Application guidelines - Canadian Film or Video Production Tax Credit (CPTC)

Canadian Audio-Visual Certification Office (CAVCO)

Published March 3, 2020

| Date | Change | Location |

|---|---|---|

| August 13, 2025 |

|

|

| February 13, 2025 |

|

|

|

|

|

|

|

|

| February 20, 2023 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

This set of updates also includes other minor edits to improve clarity and readability, and that do not result in any substantive modifications to program requirements. |

|

|

| October 27, 2021 |

|

|

| October 10, 2021 |

|

|

On this page

- Overview

- 1. Administration of the CPTC Program

- 2. Corporate Eligibility Requirements

- 3. Copyright Ownership

- 4. Ineligible Production Genres

- 5. Treaty Coproductions

- 6. Key Creative and Producer-Related Personnel

- 7. Financial Information

- 8. Exploitation of a Production

List of tables

- Table 1: Key creative point system for live action productions

- Table 2: Key creative point system for animation productions

List of figures

- Figure 1: Stages for review of applications at CAVCO

- Figure 2: A production in respect of a game, questionnaire or contest (other than a production directed primarily at minors)

List of acronyms and abbreviations

- BBC

- British Broadcasting Corporation

- CAVCO

- Canadian Audio-Visual Certification Office

- CMF

- Canada Media Fund

- CPA

- Chartered Professional Accountant

- CPTC

- Canadian Film or Video Production Tax Credit

- CRA

- Canada Revenue Agency

- CRTC

- Canadian Radio-television and Telecommunications Commission

- DG

- Director General

- DVD

- Digital Versatile Disc

- PSTC

- Film or Video Production Services Tax Credit

- VOD

- Video on Demand

- VR

- Virtual Reality

Overview

What is the Canadian Film or Video Production Tax Credit?

The Canadian Film or Video Production Tax Credit (CPTC) is a refundable corporate tax credit designed to encourage the creation of Canadian film and television programming and the development of an active domestic independent production sector in Canada. The CPTC program is jointly administered by the Department of Canadian Heritage, through the Canadian Audio-Visual Certification Office (CAVCO), and by the Canada Revenue Agency (CRA).

The CPTC is governed by section 125.4 of the Income Tax Act (the “Act”) and section 1106 of the Income Tax Regulations (the “Regulations”). Links to the full text of the Act and Regulations are available on CPTC’s website.Footnote 1 The Act and Regulations take precedence, to the extent of any inconsistency with these guidelines.

What information is in these guidelines?

These guidelines focus on the requirements a production must meet to be certified as a Canadian film or video production under the CPTC program.

They also explain how the tax credit for a production is calculated, and the CRA’s role in reviewing claims for the tax credit following the certification of a production through CAVCO.

Who can apply for the CPTC?

The CPTC is available only to a Canadian production company that is a qualified corporation. A qualified corporation is one that is throughout a given taxation year a prescribed taxable Canadian corporation with a permanent establishment in Canada, and that primarily carries on the activities of a Canadian film or video production business. A Canadian film or video production in this context is a production meeting the requirements of section 1106 of the Regulations.

How do I submit an application to CAVCO?

Applications for CPTC certification must be submitted through the CAVCO Online application system. See CPTC’s website for more information.

Production companies must apply to CAVCO for both a Canadian film or video production certificate (Part A certificate) and a certificate of completion (Part B certificate) for each production.

How is the CPTC calculated?

The CPTC is available at the rate of 25% of the qualified labour expenditure for an eligible production in a given taxation year.

The qualified labour expenditure represents the eligible labour expenses incurred for a production, capped at 60% of the production’s total cost once funding amounts considered assistance are deducted. The maximum CPTC available for a production is therefore 15% of the total cost of production net of assistance. The rules for calculating the tax credit are set out in section 125.4 of the Act.

Are all types of audiovisual content eligible for the CPTC?

To be eligible for CPTC certification, a production must be a linear, non-interactive film or video production.

An interactive project requiring some form of viewer intervention to progress the storyline is not eligible. A 360/virtual reality (VR) production can be eligible, as long as the storyline progresses in a linear way without needing any active viewer intervention. Viewer involvement outside of the context of the audiovisual project – for example, through online voting – is acceptable.

Websites, games, apps, and any similar products are not eligible for the CPTC.

What is the Film or Video Production Services Tax Credit (PSTC)?

The PSTC is the other federal audiovisual tax credit program co-administered by CAVCO and the CRA. It promotes Canada as a location of choice for foreign- and Canadian-owned film and television productions and supports the existence of a production infrastructure of international calibre in Canada.

It is available to Canadian-based production companies or production service companies at a rate of 16% of the qualified Canadian labour expenditure for a production. The qualified Canadian labour expenditure is equal to all eligible labour expenses (expenses payable to Canadian residents for services rendered in Canada) minus the total of all financing amounts considered assistance.

Productions eligible for the PSTC generally feature non-Canadian creative control and non-Canadian copyright ownership.

For more information on PSTC program requirements, see PSTC’s website.

Note that a corporation cannot receive both the PSTC and the CPTC for the same production.

What are the requirements for a production to be eligible for the CPTC?

For a production to be eligible under the CPTC program, it must meet all of the requirements set out below. Each is further described in the noted section of the guidelines. These requirements are found in section 125.4 of the Act and section 1106 of the Regulations, under the definitions for “Canadian film or video production,” “Canadian film or video production certificate” and “excluded production.”

-

1. Application and certification deadlines

CAVCO has a two-part application process. There is no deadline to submit a Part A application for a production. A Part B application must be received by CAVCO within 24 months of the production company’s first taxation year end following the start of principal photography. The Part B certificate for a production must be issued by CAVCO within six months of this application deadline. These deadlines can be extended by 18 months if valid T2029 waivers are filed with the CRA. (See section 1.09)

-

2. Canadian production company

The production company must be a prescribed taxable Canadian corporation and a qualified corporation. (See sections 2.01-2.02)

-

3. Canadian copyright ownership

Only the production company or a prescribed person may own copyright in the production during the 25-year period beginning when the production is complete and commercially exploitable. (See sections 3.01-3.03)

-

4. Production genres

The production cannot fall under any of the ineligible production genres. (See sections 4.01-4.03)

-

5. Key creative points for Canadians

The production must obtain a minimum number of points given for key creative positions occupied by Canadian citizens or permanent residents, and obtain certain points that are mandatory. (See sections 6.01-6.08)

-

6. Canadian producer

All producer-related personnel (other than those receiving exemptions permitted in limited circumstances) must be Canadian. (See sections 6.09-6.13)

-

7. Canadian cost requirements

At least 75% of the total of all costs for services related to producing the production (other than certain excluded costs) must be payable for services provided to or by individuals who are Canadian. (See section 7.10)

At least 75% of the total of all post-production costs for a production (other than certain excluded costs) must be incurred for services provided in Canada. (See section 7.10)

-

8. Canadian control over exploitation rights

Only the production company or a prescribed person may control the initial licensing of commercial exploitation rights for the production. (See section 8.01)

-

9. Exploitation in Canada

Either a Canadian distributor or a CRTC-licensed broadcaster must provide written confirmation that the production will be shown in Canada within the two-year period beginning when the production is complete and commercially exploitable. (See sections 8.02-8.06)

-

10. No distribution in Canada by non-Canadians

The production cannot be distributed in Canada by a non-Canadian entity within the two-year period beginning when the production is complete and commercially exploitable. (See section 8.08)

-

11. Acceptable share of revenues

The production company or a related prescribed taxable Canadian corporation must receive an acceptable share of revenues from the exploitation of the production in non-Canadian markets. (See section 8.09)

Note that requirements 3, 5-8 and 11 do not apply to treaty coproductions.

A treaty coproduction must meet all other requirements, and must conform to the terms of the applicable coproduction treaty. See Chapter 5 for more information on the certification of treaty coproductions under the CPTC program.

1. Administration of the CPTC Program

In this section

- 1.01 Contacting CAVCO

- 1.02 Overview

- 1.03 Role of CAVCO

- 1.04 Role of the CRA

- 1.05 Certification of Treaty Coproductions under the CPTC Program

- 1.06 Submitting an Application to CAVCO

- 1.07 Application Fees

- 1.08 Application Review Process

- 1.09 Part B Application and Certification Deadlines

- 1.10 Compliance Reviews

- 1.11 Denials and Revocations

- 1.12 Internal CAVCO Audits

- 1.13 Preliminary Opinions of Eligibility (Pre-assessments)

- 1.14 Confidentiality of taxpayer information

- 1.15 Screen Credit Requirements

- 1.16 Canadian Content Certification through the Canadian Radio-television and Telecommunications Commission (CRTC)

1.01 Contacting CAVCO

Information relevant to the CPTC program, including program guidelines, forms, and the online application portal, is available on CPTC’s website.

Contact information:

Canadian Audio-Visual Certification Office (CAVCO)

Canadian Heritage

25 Eddy Street

Gatineau, Quebec

J8X 4B5

- Telephone:

- 1-888-433-2200 (toll-free)

- TTY:

- 1-888-997-3123

- E-mail:

- bcpac-cavco@pch.gc.ca

- Website:

- canada.ca/cavco

1.02 Overview

On behalf of the Minister of Canadian Heritage, CAVCO issues certificates for productions meeting all certification requirements under the CPTC program. (See section 1.03)

Production companies submit these certificates to the Canada Revenue Agency (CRA), as part of their T2 Corporation Income Tax Returns, to receive the tax credit. (See section 1.04)

1.03 Role of CAVCO

1.03.01 General

CAVCO is responsible for assessing whether a production meets the requirements for CPTC certification set out in section 125.4 of the Act and section 1106 of the Regulations. CAVCO then recommends to the Minister of Canadian Heritage whether or not to issue a “Canadian film or video production certificate” (a “Part A certificate”) for the production.Footnote 2

Once a production is completed, CAVCO is responsible for assessing whether the production continues to meet the requirements of the Act and Regulations. CAVCO recommends to the Minister whether or not to issue a “certificate of completion” (a “Part B certificate”) for the production. A production for which a certificate of completion is not issued loses its status as a Canadian film or video production. More information on each certificate can be found in sections 1.03.02-1.03.03.

A previously issued Part A certificate may be revoked by the Minister of Canadian Heritage if an omission or incorrect statement was made for the purpose of obtaining the certificate, or where, for any reason, the production is found not to be a Canadian film or video production. A revoked certificate is deemed never to have been issued. See section 1.11 for more information on revocations.

1.03.02 Canadian film or video production certificate (Part A certificate)

This certificate confirms that a production is a “Canadian film or video production.”

The certificate also provides estimates of the production costs and labour expenditures associated with a production, as well as the tax credit applicable to the production. These estimates are based on an analysis of budget and financing information for the production.

The Part A certificate is generally issued before or during production, to help production companies secure other production financing and to allow them to claim a tax credit at the end of the first year of production. Note that it is not necessary for a production company to have received both the Part A and Part B certificates before applying for the tax credit with the CRA. A claim can be filed with just the Part A certificate.

If CAVCO cannot conclusively determine whether one or more types of financing for a production are assistance (see section 7.06), this financing will be treated as assistance for the purpose of CAVCO’s estimate of the tax credit for the production.

The estimate provided by CAVCO is not binding on the CRA, and is not a commitment as to the final value of the tax credit. A final determination of the qualified labour expenditure and tax credit for a production is made by the CRA during its review of a tax credit claim for a given year.

1.03.03 Certificate of completion (Part B certificate)

A Part B certificate is issued where a production is completed and continues to meet the requirements for being certified under the CPTC program. If this certificate is not issued within the prescribed time frame (see section 1.09), the CRA will refuse any tax credit claim for the production and reassess the corporation’s tax returns for any tax credit previously allowed.Footnote 3

An applicant may apply at the same time (with a “Part A/B application”) for both the Canadian film or video production certificate and the certificate of completion, once a production is completed.

1.03.04 Certification of episodes in a series

For the purpose of CPTC certification, each episode in a series or mini-series, or film in an anthology of short films, is considered a distinct production.Footnote 4 If an application to CAVCO is for a series, only one certificate is issued, with the suffix of the certificate number indicating the total number of eligible episodes. For example, 45678-010 means that 10 episodes have been certified.

1.04 Role of the CRA

1.04.01 General

The CRA is responsible for:

- applying the sections of the Act relevant for determining the CPTC (this includes confirming the qualified labour expenditure amount, calculating the tax credit amount, and confirming that a corporation is a qualified corporation);

- reviewing and auditing CPTC claims within a reasonable time frame;

- assessing the company’s T2 Corporation income tax return; and

- issuing timely refund cheques where applicable.

To claim the tax credit for a certified production, a qualified corporation must file with its T2 Corporation Income Tax Return:

- the Part A certificate issued for the production; and

- a CRA T1131 “Canadian Film or Video Production Tax Credit” form.

CAVCO informs the CRA if, for any reason, a Part B certificate is not subsequently issued for the production. As previously noted, the CRA will in these cases refuse any new tax credit claim for the production and reassess the corporation’s tax returns for any tax credit previously allowed.

The CPTC is a refundable tax credit. This means that the qualified corporation will be refunded the amount of the tax credit, to the extent that it exceeds the total of any tax payable for the year, and subject to the CRA’s right to offset any other amount the corporation owes.

Note that under subsection 164(1) of the Act, a tax credit for a given taxation year can only be issued in the form of a refund if the T2 Corporation Income Tax Return for that year was filed within three years of the end of that year.

As part of its review of a tax credit claim, the CRA may request any additional information it deems necessary, including in the course of a full fiscal audit of the production. This may include, but is not limited to, the books and records of the corporation and the full applications filed with CAVCO.

More information on the CRA’s role in co-administering the CPTC program, as well as its Form T1131 and its publication Canadian Film or Video Production Tax Credit – Guide to Form T1131, can be found on its website.

1.04.02 Claiming a capital cost allowance for a CPTC-certified production

A CPTC-certified production is a Class 10(x) property under Schedule II of the Income Tax Regulations, and is eligible for an accelerated Capital Cost Allowance (CCA). For more information, see the Claiming capital cost allowance (CCA) webpage or contact the applicable regional CRA Film Services Unit.

1.05 Certification of Treaty Coproductions under the CPTC Program

Treaty coproductions involving a Canadian production company can be eligible for the CPTC.

For a treaty coproduction to be considered a Canadian film or video production, the Canadian production company coproducing it must apply to Telefilm Canada (Telefilm) for Preliminary and Final Recommendations, as well as to CAVCO for a Part A certificate and a Part B certificate.

Telefilm is the administrative authority responsible for evaluating whether a production meets the criteria set out in the relevant coproduction treaty. It provides CAVCO with both a Preliminary Recommendation and a Final Recommendation as to whether a production meets treaty requirements.

CAVCO makes a recommendation to the Minister of Canadian Heritage as to whether or not the coproduction should be certified under the CPTC program.

See Chapter 5 for more information on treaty coproductions.

1.06 Submitting an Application to CAVCO

1.06.01 Complete application

Applicants are responsible for submitting complete CPTC applications to CAVCO.

Production companies must file complete applications through the CAVCO Online application system, accessible through CPTC’s website.

Supporting documentation must be included as part of a complete Part A or Part B application to CAVCO. A list of this documentation can be found in the “How to apply” section of the CPTC page on CPTC’s website. Note that CAVCO does not accept redacted documents.

Incomplete applications will not proceed for analysis with a tax credit officer unless all required information and documents are received.

If information or documentation required to determine the eligibility of a production is not provided to CAVCO upon request, CAVCO could recommend the file for denial or revocation at any time. For more information on the process for denials or revocations, see section 1.11.

1.06.02 Requests for additional information

CAVCO reserves the right to request any additional information, affidavits or sworn statements necessary to ensure that a CPTC certificate should be issued for a production.

CAVCO may also ask the production company to provide any necessary records or financial documents for auditing purposes. The production company must ensure that adequate space and time are provided, and that all relevant documents are made available, for an audit.

While a copy of a production (three representative episodes for a series) is always required at the Part B application stage, CAVCO may also request a copy at the Part A stage (a rough cut is acceptable) where necessary. This may occur, for example, where there is a potential concern related to the production meeting genre or lead performer eligibility requirements.

Where a copy of the production is requested at the Part A stage, note that a final copy of the production is still required with the Part B application for the production.

CAVCO also reserves the right to request more episodes of a series at any stage of analysis. This may occur, for example, where there is a concern with the eligibility of one or more of the episodes submitted originally. In rare cases, CAVCO may ask to see all episodes in a series.

1.07 Application Fees

A fee is required for each application to CAVCO.

The fee amount for an application may be adjusted by CAVCO prior to certification, where a change to the production budget or production financing affects the eligible production cost. In the event this results in an additional fee being owed by the applicant, the outstanding amount must be paid before the certificate is issued. Overpayments will be refunded after Part B certification for the production.

More information on application fees is available on the Fees — Film and Video Tax Credits webpage.

1.08 Application Review Process

When an application is received by CAVCO, it is reviewed for completeness. Once an application is complete, it is placed in a queue to be assigned to a tax credit officer.

When the application is assigned to a tax credit officer, they will review it and contact the production company if additional information or clarification is needed.

Once the tax credit officer’s review is complete, the file is advanced for further approvals, ending with a final recommendation being made to the Director General, Audiovisual Branch to either certify the production, or deny or revoke the certification of the production, on behalf of the Minister of Canadian Heritage. The applicant is notified as soon as possible of the decision.

Notifications from CAVCO are sent to the applicant’s Message Centre in the CAVCO Online system. It is therefore important for the applicant to check their messages on a regular basis. Applicants should also ensure that all contact information for their applications (including e-mail address, phone number and mailing address) is kept up to date.

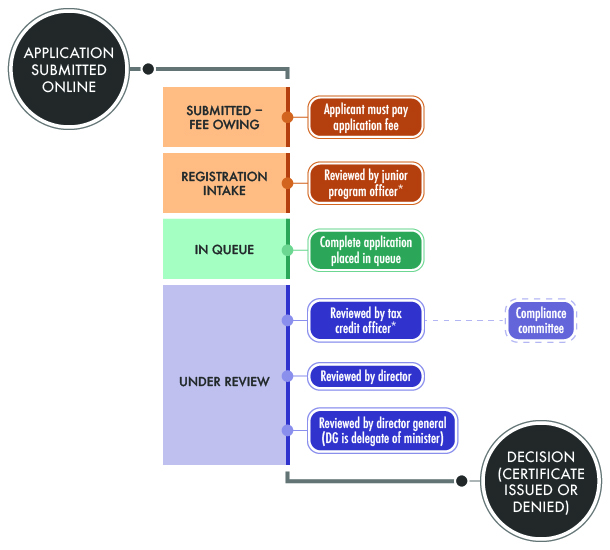

See Figure 1 below for more details on CAVCO’s application review process.

Figure 1: Stages for review of applications at CAVCO

Figure 1: Stages for review of applications at CAVCO - Text version

Step 1 – An application is submitted online

Step 2 – Submitted / fees pending” is the file status message that an applicant would see in the online system.

Step 3 – “Registration intake” is the next file status message. Note that during this stage, the application is being reviewed by a junior program officer**

Step 4 – “In queue” message that the applicant will see in the online application means that a complete application is placed in queue.

Step 5 – “Under review” message in the system is the final stages of the application process which include the following steps:

- the application is reviewed by a tax credit officer** who might submit the application to CAVCO’s Compliance Committee for review of the issue(s) of ineligibility if applicable

- the application is reviewed by the director

- the application is reviewed by the director general (DG is the delegate of the minister)

Step 6 – A decision is made to issue or deny a certificate.

Figure 1 also explains that the processing time for an application is considered to be from the start of the “In Queue” stage to the end of the “Under Review” stage.*

Figure 1: Stages for review of applications at CAVCO - Notes

The four boxes on the left side of the diagram represent the different file status messages that an applicant sees in the CAVCO Online system.

* For more information on CAVCO’s service standards and processing times, see the CAVCO Performance Results webpage.

** Officers may request missing information or additional clarification for a file, in which case applicants will see the status messages “In progress – not submitted” or “amendment in progress – not submitted”. The application does not progress to the next stage of analysis until all required information is received.

1.09 Part B Application and Certification Deadlines

1.09.01 Overview

While there is no deadline for applying to CAVCO for a Part A certificate for a production, there are deadlines for applying for a Part B certificate, and for this certificate being issued by CAVCO to the applicant.

1.09.02 Part B application deadline / CRA waiver requirements

The initial Part B application deadline is 24 months from the end of the corporation’s taxation year in which the production’s principal photography began (the “24-month deadline”).Footnote 5

This deadline can be extended to 42 months from the first taxation year end date (the “42-month deadline”), as long as the applicant files valid T2029 waivers with the CRA for both the first and second taxation years ending after principal photography began. CAVCO verifies directly with the CRA that valid waivers, when required, have been filed.

See the T2029 waiver form webpage for more information on how to fill out and file these waivers, and to view a sample waiver.

For clarity purposes:

- The Part B application must be filed with CAVCO by the 42-month deadline.

- The two properly completed waivers for the production must be filed with the CRA by the 42-month deadline, and within the normal reassessment period for the two taxation years. A waiver should not be filed for a taxation year if that year has not yet been assessed by the CRA.

- If a waiver is not completed correctly or is submitted when the relevant taxation year has not yet been assessed, the form will be returned to the claimant, causing potential delays with CPTC certification.

The normal reassessment period for a taxation year is three years from the date of the mailing of the notice of assessment for Canadian-controlled private corporations, and four years from this date for public corporations.

A failure to meet the final 42-month deadline, or to file valid waivers when required, will result in a previously issued Part A certificate being revoked, or a Part A/B application being denied.

1.09.03 Part B application deadline for domestic coproductions

When two or more Canadian production companies enter into a domestic coproduction arrangement (see section 2.03), the deadlines for applying to the CPTC are determined using the taxation year end of the primary applicant. If the primary applicant is submitting a Part B application after the 24-month deadline, the coproducing partner will also have to file waivers with the CRA.

1.09.04 Part B certification deadline

A Part B certificate must be issued within 6 months of a production’s application deadline. The 48-month deadline is therefore the final date by which CAVCO must issue a Part B certificate for a production.

An applicant must submit a complete application and respond to all requests for information or clarification from CAVCO in a timely manner, so that CAVCO’s analysis can be completed, and a certificate issued, by this final deadline.

If no Part B certificate is issued by the 48-month deadline, a previously issued Part A certificate will be revoked, or a Part A/B application will be denied.

1.09.05 Calculation of deadlines – Example

- Corporate Taxation Year End

- December 31

- Start of Principal Photography

- February 3, 2015

- End of taxation year in which principal photography began

- December 31, 2015

- End of following taxation year

- December 31, 2016

- 24-month Part B application deadline

- December 31, 2017

- 42-month Part B application deadline

- June 30, 2019

- 48-month Part B certification deadline

- December 31, 2019

In this example, if the Part B application is being submitted after the 24-month deadline:

- The Part B application must be submitted to CAVCO by June 30, 2019; and

- Valid CRA T2029 waivers, for each of the taxation years ending December 31, 2015 and December 31, 2016, would need to be filed with the CRA within the normal reassessment period for each of those two years.

1.09.06 Ensuring that the taxation year end date is correct

The applicant is responsible for ensuring that all Part B deadlines are met. As a courtesy to applicants, CAVCO does issue reminder notices of Part B application deadlines at the 22-month, 24-month, 40-month, and 41-month marks based on dates submitted in the Part A application.

When the taxation year end provided by the applicant with a Part A application is incorrect, or is later changedFootnote 6 without CAVCO being informed, CAVCO reminder notices may also be incorrect.

Note that once the first taxation year end has been confirmed through a company’s first filing of a T2 return for that year, Part B deadlines will continue to be calculated by reference to this date, even if the company later changes its taxation year.

Additional extension to Part B application deadline due to COVID-19

Due to the effect of COVID-19 on the Canadian audiovisual sector, the Department of Finance Canada has introduced temporary extensions to various timelines applicable to the CPTC.

Applicants who incurred labour expenses for a production during their taxation year ending in 2020 or 2021 may be eligible for an additional extension to their Part B application and certification deadlines for the production.

See CAVCO Public Notice 2022-03 for more information.

1.10 Compliance Reviews

If CAVCO determines that a production may not be eligible under the CPTC program, the file is submitted to CAVCO’s Compliance Committee for review of the issue(s) of ineligibility.

Based on this review, additional information or clarification may be requested from the applicant, or the file may be recommended for denial (for a Part A or Part A/B application) or revocation (for a Part B application). For more information on the process for denials or revocations, see section 1.11.

1.11 Denials and Revocations

If an application is for a Part A certificate, or for both Part A and Part B certificates at the same time, and the production does not meet the requirements for CPTC certification, the production will be denied certification.

Where a Part A certificate has already been issued for a production, it may be revoked by the Minister of Canadian Heritage where:

- an omission or incorrect statement was made for the purpose of obtaining the certificate; or

- the production is not a Canadian film or video production.

Where a review of an application reveals an issue of ineligibility, CAVCO sends the applicant an advance notice detailing the reasons why the production appears to be ineligible. The applicant is provided the opportunity to submit additional information that may impact the final evaluation of the application.

If, after considering the additional information, CAVCO makes a final recommendation that the production not be certified, or if the applicant fails to provide a response within the allotted time frame, the applicant is sent a final notification of denial or revocation issued by the Director General, Audiovisual Branch, on behalf of the Minister.

A certificate that is revoked is deemed never to have been issued. CAVCO provides a copy of the final notice to the CRA for all denials and revocations.

Applicants may apply to the Federal Court for judicial review of a final decision within 30 days of being notified by CAVCO of the decision. To apply for judicial review, an applicant must send a completed Form 301, Notice of Application (Federal Court website) (PDF format), with the appropriate filing fee, to the registrar of the Federal Court. For more information on how to file an application for judicial review, or other general enquiries, visit the Courts Administration Services website.

1.12 Internal CAVCO Audits

Each year, CAVCO performs a more in-depth review of a select number of applications. CAVCO reserves the right to request any additional information necessary for a complete audit of the application.

1.13 Preliminary Opinions of Eligibility (Pre-assessments)

A production company may ask CAVCO to provide a preliminary opinion on the eligibility of a production for CPTC certification with respect to a specific issue. This opinion is based strictly on the information made available at the time to CAVCO, and is not binding on whether or not the production will ultimately be eligible, including with respect to the specific issue identified in the pre-assessment request. Full Part A and B applications for a production must ultimately be received for CAVCO to provide a final recommendation to the Minister of Canadian Heritage regarding the production’s eligibility.

A request for a pre-assessment may be submitted to CAVCO only if a CPTC application for the production has not yet been submitted, and if the production has been substantially developed.

Requests for pre-assessments can be sent to CAVCO’s Compliance Committee at bcpacc-cavcoc@pch.gc.ca.

All pre-assessment requests must include:

- the name of the production company (or parent company if a production company has not yet been incorporated);

- the title of the production and, where applicable, the number and length of episodes;

- the broadcaster or distributor involved or being contemplated; and

- the specific eligibility issue to be addressed (e.g., a question about lead performer, genre, etc.).

If no specific eligibility concerns are identified and explained, CAVCO will not be able to proceed with a pre-assessment.

If the concern relates to whether a production falls under an ineligible genre category, the request must include, in addition to the specific genre(s) of concern:

- a detailed treatment and/or series bible (note that a one-page synopsis or concept is not sufficient);

- for series, a sample episodic breakdown providing the details and length of each segment in the episode, to show what each segment will look like once produced; and

- if available, a copy of the completed production or, for a format production, a copy of the original version of the production it is based on.

CAVCO’s pre-assessment letter must be attached to any future CPTC application made to CAVCO for the production.

1.14 Confidentiality of Taxpayer Information

1.14.01 General

All information provided by an applicant under the CPTC program is subject to the taxpayer confidentiality provisions in section 241 of the Income Tax Act. This section restricts how government officials can use or communicate information obtained for the purpose of administering the Act. The full text of section 241 of the Income Tax Act can be found on the Department of Justice website.

1.14.02 Publication of titles of certified productions

Subsection 241(3.3) of the Act allows the communication of limited information regarding productions that have been Part A certified under the CPTC program. Accordingly, CAVCO publishes a list of titles and associated production companies for all Part A certified productions. A link to the list is available on CPTC’s website.

1.14.03 Sharing information with other federal or provincial government entities

Under section 241 of the Act, CAVCO can share information with:

- other entities directly involved with the co-administration of the CPTC, including the CRA and, in the context of treaty coproductions, Telefilm Canada;

- any federal or provincial government office or agency whose mandate includes the provision of assistance for film or video productions, to the extent that the information is shared for the purpose of administering or enforcing of the program under which the assistance is offered; or

- the CRTC, to the extent that it is being provided for the purpose of the administration or enforcement of a regulatory function of the CRTC.

1.15 Screen Credit Requirements

The Canadian production company, as well as the individual(s) occupying the producer position, must be clearly identified and given prominence on screen in the main titles, and in all billing blocks.

The Canadian copyright notice must also appear in the tail-end screen credits.

The “Canada” wordmark logo, accompanied by the wording “Canadian Film or Video Production Tax Credit,” must appear on all domestic and international versions of each certified production, and in all related advertising, publicity and promotional materials. More information can be found on CPTC’s website.

1.16 Canadian Content Certification through the Canadian Radio-television and Telecommunications Commission (CRTC)

The CRTC has a Canadian content certification program that is similar in many respects to the CPTC certification process. However, no tax credit is provided through the CRTC.

For the purpose of CRTC program logs, broadcasters can submit a CPTC certificate number for a production, in lieu of the certification (“C”) number issued through the CRTC’s Canadian Program Certification section.

For more information, visit the CRTC’s website.

2. Corporate Eligibility Requirements

In this section

2.01 Prescribed Taxable Canadian Corporation

2.01.01 Overview

The production company producing a film or video production and applying for CPTC certification must demonstrate that it is a “prescribed taxable Canadian corporation,” as defined in the Regulations.

This means the corporation must be a taxable Canadian corporationFootnote 7 that is:

- Canadian-controlled, based on sections 26 to 28 of the Investment Canada Act;

- not controlled directly or indirectly in any manner by one or more persons, all or part of whose taxable income is exempt from tax under Part I of the Income Tax Act (for example, tax-exempt non-profit corporations, charitable organizations, etc.); and

- not a prescribed labour-sponsored venture capital corporation, as defined in section 6701 of the Regulations.

For the purpose of sections 26 to 28 of the Investment Canada Act, “Canadian” means:

- a Canadian citizen;

- a permanent resident within the meaning of subsection 2(1) of the Immigration and Refugee Protection Act who has been ordinarily resident in CanadaFootnote 8 for not more than one year after the time at which he or she first became eligible to apply for Canadian citizenship;Footnote 9

- a Canadian government, whether federal, provincial or local, or an agency thereof; or

- an entity that is Canadian-controlled, as determined under subsection 26(1) or (2) and in respect of which there has been no determination made under any of subsections 26(2.1), (2.11) and (2.31), or declaration made under subsection 26(2.2) or (2.32).

2.01.02 How CAVCO assesses control of a corporation

For a production company to meet the Canadian ownership and control requirements of the CPTC program, there must be control in law (“de jure” control) of the company by Canadians, with respect to shareholders’ voting rights. It must also be clear that this extends to control in fact (“de facto” control), having regard for the nature of shareholders’, officers’ or directors’ involvement with, or influence within, the company. In other words, de facto control may exist when another corporation, person or group of persons has any direct or indirect influence that, if exercised, would result in control in fact of the corporation.

The assessment of a company’s eligibility is based primarily on information provided by the applicant in the “Shareholders” section of an application.

CAVCO may in some cases request additional information to confirm the control of a corporation based on the rights, privileges and decision-making authority of shareholders (e.g., through articles of incorporation, shareholder agreements, trust agreements, legal opinions, organization charts or similar documentation).

CAVCO may request additional supporting documents for a publicly traded company, such as the company’s articles of incorporation, its notice of registered office, or a certified list of shareholders. Additional documents may also be required if a shareholder is an entity such as a sole proprietorship, a partnership or a trust.

Any corporate shareholder (or a shareholder such as a partnership or a trust) owning a majority of voting shares in the production company must also be shown to be Canadian-controlled.

Where there are several minority shareholders that are corporations or other business entities, it must be shown that a majority of shares are owned by Canadian-controlled entities.

2.02 Qualified Corporation

A company applying for the tax credit under the CPTC program must be a “qualified corporation,” as defined in the Act.

Under this definition, a corporation must be one that is, throughout a given taxation year, a prescribed taxable Canadian corporation (see section 2.01) whose activities consist primarily of carrying on a Canadian film or video production business, through a permanent establishment in Canada.

Where the business of a corporation consists primarily of other activities such as the rental of equipment or studios, the distribution of audiovisual productions, or the production of films or videos that are not Canadian film or video productions, the corporation is not considered a qualified corporation.

If a corporation engages in more than one business, the assessment of its primary activity is based on evaluating factors such as the revenues generated by each business, the capital employed in each business, and the time spent by employees, agents or officers on each business.

The CRA determines whether a production company is a qualified corporation. If a production company is unsure whether or not it is a qualified corporation for tax credit purposes, it may contact its regional Film Services Unit of the CRA prior to submitting an application to CAVCO.

2.03 Domestic Coproductions

A domestic coproduction is a production for which more than one Canadian production company incurs expenses.

Only one application for certification is submitted to CAVCO through the company designated by the coproducers as the primary applicant for the application. However, information on all coproducing companies must be included with the application. Each production company must be a prescribed taxable Canadian corporation and a qualified corporation.

For domestic coproductions, CAVCO issues only one CPTC certificate. Each production company may then claim their own portion of the tax credit with the CRA.

Note that where two or more partnering Canadian production companies incorporate a subsidiary company to be the sole production company for a production, the production should not be identified as a domestic coproduction in an application to CAVCO.

3. Copyright Ownership

In this section

3.01 General

Unless a production is a treaty coproduction, only the Canadian production company or a “prescribed person” can be a copyright owner of the production for all commercial exploitation purposes, for the 25-year period beginning when the production is completed and commercially exploitable.

No other person or entity can place any restriction on the ability of the production company or prescribed person to exercise full copyright ownership rights in the production during this period. This is verified by CAVCO through its review of documents such as exploitation, financing and chain-of-title agreements.

3.02 Copyright owner

Under the Regulations, a “copyright owner” for the purpose of the CPTC can be:

- the maker, as defined in section 2 of the Copyright Act, who at that time owns copyright in relation to the production, within the meaning of section 3 of that Act; or

- a person to whom that copyright has been assigned, under an assignment described in section 13 of the Copyright Act, either wholly or partially, by the maker or by another owner to whom this paragraph applied before the assignment

For greater certainty, the granting of an exclusive licence within the meaning of the Copyright Act (for example, to a broadcaster or a distributor) is not an assignment of copyright.

3.03 Prescribed person

3.03.01 Overview

In the Regulations, a “prescribed person” is defined as:

- a corporation that holds a television, specialty or pay-television broadcasting licence issued by the Canadian Radio-television and Telecommunications Commission;

- a corporation that holds a broadcast undertaking licence and that provides production funding as a result of a “significant benefits” commitment given to the [CRTC];

- a person to which paragraph 149(1)(l) of the Act appliesFootnote 10 and that has a fund that is used to finance Canadian film or video productions;

- a Canadian government film agency,

- in respect of a film or video production, a non-resident person that does not carry on a business in Canada through a permanent establishment in Canada and whose interest (or, for civil law, right) in the production is acquired to comply with the certification requirements of a treaty coproduction twinning arrangement; and

- a person

- to which paragraph 149(1)(f) of the Act appliesFootnote 11,

- that has a fund that is used to finance Canadian film or video productions, all or substantially all of which financing is provided by way of a direct ownership interest (or, for civil law, right) in those productions, and

- that, after 1996, has received donations only from persons described in paragraphs (a) to (e).

- a prescribed taxable Canadian corporation;

- an individual who is a Canadian; and

- a partnership, each member of which is described in any of paragraphs (a) to (h).

Note that if an entity other than the Canadian production company is a copyright owner of a production, this may have an impact on how a Capital Cost Allowance for the production is claimed. Production companies may consult with their regional CRA Film Services Unit office for further information on this issue.

3.03.02 Documentation demonstrating that an individual or entity is a “prescribed person”

- A prescribed taxable Canadian corporation must provide a “Private Company Declaration” (available on the Forms — Canadian Film or Video Production Tax Credit webpage) completed and signed by an authorized representative of the corporation.Footnote 12

- Individuals that are prescribed persons must demonstrate that they are Canadian citizens or permanent residents by either:

- providing a completed and signed “Individual Declaration – Prescribed Person” (available on the Forms — Canadian Film or Video Production Tax Credit webpage); or

- providing a CAVCO Personnel Number (see section 6.01.03).

For other entities acting as prescribed persons, CAVCO will ask the applicant to provide documentation where necessary.

3.03.03 Involvement of an individual or entity that is not a prescribed person

A non-prescribed person may make an investment in a production or participate in profits generated from a production, but cannot be a copyright owner of the production, or have any control over the initial licensing of commercial exploitation rights for the production.

Note that in cases where a non-prescribed person invests in a production without being a copyright owner, CAVCO examines relevant agreements to ensure that their involvement does not raise any concerns related to:

- production control (see section 6.10) or

- the retention by the production company of an acceptable share of revenues (see section 8.09).

4. Ineligible Production Genres

In this section

4.01 List of ineligible genres

There is not a list of production genres that are eligible under the CPTC program. Instead, the Income Tax Regulations outline ten genres (listed below) that are not eligible for the program. Additional clarifications on how CAVCO assesses ineligible genres, including relevant definitions, can be found in section 4.03.

- news, current events or public affairs programming, or a program that includes weather or market reports;

- a production in respect of a game, questionnaire or contest (other than a production directed primarily at minors);

- a sports event or activity;

- a gala presentation or an awards show;

- a production that solicits funds;

- reality television;

- pornography;

- advertising;

- a production produced primarily for industrial, corporate or institutional purposes;

- a production, other than a documentary, all or substantially all of which consists of stock footage.

4.02 How CAVCO assesses whether a production falls under an ineligible genre definition

At the Part A application stage, CAVCO reviews the synopsis for the production. If the synopsis does not provide sufficient information about a production’s genre, CAVCO may also request other script material (for example, a treatment, a screenplay, or an episodic breakdown) or, in some cases, a preliminary copy of the production.

At the Part B application stage, CAVCO reviews a copy of the production.

Note that when CAVCO is reviewing an application for a new season of a series that has been certified in previous seasons, the genre of the new season is still assessed.

See section 1.13 for more information on requesting a pre-assessment related to genre eligibility.

4.03 Additional clarifications (including definitions) for each ineligible genre

4.03.01 News, current events or public affairs programming, or a program that includes weather or market reports

Definition:

A production that:

- presents local, regional, national or international news in the form of a newscast;

- is presented in the form of specialized news programming, including, but not limited to, business news, sports news or entertainment news;

- presents live or pre-recorded coverage of current events;

- presents discussions or analysis of current political or public policy issues in the form of one-on-one, round-table or panel discussions, debates, open forums or town hall meetings;

- includes weather or market reports; or

- includes a combination of any of the above elements.

Key things to know:

- Clarification regarding each section of the definition:

- Element 1: A production that… presents local, regional, national or international news in the form of a newscast.

- This section of the definition captures traditional newscasts and clarifies that it applies to all types of newscasts, regardless of their territorial scope.

- Included within this category are daily news, evening news and 24-hour news channel programming.

- Examples: 6 p.m. news, ABC World News Tonight

- Element 2: A production that… is presented in the form of specialized news programming, including, but not limited to, business news, sports news or entertainment news.

- This section of the definition covers specialized news programming dealing with a more narrow scope of news than a traditional newscast.

- While this section identifies the most popular types of specialized news programming (business, sports and entertainment), it is not limited to those. For example, a specialized news production focusing on the video gaming industry, or on science-related news, would be included within this section.

- For clarity: To be included within this section, a show has to predominantly present news on a given subject matter. This section does not include lifestyle/human interest shows that deal with a specific subject matter (e.g., fishing, golfing, video gaming) in a broader way.

- Examples: Entertainment Tonight, ESPN SportsCentre

- Element 3: A production that… presents live or pre-recorded coverage of current events.

- This section of the definition refers to coverage of events that are typically covered by reporters or news divisions of broadcasters, but that are not presented in the form of a traditional newscast.

- This section does not include live performing arts shows.

- Examples: Election coverage, royal weddings, parades, political conventions

- Element 4: A production that… presents discussions or analysis of current political or public policy issues in the form of one-on-one, round-table or panel discussions, debates, open forums or town hall meetings.

- This section of the definition is designed to capture “public affairs programming.”

- This includes any production that predominantly consists of discussions of political news or government policy.

- Such productions are typically produced through the news division of a broadcaster.

- Examples: Meet the Press, State of the Union

- Element 5: A production that… includes weather or market reports.

- Any production that includes a weather or market report, regardless of the length of that segment, will be ineligible. For example, a talk show that includes a weather report will not be eligible.

- Productions with fictional weather or market reports will not be deemed to fall within this section of the definition.

- Example: The Today Show

- Element 6: A production that… includes a combination of any of the above elements.

- This section of the definition clarifies that a production consisting of a mixture of any of the above elements will also fall under this genre and therefore be ineligible.

- Element 1: A production that… presents local, regional, national or international news in the form of a newscast.

4.03.02 A production in respect of a game, questionnaire or contest (other than a production directed primarily at minors)

Definition:

A production where individuals or teams participate in a game, quiz, or contest that has an objective outcome (e.g., right/wrong, complete/incomplete, fastest time, highest score) to determine a winner, whether or not a prize is awarded.

A production that combines tasks that are measured objectively with tasks that are measured subjectively is included in this genre.

A production that includes competitive elements but features character development over the course of a series (e.g., by starting with a group of participants who are competing against each other and who are eliminated as the series progresses) is not included in this genre.

Key things to know:

- The definition does not apply to productions directed primarily at minors.

- The presence of prizes is not a consideration when deciding whether a production falls under this genre. Whether or not a prize is awarded, or the monetary value of a prize, does not change the basic premise of a show and is not used by CAVCO as a determining factor for eligibility.

Examples:

- Competition-based lifestyle/human interest programs with character development over the course of a series (which can therefore be eligible): Survivor, Amazing Race or American Idol

- Productions that would be ineligible: Jeopardy, The Price is Right, Who Wants to be a Millionaire, Let’s Make a Deal, American Ninja Warrior, Fear Factor, Des chiffres et des lettres

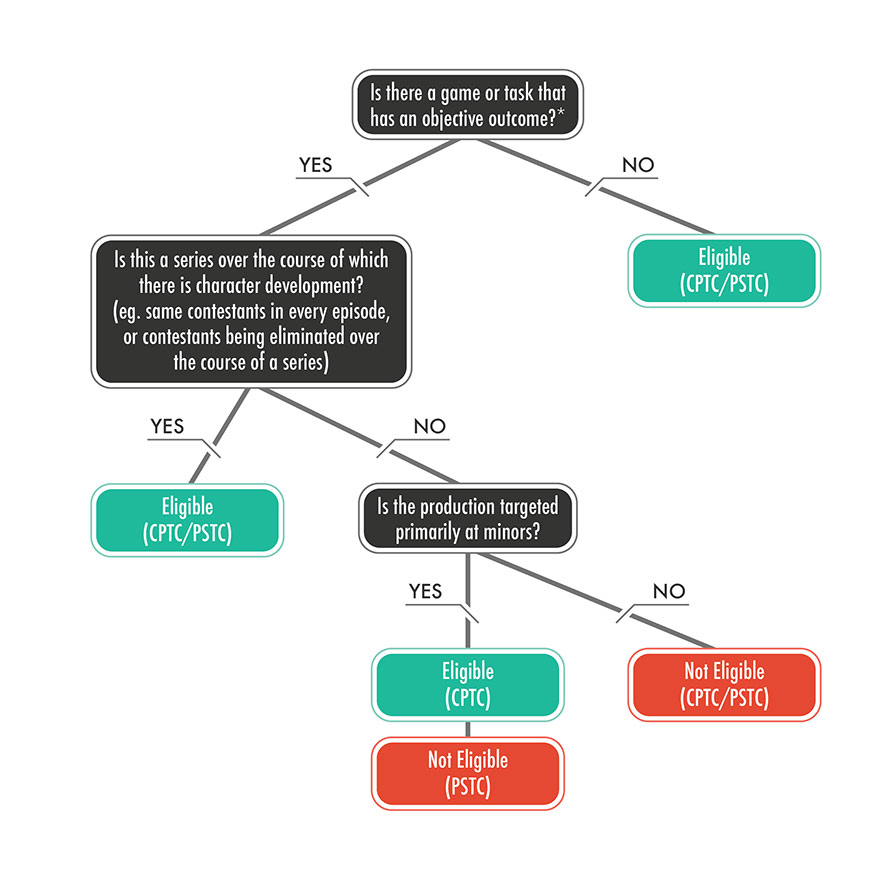

See Figure 2 below for more information on how CAVCO evaluates whether productions fall under this genre.

Figure 2: A production in respect of a game, questionnaire or contest (other than a production directed primarily at minors)

Figure 2: A production in respect of a game, questionnaire or contest (other than a production directed primarily at minors) – Text version

This figure lists a series of questions and answers on how CAVCO evaluates whether productions falls under the ineligible genre of A production in respect of a game, questionnaire or contest (other than a production directed primarily at minors)

First question – Is there a game or a task that has an objective outcome?

- If the answer is NO – The production would be eligible under both the CPTC and the PSTC

- If the answer is YES, a subsequent question needs to be answered to determine whether the production falls under this genre

Subsequent question – Is this a series over the course of which there is character development? (e.g. Same contestant in every episode or contestants being eliminated over the course of a series)

- If YES – The production would be eligible under both the CPTC and the PSTC

- If NO, a subsequent question needs to be answered to determine whether the production falls under this genre

Subsequent question – Is the production targeted primarily at minors?

- If YES –The production would be eligible under the CPTC only and not eligible under the PSTC

- If NO – The production would not be eligible under either the CPTC or the PSTC

Figure 2: A production in respect of a game, questionnaire or contest (other than a production directed primarily at minors) – Notes:

- *If there is a mix of objective and subjective outcomes, then choose “YES” for the first question.

- A “subjective outcome” is one determined by a decision-maker such as a judge or the audience.

- An “objective outcome” is one that is right/wrong, complete/incomplete, fastest time, etc.

- Whether or not there is a prize does not factor into the decision.

- Prolonged set-up to a game should still be considered part of the game.

- If the winner of each episode of a series returns in the next episode until they are defeated by a new challenger, the series is still considered to have new contestants in every episode (i.e. not an elimination series), since such a series still wouldn’t have the requisite character development.

4.03.03 A sports event or activity

Definition:

A production that consists of:

- live or pre-recorded coverage of a professional or amateur game, match, competition, or tournament; and/or

- pre- and post-game shows for sports events or activities.

Key things to know:

- This genre includes coverage of traditional sporting events or activities (e.g., hockey, football, tennis, the Olympics, motocross racing, darts, etc.) as well as coverage of other competitive tournaments (e.g., chess, poker, eSports or similar activities commonly known as “mind sports”).

- This genre does not include:

- documentaries about sports;

- lifestyle/human interest productions focused on a sport or recreational activity (e.g., skiing, fishing, snowboarding) that are informational, instructional or educational in nature; or

- a regularly scheduled, stand-alone sports talk show.

4.03.04 A gala presentation or an awards show

Definition:

A production that consists of:

- live or pre-recorded coverage of a gala presentation or an awards show; and/or

- pre- and post-event coverage of these events.

Key things to know:

- An award includes any type of honour or recognition.

- This genre includes all awards shows, whether or not they also contain other elements such as comedy or musical performances.

- This genre includes related pre- or post-event coverage (e.g., the red-carpet Oscar pre-show).

- This genre does not include behind-the-scenes or “making-of” productions about these events.

Examples:

- Gala presentation: gala dinners, gala screenings, gala performances, Miss America pageant, Kennedy Center Honors

- Awards show: The Academy Awards, The Tony Awards, La cérémonie des César, NFL Honors

4.03.05 A production that solicits funds

Definition:

A production that includes a segment of any length aimed at soliciting funds or other contributions from viewers.

Key things to know:

- This genre includes productions that visually or verbally solicit funds for any purpose (including, but not limited to, a charity or social cause) by directing viewers to a website, phone number or address through which they can make donations.

- Verbal requests are generally done by a representative of the show such as a host, announcer or regular panelist. The genre does not include productions featuring incidental soliciting of funds by guests on a show.

Examples:

Hope for Haiti Now telethon, Jerry Lewis MDA Labor Day telethon, Le téléthon de l’Association française contre les myopathies

4.03.06 Reality television

Definition:

A production that consists of:

- scenes recorded on private or public authority surveillance equipment; or

- the recording of any sort of official proceedings such as live or live-to-tape coverage of courtroom trials or governmental proceedings.

Key things to know:

- This genre refers to productions assembling pre-existing footage from public or private cameras.

- This genre does not refer to what viewing audiences have generally considered “reality television” since the late 1990’s, subsequent to the naming of this genre (e.g., Survivor, Keeping Up with the Kardashians, etc.).

4.03.07 Pornography

Definition:

A production that contains explicit depictions or descriptions of a sexual nature, without regard to artistic merit.

4.03.08 Advertising

Definition:

A production that:

- is a commercial or infomercial;

- includes a call to action soliciting the viewer to purchase a good or service (e.g., directing the viewer to a store or website other than the production’s website);

- promotes broadcast schedules or programming; or

- combines information or entertainment with the sale or promotion of goods or services into a virtually indistinguishable whole. The sale or promotion of goods or services includes extolling the virtues of one or more products, services, events, organizations or businesses, or the prominent use of logos or other brand identifiers.

Key things to know:

-

CAVCO assesses whether a production is “advertising” based on what is on-screen, using the elements set out in the definition. CAVCO does not assess the primary intent or “true nature” of a production in determining whether it is advertising.

In CAVCO’s experience, the presence of an agreement between an advertiser or sponsor and a producer or broadcaster, including where the former provides financing to a production, does not necessarily translate into any overt on-screen promotional content in the production. Similarly, the absence or non-disclosure of such contracts does not mean there will be no advertising on-screen.

- For greater certainty, the following elements do not automatically make a production advertising:

- The name of a brand is in the title of the production;

- A brand is involved in the creation of the program;

- A brand has the right to final factual review of the production;

- The production is named after a book, video game or toy;

- The viewer is directed to the production's website for more information;

- There is a link in the tail credits to a sponsor's website or to a website where products can be purchased;

- The production is broadcast with commercial breaks or other promotional content (e.g., on a website) that is related to a brand featured in the production;

- The production is filmed at the brand's place of business; or

- The production is partially or fully funded by a brand.

- The involvement of any advertiser or sponsor in a production must respect CAVCO’s producer control guidelines. These entities cannot, for example, have final creative or editorial control over a production, and are restricted to having customary consultation and approval rights. For more information on CAVCO’s assessment of producer control, see section 6.10.

-

Clarification regarding each section of the definition:

Element 1: A production that is a commercial or infomercial.

- This part of the definition refers to the most traditional types of advertising – a television commercial and a longer-form infomercial.

- A commercial may or may not include a “call to action”. In fact, most commercials do not include a clear “buy this” message.

Element 2: A production that includes a call to action soliciting the viewer to purchase a good or service (e.g., directing the viewer to a store or website other than the production’s website).

- This part of the definition refers to an explicit verbal or visual solicitation directed at viewers to purchase a product or service. Viewers may be directed to a production’s website for general information purposes.

Element 3: A production that promotes broadcast schedules or programming.

- This part of the definition includes:

- a television production including any on-screen visual presentation of upcoming broadcaster schedules; and

- a television production – whether a stand-alone production, or a special episode of a series – focusing on the promotion of broadcaster schedules or programming throughout the show. An example of this would be a show featuring stars or personalities promoting other programming on the same network.

Element 4: A production that combines information or entertainment with the sale or promotion of goods or services into a virtually indistinguishable whole. The sale or promotion of goods or services includes extolling the virtues of one or more products, services, events, organizations or businesses, or the prominent use of logos or brand identifiers.

- “Extolling the virtues” involves praising the features of the presented products or services, portraying them in an exclusively positive fashion.

- “Extolling the virtues” can be done visually (often in conjunction with verbal messaging) by presenting lingering “glamour” shots of products, services, logos or other brand identifiers.

- Productions that follow the structure of a “brochure” for a product or service will typically fall within this category. For example, if a large portion of a show dealing with a certain type of product or service is dedicated to highlighting multiple features or amenities of a specific example of that product or service, it is very likely that the production will be considered advertising.

- On-screen logos or other brand identifiers will not be taken into account if they are presented in an incidental and occasional fashion in the background, and are not focused on visually.

-

Clarification regarding review shows:

CAVCO does not consider a bona fide review of a product or service to be “extolling the virtues” of a product or service. To distinguish between these two situations, CAVCO will consider the following questions:

- Is the product or service presented in a balanced way?

- Is the product or service compared to any competitors’ products, either within an episode, or over the course of a series?

- Is there an evaluation of the product or service that goes beyond simply providing a list of all its features?

Affirmative answers to these questions are expected for CAVCO to consider the presentation of a product or service to be a review. If CAVCO determines that a production is a review show, or that a segment within a production features the review of a product or service, the positive references to these products or services, as well as any shots of logos appearing during reviews, will not be considered when assessing whether the production falls under element 4 of the definition.

4.03.09 A production produced primarily for industrial, corporate or institutional purposes

Definition:

A production primarily made to meet the specific industrial, corporate or institutional needs of a business, organization, government entity, or industrial sector.

Productions such as, but not limited to, recruitment videos, corporate training videos, public service announcements and promotional videos are included in this genre.

Key things to know:

- Productions in this genre are generally, but not necessarily, commissioned by a corporate entity for internal purposes or for promotional purposes. They are usually informational, instructional or educational with respect to the commissioning group’s activities.

- As there can be some overlap between this genre and the ineligible genre of “advertising,” a production may in some cases be ineligible on the basis of falling under both genres.

4.03.10 A production, other than a documentary, all or substantially all of which consists of stock footage

Definition:

A production, other than a documentary, all or substantially all of which consists of pre-existing footage.

5. Treaty Coproductions

In this section

5.01 Overview

An audiovisual coproduction is a production created by pooling the creative, technical and financial resources of coproducers.

Coproductions produced according to the terms of a coproduction treaty between Canada and another country are granted national status in each country, and are eligible for the CPTC where they meet all other applicable requirements under the Regulations.

The recognition of a project as a treaty coproduction must be obtained from the designated authority in each coproducing country.

5.02 Roles of Telefilm Canada and CAVCO in coproduction certification

Telefilm Canada: As the administrative authority for coproduction treaties involving Canada, Telefilm reviews coproduction applications to determine whether they meet the provisions of the applicable coproduction treaty. Telefilm provides CAVCO with a preliminary and a final recommendation on whether or not the production meets the terms of the relevant treaty.

The full text of all current coproduction treaties, as well as Telefilm’s policies, guidelines and online application portal, are available on Telefilm’s website.

CAVCO: CAVCO will assess the production’s compliance with the treaty, taking into account the recommendation made by Telefilm. CAVCO recommends to the Minister of Canadian Heritage to certify a coproduction as a “Canadian film or video production” where it meets the requirements of the treaty and all other applicable CPTC requirements under the Act and Regulations.

The Minister is responsible for rendering the final decision as to whether a production is a treaty coproduction that can be certified under the CPTC program.

For clarity: a production company must submit separate applications to both Telefilm and CAVCO to have a production certified as a treaty coproduction pursuant to the Act and Regulations.

5.03 Requirements for CPTC certification of a treaty coproduction

The following requirements in the Act and Regulations do not apply to treaty coproductions:

- All individuals occupying the producer position must be Canadian.

- The production must meet key creative point requirements.

- The production must meet minimum Canadian expenditure requirements for prescribed production and post-production costs.

- Only the Canadian production company or a prescribed person may own copyright in the production.

- Only the Canadian production company or a prescribed person may control the initial licensing of commercial exploitation rights for the production.

- The Canadian production company (or a related prescribed taxable Canadian corporation) must retain an acceptable share of revenues from foreign exploitation of the production.

All other CPTC requirements still apply to treaty co-productions.

5.04 Treaty Coproduction Attestation Process

A CPTC certificate may be used by Canadian funding programs, broadcasters or regulatory authorities as recognition that a production has been granted treaty coproduction status by the Minister of Canadian Heritage.

However, there may be cases where a production is not eligible for the CPTC, despite conforming to the requirements of a coproduction treaty. This may occur, for example, where a CPTC application or certification deadline is not met, or where the production is an interactive digital media production that is not eligible for the CPTC.

Upon request by the production company, CAVCO may in these cases issue a “coproduction attestation” letter, which provides a “CP” number for the production. This letter from the Director General, Audiovisual Branch on behalf of the Minister, confirming that the project has achieved treaty coproduction status outside of the framework of the Act, may then be filed with funders, broadcasters or other authorities as necessary.

Contact CAVCO for details on how to apply for a coproduction attestation letter.

5.05 International Co-ventures

Co-ventures are international productions that are not produced in accordance with an audiovisual coproduction treaty. Co-ventures do not qualify for the CPTC.

Additional information on co-ventures can be found in the Guide to the CRTC Canadian Program Certification Application Process.

6. Key Creative and Producer-Related Personnel

In this section

- 6.01 Requirements for Proof of Canadian Citizenship or Permanent Residency

- 6.02 Key Creative Personnel – Live Action Productions

- 6.03 Key Creative Personnel – Animation Productions

- 6.04 Key Creative Point Requirements for Documentaries

- 6.05 General Rules for Evaluating Key Creative Points

- 6.06 Screenwriters

- 6.07 Lead Performers (live action) / Lead Voices (animation)

- 6.08 Music Composer

- 6.09 Producer-related Personnel

- 6.10 Production Control

- 6.11 Chain-of-title Documentation

- 6.12 Exemptions for Non-Canadian Producer-Related Personnel

- 6.13 Non-Canadian Showrunners

6.01 Requirements for Proof of Canadian Citizenship or Permanent Residency

6.01.01 Overview

To be eligible for CPTC certification, a production must meet requirements related to the staffing of Canadian key creative and producer-related personnel on the production. See sections 6.02 to 6.12 for more information on these requirements.

An applicant must provide proof that individuals for whom key creative points are being requested, as well as individuals occupying producer-related positions, are Canadian. This is demonstrated through the applicant providing CAVCO Personnel Numbers (also known as CAVCO IDs) for these individuals, within their application.Footnote 13

The term "Canadian," in this context, refers to a person who is a Canadian citizen as defined in the Citizenship Act, or a permanent resident as defined in the Immigration and Refugee Protection Act. The person must be Canadian during the entire time they perform any duties in relation to the production.

Note that this use of the term “Canadian” is different from the definition of “Canadian” found in the Investment Canada Act, used for determining whether a production company is Canadian-controlled (see section 2.01).

6.01.02 Permanent residents of Canada

A permanent resident of Canada is a person who has acquired permanent resident status pursuant to the Immigration and Refugee Protection Act. To maintain this status, the person must meet certain minimum residency requirements during each five-year period.

Permanent residents may apply for Canadian citizenship once they have been ordinarily resident in Canada for at least three of the previous five years, and have met certain other requirements.

For more information on permanent residency status or obtaining Canadian citizenship, consult the Immigration, Refugees and Citizenship Canada website.

6.01.03 CAVCO Personnel Numbers

To obtain a CAVCO Personnel Number, an individual occupying a key creative or producer-related position must submit an application with a document demonstrating Canadian citizenship or permanent residency. More information on the application process for CAVCO Personnel Numbers is available on the CAVCO Personnel Number webpage.

Each individual confirmed as a Canadian citizen or permanent resident is assigned a unique CAVCO Personnel Number. Production companies applying to CAVCO for a production must obtain these numbers directly from individuals occupying key creative or producer-related roles. CAVCO does not provide these numbers to production companies.

Canadian citizens need to apply only once for a CAVCO Personnel Number.

Permanent residents need to resubmit proof of permanent residency status when their permanent resident card expires. CAVCO Personnel Numbers issued to permanent residents have a zero as the first digit in their numerical portion (e.g., ABCD0123).

CPTC applicants must ensure that any Canadian filling a producer-related or key creative role in their production has obtained a CAVCO Personnel Number. Production companies are encouraged to obtain the numbers at the time of hiring any individuals occupying these positions.

If the CAVCO Personnel Number provided to a production company identifies an individual as a permanent resident, the production company should ensure that the individual can demonstrate, with a valid permanent resident card, that they have permanent resident status at the time they are providing services to the production.