Archived - Corporate Governance Consultation: Improving Diversity and Facilitating Electronic Communications in Federally Regulated Financial Institutions

Introduction

Canada's federally regulated financial institutions (FRFIs) and their owners (e.g., shareholders, members of credit unions, certain insurance policyholders) are supported by a robust corporate governance framework, which is contained in the Bank Act, the Insurance Companies Act, and the Trust and Loan Companies Act (collectively referred to as the federal financial institutions statutes). As a general approach, the federal financial institutions statutes typically follow the framework set out for federally incorporated companies in the Canada Business Corporations Act (CBCA). This framework is modified as necessary to reflect the unique nature of FRFIs.

The corporate governance framework for FRFIs should take into account the changing social, economic, and technological context in which they operate, to best enable them to respond to today's challenges for the benefit of their owners and clients.

In light of recent developments, including the introduction of diversity disclosure requirements in the CBCA and the digitalization of the financial sector that has been further accelerated by the COVID-19 pandemic, the Government is reviewing certain aspects of the corporate governance framework. In this context, Budget 2021 proposed a public consultation on measures that would:

- adapt and apply the Canada Business Corporations Act diversity requirements for FRFIs; and,

- expand FRFIs' use of electronic communications with their owners, including the delivery and provision of governance documents, as well as virtual meetings.

The Department is seeking comments on the questions outlined in this consultation paper, and encourages stakeholders to provide any data and information that could support their submissions.

The Department recognizes that, in certain circumstances, the impacts of changes to corporate governance requirements may differ depending on the composition of a financial institution's ownership. To this end, the Department encourages the views of non-distributing financial institutions (including but not limited to federally regulated credit unions, certain insurance companies, and small- and medium-sized banks) and their owners, where applicable.

The Department is accepting written comments from interested stakeholders until September 23rd, 2022. Send us your comments at governanceconsultation-consultationgouvernance@fin.gc.ca with "Corporate Governance Consultation" as the subject line.

Should you wish to submit comments by mail, please direct your submission to the attention of the Financial Sector Policy Branch.

Manuel Dussault, Acting Director General

Financial Institutions Division

Financial Sector Policy Branch

Department of Finance Canada

James Michael Flaherty Building

90 Elgin Street Ottawa ON K1A 0G5

I. Adapting and Applying the Canada Business Corporations Act Diversity Disclosure Requirements

To foster diversity at the highest levels of corporate leadership in Canada, the Canada Business Corporations Act was recently amended to introduce diversity disclosure requirements. These amendmentsrequire federally incorporated distributing companies,Footnote 1 including venture issuers,Footnote 2 to report to shareholders and Corporations Canada annually on the representation of women, visible minorities,Footnote 3 Indigenous peoples, and people with disabilities on their boards and in senior management. This "comply or explain" model builds on similar rules in most provincial securities legislation that require provincially regulated reporting issuersFootnote 4 to report on gender diversity on boards and in executive officer positions. To build on this progress, the Government is consulting on measures that would adapt and apply the CBCA's "comply or explain" diversity disclosure requirements to financial institutions.

One of Canada's greatest resources is its people, however, women, racialized persons, Indigenous peoples, and people living with disabilities are underrepresented in positions of economic influence and leadership, including on corporate boards and in senior management.Footnote 5 To address these challenges, the Government has introduced a number of initiatives, including the Black Entrepreneurship Program, a partnership between the Government and the private sector to invest in Black-led Canadian businesses, and the 50-30 Challenge. The Challenge is an initiative co-created by the Government of Canada, civil society, and the private sector that aims to attain gender parity and significant representation (at least 30%) of under-represented groups on boards and senior management positions. Footnote 6 In May 2021, the Government announced the launch of the Sustainable Finance Action Council, a financial industry action group. The Council will prioritize work on gender and diversity reporting.

At the provincial level, the Canadian Securities Administrators (CSA), an umbrella organization of Canada's provincial and territorial securities regulators, is undertaking consultations on broader diversity in corporate leadership. They are consulting on issues including expanding the scope of disclosure beyond gender, and the use of targets and term limits for improving diversity on boards and in executive suites. These engagements follow the recommendations made by the independent Ontario Capital Markets Modernization Taskforce to enhance diversity reporting requirements for reporting issuers.

Studies have demonstrated that diversity and inclusion in corporate governance are important drivers of new ideas and innovation, organizational performance, and growth.Footnote 7 A 2020 study by McKinsey & Company found that companies with diverse leadership financially outperform corporations with less diverse boards, associating boardroom diversity with higher returns.Footnote 8 Diverse boards have also been found to foster a culture of broadened perspectives, diligence, critical engagement, risk awareness,Footnote 9 and may also produce better outcomes for consumers.Footnote 10

The Current Status of Corporate Governance Diversity in Canada

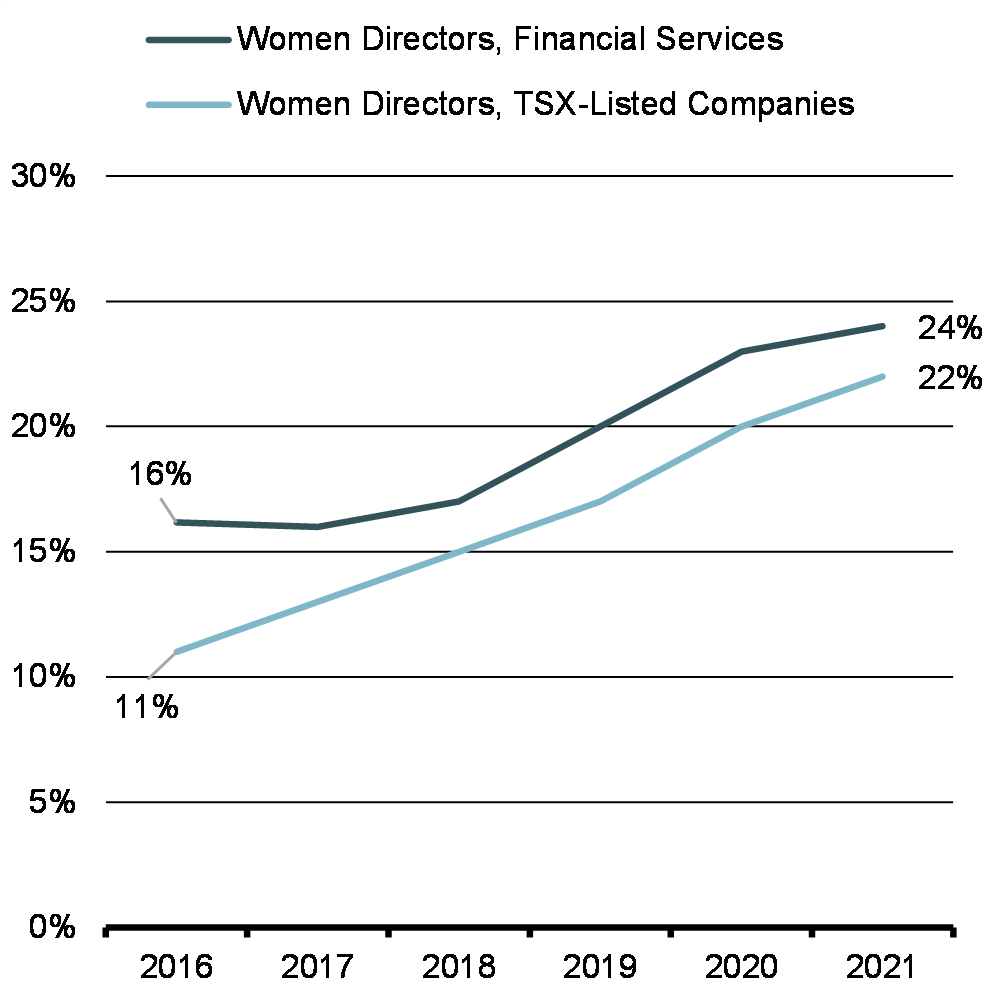

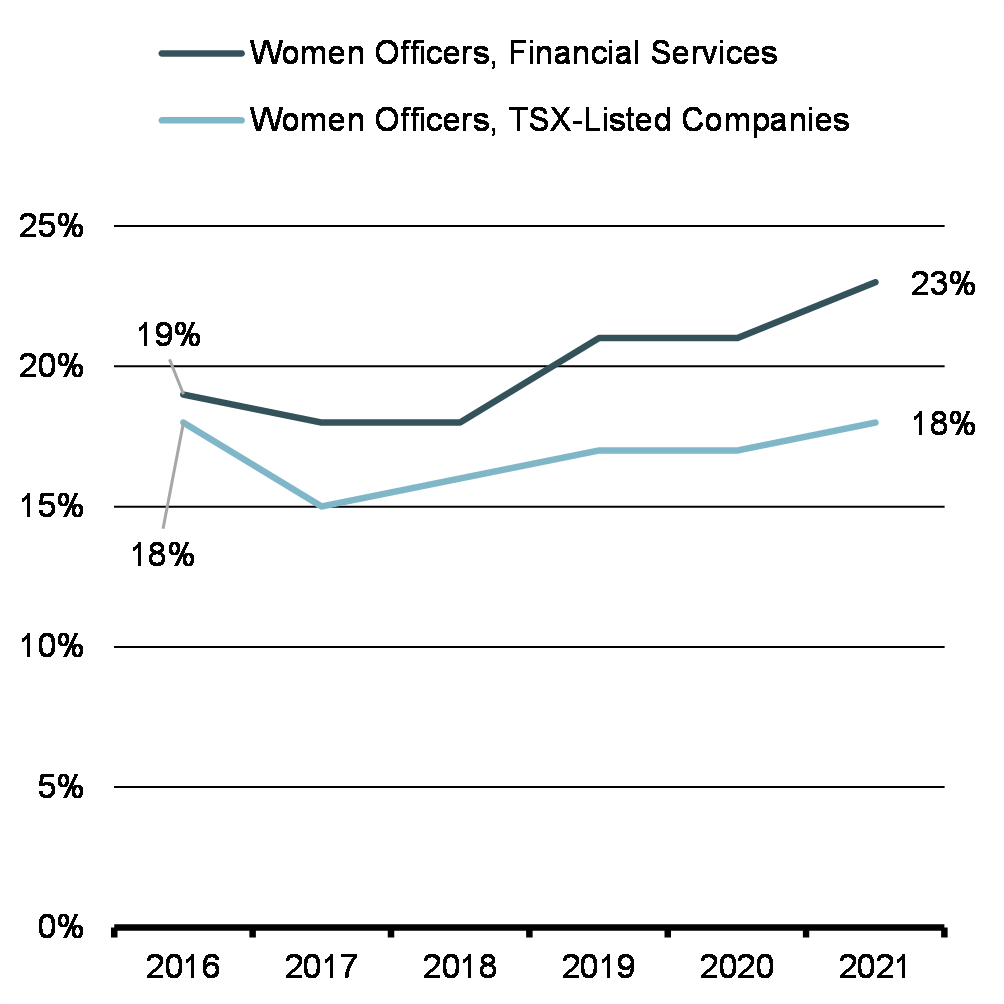

Diversity is fundamental to creating a thriving and successful financial sector that reflects Canadian values and achieves its potential. Based on 2021 disclosures, companies in the financial services sector are higher than the average of all TSX-listed companies when it comes to gender-diverse boards and executive officers. Representation of women on the boards of financial services companies has grown since disclosure rules were first introduced, from 16% in 2016 to 24% in 2021 (Chart 1). The percentage of women executive officers has grown at a slower rate, from 19% in 2016 to 23% in 2021 (Chart 2), reflecting a similar trend among all TSX-listed companies.Footnote 11

Percentage of Women Directors

Percentage of Women Officers

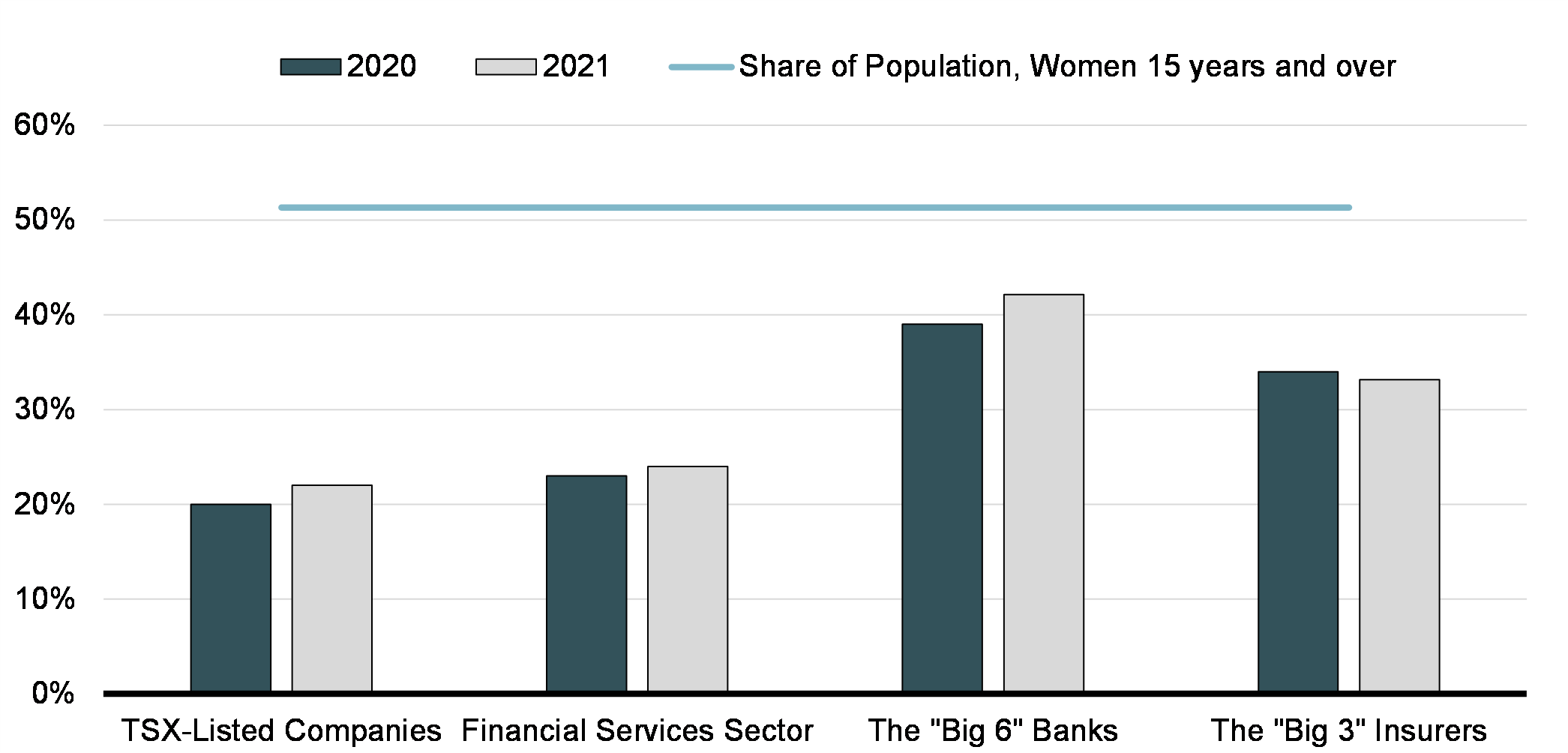

Representation of women on the boards of the six largest Canadian banks and three largest insurance companies is comparable to or higher than the average for the S&P/TSX 60 companies, where women held 33% of director positions in 2021. By comparison, women held 42% and 33% of director positions at the largest banks and insurance companies, respectively, in 2021. This is up slightly from 39% at the six largest banks and similar to 33% at the three largest insurance companies in 2020 (Chart 3).Footnote 12 Of the financial institutions that disclose board representation, all have adopted targets of at least 30% of women on their boards, and have committed to varying goals and initiatives to improve the representation of other groups, like Black, Indigenous, and people of colour. Currently, most small- and medium-sized banks do not provide publicly-available details on gender representation, diversity targets, and policies.

Percentage of Women Directors, Large Banks and Insurance Companies

Representation of other groups, including visible minorities, Indigenous people and people with disabilities, on the corporate boards and in senior management positions of federally incorporated distributing corporations is low. Members of visible minorities held 7% of the board seats and 9% of the officer positions in those companies that disclosed in 2021. Indigenous people and people with disabilities each held only 0.4% of director positions, and representation of these groups in officer positions is similarly low, at 0.4% and 0.7%, respectively. So far, CBCA corporations have almost universally not adopted targets for designated groups other than women.Footnote 13

CBCA Diversity Disclosure Requirements

In January 2020, the CBCA diversity disclosure reporting requirements took effect for federally incorporated distributing companies. These companies are required to report on the representation of women, Indigenous peoples, persons with disabilities, and members of visible minorities on their boards and in senior management. These companies may also disclose information on additional groups they believe contribute to the diversity of their board and senior management team.

CBCA distributing corporations are required to disclose information on the number and percentage of directors and officers from each of the designated groups. They must also disclose their policies and targets for representation, or explain why they do not have a policy and targets. The information disclosed also includes:

- whether the corporation has adopted term limits or other mechanisms of board renewal;

- whether, and, if so, how the board or nominating committee considers diversity on the board in identifying and nominating candidates for election or re-election to the board; and

- Whether, and, if so, how the corporation considers diversity when making senior management appointments.

These requirements are based on provincial diversity disclosure rules that were introduced in most securities legislation in 2015, that are currently limited to reporting on gender representation.

Further information on the CBCA's diversity disclosure amendments and supporting guidelines are accessible through Innovation, Science and Economic Development Canada.

Adapting the CBCA "Comply or Explain" Requirements for FRFIs

The corporate governance framework for FRFIs includes a number of requirements for boards of directors and officers, including residency requirements, risk management oversight, and board independence and composition. A bank's board must have at least seven directors, the majority of whom must be resident Canadians. Given the particular importance of risk management for financial institutions, relevant financial industry and risk management expertise are key competencies for directors.Footnote 14 Other requirements include the independence of the board from senior management and, specifically, the separation of the Chair of the Board and the CEO, and that boards collectively bring a balance of expertise, skills, experience, competencies, and perspectives.

Currently, there are no diversity-specific requirements in the financial sector statutes, and only distributing FRFIsFootnote 15 are required to comply with provincial gender diversity disclosure rules. If provincial diversity disclosure rules are expanded, distributing FRFIs would be subject to these changes.

Consultation Questions

The Government is seeking feedback on measures that would align the financial institutions statutes with the diversity disclosure requirements in the Canada Business Corporations Act.

- What are the potential benefits and limitations of applying the CBCA diversity disclosure model to financial institutions?

- Are the scope and content of the CBCA's disclosure requirements appropriate for financial institutions? Please explain.

- Are the four designated groups outlined in the CBCA model (i.e., Indigenous peoples, members of visible minorities, persons with disabilities, and women) adequate for capturing the information investors and the public require in order to assess the state of diversity on the boards and senior management of financial institutions? If not, how should this be modified?

- For investors and owners of FRFIs, are the CBCA diversity disclosures adequate to inform your investment/voting decisions for directors?

- Should the requirements apply to all federally incorporated financial institutions, or should they be differentiated based on the institution's ownership or type?

- If differentiation is preferred, why?

- In your view, what is the impact of these disclosure requirements on non-distributing FRFIs (i.e., credit unions, small- and medium-sized banks, and certain insurance companies)?

In light of potential modifications to provincial diversity disclosure, we would welcome your views on the following measures, including the use of a prescribed form to ensure data consistency and reliability, targets for directors and executive officers, director term limits, and compliance measures (i.e., penalties for non-compliance and/or benefits for those who comply):

- What are the benefits and limitations of introducing targets to achieve broader diversity goals? Should federally regulated financial institutions be required to set their own targets, or should Government introduce suggested targets or guidance in this area?

- In your view, do director term limits create more opportunities to recruit diverse candidates? What are the potential challenges to achieving this outcome?

- Should federally regulated financial institutions be required to set their own term limits, or should Government prescribe term limits?

- What are the benefits and limitations of introducing a prescribed form for reporting?

- In your view, what are effective approaches and policies to achieve compliance?

- In your view, what are effective approaches and policies to increasing diversity in financial institutions?

II. Expanding Electronic Communications and Engagement with Owners

Digital technology is changing the way Canadians access information, work, and connect with one another. In 2020, ninety-four percent of Canadians had access to the internet and used the Internet to send and receive emails.Footnote 16 The COVID-19 pandemic has only accelerated these trends. Moreover, the Government of Canada's Connectivity Strategy aims to bring high-speed internet access to one hundred percent of people in Canada by 2030.

In this context, the Department of Finance is seeking feedback on the risks, opportunities, and design considerations associated with expanding FRFIs' use of electronic communications with their owners, including the delivery and provision of governance documents and virtual meetings. Footnote 17 The following section outlines the "notice-and-access" electronic communications model in the provincial securities commissions' National Instruments, as well as the "access equals delivery" model currently under consideration. The questions request feedback on the suitability of these models for FRFIs, as well as any regulatory modifications that may be required to better capture the way financial institutions communicate with their owners. The subsequent section includes questions on virtual meetings. We also welcome comments on whether and how these changes may affect the ability of owners to engage in their governance functions, in particular for non-distributing institutions whose owners may not be shareholders (for example, members of federally regulated credit unions, and certain insurance policyholders).

Facilitating the use of electronic communications could yield benefits both for financial institutions and their owners, such as minimizing environmental impacts, decreasing the costs of communication, and increasing owner participation by making information timelier and more accessible. At the same time, the Department acknowledges that some owners may prefer not to engage with financial institutions using electronic means. People who live in rural areas and/or those aged 65 and older are less likely to have internet access than younger urban dwellers in Canada. Seventeen percent of people aged 65 and older did not have access to the internet as of 2020.Footnote 18 In considering potential changes, the Department's objective is to ensure effective and inclusive methods of communication that take into account the unique needs of different types of financial institutions and their owners.

Electronic Delivery and Provision of Governance Documents

The federal financial institutions statutes require FRFIs to send paper copies of governance documents, such as financial statements, management discussion and analysis (MD&A), proxy circulars, and forms of proxy, to their owners unless they have an owner's consent and the information is posted to the System for Electronic Document Access and Retrieval (SEDAR) and/or a website.Footnote 19 In some cases, financial institutions may seek an exemption from the Office of the Superintendent of Financial Institutions to make certain documents accessible to owners through electronic means without first obtaining consent, in accordance with the guidelines in the National Instruments issued by provincial securities commissions.

In 2013, the National Instrument guidelines were amended to give provincially regulated reporting issuers the option to use an electronic-by-default communications model called "notice-and-access" to post governance documents on SEDAR and the issuer's website instead of having to mail materials to shareholders. In 2018, the CBCA was amended to facilitate the use of notice-and-access by federally incorporated distributing corporations.Footnote 20

More recently, in April 2022,Footnote 21 the CSA published proposed amendments that would expand investors' electronic access to documents by implementing an access equals delivery model for certain governance documents. Under this model, reporting issuers effect delivery by alerting owners, via a news release, that a document is available on SEDAR. The proposed amendments do not remove an investor's ability to request documents in paper or electronic form.

Notice-and-Access

Notice-and-access is a model under which reporting issuers may provide financial statements, MD&A, and proxy-related materials to shareholders by electronic means. This model requires that the reporting issuer first send a notice alerting the shareholder that they will be making documents available electronically. By default, the notice must be accompanied by voting documents (i.e., a form of proxy) and must be delivered by mail, unless the shareholder has provided consent to receive these electronically. Reporting issuers can then "send" governance documents by posting them on SEDAR and a non-SEDAR website.

The notice must state that documents have been posted online, and explain how shareholders can access the materials. Reporting issuers must still provide investors with the option of requesting paper copies of documents, and the notice must stipulate how these can be obtained. See Annex 1 for the relevant sections of National Instruments 51-102 (Continuous Disclosure Obligations) and 54-101 (Communication with Beneficial Owners of Securities of a Reporting Issuer).

Access Equals Delivery

Access equals delivery is a model under which, for documents that issuers are required to deliver to investors, providing public electronic access would constitute delivery. Specifically, an issuer is considered to have effected delivery once: (a) the document has been filed on SEDAR; and (b) where applicable, a news release is issued and filed on SEDAR indicating that the document is available electronically and that a paper or an electronic copy can be obtained upon request. The CSA's April 2022 proposed amendments would apply to prospectuses generally, annual financial statements, interim financial reports and related MD&A. At this time, the CSA are not proposing an access equals delivery model for the delivery of documents that require immediate shareholder action and participation, such as proxy-related materials.

Electronic access to documents provides a more cost-efficient, timely, and environmentally friendly manner of communicating information to owners than physical delivery. At the same time, these models may raise investor protection concerns and could have a negative impact on owner engagement.

In considering potential changes, the Department will ensure that the electronic delivery and provision of governance documents does not replace or remove the option for owners to receive paper copies should they request them.

Consultation Questions

The Department of Finance is seeking feedback on two potential models for electronic communications, notice-and-access and access equals delivery.

- What are the benefits and limitations of a notice-and-access or access equals delivery model for: i) financial institutions and ii) their owners?

- Were a notice-and-access or access equals delivery model to be implemented, to which governance documents should it apply?

- If a notice-and-access model were implemented, are there any modifications we should make to the notice-and-access model as described in National Instruments 51-102 and 54-101 to better reflect the way financial institutions communicate with their owners? Please see Annex 1 for relevant parts of the National Instruments.

- If an access-equals-delivery model were implemented, are there any modifications we should make to the CSA's access equals delivery model as described in these proposed amendments?

- In your view, how should future regulations address:

- how, where, and when paper copies can be accessed by owners; and,

- how and when owners will be informed about the process for obtaining paper copies?

- If you are a non-distributing institution, would you make use of an e-communications model like notice-and-access or access equals delivery? If not, please describe elements of an electronic communications model that would be appropriate for your institution and its owners.

Virtual Shareholder Meetings

A virtual shareholder meeting is one that takes place exclusively online, without a corresponding in-person meeting. They can include features such as registration desks, polling, real-time voting, managed question-and-answer sessions, and one-on-one instant messaging.

The financial institutions statutes allow FRFIs to hold hybrid shareholder meetings (meetings with both in-person and virtual attendance), but prohibit virtual-only meetings unless an institution seeks a court order to exempt it from this requirement. By contrast, a corporation governed by the Canada Business Corporations Act can hold virtual-only shareholder meetings, as long as the company's own bylaws provide for it and shareholders can communicate with one another through the meeting's digital platform.

Prior to the COVID-19 pandemic, virtual shareholder meetings in Canada were rare. However, as a result of public health restrictions that limited gathering sizes and required physical distancing, approximately fifty-four percent of TSX issuers held virtual-only annual general meetings as of July 2020.Footnote 22 Among financial institutions, a group of the largest banks and insurance companies jointly obtained court orders that allowed them to hold their 2020, 2021 and 2022 annual meetings using electronic means.Footnote 23

The Department of Finance is seeking feedback on allowing financial institutions to hold virtual-only meetings with their owners without seeking a court order.

Consultation Questions

- What are the risks and opportunities of holding virtual shareholder meetings for: i) financial institutions and ii) their owners? If applicable, please include information on topics such as:

- attendance, participation, and voting;

- how questions are solicited, selected, and addressed;

- if and how participants communicate with one another during the meeting; and,

- if and how participants interact informally with management during the meeting.

- How do the risks and opportunities differ for distributing and non-distributing FRFIs, including credit unions and certain insurance companies?

- In your view, how should the legal and regulatory framework be structured to ensure that communication during virtual meetings is inclusive and effective? Should regulations governing virtual shareholder meetings include provisions that require:

- communication among participants and owners;

- authentication of attendees;

- transparent selection of shareholder questions;

- accessible presentation of shareholder proposals;

- publication of the recording after the meeting; and/or

- any other elements for which regulatory provisions should be made?

Annex 1: Canadian Securities Administrators Notice-and-Access National Instruments

The following are excerpts from the CSA's unofficial consolidations of National Instruments 51-102 and 54-101, which govern reporting issuers' use of the notice-and-access model. Stakeholders are encouraged to read the entire contents of the two National Instruments to obtain a more comprehensive understanding of the notice-and-access model.

National Instrument 51-102 Continuous Disclosure Obligations

Notice-and-Access

9.1.1 (1) A person or company soliciting proxies may use notice-and-access to send proxy-related materials to a registered holder of voting securities of a reporting issuer if all of the following apply:

- the registered holder of voting securities is sent a notice that contains the following information and no other information:

- the date, time and location of the reporting issuer's meeting for which the proxy-related materials are being sent;

- a description of each matter or group of related matters identified in the form of proxy to be voted on, unless that information is already included in a form of proxy that is being sent to the registered holder of voting securities under paragraph (b);

- the website addresses for SEDAR and the non-SEDAR website where the proxy-related materials are posted;

- a reminder to review the information circular before voting;

- an explanation of how to obtain a paper copy of the information circular and, if applicable, the documents in paragraph (2)(b) from the person or company;

- a plain-language explanation of notice-and-access that includes the following information:

- if the person or company is using stratification, a list of the types of registered holders or beneficial owners who will receive paper copies of the information circular and, if applicable, the documents in paragraph (2)(b);

- the estimated date and time by which a request for a paper copy of the information circular and, if applicable, the documents in paragraph (2)(b), is to be received in order for the requester to receive the paper copy in advance of any deadline for the submission of the proxy and the date of the meeting;

- an explanation of how the registered holder is to return the proxy, including any deadline for return of the proxy;

- the sections of the information circular where disclosure regarding each matter or group of related matters identified in the notice can be found;

- a toll-free telephone number the registered holder can call to get information about notice-and-access;

- the registered holder of voting securities is sent, by prepaid mail, courier or the equivalent, the notice required by paragraph (a) and a form of proxy for use at the meeting and, in the case of a solicitation by or on behalf of management of the reporting issuer, the notice and form of proxy are sent at least 30 days before the date of the meeting;

- in the case of a solicitation by or on behalf of management of the reporting issuer, the reporting issuer files on SEDAR the notification of meeting and record dates in the manner and within the time specified by NI 54-101;

- public electronic access to the information circular, form of proxy and the notice in paragraph (a) is provided on or before the date that the person or company soliciting proxies sends the notice in paragraph (a) to registered holders in the following manner:

- the documents are filed on SEDAR as required by section 9.3;

- the documents are posted until the date that is one year from the date that the documents are posted, on a website other than the website for SEDAR;

- a toll-free telephone number is provided for use by the registered holder of voting securities to request a paper copy of the information circular and, if applicable, the documents in paragraph (2)(b), at any time from the date that the person or company soliciting proxies sends the notice in paragraph (a) to the registered holder up to and including the date of the meeting, including any adjournment;

- if a request for a paper copy of the information circular and, if applicable, the documents in paragraph (2)(b), is received at the toll-free telephone number provided under paragraph (e) or by any other means, a paper copy of any such document requested is sent free of charge by the person or company soliciting proxies to the requester at the address specified in the request in the following manner:

- in the case of a request received prior to the date of the meeting, within 3 business days after receiving the request, by first class mail, courier or the equivalent;

- in the case of a request received on or after the date of the meeting, and within one year of the information circular being filed, within 10 calendar days after receiving the request, by prepaid mail, courier or the equivalent.

(2) Unless an information circular is included with the proxy-related materials, a reporting issuer that sends proxy-related materials to a registered holder of voting securities using notice-and-access must not include with the proxy-related materials any information or document that relates to the particulars of any matter to be submitted to the meeting, except for the following:

- the information required to be included in the notice under paragraph (1)(a);

- financial statements of the reporting issuer to be approved at the meeting and MD&A related to those financial statements, which may be part of an annual report.

(3) A notice under paragraph (1)(a) and the form of proxy may be combined in a single document.

Posting materials on non-SEDAR website

9.1.2 (1) A person or company that posts proxy-related materials in the manner referred to in subparagraph 9.1.1(1)(d)(ii) must also post on the website the following documents:

- any disclosure material regarding the meeting that the person or company has sent to registered holders or beneficial owners of voting securities;

- any written communications the person or company soliciting proxies has made available to the public regarding each matter or group of matters to be voted upon at the meeting, whether or not they were sent to registered holders or beneficial owners of voting securities.

(2) Proxy-related materials that are posted under subparagraph 9.1.1(1)(d)(ii) must be posted in a manner and be in a format that permit an individual with a reasonable level of computer skill and knowledge to do all of the following easily:

- access, read and search the documents on the website;

- download and print the documents.

Consent to other delivery methods

9.1.3 For greater certainty, section 9.1.1 does not

- prevent a registered holder of voting securities from consenting to a person or company's use of other delivery methods to send proxy-related materials,

- terminate or modify a consent that a registered holder of voting securities previously gave to a person or company regarding the use of other delivery methods to send proxy-related materials, or

- prevent a person or company from sending proxy-related materials using a delivery method to which a registered holder has consented prior to February 11, 2013.

Instructions to receive paper copies

9.1.4 (1) Despite section 9.1.1, a reporting issuer may obtain standing instructions from a registered holder of voting securities that a paper copy of the information circular and, if applicable, the documents in paragraph 9.1.1(2)(b), be sent to the registered holder in all cases when the reporting issuer uses notice-and-access.

(2) If a reporting issuer has obtained standing instructions from a registered holder under subsection (1), the reporting issuer must do both of the following:

- include with the notice required by paragraph 9.1.1(1)(a) any paper copies of information circulars and, if applicable, the documents in paragraph 9.1.1(2)(b), required to comply with standing instructions obtained under subsection (1);

- include with the notice under paragraph (a) a description, or otherwise inform the registered holder of, the means by which the registered holder may revoke the registered holder's standing instructions.

National Instrument 54-101 Communication with Beneficial Owners of Securities of a Reporting Issuer

Notice-and-Access

2.7.1 (1) A reporting issuer that is not an investment fund may use notice-and-access to send proxy-related materials relating to a meeting to a beneficial owner of its securities if all of the following apply:

- the beneficial owner is sent a notice that contains the following information and no other information:

- the date, time and location of the meeting for which the proxy-related materials are being sent;

- a description of each matter or group of related matters identified in the form of proxy to be voted on, unless that information is already included in a Form 54-101F6 or Form 54-101F7 as applicable, that is being sent to the beneficial owner under paragraph (b);

- the website addresses for SEDAR and the non-SEDAR website where the proxy-related materials are posted;

- a reminder to review the information circular before voting;

- an explanation of how to obtain a paper copy of the information circular and, if applicable, the documents in paragraph (2)(b) from the reporting issuer;

- a plain-language explanation of notice-and-access that includes the following information:

- if the reporting issuer is using stratification, a list of the types of registered holders or beneficial owners who will receive paper copies of the information circular, and if applicable, the documents in paragraph (2)(b);

- the estimated date and time by which a request for a paper copy of the information circular and, if applicable, the documents in paragraph (2)(b), is to be received in order for the requester to receive the paper copy in advance of any deadline for the submission of voting instructions and the date of the meeting;

- an explanation of how the beneficial owner is to return voting instructions, including any deadline for return of those instructions;

- the sections of the information circular where disclosure regarding each matter or group of related matters identified in the notice can be found;

- a toll-free telephone number the beneficial owner can call to get information about notice-and-access;

- using the procedures referred to in section 2.9 or 2.12, as applicable, the beneficial owner is sent, by prepaid mail, courier or the equivalent, the notice required by paragraph (a) and a Form 54-101F6 or Form 54-101F7, as applicable;

- the reporting issuer files on SEDAR the notification of meeting and record dates on the same date that it sends the notification under subsection 2.2(1);

- public electronic access to the information circular and the notice in paragraph (a) is provided on or before the date that the reporting issuer sends the notice in paragraph (a) to beneficial owners, in the following manner:

- the documents are filed on SEDAR;

- the documents are posted until the date that is one year from the date that the documents are posted, on a website other than the website for SEDAR;

- a toll-free telephone number is provided for use by the beneficial owner to request a paper copy of the information circular and, if applicable, the documents in paragraph (2)(b), at any time from the date that the reporting issuer sends the notice in paragraph (a) to the beneficial owner up to and including the date of the meeting, including any adjournment;

- if a request for a paper copy of the information circular and, if applicable, the documents in paragraph (2)(b), is received at the toll-free telephone number provided under paragraph (e) or by any other means, a paper copy of any such document requested is sent free of charge by the reporting issuer to the requester at the address specified in the request in the following manner:

- in the case of a request received prior to the date of the meeting, within 3 business days after receiving the request, by first class mail, courier or the equivalent;

- in the case of a request received on or after the date of the meeting, and within one year of the information circular being filed, within 10 calendar days after receiving the request, by prepaid mail, courier or the equivalent.

(2) Unless an information circular is included with the proxy-related materials, a reporting issuer that sends proxy-related materials to a beneficial owner of its securities using notice-and-access must not include with the proxy-related materials any information or document that relates to the particulars of any matter to be submitted to the meeting, except for the following:

- the information required to be included in the notice under paragraph (1)(a);

- financial statements of the reporting issuer to be approved at the meeting, and MD&A related to those financial statements, which may be part of an annual report.

Notice in advance of first use of notice-and-access

2.7.2 Despite paragraph 2.7.1(1)(c) and subsection 2.20(a.1), the first time that a reporting issuer uses notice-and-access to send proxy-related materials to a beneficial owner of its securities, the reporting issuer must file on SEDAR the notification of meeting and record dates at least 25 days before the record date for notice.

Restrictions on information gathering

2.7.3 (1) A reporting issuer that receives a request for a paper copy of the information circular or other documents referred to in paragraph 2.7.1(1)(e) using the toll-free telephone number or by any other means must not do any of the following:

- ask for any information about the requester, other than the name and address to which the information circular and, if applicable, the documents in paragraph 2.7.1(2)(b), are to be sent;

- disclose or use the name or address of the requester for any purpose other than sending the information circular and, if applicable, the documents in paragraph 2.7.1(2)(b).

(2) A reporting issuer that posts proxy-related materials pursuant to subparagraph 2.7.1(1)(d)(ii) must not collect information that can be used to identify a person or company who has accessed the website address where the proxy-related materials are posted.

Posting materials on non-SEDAR website

2.7.4 (1) A reporting issuer that posts proxy-related materials in the manner referred to in subparagraph 2.7.1(1)(d)(ii) must also post on the website the following documents:

- any disclosure material regarding the meeting that the reporting issuer has sent to registered holders or beneficial owners of its securities;

- any written communications the reporting issuer has made available to the public regarding each matter or group of matters to be voted on at the meeting, whether or not they were sent to registered holders or beneficial owners of its securities.

(2) Proxy-related materials that are posted under subparagraph 2.7.1(1)(d)(ii) must be posted in a manner and be in a format that permit an individual with a reasonable level of computer skill and knowledge to do all of the following easily:

- access, read and search the documents on the website;

- download and print the documents.

Consent to other delivery methods

2.7.5 For greater certainty, section 2.7.1 does not

- prevent a beneficial owner from consenting to a reporting issuer, an intermediary or another person or company's use of other delivery methods to send proxy-related materials,

- terminate or modify a consent that a beneficial owner of voting securities previously gave to a reporting issuer, an intermediary or another person or company regarding the use of other delivery methods to send proxy-related materials, or

- prevent a reporting issuer, an intermediary or another person or company from sending proxy-related materials using a delivery method to which a beneficial owner has consented prior to February 11, 2013.

Instructions to receive paper copies

2.7.6 (1) Despite section 2.7.1, an intermediary may obtain standing instructions from a beneficial owner that is a client of the intermediary that a paper copy of the information circular and, if applicable, the documents in paragraph 2.7.1(2)(b), be sent to the beneficial owner in all cases when a reporting issuer uses notice-and-access.

(2) If an intermediary has obtained standing instructions from a beneficial owner under subsection (1), the intermediary must do all of the following:

- if the reporting issuer is sending proxy-related materials directly under section 2.9, indicate in the NOBO list provided to the reporting issuer those NOBOs who have provided standing instructions under subsection (1) as at the date the NOBO list is generated;

- if the intermediary is sending proxy-related materials to a beneficial owner on behalf of a reporting issuer using notice-and-access, request appropriate quantities of paper copies of the information circular and, if applicable, the documents in paragraph 2.7.1(2)(b), from the reporting issuer for forwarding to beneficial owners who have provided standing instructions to be sent paper copies;

- include with the proxy-related materials a description, or otherwise inform the beneficial owner of, the means by which the beneficial owner may revoke the beneficial owner's standing instructions.

Application to non-management solicitations

2.7.7 (1) A person or company other than management of a reporting issuer that is required by law to send materials to registered holders or beneficial owners of securities in connection with a meeting may use notice-and-access to send the materials.

(2) Section 2.7.1, other than paragraph (1)(c), and sections 2.7.3, 2.7.4 and 2.7.5 apply to a person or company in subsection (1) as if the person or company were a reporting issuer.

(3) Paragraph 2.7.1(1)(c) and section 2.7.8 apply to a person or company referred to in subsection (1) only if the person or company has requisitioned a meeting.

Record date for notice

2.7.8 Despite subsection 2.1(b), a reporting issuer that uses notice-and-access must set a record date for notice that is no fewer than 40 days before the date of the meeting.