PACP Committee briefing binder: Appearance by the Deputy Minister of Employment and Social Development – December 2025

Official title: Appearance by the Deputy Minister of Employment and Social Development, Standing Committee on Public Accounts (PACP), study: Auditor General of Canada 2024 Report 5 - Professional Services Contacts, date: December 11, 2025, 11:00 a.m. to 1:00 p.m.

On this page

1. Opening remarks

Opening remarks for Paul Thompson, Deputy Minister of Employment and Social Development Canada, for an appearance before the Standing Committee on Public Accounts: 2024 Auditor General of Canada Report 5 on Professional Services Contracts

Thank you, Mr. Chair and committee members.

I want to acknowledge that we are meeting on the traditional unceded territory of the Algonquin Anishinaabeg People.

I'm here with (introduction of other ESDC officials at the table).

And I am honoured, as Deputy Minister of Employment and Social Development Canada, to discuss Report 5 of the Auditor General of Canada's 2024, regarding ESDC's Professional Services Contracts.

And I would like to thank the Committee members for their diligent study of this issue.

I would also like to thank the Office of the Auditor General for their report.

ESDC fully agrees with its recommendations, and we acknowledge and support all findings in the report.

Pause

I'd like to use this time to highlight ESDC's overall use of professional services.

I'll discuss the important role contractors play in our work for Canadians.

I'll highlight our lessons learned and changes we've implemented in response to the report's findings.

But first I'll start by talking about ESDC's overall approach to the use of professional service contracts.

We manage many diverse programs and services across Canada.

And contractors have specialized skills and expertise that help make sure they're delivered efficiently, effectively, and prudently.

Citizen-centred programme delivery is at the core of our contracts, all of which are tailored to specific operational needs.

Our Benefits Delivery Modernization program is a perfect example.

It's a massive undertaking to help build a new platform to help Canadians to find, apply for, and manage federal benefit programs.

It's also the largest and most ambitious IT transformation initiative ever undertaken by the Federal Government.

And a project of this scale wouldn't have been possible without hiring contractors.

Public servants work alongside the experts in these companies to learn from them and deliver the platform as promised.

Canada's Old Age Security program was the first program to migrate to the new platform.

This happened in March 2025 with roughly 7.4 million existing OAS clients migrating to the new platform.

Employment Insurance is next underway.

And once again, migrating a program as large as EI over the next several years wouldn't be possible without hiring contractors.

We manage a range of large-scale programs across diverse business lines, some of which are well suited for delivery by third parties through professional services contracts.

The Canada Student Loans and Grant program and Service Canada's 1-800 O-Canada service are two such activities.

Pause

Mr. Chair, we've developed a detailed Management Response and Action Plan in response to the findings in Report 5.

We've also introduced measures to address the findings of Government-wide procurement audits conducted by the Office of the Procurement Ombuds and the Office of the Comptroller General. Here are a few examples.

In April 2024, our Chief Financial Officer hosted an educational session for all ESDC executives on proper contracting of professional services.

In June 2024, we revised and published our Procurement Roadmap instructions on Mandatory Methods of Supply and Exemption processes for all staff.

We also communicated changes to the Treasury Board of Canada's Directive on the Management of Procurement to ensure implementation of these new measures,

Finally, to remind all of ESDC's section 34 managers of their financial responsibilities, we shared an email illustrating how stewardship is central to effective resource management.

And all action items resulting from the recommendations of all three audits were completed on time.

Mr. Chair, the steps we've taken to address the recommendations mainly focus on reducing reliance on professional services, and our current forecasts project this trend to continue.

This will be done in support of the Budget's commitment to reduce expenses on management and other consulting services by 20 per cent in three years' time.

Closing

ESDC remains fully committed to open, transparent, and fair procurement processes.

We'll continue to refine our processes to deliver the greatest value for Canadians.

They deserve no less.

Thank you for your time, Mr. Chair, and I'm happy to take members' questions.

-30-

2. Scenario note

The Standing Committee on Public Accounts (PACP)

Auditor General of Canada 2024 Report 5 - Professional Services Contracts

December 11, 2025, 11:00 a.m. to 1:00 p.m.

Overview

- On October 2, 2025, the House of Commons Standing Committee on Public Accounts (PACP) sent an invitation to the Auditor General and deputy ministers from several departments to appear for its study of the Auditor General of Canada's 2024 Report 5-Professional Services Contracts

- The first meeting took place on October 9, with the following organizations appearing before the committee: Canada Infrastructure Bank, Department of National Defence, Department of Public Works and Government Services, and the Office of the Auditor General

- The second meeting was held on November 18, with representatives from the Office of the Auditor General and the CFO of Trans Mountain Corporation

- A third meeting was held on December 2 with witnesses from Immigration, Refugees and Citizenship Canada (IRCC), the Business Development Bank of Canada (BDC), Canada Post Corporation, and the Office of the Auditor General (OAG)

- You will be appearing as part of a panel for the fourth meeting on this report, alongside the Office of the Auditor General of Canada (OAG), Canada Border Services Agency (CBSA), Innovation, Science and Economic Development Canada (ISED) and Public Sector Pension Investment Board (PSP)

Committee proceedings

- During this appearance, you, the Auditor General and officials from CBSA, ISED and PSP will be afforded the opportunity to deliver opening remarks for five minutes each. Following that, questioning will begin

- The first round of questions will give six minutes each to the CPC, LPC and BQ, in that order.

- The second (and subsequent rounds) of questions allocate five minutes to the CPC and LPC, two and a half minutes to the BQ, and then five minutes to the CPC and the LPC

- You will be accompanied by:

- John Ostrander, Business Lead, Benefits Delivery Modernization

- Serena Francis, Chief Financial Officer

About the audit

- The objective of the OAG audit, which was tabled in Parliament on June 4, 2024, was to determine whether professional services contracts were awarded to McKinsey & Company in accordance with applicable policies and whether value for money for those contracts was obtained

- The audit assessed whether the 20 federal organizations (federal departments and Crown corporations) ensured that value for money was received for the 89 sampled contracts within the audit period

- For the period between August 2020 and June 2022, ESDC awarded four non-competitive contracts worth $5.8 million (before tax) to McKinsey & Company. Of the four ESDC contracts, the OAG selected one contract valued at $40,000 for an in-depth examination, which was a non-competitive (sole sourced) contract. The OAG refers to this contract as the "original noncompetitive contract" in the chain of four ESDC's non-competitive contracts awarded to McKinsey

- Most of findings from the OAG's government-wide sample of 89 contracts, including ESDC's $40,000 contract, are reported in an aggregated manner

- Although findings related to ESDC's $40,000 contract are not explicitly discussed in the report, there were some compliance challenges with this contract, which were also raised in the Internal Audit report published in 2022. These challenges included a lack of documentation to substantiate the need for external consultant services, insufficient monitoring of the contract, and vague statement of work

- The report also comments on the other three non-competitive contracts with this vendor in the chain of the four ESDC's contracts with McKinsey

- The findings related to ESDC include:

- failing to fulfill its commitment to compete the subsequent contracts after the initial $40,000 sole-source contract

- questions the use of the non-competitive procurement vehicle (National Master Standing Offer) established by Public Services and Procurement Canada (PSPC)

- questions why ESDC waited for more than a year for this non-competitive procurement vehicle to be established by PSPC

- The OAG issued one recommendation to all departments in scope related to conflict-of-interest declarations in contracting processes, including our department

- ESDC agreed with the recommendation and although ESDC prepared a response to the recommendation and an action plan, instead of having all departments respond to the recommendation individually, TBS prepared a response on behalf of the Government of Canada

Parliamentary environment

- Prior to the prorogation and dissolution of the previous Parliament, opposition parties were seized with government contracting issues, including the frequent awarding of contracts to McKinsey & Company. In January 2023, the House of Commons Standing Committee on Government Operations and Estimates (OGGO) requested the Auditor General of Canada to conduct a performance and value-for-money audit of the contracts awarded to McKinsey & Company since January 1, 2011, by any department, agency, or Crown corporation. The House of Commons unanimously passed a motion to move forward with this request on February 7, 2023

- The Auditor General appeared before PACP on June 4, 2024, on her three spring reports of that year

- More recently, the Auditor General appeared before PACP on June 19, 2025, on Report 4-Professional Services Contracts with GC Strategies Inc. of her 2025 audits. With its emphasis on professional services contracts, this audit is related to the one in question. During the June 19, 2025, meeting, the 2024 audit that focussed on McKinsey was referred to by many committee members

- Moreover, some of the Auditor General's messages, as well as the concerns of members apply directly to the purpose of this appearance. Much of the discussion revolved around the following of basic procurement rules, with the Auditor General stating that "I think deputy ministers should be coming here to speak to why their procurement processes, and their procurement officers were not following procurement rules."

- Members can therefore be expected to ask what has been done to ensure compliance, what measures have been put in place and to seek assurances that the demonstration that external professional services are really required is clearly stated, that value for money is clear, and that knowledge transfer to public servants is occurring

- Finally, during that meeting, the Deputy Auditor General stated that "[o]ne thing that I think might help public servants is if simplification can be implemented. We found in, for example, our McKinsey report-and it would apply more broadly-that the understanding of the way that standing offers are used, and particularly whether they're competitive or not, is an area that Public Services and Procurement Canada and central agencies can make easier for the public service to understand and, by virtue of that, make it easier for them to follow the rules." Although this comment isn't directly aimed at line departments, members may ask whether any thought has been given to simplification of processes

- On October 9, 2025, PACP convened to begin this study of Report 5, Professional Services Contracts. The Committee heard testimony from the Office of the Auditor General, Public Services and Procurement Canada, the Department of National Defence, and the Canada Infrastructure Bank. Discussions focused on federal procurement practices, with particular attention to the government's reliance on external consultants such as McKinsey, efforts to improve transparency, accountability, and value for money in contracting

- During the November 18, 2025, meeting, the Committee Chair addressed participants, noting recent delays and coordination challenges. He reminded members of the committee's authority and expectations for witnesses: individuals called to appear must be accountable and able to speak on behalf of their organization, and commitments to attend must be honored. The Chair also referred to obligations under the Financial Administration Act regarding the appearance of accounting officers and reiterated the committee's power to summon witnesses if necessary.

- The December 2, 2025, meeting, focussed on value for money in consulting contracts, heavy reliance on external consultants, fairness and transparency in procurement, and security risks such as unauthorized network access. The committee emphasized the need for stronger documentation of decisions, reduced dependence on consultants, and adherence to competitive procurement processes

Conservative Party of Canada

- During the June 2024 meeting, CPC members were concerned about the increasing value of contracts and hidden costs, and favouritism due to "friends" of the previous Prime Minister finding themselves as the recipients of lucrative contracts

- MPs repeatedly discussed violation of conflict-of-interest rules and of policies

- During the debate on ordering this audit, CPC MPs accused the then-Prime Minister of waste and corruption

- During the June 2025 meeting, CPC members' questions were centered on ministerial accountability, and the "inability to follow the rules", meanwhile during the early October meeting, CPC MPs raised broader concerns related to government contracting, including issues surrounding the efforts to recover funds from GC Strategies and potential conflicts of interest in the procurement processes

- During the December 2, 2025, meeting, Mr. Deltell asked whether McKinsey helped resolve the passport backlog during the COVID crisis. IRCC Deputy Minister Kochhar, explained that McKinsey was engaged for digital transformation, not passport services, and that the backlog was managed internally in collaboration with ESDC. He further clarified the division of responsibilities: IRCC holds the policy authority, while ESDC is responsible for the delivery of passports to Canadians

Bloc Québécois

- At the June 2024 meeting, the BQ accused the government of violating the law when it comes to contracting and made comparisons to ArriveCAN and GC Strategies. The lack of justifications for non-competitive contracting processes was also discussed

- At the June 2025 meeting, the BQ member had only a few questions on professional services and was mainly concerned about the costs of IT contracts, the transfer of knowledge to public servants that should flow from these and made links to the SAAQclic situation and the Gallant Commission in Quebec

- During the October 9, 2025, meeting, on this report, the BQ member questioned the government's increasing use of consultants and the challenge of developing internal expertise even suggesting improving public sector work conditions to attract talent. The Benefits Delivery Modernization initiative was raised, with the MP expressing concerns over escalating costs, IBM's contract growing from $1.75 billion in 2021 to $4.4 billion in 2024, and projections exceeding $5 billion. Questions were raised about the absence of rigorous cost management or digital transformation within the Department

3. PACP Committee members biographies

Committee Membership and Biographies

Standing Committee on Public Accounts (PACP)

Mandate of the Committee

- When the Speaker tables a report by the Auditor General in the House of Commons, it is automatically referred to the Public Accounts Committee. The Committee selects the chapters of the report it wants to study and calls the Auditor General and senior public servants from the audited organizations to appear before it to respond to the Office of the Auditor General's findings. The Committee also reviews the federal government's consolidated financial statements - the Public Accounts of Canada - and examines financial and/or accounting shortcomings raised by the Auditor General. At the conclusion of a study, the Committee may present a report to the House of Commons that includes recommendations to the government for improvements in administrative and financial practices and controls of federal departments and agencies.

- Pursuant to Standing Order 108(3) of the House of Commons, the mandate of the Standing Committee on Public Accounts is to review and report on:

- the Public Accounts of Canada

- all reports of the Auditor General of Canada

- the Office of the Auditor General's Departmental Plan and Departmental Results Report, and,

- any other matter that the House of Commons shall, from time to time, refer to the Committee

Committee operating procedures

Witness' opening statements: 5 minutes

Questions Round 1

1- Conservative: 6 minutes

2- Liberal: 6 minutes

3- Bloc Québécois: 6 minutes

Questions Round 2 (and subsequent rounds)

1- Conservative: 5 minutes

2- Liberal: 5 minutes

3- Bloc Québécois: 2.5 minutes

5- Conservative: 5 minutes

6- Liberal: 5 minutes

Anticipated TBS-Related Activity - 45th Parliament

- Public Accounts 2025

- Real Property

- Professional Service Contracts

Committee members

Name: John Williamson

Role: Chair

Party: Conservative

Riding: Saint John-St. Croix

PACP Member since: June 2025, Chair since October 2022, Previously a Member in 2013 and from 2022 to 2025

Name: Jean Yip

Role: Vice-Chair

Party: Liberal

Riding: Scarborough-Agincourt

PACP Member since: June 2025, Previously a Member from 2018 to 2025

Name: Sébastien Lemire

Role: Vice-Chair

Critic for Public Accounts

Party: Bloc Québécois

Riding: Abitibi-Témiscamingue

PACP Member since: June 2025

Name: Gérard Deltell

Party: Conservative

Riding: Louis-Saint-Laurent-Akiawenhrahk

PACP Member since: September 2023, Previously a Member from 2017 to 2018

Name: Ned Kuruc

Party: Conservative

Riding: Hamilton East-Stoney Creek

PACP Member since: June 2025

Name: Stephanie Kusie

Critic for Treasury Board

Party: Conservative

Riding: Calgary Midnapore

PACP Member since: June 2025

Name: Kristina Tesser Derksen

Party: Liberal

Riding: Milton East-Halton Hills South

PACP Member since: June 2025

Name: Tom Osborne

Parliamentary Secretary to the President of the Treasury Board

Party: Liberal

Riding: Cape Spear

PACP Member since: June 2025

Name: Anthony Housefather

Party: Liberal

Riding: Mont Royal

PACP Member since: June 2025

Bio of the members of the committee

John Williamson (Saint John-St. Croix, NB) Conservative Chair

- Elected as MP for New Brunswick Southwest in 2011, he was then defeated in 2015 and re-elected in 2019, 2021 and 2025

- Currently also serves as a Member of the Liaison Committee and Chair of the Subcommittee on Agenda and Procedure of the Standing Committee on Public Accounts

- Previously served on many committees, including PACP for a brief time in 2013

- Prior to his election, M. Williamson occupied different positions. He was an editorial writer for the National Post from 1998 to 2001, then joined the Canadian Taxpayers Federation until 2008. In 2009, he was hired by Stephen Harper as director of communications in the PMO. Interest in the TBS portfolio:

- OAG Performance audits

- integrity of the Public Service

- transparency & Accountability

Jean Yip (Scarborough - Agincourt) First Vice-Chair, Liberal

- Elected as MP for Scarborough-Agincourt in a by-election on December 11, 2017, and re-elected in 2019, 2021 and 2025

- Has served on Public Accounts (since 2018), as well as Government Operations and Canada-China committees in the past

- Also serves on the Special Committee on the Canada - People's republic Of China Relationship and as Vice-Chair of the Subcommittee on Agenda and Procedure of the Standing Committee on Public Accounts

- Before her election, Ms. Yip was an insurance underwriter and constituency assistant

- Interest in the TBS portfolio:

- GBA+ and gender and diversity considerations in the Public Accounts

- Environmental, Social, and Governance reporting

Sébastien Lemire (Abitibi-Témiscamingue, QC), Bloc Québécois Second vice-chair

- Elected as the Member of Parliament in 2019 for Abitibi-Témiscamingue, re-elected in 2021 and 2025

- BQ critic for Public Accounts, Sport and Indigenous Relations and Northern Development

- Previously served on Indigenous and Northern Affairs and Industry and Technology

- Before politics, he worked at the Fédération de l'UPA d'Abitibi-Témiscamingue, the Juripop Legal Clinic, Octane stratégies, and the Forum jeunesse de l'Île de Montréal of the Conférence régionale des élus de Montréal

- Interest in the TBS portfolio:

- OAG Performance audits

- Government Accountability

Gérard Deltell (Louis-Saint-Laurent-Akiawenhrahk, QC) Conservative

- Elected as the Member of Parliament in 2015 for Louis-Saint-Laurent, re-elected in 2019, 2021 and 2025

- Previously served on many committees, including Public Accounts

- Was leader of the Action démocratique du Québec from 2009 to 2012.

- Prior to his election, he was a journalist with TVA, Radio-Canada and TQS

- Interest in the TBS portfolio:

- Professional Service Contracts

Ned Kuruc (Hamilton East-Stoney Creek, ON), Conservative

- Elected as the Member of Parliament in 2025 for Hamilton East-Stoney Creek

- Prior to his election, he was an entrepreneur and was Director of Events and Fighter Acquisitions at K-1 Global

- Interest in the TBS portfolio:

- Professional Service Contracts

- Government Accountability

Stephanie Kusie (Calgary Midnapore, AB), Conservative

- Elected as the Member of Parliament in 2017 for Calgary Midnapore, re-elected in 2019 and 2021

- Conservative Shadow Minister for Treasury Board

- Previously sat on the Standing Committees of Official Languages, Procedure and House Affairs, and Transport

- Has a B.A in political science from the University of Calgary and an M.B.A. from Rutgers University

- Prior to her election, Ms. Kusie occupied multiple positions, including chargé d'affaires ad interim for Canada to El Salvador, consul for Canada to Dallas, Texas and senior policy advisor to Peter Kent in Latin America

- Some of her duties before her time in office included negotiating free trade deals, work related to the Keystone Pipeline project, and lobbying the United Nations to place Canada on the Security Council

- Interest in the TBS portfolio:

- Government Spending

- Government use of Professional Service Contracts

- Whistle Blowers / Disclosure of wrongdoing in the workplace

Kristina Tesser Derksen (Milton East-Halton Hills South, ON), Liberal

- Elected as the Member of Parliament in 2025 for Milton East-Halton Hills South

- Attended the University of Toronto where she obtained a law degree

- Prior to her election, she served two terms on the Milton Town Council

- Interest in the TBS portfolio:

- Professional Service Contracts and the Government's Legal Liability

Anthony Housefather (Mount Royal, QC), Liberal

- Elected as the Member of Parliament in 2015 for Mount Royal, re-elected in 2019, 2021 and 2025

- Previously served on many committees, including Justice and Human Rights, Government Operations and Access to Information, Privacy and Ethics

- Attended McGill University where he obtained two law degrees, he also has an MBA from Concordia University's John Molson School of Business

- Prior to his election, he served as Executive Vice President Corporate Affairs and General Counsel at a multinational technological company

- He also served as mayor of Côte Saint-Luc between 2005 and 2015

- Interest in the TBS portfolio:

- Professional Service Contracts and the Government's Legal Liability

Tom Osborne (Cape Spear, N.L.), Liberal

- Elected as the Member of Parliament in 2025 for Cape Spear

- Attended Cabot College and Memorial University of Newfoundland

- Prior to his election, he was a member of the Newfoundland and Labrador House of Assembly from 1996 to 2024 where he held several cabinet posts including Minister of Finance and President of the Treasury Board

- Interest in the TBS portfolio:

- Professional Service Contracts

- Procurement Rules

4. Questions and Answers on Professional Services at ESDC

Professional Services

Q1. What is the value of professional services expenditures by Employment and Social Development Canada (ESDC)?

In fiscal year (FY) 2024-25, ESDC reported $998.5 million in professional and special services expenditures, a decrease from $1.02 billion in 2024. The majority of these expenditures supported core operational and modernization priorities, including:

- Business Services ($454M): Operational support such as program administration (e.g., Canada Student Loans, Labour Market Development Agreements - transfer payments to provinces) and logistics

- Informatics Services ($447M): IT infrastructure and digital transformation initiatives, including re-platforming federal benefit systems (EI, CPP, OAS)

- Management Consulting ($29M): Strategic advisory services to enhance departmental efficiency and service delivery

These investments reflect ESDC's continued focus on service modernization, operational excellence, and program integrity.

Based on an analysis of departmental expenditures in the top three reporting categories - Business Services, Informatics Services, and Management Consulting - as well as some expenditures under Business Development and Modernization (BDM), we estimate that spending on per diem-based consultants in FY 2024-2025 was approximately 10% of the $998.5M.

Q2. Do these expenditures align with established procurement benchmarks or industry standards?

- Overall, these expenditures demonstrate ESDC's commitment to responsible stewardship of public funds, continuous improvement, and alignment with government-wide priorities for digital transformation, accountability, and service excellence.

- Major initiatives such as BDM leverage vendors with global experience in executing complex, large-scale business transformations. ESDC also engages independent third-party firms to conduct objective assessments, ensuring accountability and informed decision-making throughout the transformation process.

Q3. What percentage of the Department's budget was spent on professional services?

Percentage (%) of the Department's total budget:

| FY | Professional Services Spending | Total Operating Expenses | Percentage of Total Operating Expenses |

|---|---|---|---|

| 2019-202020 | $680M | $4.2B | 16.2% |

| 2020-2021 | $840M | $6.1B | 13.8% |

| 2021-2022 | $960M | $5.8B | 16.5% |

| 2022-2023 | $960M | $6.4B | 15.1% |

| 2023-2024 | $1.02B | $6.6B | 15.5% |

| 2024-2025 | $998.5M | $6.5B * | 15.4% |

- *Note: For comparative purposes, total operating expenses for FY 2024-25 have been reduced by $3.9B to exclude an exceptional and material bad debt expense associated with COVID related benefits.

Q4. What are the five largest professional services expenditure categories at ESDC?

According to Volume III of the Public Accounts of Canada, for the 2024-2025 fiscal year, the five largest professional services expenditure categories at ESDC are as follows:

- Business Services: $454.2 M (includes Canada Student Loan, Labour Market Development Agreements, call centre operations and warehousing)

- Informatics Services: $446.8M (includes IT infrastructure and software support)

- Management Consulting: $29.2M (includes BDM governance and planning)

- Legal Services: $19.9M (includes specialized legal expertise and support)

- Training and Educational Services: $15.6M (includes staff training for digital systems)

These categories collectively represent the operational backbone of ESDC's modernization and service delivery efforts.

Q5. What is the the spending trajectory regarding professional services?

The table below provides total professional services expenditures over the last 5 years (excluding BDM). Please note that 2025-2026 is based on the best available forecast at P6. Overall, these expenditures demonstrate ESDC's commitment to responsible stewardship of public funds, continuous improvement, and alignment with government-wide priorities for digital transformation, accountability, and service excellence.

Text description graphic 1

The expenditures are distributed as follows

| Fiscal Year | Professional Services Expenditures (excluding BDM) |

|---|---|

| 2021-2022 | $921,909,914 |

| 2022-2023 | $833,709,032 |

| 2023-2024 | $794,412,608 |

| 2024-2025 | $807,124,061 |

| 2025-2026 | $746,234,474 |

ESDC is showing a stable/slight decrease over the years including a forecasted decrease in 2025-2026. There is also a stable trend in the 3 major professional services categories when excluding BDM and a decrease in informatic services.

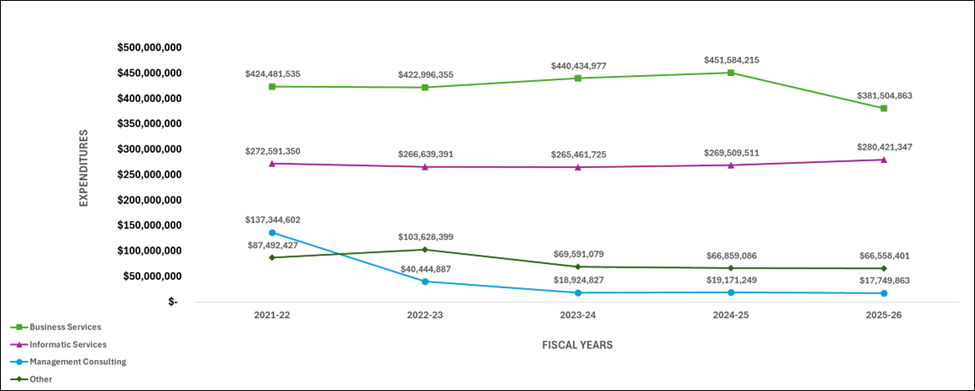

Text description graphic 2

The expenditures are distributed as follows

| Type of expenditures | 2021-2022 | 2022-2023 | 2023-2024 | 2024-2025 | 2025-2026 |

|---|---|---|---|---|---|

| Business Services | $424,481,535 | $422,996,355 | $440,434,977 | $451,584,215 | $381,504,863 |

| Informatic Services | $272,591,350 | $266,639,391 | $265,461,725 | $269,509,511 | $280,421,347 |

| Management Consulting | $137,344,602 | $40,444,887 | $18,924,827 | $19,171,249 | $17,749,863 |

| Other | $87,492,427 | $103,628,399 | $69,591,079 | $66,859,086 | $66,558,401 |

Business Services: Approximately 80 % of the expenditures in this category is non-discretionary. They related to operational support such as program administration (for example, Service Provider for Canada Student Loans, Labour Market Development Agreements) and Centrally Managed Cost Pools.

Informatics Services: IT infrastructure and digital transformation initiatives, excluding re-platforming federal benefit systems (BDM).

Management Consulting: Strategic advisory services to enhance departmental efficiency and service delivery.

*Other: Legal services, training, interpretation and translation services, Health and Welfare Services, Scientific and Research Services, Temporary Help Services and Special fees and services

Q6. What is the rationale for hiring consultants?

Consultants provide a flexible and rapid deployment of resources with specialized skills and expertise to support ESDC's operational requirements and internal systems, specifically providing guidance for the department's transformation efforts, and to help ensure ESDC programs and services are delivered efficiently, effectively, and prudently.

Q7. How does ESDC ensure value for money in professional services contracts?

To strengthen oversight and ensure value for money in professional services procurement, new measures have been introduced for contracts based on hourly or daily rates. These include enhanced benchmarking against market standards and clearer expectations for cost-effectiveness. Vendor performance management has also been formalized as a mandatory requirement for new professional services contracts, supporting greater accountability and improved outcomes.

Q8. How does the department ensure that the use of consultants complements, rather than replaces, the work of public servants?

- ESDC engages consultants strategically to address temporary gaps in capacity or to access specialized expertise not readily available within the public service. These engagements are typically project-based and aligned with departmental priorities, such as the development and implementation of complex social programs, particularly during periods of exceptional demand, including the early stages of the COVID-19 pandemic. Professional services contracts are structured to include knowledge transfer components, ensuring that public servants are equipped to sustain and manage solutions over the long term.

- The department remains committed to building internal capacity and reducing reliance on external resources as projects transition from development to operational phases. Notably, recent data indicates a substantial reduction in the number of active consultants across key branches, reflecting this shift toward sustainable, in-house delivery.

Q9. What steps is ESDC taking to reduce its reliance on consultants and optimize their use?

- A department-wide horizontal initiative is currently reviewing the use of consultants across ESDC. This exercise provides a high-level assessment of consultant engagements, with a focus on staff augmentation and per diem-based contracts. It supports strategic decision-making through targeted reviews, quarterly monitoring, and improved workforce planning.

- The initiative aims to reduce reliance on high-cost consultants by distinguishing core from non-core activities, evaluating opportunities to internalize expertise, and prioritizing high-usage areas. Reviews are also underway to assess the necessity and value of atypical or high-cost consultant engagements.

Q10. How does ESDC demonstrate stewardship and responsible management of public funds in professional services procurement?

ESDC follows all applicable policies, directives, laws, and trade agreements, in all its procurement activities. Notably, ESDC, conducts procurements in line with the key principles found in Treasury Board's Directive on the Management of Procurement, the Government Contracts Regulations (GCRs), and the guidance provided in PSPC's Supply Manual. Furthermore:

- per the requirements outlined in the Guide to the Proactive Publication of Contracts, ESDC proactively discloses all contracts/amendments valued over $10,000.00, on a quarterly basis

- ESDC carries out thorough due diligence to uphold principles of transparency and ensure value for money in all contracting activities. ESDC's efforts are supported by the Procurement Review Committee (PRC), which provides a challenge function aimed at upholding the principles of fairness, openness, transparency, and sound contract management

- ESDC relies on Public Services and Procurement Canada's (PSPC) mandatory government-wide procurement tools to manage professional services contracts, ensuring optimal value from private sector engagements, stronger contract oversight, and increased accountability for business owners

Q11. How is centralized procurement data being leveraged to strengthen departmental oversight and inform strategic decision-making?

ESDC has implemented a centralised procurement repository to strengthen oversight and accountability across all branches. This integrated platform enables real-time tracking of consultant numbers, contract durations, and expenditure trends, providing leadership with a clear, department-wide view of professional services activity. By consolidating procurement data, ESDC can quickly identify opportunities for efficiency, monitor compliance with new policies, and ensure resources are allocated where they deliver the greatest value for Canadians. The repository supports evidence-based decision-making and reinforces ESDC's commitment to transparency and responsible stewardship of public funds.

GC Strategies

Q12. Can you elaborate on ESDC's contracts with GC Strategies? What were they for?

- Project and portfolio management within ESDC is inherently complex, involving multiple programs, evolving priorities, and significant investments across diverse business lines. At the time, the department lacked a modern, integrated system capable of supporting strategic oversight, timely decision-making, and scalable deployment cycles.

- To address this gap, external expertise was required to design and implement a robust solution tailored to ESDC's needs. GC Strategies provided specialized technical resources to build and enhance the Project Management Information Solutions (PMIS), enabling the department to modernize its portfolio management practices while transferring knowledge to internal teams. PMIS is the departmental system of record and single source of truth for projects and programme. All project information such as individual project dashboards, periodic reporting and quarterly reports are produced by PMIS. The system helps manage a portfolio of approximately $550M per year with 58 active investment projects and programmes. Over the years, PMIS has supported ESDC with the management of over 600 projects.

Q13. What was the amount?

ESDC awarded three contracts to GC Strategies Inc. for a combined total of $3,132,343.05.

Q14. Will you be getting that money back?

ESDC did not find GC Strategies Inc. to be in violation of any contractual clauses, and we have not contested any work delivered. As such there are no grounds to seek restitution. ESDC has no active contracts with GC Strategies Inc. Additionally, the PSPC Contract Security Program (CSP) has revoked the organization security clearance held by GC Strategies Inc. effective April 3, 2024. As a result, no further contracts will be awarded by or on behalf of ESDC to this supplier.

Q15. Did you get value for money?

- The competitive procurement process enabled us to maximize value for money by leveraging vendor competition, which drove down costs while maintaining stringent quality standards and ensuring the suitability of the chosen vendor. The resources provided under each contract were retained and provided expertise that was otherwise not available through internal public servants at ESDC.

- This approach represented strong value for money. By leveraging external expertise to meet immediate technical needs while simultaneously transferring knowledge to internal Full-Time Equivalents (FTEs), PMIS actively matured its in-house capabilities. This strategic investment strengthened the Government of Canada's workforce in the areas of Information Management and IT solutions, reducing future dependency on external consultants.

Q16. What did they do and why couldn't that have been done in house?

- These contracts provided resources with specialized technical skills in the areas of Microsoft Project Server and Business Intelligence. These specialized resources were needed to support decision making within the organization by analysing, developing, testing, and deploying key IT solution modules for ESDC's Project Management Information Solutions (PMIS). The contracted consultants enabled the delivery of critical updates and new functionalities on a three-month deployment cycle, an essential cadence for maintaining and improving the information management (IM) solution. As there were no internal FTEs with the required expertise at the time, external consultants were brought in to meet operational demands and initiate knowledge transfer to internal staff. Knowledge transfer was conducted daily, with the long-term goal of building internal capacity and reducing reliance on external consultants.

- PMIS was designated as ESDC's mandatory tool for managing all investment projects. At the time, the existing version did not meet organizational needs and required significant enhancements (first contract). Internal resources lacked the knowledge and expertise to build integration points between multiple applications, so external resources were engaged to deliver the solution. This resulted in the first integration between MS Project (project management information) and SAP (financials), automating the production of project reports, including dashboards.

- In 2017, enhanced portfolio capabilities were added to the tool, such as portfolio analytics to support senior management in making informed decisions based on various automated scenarios (second contract). To assist with portfolio prioritization, new registers were introduced to align with ESDC's maturity levels, including Benefits, Lessons Learned, Decision Log, and Project Dependencies (within ESDC).

- While ESDC was securing its Organizational Project Management Capacity Assessment (OPMCA) Level 3 certification, a new project was initiated to migrate the platform to an infrastructure nearing end-of-life. Although the migration project was halted before implementation, a new module to capture, monitor, and report on programs was successfully completed (third contract).

The details for each contract are listed below

- Contract 1 signed December 2, 2015: The purpose of this contract was to support implementation of PMIS Phase 2.

- Contract 2 signed July 11, 2017: The purpose of this contract was to support PMIS Phase 3.

- Contract 3 signed April 1, 2022: The purpose of this contract was to continue support and further enhance PMIS to support the ESDC investment initiatives and improve the current functionalities of the PMIS product to align with departmental Project and Programme Management Maturity.

Details deposed to Parliament regarding GC Strategies Inc.

Statement: Employment and Social Development Canada (ESDC) has reviewed the information available in its financial system and found 3 contracts for GC Strategies Inc. since November 4, 2015.

Amount of GC Strategies Inc. contracts: $3,132,343.05

Due diligence practices and status of contracts: All three contracts were awarded following competitive procurement processes under a PSPC method of supply. One contract was awarded on December 2, 2015; another on July 11, 2017; and a third on April 1, 2022. Following PSPC's suspension of the Supply Arrangements for GC Strategies Incorporated, on February 16th, 2024, ESDC discontinued work on all remaining Task Authorizations ahead of their planned expiry date of March 31st, 2024. ESDC has no active contracts with GC Strategies Inc.

McKinsey

Q17. Can you elaborate on ESDC's contracts with McKinsey and Company Canada?

From January 1, 2011, to the time of the audit, ESDC awarded four sole-sourced contracts to McKinsey & Company Canada for a combined total value of $6,640,140 (including tax). Contracts 2, 3 & 4 below were awarded under PSPC's National Master Standing Offer (NMSO) no. EN578-211925/001/ZM. The NMSO was issued on February 26, 2021.

Since May 31, 2023, ESDC has had no active contracts with McKinsey & Company Canada.

The details for each contract are listed below

- Contract 1 signed August 3, 2020 ($39,999.80): The purpose of this requirement was to support the Chief Operating Officer (COO), Chief Transformation Officer (CTO) and Senior Management by providing high-level advisory services to de-risk transformation as the organization continues to change and increase the likelihood of programme success. The contractor was required to provide access to expert, strategic and tactical advisory services related to the governance of business transformation design, change standards and implementation strategies to meet organizational objectives.

- Contract 2 signed March 25, 2021 ($339,894.84): Under a PSPC tool, to provide benchmarking services as per PSPC's national master standing offer.

- Contract 3 signed October 26, 2021 ($517,387.50): Under a PSPC tool, to provide benchmarking services as per PSPC's national master standing offer.

- Contract 4 signed August 17, 2022 ($5,742,857.53): Under a PSPC tool, to provide benchmarking services as per PSPC's national master standing offer. ESDC engaged McKinsey & Company Canada to support its Service Transformation by benchmarking customer experience and designing citizen-centric service journeys. This included developing client personas to enhance engagement, forming cross-functional delivery teams, establishing executive-level collaboration models, defining measurable outcomes for journey-based initiatives, and outlining the strategic role of a Chief Client Experience Officer to champion best practices and journey lab sponsorship.

Q18. In practical terms, what did McKinsey & Company Canada actually do?

To support ESDC's transformation agenda, McKinsey & Company Canada was engaged through four contracts to provide advisory services and benchmarking services using specialized tools, proprietary data, and global expertise. This work enabled the department to assess its performance against leading Canadian and international organizations, identify areas for improvement, and inform the design of strategic initiatives aimed at modernizing service delivery. These efforts are helping us better serve Canadians, for example, through the launch of the Seniors' Hub, a centralized online portal that simplifies access to retirement planning resources and benefits. Each contract also included a knowledge transfer component to build internal capacity and ensure long-term sustainability.

Q19. What led to the decision to engage external expertise instead of relying on internal resources?

- The services acquired under these contracts were not readily available within the public service. McKinsey & Company Canada provided specialised expertise in benchmarking, strategic planning, and transformation management capabilities essential to ESDC's modernisation agenda. Their tools and advisory support enabled the department to measure performance against national and international standards and identify service delivery barriers central to improving benefits and services for Canadians.

- Each contract was tailored to specific operational needs, and the resources provided were retained for the full duration of the agreements. These engagements supported complex initiatives and the transformation of citizen-centred programme delivery and aimed to reduce implementation risks, achieving sustainable outcomes, and accelerating performance improvements across departmental transformation initiatives.

- McKinsey & Company Canada external experts also played a key role in transferring knowledge to public servants, thereby enhancing internal competencies and advancing the department's transformation efforts.

Q20. How did you ensure that the government obtained value for money out of the McKinsey & Company Canada contracts?

The National Master Standing Offer (NMSO) under which this call-up was raised include a predetermined pricing structure. ESDC established the value of the contract based on estimated Level of Effort for the work required, using the pre-established per diem rates as outlined in the Standing Offer.

For the contract awarded outside the NMSO framework, ESDC assessed McKinsey & Company Canada's proposal against prevailing market rates. The contract was actively monitored by the project authority, and the contractor fulfilled all terms and conditions, providing the specified deliverables as outlined in the proposal.

Q21. Why did ESDC use a non-competitive, sole source process?

- The first contract (contract 1) was awarded by ESDC as a non-competitive contract pursuant to sec. 6 of the Government Contracts Regulations which states that contracts for services below $40,000 may be entered into without soliciting bids.

- The other contracts (contracts 2, 3 and 4) were awarded to McKinsey & Company Canada without a competitive bidding process due to the firm's exclusive ownership of proprietary data and research essential to meeting the project requirements. Three of these contracts were issued through Public Services and Procurement Canada's NMSO, a pre-approved framework that facilitates access to McKinsey & Company Canada unique benchmarking methodologies.

Management Action Plans

Q22. What were the department's responses to audits concerning its contracting practices with McKinsey & Company Canada, and what specific action plans or corrective measures were implemented in response to the findings?

A) Internal Audit

On February 8, 2023, the Treasury Board Secretariat asked ESDC and other departments to identify and undertake an internal audit of their contracts with McKinsey & Company Canada from January 1, 2011, to February 7, 2023. Per the direction of the Office of the Comptroller General, ESDC's Chief Audit Executive conducted a formal independent internal audit of the related procurement processes and reported the results on March 22, 2023.

Recommendation

The internal review resulted in a recommendation for the Chief Financial Officer to enhance controls governing the appropriate use of procurement tools, with particular emphasis on ensuring clear identification of whether the procurement method is competitive or non-competitive.

Action

Following the review, ESDC implemented the following measures to strengthen procurement tool oversight:

- the Procurement Master Checklist has been updated to include an instruction requiring contracting authorities to confirm whether the selected procurement tool was sourced competitively or non-competitively

- a formal email was distributed to procurement operations teams, emphasizing the importance of proper use of existing tools and the need to clearly determine their competitive status

- procurement operations staff were reminded during their respective team meetings of the importance of using procurement tools appropriately and were directed to review the updated instructions

B) Office of the Procurement Ombuds

- In March 2023, the Office of the Procurement Ombudsman (OPO) initiated a review of procurement practices used by federal departments and agencies in awarding service contracts to McKinsey & Company.

- The objective of the review was to assess whether procurement activities related to McKinsey contracts were conducted in accordance with the Financial Administration Act, applicable regulations, and relevant policies and procedures, and whether they upheld the principles of fairness, openness, and transparency. This audit resulted in one recommendation for ESDC.

Recommendation

ESDC, PCO, NRCan and DND should implement procedural controls to ensure mandatory methods of supply are utilized when required and exemptions from PSPC are sought and documented, when applicable.

Action

The department responded to the audit recommendation, agreeing to strengthen controls in our procurement process. An action plan was developed, notably:

- the CFO hosted an educational session for all ESDC executives on proper contracting of professional services in April 2024

- the Procurement Master Checklist was updated to include a new item, prompting contracting authorities to confirm that mandatory procurement tools are being employed, and exemptions are documented on file as outlined. News of the update was included in an email sent out to all procurement officers on May 23, 2023

- ESDC's Procurement Roadmap instructions on Mandatory Methods of Supply and Exemption processes were revised for clarity and made available to all ESDC employees in June 2024

- in December 2024, at a team Town Hall, the Executive Director of Procurement reminded all procurement officers of the importance of using procurement tools appropriately and also instructed them to review the provided guidelines

C) Office of the Auditor General

At the same time as the OPO audit, in March 2023, the Office of the Auditor General conducted an independent review of professional services contracts awarded to McKinsey & Company by federal departments, agencies, and Crown corporations. The audit assessed whether these contracts complied with applicable procurement policies and whether they delivered value for money. This audit resulted in one recommendation for ESDC.

Recommendation

To better ensure that those involved in the procurement process do not have conflicts-of-interest, organisations should implement a pro-active process to identify actual or perceived conflicts-of-interest in the procurement process and should retain the results of such process as well as completed conflict-of-interest declarations.

Action

ESDC fully implemented the following measures, further increasing transparency in the procurement process:

- for non-competitive contracts, procurement officers are required to obtain written confirmation from project authorities attesting that no actual or apparent conflicts of interest exist, to be kept in the contract file

- for competitive contracts, evaluators are required to sign a declaration on the evaluation grid confirming that no actual or apparent conflict of interests exist between the evaluators and the bidders

Conflicts of interest and Fraud Prevention

Q23. What are the compliance obligations for employees regarding ethical conduct and conflict of interest disclosures at ESDC?

- As outlined in the letter of offer, all employees are required to familiarize themselves with the Values and Ethics Code for the Public Sector, the Directive on Conflict of Interest, and the ESDC Code of Conduct. Compliance with these standards is mandatory both during and outside of working hours, including periods of approved leave (with or without pay)

- In addition, employees must complete a Conflict-of-Interest Disclosure within 60 days of their start date and whenever a significant change occurs in their personal affairs, interests, or official duties

- In response to the Office of the Auditor General (OAG) audit, ESDC fully implemented the following measures, further increasing transparency in the procurement process:

- for non-competitive contracts, procurement officers are required to obtain written confirmation from project authorities attesting that no actual or apparent conflicts of interest exist, to be kept in the contract file

- for competitive contracts, evaluators are required to sign a declaration on the evaluation grid confirming that no actual or apparent conflict of interests exist between the evaluators and the bidders

Q24. Can the department provide evidence demonstrating whether the implementation of conflict-of-interest declarations has led to any measurable outcomes or improvements in governance, transparency, or decision-making processes?

- In October 2025, the Office of the Procurement Ombud published a review of how federal departments manage the replacement of personnel in professional services contracts.

- The review found that ESDC's practices were fair, transparent, and aligned with Canada's goal of selecting the best value supplier. No recommendations were issued, and key observations highlighted ESDC's strong implementation of measures stemming from the McKinsey audits. The department was commended and OPO highlighted the following observations from ESDC's review:

- a fair and well-documented approach to supplier engagement during requirement development

- a clear application of conflict-of-interest protocols, and a transparent solicitation process

- robust controls in place for bid evaluations related to professional services

- the procurement files were described by OPO as "exceptionally well-documented"

Q25. What does ESDC do to detect and prevent fraud?

- ESDC performs integrity checks on suppliers and verifies the security clearance of resources, when applicable, and the Ineligible and Suspended Suppliers list maintained by PSPC is consulted prior to contract award.

- The department also relies on the Treasury Board's Directive on Delegation of Spending and Financial Authorities to ensure a scaffolded, risk-based approach by financial delegations in every step of the procurement process.

- Finally, ESDC's procurement operations are routinely audited and reviewed by the department's Internal Audit branch, which serves as an accountability measure as required in the Financial Administration Act.

Fraud Risk Assessment

- As part of its ongoing commitment to strengthening safety protocols and protecting the integrity of its procurement processes, ESDC commissioned a Fraud Risk Assessment of the department's procurement operations.

- The Fraud Risk Assessment (FRA) continues to serve as a proactive and strategic component of the department's anti-fraud framework, enabling early identification of potential risks and reinforcing fraud prevention and detection capabilities across operations.

- Since FY 2019-2020, the annual FRA has informed continuous improvements to internal tools and processes. The 2024-2025 assessment led to a series of targeted recommendations, all of which have now been implemented:

- procurement staff have completed the Preventing Fraud in the Workplace e-learning course, enhancing their ability to recognize, prevent, and report fraud through practical, scenario-based learning

- fraud prevention resources from PSPC's Fraud Detection and Intelligence Directorate have been featured in the monthly Procurement, Asset, Intellectual Property and Policy (PAIPP) newsletter, reinforcing awareness of risks in federal contracting

- a bidder's declaration is in the process of being integrated into procurement templates, developed in consultation with Legal Services to address identified risks while ensuring alignment with the Government of Canada's Code of Conduct for Procurement

Q26. Investigations by PSPC found that 3 subcontractors for professional services undertook contract work across 36 Government of Canada departments and agencies. These individuals fraudulently billed the Government of Canada by an estimated $5 million by billing multiple organizations for the same period under multiple separate contracts. Is ESDC one of those 36 Departments?

Yes. The contracts in question are:

- contract no. 2000126 with Eagle Professional Services

- contract no. 2000160 (G9292-201781/001/ZM) with IPSS Cyber Solutions, and

- contract no. 2000065 (G9321-130001-010-ZM) with Veritaaq Technology House

Q27. Will ESDC recover overpayments under these contracts?

Yes, the restitution process is centralized and led by PSPC on behalf of all affected departments. PSPC has the authority to seek restitution from suppliers. This amount is estimated at $355K for all three contracts.

5. Employment and Social Development Canada (ESDC) 2024 to 2025 Departmental Results Report / Gross Operating Actual Spending

To deliver its programs and services, ESDC's actual operating spending in 2024 to 2025 was $5,467.6M.

The department has a complex funding model financed via voted appropriations (the Consolidated Revenue Fund or CRF), as well as the authority to recover costs from the Employment Insurance (EI) Operating Account, the Canada Pension Plan (CPP), and other entities.

Descriptive text of the figure

Left section

Gross operating expenditures were $5,467.6 million

Middle section

- Voted appropriation from the Consolidated Revenue Fund was $1,455.7 million

- Authority to recover costs from the EI Operating Account was $2,228.6 million

- Authority to recover costs from the CPP was $559.0 million

- Authority to recover costs from other entities was $1.1 million

- Service delivery partnership agreements (DESDA) were $502.2 million

- Other operating was $721.0 million [note: Other operating included: $489.6 million for EBP, $122.7 million for statutory Pandemic Benefits, $90.1 million in statutory administrative fees related to Canada Student Loans and Apprentice Loans, $16.1 million in net expenditures for Federal Workers' Compensation, and $2.5 million for other items.]

Right section

Internal operating actual spending was $4,244.4 mil lion

6. Q&As on BDM Contracting - Standing Committee on Public Accounts

For Deputy Minister Paul Thompson Binder Meeting of December 11, 2025

Background: BDM Programme - Report of the PACP - Oct 2025.pdf

Contracts and consultants

Q1: Please describe the competitive process that was undertaken to select the core technology suppliers (IBM for Cúram) and the four system integrators (Accenture, CGI, Deloitte, and Fujitsu)?

- The BDM Procurement Strategy was designed to be scope flexible, minimize Programme risks, and allow contractual off-ramps at each Tranche of the BDM Programme

- Through extensive industry consultations from 2016 to 2017, held by Public Service and Procurement Canada (PSPC), and learning from past IT transformation projects, options were explored to leverage the capabilities of more than one industry provider, to de-risk programme capacity challenges, and to mitigate the risk of single point of failure by relying on one transformation partner

- As part of this engagement, in May 2018, 21 vendors provided extensive feedback on two proposed procurement approaches, this feedback was leveraged to develop a hybrid between the options which became the official final strategy endorsed by ESDC, PSPC, SSC, and TBS through the ESDC Deputy Minister Governance and Oversight Committee

- Working with PSPC, the Programme then created a qualified group of suppliers, which includes some of the world's leading technology developers and System Integrators (SI)

- To select the four SIs that would form the Qualified Supplier Working Group (QSWG), PSPC held multiple procurement events and issued an Invitation to Qualify process to qualify up to four SIs and up to four Core Technology suppliers. The ITQ process took place from Summer 2018 to Winter 2019. It was

followed by a Review and Refine Requirements phase to establish the QSWG (Winter 2019 - Fall 2020). It was this Invitation to Qualify that yielded the group of Accenture, CGI, Deloitte, and Fujitsu as SIs, and IBM as the Core Technology Vendor

Additional information

Adopting the ecosystem approach was designed to give ESDC the flexibility to access best-of-breed technology products and services, including SI services from the marketplace, while maintaining a competitive environment among vendors to secure best value. The approach enables Programme flexibility to adapt to market changes, to leverage the private sector's range of capabilities, improve velocity of the Programme to increase productivity, and to manage risks associated with complex transformation.

Q2: IBM contract: What is the real value of the contract?

The IBM contract value for CTV is $117 million (including taxes) for the software licenses, maintenance and support, professional services and training, over a 10-year period ending in 2031. As of October 21, 2025, a total of $97 million (including taxes) has been spent.

Q3: How much money has been awarded to each system integrator (Accenture, CGI, Deloitte, and Fujitsu) and for what activities?

The Qualified System Integrators are responsible for implementation, integration, transition, development, testing, delivery and (potentially) service management of part or all of the BDM Solution.

Timeline: April 30, 2021 to June 18, 2025

Joint System Integrator contributions

- OAS on BDM: Planning, design, demonstration, and detailed data analysis specific to OAS

- Common Benefits Delivery (CDB): co-developing tools and resources for onboarding processes and streamlining CBD efforts for Employment Insurance

- Integrated project teams: Established cross-company project teams for common benefit Codebase refactoring and onboarding strategies to leverage collective strengths

- BDM Integrated planning for the onboarding of the next benefit

- EI on BDM: Planning, design, and proof of concept

- Integration Advisory Services: Strategic technical advisory to projects and senior leadership, collaboration to create a unified framework or best practices document for integration, with contributions from all vendors

- Security and identity management advisory services business requirements

Accenture: $173,881,377.32 (incl. taxes)

Key contributions

- Development of the Service Delivery Hub foundation

- EI jurisprudence search aid development

CGI: $61,549,294.74 (incl. taxes)

Key contributions

- Development of the Benefit Application Development foundation

- Implementation of Digital Experience and Client Data (DECD) initiatives

Deloitte: $388,081,085.61 (incl. taxes)

Key contributions

- Delivery of the OAS solution and transformation

- Development of integrity by design foundations

- Best Practices related to implementation of risk-based processing

- Integrated Interface for AI Delivery (IIAID)

Fujitsu: $44,423,811.04 (incl. taxes)

Key contributions

- Development of the BDM technology platform cloud foundation

- Services to Support Strategic Partnership & Coordination (SSPC) with BDM delivery activities

Additional Information

In addition to each of the Tranche deployment activities, Qualified System Integrators will also be expected to support planning activities for subsequent Tranches. Other vendors may be responsible for performing similar roles, if and where appropriate. To date, the SIs have developed all required prototypes to drive the transformation projects, have led numerous transformations and innovations across the different BDM projects and initiatives. Currently, Deloitte is leading the delivery of the OAS on BDM solution and Accenture is leading the EI transformation

Q4: What role did Price Waterhouse Coopers (PWC) play with BDM and how much funding was directed their way (and for what key activities)?

- Following PSPC's extensive industry engagement in 2016 to 2017, a key recommendation emerged for BDM to bring in an industry partner from the private sector with demonstrated experience in large-scale business transformation to provide methodologies and expert advice, to stand up a Programme management capability to support planning and implementation, and to transition knowledge and skills to ESDC. Following a Request for Proposals (RFP), PricewaterhouseCoopers (PWC) was awarded the Transformation Programme Office (TPO) contract in December 2017

- To date, work completed under the TPO contract has totaled $157 million (incl. taxes). The contract expired on June 30, 2025

Background information

- Through the TPO contract, PwC was responsible for providing strategic advisory services to Canada and supporting with:

- establishing and managing an effective TPO

- informing the approach for BDM solution design and implementation, conducting readiness assessments to determine preparedness for implementation, executing on programme and project definition work, and

- developing draft programme documentation (for example, strategies, business and technical architecture, requirements, assessments, etc.)

- As part of a post-mortem examination of the TPO contract, the BDM Programme determined that it now possesses the required maturity, internal expertise and experience to effectively carry out the Programme Management functions.

Q5: If you have vendors in a qualified supplier group, why are contracts being awarded outside of it and for what? Please provide some highlights of how this $127M was spent.

Where appropriate, the BDM Programme engages suppliers beyond its Qualified Supplier Working Group to address capacity constraints and specialized skill gaps-particularly in emerging digital capabilities. We recognize that not all required expertise exists in-house, and actively seek industry partners who bring deep technical knowledge and innovative practices. These services are procured through existing PSPC and ESDC supply arrangements, as well as approved methods of supply, such as Interchange Agreements. This approach not only ensures access to critical skills, but also reinforces our commitment to knowledge transfer-embedding external expertise within our teams to build long-term internal capacity and support sustainable transformation.

Q6: How does BDM manage contracts and vendor partnerships to deliver successful outcomes for Canadians?

- There are multiple levels of reporting and oversight to the BDM Programme's relationship with vendors. BDM works as an integrated team with PSPC procurement, the delegated contracting authority for the Government of Canada (GoC), and ESDC Procurement, applying due diligence throughout the procurement and contract life cycle and in compliance with GoC procurement policies and regulations. All contracts have specified deliverables and/or milestones that must be met prior to payment being released

- BDM's Governance processes provide oversight and support of the Programme's procurement activities. For example, the Task Authorization Review Board is an advisory committee that provides advice to BDM on the issuance of contracts the execution of procurements, and supports the resolution of procurement-related issues. In addition, the Programme reviews the status of each deliverable, including dependencies and risks to assess progress towards completion. In the event deliverables are not tracking to plan, actions are developed to mitigate which may involve the Vendor, the Crown, or a combination of both. This level of integration ensures effective communication, knowledge sharing, and the cultivation of partnerships, setting BDM apart as a model of successful collaboration between government entities and external vendors

- Contract and resource management: Internal to the BDM Programme, there is a dedicated team responsible to implement due-diligence tasks outlined in BDM's due-diligence framework, developed in 2022. These tasks include documenting and monitoring security requirements, network access management, resource tracking and analysis. Continuous activities are completed to maintain knowledge and awareness of staff on responsibilities when managing contracts

Q7: What is the number of FTEs vs. contractors in BDM?

- As of October 31st 2025, BDM had approximately 1,100 full-time equivalents (FTEs). This includes about 465 internal FTEs, with the remainder distributed across ESDC and key stakeholder branches, including corporate services. It is important to note that FTEs represent workload capacity, not individual employees. The number of FTEs in BDM is not fixed and fluctuates based on the number and scale of active projects

- The BDM Programme currently contracts up to 120 consultant resources across its vendor ecosystem. This represents the number of resources paid on a per diem basis and does not account for third party resources working on deliverables or solutions-based contracts and Task Authorizations

Background information

- BDM is committed to providing HR planning that provides precision where it is known, realizing there will be some planning assumptions due to the Agile nature of the project management discipline. It is an evergreen document that is reviewed and refreshed regularly to ensure the needs of the BDM Programme are met in the most efficient way possible. It is important to underscore that all resource planning captures the level of horizontal effort to support Corporate departmental requirements across the projects. The foundational services support demands and activities that are consistently needed in a Programme and project environment, in particular a Pathfinder Programme such as BDM. That said, there are also costs that vary depending on the number of projects, the complexity of the projects and impromptu shifts to the organization and/or scope of work, as examples

- It is important to acknowledge the inherently dynamic nature of the Programme and its associated resource requirements. As the Programme evolves the number and composition of required resources are subject to change. This variability is not only expected but essential to maintaining the Programme's responsiveness and effectiveness. Resource allocation fluctuates over time to reflect BDM's emerging needs, the lifecycle of any given project, and the introduction of new streams of work or deliverables