Canada Student Loans Program annual report 2017 to 2018

On this page

Alternate formats

Canada Student Loans Program annual report 2017 to 2018 [PDF - 1.66 MB]

Large print, braille, MP3 (audio), e-text and DAISY formats are available on demand by ordering online or calling 1 800 O-Canada (1-800-622-6232). If you use a teletypewriter (TTY), call 1-800-926-9105.

List of figures and tables

- Table 1 – Canada Student Grants by type

- Diagram 1 – Canada Student Grants for full- and part-time students in 2017 to 2018

- Table 2 – Canada Student Loans for full- and part-time students

- Diagram 2 – Number of RAP recipients by RAP stage and payment type in 2017 to 2018

- Table 3 – Profile of students who received Canada Student Grants and/or Canada Student Loans in 2017 to 2018

- Table 4 – Percent of full-time students studying inside and outside of Canada in 2017 to 2018

- Table 5 – Canada Student Loan 3-year default rates

- Table 6 – Consolidated Canada Student Loans Programs – Combined programs

List of abbreviations

- CAL

- Canada Apprentice Loan

- CSG

- Canada Student Grants

- CSG-LI

- Canada Student Grant for low-income students

- CSG-MI

- Canada Student Grant for middle-income students

- CSG-PT

- Canada Student Grants for Part-Time Students

- CSL

- Canada Student Loans

- CSLP

- Canada Student Loans Program

- ESDC

- Employment and Social Development Canada

- NSLSC

- National Student Loans Service Centre

- PD

- Permanent Disability

- RAP

- Repayment Assistance Plan

- RAP-PD

- Repayment Assistance Plan for Borrowers with a Permanent Disability

Message from the Minister

Canada’s economy is evolving, with new opportunities and technologies driving growth and changing the world of work.

The jobs of tomorrow will require specialized training and education. That is why we are making significant investments in the Canada Student Loans Program. We want to help every Canadian afford the education and training they need for the job they want.

More students have benefited from our increased Canada Student Grant amounts and broadened eligibility thresholds. More than 490,000 students benefited from $1.4 billion in non-repayable Canada Student Grants in 2017 to 2018, which is an increase of 29% in the number of recipients, and a 34% increase in value, compared to the previous year.

We also provided $3.4 billion in student loans in 2017 to 2018, and more than 326,000 borrowers received support under the Repayment Assistance Plan.

Finally, in January 2018 we launched the Skills Boost initiative to support adults returning to school to upgrade their skills or pursue a new career path. Through Skills Boost, full-time students who have been out of high school for 10 years or more can receive an additional $1,600 in grants each year while studying at a post-secondary institution.

I am pleased to present the 2017 to 2018 Annual Report of the Canada Student Loans Program, and to reaffirm our commitment to making post-secondary education more affordable and accessible to all Canadians. When everyone can get ahead, our economy and our communities grow stronger.

The Honourable Carla Qualtrough, P.C., M.P.

Minister of Employment, Workforce Development and Disability Inclusion

Introduction

This annual report serves to inform Parliament and Canadians about student financial assistance for post-secondary education under the Canada Student Loans Program (CSLP). It provides information and data on grants, loans, repayment assistance and other program benefits during the 2017 to 2018 loan year (August 1, 2017, to July 31, 2018).

Further detailed information, including past reports and comprehensive Statistical Reviews of the CSLP, are available on the Government of Canada website: Canada Student Loans Program reports.

Vision and mission

Employment and Social Development Canada

The mission of Employment and Social Development Canada (ESDC), including the Labour Program and Service Canada, is to build a stronger and more inclusive Canada, to support Canadians in helping them live productive and rewarding lives and to improve Canadians' quality of life.

Canada Student Loans Program

The Canada Student Loans Program (CSLP) provides targeted grants and needs‑based loans to help students access post secondary education and offers repayment assistance to borrowers with financial difficulty.

Program highlights and results

The Government of Canada recognizes the importance of student financial assistance for post-secondary students in achieving their educational goals and, ultimately, succeeding as contributing members of a productive workforce.

The CSLP works collaboratively with provincial and territorial governments to deliver student financial assistance to Canadian students. Quebec, Nunavut and the Northwest Territories do not participate in the CSLP but receive annual alternative payments in support of their own student financial assistance programs. Applicants in the remaining ten jurisdictions are assessed for federal and provincial grants and loans through a single application process.

In the 2017 to 2018 loan year, approximately 705,000 post-secondary students received financial assistance from the CSLP, in the form of grants, loans or in-study interest subsidies. CSLP provided $1.4 billion in non-repayable Canada Student Grants (CSG) to over 490,000 students and $3.4 billion in Canada Student Loans (CSL) to 592,000 students. In addition, the three non-participating jurisdictions received $456.7 million in alternative payments for the 2017 to 2018 loan year.

In Budget 2017, the Government of Canada announced additional program enhancements that would come into effect during the 2018 to 2019 loan year, including:

- Skills Boost, which will introduce a 3-year pilot project targeted to adult learners who wish to return to school after spending several years in the workforce

- expanded eligibility for Canada Student Grants and Canada Student Loans for part-time students, as well as full-time and part-time students with dependants

- amendments to the Canada Student Financial Assistance Act, so that students who are registered under the Indian Act but do not have Canadian citizenship can access the CSLP

Following are the key highlights of the components of the CSLP in the 2017 to 2018 loan year.

A. Canada Student Grants

In 2017 to 2018, 490,000 students received $1.4 billion in financial assistance they will not have to pay back; this represents an increase of 29% in the number of recipients and 35% in the value of the grants relative to the previous loan year.

Canada Student Grants (CSG) provide non-repayable funding to full- and part-time students and are targeted to students from low- and middle-income families, students with permanent disabilities and those with dependants. Students are automatically assessed for CSGs when applying for student financial assistance through their province or territory of residence.

During the 2017 to 2018 school year, a number of improvements were made to Canada Student Grants:

- the CSG for Students from Low-Income Families and the CSG for Students from Middle-Income Families was replaced by the Canada Student Grant for Full-Time Students (CSG-FT) which is based on a more generous, progressive threshold, where the grant amounts gradually decrease based on income and family size. As a result, more students are eligible for more CSG funding and no student will receive less than what they would have received before

In 2017 to 2018, the CSLP provided the following grants to eligible students:

- Canada Student Grant for Full-time Students: up to $375 per month of study

- Canada Student Grant for Full-Time Students with Dependants: $200 per month of study for each dependant under 12 years of age (or for each dependant over 12 years of age with a permanent disability)

- Canada Student Grant for Students with Permanent Disabilities: $2,000 per year for full-time or part-time students with permanent disabilities

- Canada Student Grant for Services and Equipment for Students with Permanent Disabilities: up to $8,000 per year to cover exceptional education-related costs

- Canada Student Grant for Part-Time Studies: up to $1,800 per loan year

- Canada Student Grant for Part-Time Students with Dependants: up to a maximum of $1,920

The following table provides a summary of the distribution of Canada Students Grants by type.

Table 1 – Canada Student Grants by type

| Canada Student Grant | 2015 to 2016 | 2016 to 2017 | 2017 to 2018 |

|---|---|---|---|

| Full-time students2 | 335,231 | 344,165 | 451,296 |

| Full-time students with dependants | 35,347 | 35,322 | 40,523 |

| Students with permanent disabilities | 34,104 | 37,263 | 46,432 |

| Services and equipment for students with permanent disabilities | 9,894 | 10,125 | 10,550 |

| Part-time studies | 17,432 | 19,155 | 21,261 |

| Part-time students with dependants | 408 | 332 | 376 |

| Total | 368,940 | 379,606 | 490,377 |

- 1 The number of recipients do not sum to the total, as some recipients can receive multiple grants in the same year.

- 2 In 2017 and 2018, the Canada Student Grant for Full-Time Students replaced 2 separate grants, the Canada Student Grant for low-income students (CSG-LI) and the Canada Student Grant for middle-income students (CSG-MI). The values between 2015 to 2016 and 2016 to 2017 are the total of CSG-LI and CSG-MI.

| Canada Student Grant | 2015 to 2016 | 2016 to 2017 | 2017 to 2018 |

|---|---|---|---|

| Full-time students2 | 524.8 | 803.6 | 1,118.9 |

| Full-time students with dependants | 86.3 | 87.7 | 102.6 |

| Students with permanent disabilities | 65.0 | 71.0 | 88.3 |

| Services and equipment for students with permanent disabilities | 23.5 | 23.3 | 22.0 |

| Part-time studies | 19.4 | 28.6 | 32.6 |

| Part-time students with dependants | 0.4 | 0.3 | 0.4 |

| Total | 719.5 | 1,014.6 | 1,364.9 |

- 2 In 2017 and 2018, the Canada Student Grant for Full-Time Students replaced 2 separate grants, the Canada Student Grant for low-income students (CSG-LI) and the Canada Student Grant for middle-income students (CSG-MI). The values between 2015 to 2016 and 2016 to 2017 are the total of CSG-LI and CSG-MI.

While the number of full-time students who received grants increased by 29% in the 2017 to 2018 loan year, the value increased by 35% as a result of increases in grants announced in Budget 2016. The number of part-time students who have received grants increased by 11% to 21,300 and the value increased by 14% to $33 million.

In the 2017 to 2018 loan year, the CSLP disbursed $110.4 million in grants to 46,400 students with permanent disabilities in Canada Student Grants for Students with Permanent Disabilities and Canada Student Grants for Services and Equipment for Students with Permanent Disabilities, an increase of 25% in number and 17% in value from the previous year.

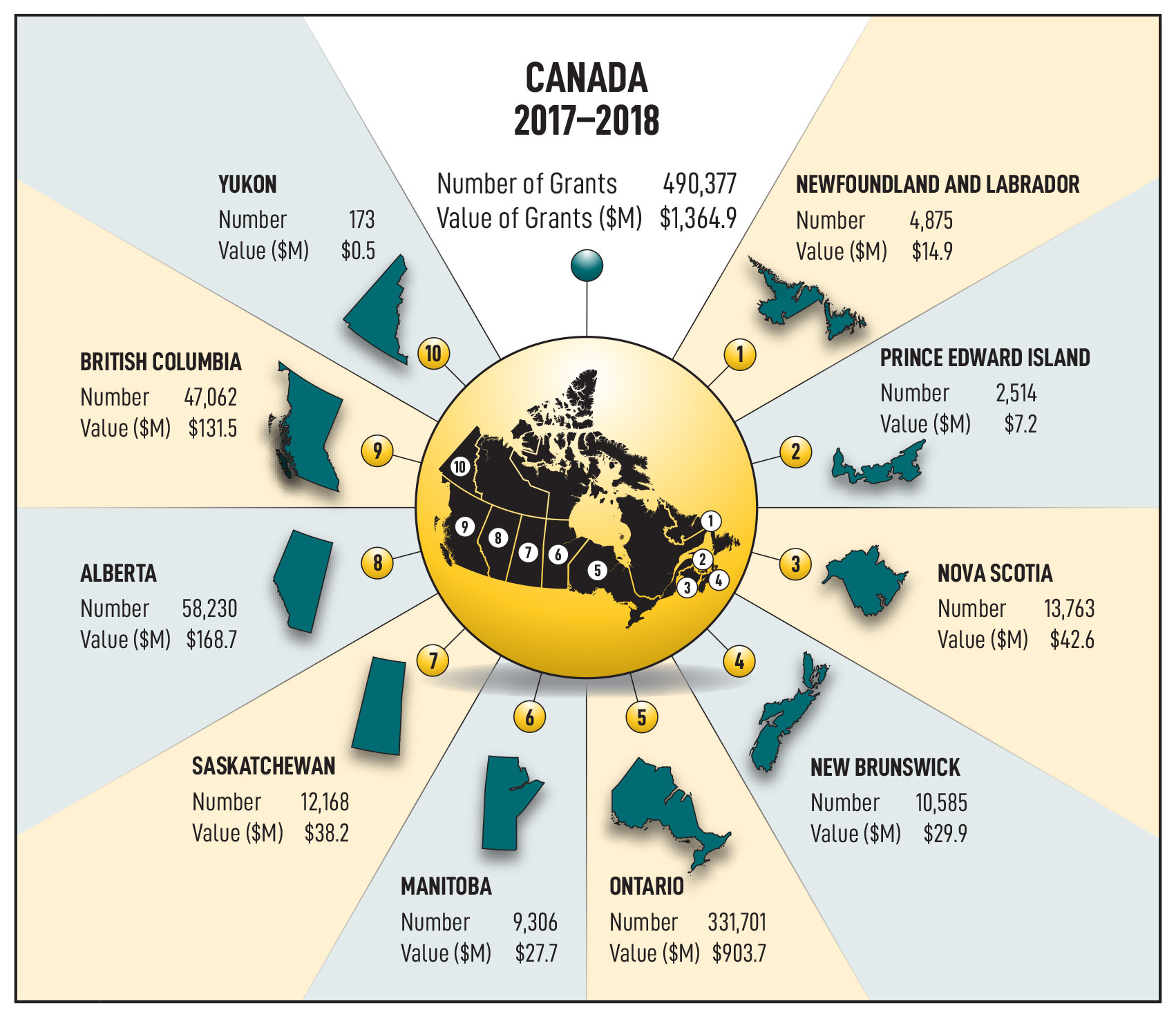

The following diagram shows the distribution of Canada Student Grants for full- and part-time students by province or territory.

Text description of diagram 1

| Province or territory | Number of recipients | Millions of dollars |

|---|---|---|

| Newfoundland and Labrador | 4,875 | 14.9 |

| Prince Edward Island | 2,514 | 7.2 |

| Nova Scotia | 13,763 | 42.6 |

| New Brunswick | 10,585 | 29.9 |

| Ontario | 331,701 | 903.7 |

| Manitoba | 9,306 | 27.7 |

| Saskatchewan | 12,168 | 38.2 |

| Alberta | 58,230 | 168.7 |

| British Columbia | 47,062 | 131.5 |

| Yukon | 173 | 0.5 |

| Total | 490,377 | 1,364.9 |

B. Canada Student Loans

In the 2017 to 2018 loan year, approximately 592,000 students received $3.4 billion in Canada Student Loans; this represents an increase of 19% in the number of recipients and 28% in the value of the loans relative to the previous loan year.

The Canada Student Loans Program provides eligible students grants and loans to help them pay their tuition, books, mandatory fees, living costs and transportation. Canada Student Loans are available to Canadian students with a demonstrated financial need who are enrolled in degree, diploma or certificate programs at designated post-secondary educational institutions in Canada and abroad.

Student loans are also interest-free for the entire period of studies.

In the 2017 to 2018 loan year, the CSLP introduced a new fixed student contribution model that replaced the previous system of assessing student income and financial assets. Under the new model, students are expected to contribute an amount between $1,500 to $3,000 to their education, with the exact amount being calculated based on their gross family income and family size. Students with dependants, students with a permanent disability, and those who self-identify as Indigenous, are exempted from making a contribution. This model allows students to work and gain valuable labour market experience without having to worry about a reduction in their level of financial assistance.

The following table provides a summary of Canada Student Loans for full- and part-time students by province or territory.

Table 2 – Canada Student Loans for full- and part-time students

| Province or territory | 2015 to 2016 | 2016 to 2017 | 2017 to 2018 |

|---|---|---|---|

| Newfoundland and Labrador | 6,131 | 6,036 | 5,956 |

| Prince Edward Island | 2,702 | 2,626 | 2,565 |

| Nova Scotia | 16,451 | 16,687 | 17,261 |

| New Brunswick | 11,572 | 12,016 | 13,866 |

| Ontario | 325,703 | 321,090 | 392,484 |

| Manitoba | 10,428 | 10,154 | 9,724 |

| Saskatchewan | 11,732 | 12,627 | 14,882 |

| Alberta | 57,059 | 63,167 | 79,265 |

| British Columbia | 55,094 | 52,520 | 55,895 |

| Yukon | 170 | 141 | 193 |

| Total | 497,042 | 497,064 | 592,091 |

| Province or territory | 2015 to 2016 | 2016 to 2017 | 2017 to 2018 |

|---|---|---|---|

| Newfoundland and Labrador | 28.9 | 27.9 | 37.1 |

| Prince Edward Island | 17.1 | 16.4 | 16.1 |

| Nova Scotia | 114.3 | 115.2 | 123.0 |

| New Brunswick | 63.8 | 56.2 | 66.9 |

| Ontario | 1,735.4 | 1,646.3 | 2,141.9 |

| Manitoba | 49.5 | 46.5 | 41.6 |

| Saskatchewan | 71.3 | 75.3 | 93.7 |

| Alberta | 321.7 | 342.0 | 487.1 |

| British Columbia | 319.2 | 300.5 | 343.4 |

| Yukon | 1.0 | 0.8 | 1.3 |

| Total | 2,722.3 | 2,627.2 | 3,352.1 |

C. Loan repayment, assistance and forgiveness

Unlike traditional loans, Canada Student Loans do not accrue interest while the borrower is in school, but rather interest begins to accumulate once the borrower leaves school.

Borrowers are not required to make payments in the first 6 months after the end of their studies. Once 6 months have elapsed, borrowers begin to repay their loans through monthly payments, typically over a 114-month period (9.5 years). Depending on their financial situation and income level, borrowers may revise their repayment terms to pay more quickly or to extend the payment period to reduce their monthly payments (up to a maximum of 14.5 years).

The average Canada Student Loan balance at the time of leaving school was $13,416 for the 2017 to 2018 loan year. The increase in available grants and students not needing to rely as heavily on loans has meant that student debt has remained relatively stable over the past years.

Differences in loan balances reflect each student’s particular situation. Loan balances are measured at the time of leaving school, which includes students who graduate, as well as those who do not complete their program of study. Among the key factors attributing to differences are the type and location of institution, as well as the program of study. In the 2017 to 2018 loan year, the average loan balance of university students was $16,894, higher than that of college students ($9,915) and those attending private institutions ($10,889). This difference is partly because university programs generally tend to take longer to complete.

Repayment Assistance Plan

More than 326,000 borrowers received support under the Repayment Assistance Plan in the 2017 to 2018 loan year; an increase of 7% from the previous loan year.

The Repayment Assistance Plan (RAP) is available to help borrowers who experience difficulty in repaying their student loans.

A single borrower does not have to repay their Canada Student Loan until they are earning at least $25,000 per year. This income threshold is adjusted based on family size, meaning that for a family of four, no payment would be required until they are earning at least $59,512. To remain on RAP, borrowers must re-apply every 6 months.

RAP offers different benefits depending on whether borrowers need short-term assistance soon after entering repayment or longer-term assistance after many years in repayment.

For the first 5 years on RAP (RAP Stage 1), the Government of Canada pays the interest not covered by a borrower’s monthly payment on their student loan. For borrowers with longer-term financial difficulty (beyond 5 years), the Government of Canada begins to contribute towards both the principal and interest (RAP Stage 2) such that the loan is fully paid off in 15 years since leaving school. If a borrower is already over 10 years in repayment when they first apply for RAP, they would be on Stage 2 from the start, that is, the Government would contribute to both interest and principal.

The Repayment Assistance Plan for Borrowers with a Permanent Disability (RAP-PD) offers more generous assistance than RAP.

The Government of Canada pays both the interest and principal not covered by the monthly payments, such that the loan is paid off 10 years after the completion of studies, for those who remain on RAP-PD. In addition, disability-related expenses are taken into account in the eligibility assessment, which may further reduce the individual’s monthly payments.

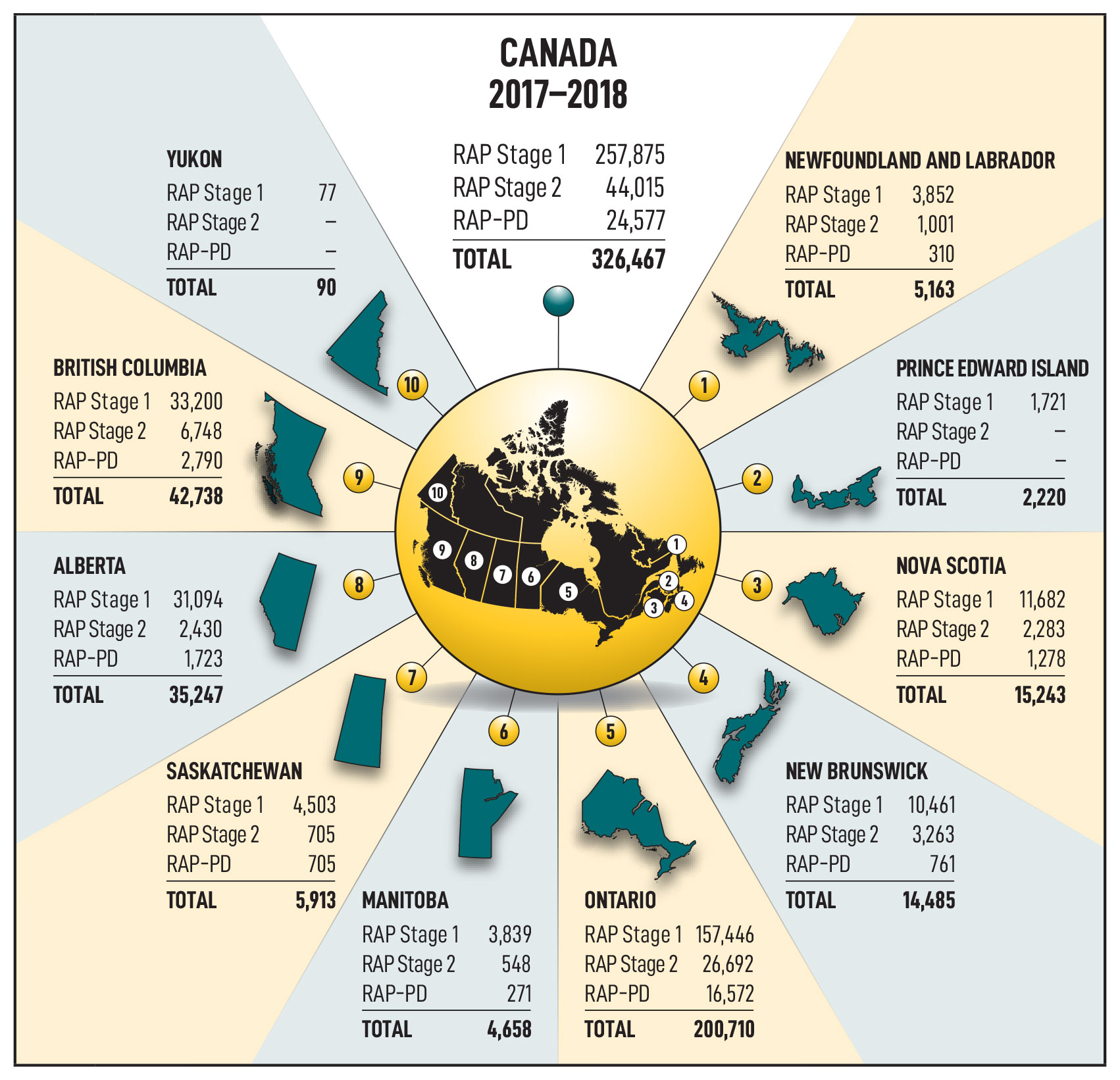

The following diagram provides a summary of the number of RAP recipients by RAP stage and payment type in 2017 to 2018.

Text description of Diagram 2

| Province or territory | All Stages | Stage 1 | Stage 2 | Permanent Disability (PD) |

|---|---|---|---|---|

| Newfoundland and Labrador | 5,163 | 3,852 | 1,001 | 310 |

| Prince Edward Island | 2,220 | 1,721 | x | x |

| Nova Scotia | 15,243 | 11,682 | 2,283 | 1,278 |

| New Brunswick | 14,485 | 10,461 | 3,263 | 761 |

| Ontario | 200,710 | 157,446 | 26,692 | 16,572 |

| Manitoba | 4,658 | 3,839 | 548 | 271 |

| Saskatchewan | 5,913 | 4,503 | 705 | 705 |

| Alberta | 35,247 | 31,094 | 2,430 | 1,723 |

| British Columbia | 42,738 | 33,200 | 6,748 | 2,790 |

| Yukon | 90 | 77 | x | x |

| Total | 326,467 | 257,875 | 44,015 | 24,577 |

- x: cells are suppressed to prevent statistical disclosure of number of recipients greater than 0 but less than 10.

Severe Permanent Disability Benefit

In very particular cases, borrowers with a severe permanent disability may be eligible for loan forgiveness. The Severe Permanent Disability Benefit makes it possible to cancel the repayment obligations of borrowers who have a severe permanent disability. A medical assessment must be completed by a physician or nurse practitioner stating that the severe disability prevents a borrower from performing the daily activities necessary to participate in studies at a post-secondary school level or in apprenticeship training, and in the labour force, and that the disability is expected to continue throughout the borrower’s life.

In the 2017 to 2018 loan year, $7.7 million in Canada Student Loans were forgiven under this measure for over 500 borrowers, with an average value of $15,295.

Loan forgiveness for family doctors and nurses

The Government of Canada offers Canada Student Loan forgiveness for eligible family doctors, residents in family medicine, nurse practitioners and registered nurses who work in rural or remote communities. This benefit is aimed at increasing health care services across Canada.

Family doctors or residents in family medicine may receive up to $40,000 in Canada Student Loan forgiveness over a maximum of 5 years ($8,000 per year), and nurse practitioners and nurses may receive up to $20,000 in loan forgiveness over a maximum of 5 years ($4,000 per year).

For the 2017 to 2018 fiscal year, nearly 5,200 health care professionals working in various rural and remote regions received $22.9 million (or an average of $4,406) of CSL forgiveness.

D. Student demographics

The demographic profile of Canada Student Loan Program recipients remained consistent with that of previous years. The majority of students who received a grant and/or loan in 2017 to 2018 were female (59%), were between the ages of 20 to 24 (45%), attended university (57%) and were enrolled in an undergraduate program (59%).

12% of students were over the age of 30, and 5% of students were pursuing a graduate or post-graduate degree.

The following table provides a summary of the profile of students who received Canada Student Grants and/or Canada Students Loans in 2017 to 2018.

| Details | Number | Percent | Millions of dollars | Percent |

|---|---|---|---|---|

| Gender | 628,935 | 100 | 4,717.0 | 100 |

| Female | 372,474 | 59 | 2,844.4 | 60 |

| Male | 256,461 | 41 | 1,872.6 | 40 |

| Age group | 628,935 | 100 | 4,717.0 | 100 |

| Younger than 20 years | 180,611 | 29 | 1,191.0 | 25 |

| 20 to 24 years | 280,929 | 45 | 2,072.4 | 44 |

| 25 to 29 years | 85,488 | 14 | 722.2 | 15 |

| 30 to 34 years | 33,769 | 5 | 302.2 | 6 |

| 35 to 39 years | 20,918 | 3 | 193.2 | 4 |

| 40 to 44 years | 13,254 | 2 | 119.2 | 3 |

| 45 to 49 years | 7,789 | 1 | 67.6 | 1 |

| 50 years and older | 6,177 | 1 | 49.2 | 1 |

| Level of study | 628,935 | 100 | 4,717.0 | 100 |

| Certificate or diploma | 224,766 | 36 | 1,596.8 | 34 |

| Undergraduate | 373,261 | 59 | 2,862.4 | 61 |

| Master | 25,555 | 4 | 209.9 | 4 |

| Doctorate | 5,353 | 1 | 47.9 | 1 |

| Type of institution | 628,935 | 100 | 4,717.0 | 100 |

| University | 359,785 | 57 | 2,776.9 | 59 |

| College | 211,526 | 34 | 1,437.1 | 30 |

| Private | 57,624 | 9 | 503.0 | 11 |

In the 2017 to 2018 loan year, the vast majority of full-time students remained in their home province or territory to pursue post-secondary education. 91% of students studied in their home province or territory within Canada, compared to just 7% who studied in Canada but outside their home province or territory. 2% studied outside Canada.

The following table provides a summary of the percent of full-time students studying inside and outside of Canada in 2017 to 2018.

| Province or territory | Study in home province or territory | Study in Canada but away from home province or territory | Study in the United States | Study outside Canada and the United States |

|---|---|---|---|---|

| Newfoundland and Labrador | 83.8 | 14.8 | 0.5 | 1.0 |

| Prince Edward Island | 58.5 | 40.4 | x | x |

| Nova Scotia | 80.8 | 18.0 | 0.5 | 0.7 |

| New Brunswick | 78.9 | 20.1 | 0.6 | 0.4 |

| Ontario | 95.4 | 2.7 | 0.8 | 1.0 |

| Manitoba | 82.0 | 15.3 | 1.7 | 1.0 |

| Saskatchewan | 80.0 | 18.0 | 1.3 | 0.7 |

| Alberta | 83.6 | 12.7 | 1.9 | 1.7 |

| British Columbia | 85.7 | 11.1 | 1.3 | 1.8 |

| Yukon | 21.8 | 73.9 | x | x |

| Total | 91.2 | 6.6 | 1.0 | 1.2 |

- x: cells are suppressed to prevent statistical disclosure of number of recipients greater than 0 but less than 10.

Program delivery

Working with partners

The CSLP works collaboratively with provincial and territorial governments to deliver student financial assistance to Canadian students. In participating provinces (all jurisdictions except Quebec, Nunavut and Northwest Territories), approximately 60% of a full-time student’s assessed financial need is funded by the Government of Canada, while the province or territory covers the remaining 40%.

A private-sector service provider, contracted by the Government of Canada, and branded as the National Student Loans Service Centre (NSLSC), administers grants and loan disbursement and loan repayment. The NSLSC also administers student aid in five integrated provinces (British Columbia, Saskatchewan, Ontario, New Brunswick and Newfoundland and Labrador) as a single, integrated loan.

In support of their own student aid programs, the 3 non-participating jurisdictions received $456.7 million in alternative payments for the 2017 to 2018 loan year, compared to the previous year’s payment of $338.5 million:

- Quebec received $451.0 million – representing an increase of $116.6 million from last year’s payment of $334.4 million

- Nunavut received $2.7 million – representing an increase of $0.8 million from last year’s payment of $1.9 million

- the Northwest Territories received $3.0 million – representing an increase of $0.8 million from last year’s payment of $2.2 million

Service modernization

The Government of Canada is dedicated to continuously streamlining and modernizing the CSLP, as well as improving services for students. In collaboration with provincial and territorial partners, the CSLP is implementing a new electronic service delivery model aimed at providing students with simple, easy-to-manage access to financial assistance. The transformation initiative aims to significantly enhance the loan experience for borrowers by:

- providing more timely and user-friendly information regarding financial assistance, including disbursements

- reducing or eliminating the paper-based administrative burden for borrowers, and increasing the number of transactions that can be completed online through access to self-service options

- producing greater efficiencies within the student financial assistance delivery system

Since April 2018, new full-time students can have their identity validated and submit their loan agreements online rather than by visiting designated Canada Post outlets. As of July 31, 2018, over 98,000, or 93%, of new full-time students have taken advantage of this online service.

Program performance measurement

Client satisfaction

The CSLP is committed to ensuring that clients receive quality service. An annual client satisfaction survey is used to assess clients’ satisfaction with the services related to their grants and loans.

In the 2017 to 2018 loan year, 83% of clients said they were satisfied with the overall quality of service they received in regard to their grant or loan. Satisfaction levels have remained high over the past number of years.

Portfolio performance

The CSLP works with the service provider and provincial partners to minimize the value of loans going into default. Although the vast majority of students repay their loans in full and on time, some borrowers experience difficulty in repayment. A loan is deemed in default when in arrears for more than 270 days (roughly equivalent to missing 9 monthly payments).

The CSLP uses a 3-year default rate as a main indicator of the performance of the portfolio. This rate compares the value of the loans that enter repayment in a given loan year, and default within 3 years, to the value of all the loans that entered repayment in that loan year.

As noted in the following table, the default rate has decreased significantly in the last decade. The introduction of grants and RAP, coupled with increased and targeted communications by the service provider, have helped a greater number of students manage their repayment obligations, leading to a lower default rate.

| Years | 2008 to 2009 | 2009 to 2010 | 2010 to 2011 | 2011 to 2012 | 2012 to 2013 | 2013 to 2014 | 2014 to 2015 | 2015 to 2016 | 2016 to 2017 |

|---|---|---|---|---|---|---|---|---|---|

| Rates | 14% | 15% | 14% | 13% | 12% | 11% | 10% | 9% | 9% |

Loan rehabilitation

The CSLP offers loan rehabilitation as a way for borrowers to bring their defaulted loans back into good standing. Borrowers can rehabilitate their defaulted loans by paying their outstanding interest, plus 2 regular monthly payments. The CSLP works closely with the Canada Revenue Agency to raise awareness of loan rehabilitation.

A targeted communication campaign was implemented in June 2016, and used behavioural insights to nudge borrowers who are most likely to be eligible for rehabilitation. As a result, the CSLP has seen an increase in the number of approved cases since the rehabilitation promotion was implemented. In the 2017 to 2018 loan year, 6,296 borrowers rehabilitated $60.1 million in student loans.

On January 1, 2020, borrowers will have a new option to rehabilitate Canada Student Loans and Canada Apprentice Loans in default. They will have the option to add their interest to the principal of their loan (capitalize the interest) and make 2 payments to rehabilitate their loan.

Loan write-off

As per standard accounting practices, the Government of Canada must write-off Canada Student Loans that have been deemed unrecoverable after all reasonable collection efforts have been made. The majority of the write-off value is comprised of loans that have not received payment or acknowledgement of debt for 6 years. Other reasons for write-off include bankruptcy, extreme financial hardship, and compromise settlements.

The value of loans written-off in 2018 was $200 million of the directly financed Canada Student Loan portfolio, which was higher than the 2017 write-off of $174.8 million and the 2016 write-off of $172 million. Although the $200 million was slightly higher than the previous 2 years, the write-off amount across these 3 years represents approximately 1% of the overall value of the directly financed Canada Student Loans portfolio. The write-off of any debt does not mean the debt is forgiven. Should an individual wish to access student financial assistance from the CSLP in the future, this debt must be addressed. In a situation where a CSL debt is reinstated, any interest charges that accrued on the debt are also reinstated.

Program integrity

The CSLP strives to safeguard the integrity of the Program by ensuring that all aspects of the Program are operating within the legal framework of the Canada Student Financial Assistance Act and the Canada Student Loans Act.

The Program has in place a number of policies and activities designed to ensure its integrity and to enhance governance and accountability:

- administrative measures may be taken when individuals knowingly misrepresent themselves to obtain student financial assistance; including being restricted from receiving student financial assistance for a specified period, being required to immediately repay any money obtained as a result of false information and having their grants converted to repayable loans. If warranted, further action may be taken such as criminal investigation or civil litigation. In the 2017 to 2018 school year, 20 cases of misrepresentation were confirmed as abuse

- in keeping with provisions of the Canada Student Financial Assistance Act, the Office of the Chief Actuary conducts a statutory actuarial review of the Program in order to provide a long-term forecast of the portfolio and program costs. The most recent Actuarial Report (2018) (PDF format) is available on the website of the Office of the Superintendent of Financial Institutions

- the Designation Policy Framework establishes Canada-wide criteria for designation—the process whereby post-secondary educational institutions are deemed eligible for student financial assistance programs. The Framework ensures that federal and provincial and territorial student financial assistance portfolios operate within the principles and practices of reasonable financial stewardship. As a part of this framework, the CSLP calculates and tracks the repayment rates of Canada Student Loans for designated Canadian institutions. The 2018 repayment rate for borrowers who entered repayment in 2016 to 2017 was 91%, which is the same as the previous year, and the highest it has been over the past 14 years

Appendix A – Canada Apprentice Loan

Support for apprentices

The Canada Apprentice Loan (CAL) provides additional financial support to apprentices in Red Seal trades during periods of technical training, to help them complete their apprenticeship, and to encourage more Canadians to consider a career in the skilled trades.

Eligible apprentices may apply for loans of up to $4,000 per period of technical training, for a maximum of 5 periods. The loans are interest-free until apprentices complete or leave their apprenticeship training program, for up to a maximum of 6 years. Given the timing of technical training requirements in their province, apprentices in Quebec do not qualify for CAL. The province of Quebec is compensated with an annual special payment.

In the 2017 to 2018 loan year, Canada Apprentice Loans amounting to $58.8 million were disbursed to 14,000 apprentices. 78% of disbursed loans went to apprentices from 3 provinces: Alberta (44%), British Columbia (21%) and Ontario (13%).

Appendix B – Financial data

Consolidated report on the Canada Student Loans Program

Since 2000, the Government of Canada has provided student financial assistance directly to borrowers, unlike earlier CSLP lending regimes that were administered by financial institutions.

Under direct lending, the Government of Canada finances and administers the CSLP, contracting with a private-sector service provider (the National Student Loans Service Centre (NSLSC)) to manage student loan accounts from disbursement to repayment.

Reporting entity

The entity detailed in this report is the CSLP only and does not include departmental operations related to the delivery of the CSLP. Expenditure figures are primarily statutory in nature, made under the authority of the Canada Student Financial Assistance Act and the Canada Student Loans Act.

Basis of accounting

The financial figures are prepared in accordance with generally accepted accounting principles and as reflected in the Public Sector Accounting Handbook of the Canadian Institute of Chartered Accountants.

Table 6 – Consolidated Canada Student Loans Programs – Combined programs

Legend:

- DL = Direct loans

- RS = Risk-shared loans

- GL = Guaranteed loans

| Revenues | 2015 to 2016 Actual (in million $) |

2016 to 2017 Actual (in million $) |

2017 to 2018 Actual (in million $) |

|---|---|---|---|

| Interest revenue on direct loans | 627.1 | 650.0 | 720.5 |

| Recoveries on guaranteed loans | 10.5 | 8.6 | 6.7 |

| Recoveries on put-back loans (RS) | 5.9 | 4.9 | 4.2 |

| Total loan revenue | 643.5 | 663.5 | 731.4 |

| Expenses | Details | 2015 to 2016 Actual (in million $) |

2016 to 2017 Actual (in million $) |

2017 to 2018 Actual (in million $) |

|---|---|---|---|---|

| Transfer payment | Canada Study Grants, Canada Access Grants and Canada Student Grants | 713.9 | 974.6 | 1,323.1 |

| Loan administration | Collection costs (all regimes)1 | 22.4 | 24.1 | 23.2 |

| Program delivery costs (DL) | 76.0 | 84.9 | 96.0 | |

| Risk premium to financial institutions (RS) | 0.0 | 0.0 | 0.0 | |

| Put-back to financial institutions (RS) | 1.8 | 1.1 | 1.4 | |

| Administrative fees to provinces and territories and Special Investment Fund (DL) | 31.8 | 30.2 | 30.6 | |

| Total loan administration expenses | 131.8 | 140.4 | 151.1 | |

| Cost of Government support benefits to students | In-study interest borrowing expense (Class A – DL)1 | 104.2 | 100.8 | 144.5 |

| In repayment interest borrowing expense (Class B – DL)1 | 123.9 | 126.0 | 182.1 | |

| In-study interest subsidy (RS and GL) | 0.2 | 0.1 | 0.1 | |

| Repayment assistance programs | 165.8 | 182.1 | 216.4 | |

| Claims paid and loans forgiven (all regimes) | 27.8 | 41.0 | 44.1 | |

| Total cost of government support benefits to students | 421.8 | 450.0 | 587.3 | |

| Bad debt expense2 | Debt reduction in repayment expense (DL) | 231.2 | 87.4 | 110.7 |

| Bad debt expense (DL) | 94.1 | 203.7 | 235.9 | |

| Total bad debt expense | 325.3 | 291.0 | 346.6 | |

| Total loan expenses | 1,592.9 | 1,856.0 | 2,408.1 | |

| Net operating results | 2015 to 2016 Actual (in million $) |

2016 to 2017 Actual (in million $) |

2017 to 2018 Actual (in million $) |

|---|---|---|---|

| Net operating results | 949.3 | 1,192.5 | 1,676.7 |

| Alternative payments to non-participating provinces (DL)3 | 258.4 | 305.4 | 376.4 |

| Final net operating results | 1,207.6 | 1,497.8 | 2,053.1 |

Table notes

- These costs are related to Canada Student Direct Loans but reported by the Department of Finance.

- This represents the annual expense against the Provisions for Bad Debt and Repayment Assistance Payments – Principal as required under Accrual Accounting.

- The figures represent the annual expense recorded under the Accrual Accounting as opposed to the actual amount disbursed to the Non-Participating Provinces. For loan year 2016 to 2017, the total amount disbursed as Alternative Payments was $338.6 million.

Glossary

- Consolidation

- Borrowers consolidate their student loan(s) 6 months after the end of their post-secondary studies (or ending full-time studies). Repayment begins once they have consolidated their loans.

- Default

- A loan is deemed in default when it is in arrears for greater than 270 days under the direct lending regime.

- Default rate

- The CSLP measures default using a 3-year default rate. This rate shows the proportion of loan dollars that enter repayment in a given loan year and default within 3 years. For example, the 2016 to 2017 default rate represents the proportion of loan dollars that entered repayment in the 2016 to 2017 loan year and defaulted before August 1, 2019.

- Designated educational institution

- A designated post-secondary educational institution meets provincial and territorial and federal eligibility criteria, and students attending these schools can apply for government-sponsored student financial assistance, such as Canada Student Grants and Canada Student Loans.

- Direct loans

- As of August 2000, the federal government issued Canada Student Loans under the direct loans regime. Loans are directly financed by the Government and a third-party service provider administers the loan process.

- Full-time

- A full-time student is a student enrolled in at least 60% of a full course load (or 40% for students with permanent disabilities) in a program of study of at least 12 consecutive weeks at a designated post-secondary educational institution.

- Guaranteed loans

- Between 1964 and 1995, Canada Student Loans were provided by financial institutions (such as banks) under the guaranteed loans regime. If a student defaulted on a guaranteed loan, the Government paid out the bank and the student’s debt was then owed directly to the Government.

- Integrated province

- In integrated provinces, federal and provincial loans are combined so that borrowers receive and repay one federal and provincial integrated loan. The federal and provincial governments work together to make applying for, managing and repaying loans easier. The CSLP has integration agreements with five provinces: British Columbia, Saskatchewan, Ontario, New Brunswick and Newfoundland and Labrador.

- In-study

- The status of borrowers attending full- or part-time studies at a post-secondary institution, or who have finished school less than 6 months ago.

- Loan year

- August 1 to July 31.

- Part-time

- A part-time student is a student taking between 20% and 59% of a full course load. Students with permanent disabilities may be accorded part-time status if they are taking between 20% and 39% of a full course load. If they are taking between 40% and 59% of a full course load they can elect to be considered either as a full-time or part-time student for the purpose of the CSLP.

- Participating provinces and territories

- The provinces and territories that choose to deliver financial assistance to students within the framework of the CSLP include Newfoundland and Labrador, Prince Edward Island, Nova Scotia, New Brunswick, Ontario, Manitoba, Saskatchewan, Alberta, British Columbia and Yukon.

- Province or territory of residence

- A student’s province or territory of residence is the province or territory where they have most recently lived for at least 12 consecutive months prior to starting post-secondary education. For example, an individual from Manitoba studying in Ontario would be considered a Manitoba student.

- Post-secondary education

- Levels of education following secondary school (high school) at all designated public or private post-secondary institutions.

- Repayment

- The status of borrowers who have begun repaying their Canada Student Loans. Repayment begins 6 months following the end of studies.

- Repayment rate

- The repayment rate is the percentage of the total principal amount of Canada Student Loans consolidated in a given loan year that is repaid or in good standing at the end of the subsequent loan year.

- Revision of terms

- A means of allowing borrowers to manage their loan repayment in a way that is responsive to their situation. It can be used to decrease monthly payments (extending the loan term to a maximum of 14.5 years), or to increase loan payments allowing the borrower to pay off the loan sooner.

- Risk-shared loans

- Between 1995 and 2000, Canada Student Loans were provided by financial institutions (such as banks) under the risk-shared loans regime. Under this regime, financial institutions assumed responsibility for a portion of the possible risk of defaulted loans in return for a payment from the Government.

- Student financial assistance

- Student financial assistance is any form of financial aid provided by the Canada Student Loans Program to students while they are enrolled in designated post-secondary education institutions, including Canada Student Grants, Canada Student Loans and in-study interest subsidies.