm’s-length employees, 75 per cent of the amount of remuneration paid, up to a maximum benefit of $847 per week; and

- 75 per cent of the employee’s pre-crisis weekly remuneration up to a maximum benefit of $847 per week or the amount of remuneration paid, whichever is less.

Beginning in Period 7, CEWS support for furloughed employees would be adjusted to align with the benefits provided through the Canada Emergency Response Benefit (CERB) and/or Employment Insurance (EI). This would ensure equitable treatment of employees on furlough between both programs, provide greater clarity to workers as to their compensation as compared to a changing subsidy rate based on their employer’s revenue in a given month and, when combined with draftlegislative changes to the interaction with the CERB (i.e., the elimination of the 14-days rule, as discussed below), make it easier to transition employees on to CEWS so that they are reconnected with their employer.

For Period 5 and subsequent periods, the CEWS for furloughed employees would be available to eligible employers that qualify for either the base rate or the top-up for active employees in the relevant period.

The employer portion of contributions in respect of the Canada Pension Plan, Employment Insurance, the Quebec Pension Plan, and the Quebec Parental Insurance Plan in respect of furloughed employees would continue to be refunded to the employer.

Eligible Remuneration

No changes are proposed to the definition of eligible remuneration. Eligible remuneration may include salary, wages, and other remuneration like taxable benefits. These are amounts for which employers would generally be required to withhold or deduct amounts to remit to the Receiver General on account of the employee's income tax obligation. However, it does not include severance pay, or items such as stock option benefits or the personal use of a corporate vehicle.

For active arm’s-length employees, the amount of remuneration would be based solely on actual remuneration paid for the eligibility period, without reference to the pre-crisis remuneration concept used for earlier CEWS periods, which is explained in the Finance Canada backgrounder of April 11, 2020. A modified special rule would apply to active employees that do not deal at arm's length with the employer. For Period 5 and subsequent periods, the wage subsidy for such employees would be based on the employee’s weekly eligible remuneration or pre-crisis remuneration, whichever is less, up to a maximum of $1,129. The subsidy would only be available in respect of non-arm's-length employees that were employed prior to March 16, 2020.

For Period 4, the pre-crisis remuneration of an employee would be based on the average weekly remuneration paid to the employee from January 1 to March 15, 2020; from March 1, 2019 to May 31, 2019; or from March 1, 2019 to June 30, 2019. For Period 5 and subsequent periods, the pre-crisis remuneration of an employee would be based on the average weekly remuneration paid to the employee from January 1 to March 15, 2020 or from July 1, 2019 to December 31, 2019. In all cases, the calculation of average weekly remuneration would exclude any period of 7 or more consecutive days without remuneration. Employers can choose which period to use on an employee-by-employee basis.

Eligible Employers and Employees

Eligible employers include individuals, taxable corporations and trusts, partnerships consisting of eligible employers, non‑profit organizations and registered charities. Public institutions are generally not eligible for the subsidy. As announced on May 15, 2020, eligible employers also include the following groups:

- Partnerships that are up to 50-per-cent owned by non-eligible members;

- Indigenous government-owned corporations that are carrying on a business, as well as partnerships where the partners are Indigenous governments and eligible employers;

- Registered Canadian Amateur Athletic Associations;

- Registered Journalism Organizations; and

- Non-public colleges and schools, including institutions that offer specialized services, such as arts schools, driving schools, language schools or flight schools.

An eligible employee is an individual who is employed in Canada. Effective July 5, 2020, the eligibility criteria would no longer exclude employees that are without remuneration in respect of 14 or more consecutive days in an eligibility period.

Calculating Revenues

An employer's revenue for the purposes of the CEWS is its revenue in Canada earned from arm's-length sources. Revenues from extraordinary items and amounts on account of capital are excluded.

For registered charities and non-profit organizations, the calculation includes most forms of revenue, excluding revenues from non-arm's length persons. These organizations are allowed to choose whether to include revenue from government sources as part of the calculation. Once chosen, the same approach would have to apply throughout the program period.

Special rules for the computation of revenue are provided to take into account certain non-arm's-length transactions, such as where an employer sells all of its output to a related company that in turn earns arm's-length revenue. As well, affiliated groups are able to elect to compute revenue on a consolidated basis.

Reference Periods for the Drop-in-Revenues Test

For the purpose of the base CEWS, eligibility would generally be determined by the change in an eligible employer's monthly revenues, year-over-year, for the applicable calendar month. Table 5 below outlines each claiming period and the relevant period for determining an eligible employer’s change in revenue. For Period 5 and all subsequent periods, an eligible employer would be able to use the greater of its percentage revenue decline in the current period and that in the previous period for the purpose of determining its qualification for the base CEWS and its base CEWS rate in the current period. This would provide certainty and be a continuation of the rules for Periods 1 to 4 that allowed an employer that met the revenue test in one period to automatically qualify for the following period.

Employers that have elected to use the alternative approach for the first 4 periods would be able to either maintain that election for Period 5 and onward or revert to the general approach. Similarly, employers that have used the general approach for the first 4 periods would be able to either continue with the general approach or elect to use the alternative approach for Period 5 and onward. Whichever approach they choose would apply for Period 5 and onward and would apply to the calculation of the base CEWS and the top-up CEWS. This would provide flexibility for employers to adjust their approach in light of new circumstances they may be experiencing as the CEWS is extended.

| Claim period | General approach | Alternative approach | |

|---|---|---|---|

| Period 5 | July 5 to August 1, 2020 | July 2020 over July 2019 or June 2020 over June 2019 | July 2020 or June 2020 over average of January and February 2020 |

| Period 6 | August 2 to August 29, 2020 | August 2020 over August 2019 or July 2020 over July 2019 | August 2020 or July 2020 over average of January and February 2020 |

| Period 7 | August 30 to September 26, 2020 | September 2020 over September 2019 or August 2020 over August 2019 | September 2020 or August 2020 over average of January and February 2020 |

| Period 8 | September 27 to October 24, 2020 | October 2020 over October 2019 or September 2020 over September 2019 | October 2020 or September 2020 over average of January and February 2020 |

| Period 9 | October 25 to November 21, 2020 | November 2020 over November 2019 or October 2020 over October 2019 | November 2020 or October 2020 over average of January and February 2020 |

For the purpose of the top-up CEWS, eligibility would generally be determined by the change in an eligible employer's revenues for a 3-month period. Table 6 below outlines each claiming period and the relevant period for determining an eligible employer’s average change in revenue.

| Claim period | General approach | Alternative approach | |

|---|---|---|---|

| Period 5 | July 5 to August 1, 2020 | April to June 2020 over April to June 2019 | April to June 2020 average over January and February 2020 average* |

| Period 6 | August 2 to August 29, 2020 | May to July 2020 over May to July 2019 | May to July 2020 average over January and February 2020 average* |

| Period 7 | August 30 to September 26, 2020 | June to August 2020 over June to August 2019 | June to August 2020 average over January and February 2020 average* |

| Period 8 | September 27 to October 24, 2020 | July to September 2020 over July to September 2019 | July to September 2020 average over January and February 2020 average* |

| Period 9 | October 25 to November 21, 2020 | August to October 2020 over August to October 2019 | August to October 2020 average over January and February 2020 average* |

| * The calculation would equal the average monthly revenue over the 3 months of the reference period divided by the average revenue for the months of January and February 2020. | |||

Legislative Amendments

The government has shared draft legislative proposals to make the changes to the CEWS described in this backgrounder as well as changes in response to feedback received from stakeholders. These proposed changes, which would generally apply as of March 15, 2020, include:

- providing an appeal process based on the existing procedure for notices of determination that allows for an appeal to the Tax Court of Canada;

- providing continuity rules for the calculation of an employer’s drop in revenues in certain circumstances where the employer purchased all or substantially all the assets used in carrying on business by the seller;

- allowing prescribed organizations that are registered charities or non-profit organizations to choose whether to include government-source revenue for the purpose of computing their reductions in qualifying revenue; and

- allowing entities that use the cash method of accounting to elect to use accrual based accounting to compute their revenues for the purpose of the CEWS.

The government is also proposing to move forward with previously released legislative changes, including relieving changes for calculating pre-crisis “baseline” remuneration, for corporations that have amalgamated and for eligible entities that use payroll service providers. The government is also proposing to move forward with the amendment that would align the treatment of trusts and corporations for the purposes of the CEWS. Some of these proposed measures can be found in the May 15, 2020 backgrounder entitled Extending eligibility for the Canada Emergency Wage Subsidy.

How Employers Would Benefit From the Redesigned CEWS

Example: Hard hit employer eligible for an 85-per-cent combined subsidy rate

Joanne and Hal run a sporting goods store in Fredericton, New Brunswick. They have 10 full‑time employees, each earning $800 per week for a total weekly payroll of $8,000. Joanne and Hal closed their store on March 15, and reopened for curbside pick-up May 1. With the help of the CEWS, they have kept half of their employees on the payroll, paying them their full regular wages. Over the first 16 weeks of the CEWS, they benefitted from the 75-per-cent wage subsidy and they received $48,000 in CEWS support. In July, with the economy reopening, they intend to rehire all of their employees and have them return to their pre-crisis schedule. As revenues were down over 50 per cent year-over-year in June, they would qualify for the maximum base CEWS rate of 60 per cent in Period 5. In addition, because their revenues from April to June 2020 were down over 70 per cent when compared to April to June 2019, they would be eligible for the 25-per-cent CEWS top-up, increasing their combined subsidy rate to 85 per cent. This would translate into $27,200 in CEWS support in Period 5, to help them pay their employees’ salaries.

Example: Employer that becomes eligible for the CEWS as a result of the removal of the 30-per-cent revenue decline threshold

Shelf Life Foods is a mid-size frozen food manufacturer in Kingston, Ontario. It has 200 full‑time employees, each earning $1,000 per week for a total monthly payroll of $800,000. Most of its pre-crisis sales were to supermarkets and have kept steady since the crisis began but the drop in its sales to restaurants during the crisis have contributed to reducing its overall revenues by 15 per cent each month. Because the revenue drop the company experienced was less than the 30-per-cent threshold over the first 16 weeks of the CEWS, the company did not qualify for the CEWS. Deciding that it could not operate at a loss much longer, the company was preparing to reduce staff hours by 15 per cent, or $120,000 per month. With the new design of the CEWS, however, the company, with a 15 per cent revenue drop, would qualify for the base CEWS in Period 5, starting on July 5, 2020, and Period 6, starting on August 2, 2020. In Periods 5 and 6, it would receive a subsidy of 18 per cent of its wages, equivalent to $144,000 for each period. Because it would qualify for the CEWS, the company decides it would not have to reduce staff hours.

Example: Employer who becomes eligible for the CEWS as a result of extension to users of payroll services

Maude runs a non-profit organization in Vancouver, providing services to youth in her community. In addition to volunteers, she hires part-time students to help organize these services. Her revenues dropped significantly because of the overall economic decline but, because she makes use of a centralized payroll service available to such non-profit organizations in her province and did not obtain her own payroll program account with the CRA, she could not qualify for the CEWS. Now, with the change of rules regarding the use of payroll service providers, her organization would qualify for the CEWS and be able to claim benefits retroactive to March 15, 2020.

Example: Recovering employer that is assured of continued support from future CEWS benefits

Maya and her brother Petr run a linen cleaning services business north of Montreal. Their cleaning services for hotels and inns have been shut down temporarily, but they managed to keep most of their other commercial linen cleaning services active. Throughout the crisis, they have been able to maintain 10 full-time employees, each being paid $800 per week for a total weekly payroll of $8,000. Over the preceding three months, revenues were down 50 per cent compared to the same period last year. During Periods 1 through 4, they qualified for the maximum subsidy rate of 75 per cent. Customers are gradually returning and they are considering seeking new lines of business. In June, their revenues are down 35 per cent. This means that, under the new CEWS rules, they would qualify for a base CEWS rate of 42 per cent in Period 5. However, with the safe harbour rule, they would be eligible for a rate of 75 per cent in Period 5—the rate they would have qualified for under the original CEWS rules. This would provide Maya and Petr a total subsidy amount of $24,000 in Period 5. In July, they have secured a new client, and revenues in July and August would be down 25 per cent from last year. With the elimination of the 30-per-cent revenue test, they would now be eligible for a CEWS rate of 30 per cent in Period 6. The extension and expansion of the CEWS would provide them with additional financial support as they rebuild their business.