Canada's Anti-Money Laundering and Anti-Terrorist Financing Regime: Report on Performance Measurement Framework (released March 2023)

Introduction

Money laundering and terrorist financing (ML/TF) are serious threats to the safety and security of Canadians, as well as the integrity of Canada's financial system. Canada's AML/ATF Regime was established in 2001 as a whole-of-government initiative to counter these illicit activities, bringing together departments and agencies while providing dedicated resources to prevent, detect, deter and disrupt money laundering and terrorist financing. Comprised of thirteen departments and agencies, the Regime advances the Government of Canada's efforts to counter global financial crime. Canadians expect their government to maintain a Regime that is responsive to Canada's ML/TF risks while demonstrating tangible and sustained results. Regular measurement of the Regime's outputs, using key performance indicators, is important for understanding whether the Regime is meeting its expected outcomes, while supporting accountability and strategic decision making.

Money laundering is the process used to conceal or disguise the origin of criminal proceeds to make them appear as if they originated from legitimate sources. Money laundering benefits domestic and international criminals and organized crime groups.

Terrorist financing is the collection and provision of funds from legitimate or illegitimate sources for terrorist activity. It supports and sustains the activities of domestic and international terrorists that can result in terrorist attacks in Canada or abroad, causing loss of life and destruction.

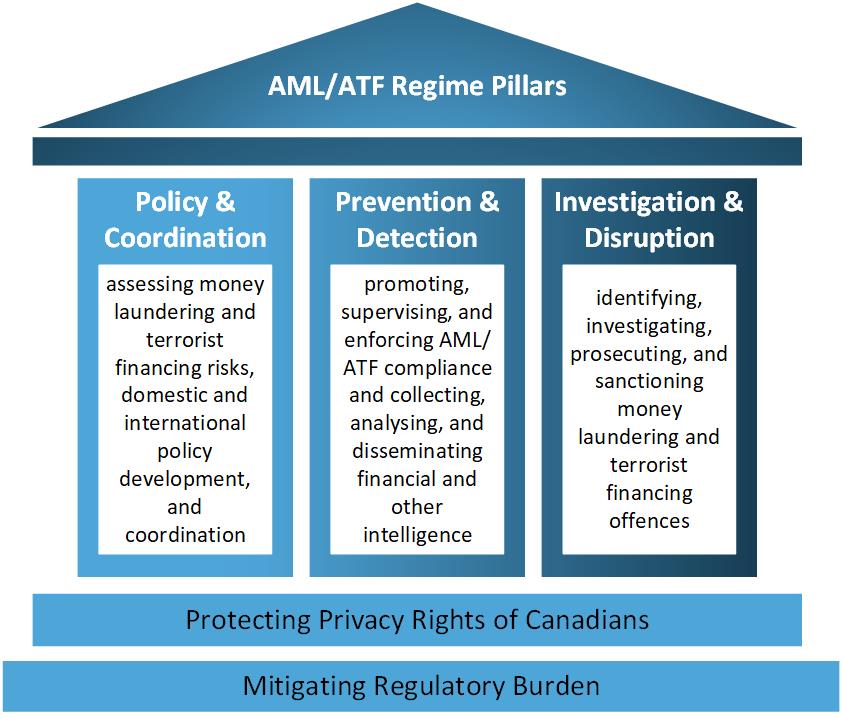

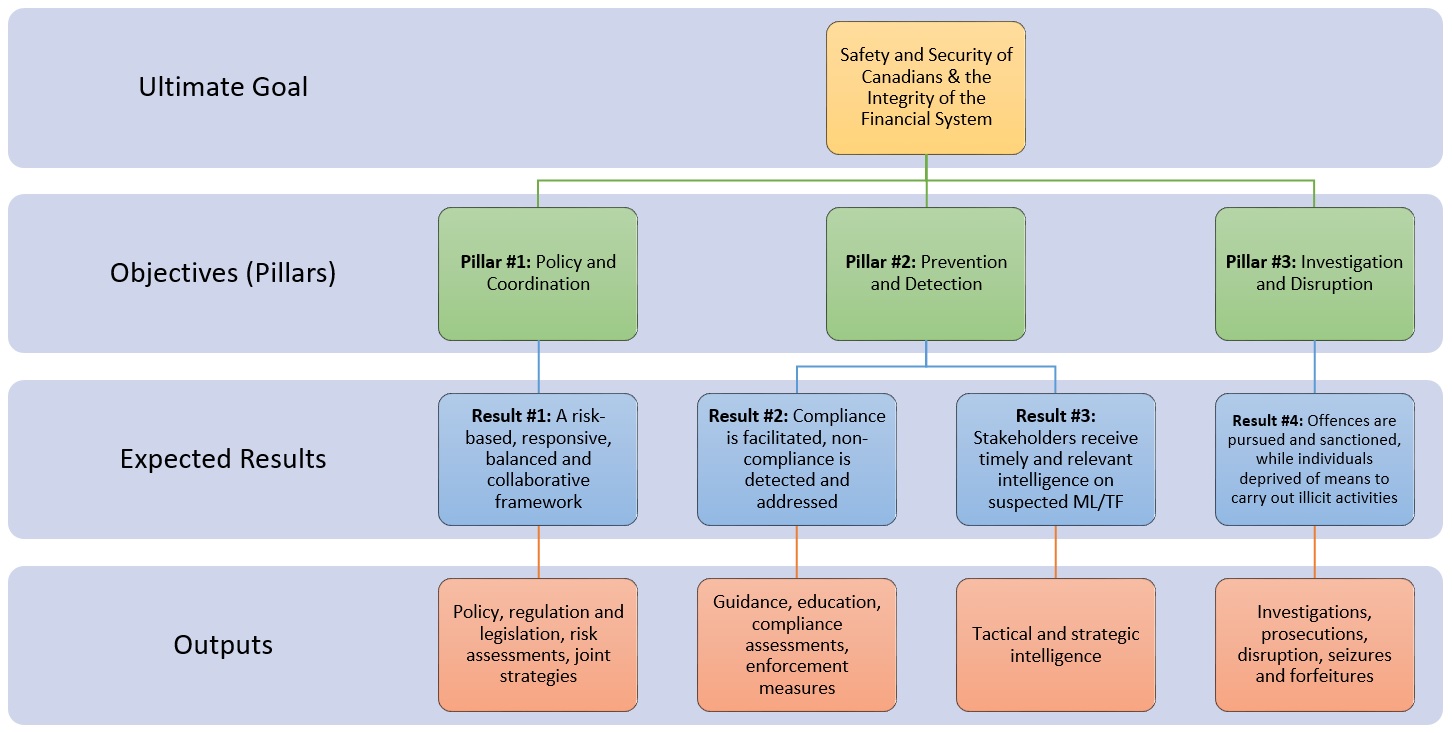

The purpose of this report is to present the latest results for key performance indicators captured under the Regime's new Performance Measurement Framework, up to the 2019-20 fiscal year. It will also identify significant long-term trends, while discussing contributing factors and their relationship to expected results. For all indicators, up to ten years of data are used where available. Results are grouped based on the core "pillars" of the Regime – policy and coordination, prevention and detection, and investigation and disruption. The three pillars are outlined below, while the more detailed logic model can be seen in Annex A.

AML/ATF Regime Pillars

Despite significant efforts by partners, additional efforts will be required by the Regime in order to achieve sustained, long-term operational results in the prevention, detection, investigation and disruption of money laundering and terrorist financing. Statistics compiled for this report show that enforcement results – as measured by the number of investigations, charges, prosecutions, convictions and asset forfeitures – have declined between 2010 and 2020. The factors contributing to these results are complex and must be considered within Canada's unique context. The Financial Action Task Force (FATF) has identified other gaps in the policy framework – particularly around beneficial ownership transparency and regulation of the legal profession – which create further vulnerabilities in Canada's Regime that impact operational effectiveness.

The Regime is taking substantive steps to address existing gaps by strengthening policy, coordination and capacity to investigate and prosecute financial crimes, advancing work to comply with international AML/ATF standards on beneficial ownership transparency and regulation of the legal profession, and implementing improved practices to better use financial intelligence and target enforcement actions. New entities such as the Canadian Integrated Response to Organized Crime (CIROC), Counter Illicit Finance Alliance (CIFA), Financial Crime Coordination Centre (FC3) and Integrated Money Laundering Investigative Teams represent the most recent initiatives to improve enforcement results. Going forward, proposed policy and operational measures will be considered in light of their contribution to increased operational effectiveness, in order to secure ML/TF charges, convictions and forfeitures where appropriate. Strengthening performance measurement is a priority for the Regime, which includes making better use of existing data sources across partners, while developing new data streams to provide additional insights into Regime effectiveness.

This report, unless otherwise noted, reflects information and statistics available up to the end of the 2019-20 fiscal year. The Government of Canada has since continued to advance policy, legislation and regulations and funding initiatives to strengthen Canada's Anti-Money Laundering and Anti-Terrorist Financing (AML/ATF) Regime. AML/ATF obligations have been introduced to cover virtual asset service providers, foreign money services businesses, armoured cars, payment service providers and crowdfunding platforms. Since 2019, the government has made investments of $319.9 million, with $48.8 million ongoing, to strengthen the federal AML/ATF Regime through data resources, financial intelligence, compliance and outreach, information sharing and investigative capacity to support money laundering investigations in Canada. Budget 2022 increased funding to support the Financial Transactions and Reports Analysis Centre of Canada representing a 24 per cent increase in funding and a 13 per cent increase in staff. It also announced the Government's intention to accelerate its commitment to implement a publicly accessible corporate beneficial ownership registry by the end of 2023, and to establish a new Canada Financial Crimes Agency, which will bolster Canada's ability to quickly respond to complex and fast-moving cases of financial crime.

The 2019-20 Performance Measurement Framework Report, supports the release of the Government of Canada's Anti-Money Laundering and Anti-Terrorist Financing Strategy for 2023-2026. The 2023 parliamentary review of the Proceeds of Crime (Money Laundering) and Terrorist Financing Act (PCMLTFA) will support continued efforts to ensure the AML/ATF Regime remains responsive and is effective in addressing evolving money laundering and terrorist financing threats to Canada.

The First Pillar: Policy and Coordination

The first pillar is policy and coordination, which covers work to assess Canada's current ML/TF risks and vulnerabilities, identify and close gaps in Canada's AML/ATF policy framework, and provide strategic direction for the Regime. Canada has a risk-based and responsive framework that balances AML/ATF measures with administrative costs, privacy and constitutionality, while aligning with broader Government of Canada criminal justice, national security and economic policy priorities. Although risk assessment, policy and governance are not easily measurable, they are highly relevant as they underpin the Regime's operations.

In 2019-20, the AML/ATF framework was strengthened through work to update the National Inherent Risk Assessment (NIRA), new policy measures to support intelligence sharing, investigations, prosecutions and confiscations, and increased interdepartmental and private sector engagement. Meanwhile, legislative and regulatory amendments made in 2019-20 have further aligned Canada's Regime with international AML/ATF standards and responded to gaps identified in prior reviews, particularly with the addition of 'recklessness' to the Criminal Code offence for money laundering. Key policy gaps in the Regime were identified as the integration of the legal profession into the Regime, beneficial ownership transparency and improving investigations, prosecutions and seizures. Measures taken to respond to these gaps are helping to address key vulnerabilities, improve transparency and deterrence, while enhancing the effectiveness of operational agencies. Work continues to assess the efficacy of information sharing policy and legislation among key enforcement partners in relation to AML and ATF investigations.

Result #1: A risk-based, responsive, balanced and collaborative framework

1.1 Inherent Risk and Vulnerability Assessments

As a member of the FATF, the global AML/ATF standard-setting body, Canada is expected to identify and assess its inherent ML/TF risks and vulnerabilities on an ongoing basis. The NIRA serves as a key tool for understanding ongoing ML/TF trends and methods. The NIRA also helps to inform new policy responses and provide risk information to industry. The first NIRA published in 2015, rated certain types of fraud, illicit drug trafficking and third party money launderingFootnote 1 as very high money laundering vulnerabilities, with transnational organized crime groups among the key money laundering threat actors in Canada. The assessment also concluded that there was a terrorist financing threat in Canada, with networks raising funds domestically that are sent outside of the country to support terrorist activities outside of Canada.Footnote 2 Understanding emerging and evolving ML/TF threats – including online crime, trade-based money laundering (TBML), the use of real estate and casinos, fentanyl trafficking and virtual currencies – remains a significant focus for the Regime.

Regime partners are updating the NIRA to reflect contemporary ML/TF risks, by renewing the existing risk profiles with recent intelligence and creating new profiles where necessary. For example, the Canada Revenue Agency Charities Directorate (CRA-CD) began a Sector Review to reassess the Canadian not-for-profit sector and identify the types of organizations within it in order to categorize those that may be at greater risk of TF abuse. The review identified that non-profit organizations, in addition to registered charities, are at risk of TF abuse. Further, through the update, the threat assessment rating for tax evasion was increased from medium to high, recognizing tax evasion as a predicate crimeFootnote 3 to the serious offence of money laundering. The Canada Revenue Agency (CRA) created the Illicit Income Audit Program with powers to obtain non-conviction based forfeiture for tax liabilities from illicit enterprise. This program provides an additional tool for the Regime in combatting money laundering and the activities of organized crime groups.

Following publication of the NIRA, Regime partners intend to further engage stakeholders to build awareness and to continue to improve the identification and analysis of emerging ML/TF risks.

1.2 Legislation, Regulations and Other Policy Measures

The Department of Finance Canada oversees the Regime's policy and legislative framework, advises the Government of Canada on domestic and international AML/ATF policies, and is responsible for the Proceeds of Crime (Money Laundering) and Terrorist Financing Act (PCMLTFA) and related regulations. The Department of Justice Canada provides legal advice on ML/TF offences to Regime partners and aids policy development by providing legal opinions with respect to legal challenges. The Department of Justice is responsible for the Criminal Code, as well as the Mutual Legal Assistance in Criminal Matters Act and the Extradition Act, the two main statutes in relation to Canada's ability to provide international cooperation to Canadian Regime partners and Canada's international partners. Public Safety Canada is the lead policy department responsible for combatting transnational organized crime, terrorism, and other threats to the security of Canada. It works closely with the Department of Finance to co-lead Canada's AML/ATF Regime governance committees, and ensure that AML/ATF policies reflect the needs of federal operational agencies, particularly those under the Public Safety portfolio.

Canadian Alignment with Financial Action Task Force Standards

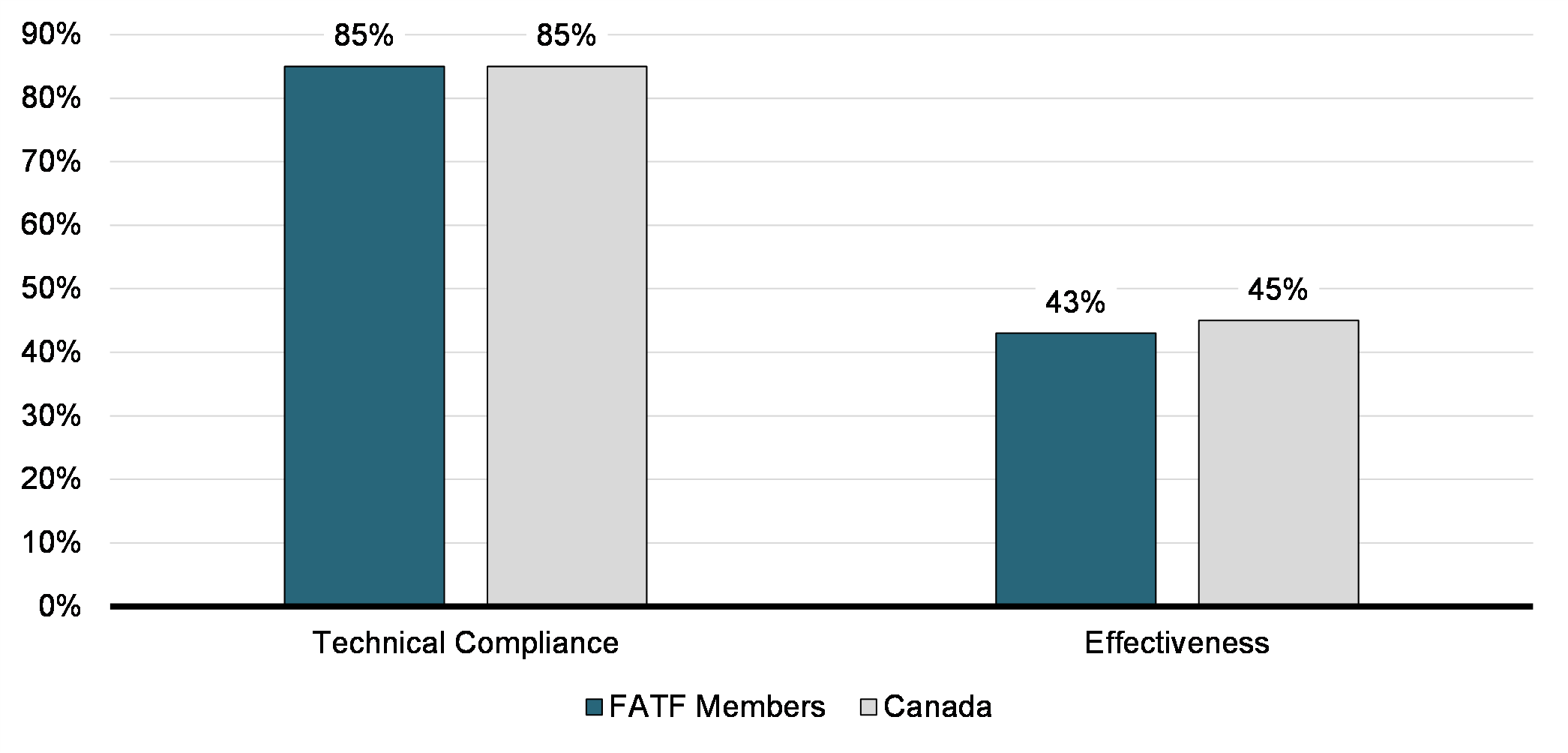

As a founding member of the FATF, Canada has committed to implementing the FATF Standards with respect to technical compliance and effectiveness. Under the FATF Methodology, technical compliance refers to the implementation of the specific requirements of the FATF Recommendations, including the framework of laws and enforceable means; and the existence, powers and procedures of competent authorities. Effectiveness is the extent to which economies and financial systems mitigate the risks and threats of money laundering, terrorist financing and financing of proliferation of weapons of mass destruction. The FATF published a Report on the State of Effectiveness and Compliance with the FATF Standards in April 2022.Footnote 4 Canada's AML/ATF Regime performs comparably to other FATF members on effectiveness, both on technical compliance and effectiveness.

FATF Ratings Above Satisfactory Threshold

Legislative and Regulatory Amendments

On July 10, 2019, amendments to the PCMLTFA Regulations were published in the Canada GazetteFootnote 5 to strengthen Canada's AML/ATF Regime. These amendments revised the preventive measures that reporting entitiesFootnote 6 – individuals and entities with AML/ATF obligations – must undertake to prevent their businesses from being misused for illicit activities. The revised regulations expanded client due diligence and beneficial ownership reporting requirements; regulated businesses dealing in virtual currency; included foreign money services businesses (MSBs)Footnote 7 in the Regime; and included other clarifications and technical amendments. These amendments came into force on June 1, 2021.

The Government of Canada also passed an amendment to the offence of money laundering in the Criminal Code to add the alternative element of recklessness to potentially allow prosecutors to more easily prosecute the offence of money laundering, and more effectively target professional money launderers. Finally, amendments to the Seized Property Management Act broadened access to specialized asset management services at Public Services and Procurement Canada, reducing the need for duplication of these services nationwide.

Policy Priorities for the Regime

Strategic policy priorities for the AML/ATF Regime include addressing the inherent money laundering and terrorist financing risks in the legal profession; improving beneficial ownership transparency of corporations in Canada; as well as legislative and policy changes to support operational effectiveness in information sharing, investigations, prosecutions, and asset recovery. These priorities reflect areas where policy action by the Government of Canada is likely to have the most material impact on operational results.

The legal profession remains highly vulnerable to exploitation given its specialized knowledge, ability to carry out transactions on behalf of its clients, and involvement in establishing trusts and corporations. In June 2019, the Government of Canada formed a new working group with the Federation of Law Societies of Canada (FLSC) to address the inherent risks of money laundering and other illicit activity that may arise in the practice of law. Regular meetings of the working group allow the FLSC and the government to collaborate on addressing AML/ATF issues in the legal profession. The Regime remains committed to collaborating on ways to improve supervision of the legal profession in order to address these money laundering risks.

The Regime has continued to make progress to strengthen beneficial ownership transparency in collaboration with Canada's provinces and territories. In June 2019, amendments to the Canada Business Corporations Act (CBCA) came into force requiring federally incorporated private corporations to create and maintain registers of individuals with significant control.Footnote 8 Around the same time, regulatory amendments were passed to make beneficial ownership information on the individuals who own, control and profit from corporations more readily available to law enforcement. Meanwhile, on June 13, 2019, several of Canada's federal, provincial, and territorial Ministers of Finance and ministers responsible for anti-money laundering and beneficial ownership transparency met to advance a national response to combat money laundering in Canada. Together, governments agreed to cooperate on consultations for making beneficial ownership information more transparent such as through public registries.

Building on the June 2019 commitment, in February 2020, the Department of Finance Canada and Innovation, Science and Economic Development Canada initiated public consultations on the proposed creation of a publicly accessible registry (or registries) of corporate beneficial ownership.Footnote 9 The government continues to collaborate with provincial and territorial counterparts on strengthening beneficial ownership transparency, while respecting jurisdictional responsibilities for corporations.

In addition, a number of new policy measures have been introduced to support intelligence sharing, investigations, prosecutions and confiscations. Legislative amendments to the PCMLTFA added Revenu Québec and the Competition Bureau as disclosure recipients of the Financial Transactions and Reports Analysis Centre of Canada (FINTRAC), while improving transparency of administrative monetary penalties issued by FINTRAC. The Regime remains focused on identifying and moving forward policy and legislative measures to improve operational effectiveness.

1.3 Joint Strategies, Action Plans, Governance Initiatives

Federal partners are jointly responsible for the Regime's outcomes. The Regime has modified its governance in response to external reviews, which highlighted the importance of effective cooperation between partners, aligned priorities and joint accountability for achieving better results. Governance enhancements since 2017 include the creation of a Deputy Minister-level committee, reporting to the Deputy Minister National Security Committee, to set and oversee implementation of strategic, risk-based priorities for the Regime. In addition, Public Safety Canada assumed the role of co-Chair of the Regime's Deputy Minister-, Assistant Deputy Minister-, and Director General-level coordinating committees alongside the Department of Finance Canada.

Interdepartmental Governance

The Regime's interdepartmental governance committees supported the 2020 beneficial ownership registry consultations, the Government of Canada's participation in the Commission of Inquiry into Money Laundering in British Columbia, the British Columbia-Canada Ad Hoc Working Group on Real Estate, the Federal-Provincial-Territorial Working Group on Beneficial Ownership Transparency, and the development of Budget 2020 measures to strengthen the policy and operational aspects of the Regime.

Case Study 1.1: B.C.-Canada Ad Hoc Working Group on Real Estate

Since late 2018, the federal government and province of British Columbia have been collaborating to better understand and address money laundering in the province's real estate sector. A multi-agency working group, led by their respective Finance ministries, and including participation from FINTRAC, law enforcement, regulators and tax authorities, have looked at the issues of money laundering and fraud in real estate.

2019-20 also saw the launch of the FC3 design phase, announced in Budget 2019 and hosted at Public Safety Canada. The aim of this new group within Public Safety Canada is to provide coordination and support to AML operational partners working to investigate and prosecute money laundering offences through the alignment of policies and priorities across the AML/ATF Regime; improvement of information sharing and access to resources; and enhancement of anti-money laundering knowledge, skills and expertise. FC3 met with domestic and international partners, including over 110 meetings with more than 200 participants in 2019-20, to better understand and identify Canada's successes and challenges in enforcement to combat money laundering and financial crime. The group undertook significant empirical research on AML gaps and opportunities in Canada, to inform its operational design and model.

Going forward, the Regime will continue to improve priority-setting, performance measurement and ongoing review of the Regime. It will also look to opportunities to integrate the goal of "following the money" into broader strategies to address organized crime and national security.

Private Sector Engagement

The Regime seeks to balance measures to reduce ML/TF risks in the Canadian economy with the compliance costs placed on the private and non-profit sectors. To better consult private sector perspectives in AML/ATF policy-making, the Regime uses the Advisory Committee on Money Laundering and Terrorist Financing (ACMLTF), co-chaired by the Department of Finance Canada and a private sector member (currently Scotiabank), with representation from Regime partners and all reporting entity sectors.

The ACMLTF meets two to three times per year, contributing to the Regime's awareness of reporting entity sector perspectives for purposes of developing legislation, regulation, guidance and policy interpretations. For instance, ACMLTF members and other industry contacts were consulted throughout the development of the aforementioned regulatory amendments to assess opportunities to adjust requirements so that the draft regulations and coming into force date did not impose undue administrative burden for the private sector, while remaining consistent with the government's policy intent. Through the Guidance and Policy Interpretation Working Group, a working group of the ACMLTF, FINTRAC consulted with reporting entities on new and revised guidance in relation to the regulatory amendments that were published in 2019. The Regime will continue to proactively engage the ACMLTF, its working groups, and other forums to build up its relationship with industry and support productive discussions on priority measures.

1.4 Discussion

In updating the NIRA, the Regime worked to revise its understanding of Canada's inherent ML/TF risks and vulnerabilities, which is needed to support effective priority-setting, policy-making, and operational planning by the rest of the Regime. Policy measures to respond to coverage gaps and weaknesses relating to the legal profession, beneficial ownership and operational effectiveness have aimed to improve the overall scope of the Regime, while laying the foundations for stronger operational results. For these policy measures to provide value to their full extent, they should ultimately help respond to operational needs and be matched by operational efforts to promote compliance.

The Regime governance structure, now co-led by the Department of Finance Canada and Public Safety Canada, supports inter-departmental and private sector engagement on a variety of initiatives, with work underway to improve strategic planning and priority-setting to more clearly align the efforts of partners. The greatest value from governance will come from proactive engagement by partners with each other and the private sector, with continued high-level senior management support for the Regime. The Regime is currently working towards establishing a clear national strategic vision, via a revised Charter and Strategy, where partners' efforts are goal-oriented and mutually supportive.

The Second Pillar: Prevention and Detection

The second pillar of the Regime is prevention and detection, which aims to prevent individuals from placing illicit proceeds and terrorist-related funds into the financial system, while detecting the placement and movement of such funds. At the centre of this approach are the reporting entities responsible for implementing the various customer due diligence, recordkeeping, reporting and other preventive measures under the PCMLTFA, while the CRA works to prevent misuse of the charitable sector for terrorist financing. Complementing the efforts by reporting entities and registered charities to fulfill their respective obligations is the analysis and disclosure of tactical and strategic intelligence on suspected ML/TF activities to appropriate authorities, where authorized by legislation.

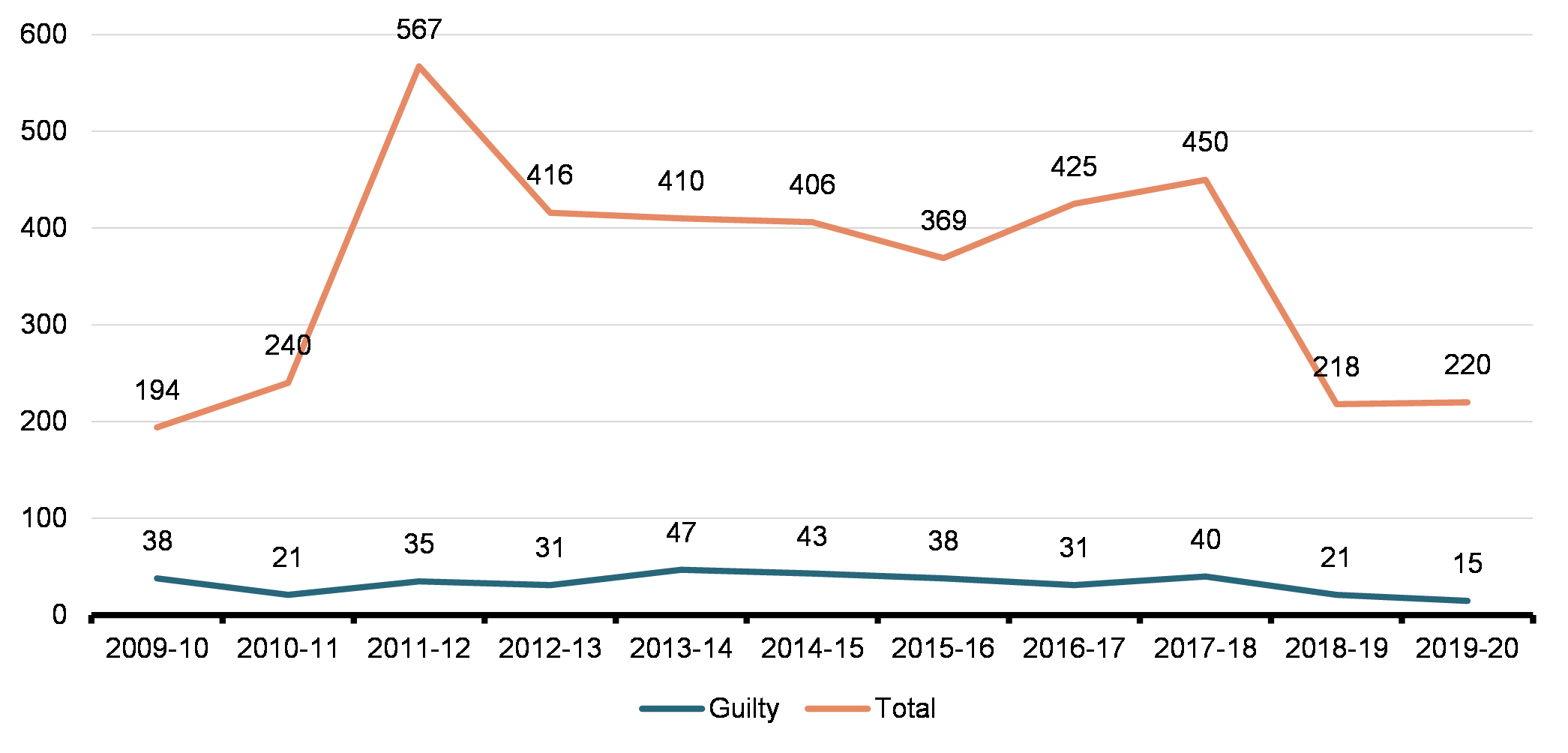

Over 2019-20, the Regime stepped up efforts to promote strong preventive measures against misuse for money laundering and terrorist financing. FINTRAC finalized a new five-year Compliance Engagement Strategy, setting the priorities for the Centre's engagement activities. Both FINTRAC and the CRA-CD increased their outreach to make entities aware of their AML and/or ATF obligations. With the launch of the assessment approach, FINTRAC's examinations are more holistic and targeted, thus improving the likelihood of detecting and correcting substantive deficiencies. In addition, FINTRAC undertook more complex, lengthy and in-depth examinations of larger businesses in higher-risk sectors. These require greater levels of resources and specialized expertise, which translates to fewer examinations conducted compared to previous years. FINTRAC will continue to monitor its use and effectiveness of the revised administrative monetary penalties policy, including its public naming component, as an improved mechanism for promoting compliance. While criminal non-compliance disclosures have risen and more charges are being laid, prosecution results were limited, with only one federal conviction or guilty plea for a PCMLTFA offence between 2014 and 2020.

It remains important for partners to receive timely and relevant financial intelligence to support the detection of money laundering and terrorist financing. FINTRAC received an increasing amount of transaction reporting from reporting entities, particularly suspicious transaction reporting, with volumes having steadily grown over the past decade. This provides FINTRAC with more information which could be turned into actionable tactical and strategic intelligence, although the greater demand can potentially affect operational output due to available resources, and an analytical capacity that can be affected by the quality of the additional reporting. FINTRAC generated a substantial number of intelligence disclosures to its partners, both proactively and in response to voluntary information records, which contributed to a significant number of project-level investigations.

There is significant demand from disclosure recipients for disclosures related to investigative priorities and ongoing cases. FINTRAC disclosures provide actionable intelligence on threat actors and methods, and multiple disclosures can contribute to a single case file. Nonetheless, these might not be sufficient for generating a new investigation without related corroborating intelligence from the receiving agencies.

Result #2: Compliance is facilitated, non-compliance is detected and addressed

2.1 Guidance and Outreach

FINTRAC

As Canada's AML/ATF regulator, FINTRAC administers a risk-based compliance program to ensure that Canadian businesses fulfill their requirements under the PCMLTFA. Effective reporting entity compliance provides FINTRAC with information that it analyzes to generate actionable financial intelligence for Canada's police, law enforcement, national security agencies, and designated Regime partners (such as the CRA), when reasonable grounds exist to suspect a money laundering or terrorist financing offence or a threat to the security of Canada. It also incorporates some deterrence by requiring appropriate due diligence and recordkeeping to deter criminals from using the legitimate financial system to launder their illicit money. FINTRAC provides businesses with guidance to help them better understand and comply with their obligations under the PCMLTFA, as set out in its Compliance Framework.Footnote 10

Effective compliance depends on reporting entities understanding their respective ML/TF risks and obligations under the PCMLTFA. The level of overall awareness is difficult to quantify, but is believed to be higher for financial institutions and other larger reporting entities. Less sophisticated entities, which may include those in sectors such as money services businesses, dealers in precious metals and stones and real estate businesses, with large and fluctuating populations of mostly small entities, often face greater obstacles to understanding their ML/TF risks and staying up-to-date on evolving PCMLTFA obligations, contributing to reduced awareness among some.

FINTRAC Outreach & Engagement Activities

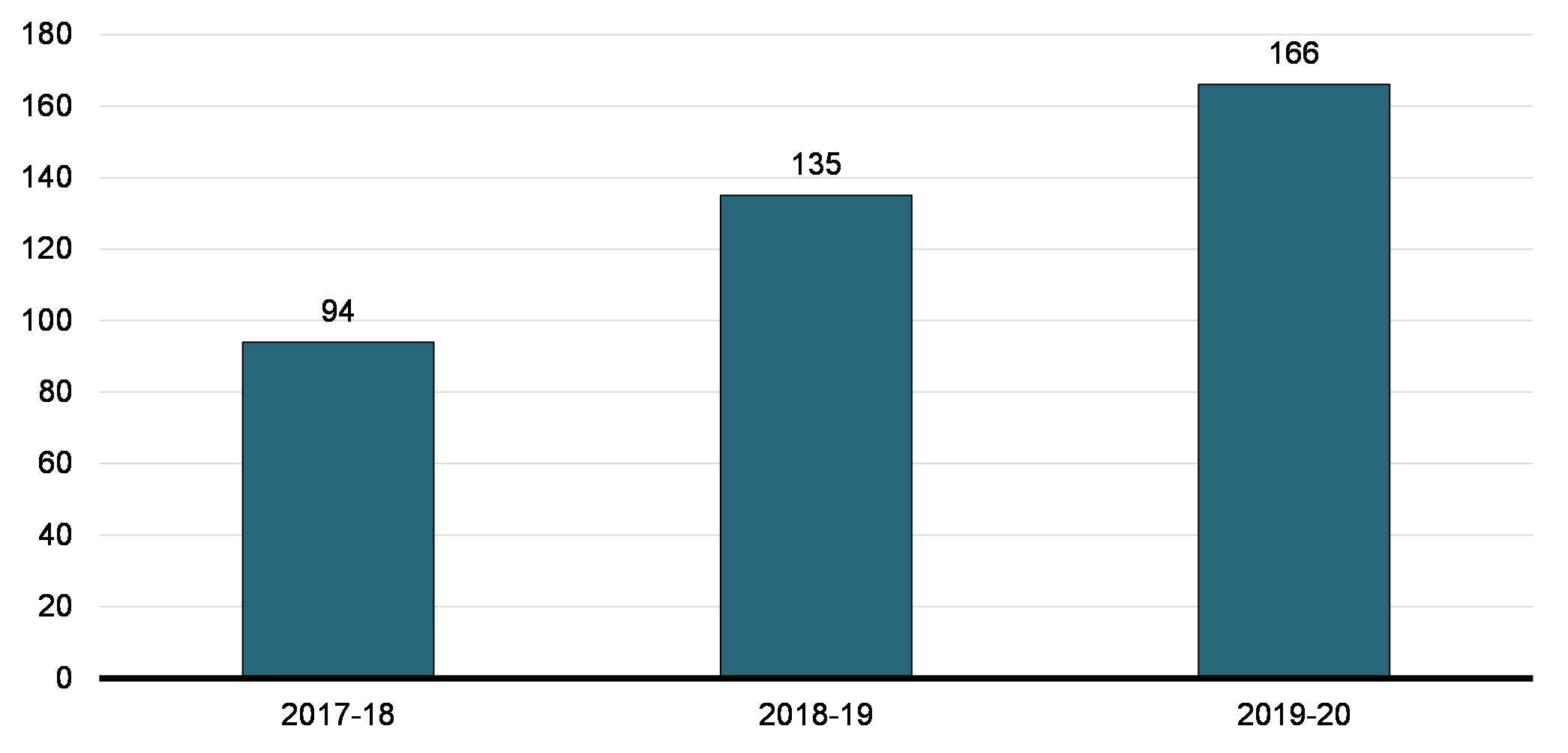

In 2019-20, FINTRAC finalized a new five-year Compliance Engagement Strategy, setting the priorities for its engagement activities. Based on this Strategy, FINTRAC undertook 166 outreach and engagement activities in that first year, such as working groups, conferences and teleconferences, presentations, training sessions and meetings with businesses and stakeholders. This marks a significant increase over the past three fiscal years, reflecting its focus on improving awareness in the real estate, casino, and money services business sectors amongst others.

As noted earlier, FINTRAC consulted reporting entities on the development of new and revised guidance in relation to regulatory amendments published in 2019. During those meetings, FINTRAC shared its approach and rationale for its draft guidance and also gained insight on the needs and expectations of businesses. The FINTRAC Reporting Working Group was used to seek feedback on changes to its reporting systems and forms related to the regulatory amendments. FINTRAC also contributed to AML/ATF training modules for licensed professionals launched by the Real Estate Council of British Columbia in January 2020, while assisting the Real Estate Council of Ontario in 2019 in developing similar training (launched in December 2019). FINTRAC also signed a new Memorandum of Understanding with the Real Estate Council of British Columbia through which both parties can share compliance-related information to strengthen compliance in the real estate sector in British Columbia.

Going forward, FINTRAC will continue to provide ongoing guidance and support through conferences, working groups, training sessions, policy interpretations, as well as through collaboration with industry associations and other regulators. FINTRAC will also explore and pursue additional measures and activities that will increase the added value of its Compliance Program and better meet the needs of reporting entity sectors, including guidance and other educational products. FINTRAC will engage with reporting entities and industry associations through various fora to increase understanding of different business models and sector-specific risks, and better manage global risks.

CRA-Charities Directorate

In carrying out its national security mandate, the CRA-CD aims to foster a charitable sector that is resilient and resistant to the risk of terrorist financing abuse, through outreach and education, and the implementation of compliance measures such as denial or revocation of registration, and penalties. The Directorate reviews applications for charitable registration, potentially denying registration where a risk of terrorist financing abuse is identified. It regularly audits charities to ensure they continue to meet their registration obligations under the Income Tax Act and common law, taking administrative actions (ranging from education to a revocation of charitable status) in cases of non-compliance.

In 2019-20, to support the CRA's education first approach to charity compliance, the CRA-CD began reviewing its web content to better raise awareness within the charity sector of the risks of terrorist financing abuse and to provide practical advice to charities so they can mitigate any risks they may face. Consultations were conducted with members of the charity sector, including legal representatives, on proposed web content and the sector's needs for future CRA-CD outreach on terrorism issues. In 2019‑20, the CRA-CD identified 12 applications for charitable registration that required detailed assessments for risks of terrorist financing abuse, which is similar to the number of files identified in the three previous years. Through the assessment process, the CRA engaged with the applicants to educate them on relevant risks and possible mitigation measures they could adopt.

2.2 Compliance Assessments

FINTRAC

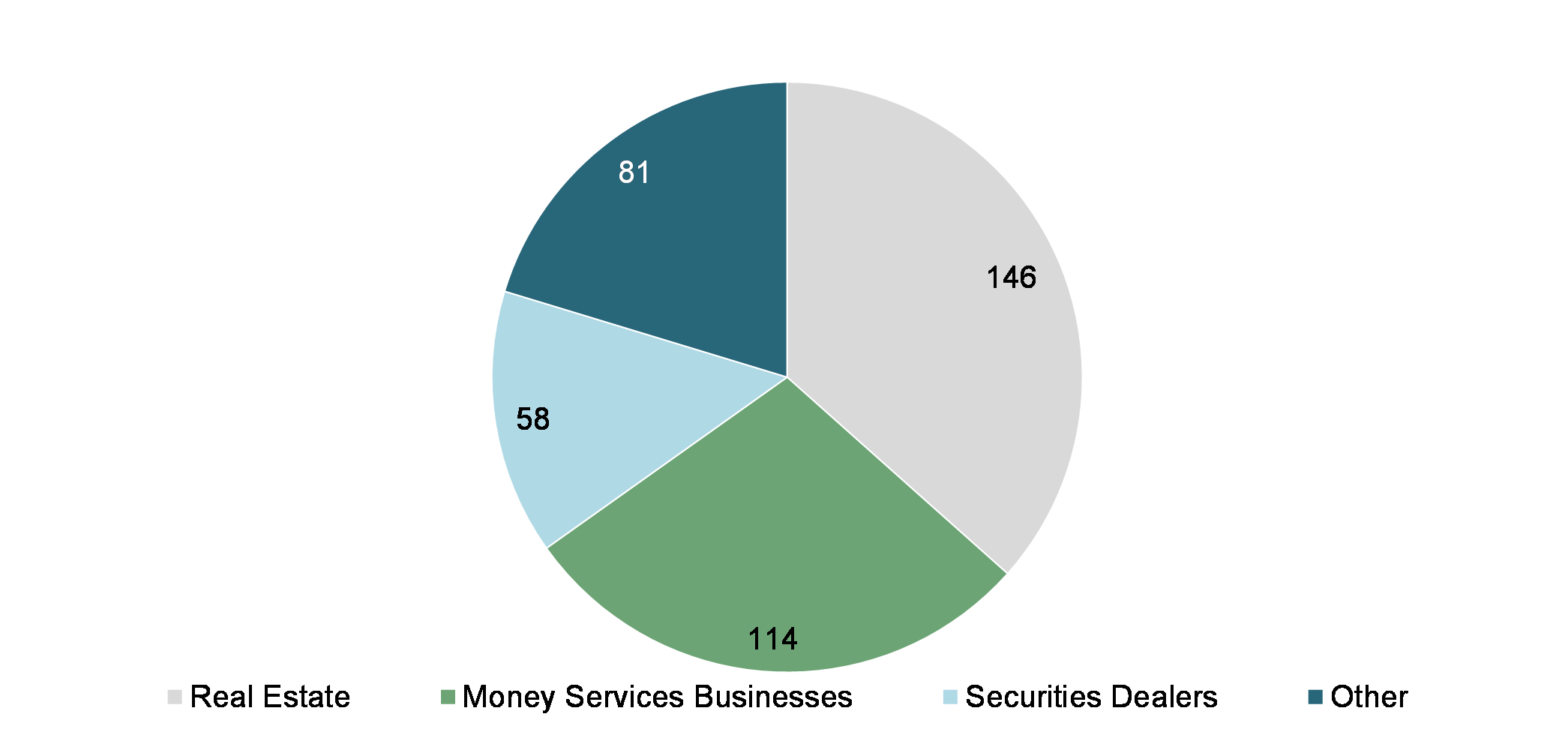

Examinations are one of FINTRAC's primary instruments for assessing the compliance of individuals and businesses subject to the PCMLTFA. With over 24,000 reporting entities estimated to exist in 2020, it would not be feasible for FINTRAC to examine every reporting entity annually. To maximize use of its compliance capacity, FINTRAC uses a risk-based approach, focusing a significant portion of its examination-specific resources on businesses that are at a higher risk of non-compliance. As of 2019-20, FINTRAC began the transition to assume full responsibility for conducting independent assessments of Canada's federally regulated financial institutions, a role formerly shared with the Office of the Superintendent of Financial Institutions (OSFI). Examinations targeted the real estate and money services business sectors, together accounting for nearly two-thirds of all 2019-20 assessments.

FINTRAC Examinations by Sector (2019-20)

FINTRAC examinations have trended downwards, from 684 in 2010-11 to 399 in 2019-20. The reduction of examinations reflects FINTRAC's evolution from using an audit to an assessment approach in its examinations. This revised approach is intended to focus less on technical compliance and more on the overall effectiveness of a reporting entity's compliance program, including the impact of non-compliance on achieving the objectives of the PCMLTFA and the Centre's ability to carry out its mandate. This transition from the audit to assessment approach allows for more complex, lengthy and in-depth examinations of larger businesses in higher-risk sectors, allowing FINTRAC to maximize its compliance resources.

FINTRAC Compliance Examinations

In addition, FINTRAC monitors the quality, timeliness and volume of the financial transaction reporting that it receives from businesses across the country. FINTRAC has invested in validating and monitoring reporting data, including improving its business processes to increase the effectiveness of its monitoring. In 2019-20, FINTRAC received a total of 31,364,164 financial transaction reports from businesses. The Centre rejected 131,747 reports for not meeting quality requirements. It accepted 347,351 financial transaction reports for which it subsequently issued a warning to businesses about the quality of those reports. Through this type of data monitoring, the Centre is better positioned to identify over-reporting, and delete from its database reports that should not have been received.

Although the vast majority of reporting entities work to comply with their PCMLTFA obligations, no sector is immune to compliance deficiencies and each faces its own unique challenges. Banks must monitor large volumes of clients and transactions while consistently applying AML/ATF policies and procedures across their operations. Casinos face a high proportion of one-time clients without ongoing business relationships, as well as anonymous transactions where there are no customer identification requirements until transaction thresholds are triggered. Due to the short lifespan and transient nature of some money services businesses (with some operating less than three years), FINTRAC must continuously identify money services businesses and conduct compliance examinations before they cease to operate. The real estate sector also represents a significant challenge, due to its high population, gaps in brokerages' awareness as to how they can be misused for ML/TF, and low (but rising) levels of suspicious transaction reporting.

As of April 2021, FINTRAC has taken full responsibility for PCMLTFA compliance examinations of federally regulated financial institutionsFootnote 11 from OSFI. FINTRAC will continue to develop business processes and build capacity as it assumes responsibility for all PCMLTFA-related activities in relation to these key reporting entities. Planned activities include conducting independent assessments, follow-ups and relationship management activities. In addition, FINTRAC will continue to work on recruiting and training individuals who will be responsible for the effective implementation of this initiative. FINTRAC will also seek to build capacity in understanding and assessing ML/TF risks in the virtual currency sector, a newly regulated sub-segment of the money services business sector very different from traditional reporting entities covered under the PCMLTFA.

CRA-Charities Directorate

As part of the ongoing efforts to mitigate the risk of terrorist financing abuse in the charitable registration system, the CRA conducts regulatory audits to ensure organizations continue to meet their obligations for registration under the Income Tax Act (ITA) and the common law. Where audits reveal non-compliance with the registration requirements, the CRA may apply a range of compliance measures set out in the ITA, including education letters, compliance agreements, sanctions and revocation of registration.

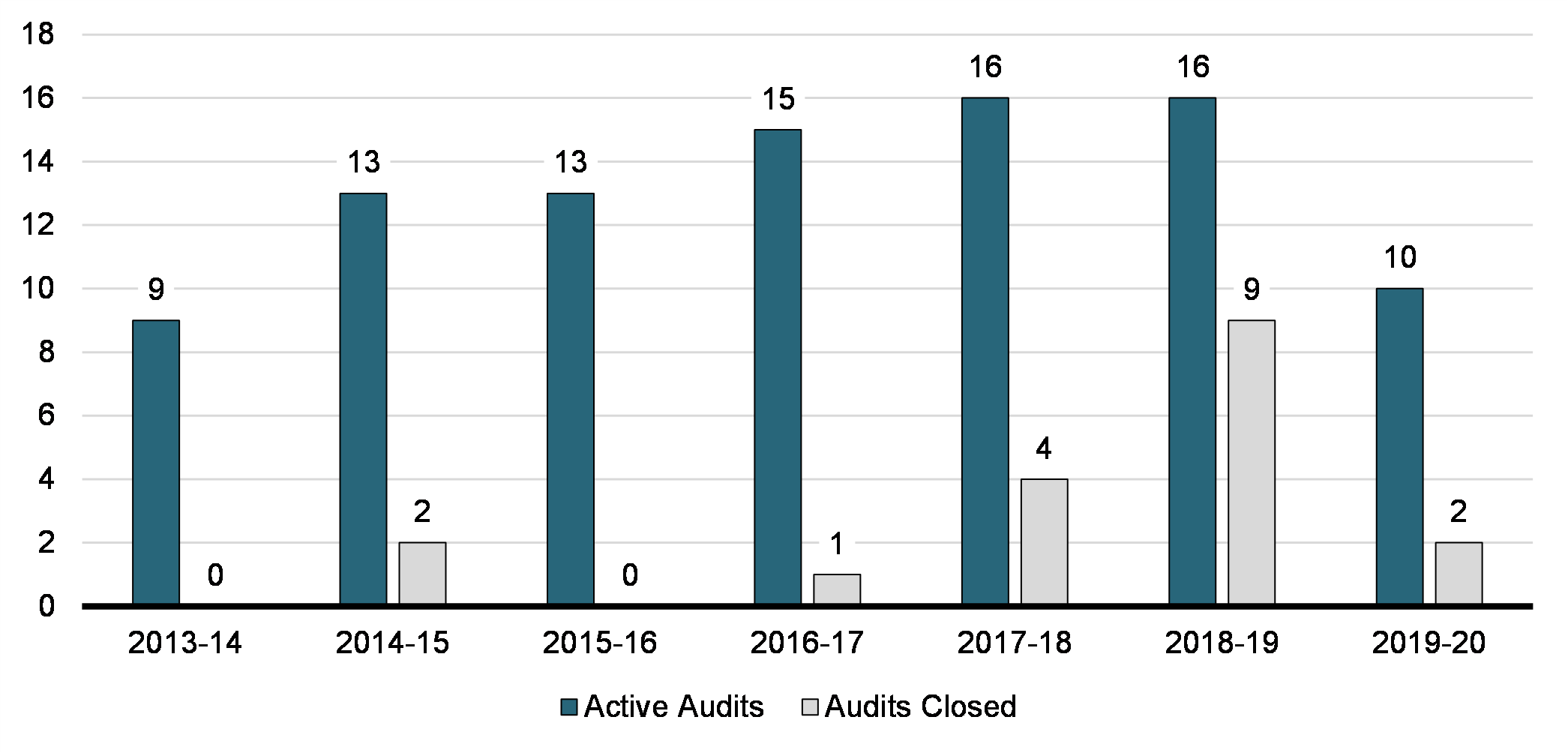

Number of Registered Charities Under Audit (CRA)

In 2019-20, the CRA had ten active audits open to ensure that charities identified as being at risk of terrorist financing abuse continued to meet their obligations for registration under the ITA and the common law. This number is lower than in the previous five years (where active audits numbered 13 to 16 in a year), because of significant efforts that were made in 2018-19 to close out a higher than average number of audits, many of which had been open for a long time. The CRA is continuing to develop in-house expertise to manage the risk of terrorist financing abuse present within the charitable sector and review the related audit program, developing efficiencies to further advance its mandate.

2.3 Remedial and Enforcement Measures

Where needed, FINTRAC uses a variety of enforcement tools to address non-compliance situations that it has identified. Among these tools are compliance meetings with reporting entities, findings letters and follow-up examinations to assess if previous non-compliance was addressed. Administrative monetary penalties may be issued in cases of serious or repeated non-compliance, and FINTRAC can also provide non-compliance disclosures to law enforcement in cases of extensive, criminal non-compliance.

Follow-up Examinations

Under its new compliance framework, FINTRAC conducted 44 follow-up examinations in 2019-20 (up from 19 the previous year), and identified improvement in compliance behaviour in more than 88 per cent of cases over the previous examination (up from 79 per cent). In instances where there was no improvement or a negative change in behaviour was observed, additional compliance and/or enforcement activities, such as administrative monetary penalties, were undertaken. This is a new indicator and thus too early to show any trends, but as only a proportion of reporting entities assessed in a given year are referred for follow-up examinations, most appear to demonstrate a satisfactory improvement in the level of PCMLTFA compliance and act readily to address known deficiencies.

Case Study 2.1: FINTRAC Follow-up Examination

An MSB was selected for a follow-up examination in 2019 due to significant gaps found in its compliance program that led to unreported transactions in the 2018 examination. The 2019 examination showed that the MSB's overall program was solid and that it had a good knowledge of the requirements that were needed. The MSB had made significant changes to its risk rating systems, one of which included a new technology that helped the organization assess client risk scoring. Although this examination found issues in some areas of the program, all the previous issues that were cited in 2018 were corrected, and the MSB showed commitment and willingness to comply. One of the major areas of concern in the previous examination was related to suspicious transaction reporting, where the organization was cited for unreported transactions. This examination only found one quality-related issue for suspicious transaction reporting. Furthermore, the MSB went from submitting zero suspicious transaction reports to FINTRAC up to ten during the scope period, thus showing a change in behaviour.

| Year | # of follow-up examinations | % where improvement in compliance behaviour identified |

|---|---|---|

| 2018-19 | 19 | 79.0 per cent |

| 2019-20 | 44 | 88.6 per cent |

Administrative Monetary Penalties

In 2008, FINTRAC received the legislative authority to impose administrative monetary penalties (AMPs) on businesses that are non-compliant with the PCMLTFA. Under the legislation, penalties are intended to be non-punitive and are focused on changing the non-compliant behaviour of businesses. The AMP program supports FINTRAC's mandate by providing a measured and proportionate response to particular instances of non-compliance. From 2010-11 to 2019-20, FINTRAC issued 84 notices of violations with a total value of $10.6 million.

Following two Federal Court decisions in 2016, FINTRAC initiated a review of its AMP program to ensure that it is one of the most open, transparent and effective AML/ATF penalty programs in the world. As part of this review, FINTRAC conducted extensive research and consultations with legal experts and stakeholders, as well as a thorough analysis of its broader assessment methodology in relation to examinations. FINTRAC completed this review in 2018–19 and published the revised AMP policy on its website in August 2019. The revised policy outlines clearly and transparently the penalty process and the new method of calculating penalties for non-compliance with the Act and associated Regulations. FINTRAC also developed and published a number of specific guides that describe its approach to assessing the harm done by the 200 violations prescribed in the Proceeds of Crime (Money Laundering) and Terrorist Financing Administrative Monetary Penalties Regulations, as well as its rationale in determining the corresponding penalty amounts.Footnote 12

Going forward, FINTRAC will continue to manage the revised AMP program as a means to encourage reporting entities to address deficiencies, and will continue to publish all AMPs that have been imposed as required under the Act since June 2019. By providing comprehensive information on the enhancements to the policy and penalty calculation methodology, FINTRAC wants to ensure that businesses will have a better understanding of its program and approach.

| Year | # of reporting entities subject to AMP | Total value of AMPs | # and type of reporting entities |

|---|---|---|---|

| 2019-20 | 2 | $239,250 | Real estate (1); MSB (1). |

| 2018-19 | 1 | $38,940 | MSB (1) |

| 2017-18 | 0 | $0 | |

| 2016-17 | 0 | $0 | |

| 2015-16 | 22 | $5,453,025 | Dealers in precious metals and stones (4); financial entities (8); life insurance (1); MSB (3); real estate (3); securities (3). |

| 2014-15 | 16 | $339,765 | Financial entities (6); MSB (5); real estate (4); securities (1). |

| 2013-14 | 16 | $2,237,025 | Casinos (2); financial entities (5); MSB (8); real estate (1). |

| 2012-13 | 13 | $636,290 | Financial entities (1); MSB (8); real estate (2); securities (2). |

| 2011-12 | 7 | $745,990 | Financial entities (2); MSB (3); securities (2). |

| 2010-11 | 7 | $927,330 | Casinos (2); financial entities (1); MSB (4). |

In 2019–20, FINTRAC issued two AMPs for non-compliance, one in the real estate sector and the other in the money services business sector, with a total value of $239,250. The resumption of AMPs is expected to make a more robust compliance regime by giving FINTRAC a broader scope of tools for responding to serious non-compliance.

Non-Compliance Disclosures

Lastly, under the PCMLTFA, FINTRAC may disclose cases of non-compliance to law enforcement when it is extensive or there is little expectation of immediate or future compliance. In recent years, FINTRAC has increased its outreach and awareness efforts with respect to non-compliance offences of the PCMLTFA, while law enforcement agencies have increasingly looked to utilize the non-compliance disclosure (NCD) tool to pursue criminal charges under the PCMLTFA. The significant growth in NCDs over the decade from very low levels does not reflect growing non-compliance by reporting entities, but rather increased law enforcement interest in making use of them, in the context of a greater focus on investigating and prosecuting financial crimes. On enforcement, FINTRAC will continue to focus on its new process of proactively disclosing non-compliance information to law enforcement, and on providing more information and outreach sessions on NCDs to address the enhanced interest from law enforcement.

FINTRAC Criminal Non-Compliance Disclosures

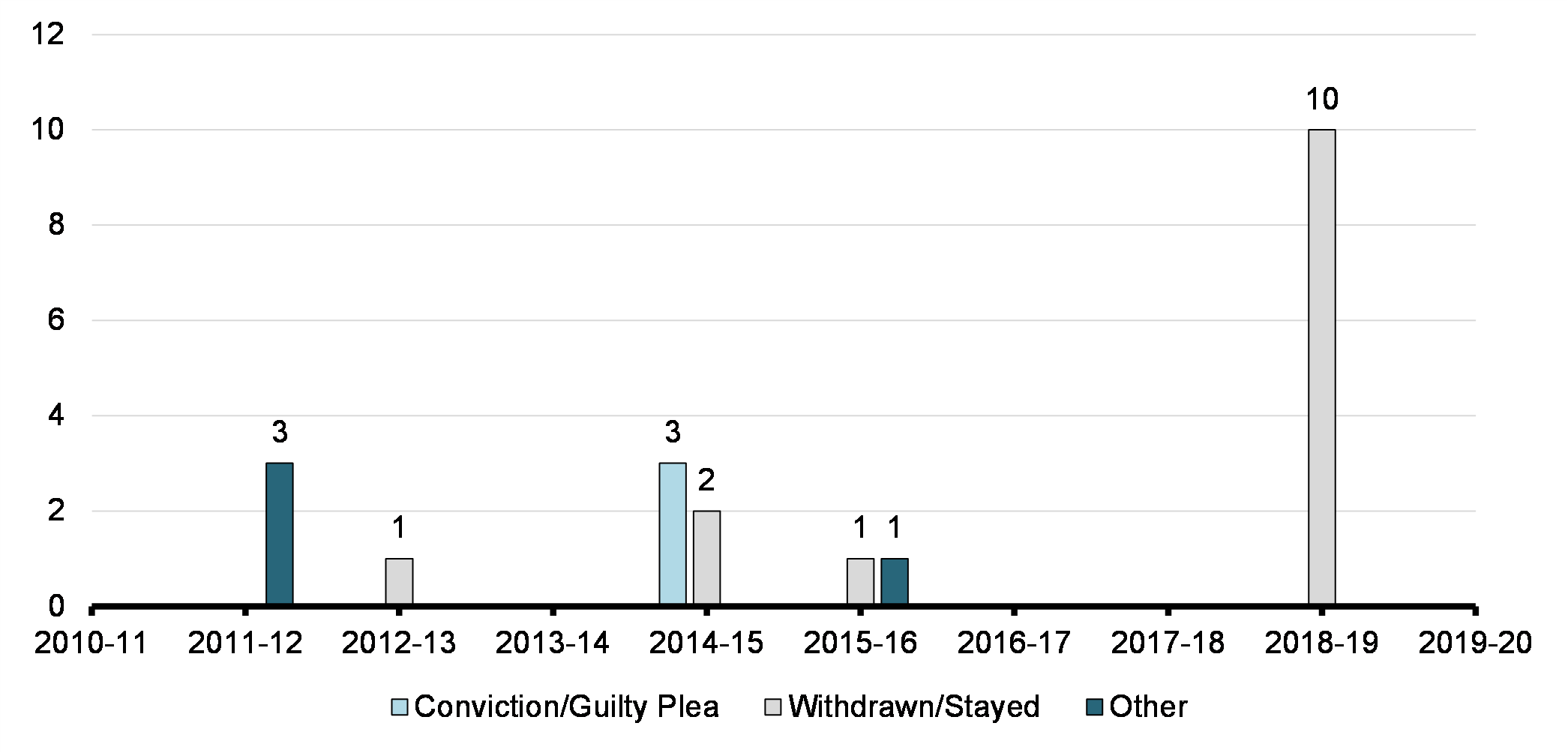

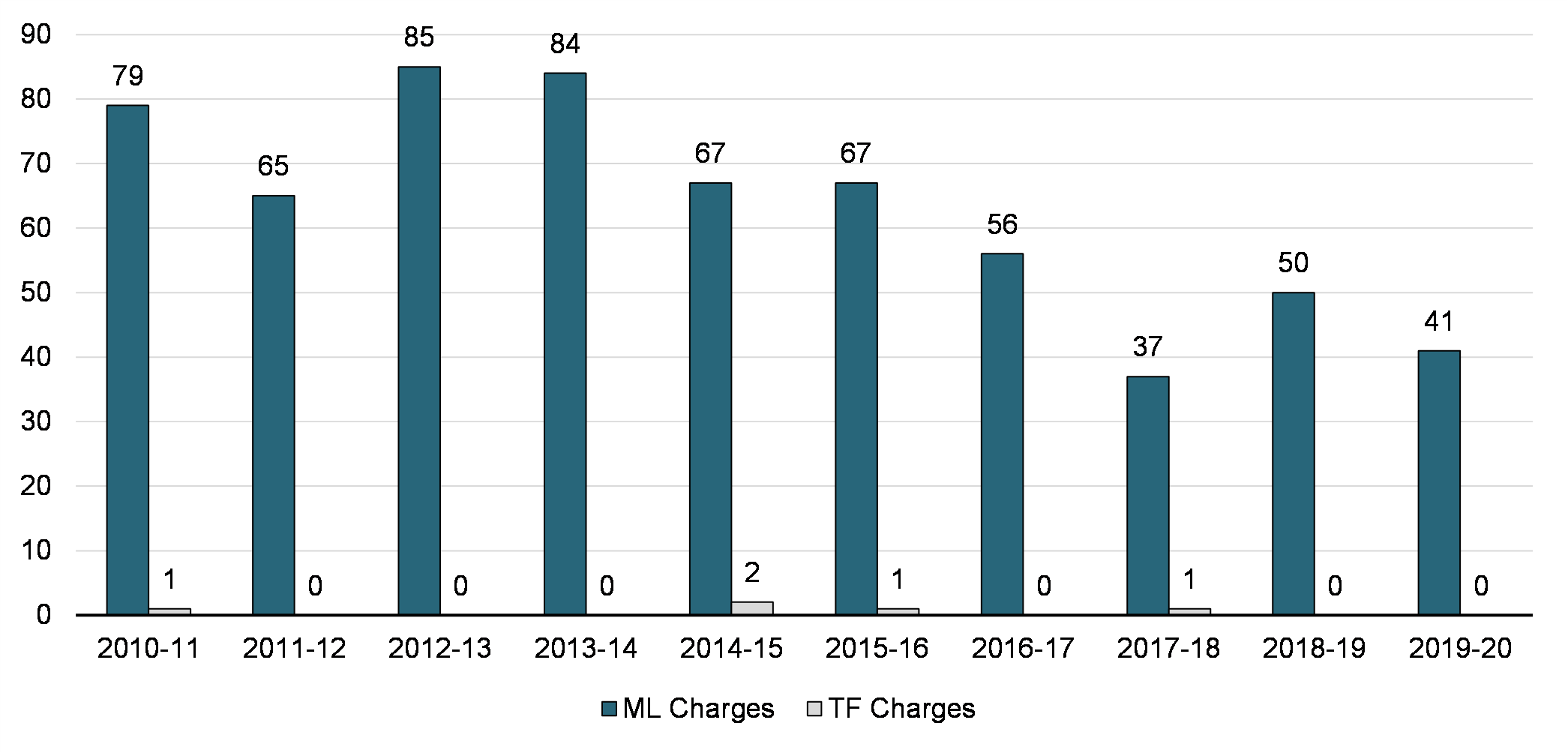

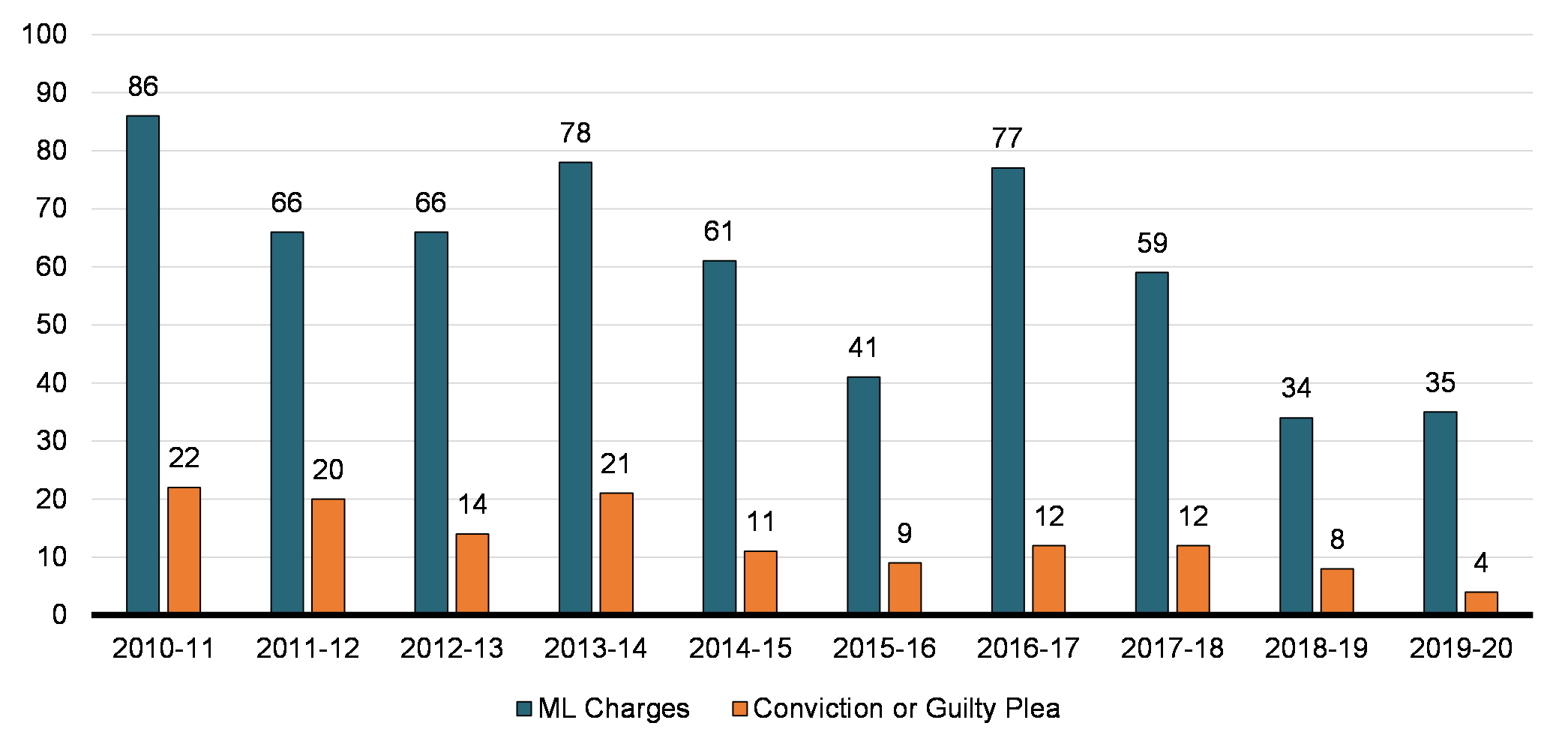

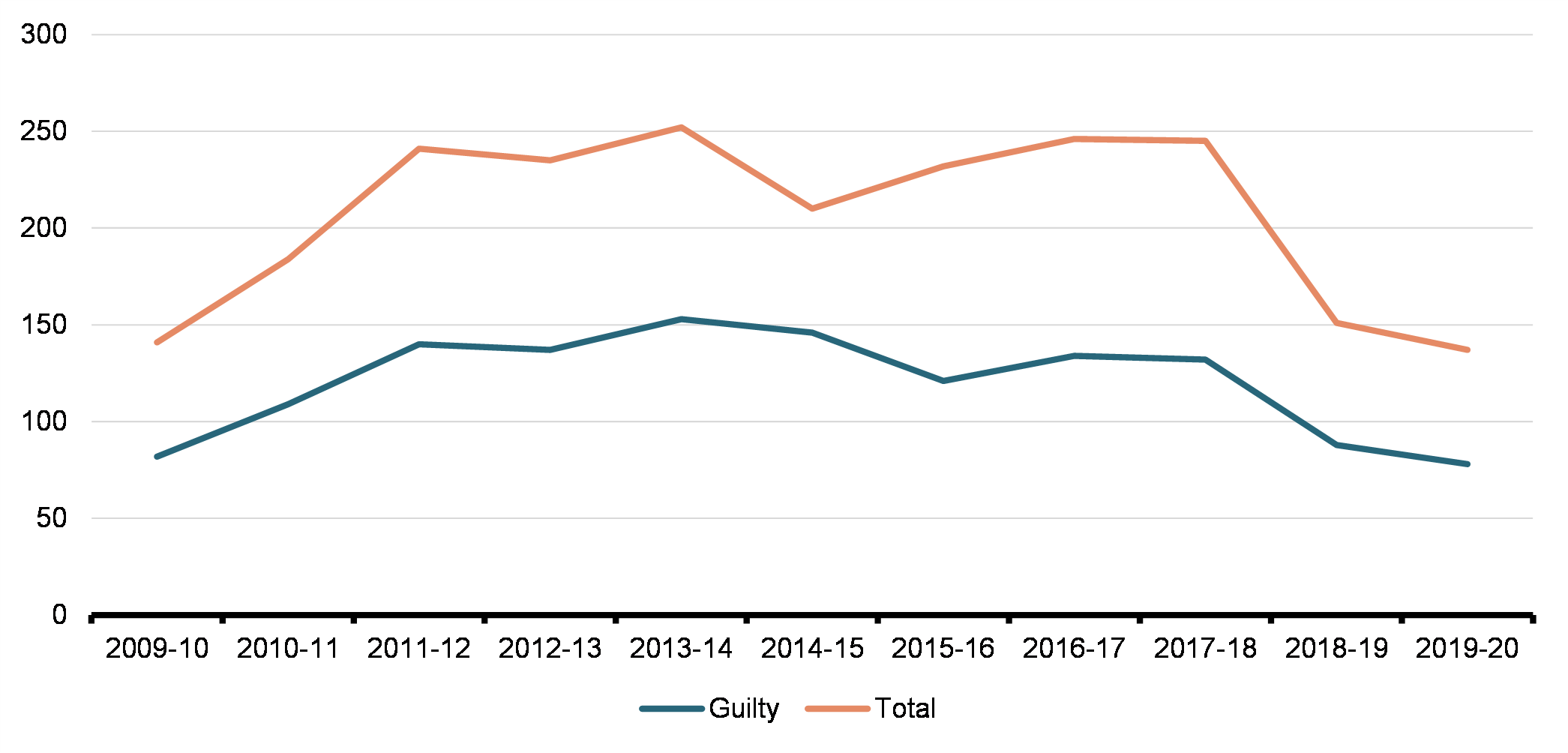

Despite the increase in law enforcement interest, NCDs have resulted in mixed enforcement results over the period up to 2019-20. The number of charges laid federally under the PCMLTFA has fluctuated year-over-year (as shown in Chart 2.5), but 2017-18 onward has seen a higher overall number of charges than in earlier years. Charges laid with respect to non-compliance offences have increased in 2019-20, although prosecution results remain low as there has not been a federal conviction or guilty plea on a PCMLTFA offence since 2014-15 (Chart 2.6). The increase in charges related to non-compliance offences can be attributed to the Royal Canadian Mounted Police (RCMP) starting to use PCMLTFA non-compliance charges as another investigative avenue. In 2019, the Canadian Integrated Response to Organized Crime (CIROC) decided to pursue PCMLTFA charges as an additional response to ongoing challenges in investigating ML.

Outcomes of Prosecuted PCMLTFA Charges

2.4 Discussion

The performance results for guidance and outreach, compliance assessments, as well as remedial and enforcement actions illustrate some of the key trends in AML/ATF compliance. Available data shows a sustained increase in outreach to make entities aware of their AML/ATF obligations. Although we cannot infer the direct impact of this outreach and guidance on compliance, effectiveness can be assessed through examination results and follow-up actions, as well as through feedback by reporting entities to support continuous improvement. While FINTRAC conducts fewer examinations than in previous years, this largely stems from a change in its assessment approach towards effectiveness-based examinations. This allows for more targeted and in-depth assessments and improves the likelihood of detecting root causes of deficiencies, and the linkages among them. Entities which may not have their compliance programs examined in a given year may still receive welcome letters, education, outreach and other engagement. FINTRAC will continue using its robust enforcement mechanism for addressing cases of serious or chronic non-compliance where identified and where outreach or follow-ups are insufficient, such as administrative penalties. It will also assess the effectiveness of its administrative monetary penalties in promoting compliance. Criminal non-compliance disclosures are on the rise, with increased enforcement interest in making use of them and charges being laid. Nonetheless, actual convictions for offences of the PCMLTFA over the reporting period have been limited.

Result #3: Stakeholders receive timely and relevant intelligence on suspected ML/TF

3.1 Tactical Intelligence

As Canada's financial intelligence unit (FIU), FINTRAC receives, analyzes, and assesses reports and information from various sources, including reporting entities, to assist in the detection, prevention, and deterrence of money laundering and terrorist financing, as well as threats to the security of Canada.

Transaction Reporting

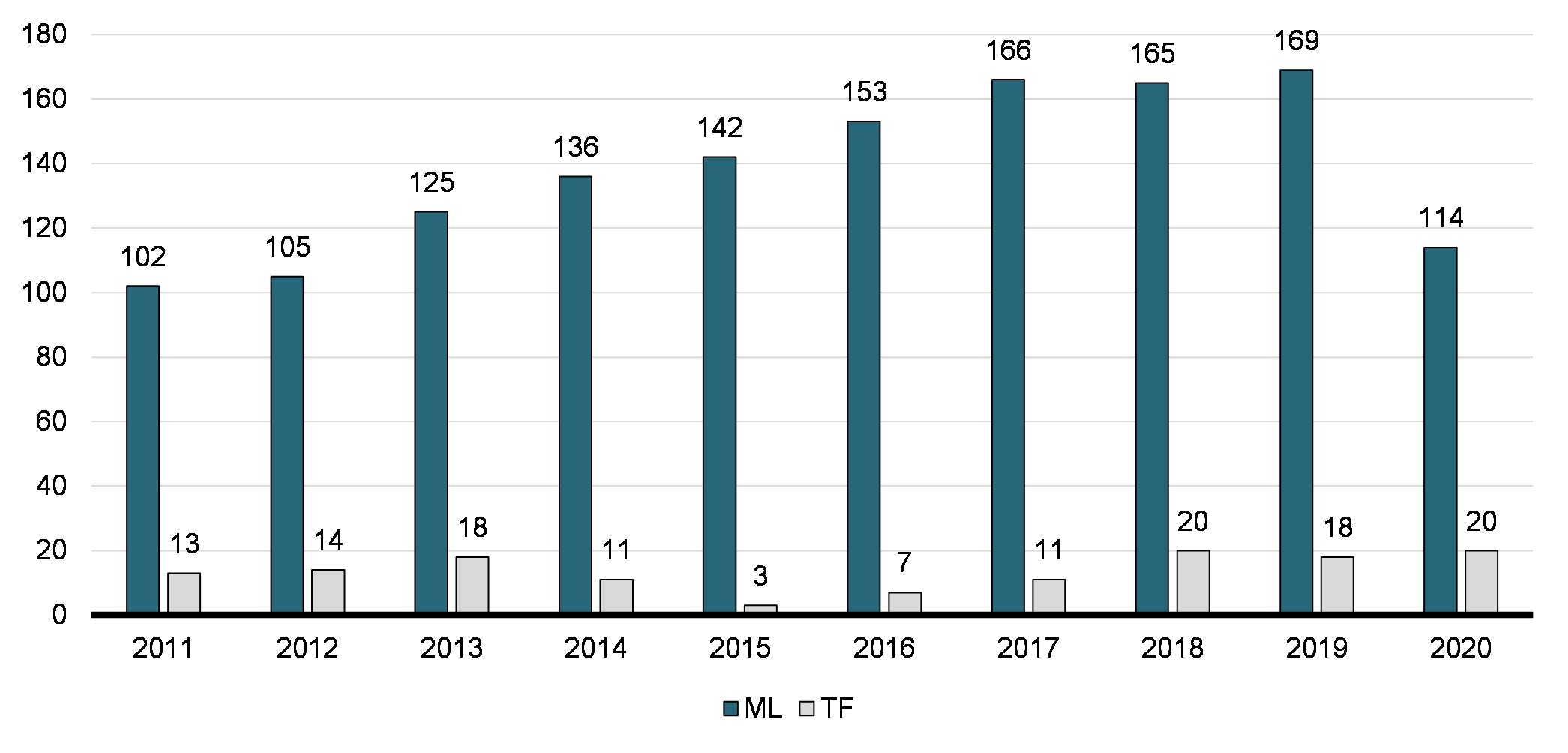

FINTRAC uses the transaction data it obtains from reporting entities as a major source of information, which it combines with other elements for generating intelligence disclosures to its partners. The vast majority of this volume consists of reports that entities must file when certain thresholds are met. This includes large cash transactions, international electronic funds transfers and casino disbursements, all at over $10,000 within a 24-hour period. With the exception of the latter, these primarily originate from financial institutions. A significant amount of information of potential intelligence value comes from suspicious transaction reports (STRs), which must be filed if there are reasonable grounds to suspect that a transaction or attempted transaction is related to the commission or the attempted commission of an ML/TF offence. Unlike all other reporting obligations, there is no monetary threshold associated with the reporting of a suspicious transaction. Timely and useful STRs from reporting entities are a necessary source of information for countering sophisticated illicit actors who may structure their transactions to evade threshold reporting requirements.

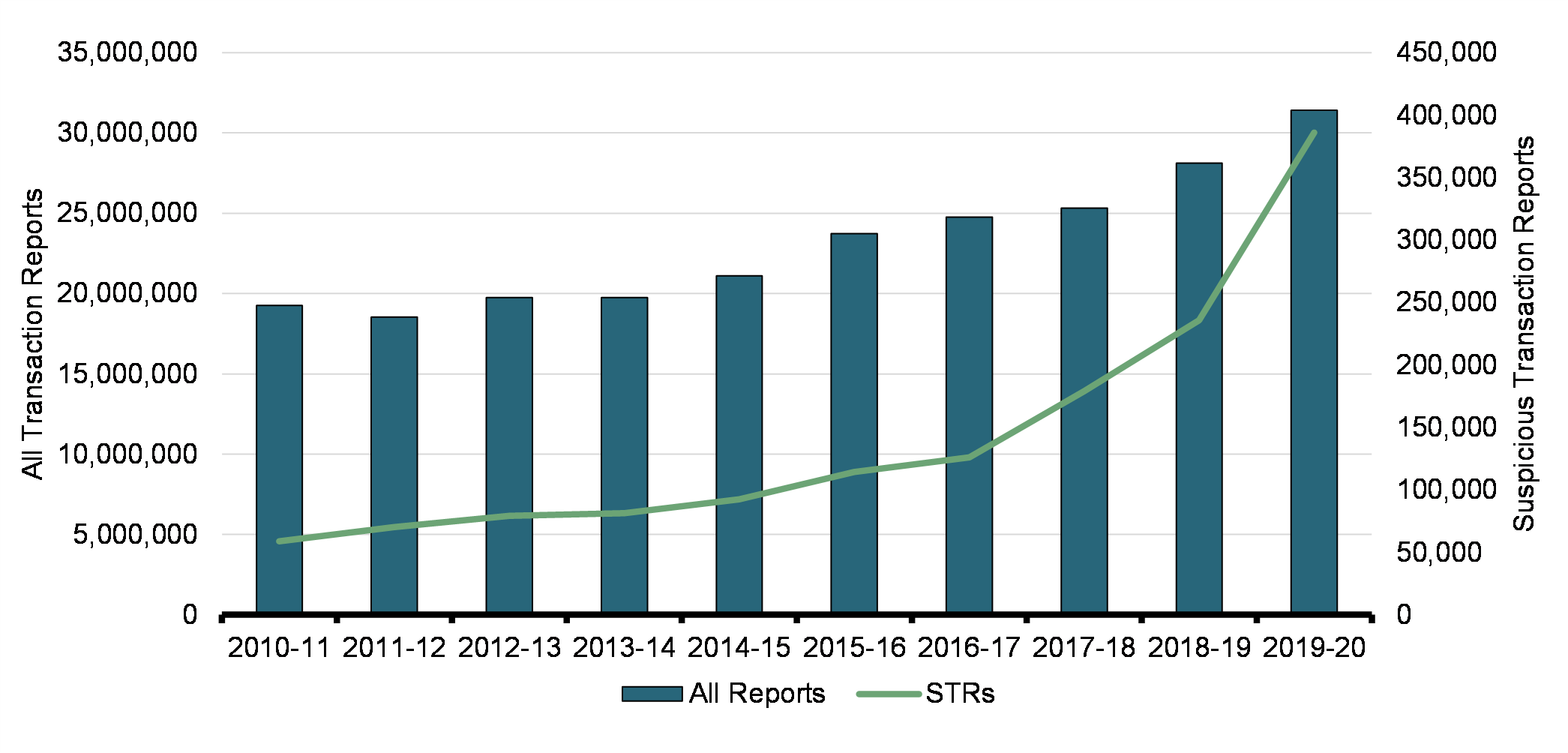

All Transaction Reports to FINTRAC

As shown in the above chart, the total volume of reports received by FINTRAC has grown by over 50 per cent over the past ten years, while STRs increased nearly eight-fold. This trend potentially represents increased awareness of the STR reporting obligation by traditionally under-reporting sectors, such as money services businesses and real estate. Improved guidance to reporting entities on their reporting obligations, as well as the publication of Operational Alerts and Briefs, and Special Bulletins advising entities what "red flags" to look for in spotting and reporting a suspect transaction, likely contribute to this change. There remain potential blind spots in certain sectors, such as the legal profession, which are vulnerable to misuse for ML/TF but are not subject to reporting requirements under the PCMLTFA. FINTRAC also receives some duplicate STR reporting due to limitations in certain transaction reporting systems. Nonetheless, more quality reporting from a broader array of sources should be seen as improving the information available to FINTRAC.

Intelligence Disclosures

When FINTRAC's analysis meets specific legal thresholds set out in the PCMLTFA, it discloses this financial intelligence to the appropriate law enforcement and national security agencies named in the Act. FINTRAC can only disclose certain identifying information set out in the PCMLTFA and Regulations. Disclosure recipients can also provide voluntary information records to FINTRAC about suspected money laundering or terrorist financing activities, which help to inform FINTRAC's analytical work although FINTRAC must reach its threshold to disclose in those situations as well. While law enforcement agencies in other jurisdictions may be able to access their FIU information directly, direct access to FINTRAC's financial intelligence by disclosure recipients is limited by the

Canadian Charter of Rights and Freedoms.

Often based on hundreds or even thousands of financial transactions, FINTRAC's financial intelligence disclosures may show links between individuals and businesses that have not been identified in an investigation, and may help investigators refine the scope of their cases or shift their sights to different targets. A disclosure can pertain to an individual or a wider criminal network, and can also be used by police and law enforcement to put together affidavits to obtain search warrants and production orders. FINTRAC's financial intelligence is also used to identify assets for seizure and forfeiture, reinforce applications for the listing of terrorist entities, negotiate agreements at the time of sentencing and advance the Government of Canada's knowledge of the financial dimensions of threats, including organized crime and terrorism.

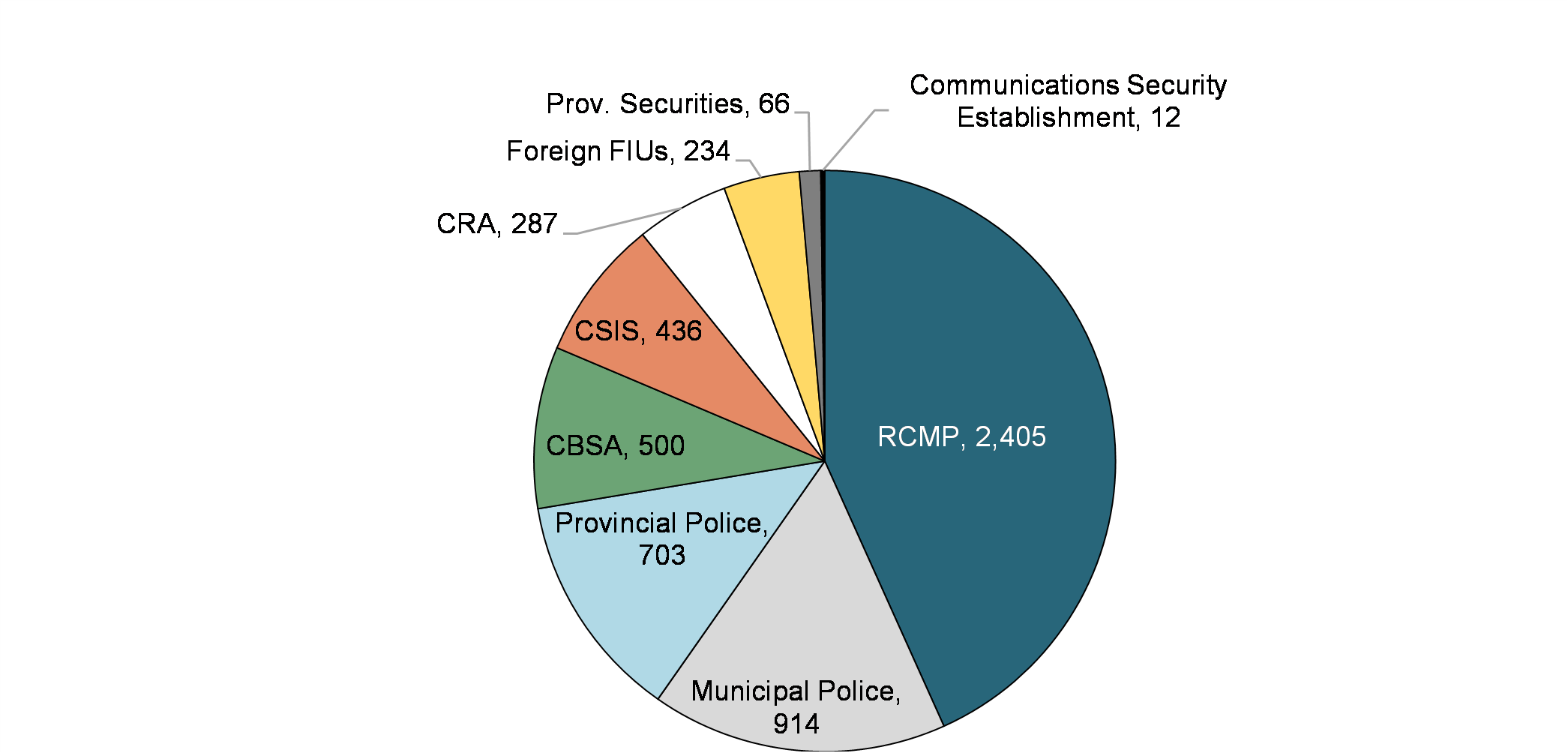

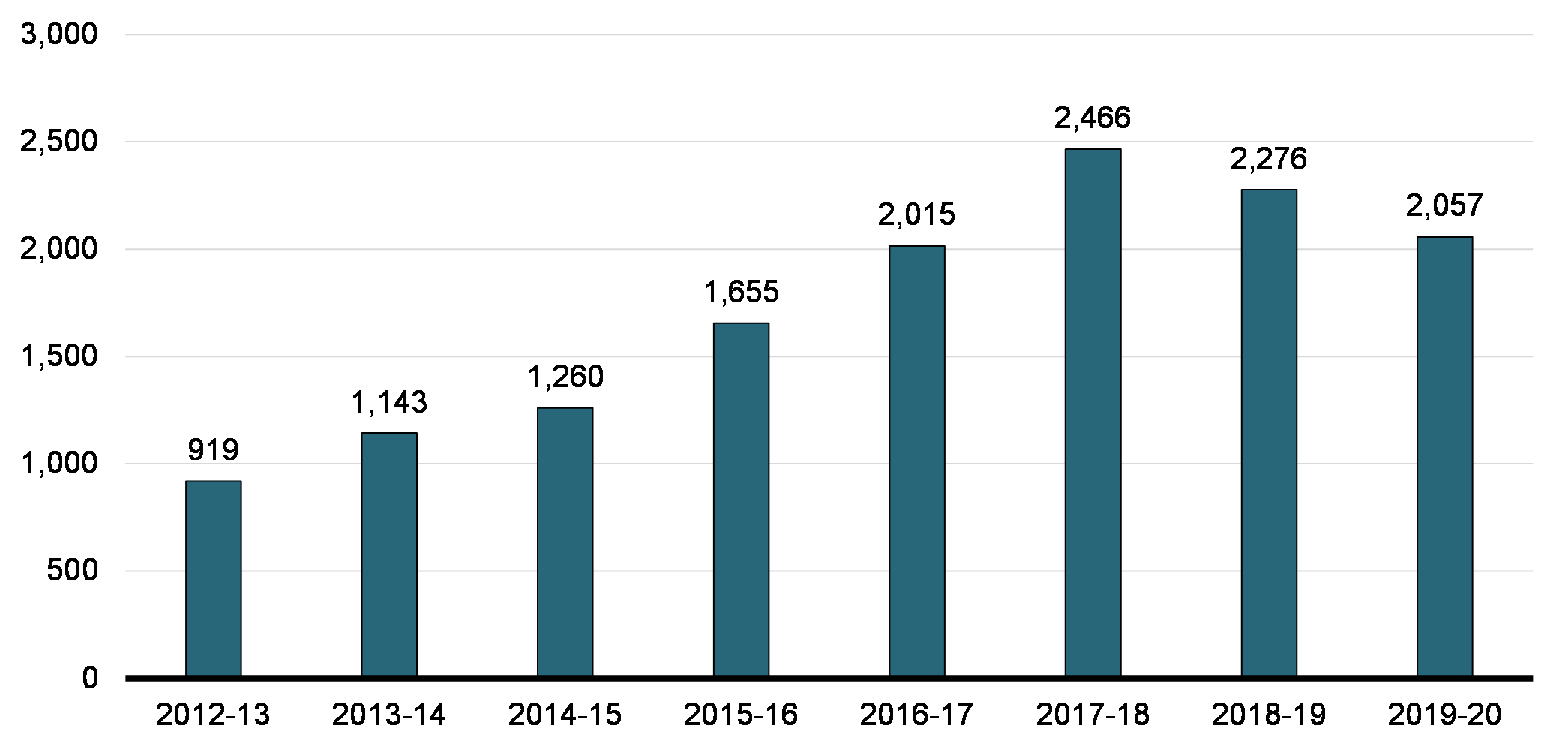

FINTRAC tracks the number of unique case disclosures it provides to disclosure recipients (a disclosure may be shared with multiple agencies). The growing list of financial intelligence recipients includes Canadian federal, provincial and municipal police forces, the CRA, Canada Border Services Agency (CBSA), Canadian Security Intelligence Service (CSIS), Revenu Québec and provincial securities regulators. It also includes foreign FIUs, which are foreign agencies with powers and duties similar to those of FINTRAC. In 2019–20, FINTRAC provided 2,057 unique disclosures of actionable financial intelligence to its Regime partners. Of these, 1,582 were related to money laundering, 296 were related to terrorist financing and threats to the security of Canada, and 179 were related to money laundering, terrorist financing and threats to the security of Canada. The top three predicate crimes related to case disclosures were drugs (31 per cent), followed by fraud (30 per cent) and tax evasion (14 per cent). FINTRAC continued to generate financial intelligence after emergency measures and restrictions were enacted to stop the spread of COVID-19. As shown in the chart below, the RCMP and, to an extent, other Canadian police forces, are the main beneficiaries of FINTRAC disclosures. Revenu Québec and the Competition Bureau were added as disclosure recipients in 2019-20.

FINTRAC Disclosure Packages by Recipient (2019-20)

Between 2012-13 (when FINTRAC began tracking unique disclosures) and 2017-18, the number of FINTRAC disclosures had more than doubled from 919 to 2,466. The volume declined in subsequent years but remained elevated in 2019-20. The growing number of disclosures reflects a number of factors: FINTRAC's requirement to disclose when the legislative threshold is met; the expansion of disclosure recipients; increases to FINTRAC's operational capacity; and the increased volume of information obtained by FINTRAC, particularly from reporting entities. The majority of disclosures are provided in response to voluntary information records submitted by disclosure recipients, with a minority of disclosures being proactive.

Number of Unique FINTRAC Intelligence Disclosures

Use of Intelligence Disclosures by Recipients

Although FINTRAC generates a considerable volume of intelligence disclosures, which more than doubled since 2012-13, the use of FINTRAC intelligence disclosures by its disclosure recipients is more difficult to measure. As noted earlier, a disclosure can have multiple uses, but the greatest value comes from disclosures that directly contribute to criminal investigations. These contributions could take the form of leads provided to support ongoing files (such as in response to a voluntary information record), or proactive disclosures resulting in the opening of new investigations.

FINTRAC Contributions to Project-level Investigations

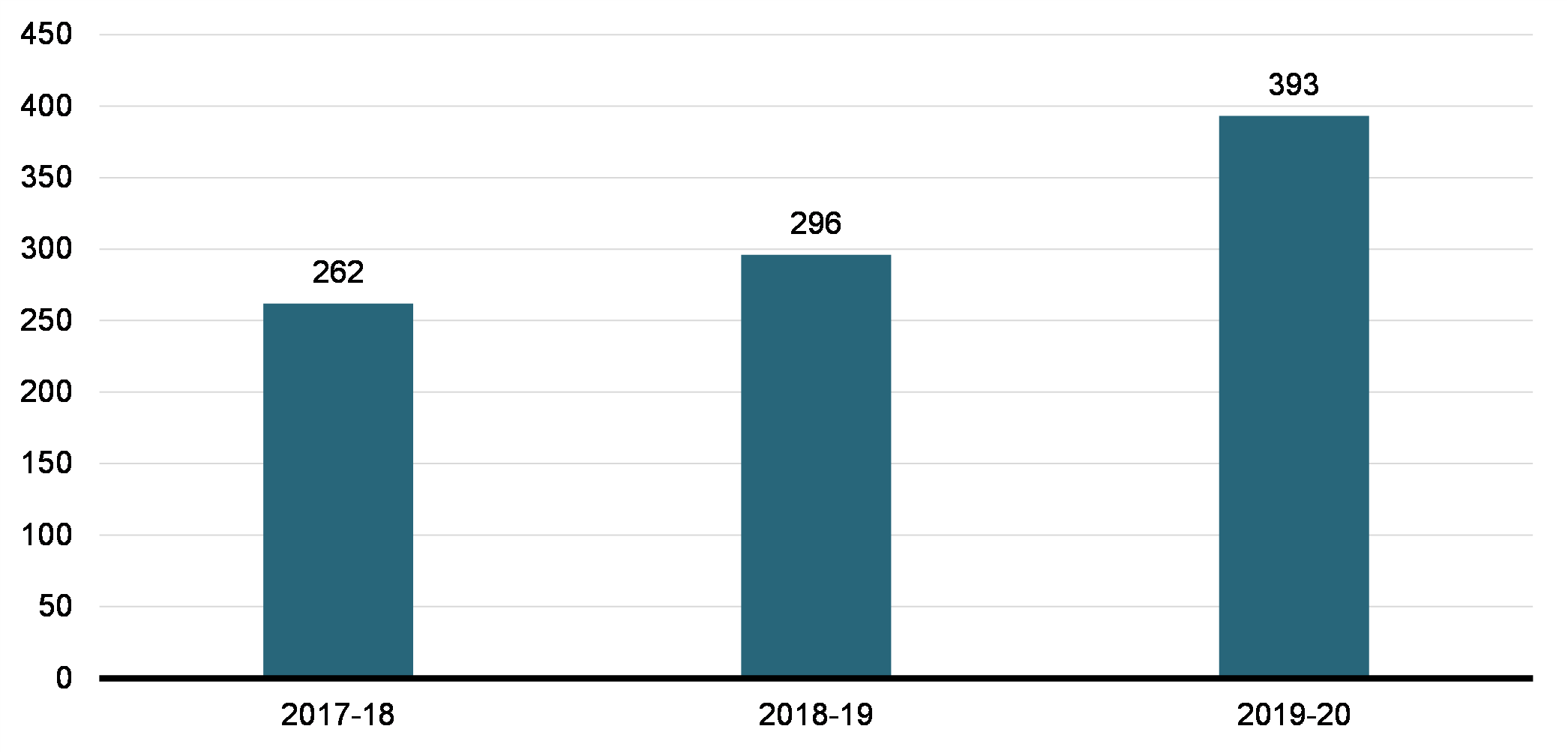

In recent years, FINTRAC has begun tracking the contribution of its disclosures to law enforcement more directly. Throughout 2019–20, FINTRAC's financial intelligence contributed to 393 project-level police investigations at the municipal, provincial and federal levels across the country, up from 296 in 2018-19 and 262 in 2017-18. FINTRAC's financial intelligence was used in a wide variety of money laundering investigations, where the origins of the suspected criminal proceeds were linked to drug trafficking, fraud, tax evasion, corruption, theft, and other criminal offences. This indicator demonstrates that, while working at arm's length from law enforcement partners, FINTRAC is contributing to their highest value, and most resource-intensive, investigations.

Case Study 3.1: Intelligence Contributions

FINTRAC's financial intelligence was used in a wide variety of counter-terrorism investigations. In one instance, FINTRAC was recognized publicly for its contributions in preventing the facilitation of a terrorist activity (SALENTO). FINTRAC has also prioritized public-private sector partnerships (PPPs) to improve the use of financial intelligence in combatting money laundering in British Columbia and across Canada, human trafficking in the sex trade, romance fraud, and the trafficking of illicit fentanyl.

As noted earlier, the RCMP receives a significant number of proactive FINTRAC disclosures annually, which are assessed by the divisions or National Headquarters depending on the transactions and summary of disclosure. The RCMP cannot assess every single disclosure, but all are held for intelligence purposes, with the major ones potentially actioned by analysts and investigators across the country. The RCMP also frequently receives disclosures following the submission of voluntary information records to FINTRAC, which play an important role in furthering ongoing money laundering investigations.

FINTRAC disclosures resulting from voluntary information records are essential to enhancing criminal intelligence, developing intelligence probes, and supporting ongoing financial crime investigations. They provide information that directly supports the development of criminal intelligence and ongoing investigations. This includes potentially expanding the scope of an investigation, or changing its direction, in addition to aiding investigative processes such as production orders. A FINTRAC disclosure can potentially highlight where a subject of interest conducts their banking, which provides law enforcement with information in support of judicial authorizations. Although the RCMP does not track how many law enforcement investigations are generated by FINTRAC disclosures each year, the RCMP has generated tiered (high priority) files solely on FINTRAC disclosures. Such files have a significant impact on public safety and economic integrity in Canada.

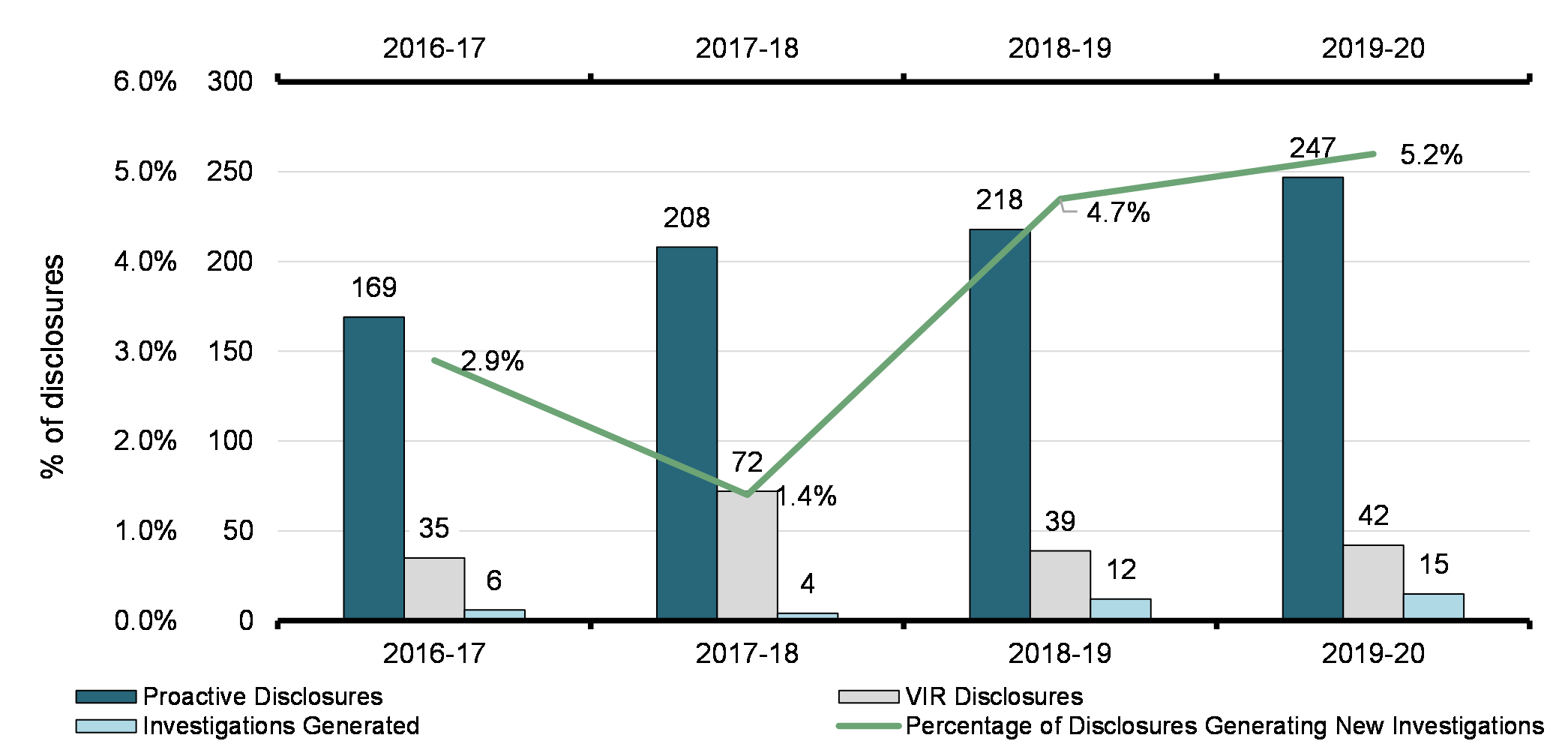

The CRA Criminal Investigations Directorate (CID) also tracks the use of FINTRAC disclosures to its cases. The CID reviews every disclosure it receives from FINTRAC for potential tax evasion or fraudulent activity. If the CID determines that there is potential for a criminal investigation, it refers the disclosure to one of its six regional offices for further analysis. The CID also shares financial information with FINTRAC through voluntary information records (VIRs), when a case is being reviewed or when it has been accepted for criminal investigation, including details used to identify additional subjects, relationships between subjects, and new bank accounts. Only about 1-5 per cent of disclosures received by the CID in a given year result in the initiation of an investigation, often due to resourcing constraints faced by law enforcement. However, significantly more investigations were generated in 2018-19 and 2019-20, compared with previous years since tracking by the CRA began.Footnote 13

Contributions of FINTRAC Disclosures to CRA Criminal Investigations

To apply for a production order or search warrant in cases where tax evasion comprises the predicate crime to money laundering, the CRA must demonstrate that they have reasonable grounds to believe that the information sought will afford evidence of these activities. Although FINTRAC disclosures provide relevant intelligence, especially when combined with tax information held by the CRA, it may not prove sufficient to meet the legal threshold necessary to pursue an investigation. When this occurs, the CRA will retain the intelligence until it can obtain sufficient data to meet such requirements in order to pursue an investigation. The referrals provided by FINTRAC are also a source of quality information that can be used for intelligence purposes in identifying offshore tax avoidance and evasion trends, and to inform future risk assessment criteria and compliance actions.

3.2 Strategic Intelligence

Products and Contributions

FINTRAC researches trends and developments in ML/TF to inform reporting entities, law enforcement authorities, and the public on the nature and extent of ML/TF domestically and internationally. Among the products they provide are Operational Briefs, which give clarification and guidance on issues that influence the ability of reporting entities to maintain a strong compliance regime; and Operational Alerts, which provide up-to-date indicators of suspicious financial transactions and high-risk factors related to new, re-emerging or particularly topical methods of money laundering and terrorist financing. These Alerts help reporting entities identify and submit suspicious transaction reports to FINTRAC.

In 2019–20, FINTRAC produced six strategic financial intelligence assessments and reports and contributed its financial intelligence insight and expertise to numerous other regime partner projects. The majority of FINTRAC's strategic intelligence was focused on ML/TF methods and mechanisms, including assessments of the financial flows involving jurisdictions that are at a high risk of money laundering. Whether a jurisdiction poses a high-risk for ML and/or TF can vary depending on their circumstances. Contributing factors can include (among other things) their level of corruption, the prevalence of particular crimes in their region, deficiencies in their AML/ATF regime, the presence of active terrorist groups, being listed in the advisories of competent authorities such as the FATF or FINTRAC, or being subject to economic sanctions, embargoes, or other special economic measures.

FINTRAC also provided strategic intelligence to assist Canadian businesses in understanding the potential risks and vulnerabilities in their sectors and in complying with their obligations under the PCMLTFA. This included publishing an Operational Alert related to the laundering of proceeds of crime through a casino-related underground banking scheme, as well as an Operational Brief regarding the risks and indicators for dealers in precious metals and stones. FINTRAC also developed money laundering indicators to assist money services businesses and foreign money services businesses dealing in virtual currency to report on virtual currency transactions beginning in June 2020.

FINTRAC also provided strategic intelligence to assist Canadian businesses in understanding the potential risks and vulnerabilities in their sectors and in complying with their obligations under the PCMLTFA. This included publishing an Operational Alert related to the laundering of proceeds of crime through a casino-related underground banking scheme, as well as an Operational Brief regarding the risks and indicators for dealers in precious metals and stones. FINTRAC also developed money laundering indicators to assist money services businesses and foreign money services businesses dealing in virtual currency to report on virtual currency transactions beginning in June 2020.

The Value of Strategic Intelligence

FINTRAC-produced Operational Alerts have shown significant value through various PPPs, including Projects Protect, Chameleon and Guardian. They allow financial institutions to align their suspicious transaction reporting and other AML activities with Canadian operational priorities, ultimately enhancing resource allocation and public safety. FINTRAC strategic intelligence products may advance investigations by providing credible indicators of money laundering.

Operational Alerts also provide valuable intelligence on money laundering trends in Canada. Intelligence contained within Operational Alerts have been used to identify Canadian money laundering threats for national intelligence purposes which can be shared with international partners such as the Five Eyes Law Enforcement Group, and enable the development of intelligence probes based on FINTRAC's indicators. Trends and methods provided by FINTRAC are used to brief public and private Regime partners on developing threats. These products can also be used for outreach and awareness for vulnerable sectors such as real estate and gaming.

The CRA, which receives financial intelligence based on a dual threshold of tax evasion and money laundering in support of its criminal investigations program, finds that FINTRAC disclosures have been providing increasingly higher quality and value over the years. The reports have also provided valuable insight into Canada's evolving national security threat environment to the CRA.

3.3 Discussion

FINTRAC continues to benefit from an increasing volume of transaction reporting by reporting entities, including a rapid year-over-year increase in suspicious transaction reports, which could be turned into actionable tactical and strategic intelligence for disclosure recipients. FINTRAC generates a considerable volume of intelligence disclosures (see Chart 3.3), both proactively and in response to voluntary information records, more than doubling since 2012-13 but trending downwards in recent years in favour of fewer but more impactful disclosures. Disclosure recipients benefit from FINTRAC disclosures in a variety of ways, although the extent of the value they provide cannot currently be broadly measured. Available statistics from the CRA suggest that only a small proportion of proactive disclosures may result in the initiation of a new investigation, relative to "reactive" disclosures provided following voluntary information records. There is also a correlation between the increasing number of project-level investigations supported and the increasing complexity of FINTRAC disclosures. Strategic intelligence is a crucial supplement to tactical intelligence in improving the overall understanding by agencies and reporting entities of ML/TF trends and methods.

The Third Pillar: Investigation and Disruption

The third pillar of the Regime, investigation and disruption, deals with enforcement action to investigate and prosecute money laundering and terrorist financing, while recovering the illicit proceeds of these activities. Regime partners, such as CSIS, the CBSA, the CRA, and the RCMP, conduct intelligence work and undertake investigations in relation to money laundering, terrorist financing, other financial crimes, and threats to the security of Canada in accordance with their individual mandates. The CRA also plays an important role in investigating and prosecuting tax evasion (and associated money laundering) and in detecting charities that are at risk, to ensure that they are not being used to finance terrorism.

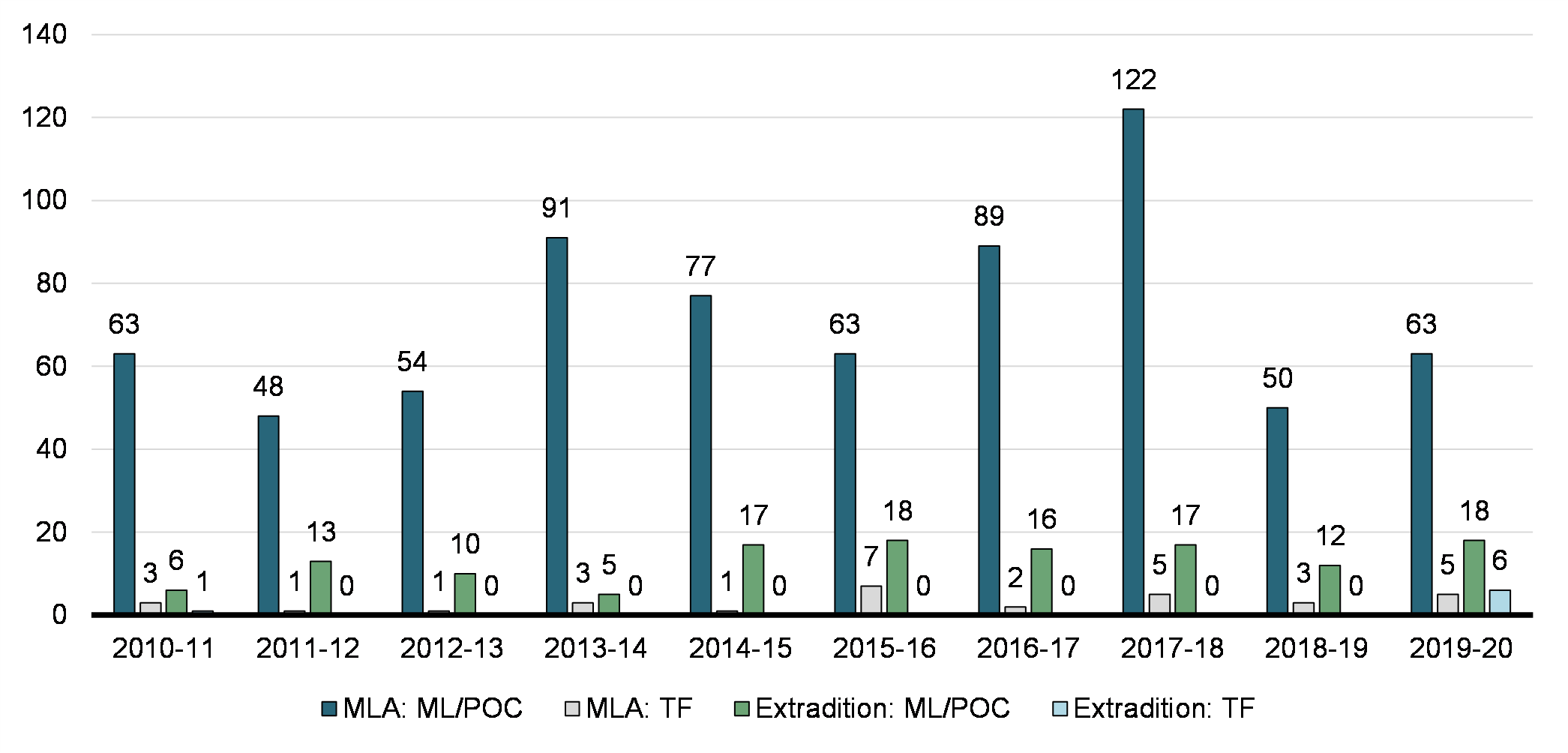

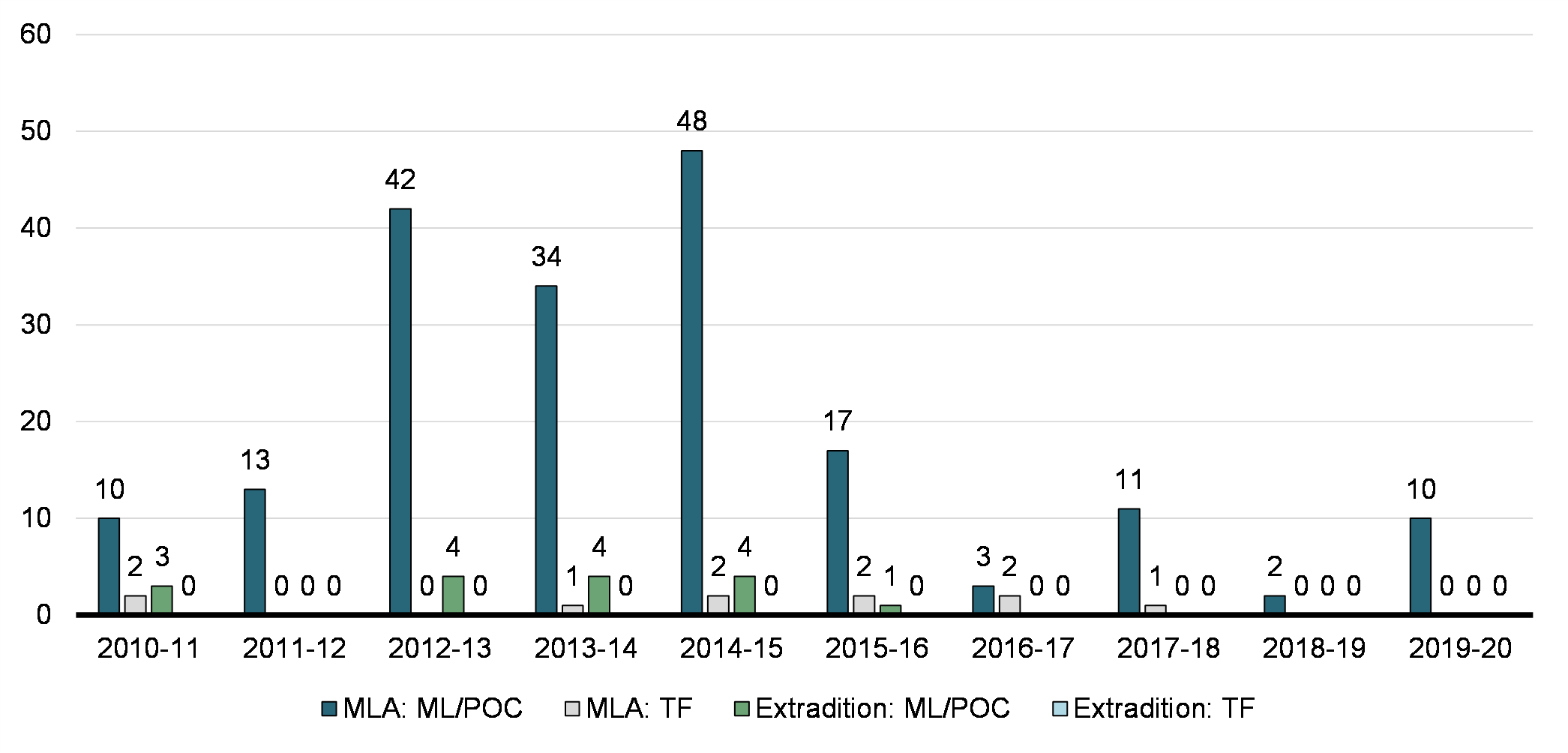

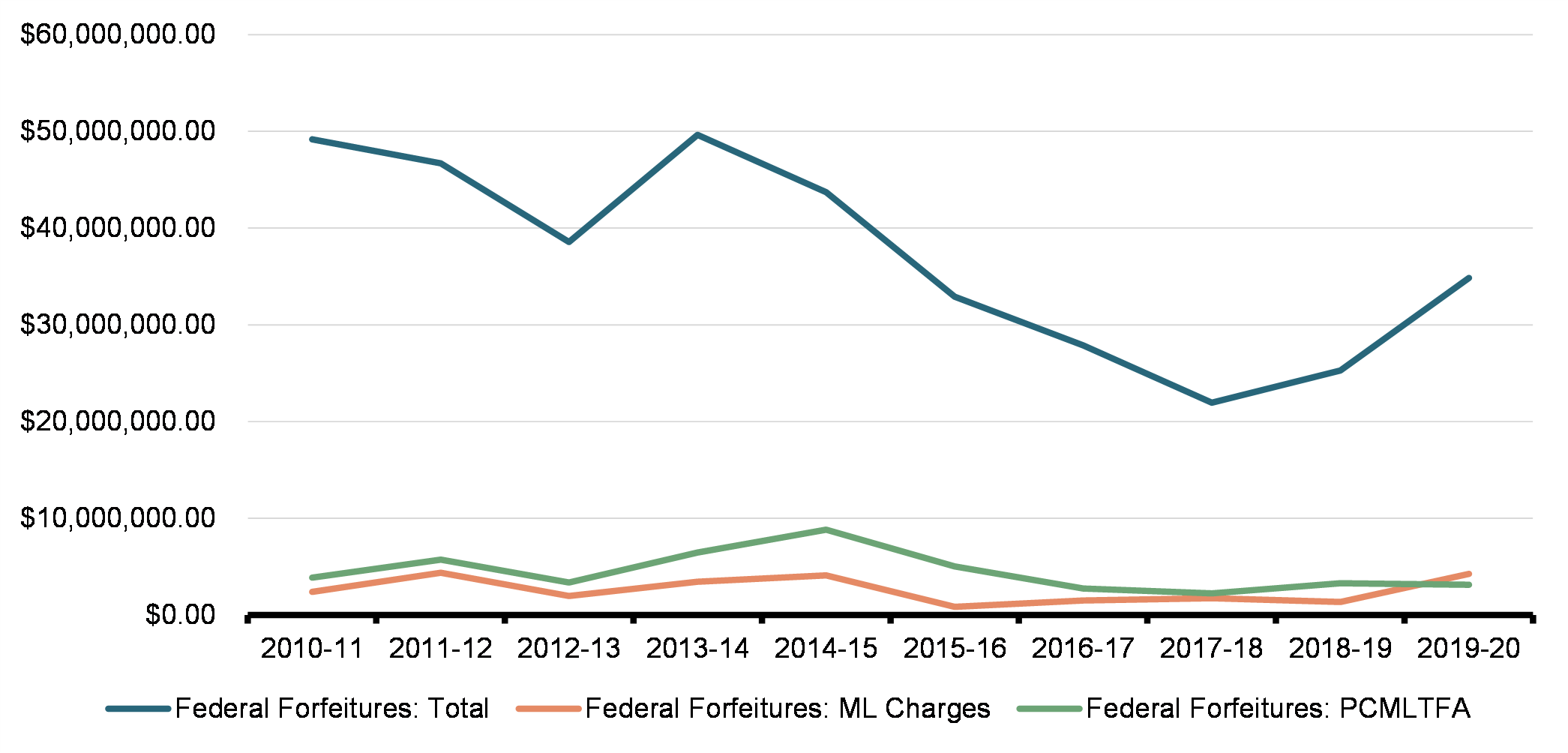

Overall, Canada's results for investigations, prosecutions, and forfeitures have declined over the past decade. Although RCMP and CRA investigations are increasingly incorporating a money laundering and/or terrorist financing component, the Regime has seen fewer money laundering charges laid by law enforcement. Incoming foreign requests for mutual legal assistance (MLA) and extradition efforts have been consistent over time, with the RCMP providing significant foreign assistance, but the number of outgoing requests for MLA and extradition by Canadian authorities has fallen. The vast majority of money laundering court cases end with charges being stayed or withdrawn, with the number of convictions and guilty pleas continuing to decline. Federal confiscations are beginning to increase, but from a point far below their earlier highs, and there are very few forfeitures in connection with money laundering charges when compared to predicate crimes. Provincial civil forfeiture results have remained relatively steady, while federal criminal forfeiture has declined.

Result #4: Offences are pursued and sanctioned, while individuals are deprived of means to carry out illicit activities

4.1 Investigations and Charges

The RCMP is the national police force, the provincial police force in all provinces except Ontario and Quebec, and the local police force pursuant to contracts with many municipalities or districts across Canada. The RCMP investigates ML/TF cases, makes arrests, lays charges, and seizes funds or assets suspected of being offence-related property and/or proceeds of crime or used in support of terrorist activity. It is also tasked with enforcing federal laws, including those related to commercial crime, counterfeiting, drug trafficking, cyber crime, border integrity, transnational and serious organized crime, and other related matters. The RCMP also provides counter-terrorism and domestic security and participates in various international policing efforts. The CRA-CID can also lay money laundering charges and refer cases of this nature to the Public Prosecution Service of Canada (PPSC). While Canada was found to perform relatively well on addressing terrorist financing, investigation and prosecution of money laundering in Canada was identified as an area for improvement in Canada's 2016 evaluation by the FATF. Examining the number of investigations and prosecutions provides insight into the level of enforcement activity undertaken by the federal Regime and other orders of government.

Case Study 4.1: COLLECTEUR

Project Collecteur was an investigation into a professional money laundering network operating in Montréal and Toronto. The network's members collected proceeds of criminal activity from organized crime groups in Montréal and laundered those illicit funds. As well, the network offered a money transfer service to drug exporting countries.

The network moved money collected in Montréal through various individuals and currency exchange offices in Toronto. The network used an informal value transfer system with connections in Lebanon, the United Arab Emirates, Iran, the United States and China. The funds were then returned to drug exporting countries, such as Colombia and Mexico. This activity allowed for the laundering of significant amounts of money originating from illegal activities, including drug trafficking.

On February 11, 2019, 17 individuals involved in the international money laundering network were arrested and charged. During the investigation and the searches, bank accounts and money in Canadian and foreign currencies was seized, for a value of $8.7 million. The CRA also proceeded with the restraint of six properties, of an estimated value of $15 million. The RCMP also seized a considered offence-related property of an estimated value of $7 million. The estimated value of the assets that were seized or restrained is more than $32.8 million. Two other individuals were arrested in foreign jurisdictions on international arrest warrants.

In Canada, money laundering investigations are required to show that the money being laundered represents the proceeds of criminal activity, which makes stand-alone investigations into money laundering difficult to undertake. The previously mentioned amendment of the Criminal Code to include the alternative element of recklessness to the money laundering offence was intended to mitigate this challenge. Evolving criminal trends such as encryption and cyber crime affect the resources that need to be dedicated to successful financial crime files. Effective ML/TF investigations also require early coordination and cooperation with partners (e.g., PPSC, CRA, and CBSA), involvement of the private sector in identifying suspicious activity, consistent case management, the ability to obtain information in a timely manner, and experienced personnel at all stages of an investigation. Coordination with partners helps to leverage expertise and maximize enforcement outcomes. For example, the RCMP could support the CBSA, which has trade-based money laundering experience and expertise, but does not have a mandate to investigate outside of trade fraud. The CRA, meanwhile, has a role to investigate tax evasion and can support money laundering investigations that have that nexus.Footnote 14

Case Study 4.2: ICON

Project Icon was a year-long investigation into an Edmonton-based company called Moxipay, which was facilitating payments for online, unregistered, illegal cannabis dispensaries. In December 2019, money laundering and proceeds of crime charges were laid against five individuals.

From January 2018 to December 2018, Moxipay facilitated over 84,000 transactions where nearly $15 million was received as proceeds from the illegal online sale of cannabis. Moxipay received the funds through e-transfer payments into several bank accounts and subsequently, the funds were laundered by Moxipay either by way of transfer back to the illegal online cannabis dispensaries or to their direct benefit through third party individuals and entities.

Along with charges laid against the five individuals, there is currently $884,000 under management by Public Services and Procurement Canada (PSPC)'s Seized Property Management Directorate. The case remained before the courts as of the time of publication of this report.

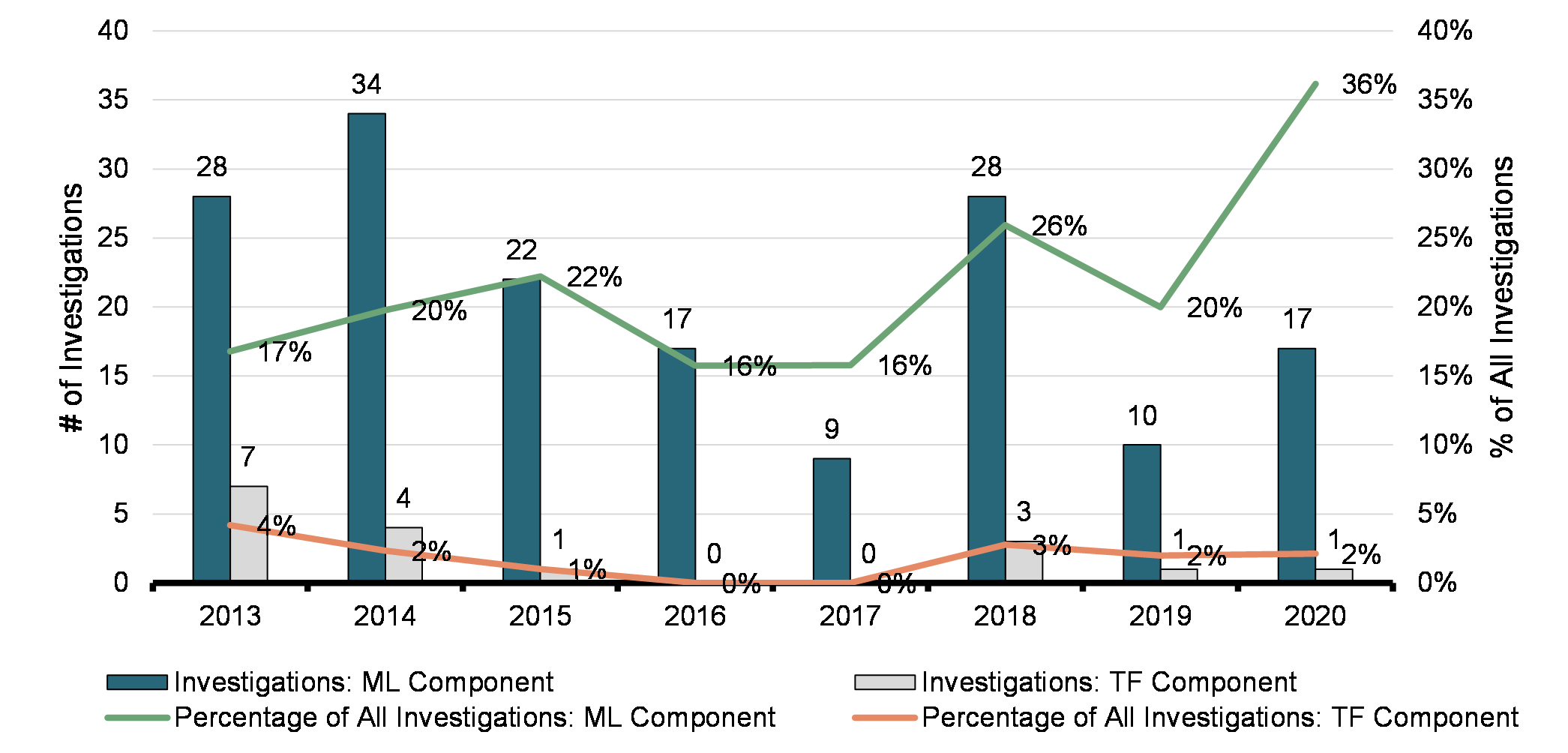

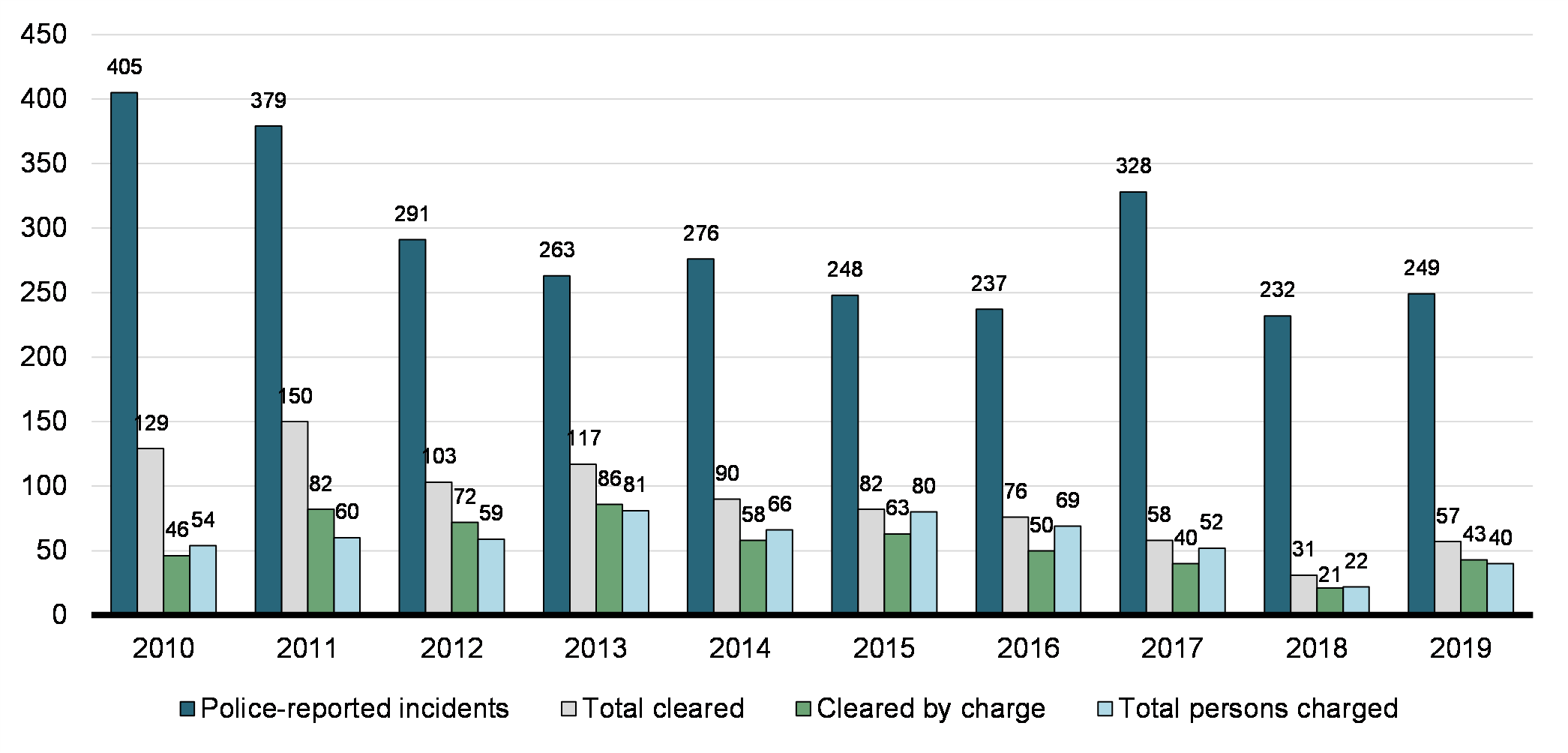

Recognizing the importance of money laundering and proceeds of crime in enabling predicate crimes, in 2019, the RCMP mandated all Tier 1 and 2 Federal Policing investigations to have a proceeds of crime component. The RCMP documented 17 Tier 1 and 2 Federal Policing investigations with a money laundering component in 2020, a decrease of 39 per cent from 2013, when there were 28 investigations with a money laundering component. However, while there has been an overall decline in the number of investigations with a money laundering component, investigations with such a component account for an increasing percentage of total investigations – over one-third of all investigations had a one in 2020, up from less than one-fifth in 2013. The RCMP also documented only one case with a TF component in 2020, compared to seven in 2013. Unlike in the case of money laundering, investigations with a terrorist financing component have also declined as a percentage of total investigations from 2013.

Tier 1 & 2 Investigations With ML/TF Component (RCMP)

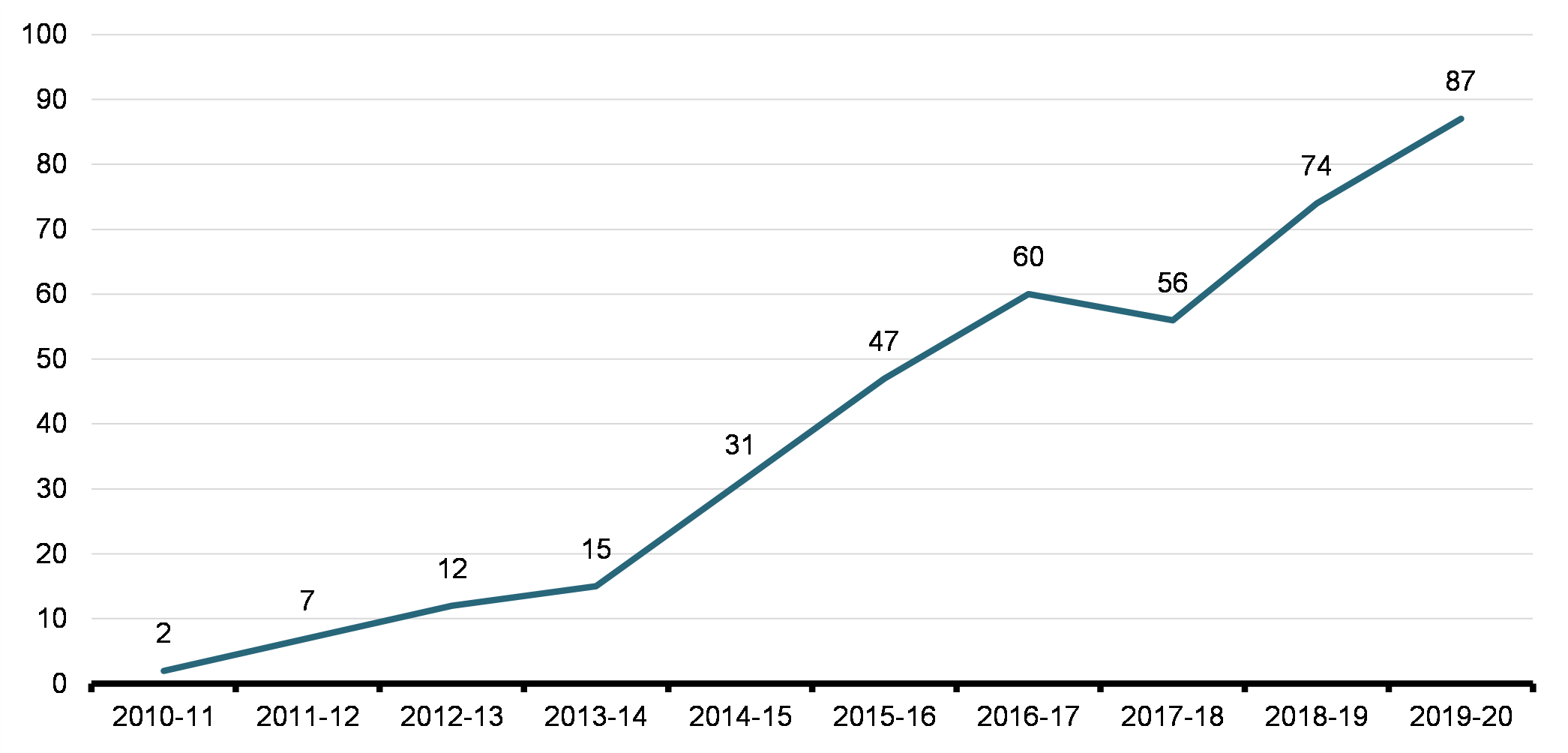

The Forensic Accounting Management Group (FAMG) within Public Services and Procurement Canada provides specialized forensic accounting services and supports Canadian law enforcement, including the RCMP, with criminal investigations that have financial elements. There has been an exceptional uptick in RCMP-FAMG ML/TF files over the past decade, going from just two active cases in 2010-11, to 87 cases by 2019-20. However, it is worth noting that the methodology used to assign or associate a client project/file as an ML/TF investigation changed in 2014-15 and again in 2018-19. Consequently, the statistics on money laundering files that the FAMG worked on prior to 2018-19 may have been understated, and part of the increase in files could be attributed to this reclassification. Nonetheless, this suggests a substantial increase in involvement of federal forensic accountants in supporting money laundering and terrorist financing cases.

Number of Active RCMP-FAMG ML/TF Files

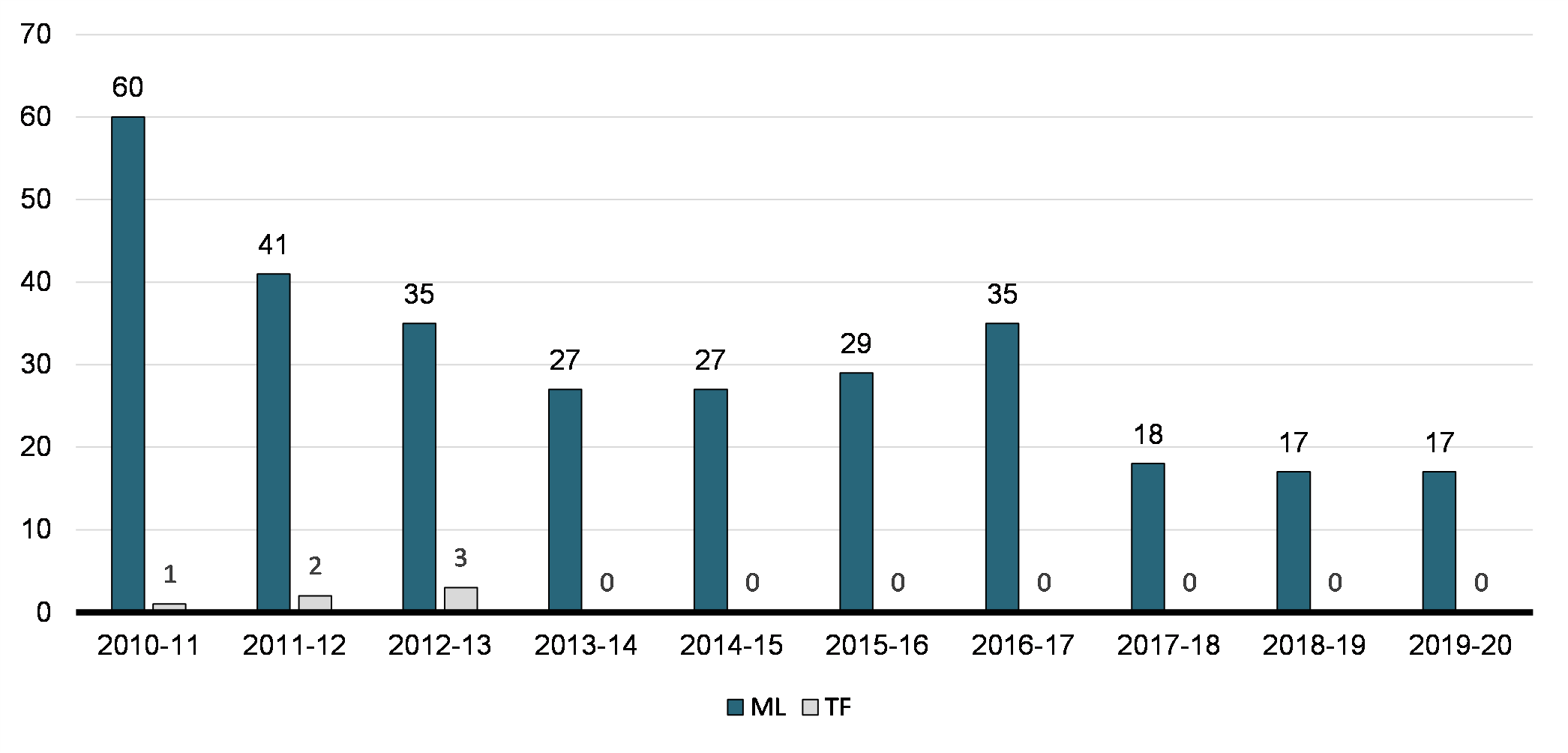

The chart below illustrates the number of occurrences that resulted in charges being laid following an investigation. Over the past decade, the number of ML/TF occurrences cleared by chargeFootnote 15 has fallen dramatically. In 2019-20, the RCMP recorded 17 money laundering occurrences cleared by charge – a 71 per cent decrease from 2010-11, when there were 60 occurrences. There have been no terrorist financing charges from 2013-14 to 2019-20 – compared with three occurrences cleared by charge in 2012-13. This suggests that ML/TF investigations are increasingly not resulting in charges, with fewer cases being carried through to the prosecution stage.

In 2011, following a reduction to its resources, the RCMP reorganized to target the highest level threats, rather than focusing on specific crimes regardless of threat. One of the consequences of this decision was to reform specialized financial crime areas into larger financial crime units, whose members were then amalgamated into Federal Serious and Organized Crime units to investigate financial crime aspects in organized crime related cases.

As these specialized units were disbanded and Federal Policing priorities shifted to address the most serious threats to Canada's safety, resources that were formerly specific to specialized programs were often used to investigate crimes that fall under the threat-based approach described above. This has resulted in fewer money laundering investigations, with a consequential reduction in the number of cases cleared by charge. Furthermore, in criminal investigations, charges have to be approved by Crown prosecutors, who may decline to prosecute money laundering charges in favour of pursuing other charges. Fewer investigations can impact the experience and skill development of investigators and prosecutors, compounding issues around the lack of financial crime and AML/ATF knowledge in Canada.

ML/TF Occurrences Cleared by Charge (RCMP)

The RCMP continues to work to identify gaps and challenges to conducting effective investigations and work toward solutions to these issues. Solutions will need to be multi-faceted and address resourcing issues, prioritization, the legislative environment, regulatory powers, and the more effective inclusion of the private sector in the fight against money laundering. The RCMP has undertaken a number of initiatives that recognize collaboration and cooperation as key components to implementing effective solutions. These initiatives are discussed in detail below.

Case Study 4.3: CIROC Money Laundering Strategy

In 2020, the Canadian Integrated Response to Organized Crime (CIROC) committee recommended developing a strategy to operationalize action against priority money laundering targets in Canada. The RCMP and operational partners developed the CIROC Money Laundering Strategy to provide a central coordination mechanism across Canada to collectively address the highest money laundering threats by building and maintaining strong collaboration with Regime partners.

The Strategy consists of three pillars: Intelligence, Enforcement (disrupt, dismantle, and deter), and Engagement. The first pillar will identify, evaluate, and prioritize the most serious organized money laundering network threats through joint intelligence activities, using tactical, operational, and strategic analysis. The second pillar will build on the first pillar and establish an enforcement strategy that includes leveraging all available legal mechanisms (including statutes outside the Criminal Code) to investigate, disrupt, deter, and/or dismantle money laundering networks operating in Canada. The third pillar will advance in conjunction with the first two pillars, and will seek to educate, inform, and enhance Canada's AML Regime and the tools and ability to combat the money laundering threat posed to Canada's economic integrity.

Case Study 4.4: CIFA-BC