Canada Health Act Annual Report 2022-2023

Download in PDF format

(35.96 MB, 430 pages)

Organization: Health Canada

Date published: 2024-02-15

Cat.: H1-4E-PDF

ISSN: 1497-9144

Pub.: 230732

Table of Contents

- Acknowledgements

- Minister's Message

- Canada Health Act 2022-2023 Year in Review Infographic

- Chapter 1 - Canada Health Act Overview

- Chapter 2 - Administration and Compliance

- Chapter 3 - Provincial and Territorial Health Care Insurance Plans in 2022-2023

- Annex A - Canada Health Act and Extra-Billing and User Charges Information Regulations

- Annex B - Financial Statements of Actual Amounts of Extra-Billing and User Charges for the Period April 1, 2020 to March 31, 2021

- Annex C - Policy Interpretation Letters

- Annex D - Reimbursement Action Plans & Progress Reports

- Contact Information

Acknowledgements

Health Canada would like to acknowledge the work and effort that went into producing this Annual Report. It is through the dedication and timely commitment of the following departments of health and their staff that we are able to bring you this report on the administration and operation of the Canada Health Act:

- Newfoundland and Labrador Department of Health and Community Services

- Prince Edward Island Department of Health and Wellness

- Nova Scotia Department of Health and Wellness

- New Brunswick Department of Health

- Quebec Ministry of Health and Social Services

- Ontario Ministry of Health

- Manitoba Health, Seniors, and Long-Term Care

- Saskatchewan Ministry of Health

- Alberta Ministry of Health

- British Columbia Ministry of Health

- Yukon Department of Health and Social Services

- Northwest Territories Department of Health and Social Services

- Nunavut Department of Health

We also greatly appreciate the extensive work effort that was put into this report by our production team, including desktop publishers, translators, editors and concordance experts, printers and staff of Health Canada.

Minister's Message

I am honoured to serve as the federal Minister of Health during a critical time for Canada's health care system. I present to Parliament and to Canadians, the 2022-2023 Canada Health Act Annual Report. This report documents the ways in which both the federal government and the provincial and territorial governments have upheld and fulfilled the principles of the Canada Health Act.

I want to first acknowledge that this past September, Canada lost a great trailblazer and tenacious advocate for Medicare, the Honourable Monique Bégin. During her tenure as Minister of Health and Welfare, at a time when our publicly funded system was under significant strain, she introduced and shepherded through the passage of the Canada Health Act, to see that our health care system reflected the Canadian values of equity, fairness, and solidarity. For this outstanding legacy, she is known as the Mother of Medicare. The Government of Canada honours her through our commitment to the Act and its principles.

Once again our health care system, and the workers that are at its core, are under enormous pressure, a situation which has been exacerbated by the pandemic and its lingering effects. All levels of government agree that immediate and ongoing action is required to deliver better health care for Canadians. This past October, I met with my provincial and territorial counterparts in Charlottetown, where we reaffirmed our commitment to working collaboratively on the shared priorities outlined in the Working Together to Improve Health Care for Canadians plan: expanding access to family health services; supporting our health workers and reducing backlogs; increasing support for mental health and addiction services; and modernizing Canada's health care systems.

As the Government of Canada makes historic investments of close to $200 billion for our health care system, I am working with all provinces and territories to make sure this funding is used to deliver better care to patients while supporting our health workers. When announcing these investments, the Prime Minister was clear that, as provinces and territories use federal dollars to bolster their health care systems, they will be expected to respect the principles of the Canada Health Act so that access to insured services is based on health needs, and not on the ability or willingness to pay.

Universal access has always been a fundamental part of our health care system, and when patients face charges when seeking required care, this government will take action. In March 2023, over $82.5 million in mandatory Canada Health Transfer deductions were levied to provinces which permitted patient charges for medically necessary services; this included the first deductions under the Canada Health Act's Diagnostic Services Policy. This Policy, which came into effect on April 1, 2020, formalized the long-standing federal position that medically necessary diagnostic services are to be considered insured services, regardless of the venue in which they are delivered (i.e., a hospital or a private facility), and that patients should not face charges to access such services.

The Government of Canada's goal in administering the Canada Health Act is not to levy penalties, but to protect the right that Canadians do not pay out of pocket for medically necessary health services. This is why provinces and territories that choose to work with Health Canada and take the necessary steps to put an end to patient charges for medically necessary services, and the underlying circumstances which led to the charges, are eligible to receive a reimbursement of their deductions under the Canada Health Act's Reimbursement Policy.

By working together with my provincial and territorial counterparts with a shared goal of getting Canadians the services they need regardless of their ability to pay, we will deliver better health care to all Canadians.

Canada Health Act 2022-2023 Year in Review Infographic

Text description

- In Budget 2023, the Government of Canada announced investments of close to $200 billion over 10 years to improve health care for Canadians. This includes $25 billion to provinces and territories (PTs) to advance shared health priorities through tailored bilateral agreements that will allow for flexibility to address the unique geographical needs of people in each province and territory. As PTs use these funds to bolster their health care systems, they are expected to uphold the principles of the Canada Health Act to protect access to health care that is based on need and not the ability to pay.

- In 2022-2023, provinces and territories received over $45.2 billion in Canada Health Transfer payments.

- On April 6, 2023, the Supreme Court of Canada decided not to hear an appeal of the British Columbia (BC) Court of Appeal decision in Cambie Surgeries Corporation et al v. BC (Attorney General), bringing this case, which was initiated in 2009, to a close.

- With this decision, the BC Court of Appeal ruling in this case stands, upholding British Columbia's ban on patient charges and the purchase of duplicative private insurance for services publicly insured under the BC Medical Services Plan, as well as BC's de facto prohibition on physician dual practice.

- In March 2023, the first deductions under the Diagnostic Services Policy were levied, resulting in over $76.4 million in Canada Health Transfer deductions to BC, AB, SK, MB, QC, NB and NS for patient charges for medically necessary diagnostic services.

- Over $8.5 million was also reimbursed to BC for actions taken to eliminate patient charges for medically necessary diagnostic services.

- Based on action taken by provinces to ensure patients do not face charges for medically necessary services more than $84.9 million in deductions has been reimbursed since 2018.

Chapter 1 - Canada Health Act Overview

This section describes the evolution of Medicare in Canada, as well as the Canada Health Act, its key definitions, requirements, regulations, penalty provisions, and excluded persons and services under the Act. It also outlines interpretation letters from former federal Ministers of Health sent to their provincial and territorial counterparts, following months of consultation:

- the Honourable Jake Epp provided guidance on the interpretation and implementation of the Act;

- the Honourable Diane Marleau announced the Federal Policy on Private Clinics; and

- the Honourable Ginette Petitpas Taylor formalized three new Canada Health Act initiatives— the Diagnostic Services Policy, the Reimbursement Policy, and strengthened Canada Health Act reporting.

The Evolution of Medicare in Canada

Canada's single-payor public health care insurance system, "Medicare", is financed through a progressive tax system, which allows risks to be pooled and costs to be shared by all Canadians. Our health care insurance system evolved into its present form over more than six decades. Saskatchewan was the first province to establish universal, public hospital insurance in 1947 and, 10 years later, the Government of Canada passed the Hospital Insurance and Diagnostic Services Act (HIDSA), to encourage provinces and territories to provide universal coverage for these services by sharing in their costs. Its unanimous adoption by the federal Parliament launched the largest single program ever undertaken in peace-time Canada and, by 1961, all the provinces and territories had public insurance plans that provided universal access to hospital services. Saskatchewan again pioneered by providing insurance for physician services, beginning in 1962. The Government of Canada enacted the Medical Care Act in 1966, to encourage provinces and territories to provide universal coverage for physician services by sharing in their costs. By 1972, all provincial and territorial plans had been expanded to include physician services.

In 1979, at the request of the federal government, Justice Emmett Hall undertook a review of the state of health services in Canada. In his report, he affirmed that health care services in Canada ranked among the best in the world, but warned that extra-billing by doctors and user charges levied by hospitals were creating a two-tiered system that threatened the universal accessibility of care. This report, and the national debate it generated, led to the enactment of the Canada Health Act.

Remembering the late Honourable Monique Bégin

1936-2023

Monique Bégin became one of the first female Members of Parliament from Quebec in the 1972 Liberal cabinet, and is well remembered as a pioneering voice for universal health care, during a time when opposition was plentiful.

Bégin held tenure as the Minister of Health and Welfare from 1977-1979 and again from 1980-1984. In 1984, Bégin introduced the Canada Health Act to protect and promote universal health care in Canada, which endures to this day.

After leaving politics in 1984, Bégin continued on to have a successful career in academia, where she held many positions. She was both an Officer and a Companion of the Order of Canada, and was bestowed 18 honourable doctorates, as well as many other notable distinctions.

"I've been called the saviour of medicare…It's a great honour, but I just did my job."

Monique Bégin

Passed unanimously in the House of Commons in 1984, the Canada Health Act, Canada's federal health care insurance legislation, codified the national principles which underpin federal funding for hospital and physician services and added prohibitions on the patient charges which threatened to undermine universal access to care.

In Canada, the roles and responsibilities for health are shared between the federal, provincial and territorial governments. The provincial and territorial governments have primary jurisdiction in health care administration and delivery. This includes setting their own priorities, administering their health care budgets and managing their own resources. The federal government, under the Canada Health Act, defines the national principles that are to be reflected in provincial and territorial health care insurance plans.

What is the Canada Health Act?

The Act establishes criteria and conditions related to insured health services and extended health care services that the provinces and territories must fulfill to receive the full federal cash contribution under the Canada Health Transfer (CHT). In fiscal year 2022-2023, the CHT was $45,208,000,000. Additional information on federal, provincial and territorial funding arrangements is available by visiting the Department of Finance's website.

The aim of the Act is to ensure that all eligible residents of Canadian provinces and territories have reasonable access to medically necessary hospital, physician, and surgical-dental services that require a hospital setting, on a prepaid basis, without charges related to the provision of insured health services.

A copy of the Act is provided in Annex A.

In Budget 2023, the Government of Canada announced additional health investments of close to $200 billion over the next ten years, including $48.7 billion in new funding for provinces and territories.

The federal government continues to work with the provinces and territories to ensure the new investments are used in the best interest of health workers and patients, while respecting the principles of the Canada Health Act, to ensure that access to insured health services is based on need, and not on ability or willingness to pay.

Key Definitions under the Canada Health Act (Section 2)

Insured health services are medically necessary hospital, physician and surgical-dental services (performed by a dentist in a hospital, where a hospital is required for the proper performance of the procedures) provided to insured persons, unless those services are provided under another Act of Parliament, or provincial or territorial workers' compensation legislation.

Extended health care services are certain aspects of long-term residential care (nursing home intermediate care and adult residential care services), and the health aspects of home care and ambulatory care services.

Insured persons are eligible residents of a province or territory. A resident of a province is defined in the Act as "… a person lawfully entitled to be or to remain in Canada who makes his home and is ordinarily present in the province, but does not include a tourist, a transient or a visitor to the province…"

Insured hospital services include medically necessary in-patient and out-patient services such as accommodation and meals at the standard or public ward level and preferred accommodation if medically required; nursing service; laboratory, radiological and other diagnostic procedures, together with the necessary interpretations; drugs, biologicals and related preparations when administered in the hospital; use of operating room, case room and anaesthetic facilities, including necessary equipment and supplies; medical and surgical equipment and supplies; use of radiotherapy facilities; use of physiotherapy facilities; and services provided by persons who receive remuneration therefor from the hospital.

Insured physician services are medically required services rendered by medical practitioners. Medically required physician services are generally determined by the provincial or territorial health care insurance plan, in consultation with the medical profession.

Insured surgical-dental services are services provided by a dentist in a hospital, where a hospital setting is required for the proper performance of the procedure.

The Canada Health Act Infographic

Text description

Requirements of the Canada Health Act

The Canada Health Act contains nine requirements that the provinces and territories must fulfill in order to qualify for the full amount of their cash entitlement under the CHT.

They are:

- five program criteria that apply only to insured health services;

- two conditions that apply to insured health services and extended health care services; and

- two provisions, with respect to extra-billing and user charges, that apply only to insured health services.

The Criteria

1.0 Public Administration (section 8)

The public administration criterion of the Canada Health Act requires provincial and territorial health care insurance plans to be administered and operated on a non-profit basis by a public authority, which is accountable to the provincial or territorial government for decision-making on benefit levels and services, and whose records and accounts are publicly audited. However, the criterion does not prevent the public authority from contracting out the services necessary for the administration of the provincial and territorial health insurance plans, such as the processing of payments to physicians for insured health services.

The public administration criterion pertains only to the administration of provincial and territorial health care insurance plans and does not preclude private facilities or providers from supplying insured health services as long as no insured person is charged in relation to the provision of these insured health services.

2.0 Comprehensiveness (Section 9)

The comprehensiveness criterion requires that the health care insurance plan of a province or territory must cover all insured health services provided by hospitals, physicians or dentists (i.e., surgical-dental services that require a hospital setting).

3.0 Universality (Section 10)

Under the universality criterion, all insured residents of a province or territory must be entitled to the insured health services provided by the provincial or territorial health care insurance plan on uniform terms and conditions. Provinces and territories generally require that residents register with the plan to establish entitlement.

4.0 Portability (Section 11)

Residents moving from one province or territory to another must continue to be covered for health care services insured by the home jurisdiction during any waiting period imposed by the new province or territory of residence (up to three months), before coverage is established in the new jurisdiction. It is the responsibility of residents to inform their province or territory's health care insurance plan that they are leaving and to register with the health care insurance plan of their new province or territory, in order to avoid any gaps in coverage.

Residents who are temporarily absent from their home province or territory, or from Canada, must continue to be covered for insured health services by their home province or territory. If insured persons are temporarily absent in another province or territory, the portability criterion requires that insured health services be paid at the host province's rate. If insured persons are temporarily out of the country, insured health services are to be paid at the home province's rate.

The portability criterion is intended to permit a person to receive medically necessary services in relation to an urgent or emergent need, when absent on a temporary basis (e.g., business or vacation) but does not entitle residents to seek services or shorter waits for non-urgent or emergent services. Prior approval by the health care insurance plan in a person's home province or territory may be required before coverage is extended for elective (non-emergency) services to a resident while temporarily absent from their province or territory.

5.0 Accessibility (Section 12)

The intent of the accessibility criterion is to ensure that insured persons in a province or territory have reasonable access to insured hospital, medical, and surgical-dental services that require a hospital setting, on uniform terms and conditions, unprecluded or unimpeded, either directly or indirectly, by charges (extra-billing or user charges) or other means (e.g., discrimination on the basis of age, race, health status, or financial circumstances).

Reasonable access in terms of physical availability of medically necessary services has been interpreted under the Canada Health Act using the "where and as available" principle. Thus, residents of a province or territory are entitled to have access on uniform terms and conditions to insured health services at the setting "where" the services are provided and "as" the services are available in that setting. For example, if a hospital in one region of a province was providing highly specialised services, that would not mean that all hospitals in the province would be required to provide the same service. Rather, it means that all residents of the province should have access to the service wherever it is being offered, on the same basis.

In addition, the health care insurance plan of the province or territory must provide:

- reasonable compensation to physicians and dentists for all the insured health services they provide; and

- payment to hospitals to cover the cost of insured health services.

The Conditions

1.0 Information (Section 13[A])

Provincial and territorial governments are required to provide information to the federal Minister of Health as prescribed by regulations under the Act.

2.0 Recognition (Section 13[B])

Provincial and territorial governments are required to recognize the federal financial contributions toward both insured and extended health care services.

The Provisions

Extra-Billing and User Charges

The provisions of the Canada Health Act pertaining to extra-billing and user charges for insured health services in a province or territory are outlined in sections 18 to 21. If it can be confirmed that either extra-billing or user charges exist in a province or territory, a mandatory dollar-for-dollar deduction from the CHT payments to that province or territory is required under the Act.

Extra-Billing (Section 18)

Under the Act, extra-billing is defined as a charge by an enrolled medical practitioner or dentist (i.e., a dentist providing insured surgical-dental services in a hospital setting) to an insured person for an insured health service in addition to the amount paid by the provincial or territorial health care insurance plan. For example, if a medical practitioner were to charge a patient any amount for an office visit that is insured by the provincial or territorial health care insurance plan, the amount charged would constitute extra-billing. Extra-billing is seen as a barrier for people seeking medical care, and is contrary to the accessibility criterion.

User Charges (Section 19)

A user charge is defined as any charge for an insured health service, other than extra-billing. This includes any charge levied for insured hospital services, or any non-physician related services provided in conjunction with an insured physician service at a non-hospital facility (e.g., private practice). In other words, if patients were charged a fee as a condition of receiving insured health services, that fee would be considered a user charge. User charges are not permitted under the Act because, as is the case with extra-billing, they constitute a barrier to access.

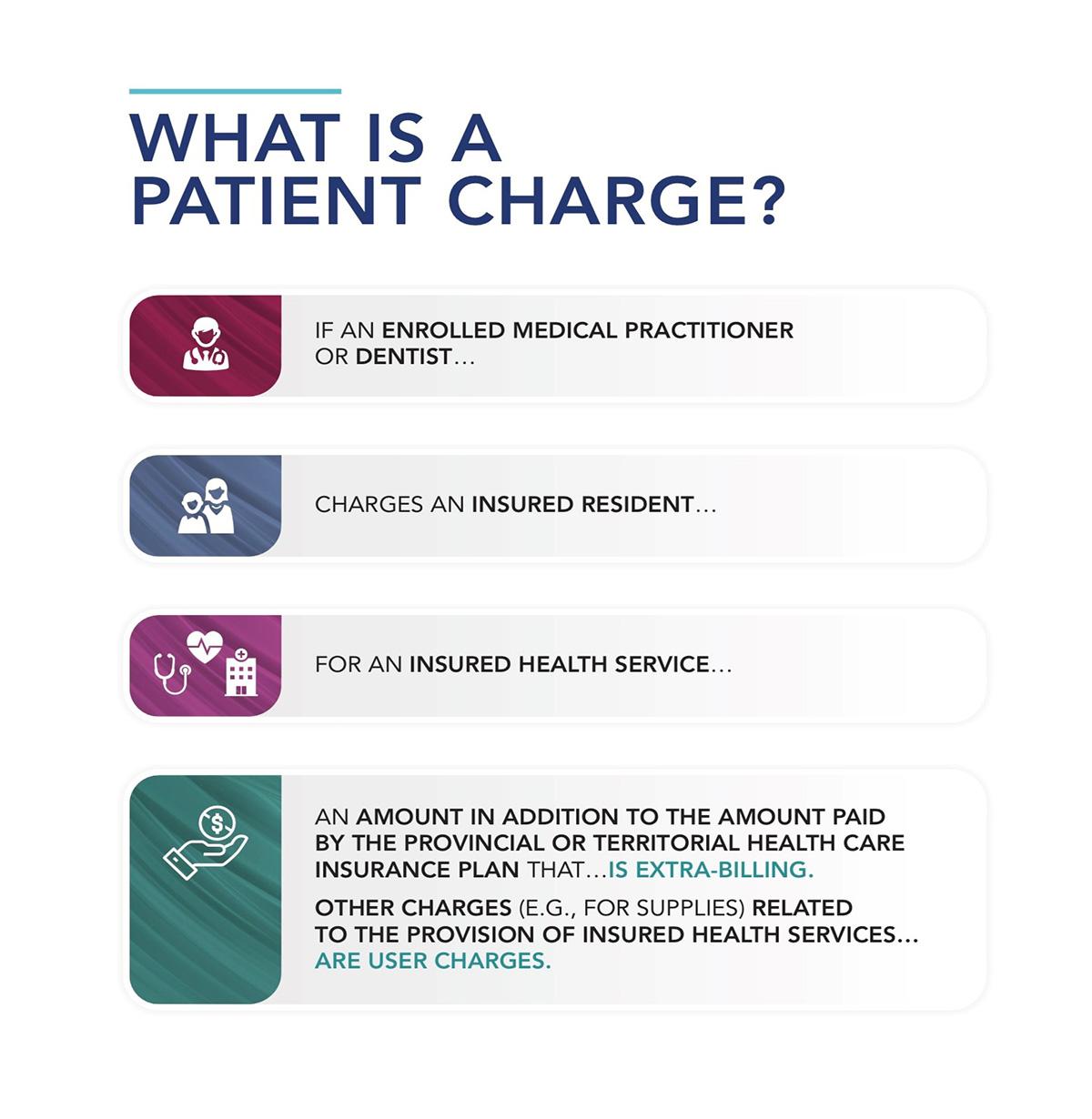

What is a patient charge?

Text description

What is a Patient Charge? Infographic

- If an enrolled medical practitioner or dentist…

- Charges an insured resident…

- For an insured health service…

- An amount in addition to the amount paid by the provincial or territorial health care insurance plan that…

- is extra-billing.

- Other charges (e.g., for supplies) related to the provision of insured health services…

- Are user charges.

Other Elements of the Act

Regulations (Section 22)

Section 22 of the Canada Health Act enables the federal government to make regulations for administering the Act in the following areas:

- defining the services included in the Act's definition of "extended health care services," e.g., nursing home care or home care;

- prescribing which services are excluded from hospital services;

- prescribing the types of information that the federal Minister of Health may reasonably require, as well as the format and submission deadline for the information; and

- prescribing how provinces and territories are required to recognize the CHT in their documents, advertising or promotional materials.

To date, the only regulations in force under the Act are the Extra-billing and User Charges Information Regulations. These Regulations require the provinces and territories to report annually to Health Canada on the amounts of extra-billing and user charges levied. A copy of these Regulations is provided in Annex A.

Penalty Provisions of the Canada Health Act

Mandatory Penalty Provisions

Under the Act, provinces and territories that allow extra-billing and user charges are subject to mandatory dollar-for-dollar deductions from the federal transfer payments under the CHT. For example, if it is determined that any amount of extra-billing by physicians has occurred in a province or territory, the federal cash contribution to that province or territory will be reduced by that same amount. Although deductions are usually based on information provided by the province or territory in accordance with the Extra-billing and User Charges Information Regulations, where information is not provided, or is incomplete, Health Canada will make an estimate of the amount of extra-billing and user charges. This process requires consultation with the province or territory concerned. Deductions based on estimates have been made on numerous occasions.

Provincial and territorial financial statements of extra-billing and user charges received during the reporting period are provided in Annex B.

Discretionary Penalty Provisions

Non-compliance with one of the five criteria or two conditions of the Act is subject to a discretionary penalty. The amount of any deduction from CHT payments is based on the magnitude of the non- compliance, and is approved by Cabinet.

The Canada Health Act sets out a consultation process that must be undertaken with the province or territory before discretionary penalties can be levied. To date, the discretionary penalty provisions of the Act have not been used.

Excluded Services and Persons

Although the Canada Health Act requires that insured health services be provided to insured persons in a manner that is consistent with the criteria and conditions set out in the Act, not all health care services or Canadian residents fall under the scope of the Act.

Excluded Services

A number of services provided by hospitals and physicians are not considered medically necessary, and, thus, are not insured under provincial and territorial health care insurance legislation. Uninsured hospital services for which patients may be charged include preferred hospital accommodation (unless prescribed by a physician or when standard ward level accommodation is unavailable), private duty nursing services, parking, and the provision of telephones and televisions. Uninsured physician services for which patients may be charged include telephone advice (unless it is insured by the provincial or territorial health care insurance plan); the provision of medical certificates (e.g., for work, school, insurance purposes); the transfer of medical records; testimony in court; and cosmetic services. Amounts for these services are governed by provincial and territorial Colleges of Physicians, which generally require that charges be reasonable and reflect the cost of services provided.

The definition of "insured health services" excludes services provided to persons under any other Act of Parliament (e.g., certain services provided to veterans) or under the workers' compensation legislation of a province or territory.

In addition to the medically necessary hospital and physician services covered by the Canada Health Act, provinces and territories also provide a wide range of other programs and services, such as prescription drug coverage, non-surgical dental care, ambulance services and optometric services, at their discretion and on their own terms and conditions. These services are often targeted to specific population groups (e.g., seniors, children, and those receiving social assistance), with levels of funding and scope of coverage varying from one province or territory to another.

Excluded Persons

The Canada Health Act definition of "insured person" excludes members of the Canadian Armed Forces and persons serving a term of imprisonment within a federal penitentiary. The Government of Canada provides coverage to these groups through separate federal programs.

The exclusion of these persons from insured health service coverage predates the adoption of the Act and is not intended to constitute differences in access to publicly insured health care.

Policy Interpretation Letters

There are three key policy statements that clarify the federal position on the Canada Health Act. These statements were made in the form of ministerial letters from former federal Ministers of Health to their provincial and territorial counterparts, following months of consultation. Copies of the letters are provided in Annex C of this report.

Epp Letter

In June 1985, approximately one year following the passage of the Canada Health Act in Parliament, federal Minister of Health and Welfare Jake Epp wrote to his provincial and territorial counterparts to set out and confirm the federal position on the interpretation and implementation of the Act. The letter sets forth statements of federal policy intent that clarify the Act's criteria, conditions and regulatory provisions. The letter highlighted the fundamental change signified by the Canada Health Act, which was the prohibition of all patient charges for insured health services provided to insured residents. The Epp letter remains an important reference for assessing and interpreting compliance with the Act.

Marleau Letter—Federal Policy on Private Clinics

Between February and December of 1994, a series of seven federal, provincial and territorial meetings dealing wholly, or in part, with private clinics took place. At issue was the growth of private clinics providing medically necessary services funded partially by the public system and partially by patients, and their impact on Canada's universal, publicly funded health care system.

At the September 1994 federal, provincial and territorial meeting of Health Ministers in Halifax, all Ministers of Health present, with the exception of Alberta's Health Minister, agreed to "…take whatever steps were required to regulate the development of private clinics in Canada."

Diane Marleau, the federal Minister of Health at the time, wrote to all provincial and territorial Ministers of Health on January 6, 1995, to announce the new Federal Policy on Private Clinics. The Minister's letter provided the federal interpretation of the Canada Health Act as it relates to the issue of facility fees charged directly to patients receiving medically necessary services at private clinics. The letter stated that the definition of hospital contained in the Act includes any facility that provides acute, rehabilitative or chronic care. Thus, when a provincial or territorial health care insurance plan pays the physician fee for a medically necessary service delivered at a private clinic, it must also pay the facility fee or face a deduction from federal transfer payments.

Petitpas Taylor Letter

On August 8, 2018, the former federal Minister of Health, Ginette Petitpas Taylor, wrote to her provincial and territorial counterparts formalizing three new Canada Health Act initiatives – the Diagnostic Services Policy, the Reimbursement Policy, and strengthened Canada Health Act reporting. These initiatives were the subject of discussion at the federal, provincial and territorial officials' level and adjustments were made to the requirements of these initiatives based on feedback received from the provinces and territories.

Diagnostic Services Policy

The Diagnostic Services Policy came into effect on April 1, 2020. This policy is a formalization of the application of the Canada Health Act to diagnostic services. It confirms the longstanding federal position that medically necessary services, including diagnostic services, are insured regardless of the venue where the services are delivered. Under this policy, provinces and territories first reported on patient charges for medically necessary diagnostic services in December 2022 (for any patient charges which occurred during 2020–2021) and will be published in the 2022-2023 Canada Health Act Annual Report.

Did you know?

Since April 1, 2020, any patient charges for medically necessary diagnostic imaging services, such as MRI or CT scans, regardless of where these services are provided (i.e., hospital or private facility), have been considered contrary to the Canada Health Act. Provinces and territories that permit patient charges for these services were subject to their first Canada Health Transfer deductions under the policy in March 2023. If you believe you have been charged inappropriately, you may report these charges to your provincial or territorial health ministry, using the phone numbers provided inside the back cover of this report. You may also contact the Canada Health Act Division of Health Canada at the following coordinates:

Reimbursement Policy

Should a province or territory be subject to a mandatory deduction, the federal Minister of Health has the discretion to provide a reimbursement if the province or territory eliminates the patient charges that led to the deductions within a specified timeframe. The first deductions eligible for reimbursement under the policy were those taken in March 2018.

Strengthened Canada Health Act Reporting

The aim of strengthened Canada Health Act reporting is to ensure Health Canada has the information required to accurately assess compliance with the Act, as well as to increase transparency for Parliament and Canadians on the administration of the Act, and the state of the publicly funded health care insurance system.

Canada Health Act Mythbusters

- MYTH:

- All health care in Canada must be publicly delivered.

- FACT:

- The Canada Health Act doesn't forbid the provision of health services by private companies, as long as residents are not charged for insured health services. In fact, many aspects of health care in Canada are delivered privately. Family physicians mostly bill the provincial or territorial health care insurance plan as private contractors. Hospitals are often incorporated private foundations, and many aspects of hospital care (e.g., lab services, housekeeping, and linens) are carried out privately. Lastly, in many provinces and territories, private facilities are contracted to provide services under the health care insurance plan.

- MYTH:

- Health care in Canada is free.

- FACT:

While you may not have to pay upfront when you receive medically necessary services, health care in Canada is not free. Health care in Canada is funded through tax revenues at the provincial, territorial, and federal levels. By spreading the cost of health care across the entire population, everyone is assured of the care they need, without the great financial burden that medical expenses could pose to a family or individual.

If you believe you have been subject to inappropriate patient charges for insured health services please contact your respective province or territory using the information contained in the Contact Information section of the report, or contact the Canada Health Act Division at medicare_hc@hc-sc.gc.ca.

- MYTH:

- I can use my health insurance card to find a shorter waitlist in another province or territory.

- FACT:

- Your health insurance card does not entitle you to seek out shorter waitlists in other provinces or territories. Although you are covered for insured health services during temporary absences from your home province or territory, prior approval may be required before coverage can be used for non-emergency services in another province or territory.

- MYTH:

- I'm a Canadian so I am automatically entitled to health care coverage.

- FACT:

- Having Canadian citizenship does not entitle you to health care coverage; rather, you must be an eligible resident within a province or territory. Canadians have their part to play in establishing and maintaining their health care coverage. In all provinces and territories, you are required to register for coverage, and then maintain your eligibility by renewing your coverage, and remaining in your home province or territory for a prescribed number of days each year. Although allowance is often made if you leave your home province or territory for school, work, or other reasons, it is important to inform your provincial or territorial health care insurance plan when you will be away for extended periods, and to understand what your responsibilities are in maintaining your coverage.

- MYTH:

- My specific medical condition is covered under the Canada Health Act.

- FACT:

- The Canada Health Act is quite a short piece of legislation and lays out standards at a very high level. Specific medical conditions are not named under the Act; rather, it requires provincial and territorial health care insurance plans to cover medically necessary hospital and physician services. Given their role in health care delivery, the decision over which services to cover is made by the province or territory, in consultation with the medical profession.

- MYTH:

- I don't need travel insurance within Canada because I'm covered under Medicare.

- FACT:

- This is a very common misconception, and one that could be quite costly under certain circumstances. Medicare ensures that if you leave your province or territory for a few hours, days or weeks, you will still have coverage for emergency medical services. The same is true during moves to other provinces or territories. However, the hospital and physician services covered under the Canada Health Act are not the only services you might need while outside your usual province or territory. Some services that are not covered by the Act (e.g., ambulance services) are highly subsidized for residents, but not for visitors, which is why you should ensure you have adequate coverage whenever you travel or move within the country.

Chapter 2 - Administration and Compliance

Administration

In administering the Canada Health Act, the federal Minister of Health (the Minister) is assisted by Health Canada staff and by the Department of Justice.

The Canada Health Act Division

The Canada Health Act Division of Health Canada is responsible for supporting the Minister in the administration of the Canada Health Act. Members of the Division fulfill the following ongoing functions:

- monitoring and analysing provincial and territorial health care insurance plans for compliance with the criteria, conditions, and extra-billing and user charges provisions of the Act;

- conducting issue analysis and policy research to provide strategic advice;

- asking provincial and territorial health ministries to investigate and provide information and clarification when possible compliance issues arise, and, when necessary, recommending corrective action to them in order to ensure the criteria, conditions, and extra-billing and user charges provisions of the Act are upheld;

- informing the federal Minister of Health of possible non-compliance and recommending appropriate action to resolve the issue;

- managing the annual extra-billing and user charges and reimbursement reporting processes;

- disseminating information on the Act and its administration;

- responding to enquiries about the Act and health care insurance issues received by telephone, mail and the Internet, from the public, members of Parliament, federal government departments, other governments, stakeholder organizations and the media;

- developing and maintaining relationships, with health officials in provincial and territorial governments, for information sharing;

- collaborating with provincial and territorial health department representatives through the Interprovincial Health Insurance Agreements Coordinating Committee;

- working with Health Canada Legal Services and Justice Canada on litigation issues that implicate the Act; and

- producing the Canada Health Act Annual Report on the administration and operation of the Act.

Canada Health Act Compliance

The Canada Health Act Division monitors the operations of provincial and territorial health care insurance plans in order to provide advice to the Minister on possible non-compliance with the Canada Health Act. Sources for this information include: provincial and territorial government officials and publications; nongovernmental organizations; media reports; and correspondence received from the public.

Staff in the Canada Health Act Division assess issues of concern and complaints on a case-by-case basis. The assessment process involves compiling all facts and information related to the issue and taking appropriate action. Verifying the facts with provincial and territorial health officials sometimes reveals issues that are not directly related to the Act, while others may pertain to the Act but are a result of misunderstanding or miscommunication, such as eligibility for health care insurance coverage and portability of insured health services within and outside Canada. In these instances, matters are generally resolved quickly with provincial or territorial assistance.

In instances where a Canada Health Act issue has been identified and remains after initial enquiries, Division officials ask the jurisdiction in question to investigate the matter and report back. Division staff discuss the issue and its possible resolution with provincial or territorial officials. Only if the issue is not resolved to the satisfaction of the Division after following the aforementioned steps, is it brought to the attention of the federal Minister of Health.

Deductions and Reimbursements under the Act

For the most part, provincial and territorial health care insurance plans meet, and often exceed, the requirements of the Canada Health Act. However, some issues and concerns remain. The most prominent of these relate to accessibility issues, and specifically patient charges for medically necessary health and diagnostic services at private clinics.

Diagnostic Services Policy

On April 1, 2020, the Canada Health Act Diagnostic Services Policy came into effect. The policy formalized the federal government's longstanding position that all medically necessary physician and hospital services, including diagnostic services, must be covered by provincial and territorial health insurance plans, regardless of the venue in which they are delivered.

Provinces and territories were expected to report patient charges for diagnostic services that occurred in fiscal year 2020-2021 in their annual report of patient charges in December 2022, which can be found in Annex B.

In the absence of reporting from most provinces on these patient charges, estimates of their magnitude were derived using a methodology based on the best available information, and shared with provinces before deductions were taken, to give them an opportunity to provide province-specific data. In March 2023, the following provinces were subject to mandatory dollar-for-dollar deductions, totalling approximately $76 million as a result of patient charges for medically necessary diagnostic services:

- Nova Scotia ($1,277,659);

- New Brunswick ($1,277,659);

- Quebec ($41,867,224);

- Manitoba ($353,827);

- Saskatchewan ($742,447);

- Alberta ($13,781,152); and

- British Columbia ($17,165,309 in deductions with $8,582,655 in reimbursements).

Mandatory deductions under the Diagnostic Services Policy will continue as long as patients continue to face charges for medically necessary diagnostic services.

Under the Canada Health Act Reimbursement Policy, mandatory Canada Health Transfer deductions may be reimbursed to provinces or territories if they eliminate the patient charges in question and rectify the circumstances that led to them, within two years of the date of the deduction. Through this process, a partial reimbursement for diagnostic services of $8,582,655 was provided to British Columbia, as a result of successfully implementing elements of its Reimbursement Action Plan with respect to eliminating patient charges for diagnostic services.

New Brunswick

In New Brunswick, surgical abortion services are insured under the provincial health care insurance plan but are only covered if performed in hospital; procedures provided in the private clinic in Fredericton are not covered. Health Canada has raised this issue with New Brunswick at the officials' level and Ministerial levels.

Although the province's financial statement of extra-billing and user charges for 2020-2021 indicated a nil amount, Health Canada used evidence provided by Clinic 554, as well as data published by the Canadian Institute for Health Information, to estimate patient charges for medically necessary surgical abortion services in the amount of $64,850. New Brunswick will continue to be subject to Canada Health Transfer (CHT) deductions for medically necessary surgical abortion services as long as New Brunswick does not cover insured surgical abortion services received outside hospitals.

Ontario

While the Ontario Health Insurance Plan provides coverage for physicians' fees related to abortion services in all settings, including private clinics, the province only covers facility fees in the four private abortion clinics licensed as Independent Health Facilities (IHF). In some instances, this has led to clinics charging patients out-of-pocket to access abortion services. Based on patient charges reported by Ontario to Health Canada, a deduction of $32,800 was levied against the province's CHT payment in March 2023 for patient charges that occurred in fiscal year 2020-2021.

In December 2021, Ontario submitted a Reimbursement Action Plan (RAP) to Health Canada, in which it committed to revisiting the current framework for the funding of insured surgical abortion services in the province. However, as a result of delays in implementing their Plan, Ontario has forfeited reimbursement of its March 2021 deduction ($13,905), as provinces are given two years to qualify for reimbursement under the Reimbursement Policy. Health Canada continues to engage with Ontario to encourage the province to fulfil the commitment made in their December 2021 Reimbursement Action Plan. A copy of Ontario's RAP as well the February 2024 status update on its implementation are presented in Annex D of this report.

British Columbia

British Columbia submitted a financial statement of extra-billing and user charges for fiscal year 2020–2021 in the amount of $5,945,221 for patient charges for medically necessary surgical services, which resulted in a deduction in the same amount to the province's March 2023 CHT payment.

In recognition of the significant strides British Columbia has made in successfully implementing elements of its Reimbursement Action Plan (RAP), and the elimination of patient charges for medically necessary surgical services during the reporting period, Health Canada authorized a reimbursement of $6,974,014 in March 2023. This represents a partial reimbursement of British Columbia's March 2021, 2022, and 2023 deductions. A copy of the RAP and February 2024 status update are presented in Annex D of this report.

| Province | Deductions for Diagnostic Services | Deductions for Surgical Services | Deduction Total | Reimbursement |

|---|---|---|---|---|

| NS | $1,277,659 | - | $1,277,659 | - |

| NB | $1,277,659 | $64,850 | $1,342,509 | - |

| QC | $41,867,224 | - | $41,867,224 | - |

| ON | - | $32,800 | $32,800 | - |

| MB | $353,827 | - | $353,827 | - |

| SK | $742,447 | - | $742,447 | - |

| AB | $13,781,152 | - | $13,781,152 | - |

| BC | $17,165,309 | $5,945,221 | $23,110,530 | $15,556,669Footnote * |

| Total | $76,465,277 | $6,042,871 | $82,508,148 | $15,556,669 |

|

||||

Additional Compliance Issues

Letter from Minister Duclos to his Provincial and Territorial Counterparts

On March 9, 2023, the previous Minister of Health, the Honourable Jean-Yves Duclos, sent a letter to his provincial and territorial counterparts that reaffirmed the Government's commitment to the Canada Health Act and communicated federal concerns with the increase in reports of patient charges related to virtual care and physician-equivalent services provided by other health care providers (e.g., nurse practitioners). The letter signalled the federal government's intent to clarify in a Canada Health Act interpretation letter that no matter how medically necessary care is delivered, Canadians must be able to access these services without patient charges. Moreover, as our health care system evolves, it must do so while respecting the Canada Health Act, in order to protect and preserve public coverage for all medically necessary health services. Minister Duclos tasked his officials to engage with provinces and territories to advance this work.

Enrollment and Membership Fees at Private Primary Care Clinics

Private primary care clinics that charge patients annual membership fees continue to be an issue of concern under the Canada Health Act. In many cases, these clinics provide their members with access to a mix of insured primary care services and uninsured health services (e.g., massage therapy and nutritional services). Typically, the clinics claim that the fees cover a basket of non-insured health services; however, in some cases these fees are also mandatory to access insured health services at the clinic.

When Health Canada becomes aware of such charges, the Department recommends the provinces and territories work with the clinics in question to make clear to insured residents that access to insured health services is not contingent or preferential based on the payment of annual fees for uninsured health services, which may also involve an investigation or audit of the billing practices of the clinic. When investigations or audits occur, Health Canada requests information about the findings and next steps to ensure any inappropriate patients charges have been eliminated. Health Canada also advises that these provinces and territories to develop legislation that is clear about patients' access to insured health services and which prohibits out-of-pocket charges to patients.

Portability

Physician services received by Quebec residents when out-of-province are not reimbursed at host province rates, which is a requirement of the portability criterion of the Canada Health Act.

For all jurisdictions, except Prince Edward Island and the three territories, the per diem rates for out-of-country hospital services appear lower than home province or territory rates, which is contrary to the requirement of the portability criterion of the Act. These concerns have been raised with the implicated provinces, and Health Canada continues to monitor the issue.

Cambie Surgeries Corporation et al v. BC (Attorney General) – The litigation has concluded

Launched in 2009, this case involved a constitutional challenge to provisions of British Columbia's Medicare Protection Act (MPA) that ban patient charges and the purchase of private duplicative private insurance for services publicly insured under the British Columbia (BC) Medical Services Plan, as well as BC's ban on enrolled physicians, who practice in the public and private system simultaneously, from charging patients for publicly insured services.

While the Canada Health Act (the Act) was not under direct challenge, Canada joined these proceedings, to play a supporting role to BC in defending its legislation, which reflects the objectives of the Act that access to insured health services should be based on need and not on the ability to pay.

The main challengers in this case, two private for-profit health facilities, argued that provisions of the MPA that place limits on a patient's ability to access more timely privately paid, medical care in order to avoid the potentially harmful affects of waiting for care in the public system violated section 7 (right to life, liberty and security of person) of the Canadian Charter of Rights and Freedoms (Charter). They also argued that exclusions under the MPA, which allow some BC residents (e.g., Workers' Compensation claimants) unobstructed access to timely care in the private system, violated section 15 (equality rights) of the Charter, claiming that removing the private pay restrictions would allow everyone the same access to private treatment, making access to health care more fair overall.

In response, BC argued that removing restrictions on private payment would reduce capacity and increase costs to the public system, while at the same time, putting the province at risk of losing federal funding for non-compliance with the requirements of the Act. Together, these factors would weaken the publicly funded system, reducing access and increasing wait times for care overall. BC argued that the most vulnerable individuals, who rely on the public system the most, would be further disadvantaged under these circumstances. The federal government agreed with BC's arguments, adding that a parallel private system would also worsen existing socioeconomic inequities, and result in negative consequences to Canadian society that go beyond health.

On September 10, 2020, Justice Steeves of the Supreme Court of British Columbia (BCSC) released his decision in the proceedings, which dismissed the constitutional challenge in its entirety. While the Court agreed that long waits for care may increase the risk of harm to some patients, it concluded that the provisions were reasonable and justified by the greater objective of safeguarding the sustainability and integrity of BC's publicly funded health system, in which access to care is based on need and not on the ability to pay.

This decision was appealed to the BC Court of Appeal (BCCA). In its July 2022 decision, the BCCA unanimously upheld the September 2020 decision of the BCSC affirming the constitutional validity of BC's challenged provisions.

The challengers in this case subsequently sought permission to appeal the BCCA decision to the Supreme Court of Canada (SCC). However, on April 6, 2023, the SCC declined to hear an appeal of the BCCA decision, bringing this case to a close.

"… It is for government and not the court to determine how to design an equitable system that achieves maximum benefit to society at large and fairly balances overall demand for necessary medical services."

Paragraph 2932, Cambie Surgeries Corporation v. British Columbia (Attorney General) Judgement by the Honourable Mr. Justice Steeves, September 10, 2020

| Date | Event |

|---|---|

| 2009 | The case is launched. |

| September 6, 2016 | The trial before the British Columbia Supreme Court begins. |

| February 28, 2020 | The trial concludes. |

| September 10, 2020 | The British Columbia Supreme Court releases its decision, which dismissed the constitutional challenge in its entirety. |

| June 14-18, 2021 | The British Columbia Court of Appeal hears the appeal of the British Columbia Supreme Court decision. |

| July 15, 2022 | The British Columbia Court of Appeal released its decision, unanimously upholding the decision of the British Columbia Supreme Court. |

| April 6, 2023 | The Supreme Court of Canada decides not to hear an appeal of the British Columbia Court of Appeal decision, bringing this case to a close. |

"The history of Medicare in Canada unequivocally demonstrates that this nation has decided that medically necessary insured health care services should not be treated as commodities or consumer goods to be purchased by the privileged few. The Canada Health Act helps to ensure that all Canadians have access to these services based on their need for them, not their ability to pay for them."

Paragraph 355, Attorney General of Canada, Closing Statements

Did you know?

The Cambie case is one of the longest trials in Canadian history? Here is a glimpse of the case by the numbers:

- 14 years between the launch and conclusion of this case.

- 131 witnesses provided evidence with 8,400 pages of affidavit evidence and almost 15,000 pages of court transcripts before the Supreme Court of British Columbia.

- 880 pages in the Supreme Court of British Columbia decision by Justice Steeves.

History of Deductions, Refunds, and Reimbursements under the Canada Health Act

The Canada Health Act, which came into force April 17, 1984, reaffirmed the national commitment to the original principles of the Canadian health care system, as embodied in the previous legislation, the Medical Care Act and the Hospital Insurance and Diagnostic Services Act. By putting into place mandatory dollar-for-dollar penalties for extra-billing and user charges, the federal government took steps to eliminate the proliferation of direct charges for hospital and physician services, judged to be restricting the access of many Canadians to health care services due to financial considerations.

Canada Health Act Compliance from 1984–1987

During the period 1984 to 1987, subsection 20(5) of the Act provided for deductions in respect of these charges to be refunded to the province if the charges were eliminated before April 1, 1987.

By March 31, 1987, it was determined that all provinces in which patients had been subject to extra-billing and user charges had taken appropriate steps to eliminate them. Accordingly, by June 1987, a total of $244,732,000 in deductions was refunded to New Brunswick, Quebec, Ontario, Manitoba, Saskatchewan, Alberta, and British Columbia.

| PTs | 1984-1985 | 1985-1986 | 1986-1987 | Total |

|---|---|---|---|---|

| NB | $3,078,000 | $3,306,000 | $502,000 | $6,886,000 |

| QC | $7,893,000 | $6,139,000 | - | $14,032,000 |

| ON | $39,996,000 | $53,328,000 | $13,332,000 | $106,656,000 |

| MB | $810,000 | $460,000 | - | $1,270,000 |

| SK | $1,451,000 | $656,000 | - | $2,107,000 |

| AB | $9,936,000 | $11,856,000 | $7,240,000 | $29,032,000 |

| BC | $22,797,000 | $30,620,000 | $31,332,000 | $84,749,000 |

| TOTAL | $85,961,000 | $106,365,000 | $52,406,000 | $244,732,000 |

In the first three years after the enactment of the Canada Health Act, almost $245 million in deductions were taken against federal health transfers to provinces; these deductions were refunded when the provinces effectively eliminated the patient charges that led to them.

Canada Health Act Compliance from 1987–2018, by Province

Following the Act's initial three-year transition period, during which refunds to provinces and territories for deductions were possible, penalties under the Act did not reoccur until fiscal year 1994–1995. See the chart later in this chapter for penalties occurring from fiscal years 1994–1995 to 2016-2017.

Federal Policy on Private Clinics

In January 1995, federal Minister of Health, the Honourable Diane Marleau, expressed concerns to her provincial and territorial colleagues about the development of two-tiered health care and the emergence of private clinics charging facility fees for medically necessary surgical services. As part of her communication with the provinces and territories, Minister Marleau announced that the provinces and territories would be given more than nine months to eliminate these user charges, but that any province that did not, would face financial penalties under the Act. Accordingly, beginning in November 1995, the deductions described below were applied to the cash contributions to Newfoundland and Labrador, Nova Scotia, Manitoba, and Alberta for non-compliance with the Federal Policy on Private Clinics.

Did you know?

Under the Canada Health Act, the term "hospital" includes more than just buildings with a big "H" on them.

Under the 1995 Federal Policy on Private Clinics, the Honourable Diane Marleau, the federal Minister of Health at the time, clarified that the definition of "hospital" set out in the Canada Health Act includes any facility that provides acute, rehabilitative, or chronic care. As such, a hospital also covers health care facilities, such as clinics.

Newfoundland and Labrador

A total of $280,430 was deducted from Newfoundland and Labrador's cash contribution due to facility fees in a private abortion clinic, before these fees were eliminated, effective January 1, 1998.

A deduction of $1,100 was taken from the March 2005 CHT payment to Newfoundland and Labrador as a result of patient charges for an MRI scan in a hospital which occurred during 2002–2003.

From March 2011 to March 2013, deductions totaling $102,249 were taken from CHT payments to Newfoundland and Labrador for extra-billing and user charges, based on charges reported by the province to Health Canada. These charges resulted from services provided by an opted-out dental surgeon who has since left the province.

Nova Scotia

Before it closed in November 2003, deductions totaling $372,135 were made to Nova Scotia's Canada Health and Social Transfer (CHST) cash contribution for its failure to cover facility charges to patients, while paying the physician fee, at a Halifax clinic. A final deduction of $5,463 was taken from the March 2005 CHT payment to Nova Scotia as a reconciliation of deductions that had already been taken for 2002–2003. A one-time positive adjustment in the amount of $8,121 was made to Nova Scotia's March 2006 CHT payment to reconcile amounts actually charged in respect of extra-billing and user charges with the penalties that had already been levied based on provincial estimates reported for fiscal 2003–2004.

The March 2007 CHT payment to Nova Scotia was reduced by $9,460 in respect of extra-billing during fiscal year 2004–2005. This amount was reported to Health Canada by the province based on the findings of an audit, concluded in 2006, of the billing practices of a Nova Scotia physician.

Quebec

In March 2017, on the basis of amounts of extra-billing and user charges reported by the Quebec Auditor General with respect to accessory fees charged in 2014–2015, the federal Minister estimated a deduction amount of $9,907,229. In light of corrective action the provincial government had already taken to eliminate accessory fees in January 2017, that amount was subsequently returned to Quebec by the Government of Canada.

In March 2018, using the amount of extra-billing and user charges reported by the Quebec Auditor General with respect to accessory fees charged in 2014–2015 as a proxy, the federal Minister estimated a deduction amount of $9,907,229. In light of the legislative changes the provincial government had already implemented to eliminate and prohibit the continuation of accessory fees in January 2017, this amount was subsequently returned to Quebec by the Government of Canada. This reimbursement pre-dated the Reimbursement Policy. Quebec's March 2017 and March 2018 deductions, which, due to reporting timelines under the Act, were taken after patient charges had already been eliminated by the provincial government, served as the inspiration for the Reimbursement Policy.

Manitoba

From November 1995 to December 1998, deductions totaling $2,055,000 were taken due to user charges anticipated by the province at surgical and ophthalmology clinics. However, during fiscal year 2001–2002, a monthly deduction (from October 2001 to March 2002, inclusively) in the amount of $50,033.50 was levied against Manitoba's CHST cash contribution on the basis of a financial statement provided by the province. The statement showed that actual amounts charged with respect to user charges for insured health services in fiscal years 1997–1998 and 1998–1999 were greater than the deductions levied on the basis of estimates. This brought total deductions levied against Manitoba to $2,355,201.

Alberta

Deductions of $3,585,000 were made, from November 1995 until June 1996, to Alberta's cash contribution in respect of facility fees charged at clinics providing surgical, ophthalmological and abortion services. On October 1, 1996, Alberta prohibited private surgical clinics from charging patients a facility fee for medically necessary services for which the physician fee was billed to the provincial health care insurance plan.

British Columbia

In the early 1990s, as a result of a dispute between the British Columbia Medical Association and the British Columbia government over compensation, several doctors opted out of the provincial health care insurance plan and began billing their patients directly. Some of these doctors billed their patients at a rate greater than the amount the patients could recover from the provincial health care insurance plan.

This higher amount constituted extra-billing under the Act. Deductions began in May 1994, relating to fiscal year 1992–1993, and continued until extra-billing by physicians was banned when changes to British Columbia's Medicare Protection Act came into effect in September 1995. In total, $2,025,000 was deducted from British Columbia's cash contribution for extra-billing that occurred in the province between 1992–1993 and 1995–1996.

In January 2003, British Columbia provided a financial statement in accordance with the Canada Health Act Extra-billing and User Charges Information Regulations indicating aggregate amounts actually charged with respect to extra-billing and user charges in private surgical clinics during fiscal year 2000–2001, totaling $4,610. Accordingly, a deduction of $4,610 was made to the March 2003 CHST cash contribution.

In 2004, British Columbia did not report to Health Canada the amounts of extra-billing and user charges actually charged during fiscal year 2001–2002. As a result of reports that British Columbia was investigating 55 cases of user charges, a $126,775 deduction was taken from British Columbia's March 2004 CHST payment, based on the amount the federal Minister estimated to have been charged during fiscal year 2001–2002.

Between 2002 and 2017, deductions totaling $1,773,183 were taken from British Columbia's Canada Health Transfer payments in light of patient charges reported by the province to Health Canada. The deduction taken to British Columbia's federal health transfers in March 2013, in respect of fiscal year 2010–2011, was estimated by the federal Minister of Health and represents the aggregate of the amounts reported to Health Canada by British Columbia and those reported publicly as the result of an audit performed by the Medical Services Commission of British Columbia. This methodology was used until fiscal year 2016–2017.

Following collaborative work with Health Canada on an audit project to determine the extent and scope of patient charges in the province, a deduction of $15,861,818 was taken in March 2018 in respect of patient charges during fiscal year 2015–2016. This deduction reflected British Columbia's private clinic audit results, patient complaints, and publicly available evidence of $4.7 million of patient charges to insured residents by enrolled physicians at the Cambie Surgery Centre.

Did you know?

Since the passage of the Act, from April 1984 to March 2023, deductions totaling $197,467,235 have been taken from transfer payments in respect of the extra-billing and user charges provisions of the Act. This amount excludes deductions totaling $244,732,000 that were made between 1984 and 1987, and subsequently refunded to the provinces when extra-billing and user charges were eliminated.

| NL | PE | NS | NB | QC | ON | MB | SK | AB | BC | YT | NT | NU | Total | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1994-1995 | - | - | - | - | - | - | - | - | - | $1,982,000 | - | - | - | $1,982,000 |

| 1995-1996 | $46,000 | - | $32,000 | - | - | - | $269,000 | - | $2,319,000 | $43,000 | - | - | - | $2,709,000 |

| 1996-1997 | $96,000 | - | $72,000 | - | - | - | $588,000 | - | $1,266,000 | - | - | - | - | $2,022,000 |

| 1997-1998 | $128,000 | - | $57,000 | - | - | - | $586,000 | - | - | - | - | - | - | $771,000 |

| 1998-1999 | $53,000 | - | $38,950 | - | - | - | $612,000 | - | - | - | - | - | - | $703,950 |

| 1999-2000 | ($42,570) | - | $61,110 | - | - | - | - | - | - | - | - | - | - | $18,540 |

| 2000-2001 | - | - | $57,804 | - | - | - | - | - | - | - | - | - | - | $57,804 |

| 2001-2002 | - | - | $35,100 | - | - | - | $300,201 | - | - | - | - | - | - | $335,301 |

| 2002-2003 | - | - | $11,052 | - | - | - | - | - | - | $4,610 | - | - | - | $15,662 |

| 2003-2004 | - | - | $7,119 | - | - | - | - | - | - | $126,775 | - | - | - | $133,894 |

| 2004-2005 | $1,100 | - | $5,463 | - | - | - | - | - | - | $72,464 | - | - | - | $79,027 |

| 2005-2006 | - | - | ($8,121) | - | - | - | - | - | - | $29,019 | - | - | - | $20,898 |

| 2006-2007 | - | - | $9,460 | - | - | - | - | - | - | $114,850 | - | - | - | $124,310 |

| 2007-2008 | - | - | - | - | - | - | - | - | - | $42,113 | - | - | - | $42,113 |

| 2008-2009 | - | - | - | - | - | - | - | - | - | $66,195 | - | - | - | $66,195 |

| 2009-2010 | - | - | - | - | - | - | - | - | - | $73,925 | - | - | - | $73,925 |

| 2010-2011 | $3,577 | - | - | - | - | - | - | - | - | $75,136 | - | - | - | $78,713 |

| 2011-2012 | $58,679 | - | - | - | - | - | - | - | - | $33,219 | - | - | - | $91,898 |

| 2012-2013 | $50,758 | - | - | - | - | - | - | - | - | $280,019 | - | - | - | $330,777 |

| 2013-2014 | ($10,765) | - | - | - | - | - | - | - | - | $224,568 | - | - | - | $213,803 |

| 2014-2015 | - | - | - | - | - | - | - | - | - | $241,637 | - | - | - | $241,637 |

| 2015-2016 | - | - | - | - | - | - | - | - | - | $204,145 | - | - | - | $204,145 |

| 2016-2017 | - | - | - | - | $9,907,229Footnote 1 | - | - | - | - | $184,508 | - | - | - | $10,091,737 |

| 2017-2018 | - | - | - | - | $9,907,229Footnote 1 | - | - | - | - | $15,861,818 | - | - | - | $25,769,047 |

| TOTAL: | $383,779 | - | $378,937 | - | $19,814,4581 | - | $2,355,201 | - | $3,798,183 | $19,660,001 | - | - | - | 46,390,559 |

|

||||||||||||||

Understanding This Chart

The first deductions under the Act were taken during the first three years after the Act's passage and were subsequently refunded. They are described earlier in this chapter and listed in a chart. There were no deductions taken between fiscal year 1987–1988 and 1993–1994.

To date, most deductions have been based on statements of actual extra-billing and user charges, meaning they are made two years after the extra-billing and user charges occurred (for example, deductions taken in fiscal year 2016–2017 would be in respect of patient charges levied in 2014–2015).

In instances where provinces and territories estimate anticipated amounts of extra-billing and user charges for the upcoming year, a deduction was taken in respect of those charges in the fiscal year for which they are estimated.

In addition to forming the basis for most deductions under the Act, the statements of actual extra-billing and user charges provide an opportunity to reconcile any estimated charges with those that actually occurred. These reconciliations form the basis for further modifications to provincial and territorial cash transfers.

Canada Health Act Compliance from 2018−Present, by Province

Reimbursement Policy and Diagnostic Services Policy

As described earlier, two policies were announced in the Petitpas Taylor letter: the Canada Health Act Reimbursement Policy and the Diagnostic Services Policy.

The Reimbursement Policy was created to provide a positive incentive for provinces and territories to come into compliance, should they be subject to mandatory penalties as a result of patient charges for insured health services. Since April 1, 2018, the federal Minister of Health has had the discretion to provide a reimbursement if the province or territory eliminates those charges, and the underlying circumstances which led to the charges, within a specified timeframe. The first deductions eligible for reimbursement under the policy were those taken in March 2018 and since then $84,938,117 in deductions have been reimbursed to provinces as a result of their efforts to eliminate patient charges and the circumstances that led to them.

The Diagnostic Services Policy, which took effect on April 1, 2020, formalized the longstanding federal position that patient charges for medically necessary diagnostic services are considered extra-billing or user charges under the Act. The policy clarifies that these services are insured, regardless of the venue in which they are delivered, and evidence of patient charges will result in mandatory dollar-for-dollar deductions from provincial and territorial CHT payments.

The first deductions taken under the Diagnostic Services Policy were levied in March 2023. However, under the Canada Health Act Reimbursement Policy, provinces and territories may be reimbursed if they eliminate the patient charges in question and rectify the circumstances that led to them, within two years of the date of the deduction.

Newfoundland and Labrador

In March 2019, a deduction of $1,349 was taken from CHT payments to Newfoundland and Labrador for extra-billing and user charges, based on patient charges for insured health services at a private ophthalmological clinic that occurred in 2016–2017, reported by the province to Health Canada. Similarly, a deduction of $70,819 was taken in March 2020, $4,521 in March 2021, and $1,723 in March 2022 in respect of charges in this clinic during 2017–2018, 2018-2019, and 2019-2020 respectively.

After its March 2019 deduction, Newfoundland and Labrador consulted with Health Canada on a Reimbursement Action Plan to eliminate patient charges. Given the province successfully carried out that plan, and eliminated these patient charges, the province qualified for full reimbursement of its March 2019 deduction as well as for immediate and full reimbursements of its March 2020, 2021, and 2022 deductions.

Nova Scotia

In March 2023, Nova Scotia was subject to a deduction of $1,277,659 under the Diagnostic Services Policy, based on estimates made by Health Canada. The deduction was a result of patient charges for medically necessary diagnostic services at a private imaging clinic in Halifax that occurred in 2020-2021.

New Brunswick

In March 2020, on the basis of evidence of patient charges for access to abortion services during 2017–2018, a deduction of $140,216 was taken to New Brunswick's CHT payments. A further $64,850 was deducted from the province's CHT payment in March 2021, March 2022, and March 2023 for patient charges levied during 2018-2019, 2019-2020, and 2020-2021, respectively. The 2021, 2022, and 2023 deductions were estimated based on patient charges reported by Clinic 554 and data published by the Canadian Institute for Health Information. As long as New Brunswick refuses to cover insured abortion services outside hospitals, and patients face charges in the clinic setting, the province will continue to be subject to mandatory CHT deductions.

In March 2023, New Brunswick was subject to a deduction of $1,277,659 under the Diagnostic Services Policy, based on estimates made by Health Canada as a result of patient charges for medically necessary diagnostic services that occurred in 2020-2021.

Quebec

A deduction of $8,256,024 was taken to Quebec's March 2019 federal health transfer, reflecting patient charges which had occurred prior to the corrective legislative action taken by Quebec and was immediately reimbursed. This reimbursement was the first made under the Reimbursement Policy.

In March 2023, Quebec was subject to a deduction of $41,867,224 under the Diagnostic Services Policy, based on estimates made by Health Canada. The deduction was a result of patient charges for medically necessary diagnostic services that occurred in 2020-2021.

Ontario

Ontario was subject to deductions for patient charges for insured abortion services in March 2021 in the amount of $13,905 for charges that occurred in 2018-2019; March 2022 in the amount of $6,560 for charges that occurred in 2019-2020; and, March 2023 in the amount of $32,800 for charges that occurred in 2020-2021. The deductions represent overhead costs charged to patients seeking abortion services at clinics that do not receive funding under Ontario's Independent Health Facilities Act.

Manitoba

In March 2023, Manitoba was subject to a deduction of $353,827 under the Diagnostic Services Policy, based on estimates made by Health Canada. The deduction was a result of patient charges for medically necessary diagnostic services that occurred in 2020-2021.

Saskatchewan

In March 2023, Saskatchewan was subject to a deduction of $742,447 under the Diagnostic Services Policy, based on Health Canada's estimate of patient charges, which was developed using information provided by the province. The deduction was a result of patient charges for medically necessary diagnostic services that occurred in 2020-2021 as a result of Saskatchewan's Patient Choice Medical Imaging Act, which authorizes private MRI and CT facilities in the province to accept payment directly from patients in exchange for medically necessary imaging services.

Alberta

In March 2023, Alberta was subject to a deduction of $13,781,152 under the Diagnostic Services Policy, based on estimates made by Health Canada. The deduction was a result of patient charges for medically necessary diagnostic services that occurred in 2020-2021.

British Columbia

A similar methodology to that used to estimate British Columbia's March 2018 deduction was used to calculate the province's Canada Health Transfer deductions in March 2019 ($16,177,259), March 2020 ($16,753,833), March 2021 ($13,949,979), March 2022 ($13,275,823), and March 2023 ($5,945,221).