Five-Year Evaluation of the 2006 Policy on Internal Audit

Acknowledgements

This evaluation was undertaken by Ference Weicker & Co. on behalf of the Office of the Comptroller General. This report has been edited for publication in accordance with the publication and communications quality assurance processes within the Treasury Board of Canada Secretariat.

Table of Contents

- Executive Summary

- Recommendations

- I. Methodology

- II. Description of the 2006 Policy on Internal Audit

- III. Evaluation Findings and Conclusions

- IV. Key Conclusions and Recommendations

- Recommendations

Executive Summary

Purpose of Evaluation

This evaluation was undertaken as per the requirements of section 5.8.6 of the Policy on Internal Audit and as part of the Secretariat’s Five-Year Evaluation Plan. The objective of the evaluation was to assess the relevance and performance of the Policy on Internal Audit. The evaluation covers the period from April 1, 2006, to March 31, 2010. The scope of the evaluation includes the 2006 Policy on Internal Audit and adjustments made to this Policy as of July 1, 2009.

Findings and Conclusions

Overall, the 2006 Policy on Internal Audit has achieved significant impacts and there exists widespread satisfaction with the Policy. The key findings and conclusions of this evaluation are outlined as follows.

- There is a continued need for the Policy.

Although there have not recently been any high-profile breakdowns of control in the federal government, there is still a need for the Policy. The importance of a risk-based internal audit function has increased as a result of the Federal Accountability Act and the new role of deputy heads as the accounting officers of their respective organizations.

In addition, by addressing a number of weaknesses, the Policy has resulted in the following:

- Independence of departmental audit committees (DACs);

- Independence of internal audit staff from line management;

- Sufficient focus on assurance services; and

- Consistency in internal audit capacity, skills and practices.

- The Policy has contributed to increasing the independence of the internal audit function from line management. The Policy requires DACs to have a majority of external members, as well as a chief audit executive (CAE) who reports directly to the deputy head of a large department or agency (LDA).

Prior to the Policy, DACs consisted primarily of senior managers from the relevant department. As a result of the Policy, DACs now have external members who are selected for their extensive experience in the public and private sectors and whose goal is to provide objective, independent observations to DACs. In addition, the direct reporting of CAEs to deputy heads and the direct access that CAEs have to the DACs have increased the independence of the internal audit function from line management.

- The implementation of the Policy, particularly the establishment of DACs that have external members, has contributed to improving risk management, governance, internal control and stewardship of resources in federal government departments and agencies.

The key factors that have helped achieve these intended outcomes include the following:

- Strong deputy head support for Policy implementation;

- The establishment of a more professional internal audit function within departments;

- Improved oversight of the internal audit function by a qualified CAE and DAC members who have audit expertise; and

- More timely implementation of internal audit recommendations, leading to improved management and business practices.

The Policy’s contribution is important because the Policy is complementary to a number of other federal government policies and initiatives that focus directly on areas such as internal control and risk management.

- Deputy heads of LDAs have confidence in the assurance provided by the internal audit function and the advice provided by their DAC on risk management, control and governance processes.

Given the depth and breadth of experience held by DAC members, many deputy heads stated that they use the DAC as a sounding board and a strategic resource for strengthening the overall institution, rather than just the internal audit function.

- Implementation of the Policy has significantly increased the effectiveness of the internal audit function across government.

The establishment of DACs that have external members has contributed to the effectiveness of the internal audit function within departments. Other contributing factors include the following:

- The establishment of a CAE position reporting directly to the deputy head;

- Strong deputy head support for Policy implementation;

- Incremental funding for departmental internal audit activities;

- Implementation of Government of Canada audit standards; and

- Horizontal audits of small department and agencies (SDAs) conducted by the Office of the Comptroller General (OCG).

The proportion of LDAs that obtained an acceptable or strong Management Accountability Framework (MAF) rating for their internal audit function more than doubled, from 42 per cent in 2005–06 to 85 per cent in 2009–10.

- Implementation of the Policy has resulted in a considerable increase in management action on internal audit report recommendations due primarily to a concerted focus by DACs and CAEs on following up on the implementation of management action plans.

Since the Policy was introduced, there has been more formal tracking of the implementation of internal audit recommendations by CAEs and internal audit staff. Although difficult to quantify, some benefits that have resulted from the implementation of management action plans include averted risks, improved operational efficiency, and improved risk management and cost savings.

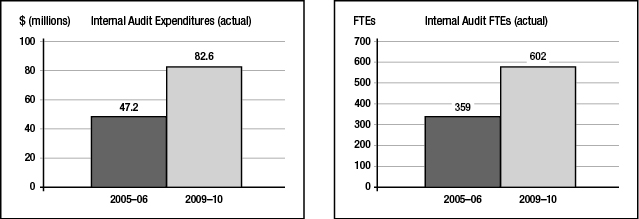

- The Policy has contributed to increasing the capacity of the internal audit function across government through the approval of $40 million annually in accompanying funding for departmental and OCG internal audit activities.

With the removal of two budgeted expenditures that have not yet been incurred ($9.7 million per year for increased departmental internal audit salaries projected to occur from reconfiguration of the internal audit community, and $1.3 million per year for technological support), the amount approved on an ongoing basis for other departmental and OCG audit activities is approximately $29.4 million per year. This funding has contributed to an increase of 75 per cent in departmental internal audit expenditures, from $47.2 million in 2005–06 to $82.6 million in 2009–10, in the 41 LDAs that provided financial information. The number of staff devoted to the internal audit function, including the administrative staff who support the DACs and CAEs, has increased by 68 per cent, from 359 FTEsSee footnote 1 in 2005–06 to 602 FTEs in 2009–10, in the LDAs surveyed.

- The Policy has contributed to audit coverage appropriate to the level of risk across government through the provision of accompanying funding to bolster departmental internal audit services, horizontal audits of LDAs and SDAs conducted by the OCG, and the preparation of risk-based audit plans that focus on high risk areas.

There are drawbacks to the current criteria for determining whether an organization should be classified as an LDA or an SDA (i.e., 500 FTEs and $300 million in annual expenditures). Some of these drawbacks include the following:

- The criteria do not reflect the characteristics of micro-agencies, which are very small (they account for less than 0.1 per cent of federal government expenditures) and have difficulty meeting the current reporting and other requirements for SDAs.

- The criteria do not take into account the level of risk within an organization in determining whether the organization should be classified as an LDA or SDA.

- The criteria do not align with the criteria used in other Treasury Board policies to separate federal government departments and agencies into large and small organizations.

- The Policy has increased the professionalism of the internal audit function by adding rigour to the internal audit standards and practices used by the federal government and by ensuring a more certified internal audit function across government.

The Policy has led to a stronger emphasis on meeting Government of Canada internal audit standards. Training expenditures have increased threefold, from $0.7 million in 2005–06 to $2.1 million in 2009–10, in the 23 LDAs that provided information on their training expenditures. The number of CAEs who have a Certified Internal Auditor (CIA) designation has increased from 12 in 2008 to 19 in 2010; another 11 CAEs are in the process of obtaining a CIA, which, when completed, will mean that approximately 62 per cent of CAEs have a CIA designation. The number of internal audit staff in the federal government who have a CIA designation has almost doubled, from 57 in 2008 to 105 in 2010.

- The Policy has been implemented as intended, but some aspects have not been implemented fully.

Some aspects of the Policy that have not been fully implemented are:

- The reconfiguration of the internal audit community (including the reclassification of internal audit staff);

- Practice inspections and external assessments; and

- Annual overview reporting and technological support for standardizing internal audit work processes.

As previously indicated, the $35.4 million increase in internal audit expenditures from 2005–06 to 2009–10 in the 41 LDAs surveyed is greater than the $24 million provided annually under the Policy to these LDAs for their incremental internal audit expenses. Approximately 71 per cent of the LDAs surveyed spent more on their internal audit function than the incremental funding provided to them; the remaining 29 per cent spent less than the incremental funding they received in 2009–10.

The 2009 changes to the Policy were appropriate and have facilitated implementation of the Policy. The changes clarified a number of areas that have been the subject of discussion since the Policy came into force in 2006 (e.g., DAC advisory role, removal of holistic opinion, Minister’s involvement with DAC members) without changing the principles of the Policy. Additional clarification is needed on how to implement the recent guidelines on annual overview reporting.

- The activities carried out by the OCG to help organizations implement the Policy have been appropriate for the effective implementation of the Policy, but some have not been very timely; however, recent improvements have been made.

The three OCG activities rated as most useful by CAEs and internal audit staff are DAC training and networking, guidance on internal audit standards and practices, and guidance provided to CAEs. The three activities rated as least useful by both CAEs and internal audit staff are HR strategies and staffing, omnibus supply arrangements (PASS), and horizontal audits of LDAs.

- The MAF rating system is the key method employed by the OCG to monitor the effectiveness and impacts of the activities related to the Policy. Respondents indicated that this system is a somewhat useful means of assessing the performance of the internal audit function within LDAs.

On average, LDA deputy heads, CAEs and internal audit staff stated that MAF ratings are between “somewhat useful” and “useful” as a measure of the performance of their departmental internal audit function. Some respondents indicated that MAF criteria have improved recently. Several respondents indicated that MAF requirements impose a heavy reporting burden, particularly on small LDAs.

- Policy implementation resource levels are appropriate due to the approval of ongoing accompanying funding to implement the Policy.

This accompanying funding has enabled federal government departments and agencies to restore the capacity of their internal audit function, which was reduced in the 1990s. Based on a comparison with other jurisdictions, the ratio between the number of internal auditors and government expenditures in the Government of Canada is similar to the ratios in the governments of the United Kingdom and Ontario.

- The Policy has been implemented efficiently and economically, but there appear to be opportunities to enhance the Policy and its implementation.

Further opportunities to enhance the Policy and its implementation are outlined as follows.

- Streamline the DAC appointment process and reduce its unpredictability.

It is necessary to reduce the excessive delays and the unpredictability of the process for obtaining ministerial approval of an external DAC member once a prospective member is selected and agreed upon by the Comptroller General and the Deputy Head. The DAC appointment process must be streamlined because a number of current appointments to DACs will be expiring soon. The renewal of existing DAC members and the appointment of new members need to be carried out quickly to avoid any vacancies in DACs, which would limit the contributions that DAC members are making. In addition, the unpredictability of the process needs to be minimized so that the most qualified DAC candidates are approved and highly qualified DAC candidates are not dissuaded from seeking a DAC membership. One option for streamlining the process and reducing its unpredictability is to delegate Treasury Board ministerial approval to the Secretary of the Treasury Board.

- Resolve issues with the current classification of internal auditors in the federal government and ensure that departments are able to staff their internal audit function with a broad range of skills.

One of the intended outcomes of the Policy is to increase the capacity and strengthen the professionalism of the internal audit function within departments. The evaluation provides evidence that the Policy indeed led to the development of a more professional internal audit function within departments as a result of adopting the IIA Professional Practices Framework and encouraging auditors to obtain a professional certification (e.g., a CIA designation). Training expenditures and the number of auditors who have CIA designations have both increased.

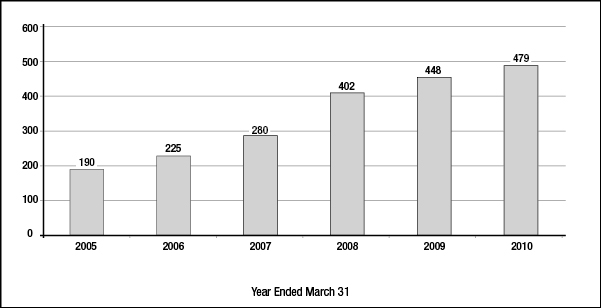

To meet the requirements of the Policy on Internal Audit and to address the decrease in the number of internal audit staff that occurred in the 1990s, more internal auditors were needed. The number of internal audit staff in the core public service was 190 in 2005 compared with 479 in 2010. This increase in demand for internal auditors has made it more difficult to attract sufficient internal audit staff. The evaluation also found that CAEs and internal audit staff believe that there is a need for a different classification for internal auditors in order to increase the professionalism of the internal audit function. In particular, CAEs and internal audit staff indicated that educational requirements and compensation levels within the AS category are factors contributing to the difficulties in attracting and retaining qualified internal audit staff.

The evaluation found that there is a shortage of qualified and experienced internal auditors in the federal government and that attracting and retaining qualified internal audit staff remains a challenge. Evidence indicated that the lack of qualified, experienced auditors negatively affected audit coverage and the quality of the work performed. To increase audit coverage and quality, the issues related to attraction and retention need to be resolved.

When addressing the issues related to attracting and retaining internal auditors, the solution must be consistent with the policy direction on professionalizing the internal audit community. In addition, the solution must take into account the concerns expressed by internal auditors and CAEs about the differences in compensation and educational requirements for the various classifications used for the internal audit function. Finally, the solution must include an HR plan that reflects the need for individuals who have a broad range of skills and experience in order to create the balance required for an effective internal audit group. HR planning is required to ensure a common understanding of the duties of the internal audit function and the core competencies needed to carry them out. This planning will support consistent work definitions for internal auditors and enable departments to better balance their HR plans to ensure that their internal audit staff have the desired combination of skills. Consistency in HR planning, work definitions and compensation for auditors will help resolve the recruitment and retention challenges noted in the evaluation.

- Investigate alternatives to the current method of dividing federal government departments and agencies into LDAs and SDAs.

It is necessary to determine whether there are alternatives or supplemental approaches that would better balance Policy requirements with the level of risk and the capabilities of different sizes and types of federal government departments and agencies. Although not an exhaustive list, some options proposed by respondents that appear worthy of investigation include the following:

- Create a separate category for micro-agencies that has reduced requirements for participating in OCG horizontal audits to reflect the fact that most SDAs are very small (42 of the 50 SDAs account for only about one quarter of all SDA expenditures and approximately 0.1 per cent of all federal government expenditures). However, it is also necessary to take into consideration that even small organizations can pose a high level of risk to the federal government (e.g., negative press coverage).

- Add the level of risk to the two existing criteria for determining whether a federal government department or agency should be considered an LDA or an SDA (i.e., $300 million in annual expenditures and 500 FTEs).

- Align the criteria used by the Policy on Internal Audit with those used by other Treasury Board policies (e.g., Policy on Evaluation).

- Increase the number of small LDAs that share a CAE and/or DAC, particularly where two LDAs have similar mandates.

- Encourage some LDAs to share their CAEs and DACs with the SDAs with which they are affiliated and where there is no potential for conflict of interest.

- Limit the number of former public servants who are external members of DACs.

The evaluation data indicated concerns related to the proportion of former public servants who serve on DACs, particularly that having too many former public servants on DACs may reduce the potential for fresh and external perspectives. It is ideal for a DAC to have external members who have a mix of private and public sector skills. The most appropriate composition for a typical DAC that has three external members is as follows:

- One DAC member who has public sector skills;

- One DAC member who has skills in financial management, accounting or auditing; and

- One DAC member who has private sector experience in a field related to the operations of the department.

Regardless of whether a DAC member is from the public or private sector, it is also important to ensure that the required skill sets and competencies are covered when selecting the most appropriate members for a particular DAC. It is preferable to have a maximum of one former public servant and a minimum of two private sector representatives serving as external members on each DAC.

- Provide guidance on implementing annual overview requirements.

Since the Policy was introduced, expectations have declined regarding the scope and nature of assurance that should be provided to the Deputy Head by the departmental internal audit function. Expectations have changed from the provision of a holistic opinion (2006 Policy) to an annual assurance report (2009 Policy) and most recently to an annual overview report. The OCG should investigate ways to implement annual overview requirements, and additional guidance should be provided to LDAs in this respect.

Recommendations

Because of the many positive effects of the Policy on Internal Audit and the widespread satisfaction with it, there is no impetus to make significant changes to the Policy. The following recommendations deal primarily with modifications that could be made to further increase the Policy’s effectiveness.

It is recommended that the OCG:

- Investigate ways to streamline the DAC appointment process and reduce its unpredictability in order to attract and retain qualified DAC members.

- Resolve issues regarding the current classification of internal auditors in the federal government and ensure that departments are able to acquire internal audit staff who have a broad range of skills.

- Examine alternatives to the current method of dividing federal government departments and agencies into LDAs and SDAs.

- Limit the number of former public servants who are external members of DACs to ensure that DACs are composed of members who have a broad range of skills.

- Investigate how annual overview requirements can be implemented in order to provide guidance to LDAs.

I. Methodology

This section describes the purpose and methodology used to perform the evaluation.

A. Purpose of Evaluation

This evaluation was undertaken as per the requirements of section 5.8.6 of the Policy on Internal Audit and as part of the Secretariat’s Five-Year Evaluation Plan. The objective of the evaluation was to assess the relevance and performance of the Policy on Internal Audit. The 2006 Policy on Internal Audit specifically states that an evaluation of the Policy is to occur and a report is to be provided to the Treasury Board by April 1, 2011. The evaluation covers the period from April 1, 2006, to March 31, 2010. The scope of the evaluation consists of the 2006 Policy on Internal Audit and adjustments made to it as of July 1, 2009.

B. Evaluation Methodology

As stipulated in the Standard on Evaluation for the Government of Canada, evaluators considered the risks associated with the Policy on Internal Audit. To address these risks, the data for the evaluation was collected in two phases. In the first phase, evaluators collected data through a review of documents and files, key informant interviews, a cost analysis, and surveys. Evaluators then analyzed the quality of the data gathered from the first phase (e.g., response rate, recall factor of respondents, key issues) to design the methods to be used to collect data in the second phase, namely, the case studies and focus groups. This strategy enabled the evaluators to adjust the data collection strategies to more effectively cover all aspects of the Policy and focus on the key issues.

As a result of the preliminary evaluation carried out in the first phase, the evaluation team identified the need to further explore the importance of the DACs, given their innovative and major role under the Policy. In addition, the preliminary evaluation identified the need to explore in more detail the effects of the differences in CAE reporting relationships, as well as the issues related to obtaining a different classification for internal auditors.

The methods used to collect data for the evaluation of the 2006 Policy on Internal Audit are outlined as follows.

1. Detailed Document and File Review

This review consisted of examining the available documents in detail, including the following:

- The Policy and its guidelines;

- Previous policies, evaluations and reviews of the current and previous policies;

- CAE and DAC reports;

- Reference and other materials produced by the OCG to facilitate implementation of the Policy;

- Studies conducted by the OCG and other federal government organizations; and

- Cost information compiled by the OCG on internal audit expenditures in the federal government.

2. Key Informant Interviews

A total of 25 key informant interviews were conducted with individuals involved in designing and implementing the Policy, and with experts in the field of internal audit, specifically

- Current and previous Comptrollers General of Canada;

- Current and previous staff of the OCG who were involved in Policy design and implementation;

- OCG audit staff involved in horizontal departmental audits;

- Senior managers at the Treasury Board of Canada Secretariat;

- Representatives of internal audit associations (e.g., the IIA); and

- Academics and experts in the field of internal audit.

3. Survey of Internal Audit Stakeholders

The following types of internal audit stakeholders were surveyed.

-

Deputy heads: Evaluators interviewed 54 deputy heads, including respondents from both SDAs and LDAs.

- Deputy heads of LDAs—Of the 46 federal government departments and agencies classified as LDAs under the Policy, 29 deputy heads (about two thirds of all deputy heads) of these organizations were engaged.

- Deputy heads of agents of Parliament and the Public Service Commission of Canada—The Policy states that, although the principles of the Policy as it applies to LDAs will apply to the seven agents of Parliament and the Public Service Commission of Canada, the deputy heads of these organizations may authorize any departures from specific Policy requirements as they deem appropriate in light of the governance arrangements, statutory mandate and risk profile of the organization. To examine this unique group, evaluators conducted five interviews with deputy heads of agents of Parliament and the Public Service Commission of Canada. For the purposes of this evaluation, evaluators combined the responses obtained from the deputy heads of agents of Parliament and the Public Service Commission of Canada with those obtained from deputy heads of LDAs because all of these organizations must comply with similar requirements under the Policy.

- Deputy heads of SDAs—20 deputy heads of SDAs were interviewed (40 per cent of the total number of SDA deputy heads). The 50 SDAs in the federal government are small organizations that collectively account for less than one per cent of total federal government expenditures.

- CAEs—All CAEs in LDAs, agents of Parliament and the Public Service Commission of Canada were surveyed using an online questionnaire. In addition, evaluators also placed follow-up telephone calls in some cases to clarify responses to the questionnaire and to increase the response rate. Responses were received from 48 CAEs. Taking into account vacancies and situations where one CAE serves two LDAs, there are 52 CAEs in total. Therefore, the response rate was 92 per cent.

- DAC members—All external DAC members were surveyed using an online questionnaire. When necessary, follow-up telephone calls were made in order to clarify responses to the questionnaire and to increase the response rate. Evaluators obtained responses from a total of 97 DAC members, which corresponds to a response rate of 78 per cent.

- Chief financial officers (CFOs)—All CFOs in LDAs, SDAs and agents of Parliament were surveyed online, and follow-up telephone calls were placed to increase the response rate. Responses were obtained from 34 CFOs in LDAs and agents of Parliament, which corresponds to a response rate of 63 per cent. Evaluators obtained responses from 25 CFOs in SDAs, which corresponds to a response rate of 50 per cent.

- Internal audit staff of federal government departments and agencies—Internal auditors were surveyed using an online questionnaire, and follow-up telephone calls were placed to increase the response rate. Although evaluators initially used the membership list from the Ottawa chapter of the IIA to determine the internal auditors to be surveyed, they found the list to be out of date and incomplete. The Government of Canada employee directory was therefore used to develop a list of internal auditors for survey purposes. In addition, evaluators requested that all CAEs ask all of their internal audit staff to complete the online survey. Evaluators obtained a total of 209 completed surveys from departmental internal audit staff, which corresponds to a response rate of approximately 43 per cent.

- Assistant deputy ministers (ADMs)—Evaluators conducted an online survey and follow-up telephone calls were place to a sample of ADMs. To determine which ADMs were to be surveyed, evaluators requested that all CAEs provide the names of ADMs who were subject to an internal audit completed in 2009–10. A total of 133 names were provided and a sample of 75 were surveyed, yielding responses from 54 ADMs. That number represents 41 per cent of the ADMs on the list.

4. Cost Analysis of Internal Audit Expenditures

To obtain information on the costs incurred in Policy implementation, all CAEs were asked to provide information on internal audit expenditures and the number of FTEs devoted to internal audit in 2005–06 and 2009–10, as well as their estimated internal audit expenditures. Evaluators also requested a breakdown of internal audit expenditures in order to determine what was spent on internal audit staff salaries and benefits, professional services, training, and DAC costs.

5. Case Studies

Evaluators conducted six case studies. The topics of the case studies were selected after a large portion of the key informant interviews and stakeholder surveys were completed to obtain a better understanding of the key issues that should be investigated. The topics for the six case studies are outlined as follows.

- Case studies 1, 2 and 3: The purpose of these studies was to determine whether there were any differences in contributions made by DACs, based on who was chair of the DAC. The following three alternative DAC models were the subject of a separate case study:

- The deputy head is the DAC chair.

- An external member is the DAC chair.

- The deputy head does not attend DAC meetings but is briefed on them.

- Case study 4: This study examined the issues related to obtaining a different classification for internal auditors. Funding was provided to the OCG to help reconfigure the internal audit community (including a separate classification for internal auditors in the federal government), but a separate classification has not yet been created. Based on the pretest results, a different classification was considered to be an important part of enhancing the professionalism of the internal audit community. The purpose of the case study was to examine the constraints that have prevented the completion of the proposed reconfiguration of the internal audit community and the likely success of current efforts to accomplish that goal.

- Case studies 5 and 6: The purpose of these two studies was to analyze different CAE reporting relationships. According to MAF data on CAE reporting relationships, 27 of 45 CAEs report "solely and exclusively to the deputy head," and 18 of 45 CAEs report "solely and substantively to the deputy head." Evaluators conducted two case studies to examine the effects of different CAE reporting relationships, one where CAE reports "solely and exclusively to the deputy head" and one where the CAE reports "solely and substantively to the deputy head."

6. Focus Groups

Evaluators conducted four focus groups, prepared guides for each of the groups, and submitted them to the Evaluation Working Group for feedback. Based on the feedback obtained, evaluators finalized the guides and sent them to participants a few days prior to the session. The four focus groups are described as follows.

- Deputy head focus group: The purpose of this group was to obtain elaboration on issues identified during the survey of deputy heads and to address the case study topics. Four deputy heads participated in the focus group.

- CAE focus group: The purpose of this group was to obtain elaboration on issues identified during the survey of CAEs and to address the case study topics. The criteria used to select the focus group participants included the CAE reporting relationship (i.e., "strong" and "acceptable" departmental MAF ratings); DAC chair (i.e., external chair, deputy head chair); sector (e.g., economic operations, government operations); and size of organization (FTEs). Based on these criteria, 18 CAEs were initially selected and invited to participate in the focus group. Several CAEs were unable to attend because of other activities, and a few declined at the last minute. Six CAEs attended the focus group. The CAEs who attended were representative of the CAE population, as they were from different types and sizes of departments, and had different reporting relationships and different DAC chairs.

- External DAC member focus group: The purpose of this group was to obtain elaboration on issues identified during the survey of external DAC members and to address the case study topics. The criteria employed to select the focus group participants included the CAE reporting relationship (i.e., "strong" and "acceptable" departmental MAF ratings); DAC chair (i.e., external chair, DH chair); sector (e.g., economic operations, government operations); and size of organization (FTEs). A total of 14 DAC members were invited to attend the focus group. Five members attended either in person or by telephone. The DAC members who attended were representative of the DAC population, as they were from different types and sizes of departments, and had different CAE reporting relationships and different DAC chairs.

- Departmental internal audit staff focus group: The purpose of this group was to obtain elaboration on issues identified during the survey of internal audit staff and to address the case study topics. The criteria employed to select the focus group participants included years of internal audit experience; CAE reporting relationship (i.e., "strong" and "acceptable" departmental MAF ratings); DAC chair (i.e., external chair, DH chair); sector (e.g., economic operations, government operations); and size of organization (FTEs). A total of 16 internal audit staff were invited to the focus group, eight of whom attended. The staff who attended were representative of the internal audit community.

7. Review of Similar Policies in Other Jurisdictions

Evaluators conducted a comparative analysis of the Policy with similar policies in other jurisdictions. The other jurisdictions investigated were the United Kingdom, Australia and Ontario. In addition, extensive Internet and library research was conducted to obtain available information on the internal audit policies and practices in these jurisdictions. Evaluators then conducted telephone interviews with representatives of federal government internal audit departments and branches in these jurisdictions.

C. Limitations

The key limitations are outlined as follows.

- Because of the small number of informants interviewed, a detailed breakdown of findings by subgroup could not be completed.

- Because the Policy on Internal Audit is complementary to a number of other policies and initiatives that focus directly on areas such as internal control and risk management (e.g., Policy on Internal Control, Risk Management Policy, Federal Accountability Act and Policy Suite Renewal), it is difficult to attribute the impact of the Policy on Internal Audit because its intended outcomes are shared with complementary programs.

- Because some departments are at various stages of implementing the Policy on Internal Audit, it is difficult to generalize findings across departments.

- Given that only a small proportion of the individuals invited chose to attend the focus groups, the observations of the focus groups cannot be generalized for the entire population.

D. Report Outline

The next section provides a brief description of the 2006 Policy on Internal Audit, including its objectives and intended outcomes. Section III provides the evaluation findings and conclusions for each evaluation issue. The last section summarizes the key evaluation conclusions and provides recommendations to enhance the Policy’s effectiveness.

II. Description of the 2006 Policy on Internal Audit

This section provides a brief profile of the 2006 Policy on Internal Audit.

A. Rationale

Many factors internal and external to the federal government influenced the development of the 2006 Policy on Internal Audit. The Auditor General of Canada played an important diagnostic and influential role by auditing the federal government internal audit function in 1994 and 2004. In the 2004 November Report of the Auditor General of Canada, Chapter 1, “Internal Audit in Departments and Agencies,” the Auditor General noted that considerable work remained to strengthen the internal audit function in the Government of Canada. The Auditor General also mentioned that, despite additional funding for internal audit in the past four years, the same problems have remained for more than a decade. Some of the other internal and external factors that influenced the development of the 2006 Policy on Internal Audit include the following:

- Public scrutiny increased as a result of the Enron, Sarbanes-Oxley and Gomery scandals;

- The Public Accounts Committee indicated that internal audit lacked sufficient independence from line management.

- Audit committees were not independent.

- Deputy heads were not consistently provided with the independent assurance they need to support them in discharging their responsibilities.

- Internal audit was not focused on assurance; its focus on reviews and consulting presented a potential conflict of interest.

- There was a lack of consistency in internal audit capacity, skills and practice throughout the federal environment.

- Internal auditors were not mobile within government.

- The government was unable to articulate how well its control framework was working within an entity or across government.

- The audit environment became more complex and driven by information technology.

- The provisions of the Access to Information Act weakened the audit regime.

B. Policy Description

In October 2005, the Comptroller General submitted to the Treasury Board a proposed new Policy on Internal Audit. The Policy was approved and took effect on April 1, 2006, along with three related directives. Implementation occurred in stages, between the effective date and April 1, 2009. The new Policy addressed the following:

- The government would sustain a strong, credible internal audit regime that holds the confidence of the government and contributes directly to effective risk management, sound resource stewardship and good governance.

- The government would ensure the independence of the internal audit function from line management by requiring DACs to have a majority of external members recruited from outside the federal public administration and by requiring CAEs to report directly to the deputy head.

- CAEs would provide deputy heads with annual opinions on the adequacy of risk management, control and governance processes, and would report on individual risk-based audits.

- The OCG would take on new responsibility for horizontal and sectoral audits, as well as focused horizontal or sectoral auditing in SDAs.

- The OCG would establish an audit committee to provide advice and guidance on its work in SDAs.

- The OCG would report annually to the Treasury Board on the state of risk management, control and governance processes across government, and would report on audit work within departments.

- The OCG would establish standards and guidance that align with internationally recognized internal audit practices.

- The OCG would conduct horizontal audits integrated with departmental audit activity, and would provide advice and services on internal audit matters.

- The OCG would implement performance monitoring and accountability reporting for internal audits.

- The Policy created a framework to better balance the internal audit responsibilities of deputy heads and the OCG.

- The Policy stipulated an investment in the recruitment of skilled professionals and in the professional development of auditors.

- The Policy reinforced the assurance role of internal audit in accountability relationships, decision making and program improvement, and expanded the role as it pertains to risk management, control and governance.

- The Policy stipulated a comprehensive, government-wide approach to the way internal audit activities are planned and carried out in federal departments.

C. Objectives

The objective of the 2006 Policy on Internal Audit is to strengthen public sector accountability, risk management, resource stewardship and good governance by reorganizing and bolstering internal audit services across government. In 2009, the Policy objective was updated to state the following: “The objective of the Policy is to support strong and accountable public sector management by ensuring effective internal auditing within departments and across governments.”

D. Related Legislation

The Federal Accountability Act was enacted in December 2006. It is a key framework, driver and enabler for the government’s public accountability agenda. Within this omnibus legislation, several important steps were taken that pertain directly to the internal audit function. The Act brought the first recognition of internal audit in Canadian federal legislation. The Act included a specific requirement for departments to have an appropriate internal audit capacity and to have a DAC. It also designated deputy heads as the accounting officers of their respective departments, answerable to parliamentary committees and responsible for areas such as systems of internal control and compliance. In addition, changes to the Access to Information Act allowed for a discretionary exemption for internal audit working papers for up to 15 years.

A more recent development that further enhanced public accountability was the preparation of the financial management policy suite for the federal government, including the Policy on Financial Management Governance and the Policy on Internal Control. The latter focuses primarily on internal controls over financial reporting and letters of representation from deputy heads and CFOs.

E. Policy Implementation

The 2006 Policy on Internal Audit applies to “departments” within the meaning of section 2 of the Financial Administration Act. This does not include the Canada Revenue Agency or Crown corporations. Of the 104 departments covered by the Policy, 46 are LDAs (meaning that they have annual expenditures of $300 million or more, or 500 or more FTEs). There are 50 SDAs (less than $300 million in annual expenditures and fewer than 500 FTEs). With regard to the remaining federal government departments, the Policy states that the principles of the Policy, as it applies to LDAs, will apply to the offices of agents of Parliament and to the Public Service Commission of Canada. In that respect, the deputy heads of these organizations may authorize any departures from specific policy requirements as they may deem appropriate in light of the governance arrangements, statutory mandate and risk profile of the organization.

Some of the key requirements and provisions of the 2006 Policy on Internal Audit that pertain to LDAs include the following:

- CAEs must report directly to the deputy head.

- DACs must have a majority of external members recruited from outside the federal public administration.

- A risk-based internal audit plan (i.e., a plan that addresses the areas of higher risk and significance) must be developed and implemented.

- An internal audit capacity must be provided that is appropriate to the needs of the department and that operates in accordance with the Policy and professional internal audit standards.

- Chief audit executives must provide deputy heads with added assurance on the adequacy and effectiveness of risk management, internal control and governance processes within the department.

To help implement the Policy, accompanying funding was provided to enable LDAs to carry out activities such as hiring and training internal audit staff, and to pay for the costs of external DAC members.

Some of the key requirements and provisions of the 2006 Policy on Internal Audit that pertain to SDAs include the following:

- The OCG will conduct horizontal and other audits of SDAs each year and will provide deputy heads with copies of all relevant audit reports.

- The Comptroller General is responsible for establishing a Small Departments and Agencies Audit Committee (SDAAC) to provide a review, advice and recommendations on internal audits of SDAs conducted by the OCG.

- The OCG will facilitate access to independent and qualified internal audit resources when deputy heads of SDAs determine a need for internal audit work beyond that performed by the OCG.

In addition to these requirements and provisions, the Policy states that the Comptroller General is responsible for focused, sustained functional leadership of internal audit across government in order to build and develop capacity, ensure adequate levels of professionally qualified resources, and ensure adherence to professional standards and rigour in the delivery of internal audits.

The implementation of the Policy is a mixed model; it is decentralized to departments, with strong, centralized functional guidance and operational capacity at the OCG. The Policy outlines the responsibilities of the OCG, as well as how departmental and OCG roles and responsibilities are expected to interact.

F. Interim Assessment of the Policy

In 2008, the OCG performed an interim assessment of the implementation of the 2006 Policy on Internal Audit. The objective was to identify critical policy changes that were required immediately. The assessment criteria were the Policy’s relevance, alignment with statutory amendments brought about through the Financial Administration Act, criticality, practicality and achievability, and harmonization with the reporting requirements set out in federal government financial management policies. In 2008, the OCG reviewed prior assessments, conducted a line-by-line review of the Policy as well as the Policy’s directives and guidelines, and sought feedback from stakeholders. The outcome of the interim assessment resulted in several amendments to the Policy, effective July 1, 2009, that codified the practice and understanding of roles and functions that were operative early on in the life of the Policy. The 2009 amendments were not new, but were based on practice and experience as well as legislative changes that occurred in 2006–07. Some of the key amendments made to the Policy in 2009 included the following:

- Updated the language subsequent to the 2007 changes to the Financial Administration Act concerning the role of the deputy head as the accounting officer and the advisory role of the DAC.

- Reframed the role of CAEs in providing assurance on departmental governance, risk management and control processes.

- Harmonized the OCG’s reporting role and the delegation of authority to the President of the Treasury Board with requirements delineated in the financial management policy suite.

- Permitted agents of Parliament and the Public Service Commission of Canada to authorize specific risk-based departures from the Policy, insofar as the underlying Policy principles are adhered to, and the legislative requirements applicable to internal audit are observed.

- Removed the concept of the DAC as a direct assurance provider and instead stated that DACs should provide the Deputy Head with advice and recommendations regarding the sufficiency, quality and results of assurances.

- Highlighted the notion of risk-targeted (versus comprehensive) audit coverage and sought to inject risk considerations to reduce the process burden on DACs.

- Adjusted the requirement for DAC comments on Departmental Performance Reports.

- Removed the need for CAEs to provide annual holistic opinions to deputy heads and DACs on the effectiveness and adequacy of risk management, control and governance processes in their departments. The revised Policy states that the CAE should provide the Deputy Head with an independent assurance report on the adequacy and effectiveness of risk management, control and governance processes within the department.

- Changed the timing of reports to the Treasury Board from periodic to annual.

- Removed the notion of in camera meetings of DACs with their respective minister.

G. Resources

In keeping with one of the cornerstone objectives of the 2006 Policy on Internal Audit, the Treasury Board approved the progressive allocation of incremental resources to help the internal audit community implement the Policy’s new requirements. This began with incremental investments of approximately $13 million in 2006–07 and $24 million in 2007–08. Once the strategy for reconfiguring the internal audit community is fully implemented, total incremental funding across government is expected to rise to about $40 million on an ongoing basis. The funding approved by the Treasury Board is incremental to investments made by departments.

In addition to this allocated funding, the OCG established an operational capacity to conduct horizontal audit work across SDAs and LDAs. In mid-2008, the OCG also established an omnibus supply arrangement for audit and related support services (called Professional Audit Support Services, or PASS). PASS provides departments and agencies with timely access to qualified, contracted audit services. This arrangement is important as an essential supplement to internal audit capacity during the implementation transition period and beyond.

H. Activities

The following is a brief description of some activities that have been carried out to date as a result of the Policy on Internal Audit.

-

Independent DACs: Working with departments and the internal audit community, the OCG put in place processes to recruit, select, retain and compensate external members of the independent DACs, which are mandated to provide deputy heads with advice on the functioning and adequacy of departmental governance, risk management and control frameworks and processes. Recruitment activities have resulted in the establishment of a DAC for almost every LDA (47 audit committees with 152 external members). Some activities carried out by DACs include preparing an annual report for the Deputy Head, and providing advice and recommendations as requested by the Deputy Head on emerging priorities, concerns, risks, opportunities, and accountability reporting.

To support the evolution of an effective and sustainable community of practice for DACs, the OCG implemented a curriculum for learning and engagement. The curriculum includes an orientation to the federal government and core subject-matter workshops (e.g., risk management). A generic DAC Charter was developed in 2006, and the terms and conditions of appointment as well as the Guidebook for a Departmental Audit Committee were released in 2007. The latter provides reference tools to help DAC members fulfill their role and responsibilities.

The Government of Canada Audit Committee was established to provide advice to the Secretary (Deputy Head) of the Treasury Board of Canada Secretariat and to provide oversight support to the Secretary and the Comptroller General in relation to the government wide activities of the OCG regarding its functional leadership, operations, monitoring and reporting responsibilities in the area of internal audit. To support the OCG’s horizontal audit responsibilities in relation to SDAs (as called for in the Policy), the SDAAC was also established. The SDAAC performs a role similar to that of a DAC.

CAE appointments: With one exception, all LDAs in the federal government have appointed CAEs that report directly to the Deputy Head. The CAEs were hired by the department in consultation with the OCG. CAEs are responsible for leading the internal audit function within the department, including establishing three-year, risk-based audit plans and performing risk based internal audits as needed to provide the Deputy Head with an independent annual overview report on the adequacy and effectiveness of risk management, control and governance processes within the department. In addition, the CAE is responsible for following up on management action plans to address any issues raised as a result of the internal audits. The OCG has established a training and mentoring program for CAEs.

-

Internal audit standards and guidance: As part of the Policy’s implementation, Internal Auditing Standards for the Government of Canada were produced to prescribe the internal auditing standards that are to be applied in all departments subject to the Policy on Internal Audit. The standards stipulate that the Government of Canada has adopted the IIA Professional Practices Framework and that all government departments must meet IIA standards in fulfilling their internal audit responsibilities, unless the standards conflict with the Policy or any related directives or guidelines provided by the Comptroller General or the Treasury Board. By establishing minimum standards, the Policy is intended to ensure that all departments have common internal audit standards and processes; however, this does not mean that departments need to employ identical internal audit processes.

In fall 2006, the OCG prepared a draft maturity model to set out expectations in relation to the Policy and to help departments assess their current internal audit operation, identify priorities and develop a plan of action. At the end of 2006, a draft internal audit Policy, standards and a practices manual were issued by the OCG to the federal internal audit community. As a result of further analyses and comments received from CAEs, this professional practices product was revised and resulted in the creation of the OCG Internal Audit Reference Centre, which incorporates the IIA Professional Practices Forum and provides a fully integrated, single-window, online reference library to guide audit practitioners in their work. The Web-based beta version of the reference centre was launched at the beginning of 2009 and has since been refined to reflect subsequent developments (e.g., the 2009 IIA Professional Practices Framework and amendments to the Policy in 2009).

The development of a core controls framework facilitated the conduct of audits and gave assurance to CAEs. The OCG developed and released a draft framework on core management controls in 2007, drawing from landmark initiatives such as the Control Objectives for Information and related Technology (COBIT), Criteria of Control Board (CoCo), and the Committee of Sponsoring Organizations of the Treadway Commission (COSO), and organized around the 10 key elements of MAF.

A further initiative involves developing a risk assessment methodology to support internal audit planning, specifically by creating a government-wide internal audit plan at the whole of government level and risk-based audit plans at the departmental level. Initial guidance on developing a risk assessment methodology was released as part of the OCG Internal Audit Reference Centre at the beginning of 2009.

The OCG has begun development work on practice inspections of the internal audit operations in individual departments and agencies. This development work, as well as related work on the OCG Internal Audit Maturity Model and the OCG Internal Audit Reference Centre, has yielded a practice inspection suite (e.g., a manual, a guidebook and a self-diagnosis) that helps departments and agencies participate in this activity and guides those conducting practice inspections. The most recent guidance is the Internal Audit Practice Inspection Guidebook, which was released in June 2010.

- Horizontal and sectoral audits: The OCG produced an initial 2007–10 horizontal audit plan using a risk assessment methodology. Along with this plan, the OCG has completed a number of horizontal audits of LDAs and SDAs.

- HR strategy and staffing: Since the Policy was introduced, OCG Capacity Building and Community Development has worked with the federal government internal audit community to build an HR framework for internal audit. The HR framework has several components, including a human capital plan; standardized organizational models and pre classified work descriptions; competency profiles for these work descriptions; resourcing to ensure that recruitment and capacity building activities meet the needs of the community; learning, professional and management development; and community outreach.

- Internal auditor training: The last few years have seen enhancements to the training curriculum for internal auditors. The core of this curriculum, which has been in place for several years, includes the following elements: orientation to internal audit, conducting internal audits, and managing internal audits. Courses have been developed and delivered with the Canada School of Public Service, including training in risk-based audit planning, assessment of internal control, communications, and ethics. Periodic armchair sessions also provide perspectives on specific aspects of the Policy and its implementation. In addition, the OCG is working with the IIA to provide training to support internal audit certification.

- Accountability of the internal audit function: As part of MAF, the Treasury Board of Canada Secretariat performs an annual assessment of the internal audit function in federal government departments. The MAF assessment examines the progress made by the internal audit function within federal government departments

- Annual assurance reporting: One of the amendments to the 2006 Policy, effective July 1, 2009, stipulated that, instead of providing a holistic opinion, CAEs should provide the Deputy Head with an independent assurance report on the adequacy and effectiveness of risk management, control and governance processes within the department. Upon further consideration of this requirement, the OCG’s current vision is for the CAE to provide the Deputy Head with an annual overview report on the audit and other work performed. The annual overview report should give the Deputy Head a timely overview of the internal audit findings resulting from the execution of the risk-based audit plan, summarized in the context, mandate, priorities and risk profiles of the organization. Draft OCG guidance on the annual overview reporting requirements is in progress.

I. Intended Outcomes

The intended outcomes of the 2006 Policy on Internal Audit are outlined as follows.

- Immediate Outcomes

- Independence of the internal audit function within departments;

- Increased assurance and advice to deputy heads regarding risk management, control and governance;

- Increased capacity and strengthened professionalism of the internal audit function within departments; and

- Audit coverage appropriate to the level of risk.

- Intermediate Outcomes

- Increased deputy head confidence in the assurance and advice provided by the internal audit function and DACs on risk management, control and governance;

- Increased effectiveness of the internal audit function;

- Increased management action on internal audit recommendations leading to improved risk; and management, governance and internal control in audited areas.

- Long-Term Outcomes

- Support for deputy heads in their role as accounting officers;

- Strong credible internal audit regime;

- Improved overall departmental risk management, internal control, governance and resource stewardship; and

- Increased ability of departments and agencies to effectively meet their objectives.

- Ultimate Outcome

- Strong and accountable public sector management.

J. Logic Model

Figure 1 provides a logic model for the 2006 Policy on Internal Audit and depicts the causal relationships and links between the input, activities, outputs and intended outcomes of the Policy. The links between the activities and the hierarchy of outcomes in the logic model constitute testable hypotheses, which form the essence of the evaluation of the Policy. The intended outcomes are grouped into immediate, intermediate, long-term and ultimate categories. All of the inputs, activities and outputs shown in the logic model contribute to the ultimate outcome of the Policy, which is “strong and accountable public sector management.” The evaluation of the Policy concentrates primarily on assessing whether the immediate and intermediate outcomes have been achieved, given that they are more quantifiable and directly attributable to activities carried out as a result of the Policy. In addition, sufficient time may not have elapsed to measure whether all of the long-term outcomes (as well as the ultimate outcome) of the Policy have been achieved.

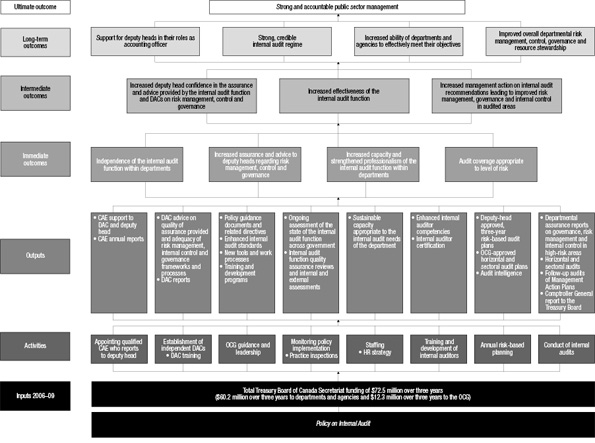

Figure 1. The logic model for the 2006 policy on internal audit - Text version

This graphic image provides the logic model for the 2006 Policy on Internal Audit.

As illustrated, the logic model shows that the ultimate outcome of the Policy is strong and accountable public sector management.

The four long-term outcomes are that Deputy Heads are supported in their roles as accounting officer; strong credible internal audit regime; increased ability of departments and agencies to effectively and efficiently meet their objectives; and improved overall department risk management, control, governance, and resource stewardship. The three intermediate outcomes presented are Deputy Heads have increased confidence in the assurance and advice provided by the internal audit function and DACs on risk management, control, and governance; increased effectiveness on the internal audit function; and increased management action on internal audit recommendations leading to improved risk management, governance, and internal control to audited areas. Four immediate outcomes are provided: independence of the internal audit function within departments; increased assurance and advice to Deputy Heads regarding risk management, control, and governance; increased capacity and strengthened professionalism of the internal audit function within departments; and audit coverage appropriate to level of risk. The following outputs lead to the stated outcomes: Chief Audit Executive support to DAC and Deputy Head, Chief Audit Executive Annual Reports, DAC advice on quality of assurance provided and adequacy of risk management, governance, and internal control frameworks and processes, DAC reports, Policy guidance documents and related directives, enhanced internal audit standards used by all departments, new internal audit tools and work processes, training and development, ongoing assessment of the state of the internal audit function across government, internal audit function quality assurance reviews and internal/external assessments, sustainable capacity appropriate to the internal audit needs of the department, enhanced internal auditor competencies, internal auditor certification, Deputy Head approved 3-year Risk-based Audit plans, Office of the Comptroller General approved horizontal and sectoral audit plans, audit intelligence, departmental audit reports provide assurance on governance, risk management, and internal control in high risk areas, horizontal and sectoral audits, follow-up audits of management action plans, and the Comptroller General’s report to Treasury Board. The activities leading to the production of the named outputs are as follows: appointing qualified Chief Audit Executive who reports to the Deputy Head; Establishing an independent Departmental Audit Committee, Departmental Audit Committee training; Office of the Comptroller General guidance and leadership; Monitoring policy implementation and practice inspections; Staffing, Human Resources strategy; Training and development of internal auditors; Annual risk based planning; and Conducting internal audits. To implement the activities that produce the outputs which result in the stated outcomes, the following inputs have been allocated: Total TBS funding of $72.5 million over three years. $60.2 million dollars over three years to departments and agencies and $12.3 million /3 years to the Office of the Comptroller General.

III. Evaluation Findings and Conclusions

The 2009 Policy on Evaluation stipulates that, in the Government of Canada, evaluation is the systematic collection and analysis of evidence on the outcomes of programs to make judgments about their relevance and performance, and alternative ways to deliver them or to achieve the same results. Pursuant to the Policy on Evaluation, this section provides the evaluation findings and conclusions related to evaluation questions dealing with program relevance, performance and alternatives.

A. Relevance

This section presents findings and conclusions on evaluation questions dealing with the extent of the need for and the relevance of the Policy on Internal Audit.

Evaluation Question 1: Is there a continued need for the current Policy?

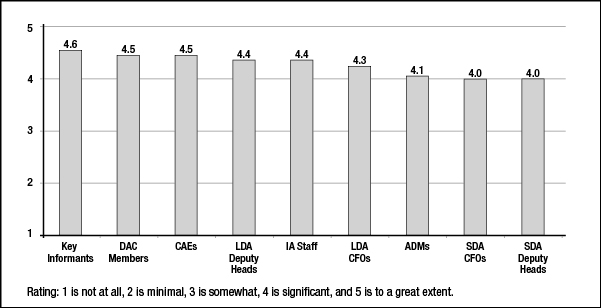

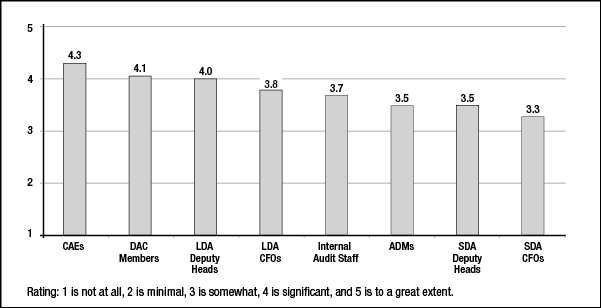

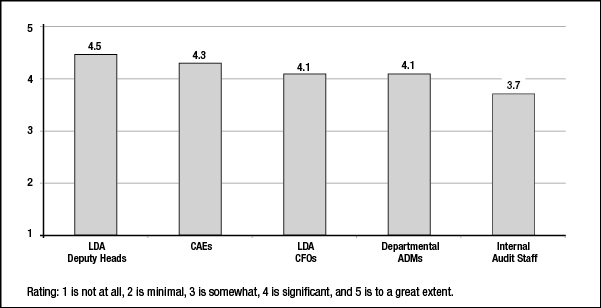

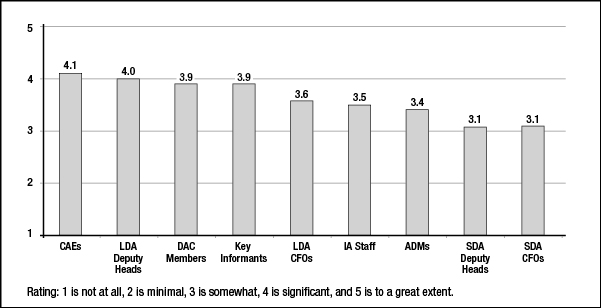

To assess need, a survey of stakeholders was conducted. They were asked to indicate to what extent there is a need for the current Policy on Internal Audit (i.e., the 2006 Policy with 2009 modifications), on a scale of 1 to 5, where 1 is not at all, 3 is somewhat, and 5 is to a great extent. Based on average ratings provided, all respondent groups indicated that the need for the current Policy is still significant, as shown in Figure 2.

Figure 2. Need for the Policy - Text version

This bar graph illustrates interviewed respondents’ views regarding the need for the Policy on Internal Audit. Individual groups provided the following results: Deputy Heads of Small Departments and Agencies, 4.0, Chief Financial Officers of Small Departments and Agencies, 4.0, Assistant Deputy Ministers, 4.1, Chief Financial Officers of Large Departments and Agencies, 4.3, Internal Audit staff, 4.4, Deputy Heads of Large Departments and Agencies, 4.4, Chief Audit Executives, 4.5, Departmental Audit Committee Members, 4.5 and key informants, 4.6.

The most frequent reasons given by stakeholders, particularly LDA deputy heads, for their ratings were as follows:

- The need for independent audit advice has never been greater because of increased public scrutiny and expectations regarding accountability as stipulated in the Federal Accountability Act.

- The Policy provides assurance for deputy heads to help fulfill their role as the accounting officers of their organization.

- The Policy provides central guidance on the responsibilities of all stakeholders and ensures that the internal audit function is adequately resourced.

- The Policy provides deputy heads with independent opinions to help them monitor and manage their organization.

- The Policy supports strong and accountable management across government.

A review of the available documentation, including CAE and DAC reports, indicated that the following activities performed as part of Policy implementation have addressed most of the factors that led to the Policy’s introduction:

- Establishment of DACS that have a majority of external members;

- Establishment of a CAE position that reports directly to the Deputy Head;

- Development and use of Government of Canada internal audit standards by all federal government departments and agencies;

- Focus on assurance services;

- Horizontal audits conducted by the OCG to ensure appropriate internal audit coverage and capacity in small entities;

- Changes made to the Access to Information Act (as part of the Federal Accountability Act) to protect internal audit working papers for a period of up to 15 years; and

- HR strategy developed by the OCG for the internal audit function in the federal government.

Almost all the key informants surveyed indicated that most of the factors supporting the need for the current Policy on Internal Audit have not changed. These respondents indicated that it is critical for the internal audit function to remain independent and for the capacity and professionalism of the internal audit function not to revert to the situation that existed before the Policy was introduced. Although there have not recently been any high-profile breakdowns of control in the federal government, several stakeholders indicated that the importance of a risk-based internal audit function has increased as a result of the Federal Accountability Act and the new role of deputy heads as the accounting officers of their respective organizations. In addition, respondents indicated that there is a high level of public scrutiny and expectation with regard to the accountability of federal government ministers and employees.

Conclusion: The need for the Policy remains.

Evaluation Question 2: To what extent have the internal and external factors that led to the introduction of the 2006 Policy on Internal Audit changed or remained the same?

According to the documentation reviewed, the Auditor General of Canada played an important diagnostic and influential role by auditing the federal government internal audit function in 1994 and 2004. In the 2004 November Report of the Auditor General of Canada, Chapter 1, “Internal Audit in Departments and Agencies,” the Auditor General noted that considerable work remained to strengthen the internal audit function in the Government of Canada. The Auditor General also mentioned that, despite additional funding for internal audit in the past four years, the same problems have remained for more than a decade. The report identified the following factors that, if implemented, could positively affect the quality of internal audit across government:

- A consistent understanding by senior management of the role that internal audit can and should play;

- A DAC that has external members who are independent from management;

- A clear HR strategy at the departmental, central agency and government wide levels that sets out the qualifications and the appropriate number of staff for the internal audit community;

- A focus on assurance services; and

- A strategy to ensure appropriate internal audit coverage and capacity in small entities.

Some other factors that influenced the development of the 2006 Policy on Internal Audit include the following:

- Public scrutiny of accountability in the government and the private sector increased as a result of Enron, Sarbanes-Oxley and Gomery scandals.

- The Public Accounts Committee indicated that internal audit lacked sufficient independence from line management.

- There was a lack of consistency in internal audit capacity, skills and practice throughout the federal environment.

- Internal audit methods and standards were not applied consistently.

- Internal auditors were not mobile within government.

- Internal audit was not focused on assurance, and its focus on reviews and consulting presented a potential conflict of interest.

- Audit committees were not independent.

- The provisions of the Access to Information Act weakened the audit regime.

- Deputy heads were not consistently provided with the independent assurance they required to help them discharge their responsibilities.

Conclusion: Most of the internal and external factors that led to the introduction of the 2006 Policy on Internal Audit have remained the same.

Evaluation Question 3: To what extent are the Policy objectives still relevant?

The Policy objectives are to strengthen public sector accountability, risk management, resource stewardship and good governance by reorganizing and bolstering internal audit across government. As evidence that the Policy objectives are still relevant, the Federal Accountability Action Plan states that independent, objective and timely internal audit services within departments are necessary because they provide assurance to deputy ministers and reinforce good stewardship practices and sound decision making. In addition, the Federal Accountability Act supports the Policy by requiring that deputy heads ensure an appropriate internal audit capacity and establish DACs.

All key informants who responded to this evaluation question stated that the Policy objectives are relevant because a professional and independent internal audit function will always be essential to public sector accountability, risk management, resource stewardship and good governance. They also indicated that, by focusing on a professional and independent internal audit function, the Policy requires federal government departments and agencies to address the areas of highest risk and to obtain assurance that the necessary controls are in place and operating effectively. These controls are critical to public sector accountability, risk management, resource stewardship and good governance.

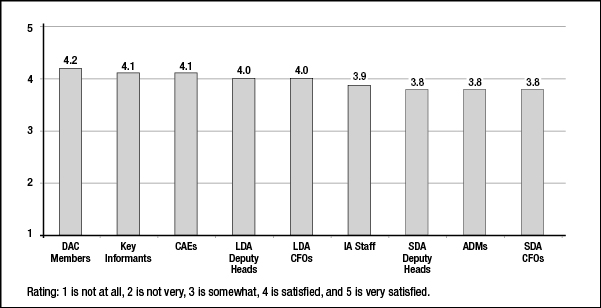

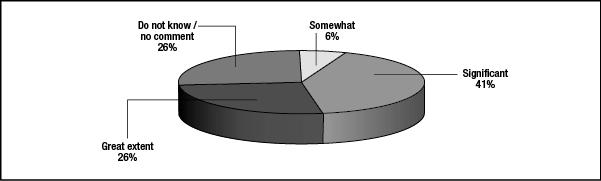

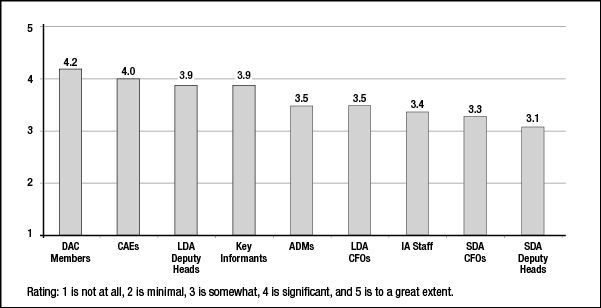

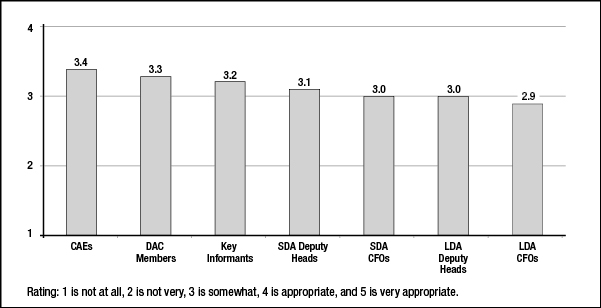

Stakeholders were asked to indicate their overall degree of satisfaction with the Policy, on a scale of 1 to 5, where 1 is not at all, 3 is somewhat, and 5 is very satisfied. If the degree of satisfaction is high, it can be presumed that the Policy objectives are still relevant. A low degree of satisfaction indicates that the Policy objectives may not be relevant; however, it could also indicate that other factors, such as Policy implementation, have not proceeded as intended. As indicated in Figure 3, there was widespread satisfaction with the Policy, as evidenced by the fact that the average rating provided by all respondent groups is 4 out of 5, and there are no significant variations in the average ratings of the different respondent groups.

Figure 3. Degree of Satisfaction With the Policy - Text version

This bar graph shows the various respondent groups’ levels of satisfaction with the Policy on Internal Audit. The following results are shown in graphic form: Departmental Audit Committee Members and key informants, 4.2, Chief Audit Executives, 4.1, Deputy Heads of large departments and agencies, 4.0, Chief Financial Officers of large departments and agencies, 4.0, Internal Audit staff, 3.9, Deputy Heads of small departments and agencies, 3.8, Assistant Deputy Ministers, 3.8, and finally, Chief Financial Officers of small departments and agencies, 3.8.

Of the 29 LDA deputy heads who responded to this evaluation question, 25 of them, or 83 per cent, stated that they were either satisfied or very satisfied with the Policy. The highest average satisfaction rating was provided by DAC members (4.2 out of 5); the lowest average satisfaction rating (3.8) was provided by SDA respondents and ADMs.

The most frequent reasons given by respondents for their degree of satisfaction with the Policy are as follows:

- The establishment of DACs that have external members has been one of the most important activities carried out to achieve Policy objectives.

- The Policy enables federal government departments and agencies to address their areas of highest risk internally, rather than relying on external assessments.

- The Policy provides assurance to accounting officers that controls are in place to ensure public sector accountability, risk management, resource stewardship and good governance.

- The provision of incremental funding in conjunction with the Policy has enabled the establishment of a professional and independent internal audit function within the federal government.

Although SDA deputy heads and CFOs stated that they appreciate the audit coverage provided to SDAs as a result of OCG horizontal audits, the most frequent reason given for their lower degree of satisfaction is their desire for the Policy to recognize the limited capabilities of the smaller SDAs (i.e., micro-agencies) in terms of participating in horizontal audits.

Conclusion: The Policy objectives are still relevant.

Evaluation Question 4: To what extent does the Policy meet the Government of Canada’s policy priorities, specifically those pertaining to accountability, transparency, risk management, control and governance?

The policy priorities of the Government of Canada with regard to accountability, transparency, risk management, control and governance are stipulated in the Financial Administration Act, which was introduced on April 11, 2006, to make government more accountable. The Financial Administration Act designates deputy ministers and deputy heads as accounting officers who are accountable to the appropriate committee of Parliament to answer questions related to their responsibilities. These responsibilities consist of the following:

- Ensuring that resources are organized to deliver departmental objectives in compliance with government policies and procedures;

- Ensuring that effective systems of internal control are in place;

- Signing departmental accounts; and

- Performing other specific duties assigned by law or regulation in relation to the administration of the department.

The Financial Administration Act states that independent, objective and timely internal audit services within departments are necessary to provide assurance to deputy ministers and to reinforce good stewardship practices and sound decision making. The Financial Administration Act specifies that deputy heads must ensure an appropriate internal audit capacity and establish DACs. The Policy on Internal Audit closely aligns with this Act because the Policy states that departments must have a DAC that has a majority of external members, and accompanying funding was provided with the Policy to ensure that departments have an appropriate internal audit capacity. In addition, the Policy objectives align with the Government of Canada priorities of increased accountability, transparency, risk management, control and governance, as set out in the Financial Administration Act.

Government of Canada priorities regarding internal control are also described in the financial management policy suite for the federal government, including the Policy on Financial Management Governance and the Policy on Internal Control. The Policy on Internal Audit is complementary to both of these because its intended outcomes include improved internal control and governance. A review of the Policy on Internal Control indicates that it focuses primarily on internal controls over financial reporting and letters of representation from deputy heads and chief financial officers—matters relevant to the practice of internal audit and to related governance mechanisms and processes.