Evaluation of the Old Age Security program: Phase 2

On this page

- List of acronyms

- List of figures

- List of tables

- Introduction

- Rationale for the Allowances and profile of recipients

- Deferral of the Old Age Security pension

- Management response and action plan

- Annex 1: Old Age Security program description

- Annex 2: Key findings of phase 1 of the evaluation

- Annex 3: Evaluation questions

- Annex 4: Limitations and summary of studies to support phase 2 of the evaluation

- Annex 5: References

List of acronyms

- CPP: Canada Pension Plan

- C/QPP: Canada or Quebec Pension Plan

- ESDC: Employment and Social Development Canada

- GIS: Guaranteed Income Supplement

- ISSD: Income Security and Social Development branch

- LICO: Low Income Cut-Off

- PASRB: Public Affairs and Stakeholder Relations Branch

- OAS: Old Age Security

- RRSP: Registered Retirement Savings Plan

List of figures

- Figure 1: Proportion of near-seniors receiving the Allowances

- Figure 2: Sources of total income of the recipients of the Allowance for the Survivor in 2016, by income range

- Figure 3: Sources of total family income of the recipients of the Allowance in 2016, by income range

- Figure 4: 2016 recipients of the Allowances

- Figure 5: Number of seniors receiving a deferred OAS pension (2014 to 2018)

- Figure 6: Distribution of lengths of deferral among 2013 cohort who received a deferred OAS pension in 2018

- Figure 7: Proportion of the 2013 cohort employed in 2013 to 2016 (%)

- Figure 8: Average individual income (in 2016 dollars) of the 2013 cohort in 2013 to 2016

List of tables

Alternate formats

Evaluation of the Old Age Security program: Phase 2 [PDF - 1.1 MB]

Large print, braille, MP3 (audio), e-text and DAISY formats are available on demand by ordering online or calling 1 800 O-Canada (1-800-622-6232). If you use a teletypewriter (TTY), call 1-800-926-9105.

Introduction

Program description

The Old Age Security (OAS) program is the first pillar of Canada's retirement income system. Program costs amounted to $51 billion in fiscal year 2017 to 2018Footnote 1, including $500 million for the Allowances.

The OAS program provides a basic pension upon which individuals may add income from other sources, such as the Canada or Quebec Pension Plan (C/QPP), employer pension plans and personal savings.

The OAS program includesFootnote 2:

- the OAS pension: a basic pension to nearly all seniors

- the Guaranteed Income Supplement (GIS): a supplement to low-income seniors

- the Allowances:

- Allowance (spousal Allowance): benefits to low-income near-seniors who are spouses of GIS recipients

- Allowance for the Survivor: benefits to low-income near-seniors who are widows or widowers

Near-seniors are defined in this evaluation as individuals who are 60 to 64 years old.

Evaluation context

The OAS evaluation was implemented in 2 phases.

Phase 1, completed in June 2018, focused on the labour market participation of OAS beneficiaries, the GIS top-up and service delivery. Key findingsFootnote 3 included the positive impact of the 2008 increase in the GIS earnings exemption (from $500 to $3,500) which:

- raised employment rates among recipients of the Allowances by 1 percentage point

- raised average employment income by 15% among working Allowances recipients

Phase 2 focuses on the Allowances and the deferral of the OAS pension:

- the rationale for the Allowances and the characteristics of recipients are examined as part of the first evaluation of the Allowances in the last 25 years

- the work and income profile of those deferring their pension, in addition to the incidence of deferral, provide the first assessment of deferral since its introduction in 2013

This evaluation supports efforts by the department to provide information to Canadians on deferral of the OAS pension and Canada Pension Plan (CPP) programs.

The Old Age Security pension and the Guaranteed Income Supplement contribute to reducing poverty in Canada

Recent resultsFootnote 4 indicate that:

- the OAS program contributed to reducing the percentage of seniors below Statistics Canada's Low Income Cut-Off (LICO) to 4% in 2015. This rate would have been 19 percentage points higher without the program

- OAS benefits represented 23% of seniors' after-tax income on average in 2015. The contribution of benefits to after-tax income of seniors varies by income group, with benefits representing 65% of income for those in the lowest income quintile and 8% of income for those in the highest income quintile

A previous evaluation in 2012 also showed that the program contributes to reducing poverty among seniors and that its benefits represent a significant proportion of seniors' incomeFootnote 5.

Rationale for the Allowances and profile of recipients

The Allowances were introduced to help alleviate financial difficulties of near-senior spouses of seniors, and then extended to widows and widowers.

1975: Introduction of the Allowance. 30% of married women participated in the labour market in 1970Footnote 6. Before the introduction of the Allowance, retirement of the husband led some couples to live on a single OAS/GIS benefit, as only 1 spouse had the age requirement to qualify for the OAS benefits.

1978: Extension of Allowance eligibility to widows and widowers to include the 6-month period following the death of the OAS pension recipient.

This was to recognize the difficult circumstances some near-senior spouses could face when their older spouse passes away (including losing their Allowance benefits and the OAS benefits of their spouse).

1979: Extension of Allowance eligibility to widows and widowers: 6-month limit was extended to continue until age 65 or remarriage, whichever came first.

1985: Extension of the Allowance eligibility to widows and widowers: Allowance for the Survivor was introduced for all near-senior widows and widowers.

Parliament raised concerns about the financial situation of many near-seniors, particularly single women, but it was too costly to expand the eligibility of the Allowance to all near-seniors.

Widows' vulnerability was highlighted:

- most had been financial dependents for most of their lives

- societal norms encouraged them to perform only unpaid roles (mother, housekeeper, community worker, etcetera)

- many would have difficulty finding paid work at the time

2019: The spousal Allowance was introduced in 1975. Since that time, the participation rate of women in the labour market has doubled (64% of married women participated in the labour market in 2018 versus 30% in 1970Footnote 7). This trend is likely to continue.

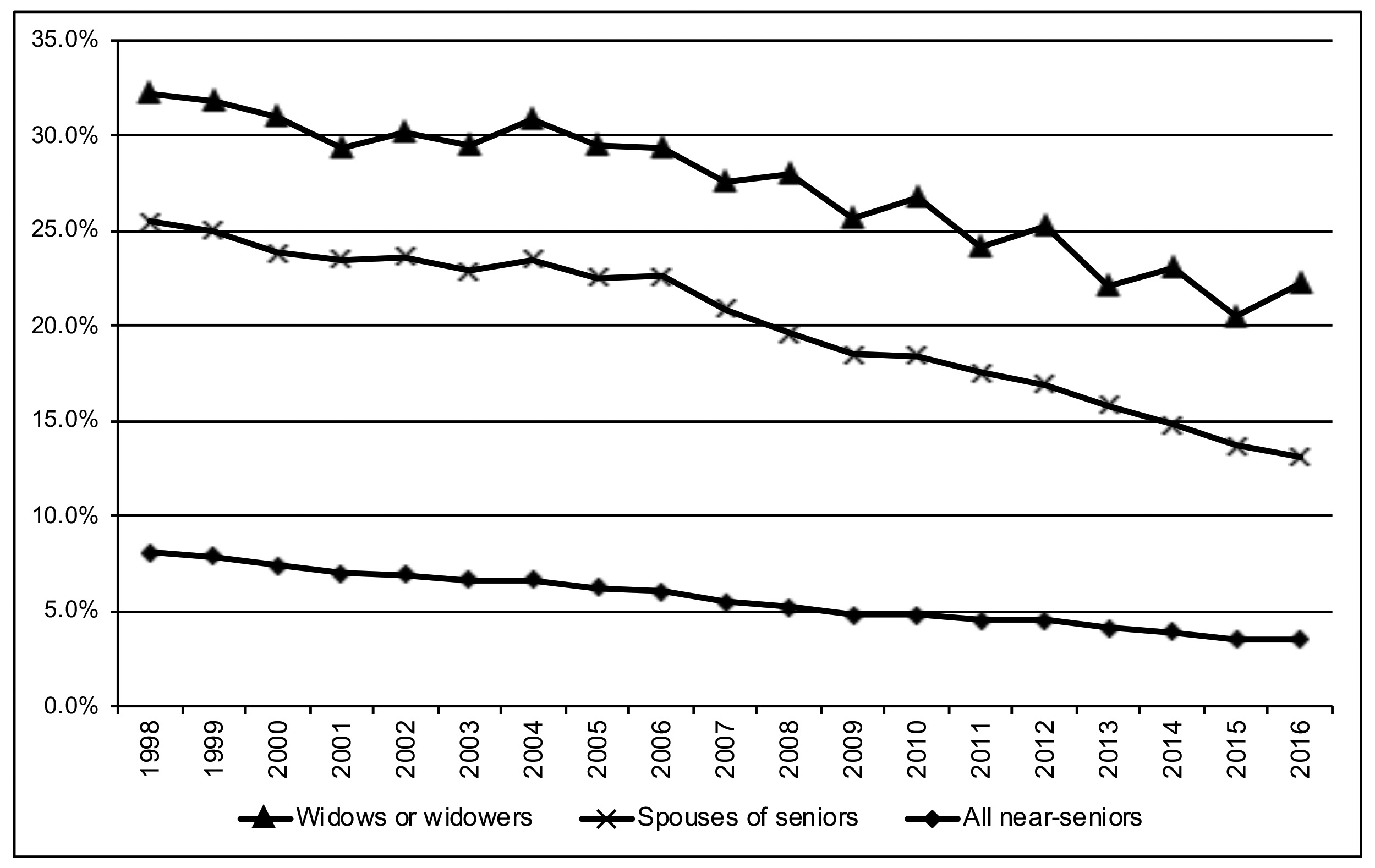

Recipients of the Allowances represent a small proportion of all near-seniors but a significant share of near-senior widows and spouses of seniors.

In 2016, recipients of the Allowances represented:

- 3% of all near-seniors (78,810 recipients)

- 22% of near-senior widows or widowers (24,900 recipients)

- 13% of near-senior spouses of seniors (53,910 recipients)

These proportions have been decreasing, as incomeFootnote 8 among near-seniors has increased.

Text description of Figure 1

| Year | Widows or widowers | Spouses of seniors | All near-seniors |

|---|---|---|---|

| 1998 | 32.2% | 25.5% | 8.1% |

| 1999 | 31.8% | 25.0% | 7.9% |

| 2000 | 31.0% | 23.8% | 7.4% |

| 2001 | 29.4% | 23.5% | 7.0% |

| 2002 | 30.2% | 23.6% | 6.9% |

| 2003 | 29.5% | 22.9% | 6.6% |

| 2004 | 30.9% | 23.5% | 6.6% |

| 2005 | 29.5% | 22.5% | 6.2% |

| 2006 | 29.3% | 22.6% | 6.0% |

| 2007 | 27.5% | 20.9% | 5.5% |

| 2008 | 28.0% | 19.6% | 5.2% |

| 2009 | 25.6% | 18.5% | 4.8% |

| 2010 | 26.7% | 18.4% | 4.8% |

| 2011 | 24.2% | 17.5% | 4.5% |

| 2012 | 25.2% | 16.9% | 4.5% |

| 2013 | 22.1% | 15.8% | 4.1% |

| 2014 | 23.0% | 14.8% | 3.9% |

| 2015 | 20.5% | 13.7% | 3.5% |

| 2016 | 22.2% | 13.1% | 3.5% |

Source: 10% sample of the T1 file from the Canada Revenue Agency.

80% of near-senior spouses of seniors and widows/widowers are women, half were working in 2016.

Most recipients of the Allowances had very low incomes, low levels of education, and were women.

Income distribution of recipients of the Allowance for the Survivor in 2016Footnote 9:

- 44% of recipients had income below $18,000

- 29% had income between $18,000 and $25,000

- 27% had income above $25,000Footnote 10

Since 1998, the average real income of recipients has increased (from $20,000 in 1998 to $24,000 in 2016)Footnote 11 Footnote 12

Income distribution of recipients of the Allowance (spousal) in 2016Footnote 13:

- 41% of recipients had family income below $30,000

- 33% had family income between $30,000 and $40,000

- 25% had family income above $40,000Footnote 14

Since 1998, the average real family income of recipients has increased (from $33,000 in 1998 to $37,000 in 2016)Footnote 15 Footnote 16

Gender of recipients of the Allowance for the Survivor in 2016:

- 87% of recipients were womenFootnote 17

Gender of recipients of the Allowance (spousal) in 2016:

- 89% of recipients were womenFootnote 18

Education of recipients of the Allowance for the Survivor in 2016Footnote 19:

- 41% of recipients had less than a high school degree

- 30% with only a high school degree

- 29% with other degrees

Education of recipients of the Allowance (spousal) in 2016Footnote 20:

- 37% of recipients had less than a high school degree

- 32% had only a high school degree

- 30% had other degrees

Due to the lack of 2016 data for the Market Basket Measure at the time of analysis (early 2018), 2016 before-tax LICO was used to present the incidence of low income.

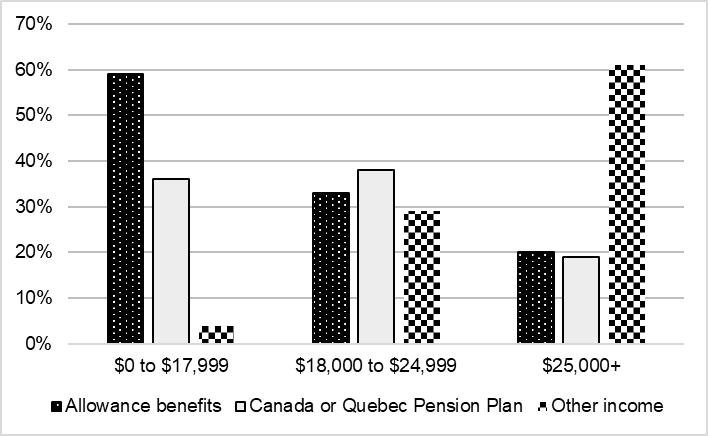

Allowance for the Survivor benefits account for a significant share of the income of most recipients.

In 2016, Allowance for the Survivor recipients with income below $18,000 relied mainly on Allowance benefits (representing 60% of income for the average recipient) and C/QPP benefits (35%) as their sources of income.

For recipients with income between $18,000 and $25,000, Allowance and C/QPP benefits represented together about 70% of their income, both with similar amounts.

For recipients with income above $25,000, Allowance benefits represented about 20% of their income.

Text description of Figure 2

| Income range | Allowance benefits | Canada or Quebec Pension Plan | Other income |

|---|---|---|---|

| $0 to $17,999 | 59% | 36% | 4% |

| $18,000 to $24,999 | 33% | 38% | 29% |

| $25,000+ | 20% | 19% | 61% |

Source: 10% sample of T1 file from the Canada Revenue Agency.

Note: Other income includes Registered Retirement Savings Plan (RRSP) withdrawals, employment income, other pension income (private pensions, annuities, Pooled Registered Pension Plans and Registered Retirement Income Funds withdrawals), and income from other sources.

The impact of the Allowance for the Survivor: benefits reduced the proportion under the after-tax LICO by 27 percentage points (from 53% to 26% of recipients) in 2011Footnote 21.

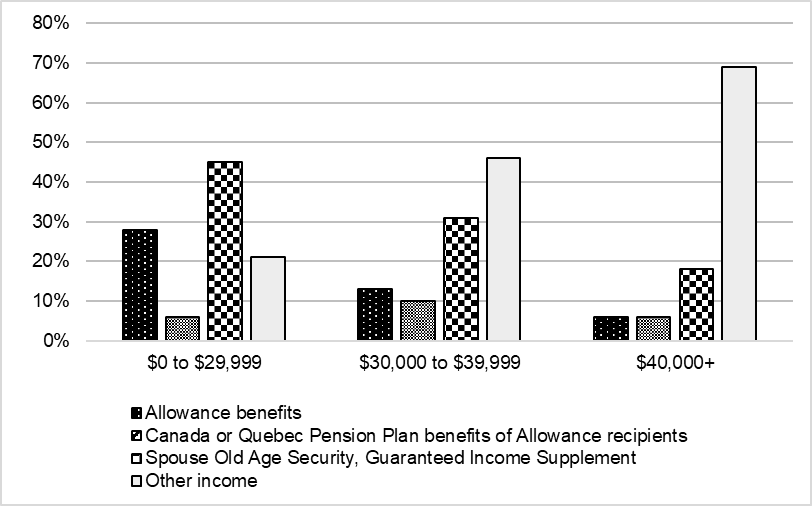

Allowance (spousal) and other OAS benefits account for a significant share of the family income of most recipients.

In 2016, recipients with family income under $30,000 relied mainly on OAS benefits (representing 75% of family income for the average recipient), including about a quarter of their income coming from Allowance benefits.

For beneficiaries with family income between $30,000 and $40,000, Allowance benefits represented about 15% of their income, with 45% of their income coming from OAS benefits (including the Allowance).

For beneficiaries with family income over $40,000, Allowance benefits represented only about 5% of their income.

Text description of Figure 3

| Income range | Allowance benefits | Canada or Quebec Pension Plan benefits of Allowance recipients | Spouse Old Age Security, Guaranteed Income Supplement | Other income |

|---|---|---|---|---|

| $0 to $29,999 | 28% | 6% | 45% | 21% |

| $30,000 to $39,999 | 13% | 10% | 31% | 46% |

| $40,000+ | 6% | 6% | 18% | 69% |

Source: 10% sample of T1 file from the Canada Revenue Agency.

Note: Other income includes RRSP withdrawals, employment income, other pension income (private pensions, annuities, Pooled Registered Pension Plans and Registered Retirement Income Funds withdrawals), and other individual or spousal income (excluding spousal OAS/GIS).

The impact of the Allowance: benefits reduced the proportion of recipients under the after-tax LICO by 11 percentage points (from 15% to 4% of recipients) in 2011Footnote 22.

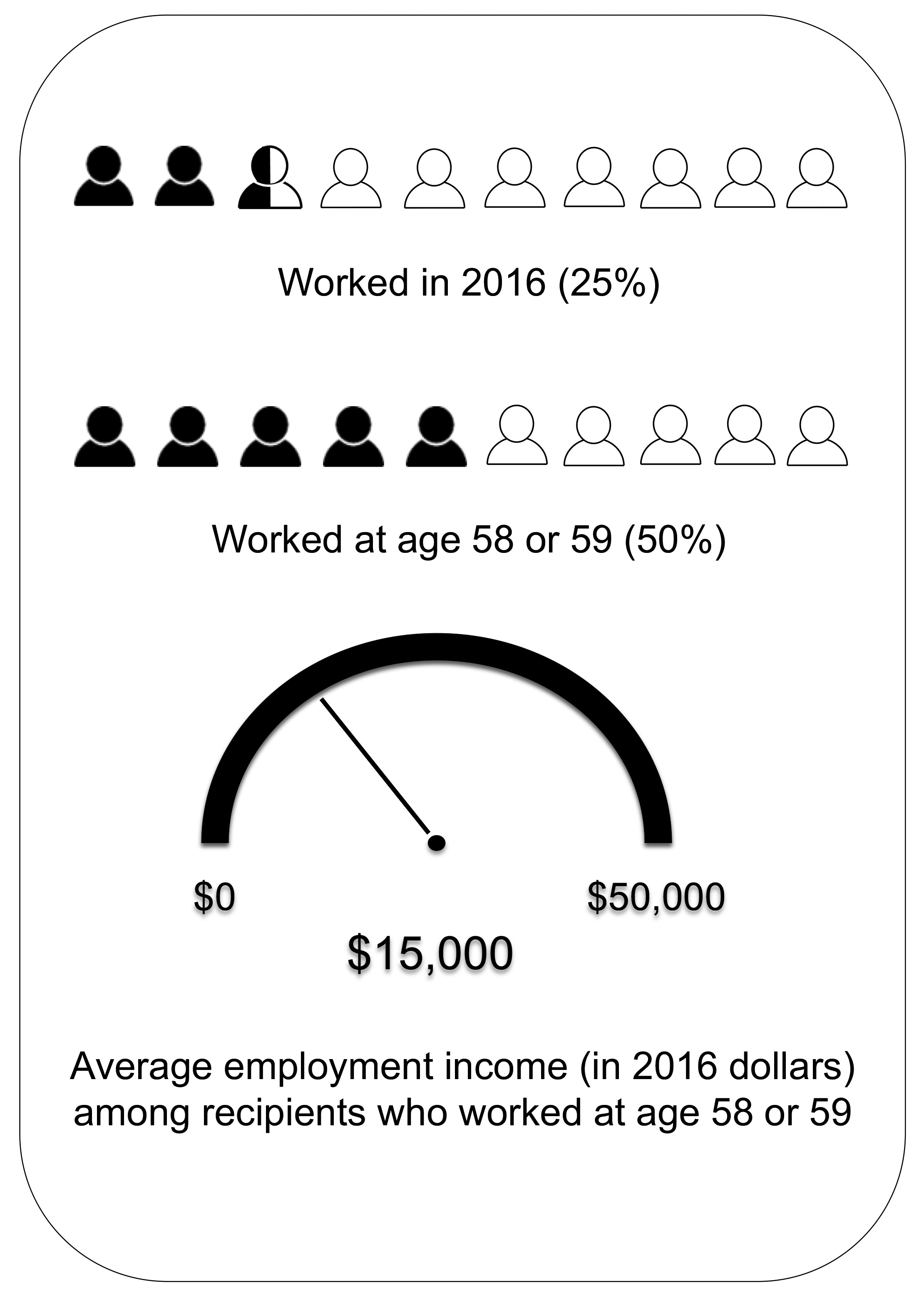

Most recipients of the Allowances did not have a significant attachment to the labour market, even at age 58 or 59.

- A quarter of all the recipients of the Allowances worked in 2016

- Half of the recipients of the Allowances worked when they were 58 or 59 years old

- Even among those who worked, employment income was already very limited at that age for most

Text description of Figure 4

25% of Allowances recipients worked in 2016. 50% of these recipients worked at age 58 or 59 and their average employment income was $15,000 (in 2016 dollars).

Source: 10% sample of T1 file from the Canada Revenue Agency.

The majority of low-income near-seniors are not eligible for the Allowances due to their marital status or the age of their spouse.

- In 2016, 600,000 near-seniors (or 27%) had income below the Allowances income qualifying thresholdsFootnote 23.

- About 450,000 (or 75%) of these individuals were near-seniors who did not have the marital status to qualify for the Allowances (they were not widowed or their spouse was younger than 65 years old)Footnote 24.

- 275,000 (or 45%) of these near-seniors were single and not widowed, half of which were womenFootnote 25.

- 180,000 (or 30%) of these were near-seniors with spouses younger than 65 years old, a third of which were womenFootnote 26.

Low-income non-widowed single near-seniors had lower income, on average, than recipients of the Allowance for the SurvivorFootnote 27.

- Over two-thirds of low-income non-widowed single near-seniors had income below $18,000.

- These individuals' income was lower on average than the ones for the Allowance for the Survivor recipients, mainly because they did not receive the Allowance benefits.

- This was the case for both women and men.

| Characteristic | All single near-seniors* | Recipients of the Allowance for the Survivor: total income* | Recipients of the Allowance for the Survivor: income excluding Allowance benefits* | Non-recipients of the Allowance for the Survivor: non-widowed single near-seniors* |

|---|---|---|---|---|

| Income distribution in 2016: $0 to $17,999 | 65.2% | 43.6% | 71.2% | 67.4% |

| $18,000 to $24,999 | 15.4% | 29.2% | 14.2% | 14.1% |

| $25,000+ | 19.5% | 27.2% | 14.6% | 18.6% |

| Average family income | $17,563 | $23,814 | $15,651 | $16,900 |

Source: 10% sample of T1 file from the Canada Revenue Agency.

Note: All single near-seniors include widowed, divorced, separated or never married.

*The table only includes near-seniors with income below the Allowance for the Survivor threshold.

The marital status requirement of the Allowance for the Survivor was challenged in Federal Court. The court ruled that the Charter of Rights does not require public pensions to provide the same benefits to everyone.

Low-income near-seniors with a spouse younger than 65 had lower income, on average, than recipients of the AllowanceFootnote 28.

Half of low-income near-seniors with spouses younger than 65 had family income below $30,000.

These near-seniors' family income was lower than the ones of the recipients of the Allowance, mainly because they did not receive Allowance benefits.

| Characteristic | All married near-seniors** | Recipients of the Allowance: total income** | Recipients of the Allowance: income excluding Allowance benefits** | Non-recipients of the Allowance: near-seniors with spouse younger than 65** |

|---|---|---|---|---|

| Income distribution in 2016: $0 to $29,999 | 49.0% | 40.7% | 57.5% | 52.6% |

| $30,000 to $39,999 | 21.6% | 33.1% | 22.3% | 18.7% |

| $40,000+ | 29.4% | 26.3% | 20.3% | 28.8% |

| Average family income | $35,212 | $36,596 | $31,363 | $34,281 |

Source: 10% sample of T1 file from the Canada Revenue Agency.

Note: Married near-seniors include those in a common-law relationship. All married near-seniors include those whose spouse is a senior (65+) and those whose spouse is younger than 65.

**The table only includes near-seniors with income below the Allowance threshold.

Even with a similar financial situation, all near-seniors do not receive the same financial support from the federal government as recipients of the Allowances do. However, individuals in this age group may be eligible for provincial or territorial assistance.

Conclusions on the Allowances

The Allowances are important for low-income near-seniors. Most recipients have very low income and benefits represent a significant proportion of their income.

Most recipients of the Allowances continue to be predominantly women, most have low levels of education and most had limited attachment to the labour market already at 58 and 59 years old.

The limited attachment to the labour market of married women was central to the rationale for introducing the Allowances. Social changes since the 1970s have been significant but challenges remain for many near-seniors.

There are also many vulnerable individuals among other single near-seniors and other near-senior couples whose marital status makes them ineligible for the Allowances.

Even with similar financial situations to recipients of the Allowances, they do not receive the same financial support from the federal government as recipients of the Allowances. However, individuals in this age group may be eligible for provincial or territorial assistance.

Recommendation

The department should take into account the evaluation findings to inform its analysis on the Allowances.

Deferral of the Old Age Security pension

Since 2013, seniors have the option to defer the start of their OAS pension by up to 5 years in exchange for a higher monthly payment.

The monthly OAS pension amount is increased by 0.6% for every month the OAS pension is deferred, up to a maximum of 36% (for delaying for 5 years), in addition to regular indexation of OAS benefits. The deferred pension amount is calculated on an actuarially neutral basis.

There are data lags when assessing the characteristics of those who defer their OAS pension.

- There is a 5-year data lag to identify all individuals that deferred in a cohort that reaches 65 years old. The data on the deferral decision is available only once the person starts receiving their OAS pension (or once their application is processed)

- Complete data on the first cohort of seniors who could have deferred for up to 5 years was available at the end of 2018. Partial data is available for younger cohorts

There is a limited number of seniors deferring their OAS pension, but it is rising.

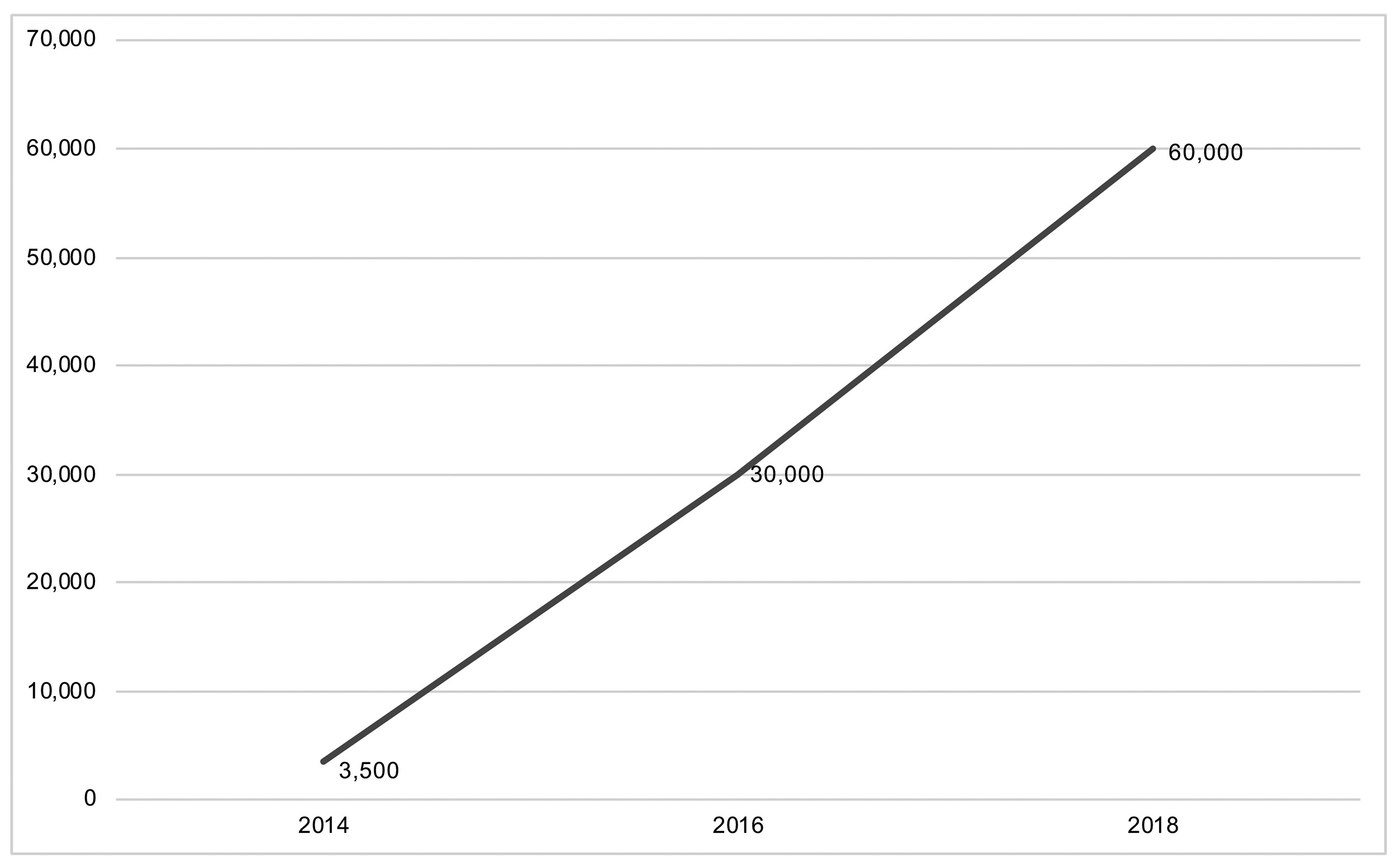

In 2018, 60,000 seniors received a deferred OAS pension, up from 3,500 in 2014 and 30,000 in 2016.

Text description of Figure 5

| Year | Number of seniors who deferred their Old Age Security pension |

|---|---|

| 2014 | 3,500 |

| 2016 | 30,000 |

| 2018 | 60,000 |

Source: 10% sample of linked T1 and OAS administrative data.

4% of seniors in the first eligible cohort chose to defer their OAS pension (Employment and Social Development Canada [ESDC], 2019b). This is in line with projections from the Chief Actuary.

One of the reasons few people choose to defer their OAS pension is awareness. A 2018 departmental online survey found that awareness of OAS deferral was low, with 25% of 60 to 64-year-old respondents aware they could defer their OAS pensionFootnote 29.

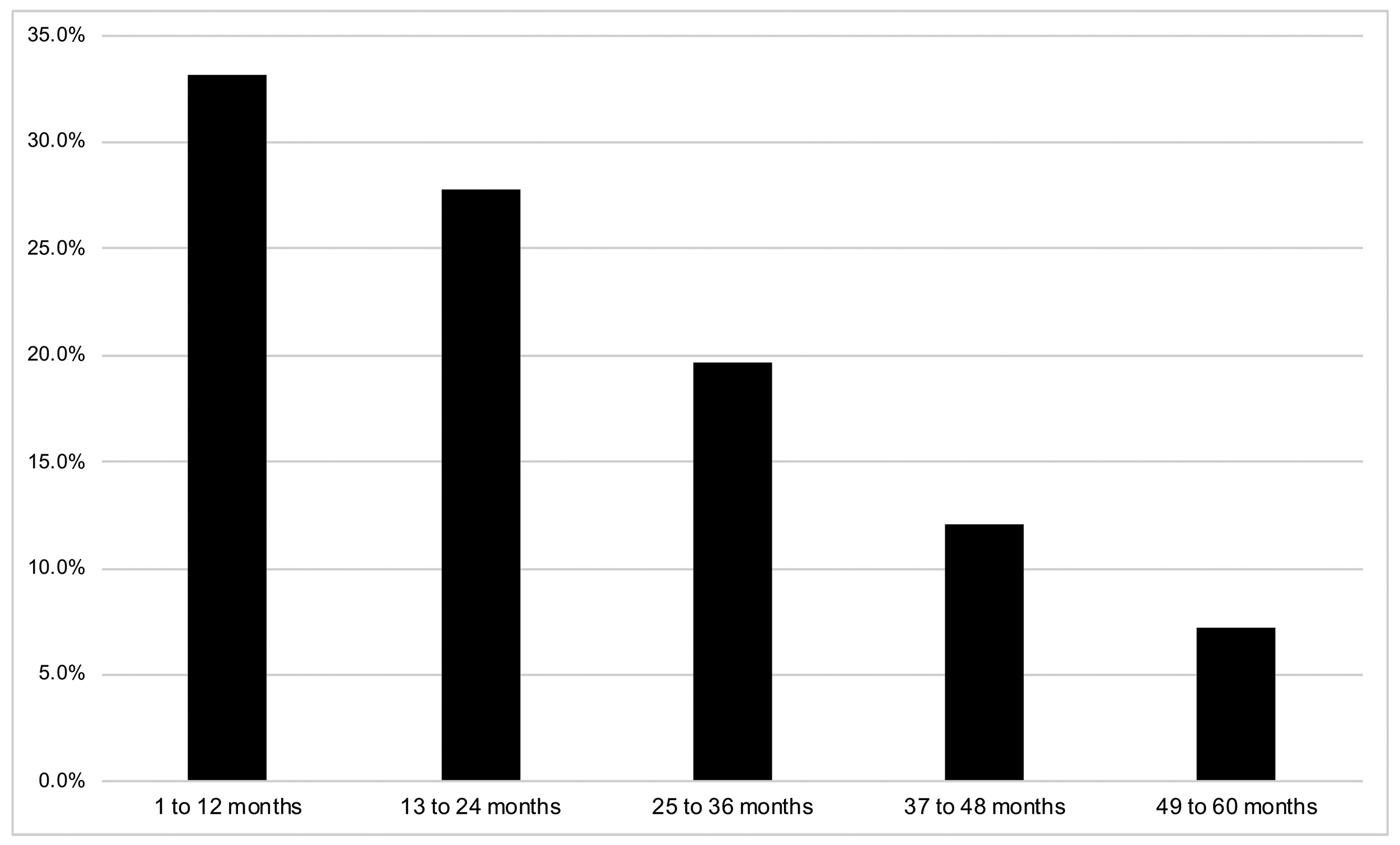

The length of deferral chosen varies among individualsFootnote 30.

Among seniors who deferred their OAS pension, the length of deferral was 23 months on average.

A third of seniors deferring did so for a year or less and over 60% for 2 years or less. Another 20% deferred for 2 to 3 years, while the remaining 20% deferred for more than 3 years.

Text description of Figure 6

| Length of deferral | Percentage of seniors deferring |

|---|---|

| 1 to 12 months | 33.2% |

| 13 to 24 months | 27.8% |

| 25 to 36 months | 19.7% |

| 37 to 48 months | 12.1% |

| 49 to 60 months | 7.2% |

Source: 10% sample of linked T1 and OAS administrative data.

Note: The 2013 cohort is the first cohort eligible for deferral. It includes only people reaching 65 years old in June to August 2013, due to data availability.

About 9% of those who deferred received the GIS in 2018. The average length of deferral was 17 months among GIS recipients.

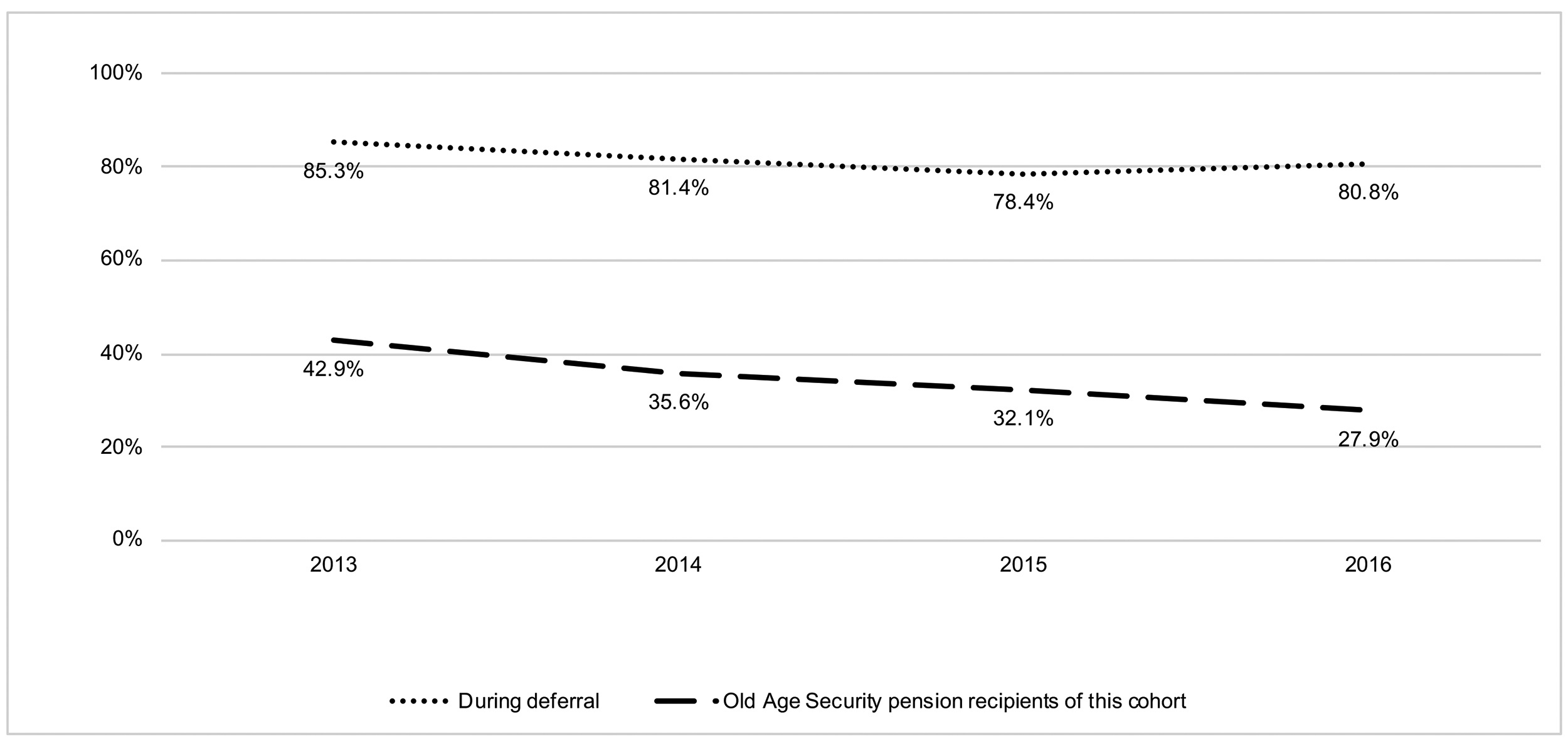

Most seniors worked during deferral and most had high income.

About 80% worked during deferral among the first 2013 cohort of seniors deferringFootnote 31. This is much higher than among OAS recipients of this cohort, among which the proportion working varied from 30% to 40%.

Text description of Figure 7

| Year | During deferral | Old Age Security pension recipients of this cohort |

|---|---|---|

| 2013 | 85.3% | 42.9% |

| 2014 | 81.4% | 35.6% |

| 2015 | 78.4% | 32.1% |

| 2016 | 80.8% | 27.9% |

Source: 10% sample of linked T1 and OAS administrative data.

Note: The 2013 cohort is the first cohort eligible for deferral. It includes only people reaching 65 years old in June to August 2013, due to data availability.

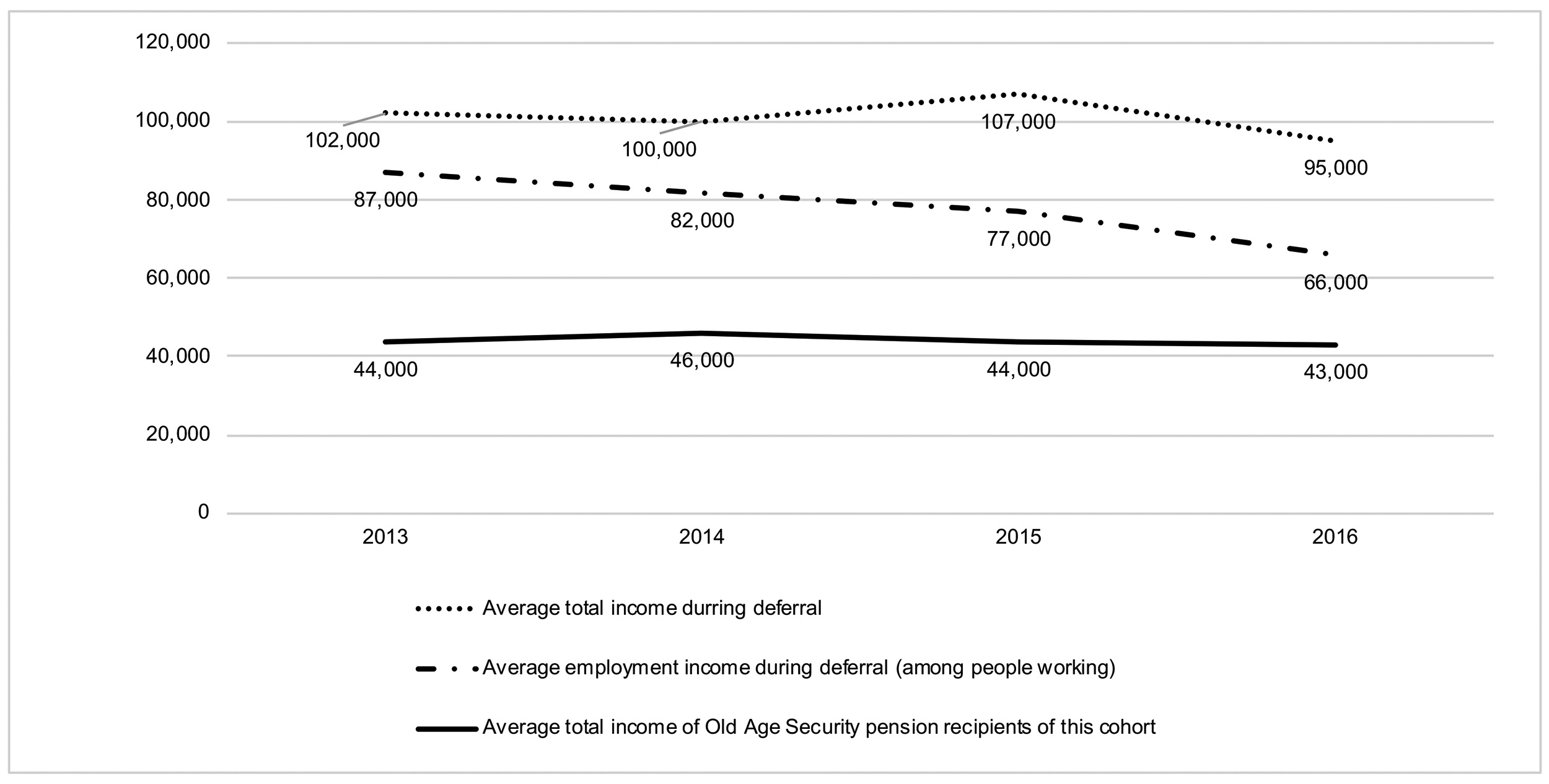

During deferral, the average individual income of these seniors was about $100,000 from 2013 to 2016, which is more than twice as much as among OAS recipients of this cohort.

Text description of Figure 8

| Year | Average total income durring deferral | Average employment income during deferral (among people working) | Average total income of Old Age Security pension recipients of this cohort |

|---|---|---|---|

| 2013 | 102,000 | 87,000 | 44,000 |

| 2014 | 100,000 | 82,000 | 46,000 |

| 2015 | 107,000 | 77,000 | 44,000 |

| 2016 | 95,000 | 66,000 | 43,000 |

Source: 10% sample of linked T1 and OAS administrative data.

Note: The 2013 cohort is the first cohort eligible for deferral. It includes only people reaching 65 years old in June to August 2013, due to data availability.

A similar pattern is present for family income, with the average during deferral almost twice as high as among OAS pension recipients of this cohort.

Many seniors deferring would have paid the OAS recovery tax if they had received the OAS pensionFootnote 32.

Nearly 60% of those deferring had income over $75,000 in 2013 to 2015, so they would have paid the OAS recovery tax if they had received the OAS pension. Over 30% of those deferring had income over $120,000 in 2013 to 2015, so they would have completely repaid their OAS pension through the OAS recovery tax if they had received the OAS pension in those years.

There are seniors deferring their OAS pension in all income groups.

| Characteristic | 2013 | 2014 | 2015 |

|---|---|---|---|

| Age | 65 | 66 | 67 |

| Individual income group (in 2016 dollars): $0 to $49,999 | 26.8% | 27.5% | n/a |

| $50,000 to $74,999 | 17.1% | 14.7% | n/a |

| $75,000 to $119,999 | 25.4% | 26.5% | 25.0% |

| $120,000+ | 30.8% | 31.4% | 36.2% |

Source: 10% sample of linked T1 and OAS administrative data.

n/a: not available due to small sample size.

The 2013 cohort is the first cohort eligible for deferral in 2013. It includes only people reaching 65 years old in June to August 2013, due to data availability.

Even after deferral, seniors are more likely to work and to have high family income.

Among seniors who deferred their OAS pension for up to 2 years in the 2013 cohortFootnote 33:

- 46% worked in 2016 (when they reached 68 years of age)

- average income was $65,000, with family income averaging $110,000 in 2016

In comparison, among all OAS recipients of the same cohort:

- 28% worked in 2016

- average income was $45,000 and average family income was $75,000 in 2016

There were people receiving a deferred OAS pension in all income groups.

Conclusions on Old Age Security deferral

Most seniors worked during deferral.

Most of those deferring had high income. However, there were seniors deferring their OAS pension in all income groups.

Awareness of OAS pension deferral is low, as is the proportion of seniors who chose to defer. About a quarter of 60 to 64-year-olds are aware of this possibility and 4% of the first cohort of eligible seniors chose to defer.

Raising awareness on deferral will help Canadians make better retirement planning decisions, including whether to continue working.

Recommendation

The department should continue to promote awareness of OAS pension deferral.

Management response and action plan

Overall management response

The evaluation is integral to ensuring that the OAS program remains relevant and continues to meet its objectives.

The department agrees with all of the report's recommendations and is pleased to present the following management response.

Recommendation 1

The department should take into account the evaluation findings to inform its analysis on the Allowances.

Management response

The department agrees with this recommendation and welcomes the new data the evaluation provides.

Historically, the Allowances were designed to:

- recognize the difficult circumstances that low-income couples face when living on only 1 pension until the other spouse becomes eligible, at age 65, for the OAS pension and the GIS (the Allowance); and

- assist 60 to 64-year-old widows or widowers who are facing financial difficulties and have not remarried or become the common-law partner of another person (the Allowance for the Survivor)

The OAS program is part of an extensive network of income security programs in Canada.

Generally, income security for low-income persons under the age of 65 is a provincial/territorial responsibility. There are various provincial/territorial programs in place to help people navigate through financially difficult periods in their lives.

While the evaluation has shown that other 60 to 64-year-old low-income individuals are not eligible for the Allowances, low-income individuals in this age group, such as single, separated or divorced individuals, who face financial hardship and meet the eligibility requirements may be able to receive social assistance from their province or territory of residence.

Furthermore, individuals who have contributed to the CPP or the Quebec Pension Plan are eligible to start receiving benefits at age 60.

Management action plan

1.1 No additional action required.

Completion date: completed.

Recommendation 2

The department should continue to promote awareness of OAS pension deferral.

Management response

The department agrees with this recommendation.

To measure awareness about pension deferral provisions, the department undertook an online survey in 2018, recruiting respondents among visitors, aged 40 to 64, to the canada.ca website.

The survey showed that awareness of the OAS pension deferral option was low, with only 17% of respondents aware that they could defer their OAS pension for up to 5 years, from age 65 to 70. Awareness was found to increase with age, income, education, and financial literacy. In addition, women had slightly lower awareness rates than men.

The department identified a series of actions to increase Canadians' awareness of the OAS deferral option and to ensure that Canadians have access to information about OAS deferral.

Several of these activities are already underway and include:

- using ESDC's social media channels to raise awareness, as well as publicly releasing the results of ESDC's online survey

- disseminating articles on pension deferral in publications or websites targeting near-retirees

- reviewing Government information such as ESDC's website, the OAS/GIS automatic enrolment letter and application form, and community outreach material

The department will continue its ongoing activities aimed at increasing awareness about OAS deferral and explore options to monitor the reach of its activities.

Management action plan

2.1 Public release of the ESDC deferral survey – Income Security and Social Development branch (ISSD) / Public Affairs and Stakeholder Relations Branch (PASRB).

Completion date: March 2020.

2.2 Raise awareness on ESDC's social media channels – ISSD / PASRB.

Completion date: June 2020.

2.3 Disseminate articles on deferral – ISSD / PASRB.

Completion date: June 2020.

2.4 Review Government information – ISSD / Transformation and Integrated Service Management Branch / Citizen Service Branch / PASRB.

Completion date: December 2020.

Annex 1: Old Age Security program description

Old Age Security pension

Description

In January 2019, the OAS pension provided benefits to 6.3 million seniors with the full basic pension amounting to $601.45 per month (or about $7,200 per year). All benefits under the OAS program are indexed quarterly.

The OAS recovery tax, which is part of the Income Tax Act, requires all higher-income pensioners to repay part, or all, of their OAS pension if their individual income exceeds a threshold. For the 2018 tax year, seniors must repay $0.15 for every dollar of income exceeding $75,910. Benefits are completely repaid when income reaches $123,386 (for those not receiving a deferred OAS pension).

Eligibility requirements

To qualify, a person living in Canada at the time of application must be 65 years or older and have resided in Canada for at least 10 years after age 18.

The full basic OAS pension is payable to seniors who have resided in Canada for at least 40 years after age 18.

A partial pension is paid to seniors who have lived in Canada for at least 10 years after age 18, and their benefits are prorated at the rate of one fortieth of the full pension for each complete year of residence.

Guaranteed Income Supplement

Description

In January 2019,GIS benefits were paid to 2 million low-income seniors and could reach $898.32 per month for single seniors and $540.77 per month for seniors who were married or in a common-law relationship (or up to about $10,800 or $6,500 per year respectively).

Eligibility requirements

In order to be eligible for the GIS, a person must receive the OAS pension, be a legal resident of Canada and have income, or combined income for couples, below the maximum annual thresholds.

Single seniors qualified for the GIS with incomes up to $18,240 per year and up to $24,096 for senior couples in January 2019.

The Allowances: Allowance (spousal) and the Allowance for the Survivor

Description

In January 2019, the Allowance was paid to 51,000 people and the Allowance for the Survivor to 22,000 people. Benefits can reach $1,142.22 per month for the Allowance and $1,361.56 per month for the Allowance for the Survivor (or about $13,700 and $16,300 per year respectively, based on January 2019 rates).

Eligibility requirements

In order to qualify for the Allowances, a person must be 60 to 64 years old, be a legal resident of Canada and have resided in Canada for at least 10 years after the age of 18.

In addition, a person must be a low-income widow or widower to qualify for the Allowance for the Survivor, or the spouse or common-law partner of a recipient of the GIS to qualify for the Allowance.

Annex 2: Key findings of phase 1 of the evaluation

Many factors contributed to the increase in the employment rate of seniors and near-seniors, including among OAS beneficiaries, notably growth in the service sector, technological advances and improved health levels. The increase in the GIS earnings exemption in 2008 increased employment rates among recipients of the Allowances by 1 percentage point and increased average employment income among working GIS and Allowances recipients.

The GIS top-up reached many groups of vulnerable seniors, as did other OAS benefits. For the average top-up recipient, the top-up represented 4% of OAS benefits and was equivalent to 10% of their other sources of income.

With population aging and increases in the number of OAS beneficiaries, total administrative costs of the OAS program have increased from $118 million in fiscal year 2007 to 2008 to $177 million in fiscal year 2016 to 2017. Administrative costs represented about 0.4% of program costs throughout this period.

Some of the most relevant indicators of service delivery quality are monitored closely by the department; notably, access to Service Canada agents, timeliness of benefit receipt, take‑up and payment accuracy.

However, the client satisfaction survey conducted on behalf of Service Canada was discontinued in 2010, leading to an important knowledge gap since then.

Recommendation

Consider regularly monitoring client satisfaction with OAS service delivery, including monitoring client satisfaction of the various service delivery channels.

Annex 3: Evaluation questions

Evaluation questions

Do the Allowances continue to address a demonstrable need? Who are the beneficiaries of the Allowances and how has their profile changed over time?

Source documents

- Canada Revenue Agency T1 data analysis: "Recipients of the Allowances Program: a Historical Perspective"

- National Household Survey data analysis: "Participation in the Old Age Security Program – National Household Survey"

Evaluation question

To what extent is ESDC prepared to monitor and assess the characteristics and patterns of seniors deferring their OAS pension?

Source document

OAS and T1 administrative data analysis: "Who Defers the Start of their OAS pension?"

Annex 4: Limitations and summary of studies to support phase 2 of the evaluation

Technical study: ESDC (2019a), "Recipients of the Allowances Program: a Historical Perspective"

Description:

This report uses T1 data from the Canada Revenue Agency. Its purpose was to examine the characteristics of the recipients of the Allowances, how their profile has changed over time, the rationale behind the introduction of the Allowances in the 1970s, and whether the Allowances continue to address a demonstrable need today. Additionally, this report illustrates the characteristics of other low-income near-seniors who are not eligible for the Allowances.

Limitations:

Reliable data on the characteristics of recipients of the Allowances was only available back to 1998. Ideally, comparison to Allowance recipients back to 1975 would have been useful to examine changes to beneficiaries since the introduction of the program.

Technical study: ESDC (2019b), "Who Defers the Start of their OAS pension?"

Description:

This paper uses linked administrative data from the Canada Revenue Agency (T1) and the OAS program. The report examines to what extent the department can monitor the characteristics of seniors deferring their OAS pension. It also provides a profile of individuals who defer the start of their OAS pension and illustrates the extent to which seniors are deferring their OAS pension.

Limitations:

Complete data on OAS deferral of each cohort of 65year-olds is only available with a 5-year delay. Therefore, most of the analysis had to be based on the cohort who reached 65 years old in 2013.

It was not possible to find a methodology to measure the impact of OAS deferral on the employment rates of seniors. No appropriate control group could be found. The report shows, however, that employment rates are high while seniors are deferring their OAS pension.

Technical study: ESDC (2016b), "Participation in the Old Age Security Program – National Household Survey"

Description:

This report uses data from the National Household Survey. The report examines participation in the OAS program, take-up rates among different sub-groups of the population, and presents a financial profile of beneficiaries of the Allowances. These findings help to show how the Allowances continue to address a demonstrable need.

Limitations:

The report uses older data from 2011.

Annex 5: References

ESDC (2019a), "Recipients of the Allowances Program: a Historical Perspective".

ESDC (2019b), "Who Defers the Start of their OAS pension?".

ESDC (2018a), "Evaluation of the Old Age Security Program: Phase 1", (accessed on August 5, 2019). Retrieved from https://www.canada.ca/en/employment-social development/corporate/reports/ evaluations/oas-program-phase-01.html.

ESDC (2018b), "The CPP & OAS Stats Book 2018".

ESDC (2017a), "The CPP & OAS Stats Book 2017".

ESDC (2017b), "Seniors' Labour Force Participation, Income and the GIS Top-up".

ESDC (2016a), "Document Review of Service Delivery of Old Age Security Program".

ESDC (2016b), "Participation in the Old Age Security Program – National Household Survey".

ESDC (2014), "ESDC Departmental Performance Report 2013-14".

ESDC (2013), "The CPP & OAS Stats Book 2013".

ESDC (2012), "Summative Evaluation of the Old Age Security Program", (accessed on August 5, 2019). Retrieved from http://publications.gc.ca/pub?id=9.696235&sl=1.

Gilbert, Sabrina, Zechuan B. Deng, Sebastian Yeung and Gail Fawcett (2015), "Income and Employment of Adults with Disabilities: Findings from the 2012 Canadian Survey on Disability", ESDC.

Health and Welfare Canada (1992), "Evaluation Report: Old Age Security Program", September.

House of Commons (1985), "House of Common Debates", February 4, 1985, pages 1941 to 1943.

House of Commons (1983), "Report of the Parliamentary Task Force on Pension Reform", page 180.

House of Commons (1975), "House of Common Debates", June 6, 1975, pages 6518 to 6521.

Office of the Chief Actuary (2017), "Actuarial Report (14th) on the Old Age Security Program", Office of the Superintendent of Financial Institutions Canada, (accessed on August 5, 2019). Retrieved from http://www.osfi-bsif.gc.ca/Eng/Docs/oas14.pdf.

Office of the Chief Actuary (2011), "Actuarial Report (9th) on the Old Age Security Program", Office of the Superintendent of Financial Institutions Canada, (accessed on August 5, 2019). Retrieved from http://www.osfi-bsif.gc.ca/eng/docs/oas9.pdf.

Old Age Security Policy and Legislation Division (2016), "Expert Report on the Allowances under the Old Age Security Act", Report prepared for the Social Security Tribunal hearing, ESDC, July.

Royal Commission on the Status of Women in Canada (1970), "Report of the Royal Commission on the Status of Women in Canada".

Schirle, Tammy (2008), "Why Have Labor Force Participation Rates of Older Men Increased since the Mid-1990s?", Journal of Labor Economics, vol. 26 (4), pages 549 to 594.

Service Canada (2015), "Information Sheet: Statement of Income for the GIS, the Allowance and the Allowance for the Survivor", SC ISP-3026A (2015-01-27) E.

Statistics Canada (2017), "2015 Canadian Income Survey".

Standing Senate Committee on Banking, Trade and Commerce (2006), "The Demographic Time Bomb: Mitigating the Effects of Demographic Change in Canada", Senate of Canada, June.

Tamagno, E. (2007), "Strengthening the Foundations of Canada's Pension System: a Review of the Old Age Security Program", Caledon Institute of Social Policy.