Guidebook for a Departmental Audit Committee

Note

- This document is intended as advice or guidance, and contains questions and considerations, though not exhaustive, that are critical to the functioning of Departmental Audit Committees.

- This document does not constitute a departmental legal or policy requirement nor does it establish monitoring obligations on the part of the Treasury Board of Canada Secretariat.

- This document was revised to reflect the latest changes to the Policy on Internal Audit, Directive on Internal Audit (effective June 2023) as well as the new Global Internal Audit Standards which were released in January 2025 by the Institute of Internal Auditors.

- Please contact the Audit Communities Division at acrds-srdcv@tbs-sct.gc.ca for any inquiries related to this guidebook.

On this page

- Introduction

- 1. Overview of a Departmental Audit Committee

- 2. Functioning of a Departmental Audit Committee

- 3. Aides-mémoire

- Appendix A: suggested departmental support for the DAC

- Appendix B: sample table of contents for a DAC orientation/reference

- Appendix C: self-assessment questionnaire

Introduction

Since their inception in 2006, Departmental Audit Committees (DACs) have formed an integral component of the Government of Canada’s efforts to ensure rigorous stewardship and accountability for public resources. Meanwhile, much has changed in the federal government’s operating environment over that time, characterized not only by a fast-moving and ever-evolving risk environment, but an enhanced emphasis on horizontal approaches and business transformation initiatives to address growing complexity in how government works.

In this context, DACs face significant challenges but remain uniquely positioned to offer advice and guidance, with the power to address some of the most pressing matters in modern public administration.

The Guidebook for a Departmental Audit Committee has been updated to reflect the latest changes to the Policy and Directive on Internal Audit (effective June 2023) and the new Global Internal Audit Standards (released January 2025).

As such, the Guidebook continues to present a framework to support the work of DACs and remains premised on the understanding that its contents should be adapted to meet each committee’s and each department’s unique needs and circumstances.

The Guidebook is divided into three broad sections:

- the first is an overview of a DAC

- the second discusses the functioning of a DAC

- the third comprises aides-mémoire and appendices to supplement the information provided in the first two sections

The Guidebook will function as an evergreen document, with updates to be posted, as needed, on appropriate web-based platforms or communicated to DAC members through their host departments.

1. Overview of a Departmental Audit Committee

In this section

The sections that follow set out the roles and responsibilities of a DAC as a whole and of DAC members individually.

1.1 Role and responsibilities of the Departmental Audit Committee

A DAC is an advisory body whose role is defined in the Treasury Board Policy on Internal Audit and the Directive on Internal Audit. The Terms and Conditions for Audit Committee Members address the key issues that surround the initiation and management of members’ tenure.

A DAC is expected to support the deputy head in their accounting officer roleFootnote 1 by providing the deputy head with objective advice and guidance, independent of management, in the areas of governance, risk management and control.Footnote 2

The DAC members’ knowledge, experience, expertise and independence as external to the public service should provide a valuable, impartial and respectful supplementary perspective on departmental operations.

DACs play a critical role in challenging management, a key function of their external composition. In doing so, these committees help strengthen management processes and practices across federal government departments.

Although policies related to internal audit and audit committees are continuously updated, the core areas of DAC responsibility remain constant:

- values and ethics

- risk management

- management control framework

- internal audit function

- external assurance providers

- follow-up on management action plans

- financial statements and public accounts

- accountability reporting

The amount of time spent by the DAC on each of these core areas of responsibility varies in accordance with the complexity, risks and priorities of the department in question. The intention is for the DAC to provide sufficient and appropriate coverage to all areas over the course of a year.

The approach to addressing some of the responsibilities listed above will necessarily be adapted by the Small Departments Audit Committee and by the Treasury Board Secretariat Audit Committee due to the horizontal nature of their mandates (e.g., accountability instruments and financial statements).

The DAC’s independence from line management situates the chair and members to provide the deputy head with strategic guidance and advice in areas that may appear to fall outside of the core responsibilities listed above. This guidance could be in the form of advice on topics ranging from strategic planning to large IT-enabled business transformation projects to digital government.

For instance, the DAC could play a critical role in questioning whether and how management has taken steps to adhere to IT project oversight and management processes and principles. With respect to strategic planning, the DAC could play a valuable challenge function regarding alignment between departmental performance targets and strategies to deliver on them. These activity areas in fact support the DAC’s core responsibilities for risk management, management control frameworks, and accountability reporting (see corresponding aides-mémoire 3.2, 3.3 and 3.8), and are expected to be undertaken in accordance with the department’s risk and operational environment.

In all areas of their responsibilities, DACs must always be satisfied that they have received sufficient information in order to be confident in the advice they provide to the deputy head. Consistent with the Terms and Conditions of Appointment for Audit Committee Members, DACs must devote appropriate time to preparation and should raise any information gaps with the chief audit executive (CAE). Just as auditors are often referred to as “professional sceptics,” DAC members must endeavour to ensure that they have received some acceptable level of substantiation of the information, findings and conclusions that are presented to them for deliberation.

Where the substantiation is not present, DAC members are justified in challenging departmental staff to better support their material prior to the committee forming a decision on their advice to the deputy head.

1.2 Accountability relationships

The DAC’s primary role is to advise the deputy head in monitoring the organization’s core systems of control and accountability. The deputy head, defined as the accounting officer in the Financial Administration Act, is ultimately accountable for the internal audit function.

The DAC reports directly to the deputy head, providing objective advice and guidance in the areas of governance, risk management, and control, independent of management. Its advisory capacity is critical to achieving the objectives of the Treasury Board Policy on Internal Audit. The DAC should be well-versed in the policy as well as with the directives and guidance that support it, to effectively fulfill its responsibilities and expected outcomes.

It is also important to note that the DAC has no reporting relationship or accountability to the corresponding Minister.

The Office of the Comptroller General (OCG) is another key player in this relationship. In addition to co-recommending the appointment of DAC members, the Comptroller General of Canada is responsible for providing functional direction to the internal audit community across the federal government.Footnote 3

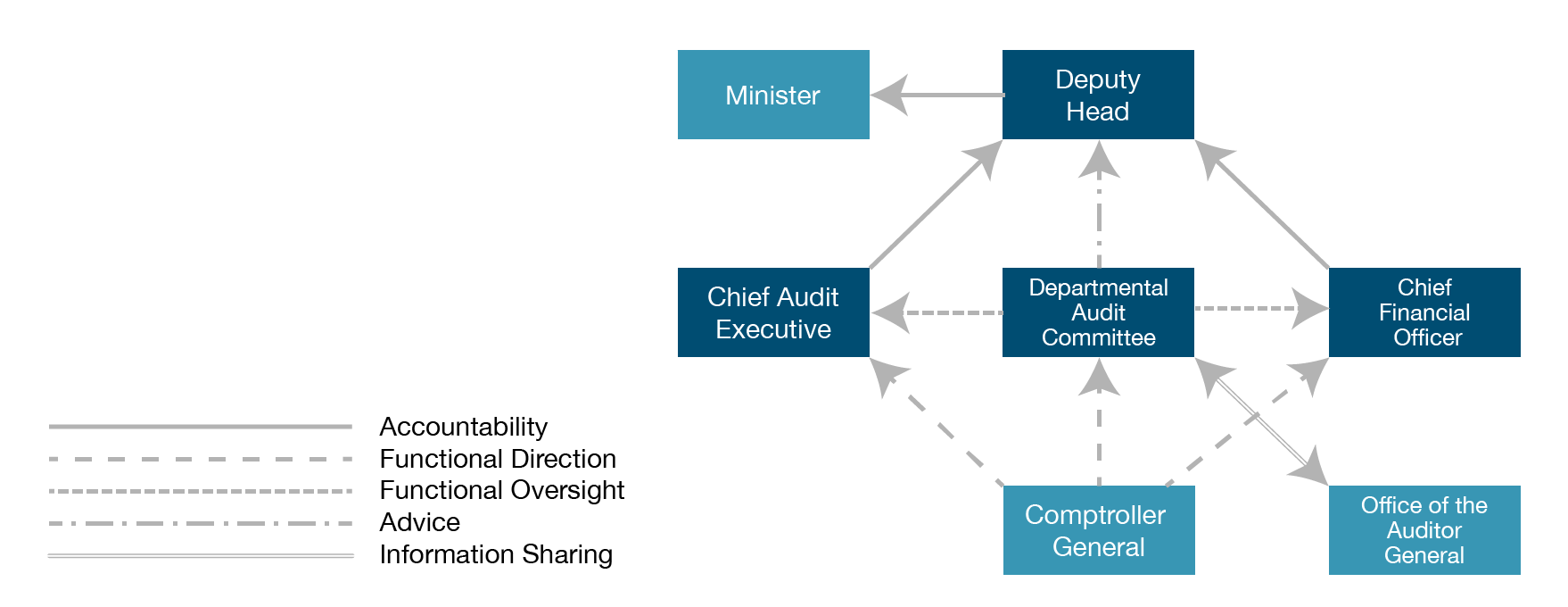

The following diagram illustrates the DAC’s key accountability and reporting relationships.

Figure 1: DAC Accountability Relationship - Text version

The DAC’s accountability relationship to the deputy head fits within broader departmental relationships and accountabilities as follows:

- The Departmental Audit Committee provides advice to the deputy head, functional oversight to the Chief Audit Executive and the Chief Financial Officer.

- The Chief Audit executive and the Chief Financial Officer are accountable to the deputy head.

- The deputy head is accountable to the Minister.

- The Comptroller General provides functional direction to the Departmental Audit Committee, the Chief Audit Executive and the Chief Financial Officer.

- The Office of the Auditor General and the Departmental Audit Committee share information.

1.3 Authority

While the DAC plays an important role in providing the deputy head with independent advice, it does not have approval authority, and its role does not include managing internal audit activities for the department nor directing departmental staff.

Within the same context, the DAC chair has no authority over DAC members or the CAE. The role involves additional responsibilities aimed at ensuring that established committee procedures are respected and that expectations for the DAC are met.

1.4 Knowledge of business and relationship with management

The importance of orienting DAC members to their roles is especially critical. Upon joining a DAC, external members should be briefed by management on the expectations for the DAC and on the department’s business through presentations and discussions, and, where appropriate, through site visits. In addition, sessions orienting the DAC to public service governance and the machinery of government are offered annually.

It is important that DAC members continue to increase their understanding of the department’s business throughout their tenure, particularly in the areas of the business that are undergoing significant change. To this end, members should discuss their information needs with the CAE and arrive at an effective system of briefings to stay current on important departmental developments. This may be done through a variety of technologically enabled communications channels and methods, as well as through discussions with management. Important to note that DAC members should only be meeting with the organization’s executive team as part of regular DAC meetings.

Strong, open relationships between the DAC and management with respect to these responsibilities are also critical to the committee’s success. Of particular importance is the relationship and dialogue between the DAC chair and the deputy head. This interaction should be marked by its candour so that discussions of risk exposures and areas for improvement are unambiguous and focus on opportunities for effective mediation.

Open communication with the CAE and the chief financial officer is essential in building effective relationships with the management team and in bolstering knowledge of departmental operations. The DAC may also want to invite a member of the executive team and/or members of the internal audit team to attend DAC meetings as observers, perhaps on a rotating basis. This participation can be a valuable learning opportunity for observers to strengthen their understanding of the DAC and its work while at the same time increasing awareness of the DAC mandate and operations in the department.

The OCG hosts an annual DAC symposium where current issues and relevant topics are presented and discussed. This event is widely recognized as an important opportunity for members to learn and share.

1.5 Comparison of a DAC to a private sector audit committee

The role of the DAC is different from that of an audit committee in the private sector.

In the private sector, the board of directors is responsible for governing the organization and has the full authority to do so. According to the glossary of the Internal Audit Standards, “the board” is defined as the highest-level body responsible for governance such as:

- a board of directors

- an audit committee

- a board of governors or trustees

- a group of elected officials or political appointees

- any other body with authority over relevant governance functions

Audit committees are a sub‑committee of the board of directors. The board nominates members for appointment and delegates authority to the audit committee for financial oversight. The audit committee has a fiduciary role in helping the board fulfill its governance and oversight responsibilities in the areas of financial management and reporting, risk management, control assessment, external auditors, and the effective use of internal auditing. The audit committee also has the responsibility to review and recommend to the board the approval of the audited financial statements of the organization.

In contrast, in the Government of Canada and for departments under section 6.1 of the Policy on Internal Audit, the “Board” is interpreted to be the deputy head, given their role as the highest-level governance body. While the Departmental Audit Committee plays an important role in providing independent advice to the deputy head, they do not have approval authority.

Furthermore, individual departments in the Canadian government generally do not produce their own audited financial statements. Instead, departmental financial results are consolidated into the public accounts and audited by the Auditor General of Canada. Therefore, DAC members’ responsibility over financial matters is limited to reviewing and providing advice to the deputy head on the key financial management reports and disclosures of the department.

Unlike other sectors, DACs in the federal government are strictly advisory and not a part of the governance structure of federal departments. DACs are appointed by the Treasury Board on the recommendation of the President of the Treasury Board. DAC members have no authority to make decisions or to direct the activities of public servants. Their role is to advise the deputy head on the key areas of responsibility as defined by the Comptroller General of Canada.

1.6 Membership

As set out in the Treasury Board Policy on Internal Audit and Directive on Internal Audit, the DAC must have a majority of independent, external members who do not hold a position in the federal public administration. The membership is to reflect Canada’s diversity in terms of gender, official languages, Indigenous, minority groups and regional representation.

The Directive on Internal Audit states that Committee members are to be familiar with financial reporting or become familiar with such reporting within the first year of their appointment. In order to support good governance practices across the committee, section B.1.2.3 of the Directive stipulates that at least one external member is to be a financial expert (FE) holding a professional accounting designation in good standing. On an exceptional basis, the Comptroller General may grant an exception to the requirement for the financial expert to hold a valid professional accounting designation.

External members are jointly selected by the deputy head and the Comptroller General of Canada for approval by the Treasury Board. The collective skills, knowledge and experience of the members are to enable the committee to undertake its duties competently and efficiently. DAC membership from within the federal public administration is to be limited to individuals at the level of deputy head unless an exception is granted by the Comptroller General of Canada.

Although they are not members of the committee, by virtue of their central roles in the department, the chief financial officer and the CAE are expected to attend all committee meetings. As necessary, the chair may also request other departmental officials and representatives from the Office of the Auditor General (OAG) and the Treasury Board of Canada Secretariat (TBS) to attend.

2. Functioning of a Departmental Audit Committee

In this section

2.1 Charter or terms of reference

The DAC is expected to document its roles and responsibilities in a charter or terms of reference. The DAC’s roles and responsibilities should be consistent with Treasury Board policies and guidance, while recognizing that the committee may be requested to provide advice in additional related areas where the deputy head feels they can benefit from the DAC’s counsel.

The charter or terms of reference must be approved by the deputy head and reviewed periodically. Changes to relevant policies and standards should be factored into the process for reviewing and updating the charter or terms of reference.

The DAC charter may indicate a continued requirement to provide advice in areas that may no longer be required by policy but where the deputy head feels the DAC can continue to add value. For example, the DAC may be requested to review and provide advice on departmental accountability reports or financial reports prior to their finalization even though this is no longer a policy requirement.

2.2 Annual plan

To ensure the fulfillment of its responsibilities, the DAC is expected to prepare an annual plan for the deputy head’s approval. DAC members and the deputy head should be actively engaged in this process. The annual plan will help the DAC use a risk-based approach to reviewing the core areas of responsibility as well as scheduling any additional areas where the deputy head wants the DAC to provide strategic advice. DAC members may want to review pertinent elements of this Guidebook, either individually or as a committee, when developing the annual plan.

Recognizing that not all core areas of responsibility may be covered in a single year, the DAC may find it beneficial to have the plan cover a two-year horizon.

2.3 Meetings

Meetings are a main working forum for the committee, and members should participate actively. Meetings provide an opportunity to review information, identify and discuss important issues, and develop informed judgments. The usefulness of meetings and the DAC’s overall effectiveness depend on members’ thorough preparation beforehand and their willingness to discuss key issues at meetings.

The number of meetings each year largely depends on the extent and nature of the DAC’s work. On average, DACs meet three to four times per year. The committee may find it beneficial to use teleconferencing and/or video conferencing as a means to carry out DAC business where there is important, time-sensitive work to be done but the nature or volume of it does not warrant an in-person meeting. For example, a DAC meeting may be held via teleconference to review and provide advice on the department’s financial statements, including any associated auditor’s report.

In camera discussions should be a regular and integral part of each DAC meeting. The committee should meet separately in camera with the CAE, the chief financial officer and the external auditor, when in attendance. A good practice is for the external DAC members themselves to meet in camera, either before the meeting, as part of the agenda, or both.

It is the chair’s responsibility to include these in camera discussions at every DAC meeting and to ensure that sufficient time is set aside for them. Regularly scheduling such meetings provides an excellent opportunity for the DAC and key stakeholders to communicate privately and candidly.

2.4 Expectations of the DAC

As previously noted, in fulfilling its responsibilities, it is expected that the DAC will exercise due diligence, provide constructive challenge in its work and maintain independence from line management.

2.4.1 Expectations of the DAC chair

The chair of the DAC is to be from outside the federal public administration (unless an exception is granted by the Comptroller General of Canada). Exceptions exist primarily to address sudden vacancies or delays in the Treasury Board appointment process. The position holds no authority beyond the functioning of the committee.

The expectations of the DAC chair include, but are not limited to, the following:

- Prepare a DAC annual plan: In consultation with the DAC members and the CAE, prepare the annual plan, to be presented to the deputy head for approval. The chair should ensure that the DAC’s areas of responsibilities are fully addressed, including any additional areas found in the DAC charter or where the deputy head is seeking strategic advice.

- Oversee preparations for DAC meetings: This includes the following:

- leading the development of the agenda, which includes in camera sessions as part of each meeting, in consultation with the deputy head

- influencing the timely distribution of pre-meeting materials, which facilitates the DAC’s ability to prepare for the meeting

- meeting informally with members before the meeting if necessary

- encouraging and supporting DAC members’ attendance at all DAC meetings

- recommending the general nature and length of presentations

- Chair DAC meetings: The chair is responsible for:

- facilitating discussion among DAC members and management in accordance with the DAC annual plan

- leading discussions in a manner that reinforces reasonable expectations of DAC members

- encouraging meaningful and respectful participation in keeping with the principles of inclusive leadership, including ensuring that all DAC members who want to address a matter are provided with the opportunity to do so

- leading discussions among members as to whether sufficient information or material has been provided to inform DAC deliberations or decisions

- attempting to achieve consensus where members express conflicting positions, views or advice

- as appropriate, inviting representatives from external assurance providers to attend committee meetings to discuss the plans, findings and other matters of mutual concern

- Lead the DAC’s self-assessment process: The chair should champion and manage the development of the DAC’s annual self-assessment process to support open and frank discussions on the committee’s performance, and in support of continuous improvement.

- Support a positive DAC culture: A positive DAC culture is nurtured by the DAC chair and is characterized by the following:

- DAC’s acceptance of its responsibilities and mandate

- DAC’s willingness and capacity to exert a healthy challenge function

- respect and trust among DAC members and management

- welcoming a diversity of opinions and perspectives, including acceptance of the right of each DAC member to hold and express dissenting opinions

- a positive atmosphere favourable to collaboration and progress toward the achievement of departmental objectives

- a genuine commitment to good governance practices on the part of DAC members

- a willingness to act as a team

2.4.2 Expectations of DAC members

In discharging their responsibilities, DAC members are each expected to:

- be familiar with those sections of the Treasury Board Policy on Internal Audit relevant to their work

- know, respect and comply with the Terms and Conditions of Appointment for Audit Committee Members

- be familiar with the scope of internal audit and the limits of its purview

- be aware at all times of the implications of taking on activities that could pose potential eligibility concerns,Footnote 4 mindful of the fact that the Financial Administration Act prohibits DAC members from occupying positions in the federal public administration

- attend all DAC meetings and provide adequate advance warning to departments should attendance not be possible

- be prepared for DAC meetings by reviewing information, reports and background material provided in advance of each meeting

- ask probing questions and expect, encourage and elicit reasonable answers

- encourage a culture of open, candid, respectful and direct communication between management and the committee

- provide sound advice while respecting management’s authority to make decisions

- help the deputy head prepare for being held to public account by periodically subjecting the deputy head’s executive decisions to constructive challenge and by encouraging the deputy head to demonstrate that the best possible decisions have been made in light of all available information and evidence

- provide timesheets and expense claims in a timely manner to meet proactive disclosure timelines

2.5 Support from the department

To perform its work, the DAC requires the support and cooperation of the department’s management. The committee depends on management for information, reports, knowledge and insight about the department’s practices and the issues it faces. There is no set model for the provision of this support. Nor is there a set lead within departments for the provision of this support. In some departments, it is provided by the corporate secretariat; in others, it is provided by the internal audit function. Where support is provided by internal audit, the CAE should keep the DAC secretariat separate from the other internal audit business to maintain the internal audit function’s actual and perceived independence and objectivity.

Support provided to the DAC can cover many activities, including administrative, strategic and logistical support. This could include:

- booking meeting rooms and travel arrangements

- processing proactive disclosure of DAC members’ expenditures

- identifying issues

- preparing reports and charters

- researching topics

- liaising with management

Departments should provide updates on ongoing matters of importance to the DAC and relay key communications from the OCG. The department should also support the external members in developing a sound understanding of their role and responsibilities and those of the department, and in complying with their Terms and Conditions of Appointment. This Guidebook can also be used by the department to support the DAC, particularly by those providing secretariat support. In addition, this Guidebook may be shared with the chief financial officer, whose presence is required at every DAC meeting.

Appendix A describes examples of the kind of support and assistance departments should consider providing to DACs. A sample table of contents for a DAC orientation/reference binder is included as Appendix B.

2.6 Self-assessment

While considered a good practice, there is no requirement from the OCG for DACs to submit an annual report. The decision whether to adopt the practice will be made by the deputy head and will depend on a number of factors that determine the relative value derived by developing this report.

A formal, external assessment of the DAC’s performance is part of the external assessment of the internal audit function to be carried out every five years. The DAC should also undertake a periodic self-assessment of its own performance.

Self-assessments help ensure that the DAC delivers on its charter or terms of reference and continually enhances its value to the deputy head. Self-assessment can take many different forms, involve several participants and use diverse techniques. The key to successful self-assessments is a willingness to actively seek out opportunities to improve performance and recognition of the importance of acting on the results. Management should not hesitate to use the self-assessment as a basis to assess DAC performance and determine whether the DAC is adding value.

The format of the self-assessment is up to the department. Appendix C contains a sample DAC self-assessment questionnaire, which sets out the kinds of questions that can help members gain insight into the DAC’s performance.

To obtain more comprehensive insight into the DAC’s performance, value and opportunities for improvement, consideration should be given to including attendees at DAC meetings as well as members of management who have extensive interactions with the committee in the self-assessment process.

Regardless of the tool used, the critical element is the dialogue and discussion at the DAC with regard to the results so as to identify and effectively address any noted areas for improvement in a timely manner.

2.7 Conflict of interest

The search for subject matter experts on a DAC can result in the consideration of candidates who are active in a departments’ sector of operations. When recruiting, departments should consider whether the benefits of appointing a subject matter expert on the audit committee outweighs the risks of the emergence of a real, apparent or potential conflict of interest. Conflicts of interest do not relate exclusively to matters concerning financial transactions or the transfer of economic benefit; any area of activities can have a negative impact on the perceived objectivity of the appointee. Each situation must be assessed on a case-by-case basis. Details on DAC’s responsibility when it comes to conflict of interest can be found in the DAC “Guidance on Conflict of Interest and Disclosure Requirements.”

3. Aides-mémoire

In this section

- 3.1 Values and Ethics aide-mémoire

- 3.2 Risk management aide-mémoire

- 3.3 Management control framework aide-mémoire

- 3.4 Internal audit function aide-mémoire

- 3.5 External assurance providers aide-mémoire

- 3.6 Follow-up on management action plans aide-mémoire

- 3.7 Financial statements and Public Accounts reporting aide-mémoire

- 3.8 Accountability reporting aide-mémoire

- 3.9 Large transformation initiatives aide-mémoire (supplemental)

This section contains eight aides-mémoire, one for each of the DAC’s eight core areas of responsibility:

- 3.1 Values and ethics

- 3.2 Risk management

- 3.3 Management control framework

- 3.4 Internal audit function

- 3.5 External assurance providers

- 3.6 Follow-up on management action plans

- 3.7 Financial statements and public accounts reporting

- 3.8 Accountability reporting

- 3.9 Supplementary aide-mémoire: Large transformational initiatives

The specifics of each of these core areas may vary due to changes in Treasury Board policy and the department’s specific needs. For this reason, each aide-mémoire should be reviewed in the context of the DAC’s charter or terms of reference.

These interrelated aides-mémoire are intended to support the DAC as a whole, and members individually, in performing their due diligence. Each aide‑mémoire includes a series of prompts or questions that individual members can ask themselves and/or management when reviewing materials, reports and information provided to the committee.

There is no requirement for the DAC to use these aides-mémoire and, if employed, no requirement to use the entire list of questions where the risk is not assessed as significant. However, they can help stimulate meaningful discussion in each of the DAC’s key areas of responsibility. They are not an exhaustive list and should also help DAC members ask the necessary probing questions and consider the reasonableness of responses with greater knowledge and understanding.

In addition to a set of questions, each aide-mémoire provides a list of guidance material that is pertinent to the particular subject matter. Departments should make this guidance available to DAC members as requested or required.

3.1 Values and Ethics aide-mémoire

This aide-mémoire is designed to help DAC members consider values and ethics when reviewing materials, participating in discussions or receiving presentations from senior management.

Overview of DAC responsibilities

Specific DAC responsibilities in this area are expected to be outlined in the department’s DAC charter or terms of reference. In general, it is expected that the DAC’s work will include reviewing and advising the deputy head on departmental systems and practices established to monitor compliance with laws, regulations, policies and standards of ethical conduct, and identify and deal with any legal or ethical violations. It may also include the procedures and feedback mechanisms established to monitor conformance with its code of conduct and ethics policies, as well as how its processes encourage and maintain high ethical standards.

Pertinent government policies and related guidance

- Government of Canada web page on values and ethics of the public service

- Values and Ethics Code for the Public Sector

- Treasury Board Directive on Conflict of Interest

- Public Servants Disclosure Protection Act

- Criminal Code, Part IV

- Department-specific values and ethics code and related guidance

Leadership and people management

- What support does the deputy head provide to set the required “tone from the top” for the department’s ethics program?

- How does the department ensure that its leadership and management practices reflect public service values and ethics?

- Does the department have a senior official for values and ethics?

- Does the department have a senior official to receive and investigate disclosures of wrongdoing, including alleged instances of harassment and breaches of the values and ethics code?

- Is the quality of values and ethics leadership regularly assessed internally and externally?

- Is performance information on public service values and ethics, including people management, integrated into hiring, promotion and performance management?

- What processes or structures does the department have in place to ensure active values and ethics dialogue among senior management?

- What are the results of the Public Service Employee Survey and management’s plans to address noted issues? How does the department ensure employees remain engaged between survey cycles?

Departmental culture

- How does the department maintain an ongoing dialogue on public service values and ethics relevant to the specific departmental challenges?

- How does the department ensure that values and ethics are embedded in what staff do every day?

- Is there value in carrying out a review or audit of departmental culture?

Policies and guidelines

- Does the department have its own values and ethics code consistent with the Values and Ethics Code for the Public Sector and the Treasury Board Directive on Conflict of Interest?

- If so:

- does it clearly state acceptable and unacceptable behaviour, particularly in areas of significant ethical risk?

- does it identify which departmental programs and functions may be of highest risk for conflicts of interest?

- How does the department communicate its own values and ethics code and the Values and Ethics Code for the Public Sector to staff to ensure that they understand their responsibilities, the expectations of them regarding ethical behaviour and the consequences of non-compliance?

- How does the department communicate recourse and disclosure mechanisms to staff?

- How does the department ensure that employees are aware of its disclosure procedures and are encouraged to expose wrongdoing without fear of reprisal? In other words, how does the department ensure a safe environment?

- How does the department ensure that public servants intending to leave the public service are aware of the post-employment obligations of the departmental code and the Values and Ethics Code for the Public Sector?

Values and ethics program

- Does the department have a values and ethics program in place?

- If so, is there a plan in place that sets out the expected benefits, results and performance measures of this program, including the applicable sections of the Public Servants Disclosure Protection Act?

- How do employees obtain advice when facing difficult ethical decisions?

- How does the department identify, assess and manage values and ethics risks, including the risk of fraud?

- How does the department investigate complaints of wrongdoing, harassment and conflicts of interest?

- What are the processes and mechanisms in place to ensure that investigations proceed promptly, fairly and objectively, with due regard for confidentiality?

- What procedures and mechanisms does the department have in place to establish, promote and manage disclosures made under the Public Servants Disclosure Protection Act, as it applies to the department?

- How does the deputy head ensure:

- the confidentiality of those involved in the disclosure process?

- the security of information collected through disclosures?

- prompt public access to information if wrongdoing as described by the Act is found?

Values and ethics learning

- What training on the Values and Ethics Code for the Public Sector and on recourse and disclosure do new and existing employees and managers receive? Is this training mandatory? Is it provided on an ongoing basis?

- How frequently are training materials updated to ensure that they maintain their relevance and appeal?

- How does the department measure the effectiveness of its values and ethics learning activities?

- What other mechanisms or approaches are in place to share lessons learned and best practices, e.g., sharing examples of ethical dilemmas and how they were handled?

Values and ethics monitoring and reporting

- How does the department monitor compliance with its own code and the Values and Ethics Code for the Public Sector?

- How does the department measure and report on employees’ and managers’ understanding of the Values and Ethics Code for the Public Sectorand their confidence in the department’s recourse and disclosure mechanisms?

- How does the deputy head know that behaviour throughout the department is consistent with the expectations and standards of the department’s code and the Values and Ethics Code for the Public Sector?

- What role does internal audit play in providing assurance on values and ethics, including departmental compliance with the department’s code, the Values and Ethics Code for the Public Sector and relevant sections of the Public Servants Disclosure Protection Act?

- How are unlawful activities (known or potential) reported in the department and to whom?

- What reports does the deputy head receive on ethics concerns or investigations, including findings and recommended actions?

- What processes are in place to monitor the implementation of required actions to ensure that they are implemented on a timely basis and address the reported findings?

3.2 Risk management aide-mémoire

This aide-mémoire is designed to help DAC members consider risk management when reviewing materials, participating in discussions or receiving presentations from senior management.

Overview of DAC responsibilities

Specific DAC responsibilities in this area are expected to be outlined in the department’s DAC charter or terms of reference. In general, it is expected that the DAC’s work focuses prominently on reviewing and advising the deputy head on the department’s risk management arrangements.

Pertinent government policies and related guidance

- Treasury Board of Canada Secretariat risk management web page

- Framework for the Management of Risk

- Guide to Integrated Risk Management

- The department’s own risk management policy and guidance

Risk management responsibility

- Is there a senior management risk champion (assistant deputy minister level or above) who is responsible for the department’s risk management framework and related activities and corporate risk profile?

- How is the champion held to account for their risk management responsibilities?

- Is it clear that senior managers are responsible for managing and mitigating risks in their programs, functions and areas?

Risk management Strategy

- Does the department have a risk management policy or framework?

- If so, does this policy or framework:

- establish an approach for integrating risk management into the department’s decision-making processes?

- link with the entity’s strategic documents (i.e., accountability reports to Parliament)?

- reflect departmental roles and responsibilities for implementing and practising risk management?

- include reporting and monitoring requirements to ensure compliance with the risk management policy or framework?

- What are the key elements of the department’s risk management approach? Does it include an annual risk assessment that includes an assessment of:

- the risk of fraud?

- information technology risks, including data integrity, infrastructure, capacity and cybersecurity risks?

- physical security risks?

- risks associated with major IT-enabled and non-IT projects?

- business continuity planning and disaster recovery planning?

- risks with respect to all significant departmental changes, projects and programs?

- How is staff informed of the department’s approach to risk management?

Corporate risk profile

- Does the department have a current corporate risk profile approved by senior management?

- If so, does this profile:

- identify the department’s key strategic risks?

- include an assessment of the key risks identified?

- reflect the risk tolerance of key clients and other stakeholders?

- outline the strategies to mitigate or manage key strategic risks?

- How does the department identify and assess strategic and business risks?

- How does the department identify and assess new and emerging risks?

- What controls are in place to manage or mitigate the highest inherent risks? (See subsection 3.3 for the aide-mémoire on management control frameworks.)

- How has management determined the opportunities for innovation and experimentation? How are the associated risks identified, assessed and prioritized? Is the associated risk tolerance discussed and incorporated into risk mitigation plans?

- How is the corporate risk profile communicated across the department?

- How does the department identify and assess strategic and business risks?

- How does the department identify and assess new and emerging risks?

- What controls are in place to manage or mitigate the highest inherent risks? (See subsection 3.3 for the aide-mémoire on management control frameworks.)

- What processes are in place to ensure that risk management strategies outlined in the profile are implemented?

- How often does management review and update its corporate risk profile?

Fraud risk management

- What mechanisms does the department have in place to manage the risk of fraud, recognizing that it can result in a loss of public money or property, hurt employee morale and can undermine Canadians’ confidence in public services?

- Has the department undertaken a fraud risk assessment? If not, why not?

Integrated risk management

- What role does internal audit play in helping manage the risk of fraud?

- How are risk management practices integrated into the management of programs throughout the department?

- How is risk management aligned with the department’s expected results and performance measurement practices?

- How is risk integrated into the department’s key business planning and decision-making processes?

- How does the department demonstrate that it is performing in accordance with the approved business plan and within risk tolerance limits?

Continuous risk management learning

- What risk management training, including training to mitigate risk, does staff receive?

- To what extent does management review lessons learned from major departmental events, surprises and disasters and how it has responded to these occurrences?

- How are lessons learned and best practices communicated across the department?

- How are lessons learned and best practices built into risk management practices?

Risk management reporting and monitoring

- How are risk or control failures escalated within the department (e.g., risk and incident reporting and tracking)? To whom and through what mechanisms are they reported?

- To what extent does senior management receive reports throughout the year on risk management plans and take corrective action as required?

- What reports or information does the deputy head receive on departmental risk management?

- What role does internal audit play in providing assurance on risk management practices, key risks and/or controls mitigating the highest inherent risks?

- Is risk management monitored and discussed regularly at senior governance committees? If so, how?

3.3 Management control framework aide-mémoire

This aide-mémoire is designed to help DAC members consider the department’s management control framework when reviewing materials, participating in discussions or receiving presentations from senior management.

Overview of DAC responsibilities

Specific DAC responsibilities in this area are expected to be outlined in the DAC charter or terms of reference. In general, it is expected that the DAC’s work will include reviewing and advising the deputy head on the departmental internal control arrangements, and that its work will be informed on all significant matters that arise from the work performed by others who provide assurances to senior management and the deputy head.

The DAC should understand the level of comfort that the deputy head has with regard to their responsibilities under subsection 16.4 of the Financial Administration Act to maintain effective systems of internal control in the department and whether that comfort is justified.

Pertinent government policies and related guidance

- Treasury Board Policy on Financial Management

- Treasury Board Guide to Internal Controls Over Financial Management

- Treasury Board Policy on Results

- Management Accountability Framework: methodology and findings

- Financial Administration Act

- Department-specific management and internal control policy or framework

Management controls: roles and responsibility

- Is it clearly articulated and understood that the deputy head has overall responsibility for the department’s systems of internal control?Footnote 5

- Is it clearly articulated and understood that management has a fundamental responsibility to identify, document and monitor controls?

- Does the department have a chief results officer and, if so, is that position at an appropriate level?

- Are delegations of authority and responsibility to individuals documented, properly approved and kept up to date?

- Are delegations of authority communicated to all departmental staff?

Management controls: control framework and departmental systems

- Does the department have a control framework that:

- includes, but is broader than, internal controls over financial reporting?

- reflects the department’s key controls to ensure sound management practices, consistent with the Treasury Board Management Accountability Framework and Treasury Board policies and legislative requirements?

- reflects other key controls that help mitigate the department’s key strategic and business risks?

- reflects financial management controls, including controls with respect to budgeting, forecasting and costing?

- includes controls to support the management of large departmental projects?

- is aligned with the department’s results framework?

- explicitly supports departmental innovation and experimentation, including learning from experimentation?

- reflects departmental roles and responsibilities for developing, reviewing, implementing and sustaining key controls?

- includes reporting and monitoring requirements to ensure compliance with this framework?

- If the system of internal controls is lacking in key elements, what is the department’s strategy for developing a sound management control framework in support of the ongoing effectiveness of internal controls across the department, including financial management processes and practices?

- How does management identify and implement required controls necessary to mitigate, manage and monitor new or emerging risks?

- How does the department identify and implement management controls in support of innovation and experimentation?

- How is staff informed of the department’s control framework and held to account for ensuring sound controls in their area?

- Does management review the Annex to the financial statements of common service providers to identify any control issues with respect to the related services provided?

- Are processes in place to review and strengthen the adequacy of internal controls for significant new departmental systems, business transformation projects or programs?

- What training in management or internal controls do employees receive?

Management controls: project management

- What major projects (i.e., transformation, modernization, information technology, program delivery) does the department have planned or underway? Are they reflected in the Departmental Plan and the investment plan? Are they aligned with the Government of Canada Digital Ambition? (See section 3.9: Large transformation initiatives aide-mémoire (supplemental).)

- For projects that cut across multiple departments:

- how are client/recipient departments engaged throughout the project?

- what is the status of the project (i.e., on track, on time, notable issues identified and managed)?

- what is internal audit’s role? If not playing a role, why not?

- For major projects, is the following clear and sufficiently robust:

- governance structures, including performance expectations, monitoring, challenge function, oversight and reporting?

- project scope, timing and milestones, roles and responsibilities, linkages within the department and with other departments?

- key risks and how they are being managed or mitigated?

- How are lessons learned from major government or departmental projects used to strengthen the management of future projects?

Management controls: control certifications

- As part of the financial statements, does the department produce a Statement of Management Responsibility Including Internal Control over Financial Reporting each year that is signed off by the deputy head and chief financial officer (CFO)?

- If so, what evidence underpins this statement?

- Do assistant deputy ministers or their equivalents provide the deputy head and/or CFO with internal control certifications?

- If so, how often are they provided, and what evidence underpins these certifications?

Reporting and monitoring of controls

- How are risk or control failures escalated within the department?

- How are required changes to the design or implementation of key controls identified and implemented in a timely manner?

- What performance information does each level of management receive, and how often, that compares actual performance against budget and performance targets?

- In addition to the control certifications, what arrangements are in place to periodically assess the effectiveness of the department’s control framework (e.g., internal audits, management review and signoffs)?

- How does management report the detection of fraud to the deputy head and the DAC?

3.4 Internal audit function aide-mémoire

This aide-mémoire is designed to help DAC members consider the department’s internal audit function when reviewing materials, participating in discussions or receiving presentations. Given the DAC’s independence from line management and responsibilities in this area, the DAC is well positioned to influence the professionalism, quality, performance and capacity of the internal audit function and provide the deputy head with advice on addressing areas of concern. This aide-mémoire provides questions for consideration to assist the DAC in this work.

Overview of DAC responsibilities

The specific DAC responsibilities in this area are expected to be outlined in the department’s DAC charter or terms of reference. The DAC should be able to reasonably determine if the deputy head is meeting the requirement of subsection 16.1 of the Financial Administration Act to ensure “an internal audit capacity appropriate to the needs of the department.”

In general, it is expected that the DAC’s work will include reviewing and advising the deputy head on:

- the department’s internal audit policy or charter

- the sufficiency of internal audit resources

- the quality and substance of the department’s Risk-Based Internal Audit Plan and progress against the plan

- internal audit reports

- the performance of the internal audit function (including the results of external practice assessments and ongoing and periodic internal assessments)

- the recruitment, qualifications and performance of the CAE

It is also generally expected that DAC members would be informed of any internal audit engagements or tasks that do not result in a report to the DAC, including all matters of significance arising from such work.

Pertinent government policies and related guidance

- Section 16 of the Financial Administration Act

- Treasury Board Policy on Internal Audit

- Treasury Board Directive on Internal Audit

- International Professional Practices Framework (The Institute of Internal Auditors)

- Treasury Board of Canada Secretariat frameworksfor oversight of internal audit

Internal audit policy or charter

- Does the department have an internal audit policy or charter?

- If so, does this policy or charter:

- reflect the purpose, authority and responsibility of the internal audit function?

- align with the OCG’s Value Proposition and Attributes of an Ideal Internal Audit Function?

- reflect the primary focus on the provision of assurance services to the department?

- describe non-assurance services provided (i.e., advisory, consulting)?

- have periodic reviews and revision, as required?

Independence and objectivity

- Does the CAE report directly to the deputy head? If not, why not?

- Does the CAE have the necessary certification or designation for the position? If not, does the CAE possess an acceptable combination of education, training and/or experience as determined by the Comptroller General for this particular case?

- Is internal audit free from interference in determining the scope of internal auditing, performing the work and communicating the results?

- Does the CAE have responsibility for functions other than audit? If so, how is independence assured? If so, do these other duties impede the ability of the CAE to meet their responsibilities under the policy and the Institute of Internal Auditors Standards (the Standards)?

- Is the CAE a member of the senior executive table while still maintaining their independence? If not, why not?

- Does internal audit have unencumbered access to all departmental information, records and locations as required?

- Does internal audit receive the necessary cooperation and assistance from departmental staff and management?

Internal audit planning

- What is the process for developing the Risk-Based Internal Audit Plan (RBAP)?

- Does the RBAP conform to the Standards according to OCG maturity models and/or assessment tools?

- Does the RBAP comply with the requirements of the Policy on Internal Audit?

- Is the RBAP risk assessment process thorough, documented and clear to the DAC?

- How does the RBAP link with the department’s corporate risk profile and key strategic and operational risks?

- Have departmental objectives and risks with respect to innovation and experimentation been considered in the development of the RBAP?

- Have fraud risks been considered in the development of the RBAP, as well as the planning for individual internal audit projects or major transformation projects?

- Has internal audit considered major capital projects in the development of the RBAP? If not, why not?

- How does the RBAP align with the department’s Evaluation Plan? How are these functions aligned, and are there opportunities for joint work?

- How are the proposed audit projects determined and prioritized (i.e., are they linked to the department’s risk management strategy or to internal audit’s own risk assessment process)?

- Where the plan includes advisory services, does the internal audit team have the necessary expertise and capacity in place to deliver these services? Are advisory engagements conducted according to the Standards?

- Does the plan adequately detail the objectives, scope, timing and resource requirements (dollars and staffing resources) for each of the proposed projects?

- Does the RBAP make appropriate provision for the work of external assurance providers (i.e., horizontal audit activities to be undertaken by the OCG and engagements by the OAG)?

- Does the RBAP document resources allocated for follow-up on recommendations resulting from internal and external engagements, including management letters and horizontal engagements?

- Does the RBAP reflect the impact of any resource limitations?

Internal audit delivery

- Does the internal audit service delivery modelFootnote 6 meet the department’s needs?

- Where the internal audit delivery is co-sourced, what processes are in place to manage the engagement and ensure compliance with the Institute of Internal Auditors’ International Professional Practices Framework?

- Where an interdepartmental engagement or joint audit and evaluation engagement is conducted, is sufficient background and context provided to the DAC on risk levels, maturity of collaborating functions and any other pertinent information?

Internal audit reports

- Are internal audit reports clear, concise and compelling? Do they satisfactorily address audit objectives?

- Is technology leveraged to support modern, compelling internal audit reporting?

- Do audit reports include a statement of conformance? If not, why not?

- Are internal audit reports issued on a timely basis (i.e., what is the elapsed time from the start of the engagement to issuing the final report)?

- Are the recommendations relevant, practical and achievable?

- Do audit reports include management’s response and action plan to address all agreed-upon recommendations? Does the response and action plan appear to effectively respond to the observations and findings, or the root cause of the problems and issues outlined in the report?

- For interdepartmental or joint engagements, are approvals coordinated to facilitate the publishing of reports and related performance information?

Internal audit capacity and resources

- Does the internal audit team have sufficient resources (full-time equivalents and/or money) to support the deputy head in their legislative responsibilities, including delivering on the approved risk-based internal audit plan (assurance and advisory services, as applicable) and maintaining a quality assurance and improvement program?

- Is there a human resources and learning strategy in place to support the professionalism of the function (i.e., certified internal auditor, chartered professional accountant and other relevant recognized designations) and the needs of the department?

- Does the internal audit team have the necessary complement of required skills and experience to deliver on its RBAP? Does this include a multidisciplinary team that reflects the mandate and risks of the department? If not, what is internal audit’s plan to acquire these skills and expertise?

- Is internal audit able to access specialist skills, where and when required?

Performance of the internal audit function

- Does internal audit have a sound understanding of the department’s business, including key strategic and operational risks?

- Does internal audit have a performance framework, consistent with TBS expectations, to outline, monitor and report on the performance of the function, including results of follow-up on management action plans? Does the framework support innovation and growth of the function?

- To what extent does the internal audit team complete its engagements on time?

- Does internal audit publicly report on its performance? If so, is this report consistent with the OCG performance framework, and is it provided to the deputy head and the DAC and posted on the department’s website?Footnote 7

- Does internal audit have a formal Quality Assurance and Improvement Program (QAIP) in place to ensure that internal audit provides quality and value-added services, and complies with Treasury Board policies and the IIA Standards? Do these processes provide timely feedback on issues or areas of concern?

- Does the audit committee receive a periodic comprehensive briefing on the QAIP, including areas for attention and conformance to the Standards for ongoing monitoring and both internal and external assessments?

- Has the CAE explained to the DAC the implications of not having an appropriate QAIP in terms of policy compliance and standards conformance?

- Has internal audit undergone an independent external quality assessment within expected time frames? If not, why not?

- If so:

- what were the results of the external quality assessment?

- has an action plan been prepared to address noted areas for improvement, and has this report been provided to the DAC?

- are periodic reports provided to the DAC to monitor the implementation of actions flowing from the external quality assessment?

- Does internal audit maintain effective liaison with the OCG, the OAG and other assurance providers and stakeholders, as required?

- Does internal audit provide OCG with required and requested documents and information within deadlines? If not, why not?

- Does internal audit provide the DAC with the department’s results/benchmarks with regard to the OCG internal audit community performance framework (e.g., Capacity Assessment Template, RBAP self-assessment, etc.)?

- Does internal audit have a professional relationship with departmental management?

- How does the function use the information gained from the post-engagement surveys?

3.5 External assurance providers aide-mémoire

This aide-mémoire is designed to help DAC members consider reports of external assurance providers and accompanying materials when participating in discussions or presentations from senior management.

Overview of DAC responsibilities

Specific DAC responsibilities in this area are expected to be outlined in the DAC’s charter or terms of reference. In general, it is expected that the DAC’s work in this area will include being informed of and advising the deputy head on the results of the work of external assurance providers,Footnote 8 and providing advice on audit-related issues or priorities raised by the external assurance providers.

Pertinent government policies and related guidance

The Office of the Auditor General of Canada (OAG) produces functional audit guidance and tools for general application in performance audits, or for use in audits on specialized areas.

Leadership and support

- Is there a senior lead for monitoring and reporting on the work of external assurance providers done in the department, including audits and special reviews?

- Does the department have a designated OAG or external assurance liaison resource? What does the role entail?

- How does the department support external assurance providers undertaking audits and special reviews in the department?

OAG and central agency audits and management improvement initiatives

- What are the processes in place to ensure that management and the DAC is kept up to date on work planned and being carried out by external assurance providers?

- Are audit projects planned by external assurance providers considered and identified in the department’s RBAP?

- What processes are in place to review and develop the necessary management responses to issues raised by external assurance providers?Footnote 9 If there are no such processes, what needs to be put in place to facilitate management responses?

- What processes are in place to review, assess and report on issues and priorities raised by external assurance providers?

- Does the DAC receive external assurance provider reports on a timely basis? If not, what processes are in place to support DAC members in providing the deputy head with advice on management’s response as well as on any noted audit-related issues or priorities?

- What is the process and time frame for monitoring, assessing and briefing the deputy head and the DAC on the departmental impacts of resulting government-wide initiatives to improve management practices?

3.6 Follow-up on management action plans aide-mémoire

This aide-mémoire is designed to help DAC members consider follow-up of management action plans when reviewing materials, participating in discussions or receiving presentations from senior management.

Overview of DAC responsibilities

Specific DAC responsibilities in this critical area of oversight are expected to be outlined in the DAC charter or terms of reference. In general, it is expected that the DAC’s work in this area will include regularly reviewing and advising the deputy head on the progress of implementing approved management action plans resulting from the work of internal audit and external assurance providers.

Pertinent government policies and related guidance

- International Professional Practices Framework (The Institute of Internal Auditors)

- Treasury Board Directive on Internal Audit

Roles and responsibilities

- Is a senior manager identified as being responsible for implementing agreed-upon management action plans articulated in departmental internal audit reports, internal responses to OAG audits or audits from other assurance providers?

- Is it clearly understood that the CAE is responsible for monitoring and following up on management action plans, including plans that result from the work of external assurance providers?

- Is it clearly understood that the CAE is responsible for monitoring and following up on action plans for recommendations resulting from quality assessments?

Monitoring and reporting

- What process and procedures does the CAE have in place for monitoring the implementation of management action plans, including management action plans arising from audits conducted by external assurance providers?

- What methodology and process does the CAE have in place to follow up on whether management actions taken have been effective?

- How often does the CAE report to the deputy head and the DAC on management follow-up?

- What management procedures are in place to ensure timely action on recommendations resulting from audit engagements? For example, are actions for recommendations that are deemed serious or imperative incorporated into the performance agreement of managers of the office of primary interest (OPI)?

- Does a senior management representative from the OPI attend the follow-up segment of the DAC meeting to discuss delays in the implementation of the management action plans?

- What is the nature of the CAE’s reporting to the DAC on management follow-up (i.e., verbal or written report)? Does this report:

- reflect the extent to which management action plans are being implemented within the specified time frame and adequately explain delays and revised time frames for completion?

- indicate the extent to which actions implemented are effective (if actions are not effective, why not)?

- indicate why the CAE believes management has accepted a level of risk that is unacceptable to the department or to the government, if applicable?

- Does the CAE maintain timely reporting of follow-up results for internal audit performance that are made publicly available?

3.7 Financial statements and Public Accounts reporting aide-mémoire

This aide-mémoire is designed to help DAC members consider the departmental financial statements and Public Accounts reporting when reviewing materials, participating in discussions or receiving presentations from senior management.

Overview of DAC responsibilities

Specific DAC responsibilities in this area are expected to be outlined in the DAC’s charter or terms of reference. In general, it is expected that the DAC’s work in this area will include reviewing and, as appropriate, advising the deputy head on key departmental financial reports and disclosures of the department, including quarterly financial reports, annual financial statements and Public Accounts, and the annual Statement of Management Responsibility and associated plans and assessments with respect to internal controls over financial reporting. The DAC is not required to recommend these materials for approval by the deputy head, nor are they expected to participate in their development.

If the financial statements are audited, it is generally expected that the DAC will review the financial statements with the external auditor and senior management, discussing any significant accounting estimates and adjustments, as well as any difficulties or disputes the external auditors encountered with management during the course of the audit. It is also generally expected that the DAC will review any management letters arising from the external audit and the auditor’s findings and recommendations relating to internal controls over financial reporting and consider their impact on departmental governance, risk management and control processes.

Pertinent government policies and related guidance

- Treasury Board Directive on Accounting Standards

- Government of Canada Accounting Handbook (GCAH)

- CPA Canada Public Sector Accounting Standards (PSAS)

- Treasury Board Policy on Financial Management

Accounting policies and practices

- Are the department’s accounting policies and practices consistent with Treasury Board directives and requirements? If not, why not?

- What is the process for obtaining advice for the proper accounting treatment when significant accounting issues arise (e.g., during consultation with the OCG or the OAG)?

- Are the department’s significant accounting policies disclosed in the financial statements, including changes in the accounting policies from the previous year?

- Do the processes that underpin the preparation of the financial statements also support the financial health and financial management of the department

- Has the DAC or management identified other key financial disclosures that members will receive as part of discharging this responsibility?

- Where the DAC receives Quarterly Financial Reports, is sufficient contextual information included, such as risks, significant changes, risks and uncertainties, results, impacts of large transformation initiatives and/or horizontal initiatives? Are year-to-year comparisons discussed?

- Is there sufficient and appropriate context to support the material that is presented (e.g., information on relevant external influences, mandatory templates, departmental or government-wide specific financial practices or protocols not included in Treasury Board policies, etc.)?

Financial statement presentation

- Do the financial statements comply with required Treasury Board accounting standards? If not, why not?

- To what extent are there significant departmental legal matters, contingencies, claims or assessments that could have a material impact on the financial statements (i.e., the departments and/or the government as a whole)? How have these been reflected in the department’s financial statements?

- What are the processes in place to estimate significant accounting accruals, reserves and other estimated liabilities?

- What is the support for significant valuations, assumptions or judgments reflected in the financial statements?

- Do the financial statements reflect any significant or unusual transactions that occurred during the year?

- Have significant financial statement variances from the budget and prior year’s statements been satisfactorily explained?

Review and signoff

- Is there a process in place for the CFO to review the financial statements on a timely basis with the deputy head and with management?

- Is there a process in place to inform the deputy head, senior management and the DAC throughout the year of significant issues that impact or may impact the department’s financial statements?

- Is there a process in place to identify which, if any, of these issues should be communicated to the Comptroller General of Canada?

- Have the deputy head and CFO signed off on or certified the financial statements?

- If not, why not?

- If so, what are the processes in place to support the deputy head and CFO in signing off on or certifying the financial statements (i.e., the key procedures, systems, resources and tasks for the preparation and review of the financial statements to ensure that they do not contain any material errors or omissions)?

Audited financial statements / Public Accounts

- Have the deputy head and CFO signed off on the Management Representation Letter required as part of the audited financial statements?

- If not, why not?

- If so, what are the processes in place to support the deputy head and CFO signoff?

- Were there any breakdowns in controls that impacted the audit of the financial statements or the Public Accounts?

- What adjustments, if any, to the financial statements or the Public Accounts were required as a result of the audit?

- What was the nature of any significant disagreements between management and the external auditors, and to what extent were these disagreements satisfactorily resolved?

- Did the department receive an unmodified audit opinion? If not, what action is being taken to address the reasons for the modified or denied opinion on a timely basis?

3.8 Accountability reporting aide-mémoire

This aide-mémoire is designed to help DAC members consider accountability reporting when reviewing materials, participating in discussions or receiving presentations from senior management.

Overview of DAC responsibilities

Specific DAC responsibilities in this area are expected to be outlined in the DAC’s charter or terms of reference. In general, it is expected that the DAC’s work will include receiving copies of departmental accountability reports (i.e., reports to Parliament). Regardless of the timing and focus of the DAC’s review of actual accountability reports, it is expected that through this area of responsibility or that of the management control framework, the DAC would generally review and comment on their confidence in the underlying processes that support effective accountability reporting, consistent with requirements of the TBS. The committee may also receive plans and reports prepared by the department’s evaluation function for information.

These reports are intended to provide context on departmental operations and oversight. The DAC is not required to recommend these documents for approval by the deputy head, nor is there an expectation that the DAC would be involved in the development of these reports.

Pertinent government policies and related guidance

- Treasury Board Policy on Results

- Treasury Board guidance for accountability reports to Parliament

Process and timing

- Does the DAC receive the accountability reports on a timely basis? If not, why not?

- If the deputy head asks for the DAC’s advice on a draft accountability report to Parliament, is there a process in place to facilitate members’ review of the report electronically, recognizing the tight time frame for the reports’ preparation, review and approval?

Presentation and linkage between accountability reports

- Do the accountability reports to Parliament include key performance measures and targets that are clearly linked to expected outcomes such that the reader understands the basis upon which performance will be assessed?

- Is performance information provided in the year-end results report to Parliament consistent with the performance metrics and targets outlined in the department’s results reporting instruments and the departmental plan reported to Parliament, together with explanations for significant changes or variances?

- Is there a discussion of the results the department seeks to achieve and does achieve, and the resources used to achieve them?

- What processes and procedures ensure the completeness and reliability of the performance information contained in the department’s accountability reports?

- Are the accountability reports to Parliament clear, straightforward and easy to understand?

- Do the accountability reports to Parliament include a brief explanation as to why the reader can have confidence in the methodology and data used to substantiate the department’s plans and performance?

- Does the narrative in the planning report to Parliament clearly identify the expected results, departmental priorities aligned with those of the government, and the progress the department intends to make toward its strategic outcomes?

Review and certification

- What is the underlying process and support for the Management Representation Letter signed by the deputy head (i.e., to ensure that the representations made contain no material misstatements)?

3.9 Large transformation initiatives aide-mémoire (supplemental)

This aide-mémoire is designed to help DAC members exercise their challenge function when reviewing materials, participating in discussions or receiving presentations from senior management regarding large change management initiatives or horizontal projects.

Overview of DAC responsibilities