Briefing binder created for the Minister of Finance and National Revenue and the Deputy Minister of Finance on the occasion of their appearance at the Standing Committee on Finance on October 6, 2025 on the Budgetary Cycle 2025-26 and Bill C-4, An Act respecting certain affordability measures for Canadians and another measure

Table of contents

- Bill C-4, Making Life More Affordable for Canadians Act

- Backgrounder: A New Approach to Budgeting

- Budget Cycle 2025-26

- Timing of Federal and PT Budgets

- Affordability Measures

- Building Canada Act and Major Projects Office

- Comprehensive Expenditure Review

- Canada-U.S. Trade and Tariffs

- Chinese and Other Tariffs

- Combatting Financial Crimes (Anti-Money Laundering Measures)

- Defence Spending (incl. Ukraine)

- Debt Management Strategy

- Draft Legislation on Previously Announced Tax Measures

- Economic and Fiscal Overview

- Canada Key Financial Metrics

- G7 Fiscal Comparison

- Grocery Affordability / Food Inflation

- Housing Affordability

- Pre-Budget Consultations 2025

- Committee Member Biographies

Bill C-4, Making Life More Affordable for Canadians Act

Key Facts and Figures

- Bill C-4 proposes to:

- Reduce the lowest personal tax rate from 15 per cent to 14 per cent, providing tax relief for nearly 22 million Canadians.

- Rate of 14.5 per cent applies for 2025.

- Individuals could receive tax relief of up to $420 in 2026 (the first full year where the rate would be 14 per cent).

- Two-income families could receive tax relief up to $840.

- Eliminate the Goods and Services Tax (GST) for first-time home buyers on new homes valued up to $1 million, saving them up to $50,000, and lower the GST for first-time home buyers on new homes valued between $1 million and $1.5 million.

- Remove the consumer carbon price from law, following the ceasing of its application, effective April 1, 2025.

- Amend the Canada Elections Act to make changes to the requirements relating to political parties' for the protection of personal information.

- Reduce the lowest personal tax rate from 15 per cent to 14 per cent, providing tax relief for nearly 22 million Canadians.

- The bill was adopted at Second Reading in the House of Commons with all party support on June 12, 2025. The bill currently stands referred to the Standing Committee on Finance for study.

Supplementary Information

Bill C-4, Making Life More Affordable for Canadians Act, is composed of four parts:

- Part 1 amends the Income Tax Act to reduce the marginal personal income tax rate on the lowest tax bracket ($57,375 and below in 2025) to 14.5% for the 2025 taxation year and to 14% for the 2026 and subsequent taxation years.

- Nearly 22 million Canadians would benefit from tax relief of up to $420 per person in 2026, saving two-income families up to $840 a year.

- The bulk of tax relief will go to individuals whose total taxable income is under $114,750 in 2025, with nearly half of the relief benefitting Canadians in the first bracket (taxable income $57,375 and below in 2025).

- The Canada Revenue Agency has updated its source deduction tables for the July to December 2025 period so that employers and pay administrators were able to reduce tax withholdings as of July 1. This means that individuals with employment income and other income subject to source deductions could already have tax withheld at the new rate of 14 per cent. Otherwise, individuals will realize this tax relief when they file their 2025 tax returns in spring 2026.

- Part 2 amends the Excise Tax Act and related regulations to implement a temporary GST new housing rebate for first-time home buyers.

- It is estimated this measure will save first-time home buyers a total of $3.9 billion over five years.

- Eliminating the GST on new homes up to $1 million and lowering GST on new homes up to $1.5 million will also create demand for newly built homes, which could in turn help spur new construction. Expanding the housing stock is key to addressing housing affordability issues.

- The measure is intended to help first-time home buyers enter the housing market, rather than people who already own a home.

- Part 3 repeals Part 1 of the Greenhouse Gas Pollution Pricing Act and the Fuel Charge Regulations.

- Part 4 amends the Canada Elections Act to make changes to the requirements relating to political parties' policies for the protection of personal information.

Issues Raised by Parliamentarians and Stakeholders

Part 1 – Income Tax Act

Some senators and stakeholders have questioned the potentially negative impact that the reduction to the first personal tax rate (and thus the non-refundable credit rate) will have for certain individuals who receive non-refundable tax credits, particularly on the Disability Tax Credit (DTC) and the Medical Expense Tax Credit (METC).

Question:

Will the government address concerns about the consequences of reducing the first personal tax rate from 15% to 14% on Canadians who receive tax relief under the Disability Tax Credit and the Medical Expense Tax Credit?

Response:

For any tax change, what matters is the impact on an individual's overall tax bill. For millions of Canadians, including 4.5 million individuals who claim the Disability Tax Credit and/or Medical Expense Tax Credit, tax savings from the middle-class tax cut will outweigh the reduction in the value of non-refundable credits.

The Government has heard the concerns about the potential negative impact of C-4 on a very small number of the people who receive the Disability and/or Medical Expense tax credits. We are taking a closer look at this issue.

Part 2 – Excise Tax Act

- Some stakeholders questioned why the GST rebate for new homes only applies to purchases under agreements entered into on or after May 27, 2025.

Question:

Why doesn't the policy apply to purchases that had not closed prior to May 27, 2025?

Response:

Any time there is a change in policy, there will be people that fall on either side of the change. Individuals that have already decided to buy a new home before May 27, 2025 agreed to a price that did not reflect the measure. This approach ensures fairness since it treats all buyers who entered into agreements before May 27 the same way.

Part 3 - Greenhouse Gas Pollution Pricing Act

- Members of parliament and senators may question why Part 1 of the Greenhouse Gas Pollution Pricing Act (GGPA) is being repealed in phases.

Question:

Why is it necessary to proceed with the repeal in phases rather than all at once?

Response:

A sequential repeal of the fuel charge provisions would help ensure an orderly process for charge payers. Charge payers will have a further six months to claim rebates to which they are entitled, for example for fuel charge paid on fuel purchased prior to April 1, 2025 but exported on or after that date from a province or territory where the fuel charge applied. Various administrative provisions will remain in the legislation for a longer period to provide continuity and certainty for final wind-down activities, including CRA administrative processes that may continue to rely on existing rules, such as definitions. These additional phases of repeal relate to fuel charge obligations for reporting periods prior to April 1, 2025. The fuel charge ceased to apply as of April 1, 2025.

- During Second Reading debate several Conservative Party members called for the government to also repeal Part 2 of the GGPPA which implements an output-based pricing system on large emitters in listed jurisdictions.

- The Bloc Quebecois has argued that it is unfair for the government to have proceeded with a final Canada Carbon Rebate payment in April 2025 (only in provinces where the fuel charge applied) that was not funded by the fuel charge but out of the consolidated revenue fund.

Question:

Why did the government provide a final Canada Carbon Rebate payment in April 2025 only to residents of provinces where the fuel charge applied?

Response:

As part of the transition away from the fuel charge, eligible Canadians received a final Canada Carbon Rebate payment, starting in April 2025.

The government decided to provide this final payment to eligible households in provinces where the federal fuel charge applied because Canadian families, especially low-income families, had been counting on it, and planning their family budgets on the assumption they would be getting it.

The federal fuel charge only applied in provinces that did not have their own systems in place to put a consumer price on pollution, and the majority of proceeds from the federal fuel charge were returned to households in these provinces via the Canada Carbon Rebate.

Part 4 - Canada Elections Act

- No major concerns were raised by opposition parties in the House of Commons about Part 4. During second reading debate, MP Bonk (CPC) noted that the government should be taking the opportunity to create a clear, principled and enforceable privacy framework. He went on to note that while the bill addresses jurisdictional gaps, it should not be mistaken for a comprehensive solution.

- Concerns have been raised in the senate regarding Part 4 provisions weakening privacy protections and potentially leaving voters' personal information vulnerable to misuse by political parties

Question:

Why would federal political parties be exempt from complying with provincial personal information protection laws? Is this in response to the ongoing litigation out of British Columbia?

Response:

In 2022, British Columbia's Information and Privacy Commissioner found that the provincial act, the Personal Information Protection Act, applies to federal political parties in the province. This opens the door to competing authorities and a patchwork of provincial privacy rules applicable to federal political parties, where the obligations of federal political parties vary across jurisdictions, which could lead to uncertainty, inefficiency, confusion, and ultimately an erosion of trust amongst voters in how their personal information is managed. The federal government has been clear that the Canada Elections Act provides a uniform federal approach in respect of federal political parties' activities involving personal information, including but not limited to collection, use, disclosure, retention, and disposal.

- While it is not expected to receive much attention, opposition parties may ask about how Part 4 will be enforced.

Question:

What happens if someone does not comply with the privacy policy?

Response:

Federal political parties and those acting on their behalf (e.g., volunteers) will be required to comply or may newly face consequences under the Canada Elections Act's existing enforcement regime, including caution and information letters or, if warranted, an administrative monetary penalty of $50 to $1,500 for a person or $300 to $5,000 for an entity.

Question:

Will the Privacy Commissioner have a role?

Response:

No. Consistent with the regulation of federal political parties through the Canada Elections Act, regulatory oversight would remain with the Chief Electoral Officer and the Commissioner of Canada Elections. The Privacy Commissioner does not have a mandate under the Act. This bill does not change that.

- In addition, Green Party Leader Elizabeth May argued that Part 4 has no clear link with affordability, therefore turning C-4 into an omnibus bill which would require separate votes.

An Act respecting certain affordability measures for Canadians and another measure

Part 1 – Income Tax Act

Lowering Income Tax Rates for Individuals

Key Messages

- The federal government is proposing to reduce the lowest personal tax rate from 15 per cent to 14 per cent, effective July 1, 2025, which will put more money back into the pockets of hard-working Canadians.

- Working Canadians could already be seeing these tax savings on their pay cheques as of July 1 when withholding rates were adjusted.

- Individuals who benefit would receive tax relief of up to $420 in 2026 (the first full-year where the rate would be 14 per cent), and two-income families would receive tax relief up to $840.

Questions & Answers

Q. The Government announced that the lowest personal income tax rate is changing to 14% effective July 1, 2025. If so, why will the tax rate be 14.5% for the 2025 taxation year? What happens to employment income that has had tax withheld at 15% in the first half of the year?

A. Income is reported and tax is calculated on an annual basis. To reflect a one-percentage-point cut in the lowest tax rate coming into effect halfway through the year, the full-year tax rate for 2025 would be 14.5 per cent and the full-year rate for 2026 and future tax years would be 14 per cent.

This approach would make the proposed tax rate reduction simple for all Canadians.

The Canada Revenue Agency has updated its source deduction tables for the July to December 2025 period so that pay administrators were able to reduce tax withholdings as of July 1. This means that, since July 1, individuals with employment income and other income subject to source deductions could have tax withheld at 14 per cent. Otherwise, individuals would realize this tax relief when they file their 2025 tax returns in spring 2026.

Q. How much will the tax rate reduction cost?

A. This middle-class tax cut is expected to provide $2.6 billion in tax relief to Canadians in 2025 and $5.4 billion in 2026, the first full year when the tax rate is 14 per cent. Over five years, the total fiscal cost would be $27.2 billion.

Q. Who will benefit the most from this tax cut? Is this tax cut going to help Canadians struggling with a higher cost of living?

A. Nearly 22 million Canadians would benefit from tax relief of up to $420 per person in 2026, saving two-income families up to $840 a year.

The bulk of tax relief will go to those with incomes in the two lowest tax brackets whose total taxable income is under $114,750 in 2025, with nearly half of the relief benefitting Canadians in the first bracket (taxable income $57,375 and below in 2025).

Q. Why is the credit rate applied to most non-refundable tax credits also being lowered?

A. The rate applied to most non-refundable tax credits is linked to the first personal income tax rate to offset the tax on income that was used to pay for the expenses that are recognized by these credits.

The lowest tax rate is used to determine this offsetting amount given that all taxpayers, in every tax bracket, pay tax at the lowest rate on at least a portion of their income. Using the same credit rate for all individuals ensures that our tax system is fair, and that those claiming similar amounts receive the same amount of tax relief, regardless of their income level.

As such, the credit rate will automatically adjust to reflect the lower tax rate of 14.5 per cent for 2025 and 14 per cent starting in 2026.

Background

Canada's personal income tax system has a progressive rate structure where tax rates increase with income. Marginal tax rates currently range from 15 per cent to 33 per cent and bracket thresholds are indexed to inflation so that they keep up with the cost of living.

This measure would reduce the first tax rate, which applies to taxable income of $57,375 and below in 2025, from 15 per cent to 14 per cent.

As income is reported and tax is calculated on an annual basis, to reflect a one-percentage-point cut in the lowest tax rate coming into effect halfway through the year (i.e., on July 1, 2025), the full-year tax rate for 2025 would be 14.5 per cent and the full-year rate for 2026 and future tax years would be 14 per cent. The rate applied to most non-refundable tax credits would continue to be the same as the lowest personal income tax rate.

This change would benefit nearly 22 million Canadians. Individuals who benefit would receive tax relief of up to $420 in 2026 (the first full year where the rate would be 14 per cent) and two-income families would receive tax relief up to $840.

The Canada Revenue Agency has updated its source deduction tables for the July to December 2025 period so that pay administrators were able to reduce tax withholdings as of July 1. This means that, since July 1, individuals with employment income and other income subject to source deductions could have tax withheld at 14 per cent. Otherwise, individuals would realize this tax relief when they file their 2025 tax returns in spring 2026.

Part 2 - Amendments to the Excise Tax Act and Related Regulations

First-Time Home Buyers' GST Rebate

Key Messages

- The First-Time Home Buyers' GST Rebate is intended to help first-time home buyers access the housing market.

- The measure would eliminate the GST for homes up to $1 million and provide partial GST relief for homes between $1 million and $1.5 million.

- This measure will save Canadians up to $50,000 on a new home – allowing more young people and families to enter the housing market.

Questions & Answers

Q. Why doesn't the policy apply to recent purchases that have not yet closed?

A. Any time there is a change in policy, there will be people that fall on either side of the change. The approach the Government has taken ensures that the GST relief accords with the dual purpose of the measure – which is to:

- incentivize first-time home buyers to buy a newly built home by lowering upfront costs; and

- in turn, encourage developers to increase the supply of new housing to meet the increase in demand.

Providing the rebate to first-time home buyers who have already entered into an agreement would not serve either of these purposes.

This is also the fairest approach. It ensures that home buyers who entered into agreements before the May 27 announcement – and who agreed to a price that would not have reflected the rebate – are all treated equally, regardless of the closing date on their homes.

It would be unfair to extend the rebate to some of those buyers but not others based solely on their closing date.

*Redacted*

Q. What is this measure meant to do?

A. The measure would eliminate the GST for first-time home buyers of homes up to $1 million and reduce the GST for first-time home buyers of homes between $1 million and $1.5 million. This will reduce the upfront cost of buying a new home for these buyers in order to help them enter the housing market.

Q. Why is the measure restricted to first-time home buyers, why not all buyers?

A. The measure is intended to help first-time home buyers enter the housing market, rather than people who already own a home.

Q. Why does the test to determine whether a person is a first-time home buyer only look back four years?

A. This timeframe is consistent with that used for the other federal tax measures including the First Home Savings Account, the Home Buyers' Plan, and the Homebuyers' Tax Credit and will facilitate administration and compliance.

*Redacted*

Q. What is the government hoping to achieve by removing the GST on new homes for first-time home buyers?

A. This measure could incentivize first-time home buyers to consider buying a newly built home rather than a home in the re-sale market. This increased demand for newly built homes would encourage developers to build more homes to meet this demand, which could in turn have a positive effect on housing supply. Expanding the housing stock is key to addressing housing affordability issues.

Q. Why is the measure temporary?

A. The measure is intended to not only assist first-time home buyers enter the housing market, but also to encourage developers to quickly ramp up supply to meet this demand. The temporary nature of the measure is expected to accelerate this activity to take advantage of the availability of the rebate.

Q. Does this measure also relieve the provincial portion of HST? If not, can provinces choose to relieve the provincial portion of HST?

A. This is a federal rebate that applies only to the 5% GST or federal component of the HST. It does not apply to the provincial component of HST. Questions regarding the provincial component of the HST should be directed to the HST provinces.

Q. How many more units will be built because of the measure?

A. This measure may incentivize first-time home buyers to consider buying a newly built home rather than a home in the re-sale market. This increased demand for newly built homes could encourage developers to build more homes to meet this demand. It would be imprudent to estimate how many additional housing units will be built because of this measure given the many other factors that impact housing supply. However, the measure is expected to have a positive impact on housing supply.

Q. What is the estimated fiscal cost of the measure?

A. This measure is expected to deliver $3.9 billion in tax savings to Canadians over five years, starting in 2025-26.

*Redacted*

| Estimated Cost (in $ millions) | 24-25 | 25-26 | 26-27 | 27-28 | 28-29 | 29-30 | Total |

|---|---|---|---|---|---|---|---|

| First-Time Home Buyers' GST Rebate | 0 | 145 | 735 | 950 | 1,025 | 1,055 | 3,910 |

The cost is lower in the initial years to account for (1) purchase agreements entered into prior to the implementation date that are ineligible for the rebate, and (2) the lag in claims associated with average construction times, as the rebate is only available upon the completion of the unit.

Q. This measure applies to a relatively small number of homes. It only applies to new homes, which are small fraction of a home sales, and then, only those purchased by a first-time home buyer. Will this measure move the needle on housing affordability?

A. It is estimated that at maturity the measure would apply to approximately 47,000 newly built homes annually. This will provide meaningful relief to young Canadians across the country in their pursuit of owning a home.

Q. What about renters—what measures are being taken to support those who aren't looking to buy a home but are struggling with high rents?

A. The government has already introduced a 100% GST rebate for new purpose-built rental housing, which is having a positive impact on the construction of new rental housing. This increased supply of rental units will in turn help make renting more affordable for those who cannot or do not want to own their home.

Q. How does this measure support Canadians in high-cost markets like Vancouver or Toronto versus smaller communities?

A. In addition to fully relieving the GST on new homes up to $1 million, the measure provides a partial GST rebate for homes between $1 million and $1.5 million. This feature of the measure is intended to ensure that the rebate is also available in high-cost markets like in Vancouver and Toronto.

Across Canada, the vast majority of First-Time Home Buyers would qualify for full GST relief since they are generally buying new homes under $1 million—the average home price for a First-Time Home Buyer is around $500,000.

Background

This measure introduces the First-Time Home Buyers' GST Rebate, which is intended to assist individuals entering the housing market for the first time and to encourage real estate developers to increase housing supply. The rebate would provide 100% relief of the GST on new homes priced up to $1 million and partial GST relief for homes priced between $1 million and $1.5 million. The rebate would provide up to $50,000 of relief on the purchase of a new home by an eligible first-time home buyer.

The measure would generally be available to eligible first-time home buyers, who are individuals that:

- are at least 18 years of age;

- are a Canadian citizen or permanent resident; and

- have not, in the current year or the previous four years, lived in a home owned by either themselves or their spouse/common-law partner as the individual's primary place of residence.

The types of housing for which the relief would apply would be the same types of housing eligible for the existing GST New Housing Rebate, including:

- detached homes, semi-detached homes, rowhouses, townhomes, and duplexes;

- residential condominium units;

- certain shares of cooperative housing corporations; and

- mobile homes and floating homes.

The measure would generally apply to purchases under agreements entered into on or after May 27, 2025 and to owner-built homes where construction begins on or after May 27, 2025. The measure is temporary and would generally not apply to new housing purchases under an agreement entered into after 2030 or to housing for which construction begins after 2030.

Part 3 - Amendments to the Greenhouse Gas Pollution Pricing Act and Other Related Texts

Removing the consumer carbon price from Canadian law

Key Messages

- The proposed amendments would repeal the fuel charge framework under the Greenhouse Gas Pollution Pricing Act. This follows the regulations made in March that ceased the application of the federal fuel charge, effective April 1, 2025.

- This repeal would occur in four phases, starting with the retroactive repeal of charging provisions effective April 1, 2025. Other provisions would be sequentially repealed to ensure an orderly process for charge payers with respect to past reporting periods.

- The proposed legislative amendments would provide certainty to Canadian consumers and businesses about the elimination of the consumer carbon price.

Questions & Answers

Q. Why is legislation needed if the fuel charge application has already been ceased via regulations?

A. Repealing the fuel charge legislative framework under Part I of the Greenhouse Gas Pollution Pricing Act (GGPPA) would provide certainty to Canadian consumers and businesses about the permanent elimination of the consumer carbon price.

Q. Why is it necessary to proceed with the repeal in phases rather than all at once?

A. A sequential repeal of the fuel charge provisions would help ensure an orderly process for charge payers. Charge payers will have a further six months to claim rebates to which they are entitled, for example for fuel charge paid on fuel purchased prior to April 1, 2025 but exported on or after that date from a province or territory where the fuel charge applied. Various administrative provisions will remain in the legislation for a longer period to provide continuity and certainty for final wind-down activities, including CRA administrative processes that may continue to rely on existing rules such as definitions. These additional phases of repeal relate to fuel charge obligations for reporting periods prior to April 1, 2025. The fuel charge ceased to apply as of April 1, 2025.

Q. What is the impact of the fuel charge repeal on emissions?

A. As the fuel charge was effectively already removed via regulations made in March 2025, there is no incremental impact on emissions from the proposed legislative amendments.

That said, as indicated in the Regulatory Impact Analysis Statement accompanying the regulations made in March 2025, the Department of Finance Canada, using Environment and Climate Change Canada's emissions data, estimated that the elimination of the fuel charge would lead to a loss of 12.57 Mt cumulative greenhouse gas emissions reductions from 2025 to 2030.

Impacts on emission reductions may be mitigated by other future climate policies implemented in place of the fuel charge. The federal government intends to refocus federal carbon pollution pricing requirements on ensuring carbon pricing systems are in place across Canada on a broad range of greenhouse gas emissions from industry.

Q. What is the impact on inflation of the fuel charge repeal?

A. As the fuel charge was effectively already removed via regulations made in March 2025, there is no incremental impact on inflation from the proposed legislative amendments.

That said, the Department of Finance estimated that eliminating the fuel charge could reduce the Consumer Price Index by about 0.7 percentage point in the first year.

Statistics Canada data showed a year-over-year decrease in CPI in April compared to March, primarily driven by a reduction in energy prices.

Q. After the cessation of the fuel charge, why did the government provide a final Canada Carbon Rebate payment in April 2025 to only residents of provinces where the fuel charge applied?

A. As part of the transition away from the fuel charge, eligible Canadians received a final Canada Carbon Rebate payment in April, 2025.

The government decided to provide this final payment to eligible households in provinces where the federal fuel charge applied because Canadian families, especially low-income families, had been counting on it, and planning their family budgets on the assumption they would be getting it.

The federal fuel charge only applied in provinces that did not have their own systems in place to put a consumer price on pollution, and the majority of proceeds from the federal fuel charge were returned to households in these provinces via the Canada Carbon Rebate.

Background

This measure would permanently repeal the fuel charge framework in Part 1 of the Greenhouse Gas Pollution Pricing Act (GGPPA). The measure would legislate the repeal of the consumer carbon price after regulations were made to remove the fuel charge effective April 1, 2025.

The proposed amendments would come into force in four phases to ensure an orderly process for charge payers and the Canada Revenue Agency:

- In the first phase, charging provisions would be retroactively repealed as of April 1, 2025.

- In the second phase, provisions allowing for certain rebates would be repealed as of October 1, 2025. For example, this would allow charge payers to claim a rebate for fuel charge paid before April 1, 2025 on fuel that is exported on or after April 1, 2025.

- All registration provisions would be repealed as of November 1, 2025, giving registrants until October 31 to file returns to claim rebates arising before October 1.

- All remaining provisions of Part 1 of the GGPPA would be repealed, including definitions, interpretation rules, administrative and procedural rules, effective April 1, 2035. This would provide continuity and certainty for final wind-down activities, including Canada Revenue Agency's processes that continue to rely on existing rules. This continuity also ensures that fuel charge payers have the ability to interact with the government in a predictable and straightforward manner in respect of any residual fuel charge obligations.

The measure does not extend to Part 2 of the GGPPA, which implements an output-based pricing system on large emitters in listed jurisdictions.

Part 4 - Canada Elections Act

Canada Elections Act

Key Messages

- In Part 4, Bill C-4 clarifies that the activities of federal political parties involving personal information fall exclusively under federal jurisdiction and the Canada Elections Act.

- If passed, it would underscore that federal political parties are not required to comply with provincial personal information protection laws and solidify the Canada Elections Act as the exclusive, national and uniform regime regarding the protection of personal information by federal political parties across Canada.

- It would also clarify that this has been the case since May 31, 2000, which is when the Canada Elections Act was repealed and replaced through a major modernization.

- Bill C-4 proposes broader requirements for federal policy parties with respect to their privacy policies going forward, covering more than simply data use and collection, and requiring they be available in both official languages and written in plain language.

Questions & Answers

Q. If Bill C-4 is passed, what will be required of federal political parties with respect to privacy?

A. If passed, eligible and registered federal political parties will need to ensure their personal information protection policies (privacy policies) comply with new requirements. For example, privacy policies will need to be updated to be made available in both official languages, written in plain language, and state the types of personal information the party collects, retains, uses, discloses, disposes of, etc. Federal political parties will also be required to explain how they carry out their activities in relation to personal information using illustrative examples.

Q. What happens if someone does not comply with the privacy policy?

A. Federal political parties and those acting on their behalf (e.g., volunteers) will be required to comply or may newly face consequences under the Canada Elections Act's existing enforcement regime, including caution and information letters or, if warranted, an administrative monetary penalty of $50 to $1,500 for a person or $300 to $5,000 for an entity.

Q. Will the Privacy Commissioner have a role?

A. No. Consistent with the regulation of federal political parties through the Canada Elections Act, regulatory oversight would remain with the Chief Electoral Officer and the Commissioner of Canada Elections. The Privacy Commissioner does not have a mandate under the Act. This bill does not change that.

Q. Why are federal political parties not covered by the Personal Information Protection and Electronic Documents Act (PIPEDA) or the Privacy Act?

A. PIPEDA applies to organizations engaged in a commercial activity, while the Privacy Act applies to federal government institutions. Because federal political parties are neither engaged in commercial activities nor government institutions, neither legislation governs the personal information practices of federal political parties. As unique democratic actors, Parliament has addressed the personal information practices of federal political parties exclusively under the Canada Elections Act, which governs the registration of federal political parties and regulates their other activities.

Q. Why was this measure included in a tax bill?

A. It was included in the earliest available vehicle to clarify Parliament's intent regarding questions pertaining to federal jurisdiction of privacy requirements for federal political parties.

Q. Why is the regime being made retroactive to 2000?

A. In June 2023, the Canada Elections Act was amended to clarify that it was and remains the national, uniform, exclusive and complete regime for federal political parties' dealings with personal information. However, the 2023 amendment itself was not expressly retroactive despite clear intention on the Government's part. Consequently, Bill C-4 seeks to further clarify Parliament's intention to assert federal jurisdiction over federal political parties' dealings with personal information since 2000, which is when the Act was repealed and replaced through a major modernization.

Q. Why would federal political parties be exempt from complying with provincial personal information protection laws? Is this in response to the ongoing litigation out of British Columbia?

A. In 2022, British Columbia's Information and Privacy Commissioner found that the provincial act, the Personal Information Protection Act, applies to federal political parties in the province. This opens the door to competing authorities and a patchwork of provincial privacy rules applicable to federal political parties, where the obligations of federal political parties vary across jurisdictions, which could lead to uncertainty, inefficiency, confusion, and ultimately an erosion of trust amongst voters in how their personal information is managed. The federal government has been clear that the Canada Elections Act provides a uniform federal approach in respect of federal political parties' activities involving personal information, including but not limited to collection, use, disclosure, retention, and disposal.

Q. Why are the more robust privacy requirements that were part of Bill C-65, which died on the order paper, not included as part of this proposal?

A. The Canada Elections Act is regularly reviewed for improvements, but the priority at this time is to clarify Parliament's intent regarding federal jurisdiction over federal political parties' dealings with personal information.

Background

Bill C-4, An Act respecting certain affordability measures for Canadians and another measure, seeks to clarify Parliament's intent that the activities of federal political parties involving personal information fall exclusively under federal jurisdiction and the Canada Elections Act.

If passed, Bill C-4 would underscore that federal political parties are not required to comply with provincial personal information protection laws, consistent with Parliament's intention that the Canada Elections Act is the exclusive, national, and uniform personal information protection regime for these parties across Canada.

It would further clarify that this has been the case since May 31, 2000, which is when the Canada Elections Act was repealed and replaced through a major modernization.

The bill also proposes additional requirements for a federal political party's privacy policy going forward, including that it: be available in both official languages; be written in plain language; state the types of personal information it collects, retains, uses, discloses, disposes, etc.; and explain how federal political parties carry out their activities in relation to personal information, including using illustrative examples.

Backgrounder: A New Approach to Budgeting

The government is adopting a new way of budgeting that will make capital investment a national priority. The cornerstone of this new budgeting approach is a Capital Budgeting Framework that distinguishes day-to-day operational spending from expenditure that stimulates public and private sector capital investment. Applying this lens in government decision-making will help identify and prioritize actions that support the government's objective of catalyzing $500 billion of incremental private sector investment *redacted*. It will also support two important fiscal objectives for Budget 2025:

- Balancing day-to-day operating spending with revenues by 2028-29, to shift the composition of overall spending towards capital investments.

- Maintaining a declining deficit-to-GDP ratio over the forecast horizon, to ensure disciplined fiscal management for future generations.

The framework will be applied to the federal budget, while preserving comparability across different fiscal publications. It is designed to augment—not replace— existing financial reporting. The Public Accounts of Canada will remain fully compliant with Public Sector Accounting Standards, which permit capitalization of costs for assets under government control.

Going forward, the government will also transition to a fall budgeting cycle, starting with Budget 2025. The fall timing, before the Main Estimates, will improve transparency and facilitate the oversight of public expenditure for Parliamentarians. It will also support effective financial planning for federal departments and agencies, provinces and territories, tax experts and businesses. Organizations that rely on federal funding to deliver programs and services to Canadians will also have clarity on available funding ahead of the fiscal year and ahead of the construction season, ensuring projects can get underway without delay. The fall budget will be complemented by an economic and fiscal update in the spring.

The importance of capital formation

Capital investments are the building blocks to economic growth. By improving Canada's productivity, capital investment fosters more—and better paying—jobs, supporting rising living standards over the long-term. However, U.S. business investment has increased steadily, Canada's has struggled, remaining close to its 2015 level (Chart 1). Further, while many countries have accelerated investment in intellectual property, advanced technologies, and modern manufacturing to strengthen their economic potential, Canada's investment has been significantly less concentrated in these types of forward-looking productivity enhancing investments (Chart 2). This lag in investment has constrained innovation, created risks to Canada's competitiveness, and has left the economy less resilient. This investment gap poses a growing challenge in a global economy increasingly shaped by shifting trade dynamics and rapid adoption of artificial intelligence. Without a step-change in capital investment, Canada risks falling further behind. Addressing this requires renewed commitment from both the public and private sectors to make capital investments a national priority.

Real non-residential business investment since 2000, Canada and U.S, 2000Q1-2025Q2

Non-residential investment as a share of GDP, Canada and U.S., 2023

Capital Budgeting Framework

The new Capital Budgeting Framework establishes a consistent way to classify spending, including tax expenditures, that contribute to capital formation—referred to here as capital investment—while maintaining pre-existing categories used in budgets and financial reports. Drawing on best practices from other advanced economies, and adapted to the Canadian context, it sets out clear, standardized criteria to assess whether a given measure qualifies as capital investment.

Under this framework, capital investment is defined broadly as any government expense or tax expenditure that contributes to public or private sector capital formation, held directly on the government's balance sheet or on that of a private sector entity, Indigenous community or another level of government. Within this broad definition, the intent is to focus on capital investments that meet the following criteria:

- Conditionality – whether the funding recipient is required to invest in capital formation to receive the benefit.

- Clear linkage – whether the spending encourages or enables capital investment in identifiable sectors or projects.

Spending that is not categorized as capital investment would be considered day-to-day operating spending. This would include major government expenditures like transfers to persons, health and social transfers, and the costs of running government operations and services, including salaries and benefits. The government is committed to balancing its operating spending with revenues by 2028-29.

Applying the above criteria, government spending classified as capital spending would generally be categorized as follows:

- Capital transfers - transfers to other levels of government and organizations that are expressly intended for the recipient to invest in infrastructure or a productive asset.

- Capital-focused corporate income tax incentives - tax expenditures intended to incentivize new capital formation.

- Capital amortization - expenses recorded to spread the cost of capital assets owned or controlled by the federal government over their useful lives.

- Private sector research and development - direct funding, or tax incentives, for research and development activities that enable commercialization or scale-up and raise future productive capacity.

- Support to unlock large-scale private sector capital investment - negotiated agreements with proponents involving exceptional, significant operating subsidies designed to unlock incremental large-scale private capital investments.

- Incentives to grow the housing stock - measures that accelerate new housing supply.

It is estimated that current projected spending in these categories, before decisions since the 2024 Fall Economic Statement and Budget 2025 measures, is between 1.2 and 1.4% of GDP. Further details will be released in Budget 2025, enabling Canadians to better understand how fiscal choices support future economic capacity.

Public Accounts

As a responsible fiscal manager, the government remains committed to ensuring the objectivity and integrity of its financial statements, which are presented in the Public Accounts of Canada. Results in this form will continue to be based on Canadian public sector accounting standards.

The lens of the new Capital Budgeting Framework will be applied to the federal budget, while preserving the ability for users to compare information across different financial publications, including the Public Accounts of Canada. The budget will continue to include tables categorizing planned spending according to Public Accounts concepts, in order to maintain the ability to compare budgeted amounts with results.

Fall Budgeting Cycle

The transition to a fall budgeting cycle will begin with Budget 2025, and will have the following implications:

- Pre-budget consultations will now take place in summer.

- The budget will be delivered in the fall, ahead of the Main Estimates.

- The budget will be the government's main fiscal event, followed by a spring economic and fiscal update as the new fiscal year begins.

Having a budget in the fall—well ahead of the new fiscal year—will mean:

- Greater predictability and better planning for organizations, businesses, provincial and territorial budget planners, and Canadians.

- More budget measures can be included in time for the Main Estimates, enabling parliamentarians to better oversee public expenditures. This responds to calls by the House of Commons Standing Committee on Government Operations and Estimates (OGGO) and the Parliamentary Budget Officer (PBO) for greater alignment between the budget and Main Estimates, which must be tabled in Parliament by March 1st every year.

- Additional time for parliamentary consideration of budget legislation for the coming fiscal year.

- Align better to construction season, ensuring projects can get underway without delay.

The government remains committed to consulting on the implementation of budget measures, including tax and legislation.

Fiscal Anchors

The government will commit itself to two fiscal anchors, and an overarching target, as part of responsible fiscal planning and in recognition of major once-in-a-generation shifts in the global economic order:

- Balancing day-to-day operating spending with revenues by 2028-29, to shift the composition of overall spending towards capital investments.

- Maintaining a declining deficit-to-GDP ratio over the forecast horizon, to ensure disciplined fiscal management for future generations.

The fiscal target that will drive this government will be to catalyze $500 billion in private investment through shifting the composition of spending toward capital investment.

Implementation

- [The 2025 Public Accounts of Canada will be tabled on October [X], 2025.]

- The release of Budget 2025 on November 4, 2025, will mark a shift to a fall budgeting cycle.

- Budget 2025 will present and apply the government's new Capital Budgeting Framework.

Related product

- News Release

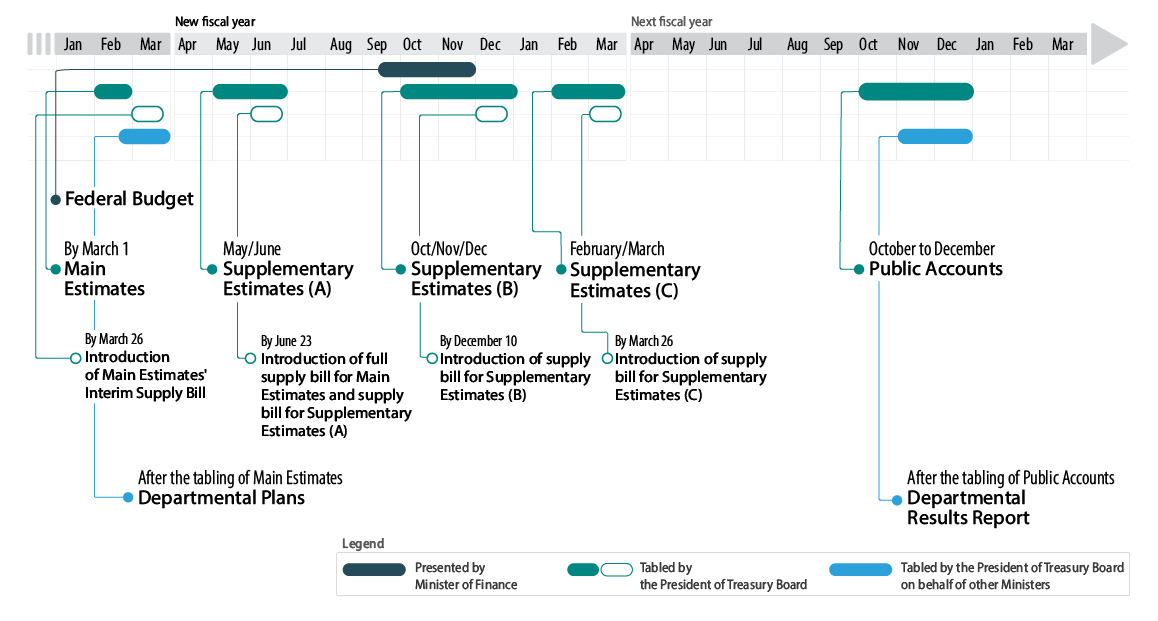

Budget Cycle 2025-26

Parliamentary cycle in fall budget scenario, with PT budget timing and traditional construction season.

| Before a new fiscal year** | ||

|---|---|---|

| June - Aug | Pre-budget consultations | |

| Fall | Federal Budget | |

| Federal | Provincial / Territorial*** | |

| Feb - April | Main estimates | Budgets Main estimates |

| Departmental plans | ||

| Interim supply | ||

| During the fiscal year | ||

| Spring | Economic and Fiscal Update | |

| May | Supplementary estimates (A) | |

| June - Aug | Approval of full supply / End of supply period | |

| Oct - Nov | Supplementary estimates (B) | |

| Dec | End of supply period | |

| Feb - April | Supplementary estimates (C) | |

| Mar | End of supply period | |

| After the fiscal year | ||

| Spring to fall | Traditional construction season | |

| Oct | Public Accounts of Canada | |

| Nov | Departmental results reports | |

|

*Table replicated from the House of Commons' Financial Procedures website ("An Overview of the Financial Cycle"), with date adjustments to reflect the change to a fall budgeting cycle, provincial and territorial budgeting dates, and the timing of the traditional construction season. **Presently, House of Commons Standing Order 83.1 provides that the Standing Committee on Finance shall conduct a pre-Budget consultations study each September to December. In light of the Government's change to a fall Budget, the House may decide to change its Standing Orders to require the committee to conduct this study in the spring for the following fall Budget. ***Dates vary by province and territory and may occasionally fall outside of these conventional timelines. |

||

| Country | By law (deadline / legal rule) | In practice (typical release & passage) | Latest Budget (when first presented publically) | Next Budget | Budget Approval Window(preliminary scan) |

|---|---|---|---|---|---|

| Canada | No requirement to publish or table a federal Budget at a specific time or even every year. | Budget usually in Feb–Apr. Fall Economic Statement typically later in the year. | April 16, 2024. | Nov.4, 2025 | ~7-9 months after budget tabling. Many spending authorities tied to Budget items arrive with Supp(A) by June. Further tranches land in December via Supp(B). Main estimates by March 1. |

| France | The PLF (projet de loi de finances) must be tabled no later than the first Tuesday in October at the Assemblée nationale | Presented in September at Conseil des ministres; deposited late Sept/early Oct; parliamentary examination Oct–mid-Dec; adoption by Dec 31. | Oct. 2, 2025. First draft for the Haut Conseil des finances publiques, presentation to the Assemblée nationale before Oct. 13. | NA | ~3 months from when the PLF is presented in Sept. at Conseil des ministres. Lois de finances rectificatives (supplementary finance laws) during the year adjust appropriations. |

| United States | The President must submit the budget on/after the first Monday in January and no later than the first Monday in February | Generally early February submission; Congress then follows its timetable | May 2, 2025. Administration released an initial ("skinny") FY2026 request; fuller volumes followed later in May/June. | NA | ~8 months after Budget submission, deadline is end of fiscal year (Sept. 30). In practice, it generally slips into the following months. |

| United Kingdom | No fixed statutory "Budget Day". The Office for Budget Responsibility must produce forecasts at least twice per financial year. | Since 2017, the main Budget is in the autumn; a Spring Statement normally provides the mid-year update. | Oct 30, 2024. Autumn Budget 2024 presented to Parliament. | Nov. 26,2025 | ~7-8 months after budget tabling. Main estimates published in April and approved in July. Supplementary Estimates are still normally presented in February for within-year changes—then debated/voted in early March |

| Germany | The federal budget is established by law before the fiscal year begins (no fixed tabling day). | Cabinet adopts draft in summer; Bundestag holds first reading in September ("Haushaltswoche"); final adoption typically by December. | July 30, 2025. The federal cabinet adopted the government draft for the 2026 federal budget and the fiscal plan to 2029. | NA | ~3 months from first reading. Possible to amend the budget when significant changes are needed during the year. Provisional management permitted if the Budget Act is not in force. |

| Italy | Government must present the state budget bill to Parliament by 20 October. If not approved by 31 December, Parliament may grant provisional exercise up to four months. | Cabinet approval in October, parliamentary passage by end-December (also alongside EU Draft Budgetary Plan process in October). | Oct. 15, 2024. Council of Ministers approved the 2025 Budget Bill; press communication released that evening, followed by a detailed press conference on Oct 16. | Mid-Oct., 2025 | ~2 to 2.5 months. If late, provisional exercise allowed up to 4 months by law. Assestamento (mid-year adjustment) and decreto-legge measures (later converted) can change appropriations during the year. |

| Japan | The Cabinet prepares and submits the budget to the Diet (no fixed calendar date in law). The ordinary Diet session convenes in January to consider the budget. | Cabinet approves the draft in late December, submits in January; enactment by end-March before the April 1 fiscal year. | Dec. 27, 2024. Cabinet approved the FY2025 draft budget (Submitted to the Diet with minister's speeches on Jan 24, 2025.). | NA | ~2 months from budget submission in Jan. Supplementary budgets are common within the fiscal year; Diet must pass them like the main budget. |

Timing of Federal and PT Budgets

Key Facts and Figures

Timing of Federal Budgets and Estimates

- While there is no legislated timeline, the federal budget is conventionally tabled in February or March, with some exceptions particularly in recent years.

- Release dates for the Estimates follow the supply calendar:

- Period ending June 23: Usually considers full supply of Main Estimates which, under House of Commons Standing Orders, must be tabled by March 1 each year and Supplementary Estimates (A).

- Period ending December 10: Considers Supplementary Estimates (B).

- Period ending March 26: Considers Supplementary Estimates (C) and interim for Main Estimates.

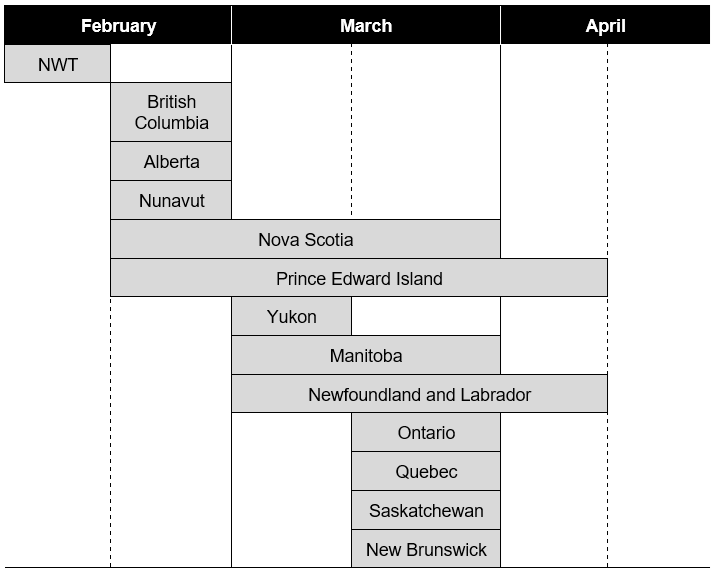

Timing of PT Budgets and Estimates

- Provincial and territorial governments have their own fiscal cycles and schedules.

- Budget dates generally vary within an 8-week period, with March being the most typical month.

- The Main Estimates are released annually, generally either at the same time as budgets or shortly thereafter.

- Supplementary Estimates are released as needed throughout the year. They are rare for some jurisdictions. In some instances, they may be published along with periodic economic and fiscal updates rather than stand-alone documents.

Supplementary Information

| Year | Budget Date | BIA Introduction Date |

|---|---|---|

| 2011 | 6-Jun-2011 | 14-Jun-2011 |

| 2012 | 29-Mar-2012 | 26-Apr-2012 |

| 2013 | 21-Mar-2013 | 29-Apr-2013 |

| 2014 | 11-Feb-2014 | 28-Mar-2014 |

| 2015 | 21-Apr-2015 | 7-May-2015 |

| 2016 | 22-Mar-2016 | 20-Apr-2016 |

| 2017 | 22-Mar-2017 | 11-Apr-2017 |

| 2018 | 27-Feb-2018 | 27-Mar-2018 |

| 2019 | 19-Mar-2019 | 8-Apr-2019 |

| 2021 | 19-Apr-2021 | 30-Apr-2021 |

| 2022 | 7-Apr-2022 | 28-Apr-2022 |

| 2023 | 28-Mar-2023 | 20-Apr-2023 |

| 2024 | 16-Apr-2024 | 2-May-2024 |

Overview of the annual approval and reporting cycle

Typical Provincial Budget Dates

| 2023 | 2024 | 2025 | |

|---|---|---|---|

| British Columbia | |||

Budget |

28-Feb | 22-Feb | 04-Mar |

Main estimates |

28-Feb | 22-Feb | 04-Mar |

Supplementary Estimates |

– | – | – |

Public Accounts |

29-Aug | 22-Aug | 07-Aug |

| Alberta | |||

Budget |

28-Feb | Feb-29 | 27-Feb |

Main estimates |

28-Feb | Feb-29 | 27-Feb |

Supplementary Estimates |

– | – | – |

Public Accounts |

29-Jun | 27-Jun | 27-Jun |

| Saskatchewan | |||

Budget |

22-Mar | 20-Mar | 19-Mar |

Main estimates |

22-Mar | 20-Mar | 19-Mar |

Supplementary Estimates |

– | 05-Dec | – |

Public Accounts |

29-Jun | 27-Jun | 30-Jun |

| Manitoba | |||

Budget |

07-Mar | 02-Apr | 20-Mar |

Main estimates |

07-Mar | 02-Apr | 20-Mar |

Supplementary Estimates |

– | – | – |

Public Accounts |

29-Sep | 27-Sep | 26-Sep |

| Ontario | |||

| Budget | 23-Mar | 26-Mar | 15-May |

| Main estimates | 20-Apr | 17-Apr | 04-Jun |

| Supplementary Estimates | 29-Nov | – | – |

| Public Accounts | 27-Sep | 19-Sep | 26-Sep |

| Quebec | |||

| Budget | 21-Mar | 12-Mar | 25-Mar |

| Main estimates | 20-Mar | 12-Mar | 25-Mar |

| Supplementary Estimates | – | – | – |

| Public Accounts | 11-Dec | 02-Oct | 26-Sep |

| New Brunswick | |||

| Budget | 22-Mar | 19-Mar | 18-Mar |

| Main estimates | 22-Mar | 19-Mar | 18-Mar |

| Supplementary Estimates | – | – | – |

| Public Accounts | 27-Sep | 16-Sep | N/A |

| Nova Scotia | |||

| Budget | 23-Mar | Feb-29 | 18-Feb |

| Main estimates | 23-Mar | Feb-29 | 18-Feb |

| Supplementary Estimates | – | – | – |

| Public Accounts | 12-Sep | 26-Jul | 22-Sep |

| Prince Edward Island | |||

| Budget | 25-May | Feb-29 | 10-Apr |

| Main estimates | 25-May | Feb-29 | 10-Apr |

| Supplementary Estimates | – | – | – |

| Public Accounts | 06-Nov | 11-Oct | N/A |

| Newfoundland and Labrador | |||

| Budget | 23-Mar | 20-Mar | 09-Apr |

| Main estimates | 23-Mar | 20-Mar | 09-Apr |

| Supplementary Estimates | – | – | – |

| Public Accounts | 30-Oct | 29-Oct | N/A |

| Yukon | |||

| Budget | 02-Mar | 07-Mar | 06-Mar |

| Main estimates | 02-Mar | 07-Mar | 06-Mar |

| Supplementary Estimates | – | – | – |

| Public Accounts | 21-Nov | 24-Oct | N/A |

| Northwest Territories | |||

| Budget | 08-Feb | 24-May | 06-Feb |

| Main estimates | 08-Feb | 24-May | 06-Feb |

| Supplementary Estimates | – | – | – |

| Public Accounts | 19-Dec | 15-Nov | N/A |

| Nunavut | |||

| Budget | 23-Feb | 26-Feb | 24-Feb |

| Main estimates | 23-Feb | 26-Feb | 24-Feb |

| Supplementary Estimates | – | – | – |

| Public Accounts | 07-May | 20-Dec | N/A |

| Province | Notes |

|---|---|

| British Columbia | The budget must be delivered on (or before) the fourth Tuesday of February unless an election year, and the main estimates also have to be tabled on or before that same date. |

| Alberta | Under the Financial Administration Act (FAA), the Government of Alberta is required to prepare and table its budget in the Legislative Assembly. While the FAA does not prescribe a specific date for tabling the budget, it mandates that the budget, known as the "Estimates," be tabled before the end of February each year. |

| Ontario | The estimates are required to be tabled within 12 sessional days of the budget." (Schedule of estimates | Legislative Assembly of Ontario) |

| Yukon | The Financial Administration Act requires that the Public Accounts be tabled by October 31. |

| Northwest Territories | The Financial Administration Act mandates that the Government of the Northwest Territories prepare and table its public accounts in the Legislative Assembly on or before December 31 following the end of the fiscal year; or if the Legislative Assembly is not then in session, on or before the fifth day of the next sitting of the Legislative Assembly. |

Affordability Measures

Key Facts and Figures

- The government is helping Canadian families (approximately 900,000 children) save thousands of dollars with the Canada-wide $10-a-day child care system, which created 166,000 new child care spaces since 2021.

- The Canada Child Benefit is helping roughly 3.5 million families with the costs of raising children by providing $28.2 billion in 2024-25.

- The recently expanded Canadian Dental Care Plan is saving the average person enrolled more than $800 per year. Over 4.8 million Canadians have enrolled in the Plan, and over 2 million are already receiving essential care.

- The National School Food Program will provide meals to up to 400,000 more kids every year, saving the average participating family with two children $800 per year in grocery costs, with lower-income families benefitting the most.

- Over the past few years, the government has modernized Canada's competition regime to strengthen competition in our economy. Stronger competition is expected to lead to lower prices, improved services for consumers, and more innovation in the marketplace.

- Access to contraceptive and diabetes medications for Canadians has been expanded, beginning with those in Manitoba, British Columbia, Prince Edward Island, and the Yukon.

Supplementary Information

Canada-wide Early Learning and Child Care

As part of Budget 2021 the Government committed to build a Canada-wide ELCC system with PTs. Key targets that PTs have committed to through bilateral agreements under the Canada-wide system include:

- Reduce fees for regulated child care by 50% by December 2022 (completed);

- Reduce fees for regulated child care to an average of $10-a-day by March 2026; and

- Build 250,000 new regulated child care spaces by March 2026.

Majority of PTs are on track to meet these targets by the end of their agreements on March 31, 2026. The majority have signed extension agreements for 2026-27 to 2030-31, which provide them with a 3 per cent funding top-up to sustain their systems without any additional targets. Alberta, Saskatchewan and Ontario have not yet signed extension agreements.

As of March 31, 2026, the Government will have provided over $35 billion for ELCC, including for Indigenous ELCC, and committed to ongoing funding of $9.2 billion annually

Canada Child Benefit

For the 2024-25 benefit year, the Canada Child Benefit provides up to $7,787 per child under the age of 6 and up to $6,570 per child aged 6 through 17. The Government provided about $28 billion in support to eligible families with children under this benefit in 2024-25. The Canada Child Benefit is legislated through the Income Tax Act and is considered an expenditure for government financial reporting purposes.

Pharmacare

Budget 2024 provided $1.5 billion over five years to support the launch of the National Pharmacare Plan. The Pharmacare Act outlines the government's vision for a national universal pharmacare program and its intention to work with PTs to implement the first phase of the program by providing universal, single-payer coverage for contraception and diabetes medications. To date Manitoba, British Columbia, Prince Edward Island and the Yukon have signed pharmacare agreements. Funding expands and enhances existing PT public drug benefit programs.

Canadian Dental Care Plan

The dental care plan is helping make the cost of dental care more affordable for eligible Canadians. The program is restricted to uninsured Canadians with a family income of less than $90,000, with no co-pays for families under $70,000. The program first launched in 2023 and was initially restricted to seniors. Program eligibility gradually expanded to persons with disabilities, children under the age of 18, and then individuals between the ages of 18 to 64. As of May 29, 2025, all eligible uninsured Canadians of all ages can apply.

National School Food Program

In Budget 2024, the Government of Canada committed $1 billion of federal funding over 5 years through Budget 2024 to develop a National School Food Program. This funding was allocated for bilaterial funding agreements with PTs, funding for school food initiatives on First Nations reserves and for First Nations, Inuit and Métis Modern Treaty and Self-government Agreement Holders, and engagement/capacity building activities related to school food.

As of March 2025, all PTs have signed agreements under the National School Food Program. The federal government is working directly with Indigenous partners on the rollout of their funding, with more information to come.

Modernizing the Competition Framework

Through the Fall Economic Statement Implementation Act, 2023 and the Affordable Housing and Groceries Act, the Government of Canada amended the Competition Act in order to help:

- Put an end to big businesses, including grocers, leveraging contracts and leases to stifle competition;

- Stop anti-competitive mergers that raise prices and limit choices for Canadians;

- Crack down on anti-competitive practices by large dominant companies that drive up prices;

- Improve the focus on worker impacts in competition analysis; and,

- Prevent manufacturers from refusing to provide the means to repair devices in an anti-competitive manner.

Building Canada Act and Major Projects Office

Key Facts and Figures

- The new Major Projects Office (MPO) was launched on August 29 and is being led by CEO Dawn L. Farrell, who brings decades of experience across energy, infrastructure, regulatory strategy, and governance fields.

- The MPO is headquartered in Calgary and will have offices in other major Canadian cities.

- Its mandate is to serve as a single point of contact to get nation-building projects built faster. It will do so in two principal ways:

- First, by streamlining and accelerating regulatory approval processes.

- Second, by helping to structure and co-ordinate financing of these projects as needed.

- On September 11, the first five projects were referred to the MPO. These projects are at an advanced stage of readiness. The MPO will recommend to the federal government the best course to complete each project approval quickly so proponents can make smart investment decisions. (See supplementary information for a list of the projects)

- Also on September 11, the government announced six project that it believes could be truly transformative, which are at an earlier stage and require further development. (See supplementary information for a list of the projects)

- The government stated it will announce a new series of projects being referred to the MPO by the Grey Cup (November 10-16).

- The government announced on September 10 the new membership of the Indigenous Advisory Council that will support the MPO by providing expert advice on policy, operational practices, and process improvements related to the inclusion of Indigenous perspectives on and interests in major projects.

Supplementary Information

First projects to be reviewed by the new Major Projects Office

- On September 11, 2025, Canada announced the first series of projects being referred to the MPO for consideration:

- LNG Canada Phase 2, Kitimat, British Columbia: This project will double LNG Canada's production of liquefied natural gas. It will diversify our trading partners and meet increasing global demand for secure, low-carbon energy with Canadian LNG

- Darlington New Nuclear Project, Bowmanville, Ontario: This project will make Canada the first G7 country to have an operational small modular reactor (SMR), a key technology that could support Canadian and global clean energy needs.

- Contrecœur Terminal Container Project, Contrecœur, Québec: This project will expand the Port of Montréal's capacity by approximately 60%, to give Eastern Canada the trading infrastructure it needs to diversify trade routes.

- McIlvenna Bay Foran Copper Mine Project, East-Central Saskatchewan: This project will supply copper and zinc to strengthen Canada's position as a global supplier of critical minerals.

- Red Chris Mine expansion, Northwest British Columbia: This major expansion project will extend the lifespan of the mine by over a decade, increase Canada's annual copper production by over 15%, and reduce greenhouse gas emissions by over 70% when operational.

- In addition to the five projects above, the government has identified several projects that could be truly transformative for this country, which are at an earlier stage and require further development:

- Critical Minerals: A priority for the MPO will be to help more critical minerals projects get to final investment decisions within a two-year window.

- Wind West Atlantic Energy: A project that will leverage over 60 GW of wind power potential in Nova Scotia, and more across Atlantic Canada, connecting that renewable, emissions-free energy to Eastern and Atlantic Canada to meet rapidly growing demand.

- Pathways Plus: An Alberta-based carbon capture, utilization, and storage project and pipeline that will substantially reduce emissions and create the prospect of facilitating low-carbon oil exports from the Alberta oil sands to a variety of potential markets.

- Arctic Economic and Security Corridor: An all-weather, dual-use, land and port-to-port-to-port infrastructure project that will contribute to Canada's defence and northern development. The project will support Northern critical mineral projects and connect communities to the rest of Canada.

- Port of Churchill Plus: In partnership with Indigenous Peoples, this project will upgrade the Port of Churchill and expand trade corridors with an all-weather road, an upgraded rail line, a new energy corridor, and marine ice-breaking capacity to turn the Port of Churchill into a major four‑season and dual-use gateway for the region.

- Alto High-Speed Rail: Canada's first high-speed railway, spanning approximately 1,000 km from Toronto to Québec City. The MPO will work to enable construction of the project to start in four years, cutting the original eight-year timeline in half.

Comprehensive Expenditure Review

Key Facts and Figures

- The Government of Canada is undertaking a Comprehensive Expenditure Review (CER) to balance the government's operating budget over the next three years.

- Organizations are reviewing their programs and activities and submitting savings proposals of up to 15% of their assigned spending base, which is drawn from planned spending in the 2025-26 Main Estimates.

- Statutory transfer payments to provinces, territories and individuals will be maintained, but most other government spending will be included in the review.

- Final decisions will be presented in the 2026-27 Main Estimates.

Supplementary Information

- Spending on government operations has grown at an unsustainable rate. To address this, the Government committed to balancing its operating budget over the next three years. The CER will ensure that government spending is sustainable and directed to programs and activities that are cost-effective, core the federal mandate, complementary to other government programming and aligned with government priorities. While the primary intent is to realize savings, this review also aims to make the public service more efficient and effective so it can better deliver for Canadians.

- The process applies to federally appropriated organizations, with the following exceptions:

- agents of parliament and arms-length organizations to preserve their independence, and

- cost-recovered organizations, because including them would not generate savings.

- The review focusses on voted operating and transfer payments. Capital budgets, such as for infrastructure and technology, are not included. Organizations will need to develop savings proposals for up to 15% of their assigned spending base, which is drawn from planned spending in the 2025-26 Main Estimates.

- Departments are expected to bring forward ambitious savings proposals to spend less on the day-to-day running of government by targeting programs and activities that are underperforming, not core to the federal mandate, duplicative, or misaligned with government priorities.

- The government is taking a broad approach to the review that also recognizes the importance of key investments being made in certain areas. As such, the government is setting a lower savings target of 2% for the Department of National Defence, the Canada Border Services Agency (CBSA) and the Royal Canadian Mounted Police (RCMP).

- Unrealized savings from the Budget 2024 Refocusing Government Spending initiative starting 2026-27 are included in the savings targets of this review.

- All departments must develop their proposals using Gender-Based Analysis Plus to identify how the benefits of programs are distributed across diverse groups of Canadians. This will help us better understand how people, particularly those most in need, would be impacted by particular decisions.

- Departments will respect Workforce Adjustment provisions and will aim to minimize the number of impacted employees by using all HR planning tools at their disposal, which include attrition and assisting employees in securing alternative positions within the federal public service.

Canada-U.S. Trade and Tariffs

Key Facts and Figures

- The United States reaffirmed a core commitment to CUSMA by reinforcing that Canadian exports to the U.S. that are compliant with CUSMA are not subject to the U.S. IEEPA tariffs of 35%.

- The U.S. maintains tariffs on Canadian exports in strategic sectors – 50% on Canadian steel, aluminum, and copper products, and 25% on Canadian autos.

- New tariffs on lumber (10%) and upholstered furniture and kitchen cabinets (25%) will take effect in mid-October. The President has also announced tariffs on trucks and branded pharmaceutical products.

- The government has applied tariffs on imports from the U.S. to defend our interests. Effective September 1, given the U.S. commitment to exempt CUSMA-compliant goods, the government recalibrated the approach by removing tariffs on all goods, with the exception of steel, aluminum, and autos.

- To date, more than $2.5 billion in revenues have been collected from Canadian tariffs.

- The government continues to work with the U.S. to address U.S. tariffs in the strategic sectors where tariffs remain in place.

- On September 17, the United States Trade Representative initiated a 45-day consultation period for the review of USMCA. Global Affairs Canada launched on September 20 a new round of consultations to get the latest views from Canadian stakeholders.

Supplementary Information

U.S. tariffs

The U.S. has imposed the following tariffs on Canada:

- 25 per cent tariff on non-CUSMA compliant autos as well as on the value of non-U.S. content in CUSMA-compliant autos.

- CUSMA-compliant auto parts from Canada are currently exempt from a 25 per cent U.S. tariff.

- 50 per cent on steel and aluminum and derivative products (increased from 25 per cent on June 4, 2025);

- 50 per cent on certain copper products;

- 10 per cent on timber and softwood lumber, 25 per cent on upholstered furniture (increasing to 30% in 2026), and 25 per cent on kitchen cabinets and vanities (increasing to 50% in 2026). These tariffs will take effect on October 14, 2025; and

- 35 per cent on all goods (except 10 per cent on energy resources, including critical minerals, and potash) that do not meet CUSMA rules of origin (increased from 25 percent on August 1, 2025).

- The U.S. Court of International Trade and the U.S. Court of Appeals for the Federal Circuit ruled that the President exceeded his authority by imposing tariffs under the International Emergency Economic Powers Act (IEEPA). The Supreme Court accepted the U.S. Administration's petition to review the rulings on an expedited basis in Fall 2025 and could issue a judgment before the end of 2025.

- The President has also announced tariffs of 25% on heavy-duty trucks and 100% on branded pharmaceutical products. The legal instruments to give effect to these tariffs have not yet been issued as of October 1, 2025.

- The U.S. has also initiated additional Section 232 investigations on the following sectors, which could result in additional tariffs: (1) semi-conductors; (2) processed critical minerals; (3) commercial aircrafts and jet engines; (4) polysilicon; (5) unmanned aircraft systems; (6) wind turbines; (7) robotics and industrial machinery; and (8) personal protective equipment and medical equipment. The government continues to monitor these investigations.

Canadian counter-tariffs

Canada imposed counter-tariffs affecting approximately $95 billion of annual imports from the U.S., including steel, aluminum, and other products. Canada's response on autos mirror the U.S. auto tariffs in the form of a 25 per cent to non-CUSMA compliant vehicles from the U.S., as well as the non-Canadian and non-Mexican content of CUSMA-compliant vehicles from the U.S.

- Effective September 1, the government removed the counter-tariffs on $44.7 billion of annual imports from the U.S., while maintaining those on steel, aluminum and autos.

To minimize the negative effects of the counter-tariffs, the government established a remission framework to provide exceptional tariff relief on a case-by-case basis. More broadly, the government also provided a temporary six-month tariff relief (remission), until October 15, 2025, for goods imported from the U.S. by listed entities that support public health, public safety, and national security. Remission of tariffs is also provided for goods used in manufacturing, processing, or food and beverage packaging to give time for Canadian businesses to adjust their supply chains and prioritize domestic sources of supply if available.

For autos, the government provided a performance-based remission framework that allows automakers to import a certain number of U.S.-assembled, CUSMA-compliant vehicles into Canada, free of the counter-tariffs. This remission is contingent on the automakers continuing to produce vehicles in Canada and on completing planned investments. The number of tariff-free vehicles a company is permitted to import will be reduced if there are reductions in Canadian production or investment. The framework will remain in force until April 2026.

Revenues from counter-tariffs

As of the end of September, the government collected more than $2.5 billion, net of remissions and other relief programs, from Canada's counter-tariffs on U.S. goods.

CUSMA review

On September 17, the United States Trade Representative (USTR) initiated a 45-day consultation period for the review of USMCA, which will include the submission of written comments and public hearings. USTR is required to report to Congress in early January 2026 its assessment of how USMCA has been operating, its policy recommendations, the U.S. position on whether to extend the agreement, and actions it proposes to take at the review.