CompassRx, 8th Edition

Annual Public Drug Plan Expenditure Report, 2020/21

ISSN 2369-0518

Cat. No. H79-6E-PDF

January 2023

PDF - 908 KB

Table of Contents

- Executive Summary

- Key Findings

- Introduction

- Methods

- Limitations

- Analyses

- 1. Trends in Prescription Drug Expenditures, 2015/16 to 2020/21

- 2. The Drivers of Drug Costs, 2019/20 to 2020/21

- 3. The Drivers of Dispensing Costs, 2019/20 to 2020/21

- References

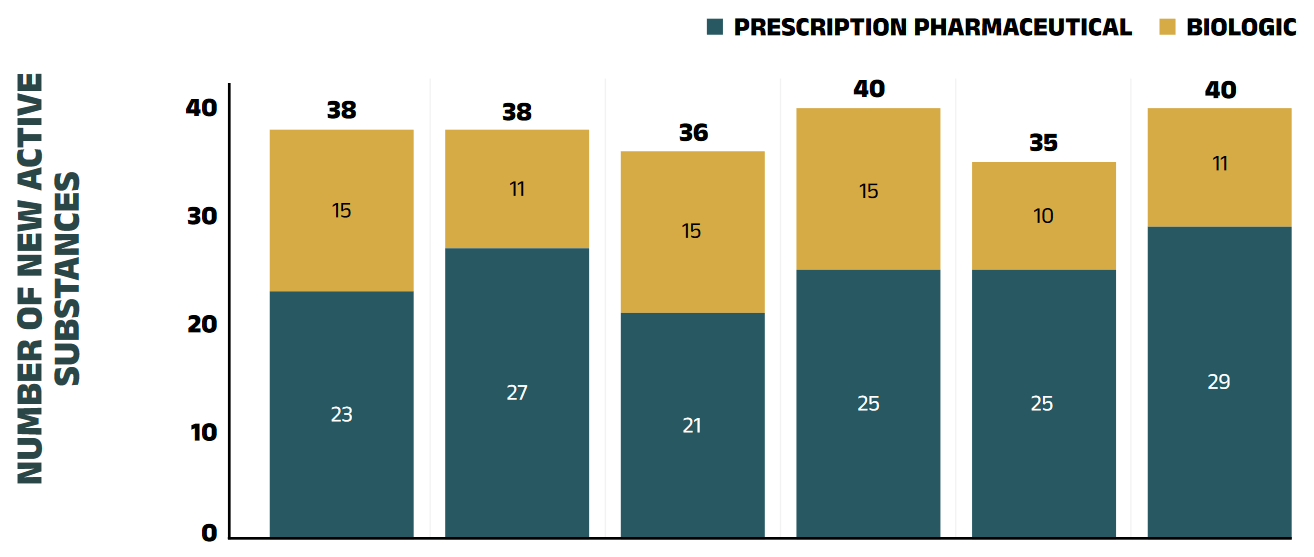

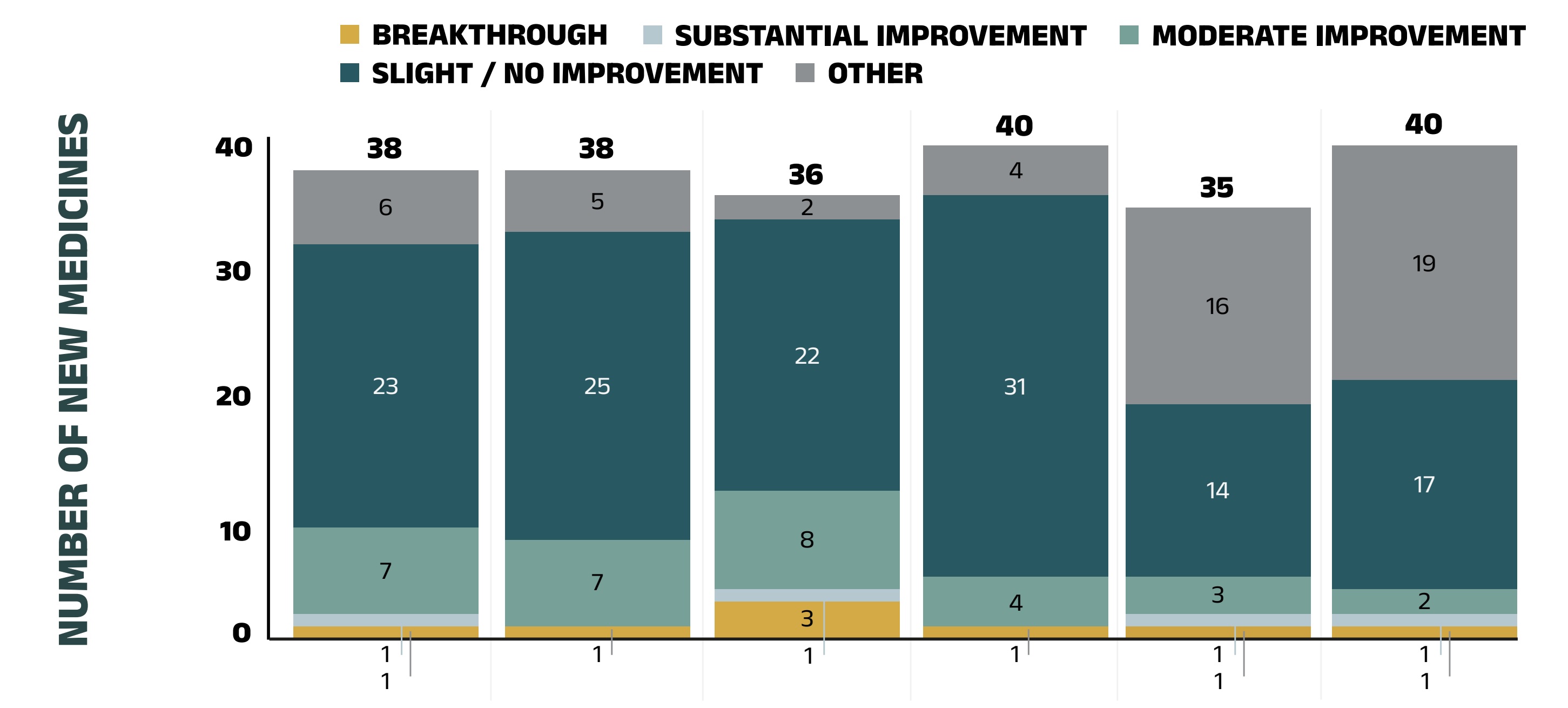

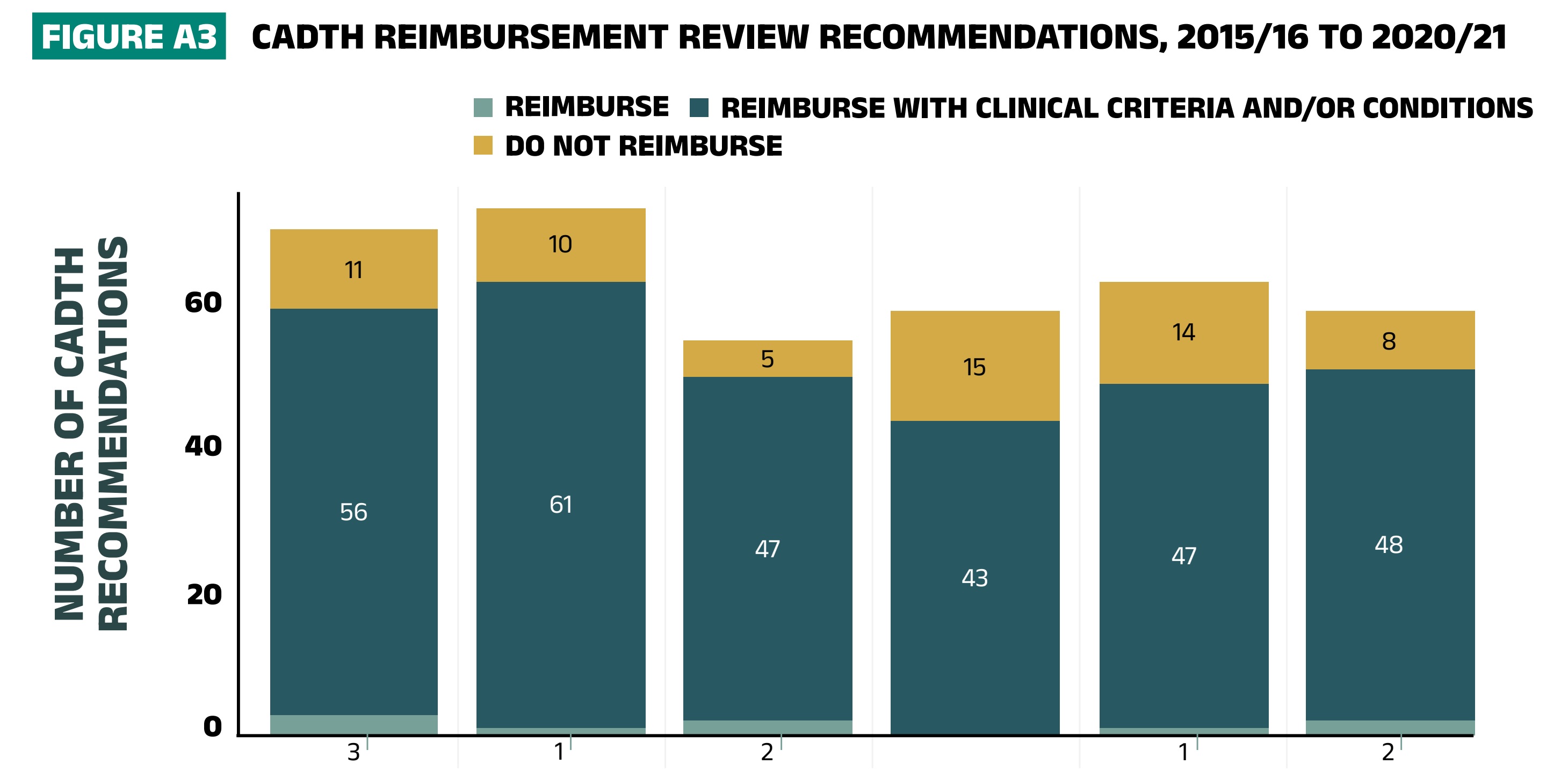

- Appendix A: Drug Reviews and Approvals

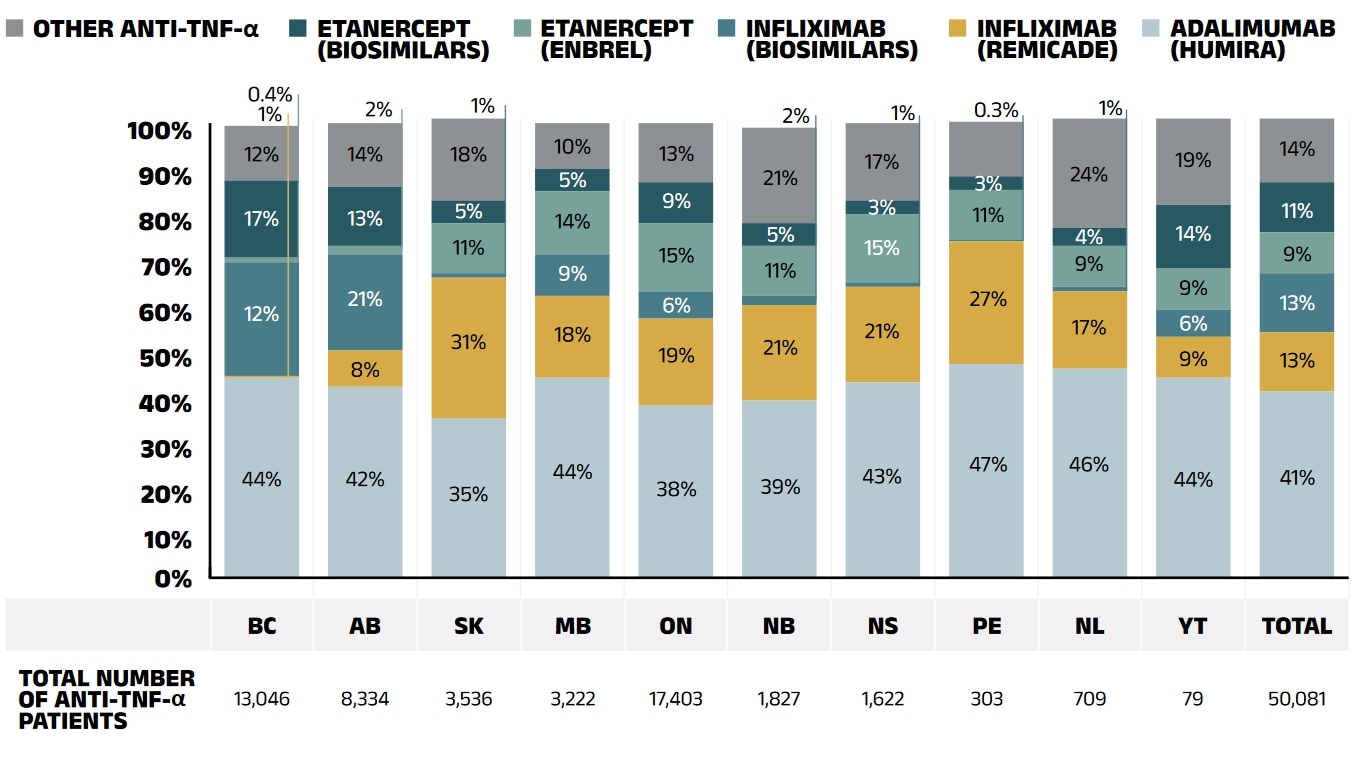

- Appendix B: Distribution of Patients on Biosimilar Initiative Medicines by Jurisdiction, 2020/21

- Appendix C: Biosimilar Switching Initiatives by Canadian Public Payers

- Appendix D: Top 50 Patented Medicines by Drug Cost, NPDUIS Public Drug Plans, 2020/21 ($million)

- Appendix E: Top 50 Multi-Source Generic Drugs by Drug Cost, NPDUIS Public Drug Plans, 2020/21 ($million)

- Appendix F: Top 50 Single-Source Non-Patented Medicines by Drug Cost, NPDUIS Public Drug Plans, 2020/21 ($thousand)

- Appendix G: Top 50 Manufacturers by Drug Cost, NPDUIS Public Drug Plans, 2020/21 ($million)

About CompassRx

CompassRx is an annual Patented Medicine Prices Review Board (PMPRB) publication that explores trends in prescription drug expenditures in Canadian public drug plans. It focuses on the pressures that contribute to the annual change in drug and dispensing costs, including the switch in use between lower- and higher-priced drugs and changes in the beneficiary population, drug prices, and the volume of drugs used, as well as other key factors.

About the PMPRB

The Patented Medicine Prices Review Board (PMPRB) is an independent quasi-judicial body established by Parliament in 1987. The PMPRB has a dual regulatory and reporting mandate: to ensure that prices at which patentees sell their patented medicines in Canada are not excessive; and to report on pharmaceutical trends of all medicines and on research and development spending by patentees.

The NPDUIS Initiative

The National Prescription Drug Utilization Information System (NPDUIS) is a research initiative established by federal, provincial, and territorial Ministers of Health in September 2001. It is a partnership between the PMPRB and the Canadian Institute for Health Information (CIHI).

Pursuant to section 90 of the Patent Act, the PMPRB has the mandate to conduct analysis that provides decision makers with critical information and intelligence on price, utilization, and cost trends so that Canada’s healthcare system has more comprehensive and accurate information on how medicines are being used and on sources of cost pressures.

The specific research priorities and methodologies for NPDUIS are established with the guidance of the NPDUIS Advisory Committee and reflect the priorities of the participating jurisdictions, as identified in the NPDUIS Research Agenda. The Advisory Committee is composed of representatives from public drug plans in British Columbia, Alberta, Saskatchewan, Manitoba, Ontario, New Brunswick, Nova Scotia, Prince Edward Island, Newfoundland and Labrador, Yukon, the Non-Insured Health Benefits (NIHB) Program, and Health Canada. It also includes observers from CIHI, the Canadian Agency for Drugs and Technologies in Health (CADTH), the Ministère de la Santé et des Services sociaux du Québec (MSSS), and the pan-Canadian Pharmaceutical Alliance (pCPA) Office.

Acknowledgements

This report was prepared by the Patented Medicine Prices Review Board (PMPRB) as part of the National Prescription Drug Utilization Information System (NPDUIS) initiative.

The PMPRB wishes to acknowledge the members of the NPDUIS Advisory Committee for their expert oversight and guidance in the preparation of this report. Please note that the statements and findings for this report do not necessarily reflect those of the members or their organizations.

Appreciation goes to Yvonne Zhang for leading this project, and to Tanya Potashnik, Kevin Pothier and Jared Berger for their oversight in the development of the report. The PMPRB also wishes to acknowledge the contribution of the analytical staff Lokanadha Cheruvu and Jun Yu, and editorial staff Shirin Paynter and Ronja Francoeur.

Disclaimer

NPDUIS operates independently of the regulatory activities of the Board of the PMPRB. The research priorities, data, statements, and opinions expressed or reflected in NPDUIS reports do not represent the position of the PMPRB with respect to any regulatory matter. NPDUIS reports do not contain information that is confidential or privileged under sections 87 and 88 of the Patent Act, and the mention of a medicine in an NPDUIS report is not and should not be understood as an admission or denial that the medicine is subject to filings under sections 80, 81, or 82 of the Patent Act or that its price is or is not excessive under section 85 of the Patent Act.

Although based in part on data provided by the Canadian Institute for Health Information (CIHI), the statements, findings, conclusions, views, and opinions expressed in this report are exclusively those of the PMPRB and are not attributable to CIHI.

Contact Information

Patented Medicine Prices Review Board

Standard Life Centre

Box L40

333 Laurier Avenue West Suite 1400

Ottawa, ON K1P 1C1

Tel.: 1-877-861-2350

TTY 613-288-9654

Email: PMPRB.Information-Renseignements.CEPMB@pmprb-cepmb.gc.ca

Web: https://www.canada.ca/en/patented-medicine-prices-review.html

Suggested Citation

Patented Medicine Prices Review Board. (2023). CompassRx, 8th edition: Annual Public Drug Plan Expenditure Report, 2020/21. Ottawa: PMPRB.

Executive Summary

Prescription drug expenditures for the NPDUIS public drug plans increased sizably by 4.2% in 2020/21, a faster pace than the 1.3% annual change to the Consumer Price Index (CPI) in Health and Personal CareReference I, with varying rates of change in its two main components: drug costs (which saw an increase of 5.3%) and dispensing costs (which saw a decrease of 0.2%). The overall growth in prescription drug expenditures continued to be primarily driven by notable increases in the use of higher-cost drugs.

The PMPRB’s CompassRx report monitors and analyzes the cost pressures driving changes in prescription drug expenditures in Canadian public drug plans. This eighth edition of CompassRx provides insight into the factors driving growth in drug and dispensing costs in 2020/21, as well as a retrospective review of recent trends in public drug plan costs and utilization.

The main data source for this report is the National Prescription Drug Utilization Information System (NPDUIS) Database at the Canadian Institute for Health Information (CIHI), which includes data for the following jurisdictions: British Columbia, Alberta, Saskatchewan, Manitoba, Ontario, New Brunswick, Nova Scotia, Prince Edward Island, Newfoundland and Labrador, Yukon, and the Non-Insured Health Benefits Program.

The findings from this report will inform policy discussions and aid decision makers in anticipating and responding to evolving cost pressures.

Key Findings

The key findings cover the three areas of analysis in CompassRx (see Analyses): the trends in prescription drug expenditures; the drivers of drug costs; and the drivers of dispensing costs.

Prescription drug expenditures

Prescription drug expenditures for the NPDUIS public drug plans grew by 4.2% in 2020/21, following a 3.7% increase in 2019/20.

- Between 2015/16 and 2020/21, the total prescription drug expenditures for Canada’s public drug plans rose by $2.5 billion, for a compound annual growth rate of 5.6%.

- Drug costs, which represent 82% of prescription drug expenditures, grew by 5.3% from 2019/20 to 2020/21, while dispensing costs, which account for the remaining 18% of expenditures, had no growth (-0.2%).

- The NPDUIS public drug plans paid an average of 87% of the total $12.3 billion in prescription costs for 289 million prescriptions dispensed to almost 6 million active beneficiaries in 2020/21.

- The overall NPDUIS public plan beneficiary population declined by 5.8% from 2019/20 to 2020/21. Approximately 366 thousand fewer Canadians filled a prescription for reimbursement to public drug plans, with the onset of the COVID-19 pandemic.

Drug costs

Drug cost growth for the NPDUIS public plans in 2020/21 was primarily driven by a greater use of higher-cost drugs combined with a sizable increase in the volume of drugs used per patient.

- Increase in drug costs was moderated, in part, by the decreasing use of direct acting antivirals (DAAs) for hepatitis C; savings from generic and biosimilar substitution; and a decrease in the number of active beneficiaries.

- The increased use of higher-cost drugs continued to be the most pronounced driver in 2020/21, pushing costs upward by 6.3%, while declining use of DAAs for hepatitis C had a pull effect of 2.1%.

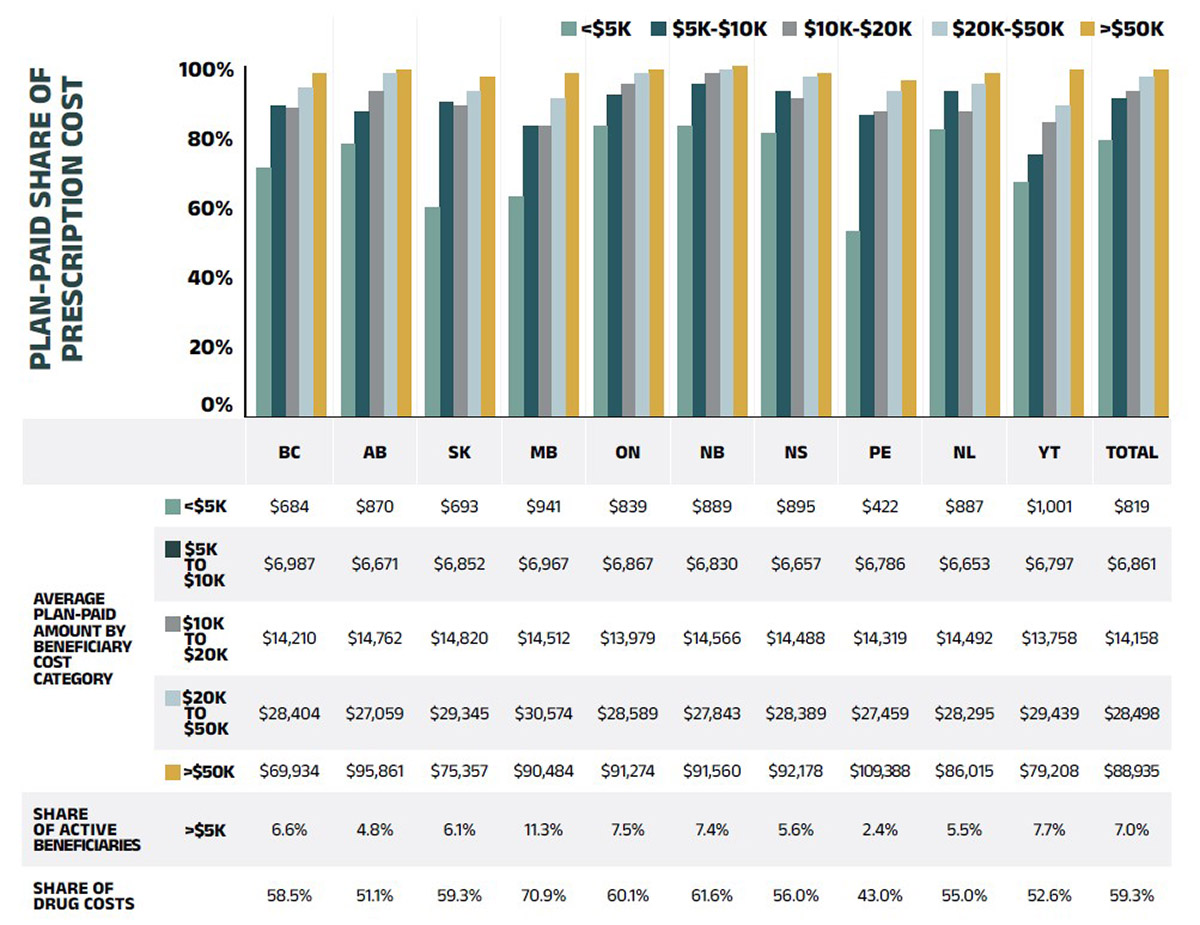

- Nealy 60% of the total drug costs in 2020/21 were attributable to just 7% of public drug plan beneficiaries. High-cost drugs, which were used by 2.5% of beneficiaries, accounted for more than one third of costs.

- Due to COVID-19, a notable decrease in the number of active beneficiaries exerted a 2.3% downward demographic effect, though this was more than offset by a 4.6% upward volume effect.

- In 2020/21, the price change effect was negligible at less than 0.1%, while the substitution effect gained strength, pulling drug costs down by 1.4%.

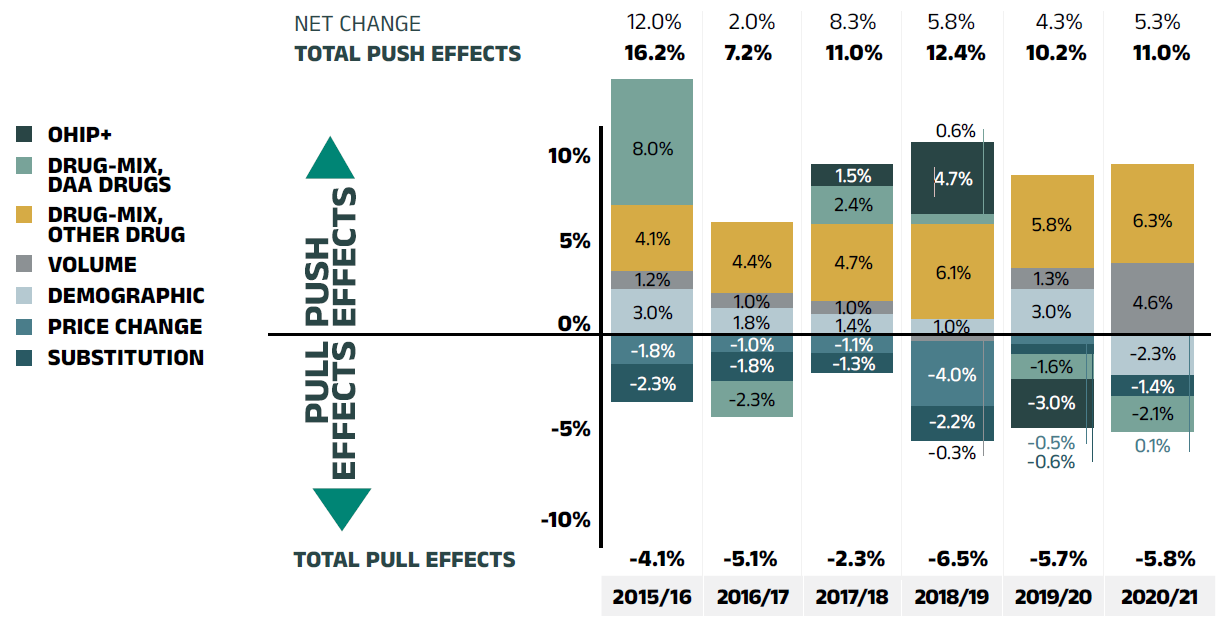

Figure description

This column graph describes the key factors or effects that impacted the rates of change in drug costs across all NPDUIS public drug plans for each year from 2015/16 to 2020/21. Each column is broken out to give the positive or negative contribution of each effect: drug-mix; volume; demographic; price change; and substitution. The drug-mix effect for direct-acting antiviral (DAA) drugs for the treatment of hepatitis C is shown separately, as is the effect of the Ontario Health Insurance Plan Plus (OHIP+ ) initiative. The OHIP+ effect is not captured for 2020/21. Separate rows above and below the bar graph show the total positive push effect, negative pull effect, and net change for each year.

| 2015/16 | 2016/17 | 2017/18 | 2018/19 | 2019/20 | 2020/21 | |

|---|---|---|---|---|---|---|

|

OHIP+ |

- |

- |

1.5% |

4.7% |

-3.0% |

- |

|

Drug-mix, direct-acting antiviral (DAA) drugs |

8.0% |

-2.3% |

2.4% |

0.6% |

-1.6% |

-2.1% |

|

Drug mix, other drugs |

4.1% |

4.4% |

4.7% |

6.1% |

5.8% |

6.3% |

|

Volume |

1.2% |

1.0% |

1.0% |

-0.3% |

1.3% |

4.6% |

|

Demographic |

3.0% |

1.8% |

1.4% |

1.0% |

3.0% |

-2.3% |

|

Price change |

-1.8% |

-1.0% |

-1.1% |

-4.0% |

-0.5% |

<0.1% |

|

Substitution |

-2.3% |

-1.8% |

-1.3% |

-2.2% |

-0.6% |

-1.4% |

|

Total push effect |

16.2% |

7.2% |

11.0% |

12.4% |

10.2% |

11.0% |

|

Total pull effect |

-4.1% |

-5.1% |

-2.3% |

-6.5% |

-5.7% |

-5.8% |

|

Net change |

12.0% |

2.0% |

8.3% |

5.8% |

4.3% |

5.3% |

A table to the right of the graph provides additional information for each effect in 2020/21.

Drug-mix, other drugs |

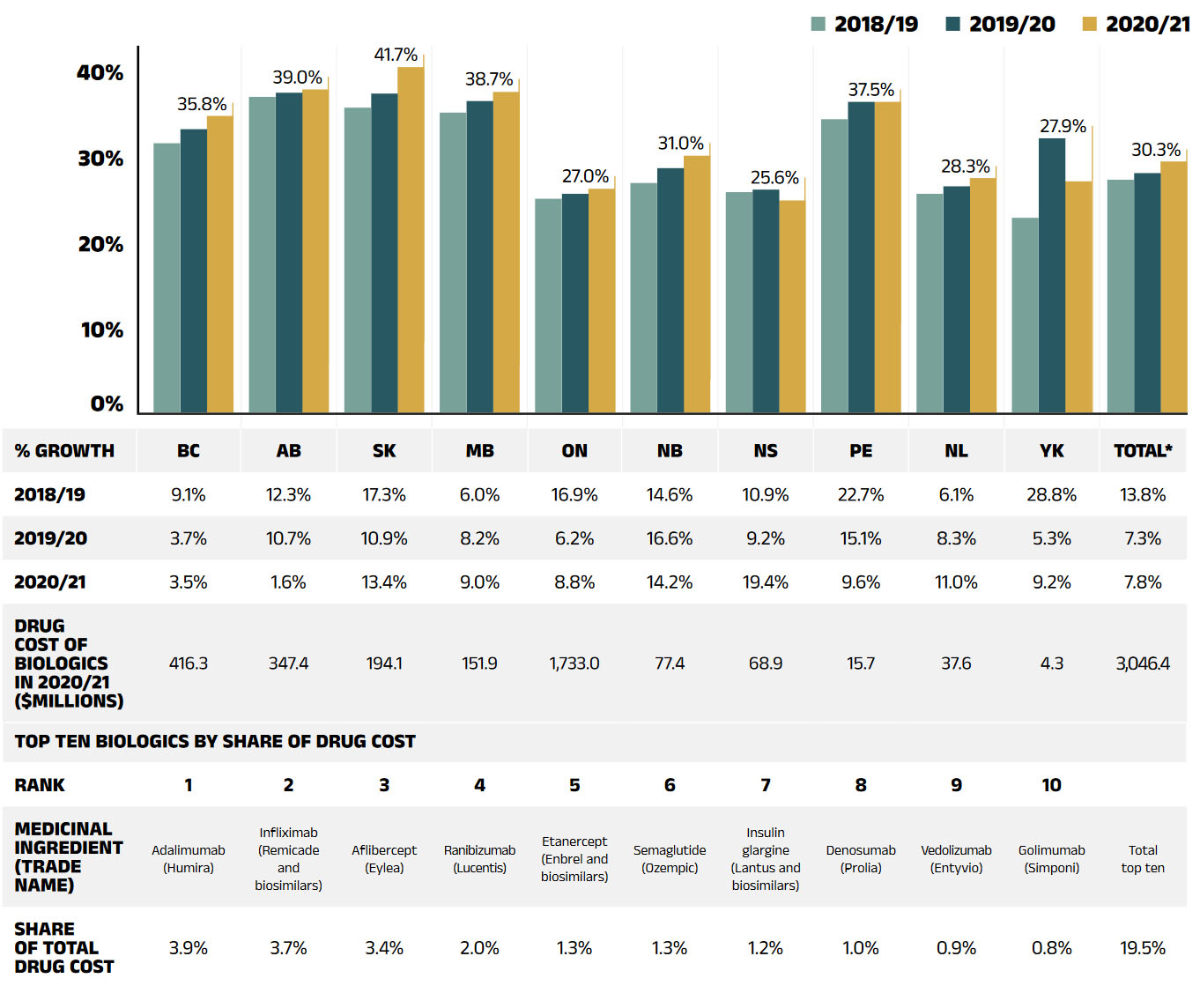

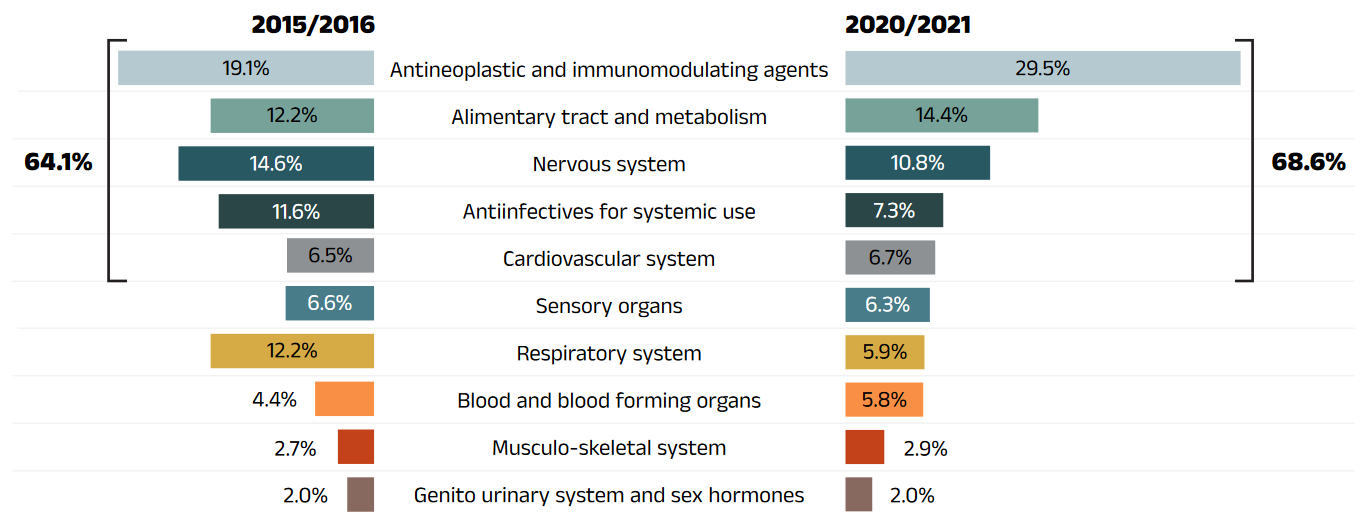

The increased use of higher-cost drugs other than DAA drugs had the greatest push effect, with an overall impact of 6.3%. The number of high-cost medicines increased from 95 in 2015/16 to 135 in 2020/21. Biologic drugs captured an increasing share of total drug costs for the NPDUIS public plans, exceeding 30%. Antineoplastic and immunomodulating agents accounted for 29.5% of drug costs, the largest share held by a single therapeutic class. The 10 highest-cost drugs for 2020/21 all had average treatment costs exceeding $200,000. |

Volume |

The increased use of drugs contributed 4.3% to the growth in drug costs despite fewer active beneficiaries. |

Demographic |

In relation to the COVID-19 pandemic, a decrease in the number active beneficiaries exerted 2.0% downward demographic effect. |

Price change |

The influence of the price change effect has diminished to less than 0.1% in 2020/21. |

Substitution |

Shifts from brand-name to generic drugs or biosimilars pulled overall drug costs down by 1.4%. Biosimilars contributed more to the substitution effect than generic medicines. |

Drug-mix, |

The use of direct-acting antiviral (DAA) drugs for hepatitis C continued to decline in 2020/21, lowering total drug costs by 2.1%. |

Note: This analysis is based on publicly available pricing information. It does not reflect confidential drug price discounts negotiated by the pan-Canadian Pharmaceutical Alliance on behalf of the public plans.

Values for 2016/17 onward reflect a revised methodology; previous results have not been updated, as there would have been no notable change in the relative contribution of each effect. Data for Yukon is also included from 2016/17 onward. Data from the NIHB Program is not included in 2020/21.

Values may not add to totals due to rounding and the cross effect.

Data source: National Prescription Drug Utilization Information System Database, Canadian Institute for Health Information.

Dispensing costs

Dispensing costs in the NPDUIS public plans were virtually unchanged in 2020/21 relative to the previous year, owing primarily to temporary changes to dispensing frequency in many provinces during the COVID-19 pandemic and policy changes in Ontario.

- The overall change in dispensing costs was -0.2% (or -$4.9 million) in 2020/21, the first negative growth of dispensing costs in the past 6 years, though results varied among individual plans.

- The zero-dollar dispensing fee model introduced to the long-term care (LTC) program in Ontario had a significant impact on the decrease in dispensing costs, pulling costs down by 4.1% ($94 million) nationally, and by 7.0% in Ontario.

- A decrease in the number of active beneficiaries reduced costs by 1.3% in 2020/21 due to the onset of the COVID-19 pandemic, though this was more than offset by a 3.1% increase in the quantity of drugs dispensed to patients.

- Changes in prescription size following the temporary changes to policies on dispensing frequency during the COVID-19 pandemic pushed costs upward by a sizable 3.4% in 2020/21.

Introduction

Canadian public drug plan expenditures represent a significant portion of the overall healthcare budget. The Canadian Institute for Health Information (CIHI) reported that the total cost of prescription drugs in Canada was $34.3 billion in 2019, with the largest component financed by the public drug plans (43.6%) and the remainder paid by private plans (36.9%) or out of pocket by households and individuals (19.9%).Reference 1

This edition of the report focuses on the 2020/21 fiscal year, with a retrospective look at recent trends. The results of this study will aid stakeholders in anticipating and responding to the evolving cost pressures that affect Canada’s public drug plans. The analysis focuses on the public drug plans.

The analysis focuses on the public drug plans participating in the National Prescription Drug Utilization Information System (NPDUIS) initiative, which includes all provincial public plans (with the exception of Quebec), Yukon, and the Non-Insured Health Benefits (NIHB) Program. These plans account for approximately one third of the total annual spending on prescription drugs in Canada.

Each public drug plan reimburses eligible beneficiaries according to its own specific plan design and implements policies related to the reimbursement of drug prices and dispensing fees. Summaries of the plan designs and policies are available on the PMPRB website.

Health Canada, the PMPRB, and the Canadian Agency for Drugs and Technologies in Health (CADTH) are responsible for drug approvals, price reviews, and health technology assessments, respectively. Details of the 2020/21 approvals and reviews are provided in Appendix A of this report.

Methods

The main data source for this report is the National Prescription Drug Utilization Information System (NPDUIS) Database, developed by the Canadian Institute for Health Information (CIHI). This database houses pan-Canadian information on public drug programs, including claimslevel data collected from the plans that participate in the NPDUIS initiative. Data is reported on a fiscal year basis.

Results are presented for the following public drug plans: British Columbia, Alberta, Saskatchewan, Manitoba, Ontario, New Brunswick, Nova Scotia, Prince Edward Island, Newfoundland and Labrador, Yukon, and the Non- Insured Health Benefits (NIHB) Program.

The analysis focuses exclusively on data for beneficiaries that met their deductible and received public reimbursement. Results reported for Saskatchewan and Manitoba include the accepted prescription drug expenditures for individuals who are eligible for coverage but have not submitted an application and, therefore, do not have a defined deductible.

Long-term care (LTC) sub-plans may not have a typical dispensing frequency due to the more specialized needs of their patients. The LTC sub-plan prescriptions were only separated out from the dispensing costs analysis in Ontario due to a notable influence from their size.

For this edition, the data from the NIHB Program was not available. Therefore, it is not included in the results for 2020/21. It is worth noting that the impact of NIHB data on the overall growth trends among NPDUIS public drug plans would be insignificant (approximately 0.1%).

The analysis of drug and dispensing cost drivers follows the methodological approach detailed in the PMPRB’s The Drivers of Prescription Drug Expenditures: A Methodological Report.Reference 2 Drug costs include any associated markups. Analyses of the average prescription size, as well as pricing, are limited to oral solids to avoid data reporting inconsistencies that may exist in the days’ supply and unit reporting of other formulations. Anatomical Therapeutic Chemical (ATC) levels reported here are based on CIHI NPDUIS data and reflect the ATC classification system maintained by the World Health Organization Collaborating Centre for Drug Statistics Methodology. Vaccines and pharmacy services are not represented in this report.

The methodological approach used in CompassRx is reviewed on an annual basis and updated as needed to respond to changes in the pharmaceutical landscape and data access. Thus, the scope of the report and the data analyzed may vary slightly from year to year. New changes to the methodology are detailed in Methods and Limitations sections of each edition.

A glossary of terms for NPDUIS studies is available on the PMPRB website.

Limitations

Drug expenditure and utilization levels vary widely among the jurisdictions and cross comparisons of the results are limited by differences in the plan designs and policies of the individual public drug plans, as well as the demographic and disease profiles of the beneficiary populations.

For example, public drug plans in British Columbia, Saskatchewan, and Manitoba provide universal incomebased coverage, while other provincial public drug plans offer specific programs for seniors, income assistance recipients, and other select patient groups. The NIHB provides universal care to its entire population. As Yukon is a small jurisdiction, any plan design changes will result in more significant fluctuations in their rates of growth.

The NPDUIS Database includes available sub-plan data specific to particular jurisdictions, such as Alberta, Nova Scotia, and Prince Edward Island. This further limits the comparability of results across plans. A comprehensive summary of the sub-plans available in the database, along with their eligibility criteria, is available on the PMPRB website.

Drug claims for beneficiaries in Ontario who also have coverage through the NIHB are primarily reimbursed by the Ontario Drug Benefit program, with any remaining drug costs covered by the NIHB. Therefore, claims reported for the NIHB include those coordinated with the Ontario Drug Benefit program.

Totals for the NPDUIS public drug plans are heavily skewed toward Ontario due to its population size. As such, the introduction and subsequent revision of the OHIP+ program for Ontario residents aged 24 years or younger had a notable influence on the overall trends for 2018/19 and 2019/20, but little impact after 2019/20 as Ontario OHIP+ program spending became stable. CompassRx will not report the effect separately after this edition. For historical data, please consult previous editions.

High-cost medicines are defined as having an annual treatment cost greater than $10,000. If medicines reach this threshold in any given year, they are included in the count for all other years. Thus, the number and composition of high-cost medicines in any given year may vary depending on the time of analysis.

The number of oncology medicines and other high-cost medicines covered by public plans may be underestimated, as some are reimbursed through specialized programs, such as cancer care, that are not captured in the data.

The reported drug costs are the amounts accepted toward reimbursement by the public plans, which may not reflect the amounts paid by the plan/program and do not reflect off-invoice price rebates or price reductions resulting from confidential product listing agreements.

The prescription drug expenditure data for the public drug plans reported in this study represents only one segment of the Canadian pharmaceutical market, and hence, the findings should not be extrapolated to the overall marketplace.

This edition of the CompassRx reports on data up to and including the 2020/21 fiscal year. Any plan changes or other developments that have taken place since then will be captured in future editions.

Analyses

The components that make up prescription drug expenditures can be expressed from two perspectives: cost-sharing and pharmaceutical.

From a cost-sharing perspective, the expenditures reported in this study represent the total amount accepted for reimbursement by the NPDUIS public drug plans. These amounts reflect both the plan-paid and beneficiary-paid portions of the prescription costs, such as co-payments and deductibles.

From a pharmaceutical pricing perspective, the cost of a prescription drug plan in this section is measured by the total of two components: the cost of the prescription drugs (including associated markups) and the cost for dispensing the prescription drugs, represented here by this formula:

Prescription Drug Expenditures = Drug Costs + Dispensing Costs

The following sections detail each component of this formula by analyzing data trends and adding greater context in the form of Brief Insights.

1. Trends in prescription drug expenditures, 2015/16 to 2020/21

Prescription drug expenditures for public plans increased by 4.2% in 2020/21.

High-cost patented medicines (other than DAAs for hepatitis C) continued to be the most significant contributor to the growth in public plan drug costs, offset in part by a continued decline in the use of new hepatitis C drugs as well as cost savings from generic and biosimilar substitution.

Brief Insights: Drug Plan Designs

The expenditure and utilization levels reported in this study depend on the specific plan design and policies of each jurisdiction, as well as the demographic and disease profiles of the beneficiary population. This affects the comparability of results across plans.

Changes in plan designs or policies can have a significant effect on trends in any given year. For instance, early in 2020, the implementation of a new capitation funding model in Ontario’s long-term care (LTC) program, as well as temporary changes to policies associated with dispensing frequency introduced in many provinces to reduce supply-chain demand and prevent stockpiling due to the onset of the COVID-19 pandemic, directly shaped the growth of dispensing costs, and had notable impacts on expenditures for the 2020/21 fiscal year.

Supplementary reference documents providing information on individual public drug plan designs, policies governing markups and dispensing fees, and a glossary of terms are available on the PMPRB website.

Prescription Drug Expenditures

Prescription Drug Expenditures = Drug Costs (82%) + Dispensing Costs (18%)

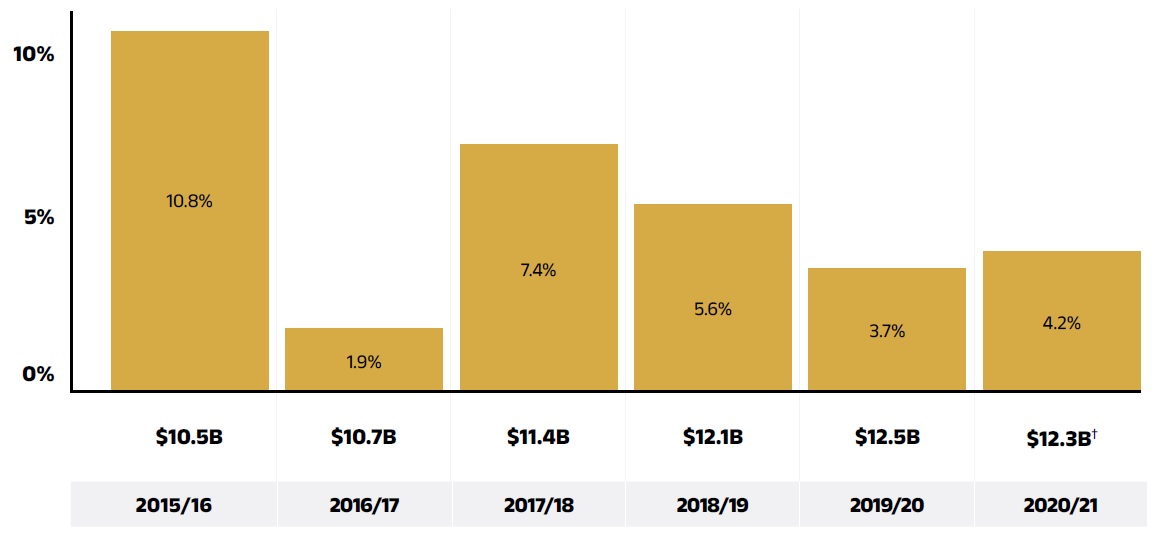

Between 2015/16 and 2020/21, annual prescription drug expenditures for the public drug plans grew at a compound annual growth rate of 5.6%, rising from $10.5 billion to $12.3 billion, with $0.5 billion of this growth seen over the last year (Figure 1.1).

Figure description

This column graph shows the trend in the annual rates of change for prescription drug expenditures from 2015/16 to 2020/21. Price tags below each bar show the annual prescription drug cost in billions of dollars.

| 2015/16 | 2016/17 | 2017/18 | 2018/19 | 2019/20 | 2020/21 | |

|---|---|---|---|---|---|---|

Rate of change |

10.8% |

1.9% |

7.4% |

5.6% |

3.7% |

4.2% |

Prescription drug expenditure (billions of dollars) |

$10.5 |

$10.7 |

$11.4 |

$12.1 |

$12.5 |

$12.3† |

Note: This analysis only includes data for beneficiaries that met their deductible and received public reimbursement.

* British Columbia, Alberta, Saskatchewan, Manitoba, Ontario, New Brunswick, Nova Scotia, Prince Edward Island, Newfoundland and Labrador, Yukon, and the Non-Insured Health Benefits Program.

† The 2020/21 total prescription drug expenditures, the 2019/20 to 2020/21 rate of change and the CAGR were calculated without data from the NIHB program. The impact of NIHB data on the rate of change would be insignificant (approximately 0.1%).

Data source: National Prescription Drug Utilization Information System Database, Canadian Institute for Health Information.

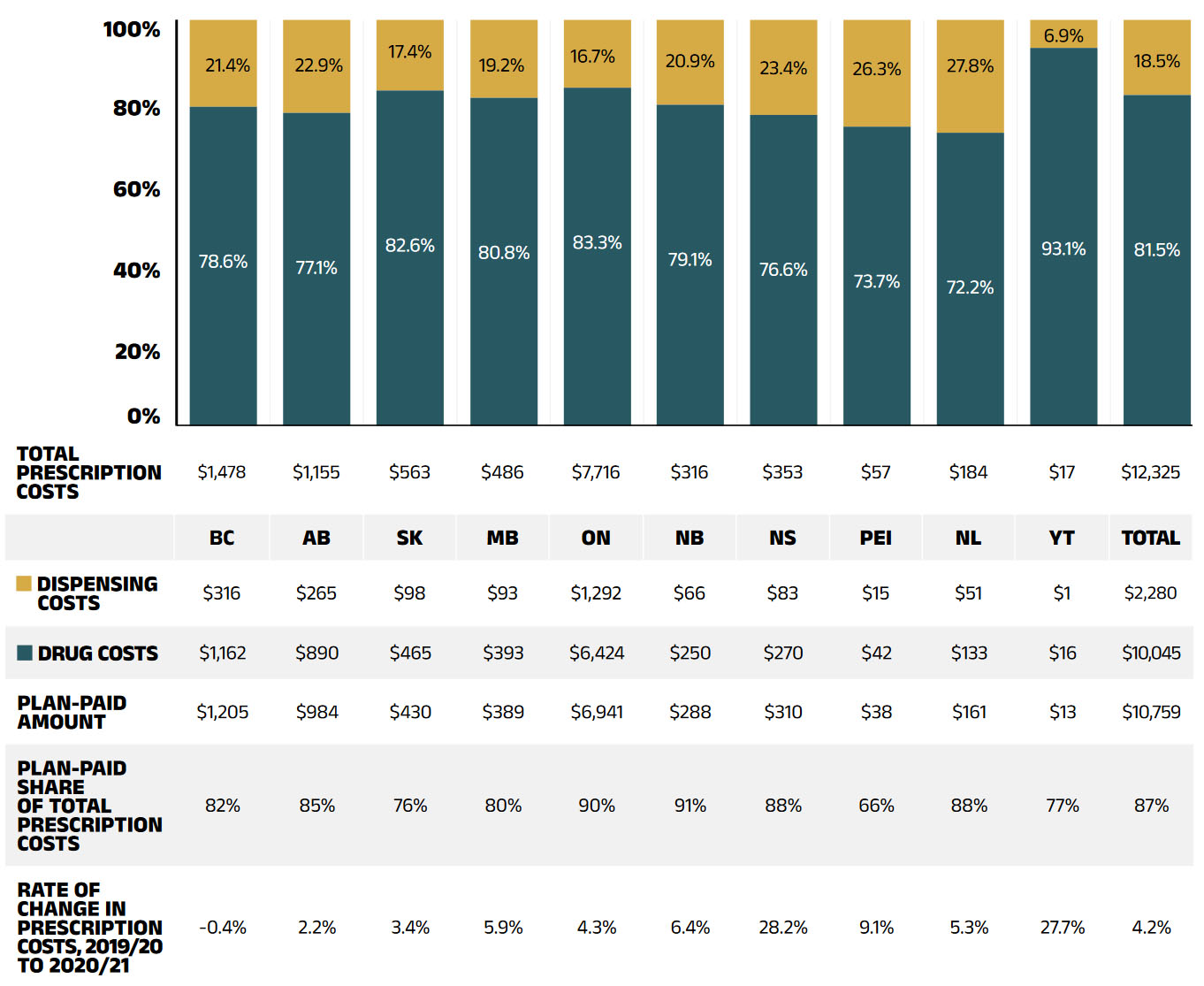

The overall growth in expenditures in 2020/21 consists of a 5.3% growth in drug costs (with associated markups) and a slight (0.2%) decrease in dispensing costs. Due to the disparity in their rates of growth, the drug cost component continued to capture a significantly greater share of overall expenditures (82%), while the dispensing costs share dropped to a new low (18%) (Figure 1.2).

These amounts reflect both the plan-paid portions of prescription costs and beneficiary-paid portions, such as co-payments and deductibles.

Beneficiary Share of Prescription Drug Expenditures

Prescription Drug Expenditures = Plan-paid (87%) + Beneficiary-paid (13%)

In 2020/21, public plans paid an average of 87% (Figure 1.2) of the total expenditures for prescription drugs that were eligible for reimbursement, with the remainder paid by the beneficiaries either out of pocket or through a thirdparty private insurer. The beneficiary-paid share varied across jurisdictions, ranging from 9% to 34%.

Figure description

This stacked column graph shows the total prescription drug expenditure in 2020/21 for each NPDUIS public drug plan broken out by percent shares of drug costs and dispensing costs, along with the total costs across all plans. A table below provides absolute values for the drug and dispensing costs in millions of dollars, as well as the plan-paid shares of the total prescription costs and the rate of change since 2019/20.

| British Columbia | Alberta | Saskatchewan | Manitoba | Ontario | New Brunswick | Nova Scotia | Prince Edward Island | Newfoundland and Labrador | Yukon | Total | |

|---|---|---|---|---|---|---|---|---|---|---|---|

Total prescription cost (millions of dollars |

$1,478 |

$1,155 |

$563 |

$486 |

$7,716 |

$316 |

$353 |

$57 |

$184 |

$17 |

$12,325 |

Dispensing cost share |

21.4% |

22.9% |

17.4% |

19.2% |

16.7% |

20.9% |

23.4% |

26.3% |

217.8% |

6.9% |

18.5% |

Drug cost share |

78.6% |

77.1% |

82.6% |

80.8% |

83.3% |

79.1% |

76.6% |

73.7% |

72.2% |

93.1% |

81.5% |

Dispensing costs (millions of dollars) |

$316 |

$265 |

$98 |

$93 |

$1,292 |

$66 |

$83 |

$15 |

$51 |

$1 |

$2,280 |

Drug costs (millions of dollars) |

$1,162 |

$890 |

$465 |

$393 |

$6,424 |

$250 |

$270 |

$42 |

$133 |

$16 |

$10,045 |

Plan-paid amount (millions of dollars) |

$1,205 |

$984 |

$430 |

$389 |

$6,941 |

$288 |

$310 |

$38 |

$161 |

$13 |

$10,759 |

Plan-paid share of total prescription cost |

82% |

85% |

76% |

80% |

90% |

91% |

88% |

66% |

88% |

77% |

87% |

Rate of change in prescription costs, 2018/19 to 2019/20 |

-0.4% |

2.2% |

3.4% |

5.9% |

4.3% |

6.4% |

28.2% |

9.1% |

5.3% |

27.7% |

4.2% |

Note: This analysis only includes data for beneficiaries that met their deductible and received public reimbursement. Markup amounts are captured in the drug costs. Values may not add to totals due to rounding.

Data source: National Prescription Drug Utilization Information System Database, Canadian Institute for Health Information.

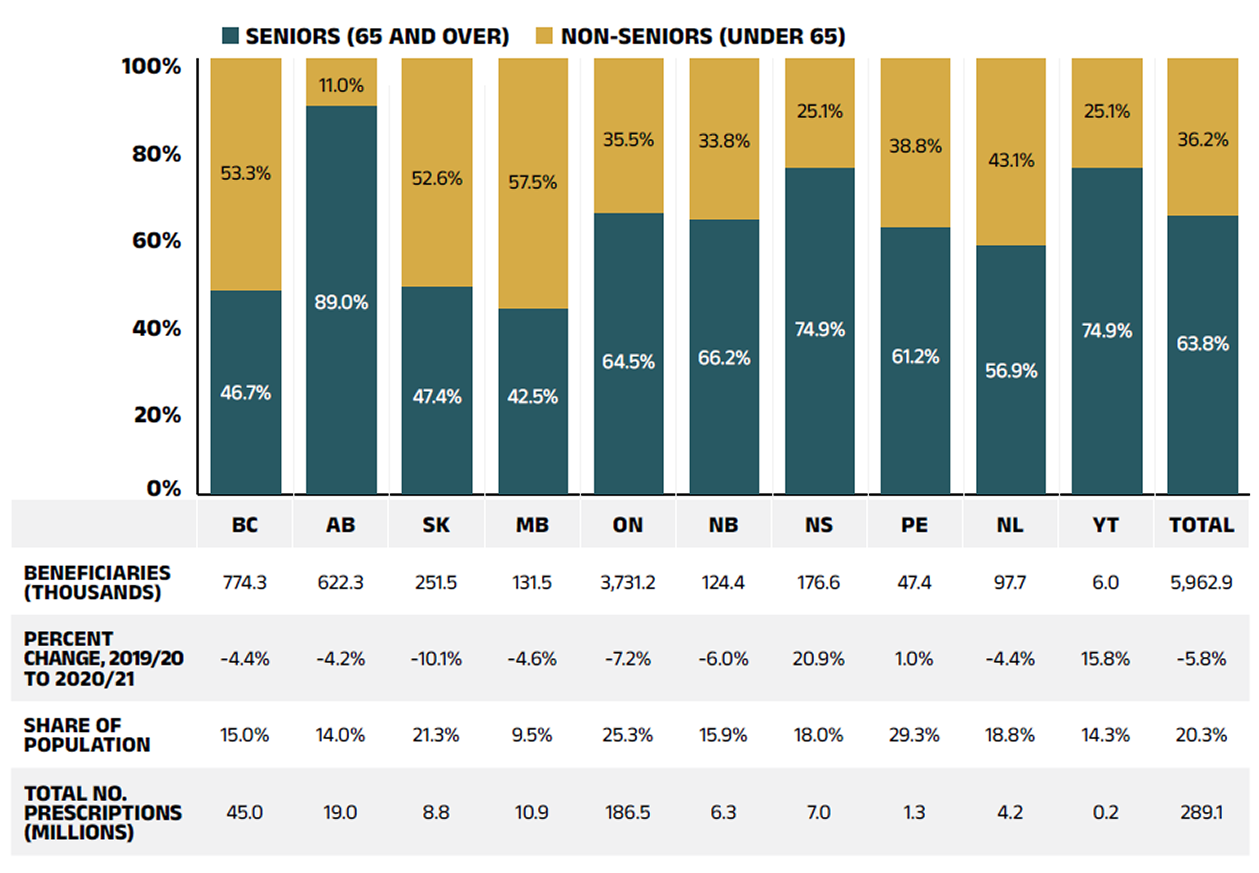

The annual growth in prescription expenditures is a function of increases in the number of active beneficiaries and their drug costs. In relation to the COVID-19 pandemic, the overall NPDUIS public plan beneficiary population declined by 5.8%. In 2020/21, close to 6 million active beneficiaries filled 289 million prescriptions that were accepted towards a deductible or paid for (in full or in part) by the NPDUIS public drug plans.

After 2019/20, the redesign of Ontario OHIP+ program was completed and became stable. It had little impact to the NPDUIS public drug plans. However, with the onset of the COVID-19 pandemic, approximately 366 thousand fewer Canadians filled a prescription for reimbursement to public drug plans. As this decline primarily impacted non-senior population, seniors made up a more dominant proportion (64%) of the total active beneficiaries, though this share varied greatly across jurisdictions because of differences in plan design, eligibility, and the demographics of the beneficiary population (Figure 1.3).

Figure description

This stacked column graph shows the percent share of utilization in senior and non-senior populations for each of the NPDUIS public drug plans in 2020/21, along with the totals across all plans. A table below gives the number of active beneficiaries in thousands, the change in beneficiary population from 2019/20 to 2020/21, the number of active beneficiaries as share of the population, and the total number of prescriptions, in millions.

| British Columbia | Alberta | Saskatchewan | Manitoba | Ontario | New Brunswick | Nova Scotia | Prince Edward Island | Newfoundland and Labrador | Yukon | Total | |

|---|---|---|---|---|---|---|---|---|---|---|---|

Seniors |

46.7% |

89.0% |

47.4% |

42.5% |

64.5% |

63.0% |

74.9% |

61.2% |

56.9% |

74.9% |

63.7% |

Non-seniors |

53.3% |

11.0% |

52.6% |

57.5% |

35.5% |

37.0% |

25.1% |

38.8% |

43.1% |

25.1% |

36.3% |

Beneficiaries (thousands) |

774.3 |

622.3 |

251.5 |

131.5 |

3,731.2 |

124.4 |

176.6 |

47.4 |

97.7 |

6.0 |

5,962.9 |

Percent change in the beneficiary population from 2019/20 to 2020/21 |

-4.4% |

-4.2% |

-10.1% |

-4.6% |

-7.2% |

-6.0% |

20.9% |

1.0% |

-4.4% |

15.8% |

-5.8% |

Beneficiary share of population |

15.0% |

14.0% |

21.3% |

9.5% |

25.3% |

15.9% |

18.0% |

29.3% |

18.8% |

14.3% |

20.3% |

Total number of prescriptions (millions) |

45.0 |

19.0 |

8.8 |

10.9 |

186.5 |

6.3 |

7.0 |

1.3 |

4.2 |

0.2 |

289.1 |

Note This analysis only includes data for beneficiaries that met their deductible and received public reimbursement. Not all the sub-plan data for the jurisdictions is reported to NPDUIS, which may impact the distribution of senior and non-senior shares.

Data source: National Prescription Drug Utilization Information System Database, Canadian Institute for Health Information; Statistics Canada, CANSIM Table 051-0005.

Drug Costs of Prescription Drug Expenditures

Prescription Drug Expenditures = Drug Costs (82%) + Dispensing Costs (18%)

Drug costs, including average reported markups of about 5%Reference II, represent the largest component of prescription drug expenditures and have the greatest influence on overall trends. Following an increase of 4.3% in 2019/20, drug costs rose by another sizable rate of 5.3% in 2020/21. The average rate of change over the last three years was 5.2% across the public plans.

Figure 1.4 reports the annual rate of change in drug costs for each NPDUIS drug plan from 2018/19 to 2020/21. Many plans experienced positive rates of change in 2020/21, ranging from 0.9% in Alberta to 29.3% in Yukon. Drug costs in British Columbia declined the second year by 1.1%.

Figure description

This column graph illustrates the trend in annual rates of change in drug costs from 2018/19 to 2020/21 for each of the NPDUIS drug plans. Total annual results for all plans are included. The compound annual growth rates for the period are given in a table below.

| British Columbia | Alberta | Saskatchewan | Manitoba | Ontario | New Brunswick | Nova Scotia | Prince Edward Island | Newfoundland and Labrador | Yukon | Total | |

|---|---|---|---|---|---|---|---|---|---|---|---|

2018/19 |

5.4% |

3.5% |

6.9% |

1.3% |

7.5% |

1.7% |

2.7% |

3.9% |

0.5% |

13.4% |

5.8% |

2019/20 |

-1.4% |

9.2% |

6.2% |

4.1% |

4.1% |

9.9% |

8.4% |

8.9% |

4.8% |

-24.9% |

4.3% |

2020/21 |

-1,1% |

0.5% |

4.3% |

6.0% |

6.4% |

8.2% |

25.3% |

9.3% |

6.9% |

29.3% |

5.3% |

Compound annual growth rate |

0.9% |

4.3% |

5.8% |

3.7% |

6.0% |

6.5% |

11.7% |

7.3% |

4.0% |

3.3% |

5.2% |

Note: This analysis only includes data for beneficiaries that met their deductible and received public reimbursement.

* Compound annual growth rate.

† The 2019/20 to 2020/21 rate of change and the 3-year CAGR were calculated without data from the NIHB program. The impact of NIHB data on the rate of change would be insignificant (approximately 0.1%).

‡ In Nova Scotia, Community Services Pharmacare Benefits (Plan F) data was not previously submitted to the CIHI NPDUIS database but has been submitted since 2020/21. This addition resulted in a large, one-time increase in the beneficiary population and their drug use in 2020/21.

Data source: National Prescription Drug Utilization Information System Database, Canadian Institute for Health Information.

Figure 1.5 breaks down the annual rate of change in drug costs from 2019/20 to 2020/21 by market segment (bar chart) and gives the corresponding market share in 2020/21 for each (pie chart). These results provide a snapshot of how the distribution of sales across market segments has shifted over the last year. As the market status of a medicine is dynamic, the medicines contributing to any one segment may differ from year to year.

Patented medicines represent the largest segment of the market, capturing 56.4% of public plan drug costs in 2020/21. Costs for direct-acting antivirals (DAAs) for hepatitis C decreased by 6.8% in 2020/21, reflecting a decline in the use of these medicines (see Spotlight on DAA drugs for hepatitis C in Section 2, under “Drug-mix effect”). Despite this pull, the patented market segment still increased moderately by 2.1%, driven mainly by the use of high-cost medicines—those with an average annual cost per beneficiary greater than $10,000, other than DAAs—which grew by a considerable 14.3%.

Unlike the substantial growth in the previous year, the single-source non-patented market decreased by 7.4% in 2020/21, reflecting diminishing costs of this segment without significant patent status changes over the course of 2020/21.

Costs for multi-source non-patented medicines, which include generics and their reference brand-name drugs as well as biosimilars and their originator biologics, increased by 11.0% in 2020/21, now accounting for 30.2% of drug costs. This segment can be broken down into two distinct sub-segments: multi-source generic medicines made up 17.2% ($1,730 million) of drug costs in 2020/21 and grew by 4.7%, while the remaining medicines, consisting mainly of off-patent biologics and biosimilars, experienced a faster growth at a rate of 20.6% to reach 13.0% ($1,304 million) of drug costs. Multi-source non-patented biologics are an important group of medicines to monitor in future years as biosimilars gain traction in the public plans.

Figure description

This graph consists of two parts: a horizontal bar chart on the left breaks down the annual rate of change in drug costs between 2019/20 and 2020/21 by market segment and a pie chart on the right displays the market share of the total drug cost for each segment. Both represent the combined totals for NPDUIS public drug plans.

The bar chart is divided into three parts. The first gives the annual rate of change for all drugs; the second displays the growth rates for the three main market segments; and the third focuses on the patented medicine segment. Results indicate whether they include or exclude the direct-acting antiviral (DAA) drugs for the treatment of hepatitis C. High-cost drugs have an annual cost greater than $10,000 and include both biologics and non-biologics. Total drug costs for each segment in 2020/21 are also given.

Annual rates of change

| Rate of change in drug costs from 2019/20 to 2020/21 | Total drug costs in 2020/21, in millions of dollars | |

|---|---|---|

All drugs |

5.3% |

$10,045 |

All drugs excluding DAA drugs |

7.4% |

$9,753 |

By market segment |

||

Patented |

2.1% |

$5,666 |

Patented excluding DAA drugs |

5.7% |

$5,378 |

Multi-source non-patented |

11.0% |

$3,034 |

Single-source non-patented |

-7.4% |

$867 |

Patented medicines |

||

High-cost drugs excluding DAA drugs |

14.3% |

$3,114 |

DAA drugs |

-6.8% |

$288 |

Biologics |

12.7% |

$1,977 |

Non-biologics excluding DAA drugs |

7.3% |

$3,402 |

Share of drug cost

| Market segment | Share of drug cost |

|---|---|

Patented† |

56.4% |

Multi-source non-patented: generic |

17.2% |

Multi-source non-patented: non-generic |

13.0% |

Single-source non-patented |

8.6% |

Other§ |

4.7% |

Note: This analysis only includes data for beneficiaries that met their deductible and received public reimbursement. DAA drugs are direct-acting antivirals used in the treatment of hepatitis C. A glossary of terms with information on each of the market segments is available on the PMPRB website.

* British Columbia, Alberta, Saskatchewan, Manitoba, Ontario, New Brunswick, Nova Scotia, Prince Edward Island, Newfoundland and Labrador, and Yukon.

† The patented medicines market segment includes all medicines that had patent protection in the period of study, whether or not the patent expired during that period. As such, the rate of growth does not reflect the loss of patent exclusivity for medicines over the course of the fiscal year.

‡ High-cost drugs have an average annual treatment cost greater than $10,000 and include both biologics and non-biologics.

§ This market segment includes devices, compounded drugs, and other products that are reimbursed by public drug plans but do not have a Health Canada assigned Drug Identification Number (DIN).

Data source: National Prescription Drug Utilization Information System Database, Canadian Institute for Health Information.

Dispensing Costs of Prescription Drug Expenditures

Prescription Drug Expenditures = Drug Costs (82%) + Dispensing Costs (18%)

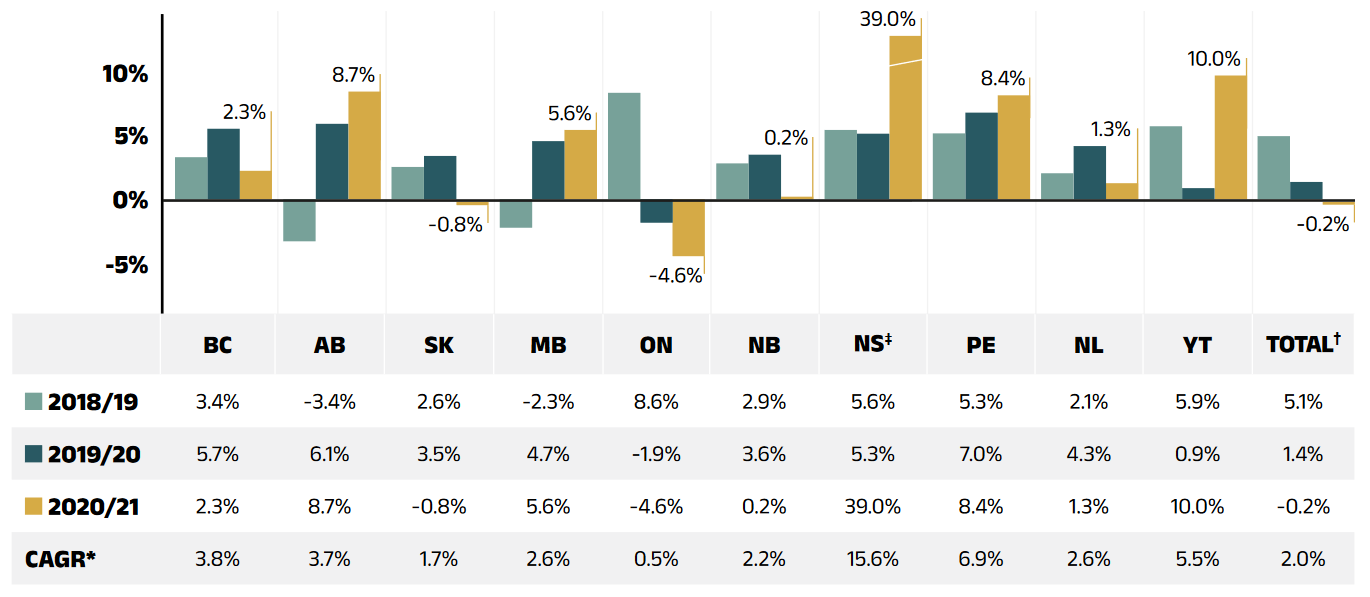

Dispensing costs make up an important part of prescription drug expenditures. Owing largely to temporary dispensing frequency practices during the COVID-19 pandemic and policy changes to the long-term care (LTC) program in Ontario, the overall dispensing costs in the NPDUIS public plans had no growth. Dispensing costs declined slightly by 0.2% in 2020/21, for a compound annual growth rate of 2.0% over the last three years. Figure 1.6 reports the annual rate of change in dispensing costs for each NPDUIS drug plan from 2018/19 to 2020/21. Jurisdictional variations may be due to changes in dispensing fee policies and plan designs, as well as changes in the number of prescriptions and their size, among other factors.

Brief Insights: Dispensing Fees and Policies

On January 1, 2020, the Ontario government introduced a new long-term care (LTC) capitation funding model. It included a shift in the payment model for professional pharmacy services (dispensing fees and professional pharmacy services) for LTC homes from fee-for-service to a fixed per-patient amount. As such, ODB-eligible prescription claims submitted for residents of LTC homes reflect a zero-dollar dispensing fee. This change is reflected in the full course of fiscal year 2020/21.

Beginning March/April 2020, most NPDUIS public drug plans introduced temporary changes to policies on dispensing frequency during the COVID-19 pandemic. These changes are also reflected in Section 3, “The Drivers of Dispensing Costs”.

A summary of dispensing fee policies for each of the public drug plans is available on the PMPRB website.

Figure description

This column graph illustrates the trend in annual rates of change for dispensing costs from 2018/19 to 2020/21 for each of the NPDUIS public drug plans. Total annual results for all plans are included. Compound annual growth rates for the period are given in a table below.

| British Columbia | Alberta | Saskatchewan | Manitoba | Ontario | New Brunswick | Nova Scotia | Prince Edward Island | Newfoundland and Labrador | Yukon | Total | |

|---|---|---|---|---|---|---|---|---|---|---|---|

2018/19 |

3.4% |

-3.4% |

2.6% |

-2.3% |

8.6% |

2.9% |

5.6% |

5.3% |

2.1% |

5.9% |

5.1% |

2019/20 |

5.7% |

6.1% |

3.5% |

4.7% |

-1.9% |

3.6% |

5.3% |

7.0% |

4.3% |

0.9% |

1.4% |

2020/21 |

2.3% |

8.7% |

-0.8% |

5.6% |

-4.6% |

0.2% |

39.0% |

8.4% |

1.3% |

10.0% |

-0.2% |

Compound annual growth rate |

3.8% |

3.7% |

1.7% |

2.6% |

0.5% |

2.2% |

15.6 % |

6.9% |

2.6% |

5.5% |

2.0% |

Note: This analysis only includes data for beneficiaries that met their deductible and received public reimbursement.

* Compound annual growth rate.

† The 2019/20 to 2020/21 rate of change and the 3-year CAGR were calculated without data from the NIHB program. The impact of NIHB data on the rate of change would be insignificant (approximately 0.1%).

‡ In Nova Scotia, Community Services Pharmacare Benefits (Plan F) data was not previously submitted to the CIHI NPDUIS database but has been submitted since 2020/21. This addition resulted in a large, one-time increase in the beneficiary population and their drug use in 2020/21.

Data source: National Prescription Drug Utilization Information System Database, Canadian Institute for Health Information.

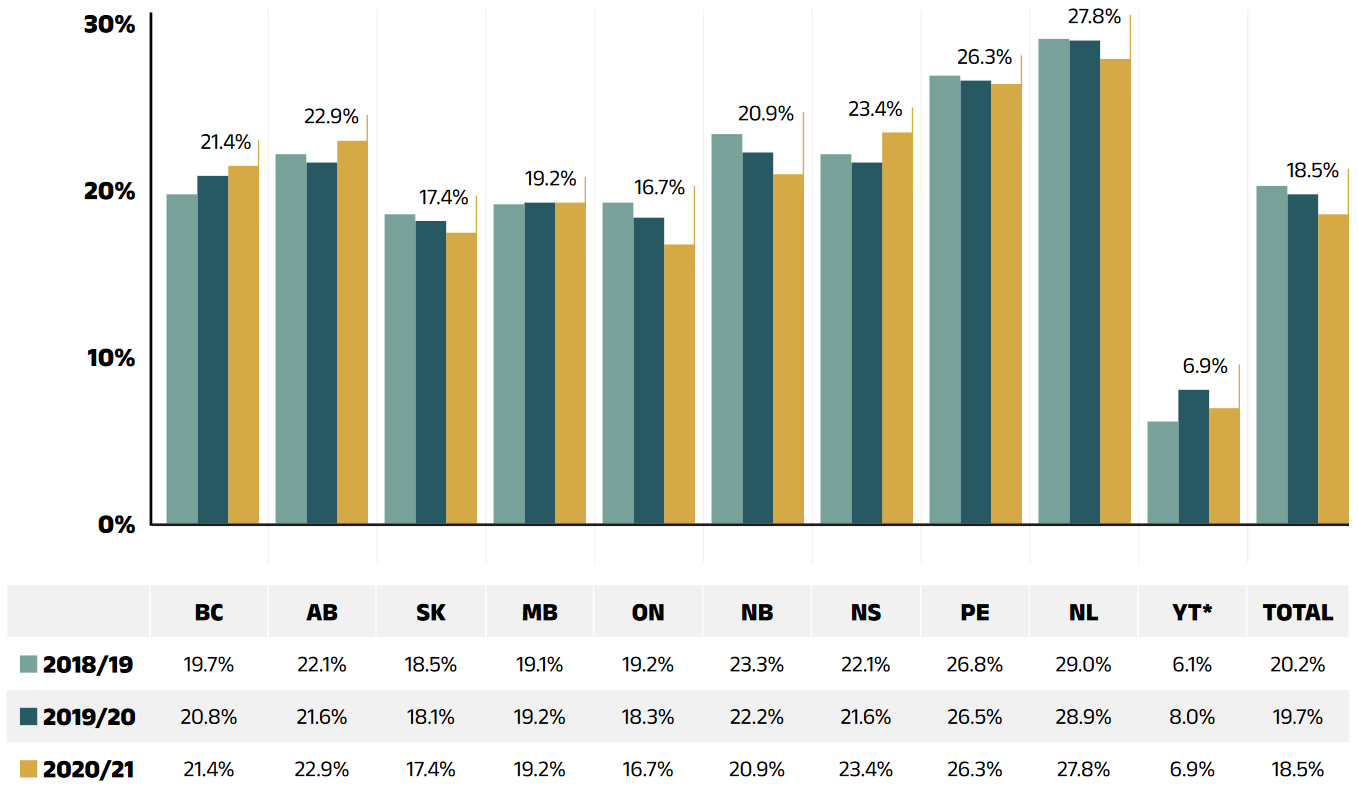

Unlike drug costs, dispensing costs have grown at a slow to negative rate over the last three years. Their share of overall prescription drug expenditures has continued to decline, from 20.2% in 2018/19 to 18.5% in 2020/21

Figure 1.7 depicts the trend in the dispensing cost share of total prescription expenditures for each NPDUIS drug plan from 2018/19 to 2020/21.

Figure description

This column graph shows the trend in annual dispensing costs as a share of the total prescription expenditures from 2018/19 to 2020/21 for each of the NPDUIS public drug plans. Total annual results for all plans are included.

| British Columbia | Alberta | Saskatchewan | Manitoba | Ontario | New Brunswick | Nova Scotia | Prince Edward Island | Newfoundland and Labrador | Yukon* | Total | |

|---|---|---|---|---|---|---|---|---|---|---|---|

2018/19 |

19.7% |

22.1% |

18.5% |

19.1% |

19.2% |

23.3% |

22.1% |

26.8% |

29.0% |

6.1% |

20.2% |

2019/20 |

20.8% |

21.6% |

18.1% |

19.2% |

18.3% |

22.2% |

21.6% |

26.5% |

28.9% |

8.0% |

19.7% |

2020/21 |

21.4% |

22.9% |

17.4% |

19.2% |

16.7% |

20.9% |

23.4% |

26.3% |

27.8% |

6.9% |

18.5% |

Note: This analysis only includes data for beneficiaries that met their deductible and received public reimbursement.

* Yukon allows for markups of up to 30%; as such, dispensing costs account for a smaller share of their total expenditures.

Data source: National Prescription Drug Utilization Information System Database, Canadian Institute for Health Information.

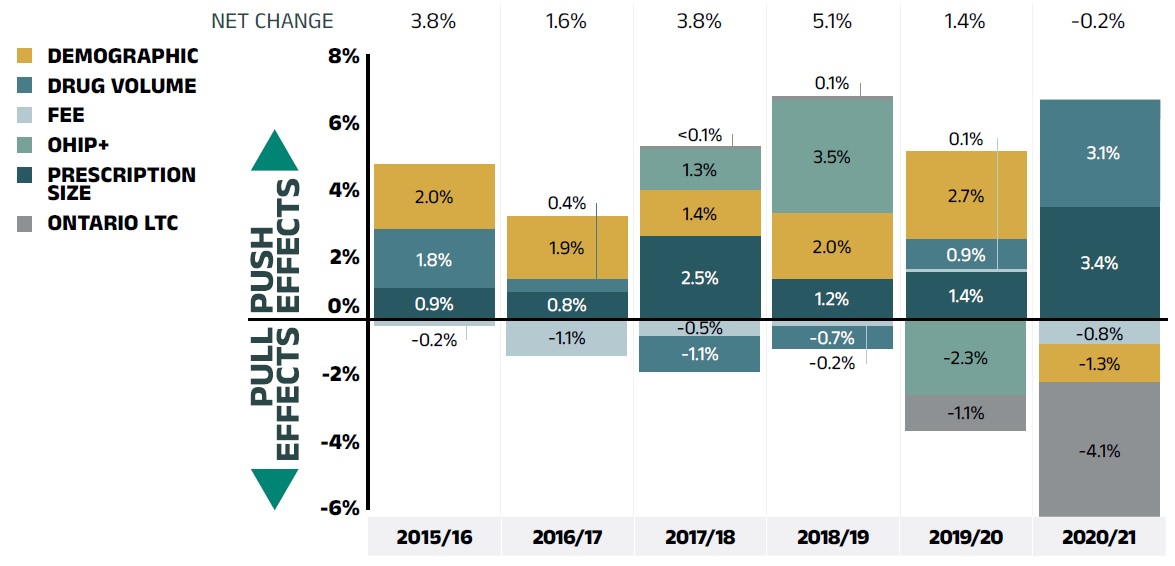

2. The Drivers of Drug Costs, 2019/20 to 2020/21

Drug cost increases in the NPDUIS public plans in 2020/21 were primarily driven by a sustained increase in the use of higher-cost medicines. This is despite the decreasing use of DAA drugs. As generic prices have stabilized, the effect from substitution became stronger than the price effect; however, these combined forces no longer offset the increasing cost pressures from the drug-mix effect. In 2020/21, there was a notable decrease in the number of active beneficiaries due to COVID-19. This exerted a downward demographic effect, which was more than offset by a sizable increase in the number of claims per patient (captured in the volume effect), pushing spending upwards and resulting in an overall increase of 5.3%.

In this section, a comprehensive cost driver analysis is used to determine how much public plan drug costs would have changed between 2019/20 and 2020/21 if only one factor (e.g., the price of drugs) was considered while all the others remained the same.Reference III

Changes in drug costs are driven by a number of push and pull effects. The net effect of these opposing forces yields the overall rate of change.

Price change effect: Changes in the prices of both brand-name and generic drugs, determined at the molecule, strength, and form level.

Substitution effect: Shifts from brand-name to generic drugs, as well as shifts to biosimilar use.

Demographic effect: Changes in the number of active beneficiaries, as well as shifts in the distribution of age or gender.

Volume effect: Changes in the number of prescriptions dispensed to patients, the average number of units of a drug dispensed per prescription, and/or shifts in the use of various strengths or forms of a medicine.

Drug-mix effect: Shifts in use between lower- and higher-cost drugs, including those entering, exiting, or remaining in the market during the time period analyzed.

In addition to the standard annual effects, Ontario’s OHIP+ program was previously treated as a separate factor in the cost driver analysis, encompassing all effects associated with the program (e.g., volume and demographic changes). As such, the OHIP+ effect reflected the overall impact from the plan design changes. After 2019/20, OHIP+ program spending stabilized and had little impact; therefore, it is no longer reported as a separate factor of cost drivers in this edition of CompassRx. For historical data, please consult previous editions.

Figure 2.1 provides insight into the pressures driving the rates of change in drug costs from 2015/16 to 2020/21.

Typically, changes in the patient population and the volume of drugs prescribed result in a slight to moderate increase of drug costs. Over the past few years, this increase has been between 1% and 3% for the demographic effect, and remained stable at 1% for the volume effect. In 2020/21, however, these forces were impacted by the COVID-19 pandemic. Despite the 2.3% downward pull of the demographic effect from a notable pandemic-led decrease in the number of active beneficiaries, there is a sizable increase in the number of claims per patient captured in the volume that pushed overall spending upward by 4.6% over the same period. These effects are expected to gradually return to pre-pandemic levels in future years.

The most pronounced upward push on costs can be attributed to the use of higher-cost medicines (other than DAAs for hepatitis C), which consistently accounted for 4% to 5% of annual growth between 2015/16 and 2017/18, and jumped to an average of 6.1% over the past three years. In contrast, the use of DAAs continued to decrease in 2020/21, pulling drug costs down by 2.1%. The combined effects of DAAs and other higher-cost drugs still added a sizable 4.3% upward pressure on drug costs in NPDUIS public plans.

Counterbalancing these upward cost pressures, generic and biosimilar substitution and price reductions generally exert a downward pull on costs. The magnitude of these effects can vary from year to year depending on the timing of generic and biosimilar market entries and the implementation of policies lowering generic prices. In 2020/21, the influence of the price change effect diminished to less than 0.1%. The substitution effect became stronger, pulling drug costs down by 1.4%. Over the past two years, the combined rate of these two effects has stabilized to slightly below -1%.

Figure description

This column graph describes the key factors or effects that impacted the rates of change in drug costs across all NPDUIS public drug plans for each year from 2015/16 to 2020/21. Each column is broken out to give the positive or negative contribution of each effect: drug-mix; volume; demographic; price change; and substitution. The drug-mix effect of direct-acting antiviral (DAA) drugs for hepatitis C is shown separately, as are the effects of the Ontario Health Insurance Plan Plus (OHIP+) initiative. The OHIP+ effect is not captured for 2020/21. The total positive push effect, negative pull effect, and net change are given for each year.

| 2015/16 | 2016/17 | 2017/18 | 2018/19 | 2019/20 | 2020/21 | |

|---|---|---|---|---|---|---|

OHIP+ |

– |

– |

1.5% |

4.7% |

-3.0% |

– |

Drug-mix, direct-acting antiviral (DAA) drugs |

8.0% |

-2.3% |

2.4% |

0.6% |

-1.6% |

-2.1% |

Drug mix, other drugs |

4.1% |

4.4% |

4.7% |

6.1% |

5.8% |

6.3% |

Volume |

1.2% |

1.0% |

1.0% |

-0.3% |

1.3% |

4.3% |

Demographic |

3.0% |

1.8% |

1.4% |

1.0% |

3.0% |

-2.0% |

Price change |

-1.8% |

-1.0% |

-1.1% |

-4.0% |

-0.5% |

<0.1% |

Substitution |

-2.3% |

-1.8% |

-1.3% |

-2.2% |

-0.6% |

-1.4% |

Total push effect |

16.2% |

7.2% |

11.0% |

12.4% |

10.2% |

11.0% |

Total pull effect |

-4.1% |

-5.1% |

-2.3% |

-6.5% |

-5.7% |

-5.8% |

Net change |

12.0% |

2.0% |

8.3% |

5.8% |

4.3% |

5.3% |

Note: Historic values are reported for 2015/16.

This analysis is based on publicly available pricing information. It does not reflect confidential price discounts negotiated by the pCPA on behalf of the public plans.

Values may not add to totals due to rounding and the cross effect. Results for Yukon were included from 2016/17 onward.

* British Columbia, Alberta, Saskatchewan, Manitoba, Ontario, New Brunswick, Nova Scotia, Prince Edward Island, Newfoundland and Labrador, Yukon, and the Non-Insured Health Benefits (NIHB) Program. Results for 2020/21 do not include the NIHB program.

Data source: National Prescription Drug Utilization Information System Database, Canadian Institute for Health Information.

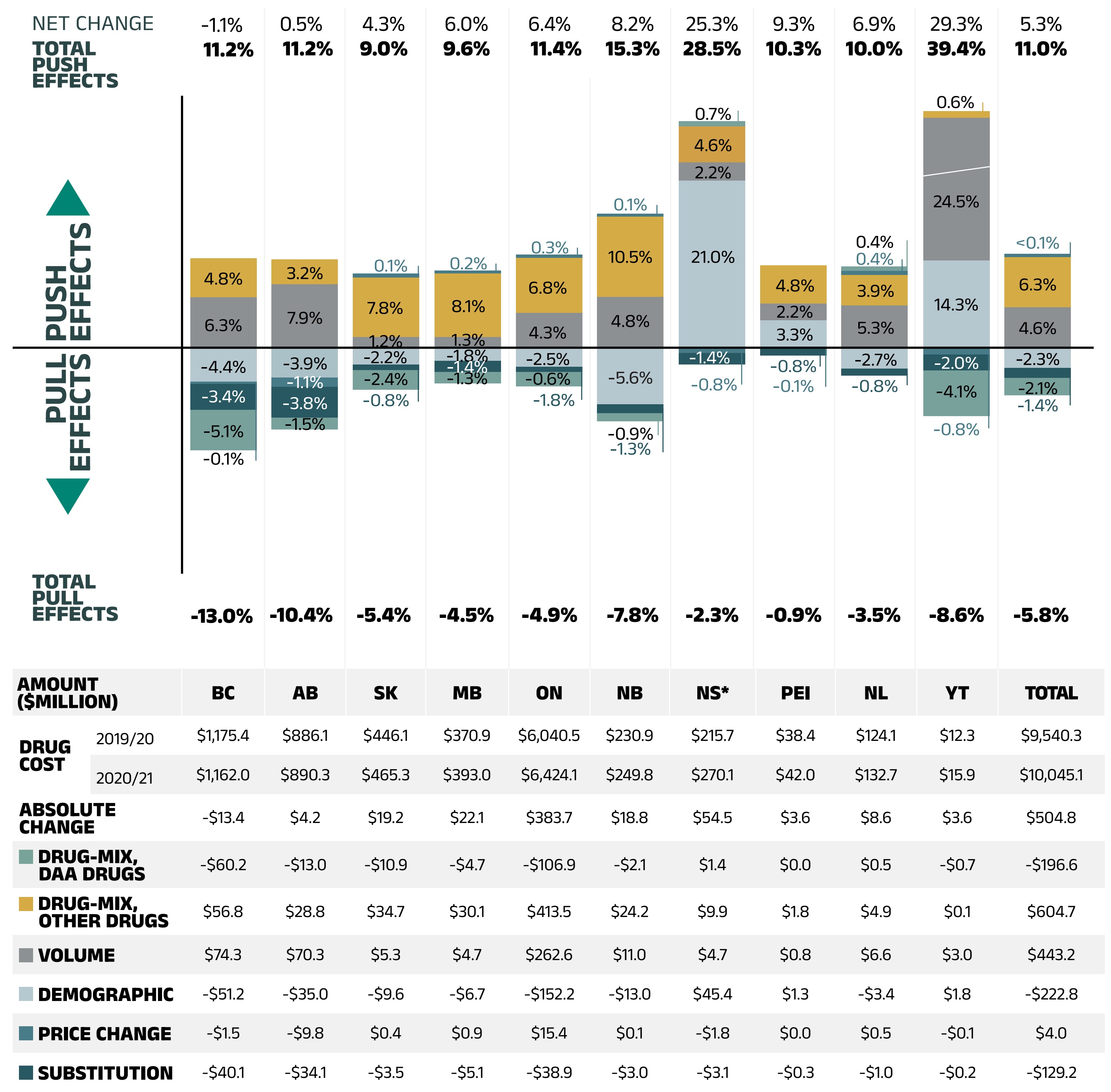

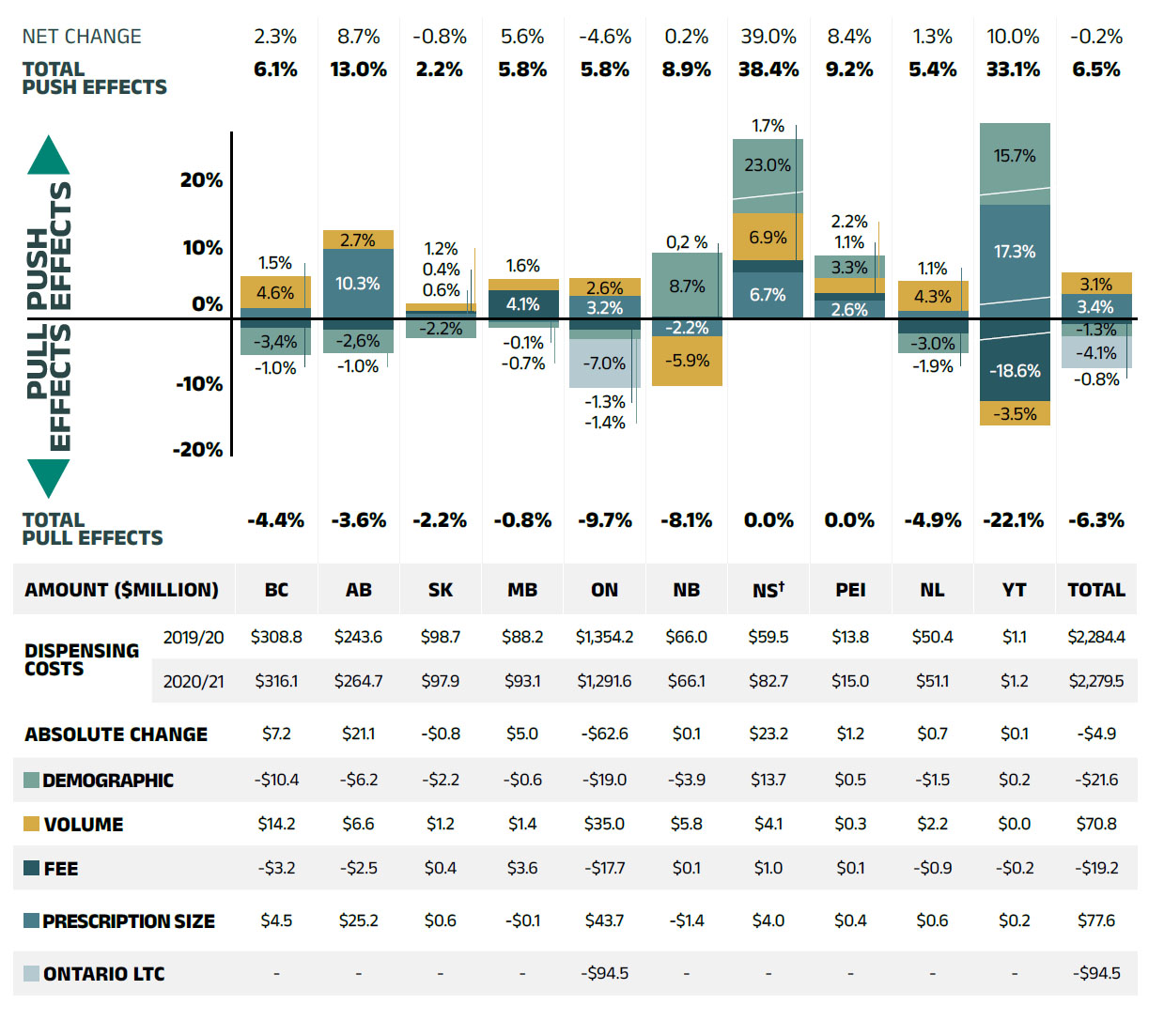

The overall 5.3% increase in drug costs in 2020/21 represents an absolute growth of $505 million, with varying rates of growth among the public drug plans ranging from approximately -1% to 9%. Nova Scotia and Yukon were the exceptions with 25.3% and 29.3% increases, respectively (Figure 2.2). These variations were mainly due to differences in the magnitude of the opposing factors. Other jurisdictions with higher overall growth rates included Prince Edward Island (9.3%), New Brunswick (8.2%), and Newfoundland and Labrador (6.9%).

The increased use of higher-cost drugs other than DAAs had the greatest push effect, with an overall impact of 6.3% ($605 million) ranging from 0.6% to 10.5% across jurisdictions. The use of DAA drugs for hepatitis C continued to decrease and drove costs down by 2.1% ($197 million). Differences in the drug-mix effect across public drug plans may be related to plan designs, formulary listing decisions, or the disease profiles of the population, among other determinants. The overall declining impact of DAA drugs also varied, with the largest downward pull in British Columbia (-5.1%), followed by Yukon (-4.1%) and Manitoba (-2.4%). The use of DAAs in Nova Scotia and Newfoundland and Labrador pushed costs upward very slightly (0.4% and 0.1%, respectively).

In recent years, as a result of growth of the overall population of a jurisdiction, an increase in the number of Canadians eligible for senior coverage (65+), and/or plan design changes that expanded coverage to new populations or patient groups, the demographic effect boosted drug costs in the NPDUIS public plans by a fairly consistent 1% to 3%. However, with the onset of the COVID-19 pandemic, in 2020/21, fewer active beneficiaries submitted claims for reimbursement to public plans in many provinces, exerting an overall downward demographic effect of 2.3% ($223 million). This downward pull effect was observed in many provinces, with the largest impact in New Brunswick (-5.6%), British Columbia (-4.4%), Alberta (-3.9%) and Newfoundland and Labrador (-2.7%).

Despite fewer active beneficiaries in many public plans, a sizable increase in the number of prescriptions dispensed per patient (captured by the volume effect) pushed overall drug costs upward by 4.6% or $443 million in 2020/21. This effect was an important driver and more than offset the downward demographic effect in Alberta (7.9%), British Columbia (6.3%), Newfoundland and Labrador (5.3%) and New Brunswick (4.8%).

The price change effect (<0.1% or $4 million) had the smallest contribution and was relatively uniform across jurisdictions. The cost savings effects of generic and biosimilar substitution (-1.4% or -$129 million) was stronger than the price change effect but varied across public plans. The substitution effect was more pronounced in Alberta (-3.8%) and British Columbia (-3.4%), as a result of the introduction of biosimilar switching initiatives. The key effects for 2020/21—price change, substitution, and drug-mix—are explored in more detail in the following section.

Figure description

This column graph and table describe the key factors or effects that impacted the rates of change in drug costs for each of the NPDUIS public drug plans from 2019/20 to 2020/21. Each column is broken out to give the positive or negative contribution of each effect: drug-mix; volume; demographic; price change; and substitution. The drug-mix effect of direct-acting antiviral (DAA) drugs for hepatitis C is shown separately. The total positive push effect, negative pull effect and net change are given for each year. Total results for all plans are also included.

| British Columbia | Alberta | Saskatchewan | Manitoba | Ontario | New Brunswick | Nova Scotia | Prince Edward Island | Newfoundland and Labrador | Yukon | Total | |

|---|---|---|---|---|---|---|---|---|---|---|---|

Demographic |

-4.4% |

-3.9% |

-2.2% |

-1.8% |

-2.5% |

10.0% |

21.0% |

3.3% |

-2.7% |

11.0% |

-2.0% |

Volume |

6.3% |

7.9% |

1.2% |

1.3% |

4.3% |

-9.4% |

2.2% |

2.2% |

5.3% |

18.0% |

4.3% |

Drug Mix, Other Drugs |

4.8% |

3.2% |

7.8% |

8.1% |

6.8% |

10.5% |

4.6% |

4.8% |

3.9% |

0.6% |

6.3% |

Price Change |

-0.1% |

-1.1% |

0.1% |

0.2% |

0.3% |

0.1% |

-0.8% |

-0.1% |

0.4% |

-0.8% |

0.0% |

Substitution |

-3.4% |

-3.8% |

-0.8% |

-1.4% |

-0.6% |

-1.3% |

-1.4% |

-0.8% |

-0.8% |

-2.0% |

-1.4% |

Drug Mix, DAA Drugs |

-5.1% |

-1.5% |

-2.4% |

-1.3% |

-1.8% |

-0.9% |

0.7% |

0.0% |

0.4% |

-5.7% |

-2.1% |

Total push effect |

11.2% |

11.2% |

9.0% |

9.6% |

11.4% |

15.3% |

28.5% |

10.3% |

10.0% |

39.4% |

11.0% |

Total pull effect |

-13.0% |

-10.4% |

-5.4% |

-4.5% |

-4.9% |

-7.8% |

-2.3% |

-0.9% |

-3.5% |

-8.6% |

-5.8% |

Net change |

-1.1% |

0.5% |

4.3% |

6.0% |

6.4% |

8.2% |

25.3% |

9.3% |

6.9% |

29.3% |

5.3% |

An accompanying table gives the corresponding changes in millions of dollars, as well as the total drugs costs in 2019/20 and 2020/21 and the absolute change for each plan.

| British Columbia | Alberta | Saskatchewan | Manitoba | Ontario | New Brunswick | Nova Scotia | Prince Edward Island | Newfoundland and Labrador | Yukon | Total | |

|---|---|---|---|---|---|---|---|---|---|---|---|

Drug cost 2019/20 |

$1,175.40 |

$886.10 |

$446.10 |

$370.90 |

$6,040.50 |

$230.90 |

$215.70 |

$38.40 |

$124.10 |

$12.30 |

$9,540.30 |

Drug cost 2020/21 |

$1,162.00 |

$890.30 |

$465.30 |

$393.00 |

$6,424.10 |

$249.80 |

$270.10 |

$42.00 |

$132.70 |

$15.90 |

$10,045.10 |

Absolute change |

-$13.40 |

$4.20 |

$19.20 |

$22.10 |

$383.70 |

$18.80 |

$54.50 |

$3.60 |

$8.60 |

$3.60 |

$504.80 |

Drug-mix, direct-acting antiviral (DAA) drugs |

-$60.20 |

-$13.00 |

-$10.90 |

-$4.70 |

-$106.90 |

-$2.10 |

$1.40 |

$0.00 |

$0.50 |

-$0.70 |

-$196.60 |

Drug-mix, other drugs |

$56.80 |

$28.80 |

$34.70 |

$30.10 |

$413.50 |

$24.20 |

$9.90 |

$1.80 |

$4.90 |

$0.10 |

$604.70 |

Volume |

$74.30 |

$70.30 |

$5.30 |

$4.70 |

$262.60 |

$11.00 |

$4.70 |

$0.80 |

$6.60 |

$3.00 |

$443.2 |

Demographic |

-$51.20 |

-$35.00 |

-$9.60 |

-$6.70 |

-$152.20 |

-$13.0 |

$45.40 |

$1.30 |

-$3.40 |

$1.80 |

-$222.8 |

Price change |

-$1.50 |

-$9.80 |

$0.40 |

$0.90 |

$15.40 |

$0.10 |

-$1.80 |

$0.00 |

$0.50 |

-$0.10 |

$4.00 |

Substitution |

-$40.10 |

-$34.10 |

-$3.50 |

-$5.10 |

-$38.90 |

-$3.00 |

-$3.10 |

-$0.30 |

-$1.00 |

-$0.20 |

-$129.20 |

Note: This analysis is based on publicly available pricing information. It does not reflect confidential drug price discounts negotiated by the pCPA on behalf of the public plans. Values may not add to totals due to rounding and the cross effect.

* In Nova Scotia, Community Services Pharmacare Benefits (Plan F) data was not previously submitted to the CIHI NPDUIS database but has been submitted since 2020/21. This addition resulted in a large, one-time increase in the beneficiary population and their drug use. As such, the overall impact was captured in the demographic and volume effects in 2020/21.

Data source: National Prescription Drug Utilization Information System Database, Canadian Institute for Health Information.

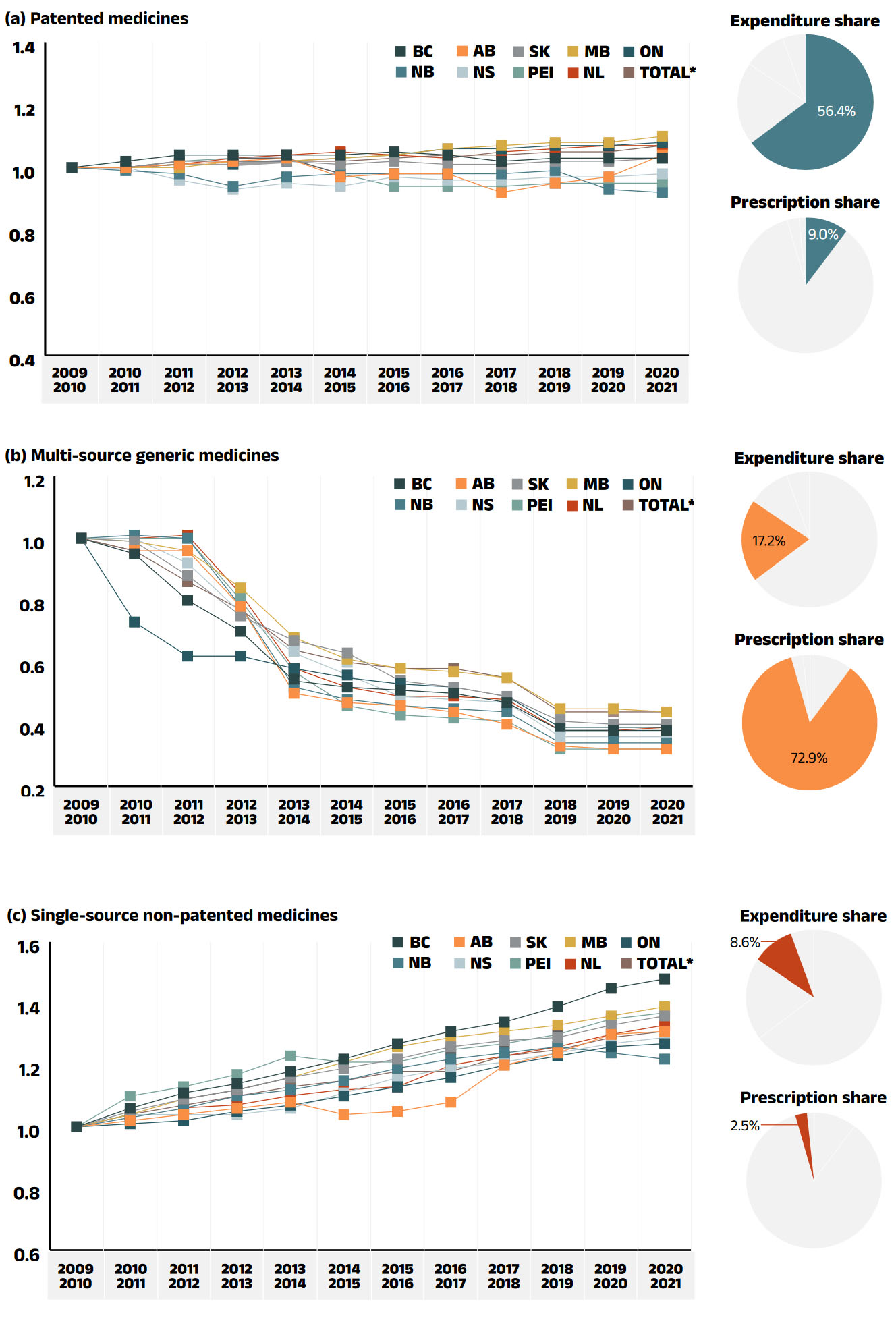

Price Change Effect

This effect captures changes in the prices of both brandname and generic medicines. Following the significant one-time drop in generic prices resulting from the implementation of the pan-Canadian Generic Price Initiative in April 2018, its influence has diminished. In 2020/21, changes in drug prices played a very minor role in the growth of drug costs, accounting for less than 0.1% ($4 million).

An analysis by market segment suggests that the reduction in the average unit costs reimbursed in the multi-source non-patented category saw little change. The average unit costs of patented medicines remained stable, while the costs of single-source non-patented medicines increased at a steady pace.

Figure 2.3 reports long-term trends in average unit costs from 2009/10 to 2020/21 by market segment for (a) patented medicines; (b) multi-source generic medicines; and (c) single-source non-patented medicines, along with their corresponding 2020/21 market shares. The results are presented as an index, with the base year (2009/10) set to one and subsequent years reported relative to this value. The findings are a cost-weighted average of changes in the reimbursed unit costs for individual medicines. The analysis was restricted to oral solid formulations to ensure unit consistency.

From 2009/10 to 2020/21, the prices of patented medicines were stable, increasing by a modest average of 7%, while prices of single-source non-patented medicines increased by an average of 31%. Despite the significant rise in prices, the impact of this segment was limited due to its small size: single-source non-patented medicines make up just 8.6% of the market, while patented medicines represent a 56.4% share. The multi-source generics market shows a similar trend across all NPDUIS public drug plans that is tied to the various waves of generic price reforms. Average unit costs rapidly declined by nearly 40% in the first few years after the initial wave of reforms, and then decreased more gradually from 2014/15 to 2016/17 as generic prices stabilized. Following the most recent pricing initiatives, prices declined by an average of 3% in 2017/18 before a more notable 11% drop in 2018/19. Since then, they have remained steady without any further decrease from 2019/20 to 2020/21. As a result, the average multi-source generic unit cost across all jurisdictions in 2020/21 was less than half of the 2009/10 average.

Brief Insights: pCPA Initiatives

Through the pan-Canadian Pharmaceutical Alliance (pCPA), the provinces, territories, and federal government have been working collectively to achieve greater value for generic and brand-name medicines for Canada’s publicly funded drug programs.

Generic medicines:

Between April 1, 2015, and April 1, 2016, the prices of 18 commonly used generic medicines were reduced to 18% of their brand-name reference products. In addition, a one-year bridging period was initiated on April 1, 2017, which further reduced the prices of six of the molecules to 15% of the brand reference price.

As of April 1, 2018, a five-year joint agreement between the pCPA and the Canadian Generic Pharmaceutical Association (CGPA) reduced the prices of 67 of the most prescribed generic medicines in Canada by 25% to 40%, resulting in overall discounts of up to 90% off the price of their brand-name equivalents.

Effective April 1, 2022, the Historical Products Policy developed by pCPA and CGPA addresses concerns regarding assessments for generic products whose brand reference product has been cancelled post market.

Brand-name medicines:

As of July 31, 2022, 454 joint negotiations or product listing agreements (PLAs) for brand-name drugs had been completed by the pCPA, with another 38 negotiations underway. The impact of the confidential drug prices negotiated is not reflected in this analysis.

For more details, see the overview of generic pricing policies and pCPA initiatives available on the PMPRB website.

Figure description

This figure has three sections, each with a line graph depicting the average unit cost index from 2009/10 to 2020/21 for (a) patented medicines, (b) multi-source generic medicines, and (c) single-source non-patented medicines. Results are given for each NPDUIS drug plan, as well as the total for all plans. Expenditure and prescription shares for 2020/21 are shown in pie charts beside each graph.

(a) Patented medicines

Expenditure share: 56.4%

Prescription share: 9.0%

| 2009/10 | 2010/11 | 2011/12 | 2012/13 | 2013/14 | 2014/15 | 2015/16 | 2016/17 | 2017/18 | 2018/19 | 2019/20 | 2020/21 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

British Columbia |

1.00 |

1.02 |

1.04 |

1.04 |

1.04 |

1.04 |

1.05 |

1.04 |

1.02 |

1.03 |

1.03 |

1.03 |

Alberta |

1.00 |

1.00 |

1.01 |

1.02 |

1.03 |

0.97 |

0.98 |

0.98 |

0.92 |

0.95 |

0.97 |

1.04 |

Saskatchewan |

1.00 |

1.00 |

1.02 |

1.02 |

1.02 |

1.01 |

1.02 |

1.01 |

1.01 |

1.02 |

1.02 |

1.03 |

Manitoba |

1.00 |

1.00 |

1.00 |

1.02 |

1.02 |

1.03 |

1.04 |

1.06 |

1.07 |

1.08 |

1.08 |

1.10 |

Ontario |

1.00 |

1.00 |

1.01 |

1.01 |

1.02 |

1.03 |

1.04 |

1.06 |

1.06 |

1.07 |

1.07 |

1.08 |

New Brunswick |

1.00 |

0.99 |

0.98 |

0.94 |

0.97 |

0.98 |

0.98 |

0.98 |

0.98 |

0.99 |

0.93 |

0.92 |

Nova Scotia |

1.00 |

1.00 |

0.96 |

0.93 |

0.95 |

0.94 |

0.97 |

0.96 |

0.96 |

0.97 |

0.97 |

0.98 |

Prince Edward Island |

1.00 |

1.00 |

1.02 |

1.03 |

1.03 |

0.98 |

0.94 |

0.94 |

0.94 |

0.95 |

0.95 |

0.95 |

Newfoundland and Labrador |

1.00 |

1.00 |

1.01 |

1.03 |

1.04 |

1.05 |

1.04 |

1.03 |

1.05 |

1.06 |

1.07 |

1.07 |

Total* |

1.00 |

1.00 |

1.01 |

1.01 |

1.02 |

1.02 |

1.03 |

1.04 |

1.04 |

1.05 |

1.05 |

1.07 |

(b) Multi-source generic medicines

Expenditure share: 17.2%

Prescription share: 72.9%

| 2009/10 | 2010/11 | 2011/12 | 2012/13 | 2013/14 | 2014/15 | 2015/16 | 2016/17 | 2017/18 | 2018/19 | 2019/20 | 2020/21 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

British Columbia |

1.00 |

0.95 |

0.80 |

0.70 |

0.54 |

0.52 |

0.51 |

0.50 |

0.47 |

0.38 |

0.38 |

0.38 |

Alberta |

1.00 |

0.96 |

0.96 |

0.78 |

0.50 |

0.47 |

0.46 |

0.44 |

0.40 |

0.33 |

0.32 |

0.32 |

Saskatchewan |

1.00 |

0.99 |

0.88 |

0.75 |

0.67 |

0.63 |

0.54 |

0.52 |

0.49 |

0.41 |

0.40 |

0.40 |

Manitoba |

1.00 |

0.99 |

0.96 |

0.84 |

0.68 |

0.61 |

0.58 |

0.57 |

0.55 |

0.45 |

0.45 |

0.44 |

Ontario |

1.00 |

0.73 |

0.62 |

0.62 |

0.58 |

0.55 |

0.53 |

0.52 |

0.49 |

0.39 |

0.39 |

0.39 |

New Brunswick |

1.00 |

1.01 |

1.00 |

0.78 |

0.52 |

0.48 |

0.46 |

0.45 |

0.44 |

0.34 |

0.34 |

0.34 |

Nova Scotia |

1.00 |

1.00 |

0.92 |

0.76 |

0.63 |

0.56 |

0.49 |

0.48 |

0.47 |

0.36 |

0.36 |

0.36 |

Prince Edward Island |

1.00 |

1.00 |

1.00 |

0.80 |

0.57 |

0.46 |

0.43 |

0.42 |

0.41 |

0.32 |

0.32 |

0.32 |

Newfoundland and Labrador |

1.00 |

1.00 |

1.01 |

0.82 |

0.58 |

0.52 |

0.49 |

0.49 |

0.48 |

0.38 |

0.38 |

0.39 |

Total* |

1.00 |

0.96 |

0.86 |

0.77 |

0.64 |

0.60 |

0.58 |

0.58 |

0.55 |

0.44 |

0.44 |

0.44 |

(c) Single-source non-patented medicines

Expenditure share: 8.6%

Prescription share: 2.5%

| 2009/10 | 2010/11 | 2011/12 | 2012/13 | 2013/14 | 2014/15 | 2015/16 | 2016/17 | 2017/18 | 2018/19 | 2019/20 | 2020/21 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

British Columbia |

1.00 |

1.06 |

1.11 |

1.14 |

1.18 |

1.22 |

1.27 |

1.31 |

1.34 |

1.39 |

1.45 |

1.48 |

Alberta |

1.00 |

1.02 |

1.04 |

1.06 |

1.08 |

1.04 |

1.05 |

1.08 |

1.20 |

1.24 |

1.30 |

1.31 |

Saskatchewan |

1.00 |

1.05 |

1.09 |

1.12 |

1.16 |

1.19 |

1.22 |

1.26 |

1.28 |

1.29 |

1.33 |

1.36 |

Manitoba |

1.00 |

1.04 |

1.09 |

1.12 |

1.16 |

1.21 |

1.26 |

1.29 |

1.31 |

1.33 |

1.36 |

1.39 |

Ontario |

1.00 |

1.01 |

1.02 |

1.05 |

1.07 |

1.10 |

1.13 |

1.16 |

1.20 |

1.23 |

1.26 |

1.27 |

New Brunswick |

1.00 |

1.03 |

1.06 |

1.10 |

1.12 |

1.15 |

1.19 |

1.22 |

1.24 |

1.26 |

1.24 |

1.22 |

Nova Scotia |

1.00 |

1.04 |

1.04 |

1.04 |

1.06 |

1.11 |

1.16 |

1.19 |

1.21 |

1.24 |

1.27 |

1.29 |

Prince Edward Island |

1.00 |

1.10 |

1.13 |

1.17 |

1.23 |

1.21 |

1.21 |

1.25 |

1.27 |

1.30 |

1.35 |

1.37 |

Newfoundland and Labrador |

1.00 |

1.04 |

1.06 |

1.07 |

1.10 |

1.12 |

1.13 |

1.20 |

1.23 |

1.26 |

1.30 |

1.33 |

Total* |

1.00 |

1.04 |

1.07 |

1.10 |

1.13 |

1.15 |

1.18 |

1.18 |

1.23 |

1.25 |

1.29 |

1.31 |

Note: This analysis only includes data for beneficiaries that met their deductible and received public reimbursement.

Yukon is not reported due to data limitations. National results for 2020/21 do not include the Non-Insured Health Benefits (NIHB) program.

The findings are a cost-weighted average of changes in the reimbursed unit costs for individual medicines. The analysis was limited to data for oral solid formulations. The remaining share of prescriptions and expenditures includes devices, compounded drugs, and other products that are reimbursed by public drug plans but do not have a Health Canada assigned Drug Identification Number (DIN).

* Total results for the drugs plans captured in this figure.

Data source: National Prescription Drug Utilization Information System Database, Canadian Institute for Health Information.

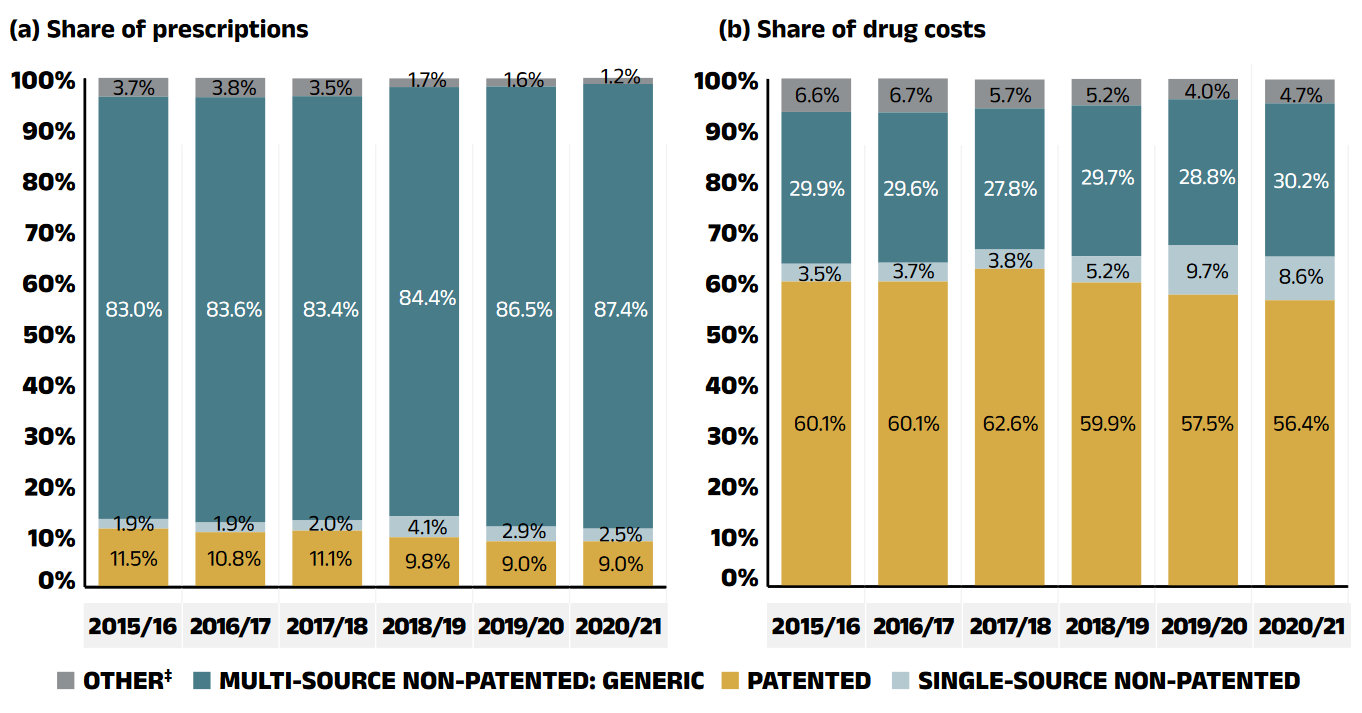

Substitution Effect

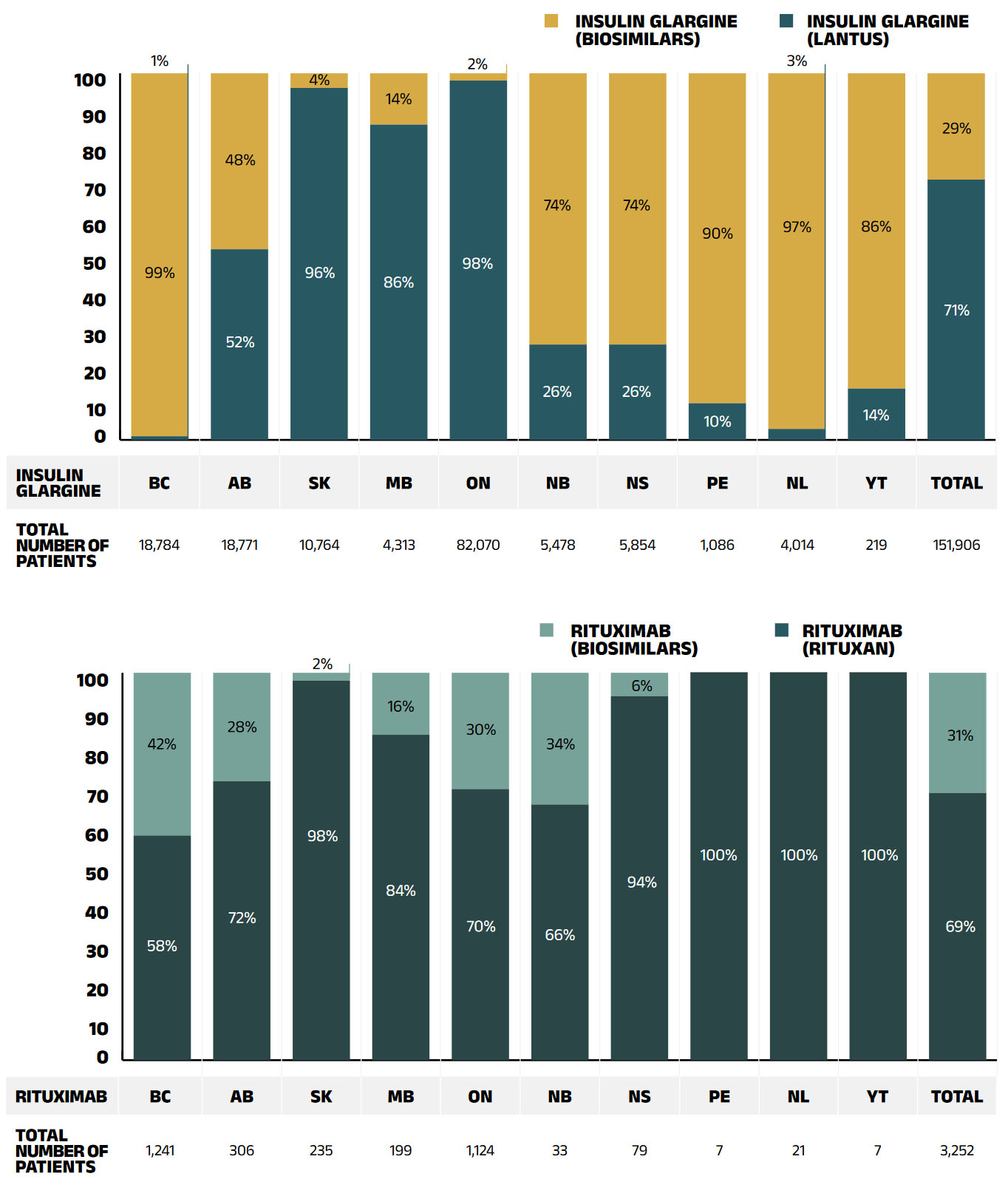

Shifts from brand-name to generic or biosimilar medicines pulled overall drug costs down by 1.4% in 2020/21, translating to savings of $129 million for the NPDUIS public plans. The top three generic contributors to the substitution effect, which included an adrenergic inhalant (fluticasone/salmeterol), and an immunomodulator (fingolimod) and a drug used in addictive disorders (buprenorphine/naloxone), offered merely -0.3% in savings. Biosimilars contributed more to the substitution effect than generic medicines in 2020/21: three immunosuppressants and one insulin were responsible for half of the savings from substitution: Inflectra/Renflexis (-0.5%), Brenzys/Erelzi (-0.1%), Basaglar (-0.04%) and Truxima/Riximyo/Ruxience (-0.03%).

The share of prescriptions for multi-source non-patented medicines in public plans increased to 87.4% in 2020/21, a significant rise over 83.0% in 2015/16, while their corresponding share of total drug costs changed little over the same time period, from 29.9% to 30.2%. This six-year trend reflects the implementation of generic pricing policies, as well as the genericization of a number of commonly used medicines that lost patent protection in recent years. Multi-source generics alone accounted for 72.9% of prescriptions and 17.2% (as shown in Figure 1.5) of drug costs on 2020/21.

Patented medicines accounted for a decreasing share of prescriptions in 2020/21, dropping from 11.5% to 9.0% since 2015/16. Their share of total public plan drug costs also fell slightly to 56.4% as a result of changes to the patent status of a few top-selling medicines. Despite the loss of patent for a few significant medicines, this segment has held steady around 60% as a result of the increased use of high-cost drugs such as biologics and oral oncology medicines and the introduction of new high-use drugs such as antidiabetics.

Figure 2.4 reports the 2015/16 to 2020/21 trends in market shares by market segment: patented, multi-source non-patented, and single-source non-patented medicines.

Figure description

This figure shows two complementary stacked column graphs. Graph (a) shows the share of prescriptions by market segment from 2015/16 to 2020/21 for all NPDUIS public drug plans. Graph (b) shows the share of drug costs by market segment for the same period.

(a) Share of prescriptions

| Market segment | 2015/16 | 2016/17 | 2017/18 | 2018/19 | 2019/20 | 2020/21 |

|---|---|---|---|---|---|---|

Patented |

11.5% |

10.8% |

11.1% |

9.8% |

9.0% |

9.0% |

Single-source non-patented |

1.9% |

1.9% |

2.0% |

4.1% |

2.9% |

2.5% |

Multi-source generic |

83.0% |

83.6% |

83.4% |

84.4% |

86.5% |

87.4% |

Other‡ |

3.7% |

3.8% |

3.5% |

1.7% |

1.6% |

1.2% |

(b) Share of drug costs

| Market segment | 2015/16 | 2016/17 | 2017/18 | 2018/19 | 2019/20 | 2020/21 |

|---|---|---|---|---|---|---|

Patented |

60.1% |

60.1% |

62.6% |

59.9% |

57.5% |

56.4% |

Single-source non-patented |

3.5% |

3.7% |

3.8% |

5.2% |

9.7% |

8.6% |

Multi-source generic |

29.9% |

29.6% |

27.8% |

29.7% |

28.8% |

30.2% |

Other‡ |

6.6% |

6.7% |

5.7% |

5.2% |

4.0% |

4.7% |

Note: This analysis only includes data for beneficiaries that met their deductible and received public reimbursement.

* British Columbia, Alberta, Saskatchewan, Manitoba, Ontario, New Brunswick, Nova Scotia, Prince Edward Island, Newfoundland and Labrador, Yukon, and the Non-Insured Health Benefits (NIHB) Program. Results for 2020/21 do not include the NIHB program.

‡ This market segment includes devices, compounded drugs, and other products that are reimbursed by public drug plans but do not have a Health Canada assigned Drug Identification Number (DIN).

Data source: National Prescription Drug Utilization Information System Database, Canadian Institute for Health Information.

Brief Insights: Biosimilars

In April 2016, the pCPA issued the First Principles for Subsequent Entry Biologics to guide negotiations and inform expectations for biologics and biosimilars. This was followed by the creation of the Biologics Policy Directions in September 2018 to further guide and define the process by which biologic and biosimilar products are negotiated and considered for reimbursement by Canada’s public drug plans.