Archived - Exploring Border Carbon Adjustments for Canada

Combatting climate change is a global imperative, and Canada is doing its part by committing to ambitious climate targets and raising its price on carbon to meet those targets. As Canada and other countries move to meet their international climate commitments, it is inevitable that there will be variations across countries, both in terms of approach and speed of implementation. A key emerging challenge is how to address these disparities in a coordinated way, to achieve results in lowering GHG emissions while mitigating pressures on international trade without inadvertently undermining Canada's global competitiveness. One mechanism to help achieve this would be the establishment of border carbon adjustments (BCAs). The Government of Canada is looking to engage with Canadians and with international partners to advance a global dialogue on this important issue.

Introduction

The objective of the United Nations Framework Convention on Climate Change (UNFCCC) is to stabilize greenhouse gas emissions "at a level that would prevent dangerous anthropogenic (human induced) interference with the climate system". The Paris Agreement aims to limit global warming to well below two degrees Celsius and to pursue efforts to limit the increase to 1.5 degrees Celsius, compared to pre-industrial levels. To contribute to this goal, countries around the world are taking climate action, including through commitments to reach carbon neutrality by 2050.

Under the Paris Agreement, countries are required to put forward increasingly ambitious climate targets (known as nationally determined contributions) every five years. Responding to the scientific evidence on the need for more ambitious climate action, this year, all countries are called upon to increase their carbon reduction targets through updated nationally determined contributions. This is why, on April 22, 2021, Prime Minister Trudeau announced Canada’s updated target of a 40-45% reduction below 2005 levels by 2030. Canada formally submitted this new nationally determined contribution to the United Nations on July 12, 2021. To support the achievement of Canada’s 2030 target, and to put the country on a path to net-zero emissions by 2050, in December 2020, the Government of Canada released A Healthy Environment and a Healthy Economy, Canada’s strengthened climate plan.

This strengthened climate change plan follows up on the 2016 Pan-Canadian Framework on Clean Growth and Climate Change, Canada’s first-ever national plan to cut greenhouse gas emissions where the federal government, together with provinces and territories, set a plan that supports clean technologies and helps adapt to the changing climate. That plan included pricing carbon pollution as a foundational pillar, with a carbon price reaching $50/tonne in 2022. Carbon pricing continues to play a central role in Canada’s strengthened climate change plan. In July 2021, the Government confirmed that Canada’s carbon price will continue to increase by $15 per year after 2022, until it reaches $170/tonne in 2030, as previously announced, in Canada’s Climate Actions for A Healthy Environment and a Healthy Economy. Our expectation is for all countries to put forward effective and ambitious plans and to report on progress to meet their commitments under the Paris Agreement. In addition to the investment of $15 billion announced in Canada’s strengthened climate plan, Budget 2021 committed $17.6 billion towards a green recovery to create jobs, build a clean economy, and fight climate change. This includes government support for home energy retrofits, new tax measures to accelerate carbon capture, utilization and storage and a major commitment to invest in decarbonisation among large emitters.

As Canada and other countries move to meet their international climate commitments, it is inevitable that there will be variations across countries, both in terms of approach and speed of implementation. There are different ways countries can take action and we need to think about how we bring those approaches together. The Government is committed to ensuring that Canada’s transition to a low-carbon economy is achieved in a way that is fair and predictable for Canadian firms and consumers, and that supports Canada’s international competitiveness. In the fall of 2020, the Government of Canada announced its intention to explore the potential of Border Carbon Adjustments (BCAs) as part of Canada’s transition to a low-carbon economy. The Government indicated, first in the 2020 Fall Economic Statement, and more recently in Budget 2021, that it would work with like-minded countries to consider how this approach could fit into a broader strategy to meet climate targets in a manner consistent with maintaining our competitiveness in a fair and open trading system. Budget 2021 also announced the Government’s intention to engage in consultations on BCAs.

This is not an issue Canada can address alone. It will be important to pursue discussions with countries with ambitious climate policies, especially with key trading partners, as they confront the same challenges. The European Union has recently taken an important step forward on BCAs by releasing a legislative proposal for a Carbon Border Adjustment Mechanism. Furthermore, recognizing the close economic relationship between Canada and the U.S., in February 2021, the Prime Minister and the U.S. President agreed to a Roadmap for a Renewed Canada-U.S. Partnership in which both countries committed to work together to address impacts on trade from global disparities in climate policies.

To support work on this issue, the Government wants to hear from Canadians and work with international partners who are also addressing the challenge of climate change.

This paper frames BCAs in a Canadian and international context with a view to establishing a common understanding of what BCAs are and how they work. It introduces the different types of BCAs, the goals they aim to achieve and considers BCAs from three main perspectives:

- Environmental outcomes – how adding BCAs to Canada’s climate policy toolbox could build on Canada’s existing climate change policies to deliver equivalent or better environmental outcomes.

- Economic pressures – what economic impacts BCAs may have, and the distribution of those impacts across sectors and regions, including for consumers.

- International engagement and trade relations – as a trade-dependent economy, how BCAs might affect Canada’s trading relationships and areas where further work is required for cooperation on BCAs with trading partners.

This paper takes another step forward on much needed thinking on how to coordinate our approaches with our international partners on climate change policies and ensuring our shared prosperity.

1. Overview of BCAs and their Objectives

While no national jurisdiction has implemented BCAs to date, they have been the subject of analysis for many years. As such, there is a body of literature exploring the objectives of such measures, their potential forms, their potential effects, and some of the complexities of their design.

What are BCAs intended to do?

BCAs account for differing carbon costs incurred in producing goods across jurisdictions that are subsequently traded internationally. BCAs have four main inter-related objectives:

- Reducing the risk of carbon leakage: Carbon leakage can occur when:

- A company or industry faces carbon costs due to carbon pricing or other climate policies (e.g., regulations to reduce emissions or a requirement to purchase emission allowances); and

- That company or industry cannot fully reflect carbon costs in its prices, due to trade exposure (i.e., competition with companies in other countries) and the competitive dynamics in the market.

- Maintaining the competitiveness of domestic industries: Domestic companies incurring carbon costs may compete with foreign businesses that do not face equivalent carbon costs. BCAs can help ensure that imported goods face the same carbon costs as domestically produced goods. BCAs can also ensure that domestic goods face similar carbon costs to foreign goods in export markets by rebating carbon costs where applicable.

- Supporting greater domestic climate ambition: By leveling the playing field between imported and domestic goods, BCAs can increase the effectiveness and ambition of domestic policies, in order to achieve deeper GHG emission reductions on the road to net-zero.

- Driving international climate action: BCAs can nudge other countries to implement stronger domestic climate policies to avoid subjecting their exported goods to the cost of a BCA and to maintain market access.

Carbon leakage is the effect of carbon costs that cause companies or investors to move production to jurisdictions with lower costs. The result is that emissions are not reduced; they are just emitted in a different location. As such, carbon leakage can undermine the goals of carbon pricing from an environmental standpoint.

How would BCAs be applied in practice?

BCAs could generally take the following forms:

- Import charges applied to goods from countries that either do not have carbon pricing or apply a lower carbon price to ensure that they face similar carbon costs (such as per unit of emission resulting from the production of a good) to those that apply to domestic producers.

- Other measures that can apply a carbon price to imported goods could include a domestic tax or charge levied on both high-carbon domestic and imported products or a requirement that emission allowances be purchased for imported goods based on their carbon intensity.

- Export rebates can be provided to producers so that domestically produced goods compete on equal footing in foreign markets, alongside goods from countries with limited or no carbon pricing.

How are carbon leakage and any resulting competitiveness pressures addressed now?

Under Canada’s current carbon pricing systems, carbon leakage risks are mitigated through the design of these domestic pricing systems. Industries most at risk (i.e., those that are emissions-intensive and trade-exposed (EITE) – see Annex 3) are subject to carbon pricing but generally do not face full pricing of emissions. Different pricing systems accomplish this in different ways. For example, the federal system uses a performance-based approach, as described in Annexes 1 and 2. Canada’s carbon pricing systems in general mitigate the carbon costs faced by EITE sectors while maintaining an incentive for these industries to decarbonise their production.

In addition, the Government provides financial support for investments in technologies to reduce emissions, which can improve the environmental performance of EITE sectors, and provides broader support for industrial innovation to help improve competitiveness.

The interim report for the review of the Pan-Canadian Approach to Pricing Carbon Pollution with respect to carbon leakage and competitiveness found that the tools and policies used to date in existing carbon pricing systems appear to have successfully addressed these risks. However, as the carbon price rises to $170 per tonne by 2030 additional measures may be needed. Moreover, if there are disparities between Canada’s climate actions and those of key trading partners, it will be important to ensure that a coordinating mechanism is in place to avoid undermining Canada’s international competitiveness.

How can BCAs contribute to addressing potential carbon leakage and competitiveness pressures?

As nations, including Canada, intensify the fight against climate change, they need to consider the best mix of policies and tools to achieve GHG emissions reductions while mitigating carbon leakage risks. BCAs could provide a useful tool that could either be an additional or an alternative option to existing approaches for mitigating carbon leakage.

When compared to other ways of addressing carbon leakage, BCAs have two key distinctions:

- Broader sharing of carbon costs: Current domestic carbon leakage mitigation measures are focused on reducing costs for production subject to carbon pricing, or by providing assistance for investments to reduce emissions. In contrast, BCAs are focused on ensuring domestic and imported goods reflect a comparable carbon cost.

- International implications: Current measures apply strictly to domestic production while BCAs apply carbon pricing to imported goods (and potentially rebate such pricing on exported goods), thereby potentially affecting the economic interests of trading partners.

By levelling the playing field between domestic and imported goods, BCAs can help address the risk of carbon leakage by eliminating the incentive of relocating production in another jurisdiction based on differences in carbon prices.

Importantly, BCAs can complement other domestic measures to reduce GHG emissions, and would need to be aligned and integrated within Canada’s domestic climate change framework, which involves federal and different provincial and territorial systems (see Annex 1). As currently implemented, this could prove to be quite complex, given differences between pricing systems in Canada. However, the federal government is in the process of strengthening the standards for provincial and territorial pricing systems, known as the federal benchmark, to ensure greater consistency and comparability across systems.

Internationally, moving forward with BCAs needs to be considered in the context of international trade and environmental frameworks, including Canada’s international legal obligations, and taking into account both GHG emission reductions and carbon leakage mitigation approaches of key trading partners. Given the importance of international cooperation on climate change, BCAs should be coordinated among partners with comparable levels of ambition on GHG reduction measures.

2. International Context and Collaboration

Internationally, there are emerging discussions on approaches to price carbon pollution and minimum carbon pricing levels to advance solutions that can deliver global emission reductions, notably from high-emitting countries and industries.

Against this backdrop, there is also an increasing focus on BCAs, particularly among countries that are taking meaningful steps to curb their GHG emissions. International organizations have also begun to consider BCAs, among other potential tools, to assess how countries could move forward to address carbon leakage in a coordinated way, without creating tensions that could undermine the multilateral trading system.

The growing international collaboration in coordinating approaches on BCAs should cover a number of key issues including:

- Scope: The risks of carbon leakage do not always affect the same industries in every country the same way. This is why the scope of existing carbon pricing systems – and the measures that currently provide relief from carbon leakage risks – can differ among jurisdictions. Another variance can be the type of GHG emissions (direct or indirect) to which carbon pricing applies. Hence coordination discussions are required to inform decisions as to the industries and types of emissions to which border carbon adjustments would apply.

- Equivalency between pricing systems and non-pricing measures: Not all countries implement explicit pricing. A key challenge to ensure that the international trading system supports BCAs is to consider whether and how non-pricing regulatory instruments can be compared to explicit pricing measures.Footnote 1

- Determining embedded emissions in goods: International coordination is necessary to establish a baseline for reliable data and methodologies to account for embedded emissions in traded products subject to BCAs.

Engaging in discussions on BCAs also brings into consideration the need for their institutional support, including from existing international trade and climate change frameworks.

The European Union is the most advanced in its work. In December 2019, the EU released the European Green Deal that outlined plans to achieve carbon neutrality. The European Green Deal directed the European Commission to propose a carbon border adjustment mechanism (CBAM), for selected sectors, to reduce the risk of carbon leakage by putting a carbon price on imports of certain goods from outside the EU. The European Commission released its CBAM legislative proposal on July 14, 2021. The CBAM proposes to establish a BCA as an extension of the EU’s Emissions Trading System (ETS), and the phase-in of the EU’s CBAM is expected to be coordinated with the phasing-out of the current free allocation of allowances to address the risk of carbon leakage because of carbon pricing in the EU’s ETS.

The EU’s CBAM initiative is part of a broader review of the EU’s climate-related policy instruments, including a proposed reform and expansion of its ETS, EU Member State targets to reduce emissions in sectors outside the ETS, and the regulation on land use, land use change and forestry. Canada and other countries have signalled their interest in CBAM.

Canada and the European Union both recognize the role of carbon pricing as a powerful and efficient way to fight climate change, and have put forward strengthened approaches to pricing carbon while addressing the risk of carbon leakage in our respective climate plans. Both also have committed to work together on carbon pricing and WTO-compatible BCAs in the context of the Canada-European Union Summit in June 2021.

The U.S., which rejoined the Paris Agreement this year, has set out a new direction for U.S. policy on climate change. Among other actions, the Biden Administration has restated its commitment to holding polluters accountable for their actions in the context of the Canada-U.S. Roadmap that was jointly agreed with Canada’s Prime Minister in February 2021. The Roadmap for a Renewed Canada-U.S. Partnership commits both countries to work together to address impacts on trade from global disparities in climate policies.

3. Considerations in Assessing the Role of BCAs for Canada

As the Government of Canada explores the role of BCAs, important considerations fall into three main categories: environmental, economic, and international trade. There are also important issues around design and administration of BCAs that are discussed below.

Environmental considerations

Addressing carbon leakage with BCAs has the potential to support robust climate change policies both in Canada and abroad by ensuring goods imported from other jurisdictions face the same carbon costs (such as per unit of emission) as domestic production at risk of carbon leakage. This gives rise to the following questions:

- Can BCAs enable domestic climate policies that will better support carbon emission reductions (including incentives for technological innovations) in Canada than existing carbon leakage mitigation measures?

- Would the costs that could result from BCAs create new carbon leakage risks for downstream sectors?

- Could Canadian BCAs create incentives for other jurisdictions to adopt more ambitious climate policies and contribute to global GHG reduction efforts?

Economic considerations

Ensuring that BCAs are the best policy to address their objectives requires assessing their overall economic impacts. BCAs, whether they complement or replace existing measures to mitigate carbon leakage, could result in an increase in costs of goods in Canada covered by the BCAs. This is because applying an import charge on foreign goods would increase the ability for domestic producers to pass through carbon costs on domestically produced goods (i.e., by allowing producers to raise their prices while remaining competitive). These increased costs could mean downstream impacts for other manufacturers and potentially consumers. This raises a number of questions:

- Would BCAs be more effective than existing carbon leakage mitigation measures to improve competitiveness for Canadian producers?

- Would BCAs create competitive pressure issues for downstream sectors?

- What impacts would there be on Canadian consumers?

International Trade considerations

As measures affecting traded products, BCAs would be subject to Canada’s international trade law obligations (e.g., under the World Trade Organization agreements and Canada’s free trade agreements). As a trade-dependent economy, Canada must consider how BCAs would affect trading relationships and the multilateral trading system more broadly. Canada must move forward in collaboration with key trading partners, as well as those taking on ambitious climate action, to ensure the continued benefits of free and open trade between partners with ambitious climate regimes.

In considering our international engagement with Canada’s trading partners, the following questions arise:

- Are there opportunities for Canada to align with other countries exploring BCAs?

- What are the risks to Canada’s trade relations in adopting BCAs?

- How can BCAs be designed to align with Canada’s international trade law obligations?

- Should BCAs provide an exemption (or other flexibility) for imports from certain developing countries or countries that are also taking ambitious measures to reduce their GHG emissions?

Scope, design, and administration considerations

The design of BCAs would be informed by the environmental, economic, and international trade considerations noted above, as well as by the main objectives driving the policy.

With respect to scope, the questions that arise include:

- Emissions scope – which emissions should be subject to a BCA (e.g., only direct emissions resulting from production, or also indirect emissions)?

- Product scope – which products should be subject to BCAs?

- Trade scope – should BCAs be applicable to imports only or combined with an export rebate?

- Country coverage – should any foreign countries be excluded from the application of BCAs? If so, on what basis?

If BCAs are set with a view to leveling the playing field and ensuring goods from other jurisdictions face

the same carbon costs per unit of emission as domestic production at risk of carbon leakage, setting the right level of BCAs would require a domestic reference cost. As well, there would be a need to determine if imports are subject to comparable costs in the country of export. This gives rise to several questions:

- How should carbon costs be established for imported goods?

- To what extent should there be flexibility to apply different rates to different countries, regions within those countries, or individual sectors or facilities?

- How should other countries’ climate measures, including non-pricing measures, be accounted for?

In addition to the above, any eventual implementation of BCAs would give rise to additional questions:

- How would BCAs be administered and enforced? What reporting and verification requirements would need to be put in place?

- What adjustments, if any, could be needed to federal and provincial/territorial climate change plans?

The above questions give a sense of the complexity of this issue, and the trade-offs that would need to be considered – both between existing policies and BCAs, and between certain elements within BCAs.

Conclusion

As countries implement more ambitious measures to meet their commitments under the Paris Agreement, it is inevitable that countries may move at a different pace depending on their domestic contexts. In doing its share to tackle the global challenge of climate change, Canada has adopted a range of climate policies, including a flexible yet effective approach to carbon pricing, with a clear trajectory for price increases over the next few years. While working towards its goals to reduce Canada’s GHG emissions, the Government is committed to ensuring that Canada’s transition to a low-carbon economy is achieved in a way that is fair and predictable for our businesses, and supports Canada’s international competitiveness. This is why the Government is exploring BCAs as a tool to address potential carbon leakage and any resulting competitiveness issues.

The potential role of BCAs, however, hinges on a number of considerations, as outlined earlier in this paper. This is why the Government intends to continue its discussions with Canadians and international partners over the coming months on this issue.

Finally, whether BCAs are necessary to mitigate carbon leakage risks ultimately depends on the level of ambition and effectiveness of other countries’ GHG emission curbing actions. There are different ways countries can take action and we need to think about how we bring those approaches together. This is why the Government wants to engage with key trading partners and other like-minded countries who are taking climate action to better understand their perspectives and plans for BCAs or alternative measures and ensure there as much coherence and coordination as possible among different policies and approaches.

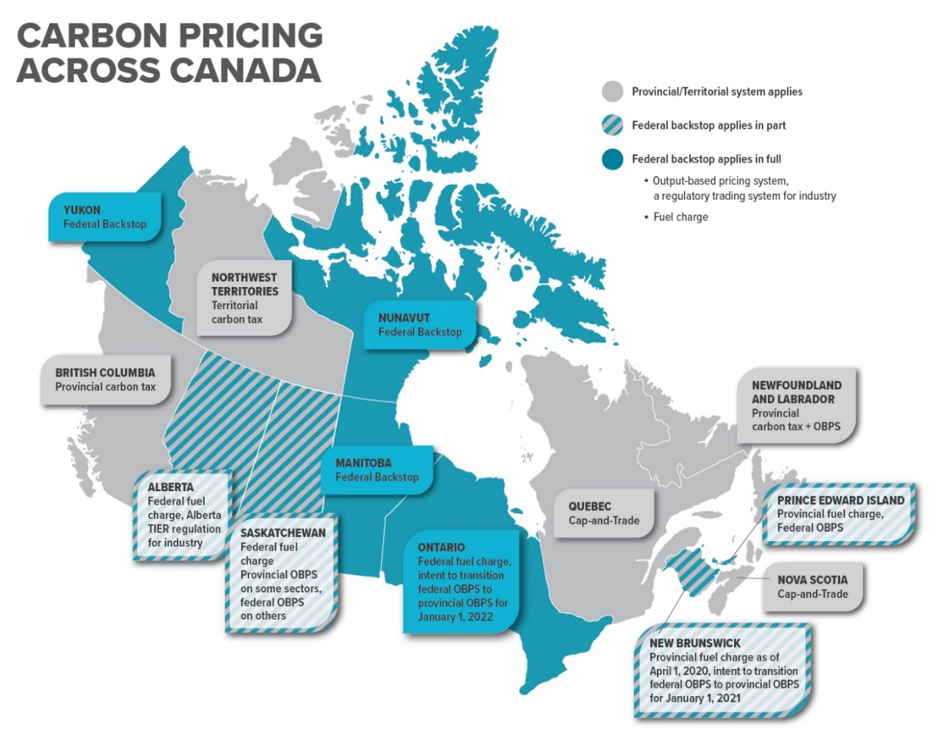

Annex 1

Carbon Pricing Across Canada

Annex 2: Carbon Pricing for EITE Sectors

In certain provinces, EITE sectors are subject to a federal or provincial output-based pricing system (OBPS). In other provinces, a cap-and-trade system applies to EITE sectors, or a carbon tax applies to both EITE and non-EITE sectors. OBPS and cap and trade systems are described below.

OBPS

Under the OBPS, industrial facilities in EITE sectors pay a carbon price on the portion of their emissions that exceed their GHG emissions limit. The limit is determined by the output-based standards applicable to the activities carried out at the facilities and the level of production. A facility that produces more emissions than its emissions limit has to compensate for its excess emissions (e.g., by paying the carbon price). Facilities whose emissions are below their emissions limit are rewarded by obtaining credits they can sell or save to use later.

Under the federal OBPS, output-based standards are established as a percentage of a sector’s historical level of emissions intensity (i.e., its emissions per unit of production). Different stringency levels (ranging from 80% to 95% of historical emissions intensity) are set depending on each sector’s competitiveness and carbon leakage risks.

With this approach, a facility’s carbon costs are reduced, while the incentive to reduce emissions from the carbon price is maintained.

Cap-and-Trade

Under cap-and-trade systems, facilities have to surrender emission allowances to cover their emissions, and there is a fixed number of emission allowances available in the market. To limit costs for facilities in EITE sectors, a portion of these allowances are provided for free. Facilities that generate more emissions than their free allocation of allowances have to purchase additional allowances, while facilities with lower emissions can sell their excess allowances.

To find out more about Canada’s carbon pricing systems, please visit this website.

Annex 3: Overview of Canada' Emissions-Intensive and Trade Exposed Sectors

BCAs would be most relevant to the products made by emissions-intensive and trade exposed (EITE) sectors, as they are the most at risk of carbon leakage. This annex provides an overview of the sectors that have been identified as being at risk of carbon leakage and competitiveness impacts under the federal Output-Based Pricing System (OBPS) in Canada, to inform thinking on the questions outlined in the considerations section, above.

What are EITE sectors?

EITE sectors are those that undertake emissions-intensive activities and are highly trade-exposed. Emissions intensity refers to the amount of GHG emissions released per unit of production. Trade exposure refers to the extent to which Canadian producers compete with foreign producers, either in Canada or internationally, which affects their ability to pass on carbon costs to customers in domestic or foreign markets. Whether a sector is considered to be an EITE sector varies across jurisdictions. In Canada, the federal OBPS considers a sector to be at significant competitiveness and carbon leakage risk from carbon pollution pricing and therefore eligible to participate in the federal OBPS if it:

- has at least one facility that emits 50 kilotonnes of CO2 equivalent or more;

- is more than 80% trade exposed; or

- is in a medium or high EITE risk category, where emission intensity and trade exposure both exceed certain thresholds.

This paper uses that definition though a BCA could have different coverage. The analysis below is for illustrative purposes only and does not pre-judge any future considerations on the exact coverage of potential BCAs in Canada.

EITE sectors in Canada

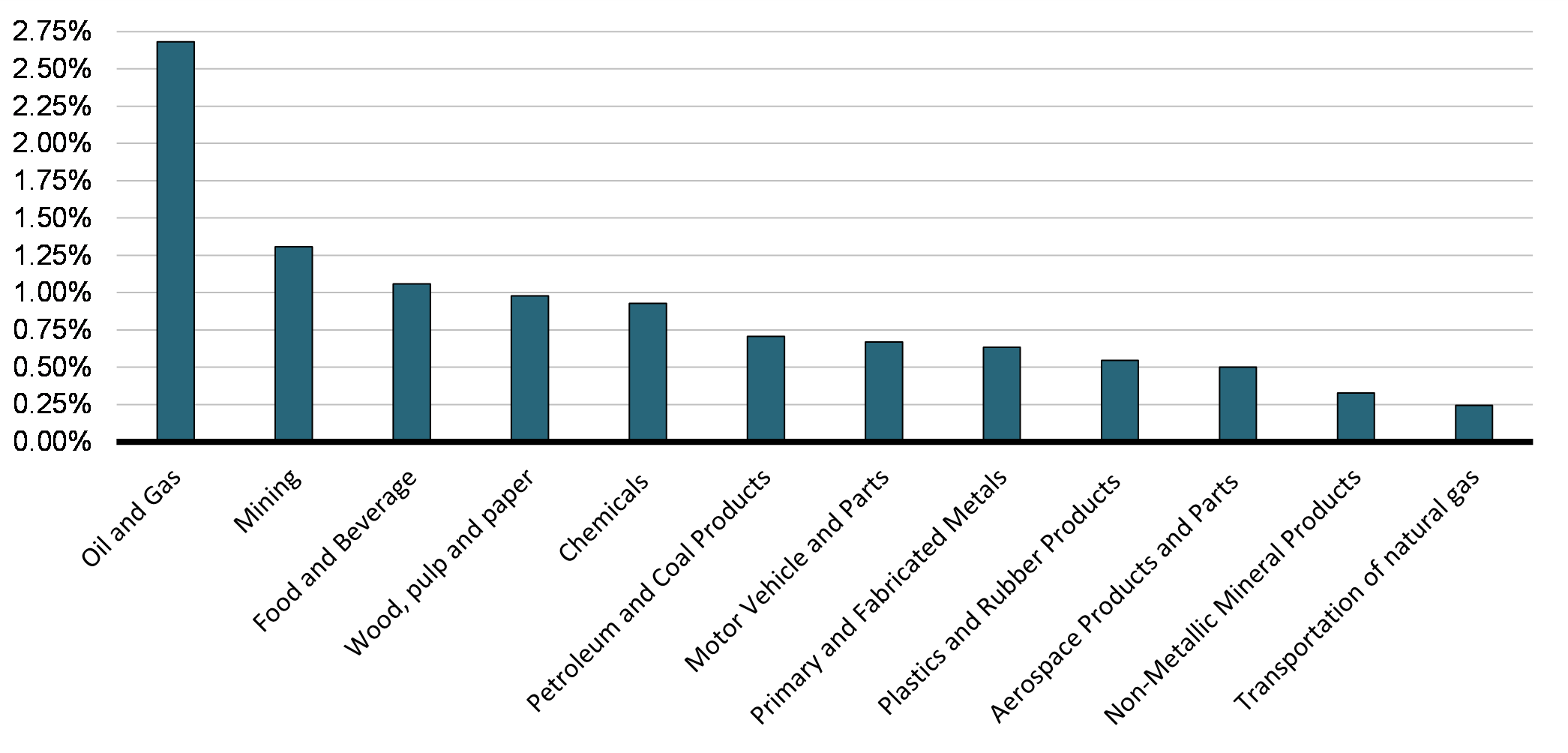

Overall, production by the EITE sectors contribute from 9.2% to 10.6% to Canada’s economy when measured by their gross value-added as a share of total GDP. Graph 1 shows each EITE sector’s contribution to GDP.

Gross-Value Added by Sector as a % of GDP

While EITE sectors are located across Canada, they are heavily concentrated in Ontario, Alberta and Quebec. Table 1 provides the output of EITE sectors by province/territory, and the proportion of output of EITE sectors in a province/territory out of total output for that province/territory.

| Province/Territory | Share of Total Output of EITE Sectors by Province/Territory | Output of EITE Sectors as a % of Total Output in a Province/Territory |

|---|---|---|

| Ontario | 38.2% | 16.3% |

| Alberta | 22.2% | 23.4% |

| Quebec | 18.5% | 16.3% |

| British Columbia | 7.8% | 10.9% |

| Saskatchewan | 5.2% | 23.0% |

| New Brunswick | 2.5% | 22.9% |

| Manitoba | 2.3% | 12.3% |

| Newfoundland and Labrador | 1.9% | 21.3% |

| Nova Scotia | 0.8% | 7.5% |

| Northwest Territories | 0.3% | 19.6% |

| Prince Edward Island | 0.2% | 11.1% |

| Nunavut | 0.1% | 15.7% |

| Yukon | 0.1% | 8.1% |

| Source: Statistics Canada Supply Use Tables (Supply Tab), Total supply at basic prices for EITE sectors in a given province/territory divided by total supply at basic prices of all EITE industries and Total supply at basic prices for EITE sectors in a given province/territory divided by total supply at basic prices in that province/territory; 2015-2017 annual average. | ||

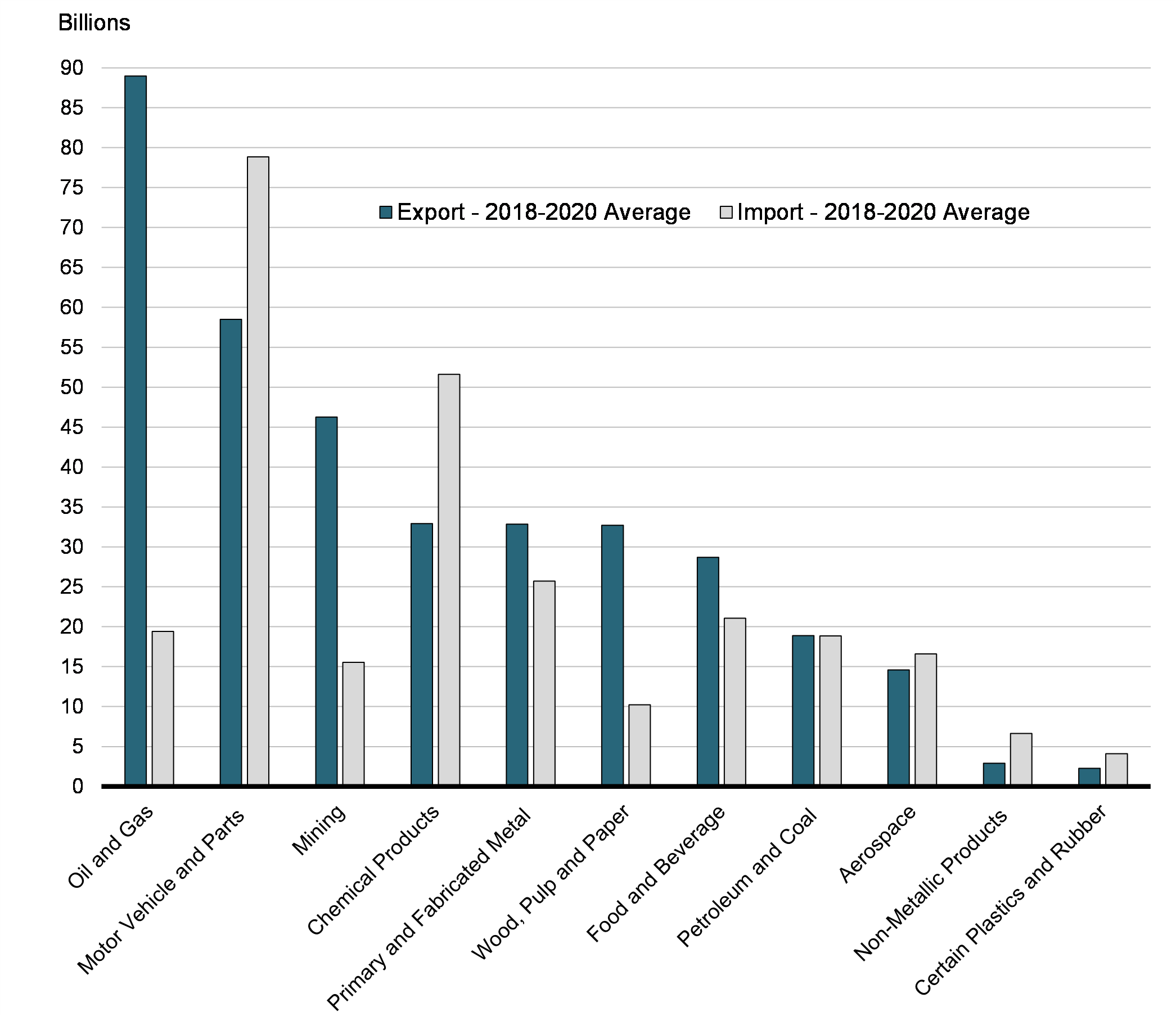

Trade profile of EITE sectors

Canada’s economy is highly-trade dependent, but EITE sectors, by definition, are those where imports or exports make up an even higher share of each sector’s market. Canadian production from EITE sectors faces relatively more competitiveness pressure from an export perspective than an import perspective.

- 69.1% of total Canadian exports of merchandise are of products from EITE sectors, amounting to $360 billion annually.

- 46.3% of total Canadian imports of merchandise are of products that compete with EITE production in Canada, amounting to $269 billion annually.

Graph 2 provides export and import data by EITE sector.

Exports and Imports by EITE Sector

Trade with three like-minded partners – the U.S., the EU and the U.K. – covers the vast majority of Canada’s trade from EITE sectors (85% for exports and 71% for imports). Table 2 provides the geographical breakdown for exports and imports, respectively, from EITE sectors.

| Country | Exports - 2018-2020 Average ($ millions) |

% of Total Exports from EITE sectors |

Imports - 2018-2020 Average ($ millions) |

% of Total Imports from EITE sectors |

|---|---|---|---|---|

| United States | 273,640 | 76.1% | 155,608 | 57.9% |

| United Kingdom | 16,216 | 4.5% | 5,492 | 2.0% |

| EU | 15,782 | 4.4% | 30,821 | 11.5% |

| China | 15,567 | 4.3% | 10,686 | 4.0% |

| Japan | 8,383 | 2.3% | 7,896 | 2.9% |

| South Korea | 4,281 | 1.2% | 5,737 | 2.1% |

| Mexico | 3,711 | 1.0% | 13,266 | 4.9% |

| India | 3,223 | 0.9% | 2,421 | 0.9% |

| Other Countries | 18,821 | 5.2% | 36,723 | 13.7% |

| Total EITE Goods | 359,624 | 100.0% | 268,651 | 100% |

| Source: Trade Data Online, Domestic Exports and Total Imports for EITE industries (NAICS codes) by country; 2018-2020 annual average. | ||||

Downstream users of EITE products

The potential effects on downstream users of EITE products is a key difference between BCAs and existing measures to mitigate carbon leakage. The extent of these effects would depend on many factors such as the scope of application of BCAs, whether they replace or complement existing carbon mitigation measures (including revenue recycling and other investment or support programs), the emission-intensity of the inputs that are used in production, and the relative importance of EITE inputs relative to other input costs.

Of note, many downstream users are themselves EITE producers (e.g. petroleum refineries are an EITE producer of gasoline and a downstream user of crude oil).