Evaluation of the Chief Financial Officer attestation for Cabinet submissions

On this page

- Introduction

- Results at a glance

- Evaluation context

- Evaluation methodology and scope

- Limitation of the evaluation

- Relevance

- Effectiveness

- Appendix A: logic model for chief financial officer attestation for Cabinet submissions

- Appendix B: evaluation methodology

- Appendix C: Management Response and Action Plan

Introduction

This document presents the evaluation of the Chief Financial Officer (CFO) attestation for Cabinet submissions, which was led by the Treasury Board Secretariat’s (TBS’s) Internal Audit and Evaluation Bureau with the assistance of Goss Gilroy Inc. The evaluation was conducted in accordance with the Treasury Board (TB) Policy on Results. It took place between November 2019 and August 2020 and assessed the relevance and effectiveness of the CFO attestation and the 2016 Guideline on CFO Attestation for Cabinet Submissions.

Results at a glance

- There is an ongoing need for the CFO attestation as an effective practice that provides independent assurance to submission owners that financial risks have been considered in TB submissions.

- Attestations are an appropriate way of achieving consistency and robust due diligence in the activities undertaken by CFOs when reviewing TB submissions.

- The Guideline on Chief Financial Officer Attestation for Cabinet Submissions has enabled a clear and consistent approach to due diligence. The guideline has not had the same influence on joint submissions (multi‑departmental), submission from small departments or submissions from departments that do not have formal centralized processes.

- Submission owners recognize CFOs as valuable business advisors. CFOs are usually involved early in the TB submission process, although this is not the case in all departments.

- Although there is a greater awareness of financial risk as a result of CFO attestations, there is a lack of consistency in risk disclosure among CFOs. Only half of assessed TB submissions (based on TBS 2019–20 Departmental Results Report) transparently disclose financial risk.

- The CFO attestations have improved the understanding of data limitations. Despite some progress, challenges remain in relation to data quality and completeness.

Evaluation context

The Guideline on Chief Financial Officer Attestation for Cabinet Submissions was published in January 2014 and amended in April 2016 to enhance the CFO attestation process and bring decision‑making into line with the modern approach to comptrollership.Footnote 1

The purpose of the guideline is to provide a framework for CFOs in the due diligence review and attestation of the financial management aspects of Cabinet submissions. In this process, CFOs review TB submissions sponsored by their department and, when satisfied, sign off by way of a CFO attestation that is appended to the submissions.

CFO attestations do not attest to a policy’s or program’s effectiveness. Rather, they support the expectations and financial due diligence needs of deputy heads, ministers, central agencies and Cabinet committees. They also help promote a coherent and consistent approach to CFO due diligence review across government.

The CFO attestation contains six fundamental assertions that support decision‑making:

- The nature and extent of the proposal is reasonably described, and material assumptions having a bearing on the associated financial requirements have been disclosed and are supported.

- Significant risks having a bearing on the financial requirements, the sensitivity of the financial requirements to changes in key assumptions, and the related risk mitigation strategies have been disclosed.

- Financial resource requirements have been disclosed and are consistent with the assumptions stated in the proposal, and options to contain costs have been considered.

- Funding has been identified and is sufficient to address the financial requirements for the expected duration of the proposal.

- The proposal is compliant with relevant financial management legislation and policies, and the proper financial management authorities are in place or are being sought through the proposal.

- Key financial controls are in place to support the implementation and ongoing operation of the proposal.

Evaluation methodology and scope

The evaluation examined the following six issue areas:

- the need for the CFO attestation

- the appropriateness of the attestation instrument

- the clarity and consistency of the approach to due diligence since the guideline was implemented

- the extent of meaningful involvement of CFOs

- the improvement of awareness of financial risk

- the understanding of data limitations

A logic model was developed with the Office of the Comptroller General for the evaluation (see Appendix A).

The evaluation covered CFO attestation requirements for TB submissions only. Attestation requirements for memoranda to Cabinet are supported by different guidance materials and different assertion areas. The evaluation also did not seek to assess program or project financial costing capacity or capabilities in departments.

The evaluation covered the time period from the implementation of the revised guideline on the CFO attestation (April 2016) to January 2020.

The methodology is described in Appendix B.

The lines of evidence were:

- comparative jurisdictional review

- document review

- interviews (29)

- focus groups (2)

- case studies (5)

Limitation of the evaluation

The COVID‑19 pandemic precluded interviews with deputy heads; however, an interview with the Secretary of the Treasury Board and assistant deputy ministers who are responsible for Cabinet submissions provided proxy information.

Relevance

Ongoing need for the CFO attestation

Conclusion

There is an ongoing need for the CFO attestation as it provides independent assurance to submission owners that financial risks have been considered in TB submissions.

Findings

Pursuant to the Policy on Financial Management, departmental CFOs are responsible for “ensuring the accuracy and reasonableness of key departmental financial information, financial statements, disclosures and reports, including the Cabinet submission documents by way of a CFO attestation.”

All respondent groups and case study departments agree that CFO attestations are still needed and are a part of a sound financial management and governance process. Case studies indicated that CFO attestations are relevant, given they provide an objective and independent opinion. Many case study participants mentioned that their deputy minister, their minister or both highly value having this separate independent perspective and advice in their decision‑making.

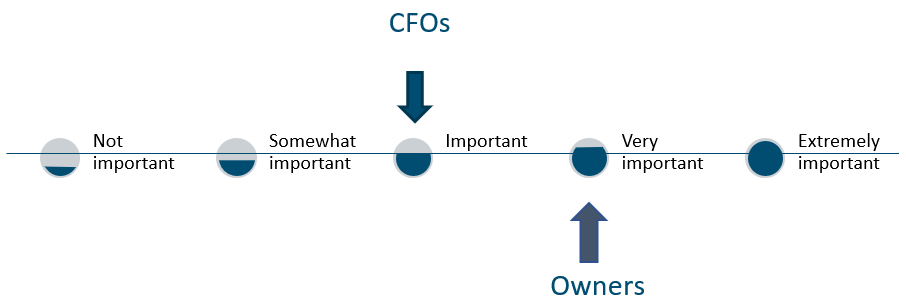

Key informants representing CFOs and Cabinet submission‑owners perceive the CFO attestation mechanism to be important for their department and for government overall (Figure 1).

Figure 1 - Text version

Possible responses are shown horizontally on a 5-level rating scale. From left to right, the levels are:

- Not important

- Somewhat important

- Important

- Very important

- Extremely important

CFOs perceive the attestation mechanism to be important.

Cabinet submission-owners perceive the attestation to be very important.

Submission owners interviewed and case study departments acknowledged that CFO attestations complement other risk processes. The fiscal lens the CFO brings to the due diligence process helps align perspectives on financial and implementation risks. According to more than half of the submission owners interviewed, insight into the “big picture” of financial practicality across TB submissions in a department (for example, total available funding) had been lacking in the past. CFO attestations have provided increased assurance that plans are reasonable and that the impact on the overall budget, and alignment with available funding in the organization, is known.

Case study findings indicate an ongoing need for the attestation process in order to continue encouraging program representatives to pay more attention to numbers, which leads to greater rigour on financial elements, a more thorough accounting of all risks, and better‑quality TB submissions.

Interviews with CFOs and TB submission‑owners reveal that the attestation fosters wider involvement and more shared responsibility in departments in the development of TB submissions. The submissions are no longer being developed exclusively by one part of the organization, further enhancing integration and reducing risk.

CFOs indicate that the attestation mechanism strengthens their ability to engage early with program representatives. It raises awareness of the advantages of the financial due diligence function. Thematic results from the case studies also support the notion that the attestation process has helped formalize the role of the CFO throughout the submission process.

Submission owners see value in the attestation mechanism in that it provides them with access to expert oversight. Furthermore, they recognize the need for scrutiny and challenge on the disclosure of financial risks.

Appropriateness of attestation instrument

Conclusion

Attestations are an appropriate way of achieving consistency and robust due diligence in the activities undertaken by CFOs when reviewing TB submissions.

Findings

Interviewed CFOs and submission owners did not identify any necessary changes to CFO attestations. They perceive attestations as part of their duty and professional practice. The professionalization of the CFO role was noted as providing deputy heads with increased assurance of and confidence in the financial soundness of TB submissions.

Further, CFOs and submission owners view the six assertions in the guideline as integral to financial risk management. They add that the guideline reinforces the importance of due diligence in the management of public funds and clarifies the six areas of assertion.

A review of 29 TB submissions dated from 2017 to 2020 confirmed that the six standard assertions were used consistently in CFO attestations across departments. Furthermore, there were no observations or qualifications added to a CFO attestation that did not align with one of the defined areas (in other words, no categories were missing).

The jurisdictional review identified similar benefits in the UK government attestation model. According to UK government documents and a key informant, UK accounting officer (AO) assessments, which had guidance documents introduced in 2015Footnote 2 and 2017,Footnote 3 have contributed to several outcomes:

- a more systematic and consistent approach

- earlier and more meaningful involvement of AOs

- stronger and more thorough business cases

- more transparency through greater financial risk disclosure

UK AO tools include The Green Book, which provides detailed direction on how the valuation of costs and benefits should be assessed; The Accounting Officer’s Survival Guide; and a guidance document on preparing AO assessment summaries.

In both the UK and Canada, the attestation is considered to have the following benefits:

- earlier and more meaningful involvement of AOs or CFOs

- risks and uncertainties are more transparent and documented

- increased thoroughness

- more participation by program staff

- systematic and consistent approach

Unlike in the UK, however, in Canada, the attestation is not considered to be an instrument that increases transparency.

To test the counterfactual, in this case, the absence of CFO attestations, interviewee groups were asked to identify potential impacts of the absence of a CFO attestation and a guideline. The responses were similar to the findings for the UK. CFOs, submission owners and the case studies participants identified the following impacts:

- less consistency in the review process

- less discipline in relation to costing

- less certainty that review of the key areas needed for due diligence was being investigated dependably across government

- less austerity of assessments

Interviewee groups were unanimous on the importance of having both a CFO attestation and a guideline. In other words, the absence of either of them would negatively impact departments and financial due diligence across the Government of Canada.

When evaluators asked about improvements to the guideline, many CFOs interviewed voiced that assertion 6, “Key financial controls are in place to support the implementation and ongoing operation of the proposal,” was possibly redundant, given that the CFO responsibility to maintain an effective system of internal controls is already covered under the Financial Administration Act and the Policy on Financial Management.

Some case study participants also flagged the need for clarity in the guideline regarding the need for a CFO attestation when funds are not being requested in a submission.

Effectiveness

In this section

Clear and consistent approach to due diligence

Conclusion

The Guideline on Chief Financial Officer Attestation for Cabinet Submissions has enabled a clear and consistent approach to due diligence. The guideline has not had the same influence on joint (multi‑departmental) submissions, submissions from small departments, or submissions from departments that do not have formal centralized processes.

Findings

Interviewed CFOs agreed the guideline provides a good base for a consistent approach. It has helped implement centralized processes in some departments. From this base, CFOs have

developed their own tools and processes to meet specific needs in their departments, for example:

- the application of standard methodologies

- checklists and templates to guide processes

- due diligence reports prepared using more working‑paper documentation

- coordinated working groups established within program areas

Across the case studies, interviewees also said that their departments had restructured to better meet the needs of the CFO attestation process. Case study interviews in departments of various sizes found that the more centralized the financial management unit was (for example, the submission team was integrated under the direction of the CFO), the more consistent they reported their TB submission and CFO attestation process to be.

CFOs who could compare pre‑2016 attestation processes with those in place after the implementation of the revised guideline stated that due diligence is more detailed now. In particular, CFOs explained that due diligence is now more database‑ and evidence‑driven. Case study respondents noted that the guideline has contributed to consistency by providing a common structure for due diligence and a more rigorous working framework. This gives better assurance that the CFO will have the information needed to attest with confidence.

Case study respondents also believed uniformity will continue to improve as expertise is strengthened over time and processes become more normalized.

In addition, submission owners mentioned greater consistency among submissions in their departments, partly because of closer collaboration with CFOs in the development of TB submissions. They praised the guideline for its clarity on the six areas of focus related to financial risk, as well as for having succeeded in instilling strong consistency in the format of CFO attestations.

The document review and TBS program sector analysts indicated that CFO attestations from across the Government of Canada now tend to follow the same format and consistently contain all six assertions. Further, CFOs agreed that the guideline provides clarity about what they must attest to and ensures that they have a common understanding of the areas they review.

Nonetheless, CFOs and submission owners identified challenges with the clarity and consistency of approach, particularly among small departments and those without centralized processes. This suggests that some minimal level of expertise or departmental capacity may be necessary to efficiently undertake the attestation process or that, in some departments, the CFO’s role may be unclear.

Respondents also reported challenges related to joint submissions, especially for smaller departments. It was noted that consistency is often challenging, as each department has a different role and a due diligence processes. Some interviewed CFOs and submission owners noted that there are variations in departments’ and CFOs’ interpretations of requirements and in their approaches to financial risk. It was said:

“Some CFOs follow instructions to the letter and take good measures. Others are quick to approve and seem to have too much confidence in the level of risk.”

For small departments, joint submissions can require a high level of effort in organizations not necessarily equipped with the needed resources. As examples of this, some CFOs interviewed noted that not all departments assign highly experienced financial officers to projects that would likely benefit from it and that some CFOs tend to give approval quickly while others require a lot more time and tend to ask many more questions. Some case study interviewees suggested that it would be helpful to have more consistency in joint submissions by, for example, obtaining general agreement on wording and on the amount of detail to provide.

Meaningful involvement of CFOs

Conclusion

Submission owners recognize CFOs as valuable business advisors. CFOs are usually involved early in the TB submission process, although this is not the case in all departments

Findings

Like Canada, the UK has wrestled with how to encourage early involvement of AOs in the proposal development process. In addressing this, the UK guidanceFootnote 4 promotes early involvement of AOs as a good practice for new or challenging proposals. It also requires more frequent AO assessments for major projects or programs. This means explicit AO sign‑off is required at all key stages of major projects and initiatives. The review also found that the UK’s AO assessments helped motivate more detailed and thorough business‑case proposals because these are required to undergo AO checks and to satisfy all essential AO standards.

One of the key benefits of the guideline that CFOs interviewed identified was the mechanism to engage program representatives earlier in the submission process, allowing them to play a more meaningful role. Their early involvement helps CFOs in three main ways:

- It positions them as contributors and allies

- Allows them to act as a single window for program representatives in departments, an advantage noted by submission owners

- It resolves financial risks or issues arising during due diligence prior to TB submissions being finalized

Submission owners also indicated that they find value working with CFOs earlier in the process and mentioned benefitting from their challenge throughout the development of the submission.

Some submission owners indicated that there has been an increase in the comprehensive involvement of CFOs compared to prior years. As it was said:

“The journey is as important as the actual attestation.”

The increased CFO involvement has positively influenced the quality of TB submissions by thoroughly challenging proposals and providing advice to programs. This includes reviewing the storyline, financials and options for cost containment. Submission owners further noted that guidance and support often went deeper than just financial advice, which helped prevent future surprises and challenges.

However, some CFOs face ongoing challenges in dealing with perceptions that attestations are a type of finance policing. It was pointed out in one case study that program analysts in departments do not always understand how they could benefit from earlier and closer CFO involvement. This department acknowledged that additional change management is needed internally.

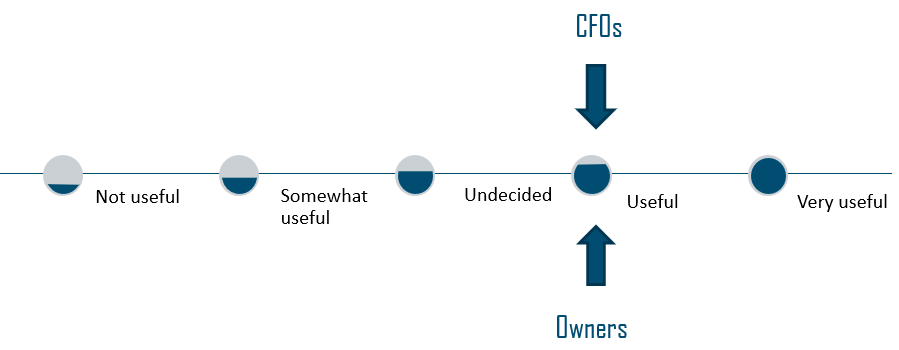

CFOs and submission owners viewed the attestation’s contribution as meaningful and useful to decision‑making (Figure 2) and identified the following factors that influence the value of the attestation process:

- strong leadership and buy‑in from the executive team

- deputy heads that have CFOs with a seat at the management table (this is not yet pervasive across the Government of Canada but is improving)

- the prioritization of financial stewardship in the department

- wider involvement and shared responsibility in the development of TB submissions (relationships with programs)

- more time to understand program files through earlier CFO involvement

Figure 2 - Text version

Possible responses are shown horizontally on a 5-level rating scale. From left to right, the levels are:

- Not useful

- Somewhat useful

- Undecided

- Useful

- Very useful

Both CFOs and Cabinet submission-owners perceive the CFO attestations to be useful.

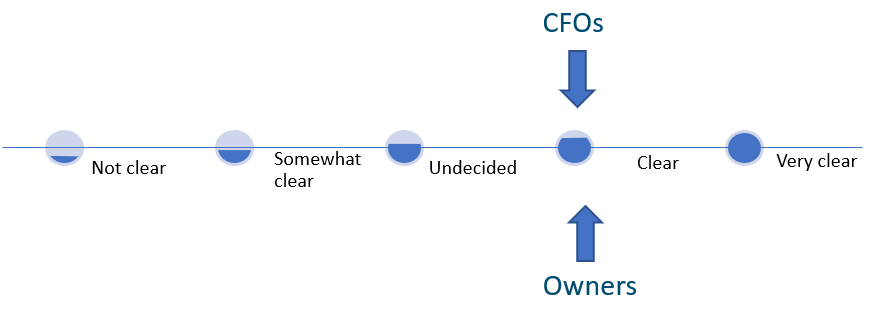

Interviewed CFOs and submission owners perceived the roles and accountabilities of all parties as being well understood and clear (Figure 3). CFOs mentioned they are now well entrenched in the submission process and the value of meaningful engagement is well recognized.

Figure 3 - Text version

Possible responses are shown horizontally on a 5-level rating scale. From left to right, the levels are:

- Not clear

- Somewhat clear

- Undecided

- Clear

- Very clear

Both CFOs and Cabinet submission-owners perceive the CFO attestations to be clear.

Improved awareness of risk

Conclusion

Although there is a greater awareness of financial risk as a result of CFO attestations, there is a lack of consistency in risk disclosure among CFOs. Only half of assessed TB submissions (based on the 2019–20 Departmental Results Report) transparently disclose financial risk.

Findings

The jurisdictional review identified a higher level of transparency in the UK, where a summary of assessments is documented in their Government Major Projects Portfolio. The summary provides Parliament with the key points that informed AO assessments and clarifies the basis on which they were approved. These summary documents are made public in the UK in the interest of transparency. The issue of transparency is pertinent in the Canadian context, where federal initiatives on open government and proactive publication provisions aim to increase transparency in government.

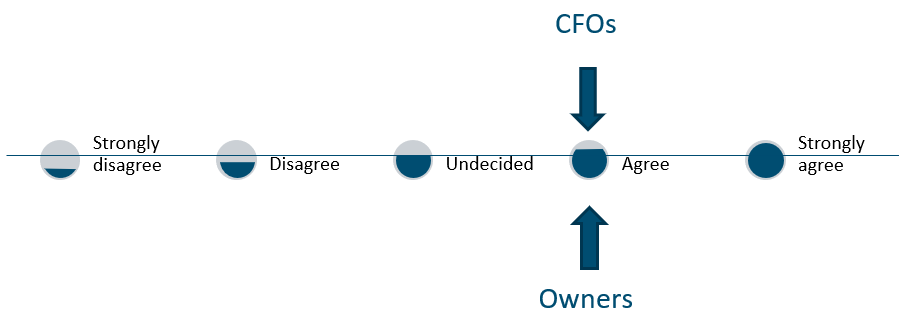

Interviewed CFOs, submission owners and case study participants all agree that financial risks and potential impacts are better understood through the attestation requirement. Submission owners indicated that it allowed them to have a clearer understanding of CFO‑validated financial risks (Figure 4).

Figure 4 - Text version

Possible responses are shown horizontally on a 5-level rating scale. From left to right, the levels are:

- Strongly disagree

- Disagree

- Undecided

- Agree

- Strongly agree

Both CFOs and Cabinet submission-owners agree that CFO attestations support understanding of financial risks and their impacts.

A review of 29 TB submissions found that 41% of the CFO attestations that were deemed to be medium‑ and high‑risk contained observations. These observations frequently provided additional details not found elsewhere in the submission. In some cases, they were carried forward to the TB submission précis.

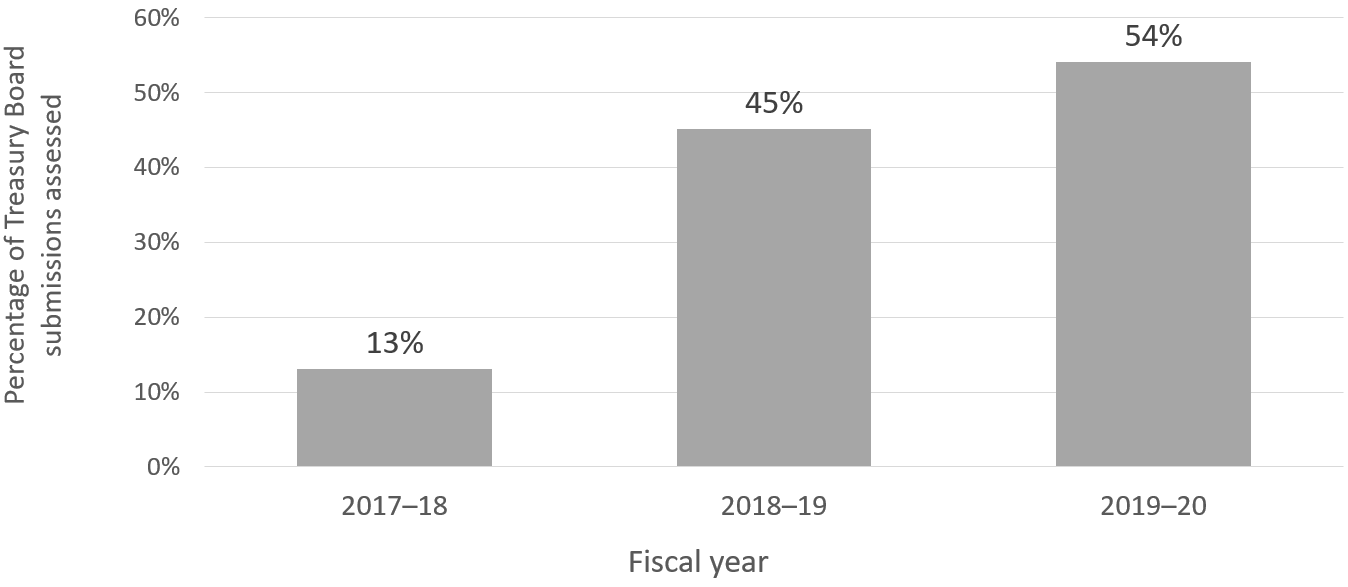

The document review indicated that the CFO attestation process may also be contributing to greater transparency in risk disclosure. The TBS 2019–20 Departmental Results Report showed that there was significant improvement in the transparent disclosure of risk for assessed submissions (from 13% in 2017–18 to 54% in 2019–20) (Figure 5). Nonetheless, only half of assessed TB submissions (based on TBS 2019–20 Departmental Results Report) transparently disclose financial risk.

Figure 5 - Text version

| Fiscal year | Percentage of Treasury Board submissions assessed that disclosed risk |

|---|---|

| 2017–18 | 13 |

| 2018–19 | 45 |

| 2019–20 | 54 |

Source: 2019–20 Departmental Results Report, Treasury Board of Canada Secretariat

TBS program sectors both support and challenge departments in the development of TB submissions. They also develop submission advice (the précis) for ministers. TBS program sector analysts stated that many attestations arrive without any residual financial risk observations raised by CFOs. It was also at times unclear whether CFOs were actually aware of issues raised by TBS. The analysts indicated that they could undertake their roles more effectively, would have better insight and provide stronger advice to ministers if they were provided with the range of considerations CFOs use in exercising their judgment on a TB submission. This would be similar to the UK practice described above, where summaries of the key points that inform AO assessments are provided and clarify the basis on which projects are approved.

Case study evidence also found that the disclosure of considerations is inconsistent, varying widely by CFO. As one case study respondent explained, “Some CFOs write three pages of caveats, while others write nothing at all…. CFO signatures are the only ones ministers see besides the deputy’s, indicating that CFO attestations are important. However, if no comments are included in the attestation, it is difficult to say whether ministers have an improved awareness of financial risks.”

CFOs who frequently write comments confirmed they appreciate the flexibility in the attestation, in large part, because it gives context to the information being presented. CFOs are able to document their comments on the cost and approval of the submission, raise issues to senior management regarding supplementary estimates, flag budget considerations, or note limitations in the review process.

Financial risks related to business assumptions and concerns about value for money were thematic findings emerging from the case studies. Though most case study respondents agreed that CFO attestations help provide decision‑makers with a more complete understanding of financial risks, many indicated that they did not agree that CFO attestations provide decision‑makers with a more complete understanding of potential impacts on project success, or at least, not beyond the extent to which funding or costing risk might impinge on implementing a project. As one respondent explained, “Though we have gotten pretty good at determining what things might cost, this has not helped provide insight into what the right program or resource requirement is.” Increasing the transparency of considerations that go into CFO attestations could inform the advice given to TB ministers, thereby providing them with greater insight into the impact of financial risks on project success.

Improved understanding of data limitations

Conclusion

CFO attestations have improved the understanding of data limitations. Despite some progress, challenges remain in relation to data quality and completeness.

Findings

Interviewed CFOs and submission owners noted that deputy heads are briefed and know in advance when data limitations in a proposal require CFO observations.

CFOs noted that attestations have forced better costing methodologies, including more attention to assumptions and financial risks, but there is still room for improvement.

All interviewee groups spoke of issues within departments related to costing in submissions. In particular, some highlighted ongoing structural tendencies to overestimate staff requirements and underestimate time and complexity. It was said:

Costing capacity does not equal due diligence. It’s about internal control management and risk management. the Attestation hits the nail on the head.

CFOs acknowledged that these issues exist and agreed that costing can always be improved. However, they emphasized that numbers and assumptions are increasingly being challenged by way of the CFO attestation process. Thus, data limitations are acknowledged, and costing is improving.

A related ongoing challenge found through interviews and the document review was the issue of cost estimates. Interviewees believe that TB submission cost estimates have low levels of certainty as they represent a point in time and are based on future‑oriented information.

Another challenge raised by CFOs and submission owners is that they do not feel well equipped to determine whether the projected human resources are realistic or sufficient. This then impedes the department’s ability to reconcile classification needs, define human resources structures and outline internal supports to implementation (in other words, the availability of full‑time equivalents (FTEs)). Many acknowledged a need for better insight and forecasting tools for FTE estimates.

Finally, some interviewees indicated that departments tend to struggle more with data limitations on submissions for new initiatives and with those that differ from what they are accustomed to delivering in their regular core business or expertise. Additionally, CFOs mentioned encountering difficulties with items that fall outside of their control, for example, projects that are weather dependent, or projects where there is limited historical data or no precedent.

Recommendations

It is recommended that the Office of the Comptroller General:

- Establish a mechanism to share best practices that would guide small departments, departments that do not have formal centralized process for the CFO attestation for TB submissions, and departments that are working together on submissions (multi‑department submissions)

- Provide guidance and support:

- on CFO attestations for joint submissions to increase consistency and to set expectations

- on data gaps to determine full-time equivalent requirements

- in cases when a CFO attestation is needed but where funds are not requested

- Explore ways to increase financial risk transparency in the CFO attestation process to improve the consistency of risk disclosure across the Government of Canada

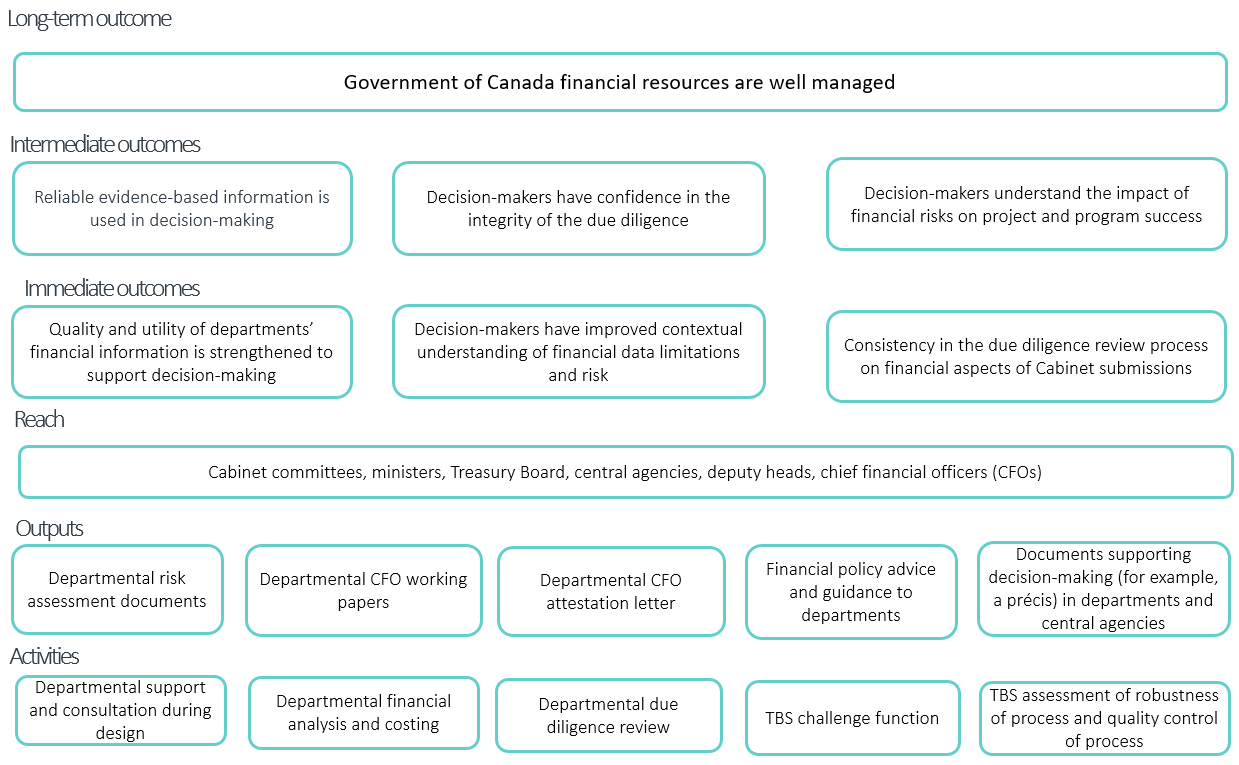

Appendix A: logic model for chief financial officer attestation for Cabinet submissions

Appendix A - Text version

Long-term outcome

Government of Canada financial resources are well managed

Intermediate outcomes

- Reliable evidence-based information is used in decision making

- Decision-makers have confidence in the integrity of the due diligence

- Decision-makers understand the impact of financial risks on project and program success

Immediate outcomes

- Quality and utility of departments’ financial information is strengthened to support decision-making

- Decision-makers have improved contextual understanding of financial data limitations and risk

- Consistency in the due diligence review process on financial aspects of Cabinet submissions

Reach

Cabinet committees, ministers, Treasury Board, central agencies, deputy heads, chief financial officers (CFOs)

Outputs

- Departmental risk assessment documents

- Departmental CFO working papers

- Departmental CFO attestation letter

- Financial policy advice and guidance to departments

- Documents supporting decision-making (for example a précis) in departments and central agencies

Activities

- Departmental support and consultation during design

- Departmental financial analysis and costing

- Departmental due diligence review

- TBS challenge function

- TBS assessment of robustness of process and quality control of process

Appendix B: evaluation methodology

In this section

The evaluation was guided by an approved evaluation framework, which was a detailed plan of the evaluation activities, questions and indicators.

The development of the evaluation framework included the conduct of 11 scoping interviews with Treasury Board Secretariat (TBS) program and corporate sectors, as well as portfolio leads, in order to broaden the evaluation team’s understanding of the CFO attestation and its relationship to other areas of work in TBS. A logic model (see Appendix B) was also developed in collaboration with the Office of the Comptroller General in order to capture expected outcomes of the CFO attestation mechanism and the intended effects of the revised Guideline on Chief Financial Officer Attestation for Cabinet Submissions. The logic model was developed specifically for use during the evaluation. The agreed‑upon outcomes of the CFO attestation for Cabinet submissions are as follows:

Immediate outcomes

- Quality and utility of departments’ financial information is strengthened to support decision making

- Decision makers have improved contextual understanding of financial data limitations and risk

- Consistency in the due diligence review process on financial aspects of Cabinet submission

Intermediate outcomes

- Reliable evidence-based information is used in decision making

- Decision makers have confidence in the integrity of the due diligence

- Decision makers understand the impact of financial risks on project and program success

As a result of the scoping interviews and the determination of expected outcomes, the evaluation focused on the following six issue areas:

- the need for the CFO attestation

- the appropriateness of the attestation instrument

- the clarity and consistency of the approach to due diligence since the guideline was implemented

- the extent of meaningful involvement of CFOs

- the improvement of awareness of financial risk

- the understanding of data limitations

Evaluation questions

Once the issue areas were defined, the evaluation questions were finalized. They fell into two categories:

- relevance

- effectiveness

Relevance

- How well does the Guideline on CFO Attestation align with the needs of decision‑makers?

- Do the conditions that drove the initial use of attestations continue to exist today?

Effectiveness

- Is the Guideline on CFO Attestation encouraging a clear and consistent approach to the due‑diligence review process on the financial aspects of Cabinet submissions across government?

- Is the Guideline on CFO Attestation driving more meaningful and earlier involvement of departmental CFOs in the planning and decision‑making process?

- Is the Guideline on CFO Attestation helping improve the awareness of financial risk presented for decision‑making at all levels?

- Is the Guideline on CFO Attestation allowing decision‑makers to have a better ability to understand the context of data limitations surrounding projects being submitted to Cabinet?

- Is the Guideline on CFO Attestation the most appropriate instrument to achieve the intended outcomes?

Methodology

Consistent with best practices, the evaluation of the CFO attestation for Cabinet submissions used multiple lines of evidence to ensure that reliable and sufficient information was produced. The methods used in the evaluation are summarized below.

Jurisdictional review

A jurisdictional review was conducted to gather publicly available information about CFO attestation models both nationally and internationally. Five jurisdictions were included in the review:

- Australia

- New Zealand

- Sweden

- United Kingdom

- the United States

- Quebec

The objective of the jurisdictional review was to review the attributes of alternate models and assess potential options for the Canadian model. The review included a comprehensive document search and follow‑up interviews with representatives when possible.

Document review

A sample of 29 Treasury Board submissions from 6 government departments was reviewed. The documents were scanned with special attention given to the form and content of CFO attestations and to financial and program risks listed throughout the submission. CFO attestations were assessed for consistency and completeness. Risks and observations on the assertions in the CFO attestation (or lack of observations) were noted and compared with risks and other items highlighted in the précis and in decision letters to identify possible gaps and evidence related to the reach of observations made in CFO attestations.

Key informant interviews

The key informant interviews sought to gather factual information, as well as personal views, from key informants selected. Interview guides were designed to address most evaluation issues and questions. Interviews were conducted with the following groups of respondents:

- 21 CFOs and financial analysts from 20 departments

- 8 Cabinet submission‑owners from 8 departments, including a combination of assistant deputy ministers, directors general and directors

Focus groups with TBS program sector analysts

Two focus groups were conducted with six TBS program sector analysts in order to gather information on the relevance and effectiveness of CFO attestations and to allow for the exploration of common trends in CFO attestations. Two more TBS analysts who could not attend the focus groups also participated in the evaluation using different means: one analyst provided their answers to the focus group questions by email; the other analyst participated by way of a one‑on‑one interview.

Case studies

Case studies explored multiple Cabinet submissions in a department for consistency and application of the CFO attestation, including timeliness of CFO involvement.

The case studies looked at submissions from the following:

- The two large departments that had the most volume in the September 2018 to August 2019 period (Public Services and Procurement Canada (PSPC) and Employment and Social Development Canada)

- The small department that had the most volume in the September 2018 to August 2019 period (Social Sciences and Humanities Research Council of Canada)

- The large department that has had the most growth and is part of the Costing Centre of Expertise costing pilot (Department of Fisheries and Oceans)

- A large department that has the CFO in an effective position of assistant deputy minister and CFO (Department of National Defence)

Interviews were completed with the CFO of each of the following departments and with Cabinet submission‑owners who were identified by the CFO. The number of interviews is in parentheses.

- Public Services and Procurement Canada (3)

- Employment and Social Development Canada (4)

- Social Sciences and Humanities Research Council of Canada (3)

- Fisheries and Oceans Canada (3)

- National Defence (3)

Appendix C: Management Response and Action Plan

In this section

The Financial Management Sector (FMS) of the Office of the Comptroller General’s (OCG’s) Office, Treasury Board of Canada Secretariat (TBS), has reviewed the evaluation report and agrees with the recommendations. Proposed actions to address the recommendations of the report are outlined in the table below.

Recommendation 1

It is recommended that OCG establish a mechanism to share best practices that would guide small departments, departments that do not have a formal centralized process for the CFO attestation for TB submission, and departments that are working together on submissions (multi-department submissions).

Management response

The OCG agrees that a mechanism needs to be established to share and guide CFO Attestation best practices for small departments, departments that do not have a formal centralized process for the CFO attestation for TB submissions and multi-department submissions.

| Proposed actions for recommendation 1 | Start date | Targeted completion date | Office of primary interest |

|---|---|---|---|

|

1. In the short term, FMS will:

|

September 2021 |

March 2022 |

FMS |

|

2. in the mid-term, FMS will build the GCpedia site and post the Guideline on Chief Financial Attestation for Cabinet Submissions along with supplementary guidance that supports CFO Attestation users. |

March 2022 |

September 2022 |

FMS |

Recommendation 2

It is recommended that the OCG provide guidance and support:

- on CFO attestations for joint submissions to increase consistency and to set expectations

- on data gaps to determine full-time equivalent (FTE) requirements

- in cases when a CFO attestation is needed, but where funds are not requested

Management response

The OCG agrees with the recommendation that additional CFO Attestation guidance and support for joint submissions and cases where funds are not requested is required. Similarly, the OCG agrees that additional actions are required to address the data gaps in determining FTE requirements.

| Proposed actions for recommendation 2 | Start date | Targeted completion date | Office of primary interest |

|---|---|---|---|

|

2.a In consultation with key stakeholders, FMS will develop supplementary guidance for the GCpedia site that will clarify expectations and increase consistency where joint submissions are required. |

March 2022 |

September 2022 |

FMS |

|

2.b In consultation with the GC Costing Community of Practice, FMS will:

|

December 2021 |

September 2022 |

FMS |

|

2.c In consultation with key stakeholders, FMS will develop supplementary guidance for the GCpedia site that supports cases where a CFO Attestation is required but funds are not requested. |

March 2022 |

September 2022 |

FMS |

Recommendation 3

It is recommended that OCG explore ways to increase financial risk transparency in the CFO Attestation process to improve the consistency of risk disclosure across the Government of Canada.

Management response

The OCG agrees with the recommendation to explore ways to increase financial risk transparency in the CFO Attestation process.

| Proposed actions for recommendation 3 | Start date | Targeted completion date | Office of primary interest |

|---|---|---|---|

|

FMS will start providing informational sessions within TBS on the CFO Attestation process in the Government of Canada. These briefings will highlight the due diligence process that CFOs follow and how TBS can support the consistent and transparent disclosure of financial risk in Cabinet documents. |

January 2022 |

March 2022 |

FMS |

|

FMS will work with Strategic Communications and Ministerial Affairs and program sectors on TBS’s Guidance for Drafters of Treasury Board Submissions to strengthen the “Risks” section and the Risk Appendix of submissions in future updates to the drafters’ guidance. |

September 2021 |

March 2022 |

FMS |