Public Security and Anti-Terrorism Initiative: Summary Report

As part of the Spring 2013 Report of the Auditor General of Canada, Chapter 8 the Public Security and Anti-Terrorism (PSAT) Initiative, the Auditor General noted that between 2001 and 2009, $12.9 billion was approved for department and agency programs to fund activities related to public security and anti-terrorism following the terrorist attacks of . The Auditor General noted that while departments and agencies reported $12.9 billion was allocated to them through PSAT, only about $9.8 billion in spending was reported to the Treasury Board Secretariat.

The review by the Auditor General was based largely on information submitted by departments and agencies to the Treasury Board Secretariat as part of a framework for PSAT reporting that was established to monitor implementation of key initiatives. The Auditor General review of the information reported by departments and agencies showed that projects were consistent with the announced objectives of the PSAT Initiative. The Auditor General did not examine the implementation of individual department programs and projects.

The initial PSAT reporting process was launched in 2003 to monitor implementation of initiatives. The framework established reporting requirements in addition to the standard reporting by organizations through Estimates and Public Accounts. The requirements for reporting changed over time to incorporate lessons learned and to respond to recommendations from the Auditor General. For example:

- in 2004 changes were made to address issues of risk and provide a more detailed breakdown of funding,

- in 2005 further changes were made to apply a risk management lens to ensure a focus on those programs designed to mitigate high security risks and for which monitoring implementation was critical,

- in 2006 the Secretariat clarified which initiatives required continued reporting, and

- in 2008 the Secretariat implemented an electronic reporting approach.

The final round of PSAT reporting was in 2008–09. Although PSAT reporting requirements changed over time, the processes that departments followed for seeking the approval of Parliament and for reporting to Parliament and Canadians on spending and results were respected, authorities were sought through supply processes and expenditures reported at an aggregate level in Public Accounts.

Table of Contents

- Objectives of this Report

- Methodology

- Findings

- Completeness of Information

- In Summary

- Annex A: Examples

- 1. Amounts that were not included in the reporting framework

- 2. Amounts that were not spent in the reporting period (re‑profiled)

- 3. Amounts that were returned to General Revenue

- 4. Amounts that were transferred to other government organizations

- 5. Amounts that were reallocated

- 6. Amounts that were not spent in the reporting period (carried forward)

- 7. Reductions

- 8. Other

Objectives of this Report

The Auditor General did not recommend a reconciliation of the difference between allocated funds and activity reported to TBS on progress. However, the Treasury Board Secretariat decided it would be prudent to do a retroactive reconstruction of the financial elements of the PSAT initiative to provide greater clarity. The purpose of this report is to explain the $3.1 billion difference.

Methodology

Information on the $3.1 billion was not available in the Treasury Board Secretariat PSAT reporting framework. To explain the $3.1 billion difference the Secretariat reconstructed PSAT allocations and expenditures from 2001 to 2009. The Secretariat used information within the Secretariat that was made available to the Office of the Auditor General and worked with over 35 organizations which received allocations and maintained this information. In addition, the Secretariat validated information from organizations against other expenditure management information within the Secretariat as well as reporting in Public Accounts.

This was an exercise of reconstruction and reconciliation, not a financial audit. In doing the reconstruction exercise, the Secretariat was able to replicate $12.847 billion in allocations and $9.859 billion in reported expenditures. This leaves an outstanding difference of $2.987 billion.

Findings

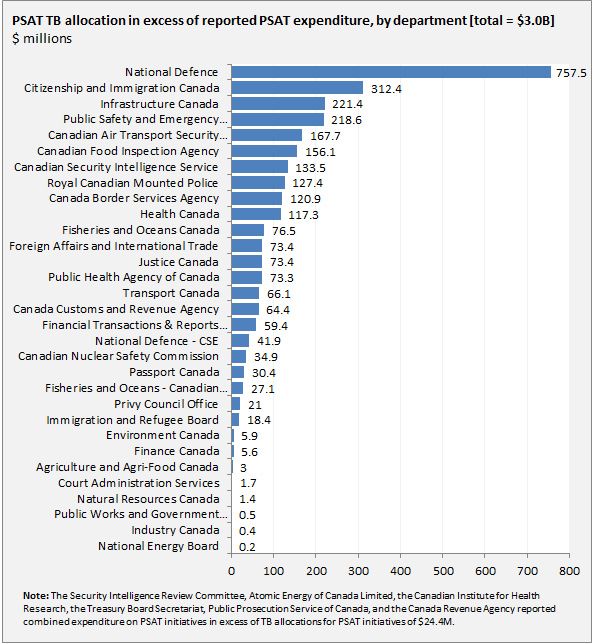

As demonstrated in Figure 1, the $3.0 billion difference can be largely accounted for and tracked through departmental information which has been subsequently provided by organizations. In other words, the variance found by the Auditor General is entirely due to the two types of documentation available at the time of his audit: one set of documents describing funds allocated to departments, another to report on departments’ progress. Over 35 organizations received PSAT funding. More than $2 billion of this difference can be explained by nine departments: National Defence, Citizenship and Immigration, Infrastructure Canada, Public Safety and Emergency Preparedness Canada, Canadian Air Transport Security Authority, Canadian Food Inspection Agency, Canadian Security Intelligence Service, Royal Canadian Mounted Police and the Canadian Border Services Agency.

Figure 1 - Text version

| Department | $ millions |

|---|---|

| National Defence | 757.5 |

| Citizenship and Immigration Canada | 312.4 |

| Infrastructure Canada | 221.4 |

| Public Safety and Emergency Preparedness Canada | 218.6 |

| Canadian Air Transport Security Authority | 167.7 |

| Canadian Food Inspection Agency | 156.1 |

| Canadian Security Intelligence Service | 133.5 |

| Royal Canadian Mounted Police | 127.4 |

| Canada Border Services Agency | 120.9 |

| Health Canada | 117.3 |

| Fisheries and Oceans Canada | 76.5 |

| Justice Canada | 73.4 |

| Foreign Affairs and International Trade | 73.4 |

| Public Health Agency of Canada | 73.3 |

| Transport Canada | 66.1 |

| Canada Customs and Revenue Agency | 64.4 |

| Financial Transactions & Reports Analysis Centre of Canada | 59.4 |

| National Defence - CSE | 41.9 |

| Canadian Nuclear Safety Commission | 34.9 |

| Passport Canada | 30.4 |

| Fisheries and Oceans - Canadian Coast Guard | 27.1 |

| Privy Council Office | 21 |

| Immigration and Refugee Board | 18.4 |

| Environment Canada | 5.9 |

| Finance Canada | 5.6 |

| Agriculture and Agri-Food Canada | 3 |

| Court Administration Services | 1.7 |

| Natural Resources Canada | 1.4 |

| Public Works and Government Services Canada | 0.5 |

| Industry Canada | 0.4 |

| National Energy Board | 0.2 |

The Treasury Board Secretariat found that while the $3.0 billion was not captured through the financial tables in the centralized reporting on the PSAT, the amount was explained through supplementary work with departments and other information in the Secretariat.

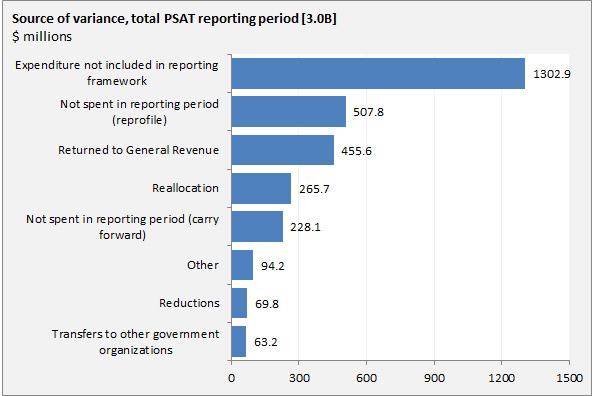

As demonstrated in Figure 2, the single greatest reason for the variance is expenditures that were simply not included in the PSAT reporting framework which was kept by the Treasury Board Secretariat to monitor implementation. The PSAT reporting framework established by the Secretariat was not intended to capture all of the PSAT initiatives – it was an incremental reporting requirement and it was modified over time. There were explicit exemptions to reporting provided, reporting on incremental funding was often not required; and reporting on corporate costs (Employee Benefit Plans and Accommodations) was not consistent.

In reconstructing this information, the Secretariat found that there were also significant amounts that were either: spent outside of the 2001 to 2009 reporting period, reallocated to other initiatives, or returned to the fiscal framework.

Figure 2 - Text version

| Variance | $ millions |

|---|---|

| Transfers to other government organizations | 63.2 |

| Reductions | 69.8 |

| Other | 94.2 |

| Not spent in reporting period (carry forward) | 228.1 |

| Reallocation | 265.7 |

| Returned to General Revenue | 455.6 |

| Not spent in reporting period (reprofile) | 507.8 |

| Expenditure not included in reporting framework | 1302.9 |

See Annex A for detailed examples

Completeness of Information

This was a reconstruction and reconciliation exercise, not a financial audit. However, based on information provided by departments and supporting information in the Secretariat, we have a reasonable level of confidence with regard to expenditures of $12.757 billion – over 99 percent of the total amount.

A few organizations (e.g. Canadian Food Inspection Agency, Justice, Public Health Agency, Public Safety and Emergency Preparedness) qualified their level of confidence with regard to the information they provided, usually within 5-10 percent and/or related to information in the early years. Although indirect evidence suggests that the expenditures were not included in the PSAT reporting, the Secretariat has a slightly lower level of confidence with regard to the following items:

- Department of National Defence: $15.2M;

- Public Safety and Emergency Preparedness Canada: $15.4M;

- Communications Security Establishment of Canada: $12.9 M.

In addition, the Secretariat reconstructed allocation and expenditure information for the Canada Customs and Revenue Agency which wound down in . The variance in CCRA for these two years is $64.4M. Of this, we have draft information on carry forward and reallocations, but little information on $25.2M. This reconstruction was based on draft reports, but not complete or final documentation.

In Summary

This exercise was not a financial audit, but a reconstruction and reconciliation exercise.

The process, overall, was robust, explaining the variance noted by the Auditor General in the Spring 2013 report. This amount was not captured through the financial tables included in the reporting on PSAT to the Treasury Board Secretariat, but was largely explained through supplementary follow-up with departments.

Generally departments were confident in the material provided, with some caveats given the passage of time and where detailed information was not available.

The Secretariat did review, challenge and make changes to information provided by departments based on other information available to the Secretariat.

The Secretariat has reasonable confidence in the summary information, and has noted where there are lower levels of confidence in the information as they relate to actual expenditures for individual initiatives.

In all cases these authorities and expenditures would have been captured in aggregate financial reporting as required through supply processes (Estimates, Reports on Plans and Priorities and Departmental Performance Reports) and in Public Accounts.

Annex A: Examples

1. Amounts that were not included in the reporting framework

The most significant portion of the variance is due to initiatives for which PSAT reports were not submitted to the Treasury Board Secretariat as part of the PSAT reporting framework. The PSAT reporting framework established by the Secretariat was not intended to capture all of the PSAT initiatives – it was an incremental reporting requirement. In all cases, financial reporting would have continued, as required through departmental supply documents (Estimates, Reports on Plans and Priorities and Departmental Performance Reports) and in Public Accounts.

There were explicit exemptions to this additional reporting, reporting on incremental funding was often not required; and reporting on corporate costs (EBP and Accommodations) was not consistent. There were cases where the amounts noted in the reports to the Treasury Board Secretariat were understated, including instances where departments did not report on the expenditures related to the Accommodations Charge or on Employee Benefit Plans, as these allocations were held centrally.

Examples include:

Department of National Defence:

DND was exempted from the additional reporting through the PSAT framework on a number of initiatives related to the immediate response to 9/11, including:

- $510M for Increased Military Capacity and Deployments to Afghanistan in 2001–02 and 2002–03;

- Technology for First Responders - $5M for (2001–02, 2002–03);

- Office of Critical Infrastructure Protection and Emergency Preparedness unforeseen costs - immediate response to 9/11 - $5M in 2001–02;

- Office of Critical Infrastructure Protection and Emergency Preparedness Program Integrity - $10M ongoing (subsequently transferred to Public Safety) and

- Critical Infrastructure protection - $5.1M in 2001–02.

Royal Canadian Mounted Police:

- RCMP did not report on $53.3M in expenditures incurred as part of the immediate response to 9/11 in its PSAT reports;

- RCMP understated expenditures in their initial reporting related the Integrated Border Enforcement Team and the Lawful Access Initiative in its PSAT reporting, accounting for $23.4M of the variance; and

- Other additional expenditures of $1.8M not included in PSAT reports.

Communications Security Establishment:

- CSEC reported additional expenditures of $57.1M that had not been previously reported in PSAT annual reports.

FINTRAC:

- FINTRAC received $10M in 2001–02, $14.7M in 2002–03, and $9.5M ongoing for activities related to the detection, prevention and deterrence of money laundering and the financing of terrorist activities. However, FINTRAC did not include financial tables on ongoing funding of $47.5M which was included in their standard departmental reporting.

Canadian Security Intelligence Service:

CSIS had expenditures of $88.6M that were not included in the PSAT reporting

- CSIS did not submit a report to the Secretariat in 2005–06.

Canadian Nuclear Safety Commission:

- One of CNSC’s programs was not subject to PSAT reporting requirements, even though it was funded through the Budget 2001 PSAT envelope. Spending for the Chemical Biological Radiological Nuclear First Responder Program was not included for 2003–04, 2004–05 and 2005–06, accounting for $31.9 M.

- In addition spending adjustments were made on other reports to account for actual expenditure for Employee Benefit Plans which accounts for a further $2.1M of the variance.

2. Amounts that were not spent in the reporting period (re‑profiled)

There are many instances in which changes in implementation plans required that departments seek approval, through Finance, to adjust their funding profile such that allocations could be moved to future years. The analysis shows a total of $507.8M in PSAT funding was re-profiled to years beyond 2008–09, which means that reporting on spending related to these allocations was not captured during the timeframe of PSAT reporting.

Examples include:

- Department of National Defence: DND re-profiled $103.6M for Marine Security Operations Centres, as well as $30M for the Secure Fleet Communication Project. Additional re-profiles of $22M were identified by DND.

- Infrastructure Canada: A total of $107.5M was re-profiled beyond 2008–09 for the Border Infrastructure Fund.

- Canadian Border Services Agency: CBSA re-profiled $74.9M in funding beyond 2008–09 for two initiatives: Arming Border Guards ($44.9M) and E-Manifest ($30M).

- Fisheries and Oceans – Canada Coast Guard: CCG re-profiled $63.2M beyond 2008–09 for the Mid Shore Patrol Vessels initiative.

- Public Health Agency of Canada: A total of $39.5M was re-profiled beyond 2008–09 for Avian and Pandemic Influenza Preparedness.

- Canadian Air Transport Security Authority: CATSA re-profiled $35M in capital funding beyond 2008–09.

- Transport Canada: Re-profiled $15.5M beyond 2008–09, primarily related to the Marine Security Contribution Program.

- Canadian Security Intelligence Service: CSIS re-profiled $14.5M in minor capital beyond 2008–09.

3. Amounts that were returned to General Revenue

Some departments did not fully expend the annual allocations, due to delays in implementation, or in some cases, as a result of cost savings achieved during implementation. In these cases, the amounts not spent were returned to the fiscal framework. Departments with significant levels of unspent funding over the eight year time period include:

- Canadian Air Transport Security Authority: $132.6M

- Transport Canada: $69.9M

- Public Safety Canada $51.9M

- Public Health Agency of Canada: $51.7M

- Citizenship and Immigration: $39.5M

- Canadian Food Inspection Agency: $37.5M

- Justice Canada: $19.7M

4. Amounts that were transferred to other government organizations

Transfers between organizations were used to move funding from one organization to another in order to more efficiently implement or manage a program or project and/or to reflect new organizational responsibilities.

Over the eight-year time period during which PSAT reporting was required, there were many funding transfers. In addition to reorganizations to realign responsibilities between existing departments and agencies, new departments and agencies were created: e.g. Canada Border Services Agency, Canadian Air Transport Security Authority, Public Health Agency of Canada, Public Security and Emergency Preparedness, and the Office of the Director of Public Prosecutions.

There were both transfers in and transfers out of PSAT initiatives. Overall, there was a net amount of $63.2M in transfers that were not captured in the PSAT reporting framework and account for that portion of the variance. These include many small amounts, transfers from PSAT organizations to non-PSAT organizations (e.g. from Transport Canada to the Canadian Space Agency; and from CFIA to Western Economic Diversification), from PSAT initiatives to non-PSAT initiatives, double counting from receiving organizations who treated funding as new.

In all cases, the transfers between organizations/votes were effected through the Supply process and reflected at an aggregate level in departmental reporting in Public Accounts.

5. Amounts that were reallocated

Deputy Heads have authority to reallocate or redirect amounts within their mandate, as approved by Parliament and subject to any conditions established by the Treasury Board. In cases where funds were reallocated to other initiatives for which PSAT reports were developed, expenditures against the additional reallocated funds were not always captured. In situations where these funds were reallocated to other security initiatives that were not funded from the $12.9 billion in new security funds allocated between 2001 and 2009, there was no requirement for expenditures to be included in the reporting framework. These amounts would not have been reported on as part of the PSAT reporting framework.

Examples of significant reallocations include:

- Canada Border Services Agency: $168.9M in funds were reallocated to other priorities within the Agency. These included $18.7 M from Free and Secure Trade to the Integrated Primary Inspection Line initiative, Harmonized Commercial Targeting, Advance Passenger Information / Passenger Name Record initiative, and Nexus Air Programs. An additional $15.4M was reallocated from Advance Commercial Information to other PSAT programs. Other amounts were reallocated within the agency to contribute to various programs designed to maintain a free and secure border, one of the PSAT and National Security Policy objectives.

- Canadian Food Inspection Agency: $49.2M was reallocated from Surveillance and Detection, Enhanced Border Controls and Avian Influenza to other security-related objectives. These included increased enforcement and compliance field activities, plant, animal and food inspection; policy and protocol negotiations to mitigate risk associated with in transit shipments from the US; food safety investigations in the field and improved federal provincial collaboration on threats to the food supply.

- Infrastructure Canada: $39.9M in reallocations from the contributions vote to the operating vote, to support implementation of their PSAT initiative.

- Public Safety Canada: $19.8M accounted for primarily by reallocations from Critical Infrastructure Protection and Emergency Preparedness ($13.3M); Interoperability project ($3.7M); Secure Communications Interoperability Project ($1.5M); and Enhanced Passenger Rail, Urban Transit and Ferry Security ($1.3M). The funds were redirected to other Public Safety and Emergency Preparedness programming.

6. Amounts that were not spent in the reporting period (carried forward)

Similar to re-profiles, departments are able to carry forward portions of their operating and capital votes between years and to future years. Some departments were able to carry forward PSAT funding to better respond to their implementation requirements. Amounts that were carried forward to years beyond 2008–09 would not have been captured in PSAT reporting.

Examples include:

- Canada Border Services Agency: $130.5M carried forward across a variety of initiatives, including Detection Equipment ($19.3M), Arming Border Guards ($33.5M); and Doubling up ($10.6M). CBSA has a two-year appropriation, which means that amounts not spent in

2007–08 and 2008–09 could have been carried forward and expended beyond the PSAT reporting period. - Department of National Defence: DND carried forward $11.7M for expenditures related to two initiatives: Marine Security Operation Centres, and Secure Fleet Communications.

- Department of Foreign Affairs and International Trade: DFAIT carried forward $21.3M, of which $11.6M relates to the increased mission security initiative.

- Department of Fisheries and Oceans – Canada Coast Guard: CCG carried forward $13.4M related primarily to two initiatives: $9M for Automatic Identification System and Long Range Tracking and $4.3M for the Mid Shore Patrol Vessels project.

- Canadian Security Intelligence Service: CSIS carried forward $11.9M related to various security activities.

7. Reductions

During the PSAT reporting period, various government-wide exercises were undertaken to identify savings and reduce expenditures. In some cases, amounts originally identified for PSAT initiatives were reduced in these exercises.

Examples include:

- Justice Canada: Justice identified $24.7M of PSAT funding between 2003–04 and 2008–09 in reductions, as part of a Budget 2003 initiative to reduce program spending.

- Department of National Defence: DND reduced its PSAT funding for the High Frequency Surface Wave Radar project by $20.6M in 2007–08 and 2008–09, to reflect reductions associated with the Budget 2006 Expenditure Review.

- Canadian Food Inspection Agency: CFIA identified reductions of $17M from its Avian Influenza allocation, further to CFIA’s 2007–08 Strategic Review. The reduction was implemented starting in the 2008–09 fiscal year.

- Department of Foreign Affairs and International Trade: DFAIT identified $4.1M in reductions from its Counter-Terrorism Capacity Building Program as part of DFAIT’s Strategic Review in 2007–08.

- Transport Canada: Transport implemented a $2.5M cut to its Marine Security Contribution Program as a result of its Strategic Review, starting in 2008–09.

8. Other

There are a range of “other” explanations that were provided for the variance between expenditures and allocations, such as:

- 2005–06 Governor General Special Warrants – certain allocations, which while approved by the Treasury Board and/or Parliament, were not drawn into departmental reference levels due to timing of an election and the subsequent use of Governor General Special Warrants, e.g.:

- Foreign Affairs and International Trade: $13.05M;

- Public Health Agency of Canada: $12.8M.

- Fisheries and Oceans: There was a duplication of funding allocations for Automatic Identification System and the Long Range Tracking projects, totalling $26M.

- Canada Customs and Revenue Agency: The Secretariat reconstructed allocation and expenditure information for the Canada Customs and Revenue Agency which wound down in . In 2002–03, CCRA had authorities in its Vote 1 (operating) of over $3.1 billion and expenditures just over $3.0 billion. This reconstruction was based on draft reports, but not complete or final documentation. It is clear that $25.2M was spent.

© Her Majesty the Queen in Right of Canada, represented by the President of the Treasury Board, 2013,

ISBN: 978-0-660-26002-0

© Her Majesty the Queen in Right of Canada, represented by the President of the Treasury Board, [2013],

[ISBN: 978-0-660-26002-0]

Page details

- Date modified: