Archived - The Fiscal Monitor - October 2022

Highlights

October 2022

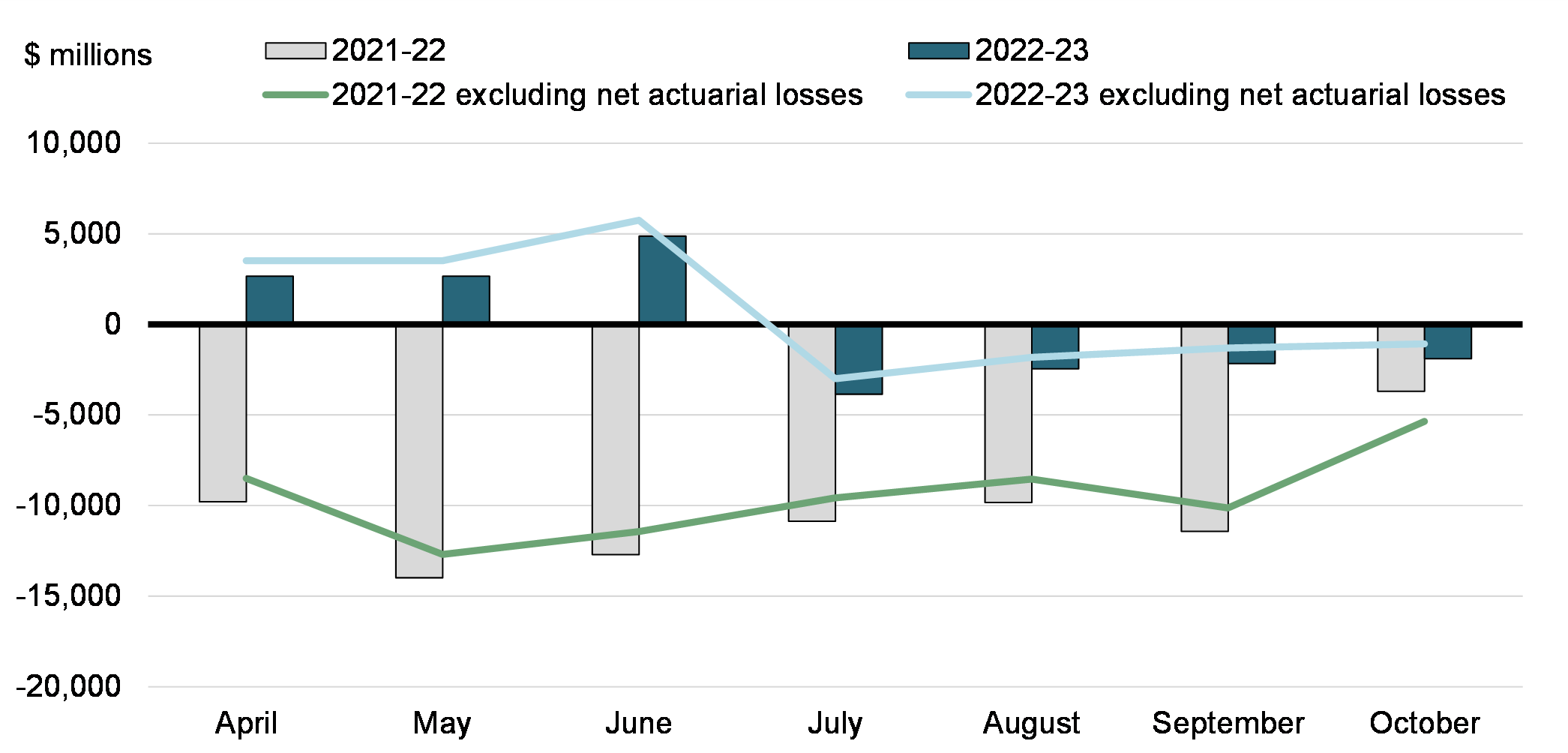

There was a budgetary deficit of $1.9 billion in October 2022, compared to a deficit of $3.7 billion in October 2021. The budgetary deficit before net actuarial losses was $1.1 billion, compared to a deficit of $5.4 billion in the same period of 2021-22. The budgetary balance before net actuarial losses is intended to supplement the traditional budgetary balance and improve the transparency of the government’s financial reporting by isolating the impact of the amortization of net actuarial losses arising from the revaluation of the government’s pension and other employee future benefit plans.

The government’s 2022-23 financial results continue to improve compared to 2021-22 as the fiscal impact of the COVID-19 crisis and the unprecedented level of temporary COVID-19 response measures wane.

Monthly Budgetary Balance and Budgetary Balance Excluding Net Actuarial Losses

Compared to October 2021:

- Revenues increased by $3.8 billion, or 12.0 per cent, reflecting broad-based improvement across revenue streams.

- Program expenses excluding net actuarial losses were down $0.1 billion, or 0.2 per cent.

- Public debt charges were down $0.4 billion, or 14.4 per cent, due to a year-to-date adjustment in October 2021 to reflect updated actuarial valuations of the government’s pension and other employee future benefit obligations as per the Public Accounts of Canada 2021, as well as lower Consumer Price Index adjustments on Real Return Bonds in October 2022. These decreases were partly offset by the impact of higher interest rates in the current year.

- Net actuarial losses were up $2.5 billion, or 148.9 per cent, largely reflecting an adjustment in the prior year to reflect the government’s latest actuarial valuations for pensions and benefits in the Public Accounts of Canada 2021.

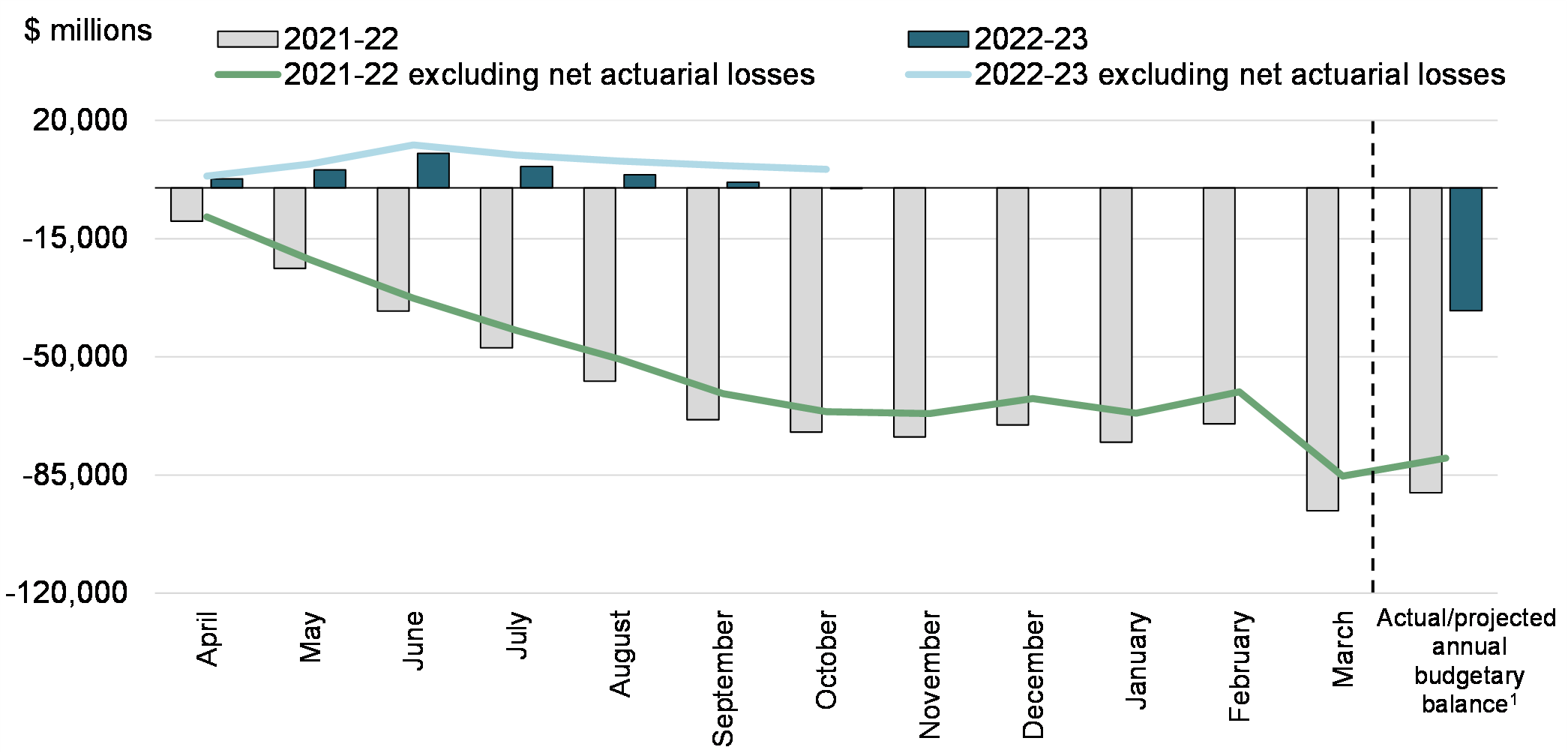

April to October 2022

The government posted a budgetary deficit of $0.2 billion for the April to October period of the 2022-23 fiscal year, compared to a deficit of $72.3 billion reported for the same period of 2021-22. The budgetary surplus before net actuarial losses was $5.6 billion, compared to a deficit of $66.2 billion in the April to October period of 2021-22.

Compared to 2021-22:

- Revenues were up $36.6 billion, or 17.6 per cent, reflecting broad-based improvement across revenue streams particularly given the waning fiscal and economic impact of COVID-19.

- Program expenses excluding net actuarial losses were down $40.4 billion, or 15.6 per cent, largely reflecting lower transfers to individuals and businesses due to expiring temporary COVID-19 measures.

- Public debt charges increased by $5.2 billion, or 35.7 per cent, primarily driven by higher interest rates and higher Consumer Price Index adjustments on Real Return Bonds.

- Net actuarial losses decreased by $0.3 billion, or 4.7 per cent.

Year-to-Date Budgetary Balance and Budgetary Balance Excluding Net Actuarial Losses

| October | April to October | |||

|---|---|---|---|---|

| 2021 | 2022 | 2021-22 | 2022-23 | |

| Budgetary transactions | ||||

| Revenues | 31,512 | 35,307 | 207,329 | 243,880 |

| Expenses | ||||

Program expenses, excluding net actuarial losses |

-34,059 | -33,974 | -259,054 | -218,628 |

Public debt charges |

-2,815 | -2,409 | -14,507 | -19,686 |

| Budgetary balance, excluding net actuarial losses | -5,362 | -1,076 | -66,232 | 5,566 |

Net actuarial losses |

1,678 | -820 | -6,020 | -5,740 |

| Budgetary balance (deficit/surplus) | -3,684 | -1,896 | -72,252 | -174 |

| Non-budgetary transactions | -17,722 | 316 | -22,882 | -31,064 |

| Financial source/requirement | -21,406 | -1,580 | -95,134 | -31,238 |

| Net change in financing activities | 20,479 | 19,153 | 96,878 | 33,567 |

| Net change in cash balances | -927 | 17,573 | 1,744 | 2,329 |

| Cash balance at end of period | 61,133 | 94,590 | ||

|

Note: Positive numbers indicate net source of funds. Negative numbers indicate net requirement for funds. |

||||

Revenues

Revenues in October 2022 totalled $35.3 billion, up $3.8 billion, or 12.0 per cent, from October 2021, reflecting broad-based improvement in economic activity relative to the greater weight of COVID-19 on the year prior.

- Tax revenues increased by $3.2 billion, or 11.6 per cent, compared to the same period in 2021-22.

- Proceeds from the pollution pricing framework were up $0.1 billion, or 31.7 per cent, reflecting higher carbon pollution pricing in 2022.

- Employment Insurance (EI) premium revenues were up $0.2 billion, or 13.4 per cent, reflecting better labour market conditions.

- Other revenues, consisting of enterprise Crown corporations’ net profits, sales of goods and services, returns on investments and net foreign exchange revenues, were up $0.3 billion, or 13.2 per cent.

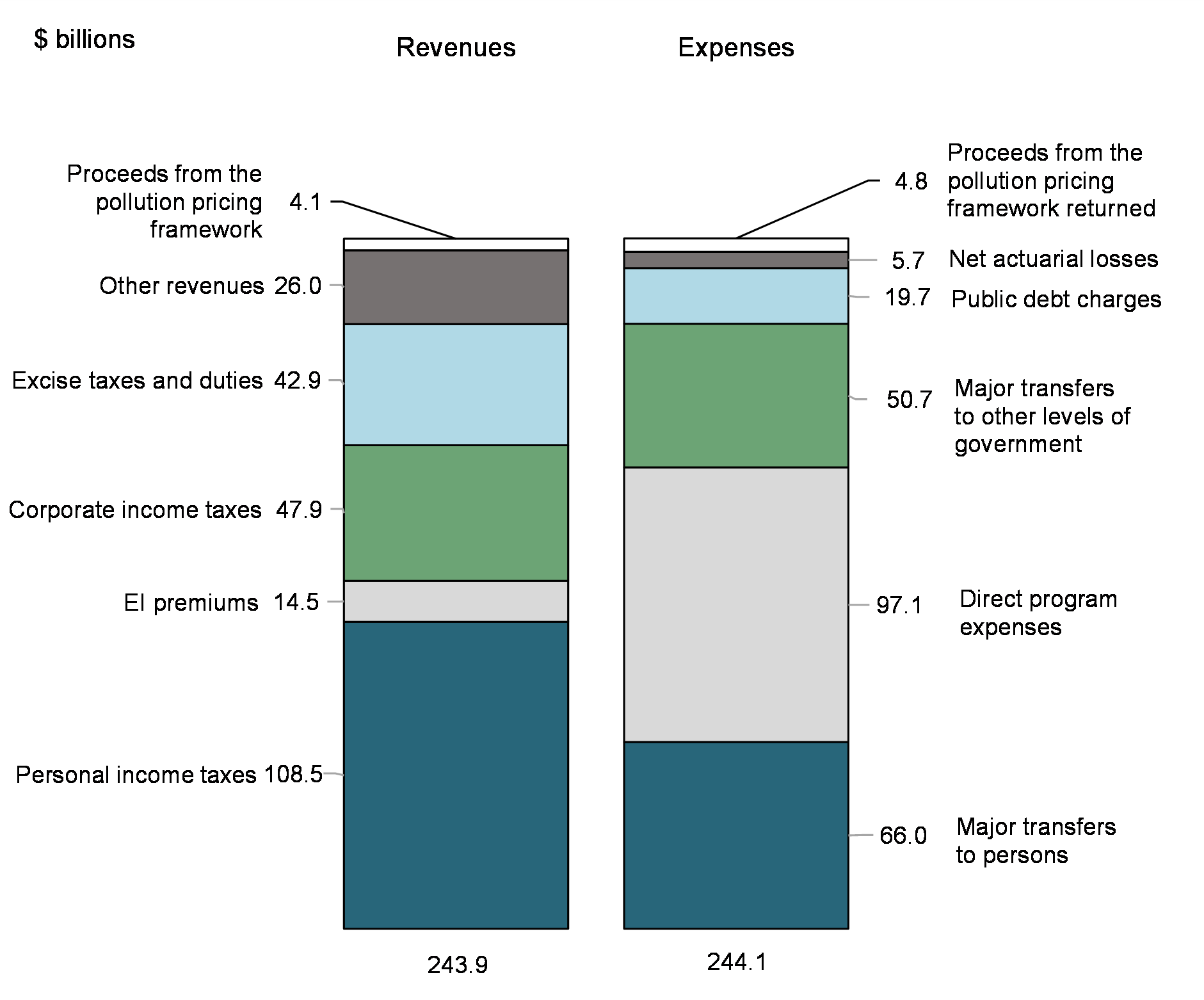

Revenues for the April to October period of 2022-23 totalled $243.9 billion, up $36.6 billion, or 17.6 per cent, from the same period in 2021-22.

- Tax revenues increased by $30.1 billion, or 17.1 per cent, compared to the same period in 2021-22, when COVID-19 restrictions weighed on revenue as well as due to strong economic growth. For its part, the federal portion of assessed cannabis excise duties increased by $17 million to $104 million over the April to October period.

- Proceeds from the pollution pricing framework were up $1.1 billion, or 35.6 per cent, reflecting higher carbon pollution pricing in 2022.

- EI premium revenues were up $1.6 billion, or 12.0 per cent, reflecting better labour market conditions.

- Other revenues were up $3.8 billion, or 25.8 per cent, due to economic improvement and normalization following COVID-19 and higher interest rates.

| October | April to October | |||||

|---|---|---|---|---|---|---|

| 2021 | 2022 | Change | 2021-22 | 2022-23 | Change | |

| ($ millions) | (%) | ($ millions) | (%) | |||

| Tax revenues | ||||||

| Income taxes | ||||||

Personal |

15,339 | 15,918 | 3.8 | 100,894 | 108,479 | 7.5 |

Corporate |

5,035 | 6,557 | 30.2 | 34,034 | 47,929 | 40.8 |

Non-resident |

939 | 1,342 | 42.9 | 5,105 | 7,471 | 46.3 |

Total income tax revenues |

21,313 | 23,817 | 11.7 | 140,033 | 163,879 | 17.0 |

| Other taxes and duties | ||||||

Goods and Services Tax |

4,522 | 5,302 | 17.2 | 26,906 | 32,043 | 19.1 |

Energy taxes |

505 | 436 | -13.7 | 3,053 | 3,196 | 4.7 |

Customs import duties |

491 | 590 | 20.2 | 3,197 | 3,887 | 21.6 |

Other excise taxes and duties |

577 | 439 | -23.9 | 3,435 | 3,740 | 8.9 |

Total excise taxes and duties |

6,095 | 6,767 | 11.0 | 36,591 | 42,866 | 17.1 |

| Total tax revenues | 27,408 | 30,584 | 11.6 | 176,624 | 206,745 | 17.1 |

| Proceeds from the pollution pricing framework | 401 | 528 | 31.7 | 3,015 | 4,088 | 35.6 |

| Employment Insurance premiums | 1,266 | 1,436 | 13.4 | 12,943 | 14,494 | 12.0 |

| Other revenues | 2,437 | 2,759 | 13.2 | 14,747 | 18,553 | 25.8 |

| Total revenues | 31,512 | 35,307 | 12.0 | 207,329 | 243,880 | 17.6 |

|

Note: Totals may not add due to rounding. |

||||||

Expenses

Program expenses excluding net actuarial losses in October 2022 were $34.0 billion, down $0.1 billion, or 0.2 per cent, from October 2021.

- Major transfers to persons, consisting of elderly benefits, EI benefits, COVID-19 income support for workers, and children’s benefits, were down $2.5 billion or 20.6 per cent.

- Elderly benefits increased by $0.9 billion, or 16.5 per cent, reflecting changes in consumer prices to which benefits are fully indexed, and growth in the number of recipients. In addition, as announced in Budget 2021 and implemented in July 2022, the Old Age Security pension has permanently increased by 10 per cent for seniors aged 75 and over.

- EI benefits decreased by $0.9 billion, or 37.0 per cent, reflecting improved labour market conditions.

- COVID-19 income support for workers decreased $1.9 billion, or 99.8 per cent, reflecting the wind-down of the Canada Recovery Benefit, Canada Recovery Sickness Benefit, and Canada Recovery Caregiving Benefit.

- Children’s benefits were down $0.6 billion, or 21.4 per cent, largely reflecting the October 2021 payment of the temporary Canada Child Benefit young child supplement.

- Major transfers to other levels of government were up $0.6 billion, or 10.3 per cent, reflecting a number of factors, including legislated growth in the Canada Health Transfer, the Canada Social Transfer, Equalization transfers and transfers to the territories, an adjustment in the prior year to reflect a revised estimate of recoveries under the Quebec Abatement, and a year-over-year difference in the timing of home care and mental health transfers.

- Proceeds from the pollution pricing framework returned increased by $1.6 billion, reflecting a change in the delivery of the Climate Action Incentive, from annually on personal income tax returns to a quarterly benefit. Direct proceeds will continue to be fully returned in the provinces or territories where they are generated.

- Direct program expenses were up $0.2 billion, or 1.2 per cent. Within direct program expenses:

- Canada Emergency Wage Subsidy (CEWS) payments decreased by $2.1 billion, or 100.0 per cent, reflecting the end of the program.

- Other transfer payments increased by $1.1 billion, or 19.0 per cent, reflecting a number of factors, including year-over-year differences in the timing of transfer payments and an increase in international assistance.

- Operating expenses of the government’s departments, agencies, and consolidated Crown corporations and other entities increased by $1.2 billion, or 15.4 per cent, largely reflecting increased personnel and public health care expenses.

Public debt charges decreased $0.4 billion, or 14.4 per cent, due to an October 2021 adjustment to reflect updated actuarial valuations of the government’s pension and other employee future benefit obligations, as well as lower Consumer Price Index adjustments on Real Return Bonds in October 2022. The decrease in public debt charges was partly offset by the impact of higher interest rates in the current year.

Net actuarial losses, which represent the amortization of changes in the value of the government’s obligations for pensions and other employee future benefits accrued in previous fiscal years and related assets, were up $2.5 billion, or 148.9 per cent, largely due to an October 2021 year-to-date adjustment to incorporate updated actuarial valuations for pensions and benefits prepared for the Public Accounts of Canada 2021.

For the April to October period of 2022-23, program expenses excluding net actuarial losses were $218.6 billion, down $40.4 billion, or 15.6 per cent, from the same period the previous year.

- Major transfers to persons were down $27.4 billion or 29.3 per cent.

- Elderly benefits increased by $4.0 billion, or 11.3 per cent, largely reflecting growth in the number of recipients and changes in consumer prices, to which benefits are fully indexed. In addition, as of July 2022, the Old Age Security pension has permanently increased by 10 per cent for seniors aged 75 and over.

- EI benefits decreased by $14.5 billion, or 53.8 per cent, reflecting improved labour market conditions.

- COVID-19 income support for workers decreased $15.1 billion, or 98.4 per cent, reflecting the wind-down of the Canada Recovery Benefit, Canada Recovery Sickness Benefit, and Canada Recovery Caregiving Benefit.

- Children’s benefits were down $1.8 billion, or 11.0 per cent, largely reflecting the temporary Canada Child Benefit young child supplement in 2021-22.

- Major transfers to other levels of government were up $1.9 billion, or 3.9 per cent, primarily reflecting Canada-wide early learning and child care transfers, which began partway through 2021-22, and legislated growth in the Canada Health Transfer, the Canada Social Transfer, Equalization transfers and transfers to the territories. These increases were offset in part by year-over-year differences in the timing of the Canada Community-Building Fund and home care and mental health transfers, as well as increased recoveries under the Quebec Abatement.

- Proceeds from the pollution pricing framework returned increased by $1.2 billion, or 33.4 per cent, reflecting an increase in the rate of the Climate Action Incentive as well as the change in the delivery of the Climate Action Incentive, from annually on personal income tax returns to a quarterly benefit.

- Direct program expenses were down $16.1 billion, or 14.3 per cent. Within direct program expenses:

- CEWS payments decreased by $19.5 billion, or 100.6 per cent, reflecting the end of the program and reassessments of previous returns.

- Other transfer payments decreased by $0.5 billion, or 1.3 per cent, in large part reflecting the wind-down of temporary COVID-19 response measures and a one-time payment to seniors aged 75 and older in August 2021. This decrease was offset in part by an increase in international assistance and transfers in respect of Indigenous Peoples.

- Operating expenses of the government’s departments, agencies, and consolidated Crown corporations and other entities increased by $3.8 billion, or 6.7 per cent, in large part reflecting increased personnel expenses.

Public debt charges increased by $5.2 billion, or 35.7 per cent, primarily driven by higher interest rates and higher Consumer Price Index adjustments on Real Return Bonds.

Net actuarial losses decreased by $0.3 billion, or 4.7 per cent.

| October | April to October | |||||

|---|---|---|---|---|---|---|

| 2021 | 2022 | Change | 2021-22 | 2022-23 | Change | |

| ($ millions) | (%) | ($ millions) | (%) | |||

| Major transfers to persons | ||||||

Elderly benefits |

5,166 | 6,016 | 16.5 | 35,177 | 39,136 | 11.3 |

Employment Insurance benefits |

2,359 | 1,485 | -37.0 | 26,911 | 12,428 | -53.8 |

COVID-19 income support for workers1 |

1,903 | 3 | -99.8 | 15,371 | 243 | -98.4 |

Children’s benefits |

2,603 | 2,046 | -21.4 | 15,968 | 14,205 | -11.0 |

| Total major transfers to persons | 12,031 | 9,550 | -20.6 | 93,427 | 66,012 | -29.3 |

| Major transfers to other levels of government | ||||||

Canada Health Transfer |

3,594 | 3,767 | 4.8 | 25,157 | 26,371 | 4.8 |

Canada Social Transfer |

1,289 | 1,328 | 3.0 | 9,026 | 9,297 | 3.0 |

Equalization |

1,743 | 1,827 | 4.8 | 12,198 | 12,787 | 4.8 |

Territorial Formula Financing |

298 | 310 | 4.0 | 2,891 | 3,005 | 3.9 |

Canada-wide early learning and child care |

- | - | n/a | - | 2,219 | n/a |

Canada Community-Building Fund |

- | - | n/a | 2,320 | 1,134 | -51.1 |

Home care and mental health |

- | 135 | n/a | 831 | 136 | -83.6 |

Other fiscal arrangements2 |

-801 | -613 | 23.5 | -3,649 | -4,260 | -16.7 |

| Total major transfers to other levels of government | 6,123 | 6,754 | 10.3 | 48,774 | 50,689 | 3.9 |

| Proceeds from the pollution pricing framework returned | 38 | 1,617 | 4,155.3 | 3,626 | 4,836 | 33.4 |

| Direct program expenses | ||||||

Canada Emergency Wage Subsidy |

2,139 | - | -100.0 | 19,362 | -122 | -100.6 |

Other transfer payments |

5,940 | 7,068 | 19.0 | 36,669 | 36,195 | -1.3 |

Operating expenses |

7,788 | 8,985 | 15.4 | 57,196 | 61,018 | 6.7 |

| Total direct program expenses | 15,867 | 16,053 | 1.2 | 113,227 | 97,091 | -14.3 |

| Total program expenses, excluding net actuarial losses | 34,059 | 33,974 | -0.2 | 259,054 | 218,628 | -15.6 |

| Public debt charges | 2,815 | 2,409 | -14.4 | 14,507 | 19,686 | 35.7 |

| Total expenses, excluding net actuarial losses | 36,874 | 36,383 | -1.3 | 273,561 | 238,314 | -12.9 |

Net actuarial losses |

-1,678 | 820 | 148.9 | 6,020 | 5,740 | -4.7 |

| Total expenses | 35,196 | 37,203 | 5.7 | 279,581 | 244,054 | -12.7 |

|

Note: Totals may not add due to rounding. |

||||||

The following table presents total expenses by main object of expense.

| October | April to October | |||||

|---|---|---|---|---|---|---|

| 2021 | 2022 | Change | 2021-22 | 2022-23 | Change | |

| ($ millions) | (%) | ($ millions) | (%) | |||

| Transfer payments | 26,271 | 24,989 | -4.9 | 201,858 | 157,610 | -21.9 |

| Other expenses | ||||||

| Personnel, excluding net actuarial losses | 4,574 | 5,133 | 12.2 | 33,649 | 36,056 | 7.2 |

| Transportation and communications | 195 | 239 | 22.6 | 1,227 | 1,515 | 23.5 |

| Information | 38 | 50 | 31.6 | 259 | 184 | -29.0 |

| Professional and special services | 1,272 | 1,393 | 9.5 | 7,282 | 7,907 | 8.6 |

| Rentals | 352 | 339 | -3.7 | 2,199 | 2,413 | 9.7 |

| Repair and maintenance | 249 | 305 | 22.5 | 1,612 | 2,047 | 27.0 |

| Utilities, materials and supplies | 336 | 841 | 150.3 | 4,156 | 4,373 | 5.2 |

| Other subsidies and expenses | 357 | 244 | -31.7 | 3,897 | 3,465 | -11.1 |

| Amortization of tangible capital assets | 407 | 432 | 6.1 | 2,860 | 2,992 | 4.6 |

| Net loss on disposal of assets | 8 | 9 | 12.5 | 55 | 66 | 20.0 |

| Total other expenses | 7,788 | 8,985 | 15.4 | 57,196 | 61,018 | 6.7 |

| Total program expenses, excluding net actuarial losses | 34,059 | 33,974 | -0.2 | 259,054 | 218,628 | -15.6 |

| Public debt charges | 2,815 | 2,409 | -14.4 | 14,507 | 19,686 | 35.7 |

| Total expenses, excluding net actuarial losses | 36,874 | 36,383 | -1.3 | 273,561 | 238,314 | -12.9 |

| Net actuarial losses | -1,678 | 820 | 148.9 | 6,020 | 5,740 | -4.7 |

| Total expenses | 35,196 | 37,203 | 5.7 | 279,581 | 244,054 | -12.7 |

|

Note: Totals may not add due to rounding. |

||||||

Revenues and expenses (April to October 2022)

Financial requirement of $31.2 billion for April to October 2022

The budgetary balance is presented on an accrual basis of accounting, recording government revenues and expenses when they are earned or incurred, regardless of when the cash is received or paid. In contrast, the financial source/requirement measures the difference between cash coming in to the government and cash going out. This measure is affected not only by changes in the budgetary balance but also by the cash source/requirement resulting from the government’s investing activities through its acquisition of capital assets and its loans, financial investments and advances, as well as from other activities, including payment of accounts payable and collection of accounts receivable, foreign exchange activities, and the amortization of its tangible capital assets. The difference between the budgetary balance and financial source/requirement is recorded in non-budgetary transactions.

With a budgetary deficit of $0.2 billion and a requirement of $31.1 billion from non-budgetary transactions, there was a financial requirement of $31.2 billion for the April to October 2022 period, compared to a financial requirement of $95.1 billion for the same period of the previous year.

The lower financial requirement in 2022-23 largely reflects the improvement in the budgetary balance, offset in part by an increase in the financial requirement from non-budgetary transactions.

| October | April to October | |||

|---|---|---|---|---|

| 2021 | 2022 | 2021-22 | 2022-23 | |

| Budgetary balance (deficit/surplus) | -3,684 | -1,896 | -72,252 | -174 |

| Non-budgetary transactions | ||||

| Accounts payable, accrued liabilities and accounts receivable1 | -13,574 | 228 | -5,359 | -16,503 |

| Pensions, other future benefits, and other liabilities | -708 | 2,790 | 6,622 | 7,716 |

| Foreign exchange accounts and derivatives1 | 2,671 | -1,462 | -8,401 | -14,272 |

| Loans, investments and advances | -5,851 | -725 | -15,518 | -6,920 |

| Non-financial assets | -260 | -515 | -226 | -1,085 |

| Total non-budgetary transactions | -17,722 | 316 | -22,882 | -31,064 |

| Financial source/requirement | -21,406 | -1,580 | -95,134 | -31,238 |

|

Note: Totals may not add due to rounding. |

||||

Net financing activities up $33.6 billion

The government financed this financial requirement of $31.2 billion and increased cash balances by $2.3 billion by increasing unmatured debt by $33.6 billion. The increase in unmatured debt was achieved primarily through the issuance of marketable bonds.

Cash balances at the end of October 2022 stood at $94.6 billion, up $33.5 billion from their level at the end of October 2021.

| October | April to October | |||

|---|---|---|---|---|

| 2021 | 2022 | 2021-22 | 2022-23 | |

| Financial source/requirement | -21,406 | -1,580 | -95,134 | -31,238 |

| Net increase (+)/decrease (-) in financing activities | ||||

| Unmatured debt transactions | ||||

Canadian currency borrowings |

||||

Marketable bonds1 |

20,681 | 17,699 | 114,880 | 29,900 |

Treasury bills1 |

1,974 | 1,812 | -23,048 | -1,872 |

Retail debt |

9 | - | -6 | - |

Total Canadian currency borrowings |

22,664 | 19,511 | 91,826 | 28,028 |

Foreign currency borrowings1 |

-2,166 | -339 | 5,055 | 5,701 |

Total market debt transactions |

20,498 | 19,172 | 96,881 | 33,729 |

Obligations related to capital leases and other unmatured debt |

-19 | -19 | -3 | -162 |

| Net change in financing activities | 20,479 | 19,153 | 96,878 | 33,567 |

| Change in cash balance | -927 | 17,573 | 1,744 | 2,329 |

| Cash balance at end of period | 61,133 | 94,590 | ||

|

Note: Totals may not add due to rounding. |

||||

Federal debt

The federal debt, or accumulated deficit, is the difference between the government's total liabilities and total assets. The year-over-year change in the accumulated deficit reflects the year-to-date budgetary balance plus other comprehensive income or loss and remeasurement gains and losses.

Other comprehensive income or loss represents certain unrealized gains and losses on financial instruments and certain actuarial gains and losses related to pensions and other employee future benefits reported by enterprise Crown corporations and other government business enterprises.

Remeasurement gains and losses represent changes in the fair value of derivatives, such as swap agreements and foreign exchange forward agreements, which are used by the government to manage financial risks. As with other comprehensive income or loss, remeasurement gains and losses are not reflected in the budgetary balance, but are instead charged directly to the accumulated deficit. The government began accounting for remeasurement gains and losses in 2022-23 with the adoption of a new standard of the Public Sector Accounting Board regarding financial instruments (see Note 8).

The accumulated deficit decreased by $2.8 billion over the April to October 2022 period, as the $0.2‑billion budgetary deficit was offset by $0.2 billion in other comprehensive income and $2.8 billion in net remeasurement gains.

| April 1, 2022 Opening balance Note 8 |

October 31, 2022 | Change | |

|---|---|---|---|

| Liabilities | |||

Accounts payable and accrued liabilities |

262,220 | 230,711 | -31,509 |

Derivative financial liabilities1 |

2,778 | 71 | -2,707 |

Interest-bearing debt |

|||

Unmatured debt |

|||

Payable in Canadian currency |

|||

Marketable bonds |

1,043,989 | 1,073,889 | 29,900 |

Treasury bills |

186,877 | 185,005 | -1,872 |

Subtotal |

1,230,866 | 1,258,894 | 28,028 |

Payable in foreign currencies |

14,473 | 20,174 | 5,701 |

Obligations related to capital leases and other unmatured debt |

5,366 | 5,204 | -162 |

Total unmatured debt |

1,250,705 | 1,284,272 | 33,567 |

Pension and other liabilities |

|||

Public sector pensions |

167,666 | 164,922 | -2,744 |

Other employee and veteran future benefits |

159,705 | 171,148 | 11,443 |

Other liabilities |

7,707 | 6,724 | -983 |

Total pension and other liabilities |

335,078 | 342,794 | 7,716 |

Total interest-bearing debt |

1,585,783 | 1,627,066 | 41,283 |

| Total liabilities | 1,850,781 | 1,857,848 | 7,067 |

| Financial assets | |||

Cash and accounts receivable |

280,026 | 267,349 | -12,677 |

Foreign exchange accounts |

104,031 | 121,548 | 17,517 |

Derivative financial assets1 |

3,403 | 224 | -3,179 |

Loans, investments, and advances (net of allowances)2 |

207,031 | 214,153 | 7,122 |

Public sector pension assets |

9,203 | 9,203 | - |

| Total financial assets | 603,694 | 612,477 | 8,783 |

| Net debt | 1,247,087 | 1,245,371 | -1,716 |

| Non-financial assets | 105,268 | 106,353 | 1,085 |

| Federal debt (accumulated deficit) | 1,141,819 | 1,139,018 | -2,801 |

|

Note: Totals may not add due to rounding. |

|||

Notes

- The Fiscal Monitor is a report on the consolidated financial results of the Government of Canada, prepared monthly by the Department of Finance Canada. The government is committed to releasing The Fiscal Monitor on a timely basis in accordance with the International Monetary Fund's Special Data Dissemination Standards Plus, which are designed to promote member countries' data transparency and promote the development of sound statistical systems.

- The financial results reported in The Fiscal Monitor are drawn from the accounts of Canada, which are maintained by the Receiver General and used to prepare the annual Public Accounts of Canada.

- The Fiscal Monitor is generally prepared in accordance with the same accounting policies as used to prepare the government's annual consolidated financial statements, which are summarized in Section 2 of Volume I of the Public Accounts of Canada, available through the Public Services and Procurement Canada website.

- The financial results presented in The Fiscal Monitor have not been audited or reviewed by an external auditor.

- There can be substantial volatility in monthly results due to the timing of revenue receipts and expense recognition. For instance, a large share of government spending is typically reported in the March Fiscal Monitor.

- The April to March results reported in The Fiscal Monitor are not the final results for the fiscal year as a whole. The final results are published in the annual Public Accounts of Canada and incorporate post-March end-of-year adjustments made once further information becomes available, including the accrual of tax revenues reflecting assessments of tax returns and valuation adjustments for assets and liabilities. Post-March adjustments may also include the accrual of measures announced in the budget that are recorded upon receipt of Royal Assent of enabling legislation.

- Table 7, Condensed Statement of Assets and Liabilities, is included in the monthly Fiscal Monitor following the finalization and publication of the government's financial results for the preceding fiscal year, typically in the fall.

- Reclassification of comparative information and adjustment to opening balances:

- Starting in 2022-23, the government has adopted a new standard of the Public Sector Accounting Board regarding asset retirement obligations. Asset retirement obligations represent requirements under an agreement, contract, legislation, or a constructive or equitable obligation to undertake specific actions to retire tangible capital assets at the end of their useful lives. This includes activities such as decommissioning of nuclear reactors and removal of asbestos. The adoption of this standard has not had a material effect on the budgetary balance for the current year. This standard has been applied on a modified retroactive basis and the prior year's budgetary transactions have not been restated for the purposes of The Fiscal Monitor. However, an adjustment to the opening balance of the accumulated deficit for 2022-23 has been reflected in Table 7, Condensed Statement of Assets and Liabilities. The amount of this adjustment may be revised as more information becomes available.

- Also starting in 2022-23, the government has adopted a new standard of the Public Sector Accounting Board regarding financial instruments. Financial instruments include receivables, payables, equity instruments, debt, and derivatives, such as forward contracts and cross-currency swaps. Under the new standard, derivatives, which were previously recorded at historical cost, are recognized at fair value. Changes in the fair value of derivatives are not reflected in the budgetary balance, but are instead charged directly to the accumulated deficit as remeasurement gains and losses. The adoption of this standard has also resulted in the reclassification of certain accounts, as follows:

- cross-currency swaps, previously reported as part of unmatured debt, are classified as derivatives and reported outside of unmatured debt;

- forward contracts, previously reported as part of accounts payable and accrued liabilities, are reported as derivatives;

- accrued interest, previously reported as part of accounts payable and accrued liabilities, is now included with the associated category of unmatured debt (i.e., marketable bonds, treasury bills, and foreign currency borrowings); and,

- unamortized discounts and premiums on market debt, previously reported as a separate item within unmatured debt, are now included with the associated category of unmatured debt (i.e., marketable bonds, treasury bills, and foreign currency borrowings).

A reconciliation of the reclassification and adjustment to the opening balance of the government's financial position as at April 1, 2022 is summarized as follows:

| March 31, 2022 Closing balance1 | Effect of change in accounting policy for asset retirement obligations | Effect of change in accounting policy for financial instruments | April 1, 2022 Opening balance | |||||

|---|---|---|---|---|---|---|---|---|

| Liabilities | ||||||||

| Accounts payable and accrued liabilities | 260,288 | 6,095 | (4,163) | 262,220 | ||||

| Derivative financial liabilities | - | - | 2,778 | 2,778 | ||||

| Interest-bearing debt | ||||||||

Unmatured debt |

||||||||

Payable in Canadian currency |

||||||||

Marketable bonds |

1,030,896 | - | 13,093 | 1,043,989 | ||||

Treasury bills |

187,381 | - | (504) | 186,877 | ||||

Subtotal |

1,218,277 | - | 12,589 | 1,230,866 | ||||

Payable in foreign currencies |

14,451 | - | 22 | 14,473 | ||||

Cross-currency swap revaluation |

(2,246) | - | 2,246 | - | ||||

Unamortized discounts and premiums on market debt |

7,443 | - | (7,443) | - | ||||

Obligations related to capital leases and other unmatured debt |

5,366 | - | - | 5,366 | ||||

Total unmatured debt |

1,243,291 | - | 7,414 | 1,250,705 | ||||

| Pension and other liabilities | 335,078 | - | - | 335,078 | ||||

| Total interest-bearing debt | 1,578,369 | - | 7,414 | 1,585,783 | ||||

| Total liabilities | 1,838,657 | 6,095 | 6,029 | 1,850,781 | ||||

| Financial assets | ||||||||

Derivative financial assets |

- | - | 3,403 | 3,403 | ||||

Other financial assets |

600,291 | - | - | 600,291 | ||||

| Total financial assets | 600,291 | - | 3,403 | 603,694 | ||||

| Net debt | 1,238,366 | 6,095 | 2,626 | 1,247,087 | ||||

| Non-financial assets | 103,873 | 1,395 | - | 105,268 | ||||

| Federal debt (accumulated deficit) | 1,134,493 | 4,700 | 2,626 | 1,141,819 | ||||

1 Source: Public Accounts of Canada 2022. |

||||||||

Note: Unless otherwise noted, changes in financial results are presented on a year-over-year basis.

For inquiries about this publication, contact Bradley.Recker@fin.gc.ca.

December 2022

©His Majesty the King in right of Canada, as represented by the Deputy Prime Minister and Minister of Finance, 2022

All rights reserved

All requests for permission to reproduce this document or any part thereof shall be addressed to the Department of Finance Canada.

Cette publication est également disponible en français.

Cat. No.: F12-4E-PDF

ISSN: 1487-0134