Meds Entry Watch 2018

ISSN 2560-6204

Catalogue number: H79-12E-PDF

January 2020

PDF - 899 KB

Previous edition

Full list of analytical studies

New Medicines Approved in 2018

New Medicines Approved in 2017

New Medicines Approved in 2016

Table of Contents

- Executive Summary

- Introduction

- Methods

- Limitations

- A. Trends in New Medicine Approvals, 2009-2017

- B. New Medicine Approvals, 2017

- C. New Medicine Approvals, 2018

- D. Spotlight on Canada

- References

- Appendix I: Change in sales of existing medicines with new or extended indications approved by Health Canada in 2017

Acknowledgements

This report was prepared by the Patented Medicine Prices Review Board (PMPRB) as part of the National Prescription Drug Utilization Information System (NPDUIS) initiative.

The PMPRB wishes to acknowledge and thank the members of the NPDUIS Advisory Committee for their expert oversight and guidance in the preparation of this report. Please note that the statements, findings, and conclusions do not necessarily reflect those of the members or their organizations.

Appreciation goes to Blake Wladyka for leading this analytical project, as well as to Tanya Potashnik and Jeffrey Menzies for their oversight in the development of the report. The PMPRB also wishes to acknowledge the contribution of the analytical staff Jared Berger, Patrick McConnell, and Lokanadha Cheruvu; and the contribution of the editorial staff Carol McKinley, Sarah Parker, and Shirin Paynter.

Disclaimer

NPDUIS operates independently of the regulatory activities of the Board of the PMPRB. The research priorities, data, statements, and opinions expressed or reflected in NPDUIS reports do not represent the position of the PMPRB with respect to any regulatory matter. NPDUIS reports do not contain information that is confidential or privileged under sections 87 and 88 of the Patent Act, and the mention of a medicine in a NPDUIS report is not and should not be understood as an admission or denial that the medicine is subject to filings under sections 80, 81, or 82 of the Patent Act or that its price is or is not excessive under section 85 of the Patent Act.

Although this information is based in part on data provided under license from the IQVIA MIDAS® Database, the statements, findings, conclusions, views, and opinions expressed in this report are exclusively those of the PMPRB and are not attributable to IQVIA.

Contact Information

Patented Medicine Prices Review Board

Standard Life Centre

Box L40

333 Laurier Avenue West Suite 1400

Ottawa, ON K1P 1C1

Tel.: 1-877-861-2350

TTY 613-288-9654

Email: PMPRB.Information-Renseignements.CEPMB@pmprb-cepmb.gc.ca

Executive Summary

This is the fourth edition of the PMPRB’s Meds Entry Watch report, which explores the market entry of new medicines in Canada and other countries. Building on the retrospective analysis of trends since 2009, this report focuses on medicines that received first-time market approval through the US Food and Drug Administration (FDA), the European Medicines Agency (EMA), and/or Health Canada in 2017 and 2018, and analyzes their uptake, pricing, sales, and availability as of the last quarter of 2018 (Q4-2018). This edition includes a new Canadian section with information on medicines that received their first Health Canada approval in 2017, as well as those that were approved for new indications.

This publication informs decision makers, researchers, and patients of the evolving market dynamics of emerging therapies in Canadian and international pharmaceutical markets.

The IQVIA MIDAS® Database was the primary source for the sales and list prices of new medicines in Canadian and international markets, as well as for the quantity sold.

International markets examined include the Organisation for Economic Co-operation and Development (OECD) members, with a focus on the seven countries the PMPRB currently considers in reviewing the prices of patented medicines (PMPRB7): France, Germany, Italy, Sweden, Switzerland, the United Kingdom (UK), and the United States (US).

Key Findings

A) Trends in New Medicine Approvals, 2009 to 2017

Although the market impact of new medicine approvals has varied from year to year since 2009, the landscape has been characterized by a continued rise in the number of specialized treatments.

- Medicines approved since 2009 accounted for over one third of brand-name medicine sales in Canada and the PMPRB7 by Q4-2018.

- From 2009 to 2017, slightly less than half (48%) of all new medicines had sales in Canada, ahead of the OECD median (40%) but behind most PMPRB7 countries, many of which have lower average patented medicine prices.

- New medicines with Canadian sales from 2009 to 2017 accounted for 94% of all new medicine sales in the OECD by Q4-2018, indicating that the higher-selling medicines were among those approved and sold in Canada.

- Orphan medicines are now dominating the market, accounting for 46% of new approvals in 2017 and 59% in 2018, a significant increase from the 33% average share between 2009 and 2014.

- Approximately 30% of the new medicine approvals in 2017 and 2018 were for the treatment of cancer, over half of which were orphan oncology medicines with treatments costs exceeding $7,500 per 28-day cycle.

- The majority of non-oncology medicines approved in 2017 and 2018 were high-cost, with 36 of the 60 with available treatment costs exceeding $10,000 annually. These results represent a continued trend toward high-cost medicines, with lower-cost medicines accounting for a smaller share of new approvals in recent years.

B) 2017 New Medicine Approvals

More new medicines were approved in 2017 than in previous years, with a significant increase in the number of high-cost orphan and oncology medicines entering the market.

- 52 new medicines received market approval through the FDA, the EMA, and/or Health Canada in 2017, significantly more than in 2016 and far above the average annual rate of 35 medicines approved from 2009 to 2014.

- 46% of the 2017 new medicines received an orphan designation from the FDA and/or the EMA and 35% were biologic therapies.

- Many new medicines came with a high cost: 14 were oncology medicines with costs exceeding $5,000 per 28-day treatment and 20 were non-oncology medicines with annual costs exceeding $10,000.

Fewer medicines were approved in Canada than in the US and Europe in 2017, although Canada compared favourably to the OECD in terms of the corresponding share of sales.

- 27 of the 52 new medicines first approved in 2017 had market authorization in Canada by Q4-2018, compared to 49 approved by the FDA and 34 by the EMA.

- 18 of the 27 approved medicines recorded sales in Canada by the end of 2018, placing Canada sixth in the OECD and in line with the PMPRB7 countries for the number of new medicines with sales.

- Although these 18 medicines represent a relatively small portion of the total number of approvals in 2017, they accounted for 88% of total sales for new medicines in the OECD.

Antivirals and central nervous system medicines accounted for the majority of 2017 new medicine sales in the last quarter of 2018.

- Overall, sales for new medicines were highly concentrated, with antivirals to treat hepatitis C making up almost 30% of new medicine sales in Canada and the PMPRB7 in 2018. Central nervous system therapies and antineoplastics followed, with 20% and 15% of the market, respectively.

- Glecaprevir/pibrentasvir, an antiviral for hepatitis C, was the top-selling new medicine in Q4-2018, accounting for over 25% of international new medicine sales.

C) 2018 New Medicine Approvals

The relatively high rate of new medicine approvals in 2017 was sustained through 2018, as the number of new high-cost specialty therapies continued to rise.

- 51 new medicines received market approval through the FDA, the EMA, and/or Health Canada in 2018, of which 19 had approval in Canada by the third quarter of 2019.

- Nearly 60% (30) of the new medicines received an orphan designation from the FDA and/or the EMA.

- Oncology treatments continued to account for around one third of new approvals, and over a quarter of new medicines were biologic therapies.

- Based on preliminary results, 12 of the 14 oncology medicines with available treatment costs exceeded $5,000 per 28-day cycle.

D) Spotlight on Canada

A number of medicines received their first Canadian approval in 2017, though new indications approved for existing medicines had a greater impact on sales.

- 36 new-to-Canada medicines were approved for market in 2017, of which 25 had reported sales by Q4-2018, accounting for 1.6% of the total pharmaceutical market.

- The top-selling Canadian approvals from 2017 received their first international market authorization in the same year.

- New and extended indications for previously marketed medicines contributed $594 million to the $1.07 billion growth in pharmaceutical sales in Canada between 2017 and 2018.

The next edition of Meds Entry Watch will build on this analysis to provide further insight into the medicines introduced in 2018 and a preliminary look at those approved in 2019, as well as a retrospective review of trends in new medicines over the past five years.

Introduction

Meds Entry Watch is an annual PMPRB publication that explores the dynamics of new medicines entering Canadian and international markets, providing information on their availability, sales, and prices.

This report builds on the three previous editions to provide a broader retrospective analysis of medicines that have entered the market since 2009, and offers a detailed analysis of the new medicines approved in 2017 along with a preliminary examination of those approved in 2018. New medicines are identified for each year based on the date of their first market authorization through the US Food and Drug Administration (FDA), the European Medicines Agency (EMA), and/or Health Canada.

This edition also features a new section focused on medicines that received their first Canadian approval in 2017. In addition to reporting the prices of new medicines approved in Canada in comparison with international markets, this analysis monitors the sales of existing medicines that received approvals for new indications in the same year.

The report consists of four main parts: Part A provides an overview of longer-term trends from 2009 to 2017; Part B focuses on new medicines that received market approval in 2017; Part C presents a preliminary analysis of the new medicines approved in 2018; and Part D spotlights Health Canada approvals in 2017.

This publication informs decision makers, researchers, and patients of emerging therapies in Canadian and international pharmaceutical markets.

Methods

This report analyzes new medicines that received initial market approval through the FDA, the EMA, and/or Health Canada in 2017 and 2018. For the purpose of this study, new medicines were identified at the medicinal ingredient level. A new medicine was selected for analysis if it received first-time market authorization from any of these regulatory bodies during the calendar year, even if it was not yet listed for reimbursement or if there were no recorded sales in the available data. Using these criteria, 52 new medicines were identified for the 2017 analysis in Section B and 51 were identified for the preliminary analysis of 2018 medicines in Section C. The approval of these medicines in Canadian and international markets was assessed as of the end of 2018.

The selection of medicines featured in the analysis of the Canadian market in Section D differs from the previous sections. Medicines analyzed in Section D include new and previously marketed medicinal ingredients that received their first Canadian market authorization through Health Canada in 2017. This includes a number of the medicines in the 2017 analysis in Section B, but also encompasses additional medicines that may have received initial approval through the FDA or EMA in previous years and were approved for the Canadian market in 2017. Section D also reports on the sales of medicines previously marketed in Canada that received authorization for additional or extended indications in 2017.

International markets examined include the Organisation for Economic Co-operation and Development (OECD) members, with a focus on the seven countries the PMPRB currently considers in reviewing the prices of patented medicines (PMPRB7): France, Germany, Italy, Sweden, Switzerland, the United Kingdom (UK), and the United States (US).

The IQVIA MIDAS® Database (all rights reserved) was the main data source for the sales and list prices of new medicines in Canadian and international markets, as well as the number of units sold. MIDAS data reflects the national retail and hospital sectors of each country, including payers in all market segments (public, private, and out-of-pocket). Sales and volume data encompass all versions of a medicine available in a particular country, produced by any manufacturer in any strength and form. For more information on the MIDAS Database and other NPDUIS source materials, see the Reference Documents section of the Analytical Studies page on the PMPRB website.

Canadian prices were based on MIDAS data, if available; otherwise, they were taken from publicly available results of the Common Drug Review (CDR) or pan-Canadian Oncology Drug Review (pCODR) processes published by the Canadian Agency for Drugs and Technologies in Health (CADTH). Treatment costs were calculated using Canadian list prices where possible; if not, the foreign median price was used. Information on dosing regimens was taken from the product monographs published by Health Canada, or if not available, from the FDA or EMA. All medicines were reviewed as of Q3-2019, unless otherwise specified.

Prices and foreign-to-Canadian price ratios were reported for the highest-selling form and strength of each medicine in Canada, or in the PMPRB7 if no Canadian sales were available at the time of the analysis. The foreign-to-Canadian price ratios presented in this report are expressed as an index with the Canadian price set to a value of one and the international median reported relative to this value. For more details on how foreign-to-Canadian price ratios are calculated, see the Reference Documents section of the Analytical Studies page on the PMPRB website.

Prices and sales in foreign currencies were converted into Canadian dollars using the 12-month or 3-month average exchange rate for the year or quarter, respectively.

Historical results for the period from 2009 to 2014 were based on the methodology employed in the first issue of Meds Entry Watch, which identified new medicines based on the date of first recorded sales in the MIDAS Database. This change in methodology is not expected to have a meaningful impact on the overall results.

Limitations

New medicines reported in Sections B and C were selected for analysis based on their date of market approval by the FDA, the EMA, and/or Health Canada; however, some may have an earlier approval date in other international markets. Likewise, the medicines included in this analysis do not necessarily represent all of those introduced in 2017 and 2018, as other national regulatory bodies not examined in this report may have approved additional medicines. Nevertheless, this should have a very limited effect on the results, as the FDA and EMA are major regulatory bodies representing large international markets and have regulatory approaches similar to those in Canada.

This report reflects the initial market penetration of these new medicines, and their availability and uptake are expected to increase in subsequent years. The availability of a new medicine in a given country at any point in time is influenced by a variety of factors including the manufacturer’s decision to launch, as well as the timing of that decision; the regulatory approval process in place; and the existing market dynamics.

Market approval through the EMA does not necessarily mean that the medicine is available in any given European country. Likewise, medicines approved through the FDA or Health Canada may not necessarily be reimbursed and/or have any recorded sales.

Some medicines with sales may not be reported in the IQVIA MIDAS® Database, and thus, the sales of new medicines in any given country may be slightly under-reported. However, as the effect is expected to be relatively consistent across all markets, this should have only a minimal impact on the overall findings.

Canadian and international sales and prices are based on manufacturer list prices as reported in the MIDAS Database, and do not capture price rebates, managed entry agreements (also known as product listing agreements), or patient access schemes. The methodology used by MIDAS for estimating medicine prices varies by country, depending on data availability, and may include assumed regulated margins and/or markups.

Publicly available prices from the Canadian Agency for Drugs and Technologies in Health (CADTH) are based on the manufacturers’ submitted prices, which may differ upon market entry.

Aggregated international sales and pricing data are heavily skewed towards the United States due to its relatively large population, and as a result, the ranking of medicines by international sales generally reflects the order of sales in the US.

The assessment of medicine availability in Canada does not consider non-marketed medicines available through programs that authorize the sale of medicines in exceptional circumstances, such as the Special Access Programme in Canada (SAP).

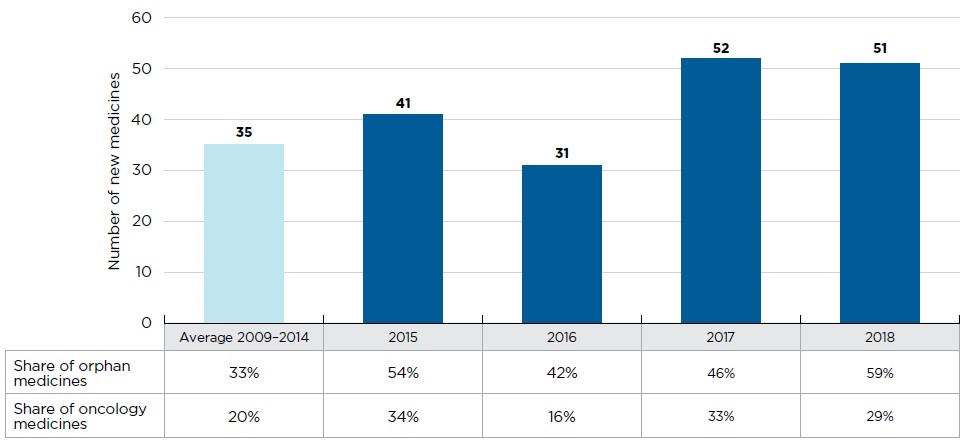

A. Trends in New Medicine Approvals, 2009–2017

A greater number of new medicines have been approved in recent years, including a rising share of new specialty treatments. Medicines first approved between 2009 and 2017 accounted for over one third of all brand-name sales by the end of 2018. Nearly half of these had recorded Canadian sales by Q4-2018, placing Canada 10th in the OECD and behind most PMPRB7 countries. Despite this, Canada ranked fourth in terms of the share of total new medicine sales, which suggests that the top-selling medicines were among those approved.

In 2017, 52 new medicines received first-time market approval through the FDA, the EMA, and/or Health Canada, a considerable increase from the 31 approved the year before and the annual average of 35 reported from 2009 to 2014 (Figure A1). Almost half (24) of these medicines received an orphan designation from the FDA and/or EMA, representing a sustained rise over the 33% average share from 2009 to 2014.

An additional 51 new medicines were approved in 2018, of which nearly 60% (30) received an orphan designation and close to one third (15) were approved to treat cancer.

New medicines continued to be concentrated in a few therapeutic areas, mostly notably among antineoplastic agents and antivirals. The number of approvals increased in 2017 for central nervous system medicines, ophthalmologicals, and non-steroidal products for inflammatory skin disorders. Additionally, a number of new migraine treatments were approved in 2018.

Figure description

This bar graph depicts the number of new medicines launched in Canada and the PMPRB7 from 2009 to 2018. The number of medicines introduced between 2009 and 2014 is averaged from a cumulative total of 212. A table shows the share of orphan and oncology medicines for each annual total.

| Average 2009‒2014 | 2015 | 2016 | 2017 | 2018 | |

|---|---|---|---|---|---|

| Number of new medicines | 35 | 41 | 31 | 52 | 51 |

| Share of orphan medicines | 33% | 54% | 42% | 46% | 59% |

| Share of oncology medicines | 20% | 34% | 16% | 33% | 29% |

Note: New medicines reported between 2009 and 2014 were identified based on the date of first recorded sales, while those reported for 2015 onward were determined based on the date of first-time market approval by the US Food and Drug Administration, the European Medicines Agency, and/or Health Canada.

* France, Germany, Italy, Sweden, Switzerland, the United Kingdom, and the United States.

Data source: IQVIA MIDAS® Database, 2009 to 2014 (all rights reserved); US Food and Drug Administration, European Medicines Agency, and Health Canada databases.

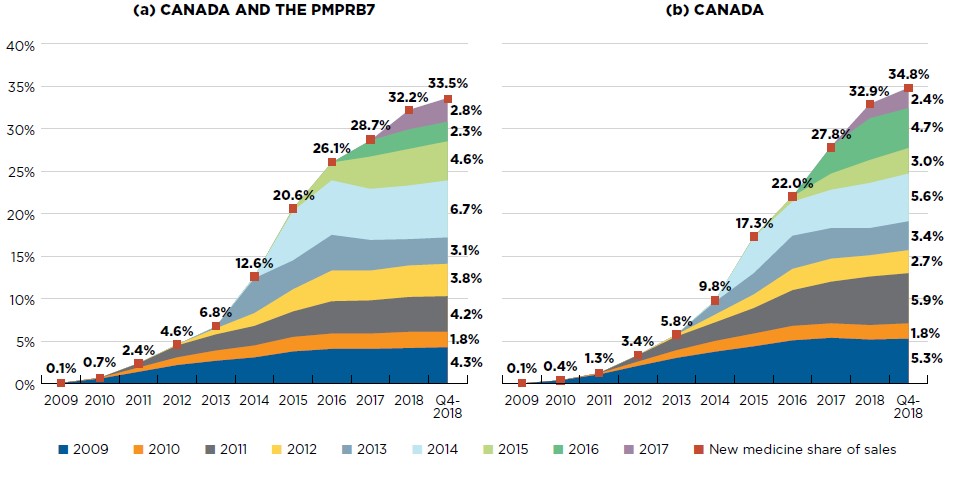

Following a period of steep year-over-year uptake in the sales of new medicines, recent entrants have held a relatively modest share of the market. Despite a significant number of approvals in 2017, these new medicines accounted for 2.8% of all brand-name pharmaceutical sales by Q4-2018. New medicines approved between 2009 and 2017 collectively made up one third of the total market in Canada and comparator countries (Figure A2).

Notably, new medicines accounted for a slightly larger share of the Canadian market than their corresponding share of the market in Canada and the PMPRB7. Driving this difference was a marked difference between the influence of the 2016 new medicines in Canada and internationally; whereas the 2016 medicines held only a 2.3% share across the PMPRB7 by Q4-2018, they represented 4.7% of all sales in Canada. This may be due, in part, to a greater impact from the hepatitis C treatment Epclusa (sofosbuvir/velpatasvir), which accounted for 0.6% of total pharmaceutical sales in the PMPRB7 and 2.2% of Canadian sales in Q4-2018.

In any given year, the impact of new medicines on pharmaceutical sales depends on their number, therapeutic relevance, and treatment costs. For example, the entry of new direct-acting antivirals (DAAs) for hepatitis C in 2014 continues to have a high impact on sales, accounting for one fifth of the new medicine share of the brand-name pharmaceutical market by Q4-2018.

Figure description

This figure consists of two area graphs depicting the new medicine cumulative share of total brand-name medicine sales by year of approval. It tracks the percentage of new medicines in yearly sales up to the fourth quarter of 2018. New medicine share of sales for each year are also marked. The first graph is for both Canada and the seven PMPRB comparator countries and the second is for Canada alone.

(a) Canada and PMPRB7

| Year of approval | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | Q4-2018 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 2009 | 0.1% | 0.6% | 1.4% | 2.2% | 2.7% | 3.1% | 3.8% | 4.1% | 4.1% | 4.2% | 4.3% |

| 2010 | 0.1% | 0.5% | 0.9% | 1.2% | 1.4% | 1.7% | 1.8% | 1.8% | 1.9% | 1.8% | |

| 2011 | 0.5% | 1.4% | 1.9% | 2.3% | 3.0% | 3.8% | 3.9% | 4.1% | 4.2% | ||

| 2012 | 0.1% | 0.7% | 1.5% | 2.6% | 3.6% | 3.5% | 3.7% | 3.8% | |||

| 2013 | 0.2% | 4.1% | 3.4% | 4.2% | 3.6% | 3.1% | 3.1% | ||||

| 2014 | 0.2% | 5.8% | 6.4% | 6.0% | 6.3% | 6.7% | |||||

| 2015 | 0.3% | 2.1% | 3.8% | 4.3% | 4.6% | ||||||

| 2016 | 1.9% | 2.3% | 2.3% | ||||||||

| 2017 | 2.3% | 2.8% | |||||||||

| New medicine share of sales | 0.1% | 0.7% | 2.4% | 4.6% | 6.8% | 12.6% | 20.6% | 26.1% | 28.7% | 32.2% | 33.5% |

(b) Canada

| Year of approval | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | Q4-2018 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 2009 | 0.1% | 0.4% | 1.1% | 2.1% | 3.0% | 3.8% | 4.4% | 5.1% | 5.4% | 5.2% | 5.3% |

| 2010 | <0.1% | 0.1% | 0.5% | 0.9% | 1.3% | 1.5% | 1.7% | 1.7% | 1.7% | 1.8% | |

| 2011 | <0.1% | 0.8% | 1.6% | 2.2% | 3.0% | 4.2% | 4.9% | 5.7% | 5.9% | ||

| 2012 | <0.1% | 0.2% | 0.9% | 1.6% | 2.5% | 2.7% | 2.5% | 2.7% | |||

| 2013 | <0.1% | 1.5% | 2.5% | 3.9% | 3.6% | 3.2% | 3.4% | ||||

| 2014 | 0.2% | 4.2% | 4.0% | 4.5% | 5.3% | 5.6% | |||||

| 2015 | 0.1% | 0.6% | 1.9% | 2.7% | 3.0% | ||||||

| 2016 | 3.2% | 4.9% | 4.7% | ||||||||

| 2017 | 1.7% | 2.4% | |||||||||

| New medicine share of sales | 0.1% | 0.4% | 1.3% | 3.4% | 5.8% | 9.8% | 17.3% | 22.0% | 27.8% | 32.9% | 34.8% |

* New medicines introduced between 2009 and 2014 were identified based on the date of first reported sales, while those reported for 2015 onward were determined based on the date of first-time market approval by the US Food and Drug Administration, the European Medicines Agency, and/or Health Canada.

† France, Germany, Italy, Sweden, Switzerland, the United Kingdom, and the United States.

Data source: IQVIA MIDAS® Database, 2009 to 2018. All rights reserved.

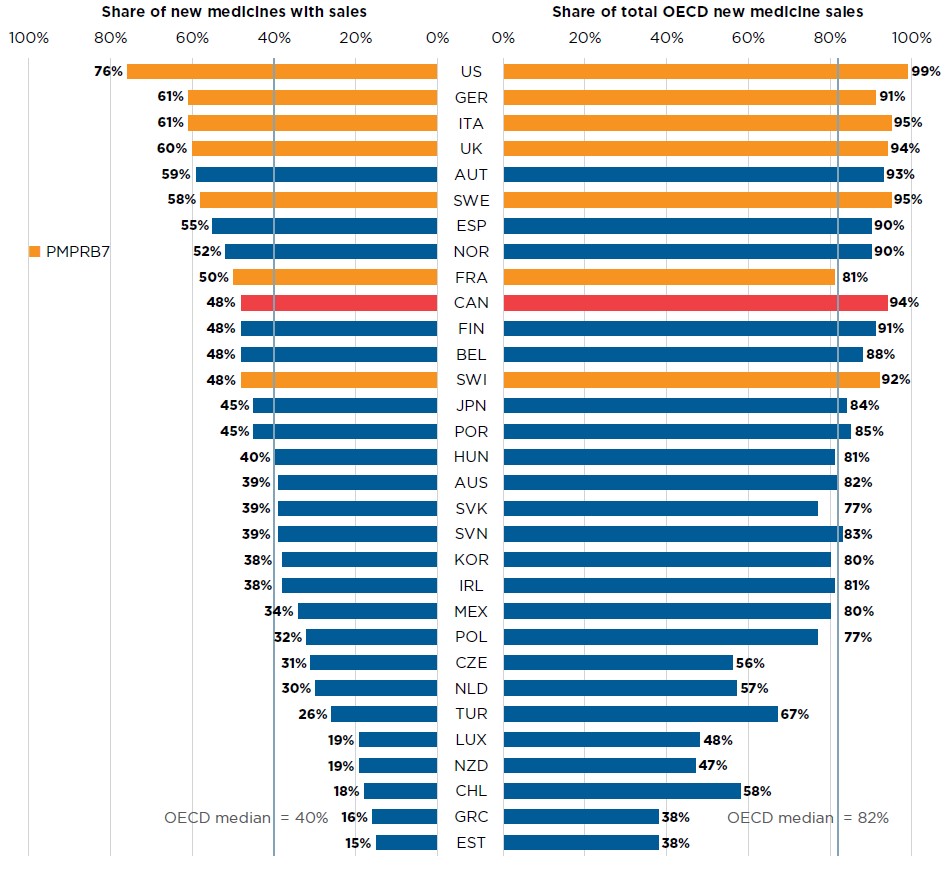

Of the 336 medicines approved in Canada and the PMPRB7 from 2009 to 2017, 48% had recorded sales in Canada by Q4-2018 (Figure A3). While this represents a greater share than the OECD median of 40%, it ranks below most PMPRB7 countries, many of which have lower average list prices for patented medicines (PMPRB). The new medicines sold in Canada accounted for 94% of the OECD sales for all new medicines analyzed, representing the fourth highest share in the OECD, well above the median of 82%. This suggests that although fewer new medicines were approved in Canada, the higher-selling new medicines were among those sold, which may have been partially influenced by Canada’s proximity to the US market.

Figure description

This is a split bar graph. For each country in the Organisation for Economic Co-operation and Development, one side of the graph gives the market share of the new medicines launched in Canada and its seven PMPRB comparator countries from 2009 to 2017. The other side gives the respective share of the Organisation for Economic Co-operation and Development sales in the fourth quarter of 2018. The Organisation for Economic Co-operation and Development median is shown for each side of the graph.

| Country | Share of new medicines with sales | Share of total Organisation for Economic Co-operation and Development new medicine sales |

|---|---|---|

| United States | 76% | 99% |

| Germany | 61% | 91% |

| Italy | 61% | 95% |

| United Kingdom | 60% | 94% |

| Austria | 59% | 93% |

| Sweden | 58% | 95% |

| Spain | 55% | 90% |

| Norway | 52% | 90% |

| France | 50% | 81% |

| Canada | 48% | 94% |

| Finland | 48% | 91% |

| Belgium | 48% | 88% |

| Switzerland | 48% | 92% |

| Japan | 45% | 84% |

| Portugal | 45% | 85% |

| Hungary | 40% | 81% |

| Australia | 39% | 82% |

| Slovakia | 39% | 77% |

| Slovenia | 39% | 83% |

| South Korea | 38% | 80% |

| Ireland | 38% | 81% |

| Mexico | 34% | 80% |

| Poland | 32% | 77% |

| Czech Republic | 31% | 56% |

| Netherlands | 30% | 57% |

| Turkey | 26% | 67% |

| Luxembourg | 19% | 48% |

| New Zealand | 19% | 47% |

| Chile | 18% | 58% |

| Greece | 16% | 38% |

| Estonia | 15% | 38% |

| OECD median | 40% | 82% |

Note: Sales are based on manufacturer list prices and include sales for all OECD countries.

* New medicines introduced between 2009 and 2014 were identified based on the date of first reported sales, while those reported for 2015 onward were determined based on the date of first-time market approval by the US Food and Drug Administration, the European Medicines Agency, and/or Health Canada.

† France, Germany, Italy, Sweden, Switzerland, the United Kingdom, and the United States.

Data source: IQVIA MIDAS® Database, 2018. All rights reserved.

B: New Medicine Approvals, 2017

A greater than average number of new medicines were approved in Canada, Europe, and the US in 2017, nearly half of which had an orphan designation. While relatively few of these medicines had sales in Canada by the end of 2018, those sold accounted for the majority of all new medicine sales.

Fifty-two new medicines were approved internationally in 2017, representing a considerable increase from the 31 medicines approved the year before. Nearly two thirds of these new medicines were high-cost, coming with treatment costs over $10,000 per year, or $5,000 per 28-day cycle for oncology medicines. Five new non-oncology medicines were identified as expensive drugs for rare diseases (EDRDs)—orphan-designated therapies exceeding $100,000 in annual treatment costs—while ten new oncology medicines qualified as EDRDs at over $7,500 per 28-day cycle.

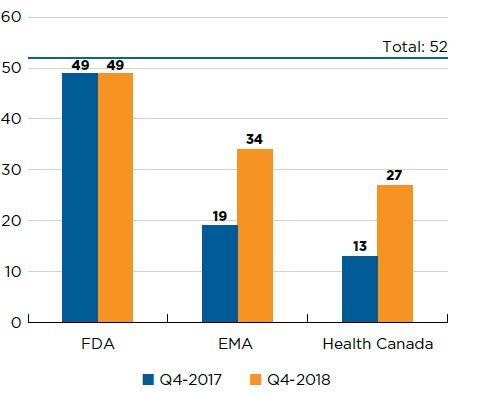

By the end of 2018, just over half (27) of the 2017 new medicines had been approved in Canada. Both the FDA and the EMA, which represent two of the largest international markets, approved more new medicines than Canada at 49 and 34, respectively (Figure B1).

Figure description

This is a bar graph with the number of 2017 new medicines approved by Health Canada, the European Medicines Agency, and the Food and Drug Administration in the United States as of the fourth quarter of 2017 and as of the fourth quarter of 2018. The total number of new medicines in 2017 was 52.

| US Food and Drug Administration | European Medicines Agency | Health Canada | |

|---|---|---|---|

| Q4-2017 | 49 | 19 | 13 |

| Q4-2018 | 49 | 34 | 27 |

Data source: US Food and Drug Administration (FDA), European Medicines Agency (EMA), and Health Canada databases.

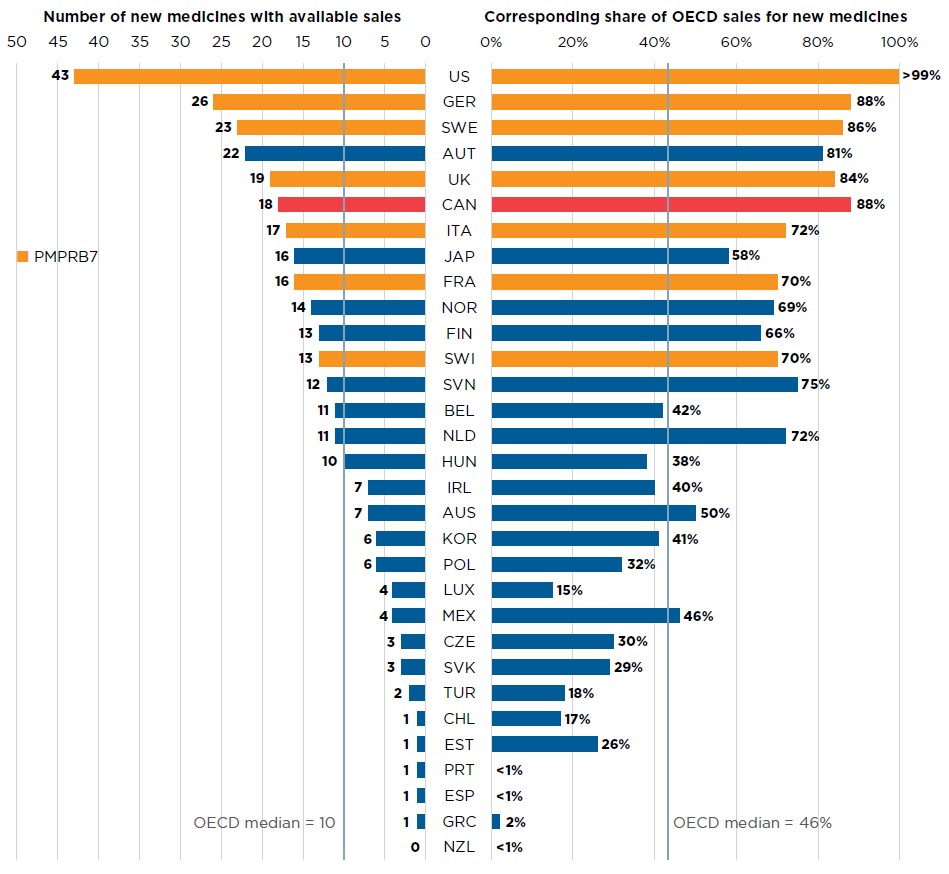

Of the 27 medicines approved in Canada, 18 had sales data available in MIDAS by Q4-2018. This placed Canada sixth in the OECD in terms of the number of new medicines sold and third in terms of the corresponding OECD sales of these new medicines at 88%, marking an increase over 2016 results. The US market, which ranked first among all OECD countries, recorded sales for 43 of the medicines approved in 2017, representing over 99% of OECD sales.

These results reflect the initial market penetration, and the availability and uptake in sales for these new medicines are expected to increase in subsequent years.

Figure description

This is a split bar graph showing the number of new medicines approved and with available sales as of the fourth quarter of 2018 and the corresponding share of 2018 fourth quarter sales in 31 Organisation for Economic Co-operation and Development countries. A median is given for each side of the graph.

| Country | Number of new medicines with sales | Share of total Organisation for Economic Co-operation and Development sales for new medicines |

|---|---|---|

| United States | 43 | >99% |

| Germany | 26 | 88% |

| Sweden | 23 | 86% |

| Austria | 22 | 81% |

| United Kingdom | 19 | 84% |

| Canada | 18 | 88% |

| Italy | 17 | 72% |

| Japan | 16 | 58% |

| France | 16 | 70% |

| Norway | 14 | 69% |

| Finland | 13 | 66% |

| Switzerland | 13 | 70% |

| Slovenia | 12 | 75% |

| Belgium | 11 | 42% |

| Netherlands | 11 | 72% |

| Hungary | 10 | 38% |

| Ireland | 7 | 40% |

| Australia | 7 | 50% |

| South Korea | 6 | 41% |

| Poland | 6 | 32% |

| Luxembourg | 4 | 15% |

| Mexico | 4 | 46% |

| Czech Republic | 3 | 30% |

| Slovakia | 3 | 29% |

| Turkey | 2 | 18% |

| Chile | 1 | 17% |

| Estonia | 1 | 26% |

| Portugal | 1 | <1% |

| Spain | 1 | <1% |

| Greece | 1 | 2% |

| New Zealand | 0 | <1% |

| OECD median | 10 | 46% |

Note: Based on medicines that received market approval through the US Food and Drug Administration (FDA), the European Medicines Agency (EMA), and/or Health Canada in 2017 with recorded sales data as of Q4-2018.

Sales are based on manufacturer list prices and include sales for the selected new medicines in all OECD countries.

Data source: IQVIA MIDAS® Database, 2018 (all rights reserved); US Food and Drug Administration, European Medicines Agency, and Health Canada databases.

Although new medicines approved in Canada and the PMPRB7 in 2017 covered a wide range of therapeutic classes, their sales were highly concentrated. The top four ATC classes by sales represented half of the 2017 new medicines and over 80% of all new medicine sales in Canada and the PMPRB7 by Q4-2018. Two medicines, glecaprevir/pibrentasvir and ocrelizumab, together accounted for 45% of sales and represented the top two therapeutic classes, antivirals and central nervous system drugs, respectively. Antineoplastics ranked as the third top-selling ATC class, with oncology treatments accounting for 12 of the 52 new medicines and 15% of sales.

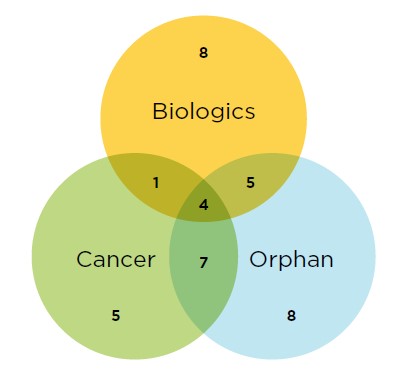

As illustrated, a significant number of new medicines fell into multiple specialty categories. Most notably, 11 of the new oncology medicines and nine of the new biologic therapies were also orphan-designated, four of which belonged to all three groups. In total, 46% (24) of the 2017 new medicines received an orphan designation from the FDA and/or the EMA. The share of oncology medicines rose to 33%, and 35% of new medicines were biologics.

Figure description

Venn diagram

This is a Venn diagram illustrating the overlap between orphan, biologic, and oncology medicines among the 2017 new medicines: 18 medicines were biologic, 24 had an orphan designation, and 17 were cancer medicines. Nine were both biologic and orphan, five were both biologic and oncological, 11 were both orphan and oncological, and four were biologic cancer medicines that also received an orphan designation.

Data source: US Food and Drug Administration, European Medicines Agency, and Health Canada databases.

Table B1 lists the new medicines approved in 2017. For each medicine, the country with the first reported sales is given, along with the availability in Canada, the share of sales in Q4-2018, and the prices and corresponding treatment costs.Footnote 1 Prices are reported for the highest-selling form and strength of each medicine at the time of the analysis.

Table B1 New medicines approved in 2017, availability, share of sales, prices, and treatment costs, ranked by therapeutic class share of sales, Q4-2018

| Rank | Therapeutic class* | Medicine (trade name, form, strength, volume)† | Availability | Share of new medicine sales (%) | No. of countries with sales | Canadian price§ (CAD) | PMPRB7‡ price (CAD) | Treatment cost** | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| First sale in Canada or PMPRB7 | First sale in Canada | Medicine | Therapeutic class | Min | Median | Max | Treatment cost (CAD) | Annual / Course | ||||||

| 1 | J5-Antivirals | Glecaprevir, pibrentasvir (Maviret, film-ctd tab, 100 mg + 40 mg) | US | Aug-17 | Sept-17 | 25.7% | 29.0% | 8 | 236 | 187 | 230 | 251 | 79,240 | 16-week treatment |

| 2 | Voxilaprevir (Vosevi, film-ctd tab, 400 mg + 100 mg + 100 mg) | US | Jul-17 | Sept-17 | 2.6% | 7 | 699 | 684 | 854 | 1,020 | 58,752 | 12-week treatment | ||

| 3 | Letermovir (Prevymis, film-ctd tab, 480 mg)O | US/CAN | Dec-17 | Dec-17 | 0.7% | 4 | 245 | 452 | 477 | 501 | 24,450 | 100-day treatment | ||

| 4 | N7-Other central nervous system drugs | Ocrelizumab (Ocrevus, infus. vial/bottle, 30 mg/ml, 10 ml)B | US | Sept-17 | Sept-17 | 17.0% | 20.1% | 8 | 8,446 | 7,124 | 8,955 | 18,885 | 33,786 | Annual |

| 5 | Deutetrabenazine (Austedo, ctd tab, 12 mg)O | US | Jun-17 | – | 1.7% | 1 | – | 108 | 108 | 108 | 19,760 / 158,100 | Annual (6 mg / 48 mg) | ||

| 6 | Edaravone (Radicava, infus. bag, 300 mcg/ml, 100 ml)O | US | Aug-17 | – | 1.2% | 1 | 712 | 661 | 661 | 661 | 190,880 / 185,182 | First year / subsequent years | ||

| 7 | Cerliponase alfa (Brineura, infus. vial/bottle, 30 mg/ml, 5 ml)B,O | SWE | May-17 | – | 0.2% | 4 | 16,190i | 15,569 | 30,478 | 346,556 | 841,900 | Annual | ||

| 8 | Valbenazine (Ingrezza, capsule, 80 mg)O | US | Mar-17 | – | 0.1% | 1 | – | 265 | 265 | 265 | 96,900 | Annual | ||

| 9 | L1-Antineoplastics | Durvalumab (Imfinzi, infus. vial/bottle, 50 mg/ml, 10 ml)B,C | US | May-17 | Nov-17 | 6.1% | 14.5% | 7 | 4,028 | 3,180 | 3,698 | 4,093 | 11,280 | 28-day cycle |

| 10 | Ribociclib (Kisqali, film-ctd tab, 200 mg)C | US | Mar-17 | Apr-18 | 1.9% | 7 | 101 | 68 | 92 | 236 | 6,340 | 28-day cycle | ||

| 11 | Abemaciclib (Verzenio, tab or film-ctd tab, 150 mg)C | US | Oct-17 | – | 1.8% | 3 | 95ii | 72 | 75 | 239 | 5,300 | 28-day cycle | ||

| 12 | Niraparib (Zejula, capsule, 100 mg)C,O | US | Apr-17 | – | 1.1% | 7 | – | 119 | 158 | 247 | 13,300 | 28-day cycle | ||

| 13 | Midostaurin (Rydapt, capsule, 25 mg)C,O | FRA | Oct-16 | Sept-17 | 0.9% | 8 | 166 | 150 | 167 | 193 | 9,270 | 28-day cycle | ||

| 14 | Inotuzumab ozogamicin (Besponsa, infus. dry bottle, 0.9 mg-1 mg)B,C,O | FRA | Apr-17 | May-18 | 0.8% | 8 | 14,256 | 15,759 | 15,775 | 21,645 | 48,490 / 40,375 | 21-day cycle / subsequent 28-day cycle | ||

| 15 | Avelumab (Bavencio, infus. vial/bottle, 20 mg/ml, 10 ml)B,C,O | US | Mar-17 | Dec-17 | 0.6% | 8 | 1,391 | 1,143 | 1,350 | 1,850 | 9,738 | 28-day cycle | ||

| 16 | Acalabrutinib (Calquence, capsule, 100 mg)C,O | US | Nov-17 | – | 0.6% | 1 | – | 283 | 283 | 283 | 15,840 | 28-day cycle | ||

| 17 | Enasidenib (Idhifa, film-ctd tab, 100 mg)C,O | US | Jul-17 | – | 0.3% | 1 | – | 972 | 972 | 972 | 27,227 | 28-day cycle | ||

| 18 | Brigatinib (Alunbrig, film-ctd tab, 180 mg)C,O | US | May-17 | – | 0.1% | 3 | 337ii | 236 | 416 | 596 | 9,435 | 28-day cycle | ||

| 19 | Tisagenlecleucel (Kymriah, infus. bag)B,C,O,G | GER | Aug-17 | – | 0.1% | 1 | – | 482,549 | 482,549 | 482,549 | 482,549 | One-time treatment | ||

| 20 | Neratinib (Nerlynx, film-ctd tab, 40 mg)C | US | Jul-17 | – | 0.1% | 1 | – | 74 | 74 | 74 | 12,538 | 28-day cycle | ||

| 21 | Copanlisib (Aliqopa, inf. dry bottle, 60 mg)C,O | US | Sept-17 | – | 0.1% | 1 | – | 5,393 | 5,393 | 5,393 | 16,200 | 28-day cycle | ||

| 22 | Tivozanib (Fotivda, capsule, 1.34 mg)C | GER | Nov-17 | – | 0.1% | 2 | – | 145 | 194 | 242 | 4,070 | 28-day cycle | ||

| 23 | D5-Nonsteroidal products for inflammatory skin disorders | Dupilumab (Dupixent, prefill syrng sc, 150 mg/ml, 2 ml)B | US | Mar-17 | Feb-18 | 8.1% | 12.7% | 7 | 1,068 | 780 | 1,013 | 1,801 | 29,386 / 27,800 | First year / subsequent years |

| 24 | Guselkumab (Tremfya, prefill syrng sc, 100 mg/ml, 1 ml)B | US | Aug-17 | Nov-17 | 4.1% | 7 | 3,139 | 2,984 | 3,543 | 12,430 | 22,100 / 20,500 | First year / subsequent years | ||

| 25 | Brodalumab (Siliq/Kyntheum, prefill syrng sc, 140 mg/ml, 1.5 ml)B | SWE | Jul-17 | Jul-18 | 0.6% | 6 | 627 | 670 | 896 | 2,164 | 17,230 / 16,300 | First year / subsequent years | ||

| 26 | J7-Vaccines | Herpes zoster vaccine [recombinant, adjuvanted] (Shingrix Vaccine, vial im, 100 mcg/ml, 0.5 ml)B | US | Dec-17 | Jan-18 | 6.8% | 6.8% | 3 | 119 | 122 | 148 | 174 | 240 | Treatment (2 doses) |

| 27 | A10-Diabetes | Semaglutide (Ozempic, prefill pen, 1.34 mg/ml, 1.5 ml) | US | Jan-18 | Feb-18 | 5.2% | 5.7% | 5 | 132 | 113 | 378 | 643 | 1,720 to 3,440 | Annual |

| 28 | Ertugliflozin (Steglaro, film-ctd tab, 5 mg) | US | Jan-18 | May-17 | 0.5% | 3 | 2i | 2 | 7 | 11 | 894 | Annual | ||

| 29 | R3-Anti-asthma and COPD products | Benralizumab (Fasenra, prefill syrng sc, 30 mg/ml, 1 ml)B | US | Dec-17 | Mar-18 | 3.0% | 3.0% | 7 | 3,770 | 2,908 | 3,299 | 5,880 | 30,160 / 24,500 | First year / subsequent years |

| 30 | M1-Anti-inflammatory and anti-rheumatic products | Baricitinib (Olumiant, film-ctd tab, 2 mg)O | UK | Apr-17 | Sept-18 | 1.8% | 2.8% | 8 | 50 | 34 | 43 | 85 | 18,270 | Annual |

| 31 | Sarilumab (Kevzara, prefill syrng/autoinj, 175 mg/ml, 1.14 ml)B | CAN | Feb-17 | Feb-17 | 1.0% | 8 | 718 | 564 | 769 | 1,941 | 50,500 | Annual | ||

| 32 | B2-Blood coagulation system, other products | Emicizumab (Hemlibra, vial sc, 150 mg/ml, 1 ml)B,O | US | Nov-17 | – | 2.5% | 2.5% | 6 | – | 15,980 | 17,446 | 18,537 | 683,900 / 635,000 | First year / subsequent years |

| 33 | Coagulation Factor IX [recombinant], glycoPEGylated (Rebinyn, vial dry, 2000 IU)B | SWE | Jun-17 | – | 0.1% | 2 | – | 4 | 4 | 4 | 8 to 13 | Dose | ||

| 34 | H4-Other hormones | Abaloparatide (Tymlos, prefill pen, 2 mg/ml, 1.56 ml) | US | Jun-17 | – | 0.9% | 1.0% | 1 | – | 2,131 | 2,131 | 2,131 | 25,500 | Annual |

| 35 | Angiotensin II (Giapreza, infus. vial/bottle, 2.5 mg/ml, 1 ml) | US | Feb-18 | – | <0.1% | 1 | – | 1,915 | 1,915 | 1,915 | 550 / 320 | Max titration / maintenance per hour | ||

| 36 | S1-Ophthalmologicals |

Netarsudil (Rhopressa, eye drops, 0.02%, 2.5 ml) | US | Apr-18 | – | 0.5% | 0.7% | 1 | – | 6 | 6 | 6 | 2,175 | Annual (per eye) |

| 37 | Latanoprostene bunod (Vyzulta, eye drops, 0.02%, 2.5 ml) | US | Dec-17 | – | 0.2% | 1 | – | 4 | 4 | 4 | 1,626 | Annual (per eye) | ||

| 38 | Cenegermin (Oxervate, eye drops, 20 mcg/ml, 1 ml)B,O | GER | Nov-17 | – | <0.1% | 2 | – | 23 | 23 | 23 | 7,690 | 8-week treatment (per eye) | ||

| 39 | Voretigene neparvovec (Luxturna)B,O,G | US | Feb-18 | – | <0.1% | 1 | – | 23,567 | 23,567 | 23,567 | 561,595 | One-time treatment (per eye) | ||

| 40 | A3-Functional gastro-intestinal disorder drugs | Plecanatide (Trulance, tab, 3 mg) | US | Mar-17 | – | 0.6% | 0.6% | 1 | – | 16 | 16 | 16 | 5,900 | Annual |

| 41 | A6-Drugs for constipation and bowel cleansers | Naldemedine (Symproic, film-ctd tab, 200 mcg) | US | Oct-17 | – | 0.2% | 0.2% | 1 | – | 13 | 13 | 13 | 4,800 | Annual |

| 42 | A7-Intestinal disorder products | Telotristat ethyl (Xermelo, film-ctd tab, 250 mg)O | US | Mar-17 | – | 0.2% | 0.2% | 5 | 85i | 16 | 19 | 81 | 92,199 | Annual |

| 43 | J1-Systemic antibacterials | Delafloxacin (Baxdela, tab, 450 mg) | US | Jan-18 | – | 0.1% | 0.1% | 1 | – | 87 | 87 | 87 | 870 / 2,450 | 5-day / 14-day treatment |

| 44 | Vaborbactam (Vabomere, inf. dry bottle, 1 g + 1 g) | US | Aug-17 | – | 0.1% | 1 | – | 197 | 197 | 197 | 16,590 | 14-day treatment | ||

| 45 | D10-Anti-acne prepararations | Ozenoxacin (Ozanex, cream, 1%, 10 g) | CAN | Jan-18 | Jan-18 | 0.1% | 0.1% | 1 | 2 | NA | NA | NA | NA | Topical use |

| 46 | A16-Other alimentary tract and metabolism products | Vestronidase alfa (Mepsevii, infus. vial/bottle, 2 mg/ml, 5 ml)B,O | US | Dec-17 | – | <0.1% | <0.1% | 1 | – | 2,630 | 2,630 | 2,630 | 683,900 | Annual (25kg) |

| 47 | V3-All other therapeutic products | Lutetium Lu 177 dotatate (Lutathera, infus. vial/bottle, 370 mg/ml, 30 ml)C,O | FRA | Apr-15†† | – | <0.1% | <0.1% | 1 | – | 23,567 | 23,567 | 23,567 | 140,000 | 32-week treatment |

| 48 | T2-Diagnostic tests | Macimorelin (Macrilen, oral u-d powdr, 0.05%, 120 ml)O | US | Jul-18 | – | <0.1% | <0.1% | 1 | – | 5,605 | 5,605 | 5,605 | NA | Topical use |

| 49 | B1-Antithrombotic agents | Betrixaban (Bevyxxa, capsule, 80 mg) | US | Jan-18 | – | <0.1% | <0.1% | 1 | – | 15 | 15 | 15 | 540 to 640 | 35- to 42-day treatment |

Medicines without sales data in MIDAS® as of Q4-2018

| Rank | Therapeutic class* | Medicine (trade name, form, strength, volume)† | First approval by FDA, EMA, and/or Health Canada | First approval in Canada | |

|---|---|---|---|---|---|

| 50 | L03-Immunostimulants | Axicabtagene ciloleucel (Yescarta)B,C,O,G | FDA | Oct-17 | Feb-19‡‡ |

| 51 | P01-Antiprotozoals | Benznidazole (Benznidazole)O | FDA | Aug-17 | – |

| 52 | L01-Antineoplastic agents | Padeliporfin (Tookad)C | EMA | Nov-17 | – |

Note: A medicine was considered to be new in 2017 if it received initial market authorization through the US Food and Drug Administration (FDA), the European Medicines Agency (EMA), and/or Health Canada during the calendar year.

Availability and sales information refer to all forms and strengths of the medicine, while pricing and treatment costs are based on the highest-selling form and strength indicated. Sales are based on manufacturer list prices.

* Level 2 of the Anatomical Classification of Pharmaceutical Products, as reported in MIDAS, except for the new medicines without sales data in MIDAS, for which the reporting is based on the Anatomic Therapeutic Chemical (ATC) Classification System maintained by the World Health Organization (WHO).

† B: biologic; C: cancer; O: orphan medicines; G: gene therapies.

‡ France, Germany, Italy, Sweden, Switzerland, the United Kingdom, and the United States.

§ Canadian unit prices were retrieved from IQVIA MIDAS® Database, where available; otherwise, they were taken from:

i CADTH's Canadian Drug Expert Committee Recommendation report.

ii pCODR Expert Review Committee (pERC) Recommendation report.

** Treatment costs were calculated using Canadian list prices if available; otherwise, the foreign median price or available foreign price was used. Information on dosing regimens was taken from the product monograph provided by Health Canada, or the FDA or EMA if unavailable though Health Canada.

†† Lutetium Lu 177 dotatate has been added to the list of 2017 new medicines reported in the previous edition of Meds Entry Watch. Despite being approved individually in France in 2015, it received its first market authorization from the EMA in 2017.

‡‡ Notice of Compliance issued as of Q3-2019.

Data source: IQVIA MIDAS® Database, 2018 (all rights reserved); US Food and Drug Administration Novel Drugs 2017; European Medicines Agency Human Medicines Highlights 2017; Health Canada databases.

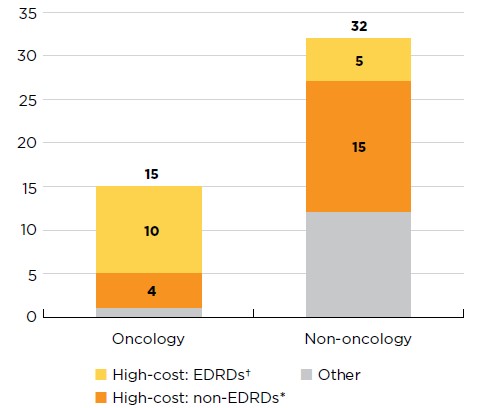

Many of the 2017 new medicines came with a high treatment cost: 14 oncology medicines had costs exceeding $5,000 for a 28-day regimen; and 20 non-oncology medicines had annual costs exceeding $10,000. Ten oncology and five non-oncology orphan medicines qualified as expensive drugs for rare diseases with treatments costs over $7,500 per 28-day cycle or $100,000 annually, respectively.

Figure description

This stacked bar graph gives the distribution of 2017 new medicines with available treatment costs by high-cost bracket. The first bar shows the distribution of new oncology medicines, while the second gives the totals for non-oncology medicines. Each bar is broken down into the number of new medicines that are expensive drugs for rare diseases (EDRDs), those that are high-cost but do not qualify as EDRDs, and all other non-high-cost medicines. High-cost medicines exceed $10,000 in annual treatment costs for non-oncology medicines or $5,000 per 28-day cycle for oncology medicines. Expensive drugs for rare diseases are defined as having treatment costs in excess of $100,000 annually for non-oncology or $7,500 per 28-day cycle for oncology medicines, as well as an orphan designation from either the US Food and Drug Administration or the European Medicines Agency.

| Expensive drugs for rare diseases† | High-cost medicines*, other than EDRDs | Other | Total | |

|---|---|---|---|---|

| Oncology medicines | 10 | 4 | 1 | 15 |

| Non-oncology medicines | 5 | 15 | 12 | 32 |

Note: This analysis considers the 47 new medicines approved in 2017 with treatment costs available as of Q4-2018.

* High-cost medicines have treatment costs exceeding $5,000 per 28-day cycle for oncology or $10,000 annually for non-oncology.

† Expensive drugs for rare diseases (EDRDs) have an orphan designation through the FDA or EMA and treatment costs exceeding $7,500 per 28-day cycle for oncology medicines or $100,000 annually for non-oncology.

Data source: IQVIA MIDAS® Database, 2018. All rights reserved.

Twenty-seven of the medicines first approved in 2017 were authorized for market in Canada by the end of 2018. Of these, 24 had been reviewed by the PMPRB’s Human Drug Advisory Panel (HDAP) as of the third quarter of 2019. The HDAP scientific review found that 75% of the new medicines assessed demonstrated slight or no improvement over their therapeutic comparators.Footnote 2

Table B2 provides an overview of the recommendations and negotiation status for the 27 approved medicines, while Table B3 provides further details on the pharmacoeconomic assessments conducted by CADTH through the Common Drug Review (CDR) and the pan-Canadian Oncology Drug Review (pCODR).

By the third quarter of 2019, 24 new medicines had been reviewed by CADTH for public reimbursement, of which 11 had completed pan-Canadian Pharmaceutical Alliance (pCPA) negotiations and five others had negotiations underway. Thirteen non-oncology medicines reviewed by the CDR received a recommendation to reimburse with clinical criteria and/or conditions while four received a recommendation not to reimburse. Of the oncology medicines reviewed by pCODR, five were recommended for funding on the condition that their cost effectiveness be improved to an acceptable level and one was recommended not to reimburse. One orphan oncology medicine, midostaurin (Rydapt), received a recommendation to reimburse without conditions.

A review of private drug plan data found that over two thirds (19) of the 27 new medicines were reimbursed by at least one private drug plan by the end of 2018. However, these are preliminary results, and their interpretation is limited. For example, if the approval date in Canada was near the end of the 2018 calendar year, the uptake in private plans may only have occurred in 2019 and would not be reflected in these results.

Table B2 Recommendations, negotiation status, and reimbursement decisions for 2017 new medicines approved in Canada by Q4-2018

| ATC* | Medicine (trade name)† | Health Canada approval | CADTH recommendation‡ | pCPA negotiation status§ | Private plans | ||||

|---|---|---|---|---|---|---|---|---|---|

| Notice of Compliance | Reimburse | Reimburse with clinical criteria and/or conditions | Do not reimburse | Active | Completed and closed | No negotiations | Reimbursed | ||

| L1 | Avelumab (Bavencio)B,C,O | Dec-17 | X | X | X | ||||

| M1 | Baricitinib (Olumiant)O | Aug-18 | X | X | |||||

| R3 | Benralizumab (Fasenra)B | Feb-18 | X | X | X | ||||

| L1 | Brigatinib (Alunbrig) C,O | Jul-18 | X | X | |||||

| D5 | Brodalumab (Siliq/Kyntheum)B | Mar-18 | X | X | |||||

| N7 | Cerliponase alfa (Brineura)B,O | Dec-18 | X | X | |||||

| B2 | Coagulation Factor IX [recombinant], glycoPEGylated (Rebinyn)B | Nov-17 | |||||||

| D5 | Dupilumab (Dupixent)B | Nov-17 | X | X | X | ||||

| L1 | Durvalumab (Imfinzi)B,C | May-18 | X | X | X | ||||

| N7 | Edaravone (Radicava)O | Oct-18 | X | ||||||

| B2 | Emicizumab (Hemlibra)B,O | Aug-18 | |||||||

| A10 | Ertugliflozin (Steglatro) | May-18 | X | X | X | ||||

| J5 | Glecaprevir, pibrentasvir (Maviret) | Aug-17 | X | X | X | ||||

| D5 | Guselkumab (Tremfya)B | Nov-17 | X | X | |||||

| J7 | Herpes zoster vaccine [recombinant, adjuvanted] (Shingrix Vaccine)B | Oct-17 | X | ||||||

| L1 | Inotuzumab ozogamicin (Besponsa)B,C,O | Mar-18 | X | X | |||||

| S1 | Latanoprostene bunod (Vyzulta) | Dec-18 | X | X | |||||

| J5 | Letermovir (Prevymis)O | Nov-17 | X | X | X | ||||

| L1 | Midostaurin (Rydapt)C,O | Jul-17 | X | X | X | ||||

| N7 | Ocrelizumab (Ocrevus)B | Feb-18 | X | X | X | ||||

| D10 | Ozenoxacin (Ozanex) | Jan-17 | X | X | X | ||||

| L1 | Ribociclib (Kisqali)C | Mar-18 | X | X | X | ||||

| M1 | Sarilumab (Kevzara)B | Jan-17 | X | X | X | ||||

| A10 | Semaglutide (Ozempic) | Jan-18 | X | X | X | ||||

| A7 | Telotristat ethyl (Xermelo)O | Oct-18 | X | ||||||

| L1 | Tisagenlecleucel (Kymriah)B,C,O,G | Sep-18 | X | ||||||

| J5 | Voxilaprevir (Vosevi) | Aug-17 | X | X | X | ||||

Note: Non-oncology medicines were assessed through CADTH’s Common Drug Review process, while oncology medicines were assessed through the pan-Canadian Oncology Drug Review (pCODR) process.

* Level 2 of the Anatomical Classification of Pharmaceutical Products, as reported in MIDAS®.

† B: biologic; C: cancer; O: orphan medicines; G: gene therapies.

‡ Initial or final recommendation issued as of Q3-2019.

§ As of Q3-2019.

Data source: IQVIA Private Drug Plan database, 2018; Health Canada Notice of Compliance Database; Canadian Agency for Drugs and Technologies in Health (CADTH) reports; pan-Canadian Pharmaceutical Alliance (pCPA) reports.

Table B3 reports information related to the results of the health technology assessments for the new medicines, including the indications assessed; the recommended condition for reimbursement; the primary evaluation; the range of reported incremental cost-effectiveness ratios (ICER) reported; and the price reduction required for the medicine to achieve an ICER of $50,000 per quality-adjusted life year (QALY). The results suggest that most new medicines sold in Canada were not cost-effective at the submitted price, and the vast majority of these medicines were approved on the condition that their price be reduced. At the high end of the reported range, the price of some medicines would need to be decreased by more than 99% in order to achieve an ICER of $50,000 per QALY. Brodalumab, midostaurin, and voxilaprevir were the only medicines to fall within the $50,000/QALY threshold.

Table B3 Summary of Common Drug Review and pan-Canadian Oncology Drug Review assessments for 2017 new medicines approved in Canada, Q2-2019

| Medicine (trade name)* | Date of recommendation† | Indication(s) | Conditional on price‡ | Type of evaluation (primary)§ | Incremental cost-effectiveness ratio (ICER) ($ per QALY) | Price reduction range ($50,000 per QALY) |

|---|---|---|---|---|---|---|

| Avelumab (Bavencio)B,C,O | Mar-18 | Metastatic Merkel cell carcinoma | Yes | CUA | 84,000 to 126,000 | – |

| Benralizumab (Fasenra)B | Aug-18 | Severe eosinophilic asthma | Yes | CUA | 62,000 to 1,534,803 | 15% to 95% |

| Brigatinib (Alunbrig)C,O | Aug-19 | Non-small cell lung cancer | Do not reimburse | CUA/CEA | 117,763 to 163,603 | – |

| Brodalumab (Siliq/Kyntheum)B | Jun-18 | Psoriasis, moderate to severe plaque | Yes | CUA | 43,000 | – |

| Cerliponase alfa (Brineura)B,O | May-19 | Neuronal ceroid lipofuscinosis type 2 | Yes | CUA | 1,718,976 | >99% |

| Dupilumab (Dupixent)B | Jun-18 | Atopic dermatitis | Do not reimburse | CUA | 579,672 | 84% |

| Durvalumab (Imfinzi)B,C | May-19 | Non-small cell lung cancer | Yes | CUA/CEA | 162,670 | – |

| Edaravone (Radicava)O | Mar-19 | Amyotrophic lateral sclerosis | Yes | CUA | 1,441,000 to 3,152,000 | >99% |

| Ertugliflozin (Steglatro/Segluromet) | Jan-19 | Diabetes mellitus, type 2 | Do not reimburse | CCA | - | – |

| Glecaprevir, pibrentasvir (Maviret) | Jan-18 | Hepatitis C, chronic | Yes | CUA | 69,000 to Dominated** | 3% to 12% |

| Guselkumab (Tremfya)B | Feb-18 | Psoriasis, moderate to severe plaque | Yes | CUA | 1,606,003 to Dominated** | – |

| Inotuzumab ozogamicin (Besponsa)B,C,O | Jul-18 | Acute lymphoblastic leukemia | Yes | CUA/CEA/CCA | Dominant** to 200,597 | – |

| Letermovir (Prevymis)O | Jun-18 | Cytomegalovirus infection, prophylaxis | Yes | CUA | 51,052 | 0.1% |

| Midostaurin (Rydapt)C,O | Dec-17 | Acute myeloid leukemia | No | CUA/CEA | 22,579 | – |

| Ocrelizumab (Ocrevus)B | Nov-17 | Multiple sclerosis, relapsing | Yes | CUA | 214,504 to Dominated** | 50% |

| Apr-18 | Primary progressive multiple sclerosis | 588,143 | 82% | |||

| Ozenoxacin (Ozanex) | Oct-18 | Impetigo | Do not reimburse | CUA | 171,907 to 244,184 | 28% to 51% |

| Ribociclib (Kisqali)C | Apr-18 | Advanced or metastatic breast cancer | Yes | CUA/CEA | 175,827 to 204,805 | – |

| Sarilumab (Kevzara)B | Apr-17 | Arthritis, rheumatoid | Yes | CCA | – | – |

| Semaglutide (Ozempic) | May-19 | Diabetes mellitus, type 2 | Yes | CUA | -- | – |

| Tisagenlecleucel (Kymriah)B,C,O,G | Jan-19 | Relapsed or refractory B-cell acute lymphoblastic leukemia | No | CUA | 211,870 | 65% |

| Voxilaprevir (Vosevi) | Jan-18 | Hepatitis C, chronic | Yes | CUA | 923 to 16,864 | – |

Note: The type of evaluation and the incremental cost-effectiveness ratio (ICER) are based on the CDR estimate (base case) and the pCODR Economic Guidance Panel (EGP) evaluations. The table reports the low-bound and high-bound range estimated for all comparators and conditions analyzed. Cost-utility analysis (CUA) and cost-effectiveness analysis (CEA) evaluations are provided as a range per quality-adjusted life year (QALY). Additional information can be accessed at https://www.cadth.ca.

* B: biologic; C: cancer; O: orphan medicines; G: gene therapies.

† Initial or final recommendation issued as of Q2-2019.

‡ Price was explicitly defined as a condition for reimbursement.

§ CUA: cost-utility analysis; CEA: cost-effectiveness analysis; CCA: cost comparison analysis.

** Dominated indicates that a high-bound ICER value cannot be calculated as the product is more costly and less effective than comparator products. Dominant refers to a negative low-bound ICER value, which indicates that the product is less costly and more effective than comparators.

Data source: Canadian Agency for Drugs and Technologies in Health (CADTH) reports.

C: New Medicine Approvals, 2018

The notable rate of approvals in 2017 was sustained through 2018, with a comparable number of new medicines authorized for market. More than half of the new medicines approved received an orphan designation, including many new oncology medicines, while a quarter were biologic therapies. Almost all new cancer treatments were high-cost, and one non-oncology orphan medicine was introduced at over $3.5 million per year.

In 2018, 51 new medicines received first-time market approval through the FDA, the EMA, and/or Health Canada. As of the third quarter of 2019, Canada had approved 19 of these new medicines, trailing behind the EMA (29) and the FDA (50) (Figure C1).

Figure description

This is a bar graph with the number of 2018 new medicines approved by Health Canada, the European Medicines Agency, and the Food and Drug Administration in the United States as of the fourth quarter of 2018 and as of the third quarter of 2019. The total number of new medicines in 2018 was 51.

| US Food and Drug Administration | European Medicines Agency | Health Canada | |

|---|---|---|---|

| Q4-2018 | 50 | 18 | 10 |

| Q3-2019 | 50 | 29 | 19 |

Note: Based on medicines that received market approval through the US Food and Drug Administration (FDA), the European Medicines Agency (EMA) and/or Health Canada in 2018.

Data source: US Food and Drug Administration, European Medicines Agency, and Health Canada databases.

By Q4-2018, 40 new medicines had available sales in Canada, the US, and/or Europe. Over two thirds (28) of these came with treatment costs exceeding $10,000 per year or $5,000 per 28-day course. Table C1 provides a full list of the 51 new medicines approved in 2018 along with the country with first reported sales, the availability in Canada, and the prices and treatment costs where available.Footnote 3 Note that this information reflects the early availability and uptake of these medicines in the markets analyzed. Prices are reported for the highest-selling form and strength of each medicine.

Table C1 New medicines approved in 2018, availability, prices, and treatment costs, Q4-2018

| Medicine (trade name, form, strength, volume)* | Therapeutic class† | Availability | No. of countries with sales | Canadian price§ (CAD) | PMPRB7‡ price (CAD) | Treatment cost** | |||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| First sale in Canada or PMPRB7 | First sale in Canada | Min | Median | Max | Treatment cost (CAD) | Annual / Course | |||||

| Andexanet alfa (Andexxa, vial dry, 100 mg) | B2-Blood coagulation system, other products | US | Sept-18 | – | 1 | – | 3,594 | 3,594 | 3,594 | 31,629 | Dose |

| Apalutamide (Erleada, film-ctd tab, 60 mg)C | L2-Cytostatic hormone therapy | US | Feb-18 | Jul-18 | 3 | 29 | 111 | 111 | 111 | 3,259 | 28-day cycle |

| Avatrombopag (Doptelet, film-ctd tab, 20 mg)O | B2-Blood coagulation system, other products | US | Jun-18 | – | 1 | – | 1,124 | 1,124 | 1,124 | 11,244/ 16,867 | 5-day treatment |

| Bictegravir (Biktarvy, film-ctd tab, 50 mg + 200 mg + 25 mg) | J5-Antivirals | US | Feb-18 | Aug-18 | 6 | 38 | 32 | 39 | 115 | 13,840 | Annual |

| Baloxavir marboxil (Xofluza, film-ctd tab, 20 mg) | J5-Antivirals | US | Nov-18 | – | 1 | – | 95 | 95 | 95 | 191 | Dose |

| Binimetinib (Mektovi, film-ctd tab, 15 mg)C,O | L1-Antineoplastics | US | Jun-18 | – | 3 | – | 37 | 51 | 71 | 8,573 | 28-day cycle |

| Burosumab (Crysvita, vial sc, 30 mg/ml, 1 ml)B,O | M5-Other drugs for disorders of the musculoskeletal system | GER | Apr-18 | – | 2 | – | 6,041 | 10,654 | 15,267 | 183,232 | Annual |

| Caplacizumab (Cablivi, vial dry, 10 mg)O | B6-All other hematological agents | FRA | Sept-18 | – | 2 | – | 2,057 | 4,475 | 6,894 | 143,206 | Treatment†† |

| Cemiplimab (Libtayo, infus. vial dry, 50 mg/ml, 7 ml)B,C | L1-Antineoplastics | US | Oct-18 | – | 1 | – | 10,775 | 10,775 | 10,775 | 10,775 | 28-day cycle |

| Dacomitinib (Vizimpro, film-ctd tab, 15 mg)C,O | L1-Antineoplastics | US | Oct-18 | – | 1 | 117ii | 505 | 505 | 505 | 3,267 | 28-day cycle |

| Damoctocog alfa pegol (Jivi, vial dry ret., 2000 IU)B | B2-Blood coagulation system, other products | US | Sept-18 | – | 1 | – | 4 | 4 | 4 | 422 to 592 | Annual |

| Doravirine (Pifeltro, film-ctd tab, 100 mg) | J5-Antivirals | US | Sept-18 | Nov-18 | 2 | 16 | 54 | 54 | 54 | 5,747 | Annual |

| Duvelisib (Copiktra, capsule, 25 mg)C,O | L1-Antineoplastics | US | Oct-18 | – | 1 | – | 246 | 246 | 246 | 13,750 | 28-day cycle |

| Elagolix (Orilissa, film-ctd tab, 150 mg) | H1-Pituitary and hypothalamic hormones | US | Aug-18 | Oct-18 | 2 | 6 | 38 | 38 | 38 | 1,131 | Annual |

| Elapegademase (Revcovi, vial im, 1.6 mg/ml, 1.5 ml)B,O | A16-Other alimentary tract and metabolism products | US | Nov-18 | – | 1 | – | 11,795 | 11,795 | 11,795 | 3,577,947 | Annual |

| Encorafenib (Bravtovi, capsule, 75 mg)C,O | L1-Antineoplastics | US | Jun-18 | – | 3 | – | 47 | 51 | 71 | 8,627 | 28-day cycle |

| Eravacycline (Xerava, inf. dry bottle, 50 mg) | J1-Systemic antibacterials | US | Oct-18 | – | 1 | – | 56 | 56 | 56 | 623 to 2,179 | 4- to 14-day treatment |

| Erenumab (Aimovig, prefill autoinj, 70 mg/ml, 1 ml) | N2-Analgesics | US | May-18 | Dec-18 | 7 | 554 | 527 | 622 | 808 | 6,646 | Annual |

| Fostamatinib (Tavalisse, film-ctd tab, 100 mg)O | B6-All other hematological agents | US | May-18 | – | 1 | – | 194 | 194 | 194 | 191,036 / 212,802 | Fist year / subsequent years |

| Fremanezumab (Ajovy, prefill syrng sc, 150 mg/ml, 1.5 ml)B | N2-Analgesics | US | Sept-18 | – | 1 | – | 724 | 724 | 724 | 8,685 | Annual |

| Galcanezumab (Emgality, prefill autoinj, 120 mg/ml, 1 ml)B | N2-Analgesics | US | Oct-18 | – | 1 | – | 723 | 723 | 723 | 9,400 / 10,120 | First year / Subsequent years |

| Gilteritinib (Xospata, film-ctd tab, 40 mg)C,O | L1-Antineoplastics | US | Dec-18 | – | 1 | – | 315 | 315 | 315 | 8,832 | 28-day cycle |

| Glasdegib (Daurismo, film-ctd tab, 100 mg)C,O | L1-Antineoplastics | US | Dec-18 | – | 1 | – | 753 | 753 | 753 | 21,091 | 28-day cycle |

| Ibalizumab (Trogarzo, infus. vial/bottle, 150 mg/ml, 1.33 ml)B,O | J5-Antivirals | US | Apr-18 | – | 1 | – | 1,362 | 1,362 | 1,362 | 149,766 / 141,597 | First year / Subsequent years |

| Inotersen (Tegsedi, prefill syrng sc, 189 mg/ml, 1.5 ml)O | N7-Other central nervous system drugs | GER | Oct-18 | – | 1 | – | 14,063 | 14,063 | 14,063 | 731,300 | Annual |

| Ivosidenib (Tibsovo, film-ctd tab, 250 mg)C,O | L1-Antineoplastics | US | Aug-18 | – | 1 | – | 531 | 531 | 531 | 29,747 | 28-day cycle |

| Lanadelumab (Takhzyro, vial sc, 150 mg/ml, 2 ml)O | B6-All other hematological agents | US | Sept-18 | – | 2 | – | 19,422 | 22,934 | 26,446 | 596,288 | Annual |

| Larotrectinib (Vitrakvi, capsule, 100 mg)C,O | L1-Antineoplastics | US | Dec-18 | – | 1 | 320ii | 712 | 712 | 712 | 39,860 | 28-day cycle |

| Lorlatinib (Lorbrena, film-ctd tab, 100 mg)C,O | L1-Antineoplastics | US | Nov-18 | – | 1 | – | 675 | 675 | 675 | 18,888 | 28-day cycle |

| Lusutrombopag (Mulpleta, film-ctd tab, 3 mg) | B2-Blood coagulation system, other products | US | Sept-18 | – | 1 | – | 1,441 | 1,441 | 1,441 | 10,089 | 7-day treatment |

| Mogamulizumab (Poteligeo, infus. vial/bottle, 4 mg/ml, 1 ml)B,C,O | L1-Antineoplastics | US | Oct-18 | – | 1 | – | 4,321 | 4,321 | 4,321 | 120,993 / 60,496 | 28-day cycle |

| Moxetumomab pasudotox (Lumoxiti, inf. dry bottle, 1 mg)B,C,O | L1-Antineoplastics | US | Nov-18 | – | 1 | – | 2,543 | 2,543 | 2,543 | 21,363 | 28-day cycle |

| Patisiran (Onpattro, infus. vial/bottle, 2 mg/ml, 5 ml)O | N7-Other central nervous system drugs | US | Aug-18 | – | 2 | – | 12,032 | 12,418 | 12,804 | 452,025 | Annual |

| Plazomicin (Zemdri, infus. vial/bottle, 50 mg/ml, 10 ml) | G4-Urologicals | US | Jul-18 | – | 1 | – | 400 | 400 | 400 | 3,357 to 5,875 | 4- to 7-day treatment |

| Revefenacin (Yulperi, lung u-d liq, 175 mcg/dose, 3 ml) | R3-Anti-asthma and COPD products | US | Dec-18 | – | 1 | – | 43 | 43 | 43 | 15,805 | Annual |

| Talazoparib (Talzenna, capsule, 1 mg)C | L1-Antineoplastics | US | Oct-18 | – | 2 | – | 611 | 611 | 611 | 17,096 | 28-day cycle |

| Tezacaftor (Symdeko, film-ctd tab, 150 mg + 100 mg)O | R7–Other respiratory system products | US | Feb-18 | – | 2 | – | 294 | 364 | 435 | 132,944 | Annual |

| Tildrakizumab (Ilumya, prefill syrng sc, 100 mg/ml, 1 ml)B | D5-Nonsteroidal products for inflammatory skin disorders | US | Oct-18 | – | 2 | – | 6,218 | 11,458 | 16,698 | 68,748 / 49,652 | First year / Subsequent years |

| Velmanase alfa (Lamzede, inf. dry bottle, 10 mg)O | A16-Other alimentary tract and metabolism products | GER | Mar-18 | – | – | – | 1,379 | 1,830 | 2,282 | 666,297 | Annual |

| Zirconium cyclosilicate (Lokelma, oral u-d powder, 10 g/dose) | V3-All other therapeutic products | SWE | Mar-18 | – | – | – | 23 | 26 | 28 | 9,457 / 9,354 | First year / Subsequent years |

Medicines without sales data in MIDAS® as of Q4-2018

| Medicine (trade name, form, strength, volume)* | Therapeutic class† | First approval by FDA, EMA, and/or Health Canada | First approval in Canada | |

|---|---|---|---|---|

| Calaspargase pegol (Asparlas)B,C,O | Not assigned as of Q3-2019 | FDA | Dec-18 | – |

| Emapalumab (Gamifant)B,O | L04-Immunosuppressants | FDA | Nov-18 | – |

| Moxidectin (Moxidectin)O | P02-Anthelmintics | FDA | Jun-18 | – |

| Omadacycline (Nuzyra) | J01-Antibacterials for systemic use | FDA | Oct-18 | – |

| Pegvaliase (Palynziq)B,O | A16 – Other alimentary tract and metabolism products | FDA | May-18 | – |

| Ravulizumab (Ultomiris)O | L04- Immunosuppressants | FDA | Dec-18 | Aug-19‡‡ |

| Sarecycline (Seysara) | J01- Antibacterials for systemic use | FDA | Oct-18 | – |

| Segesterone acetate (Annovera) | Not assigned as of Q3-2019 | FDA | Aug-18 | – |

| Tafenoquine (Krintafel)O | P01-Antiprotozoals | FDA | Jul-18 | – |

| Tagraxofusp (Elzonris)O | L01-Antineoplastic agents | FDA | Dec-18 | – |

| Tecovirimat (Tpoxx)O | J05-Antivirals for systemic use | FDA | Jul-18 | – |

Note: A medicine was considered to be new in 2018 if it received market approval through the US Food and Drug Administration (FDA), the European Medicines Agency (EMA), and/or Health Canada during the calendar year.

Availability and sales information refers to all forms and strengths of the medicine while pricing and treatment costs are based on the highest-selling form and strength indicated. Sales are based on manufacturer list prices.

* B: biologic; C: cancer; O: orphan medicines.

† Level 2 of the Anatomical Classification of Pharmaceutical Products, as reported in MIDAS, except for the new medicines without sales data in MIDAS, for which the reporting is based on the Anatomic Therapeutic Chemical (ATC) Classification System maintained by the World Health Organization (WHO).

‡ France, Germany, Italy, Sweden, Switzerland, the United Kingdom, and the United States.

§ Canadian unit prices were retrieved from IQVIA MIDAS® Database, where available; otherwise, they were taken from:

i CADTH's Canadian Drug Expert Committee Recommendation report.

ii pCODR Expert Review Committee (pERC) Recommendation report.

** Treatment costs were calculated using Canadian list prices if available; otherwise, the foreign median price or available foreign price was used. Information on dosing regimens was taken from the product monograph provided by Health Canada, or the FDA or EMA if unavailable though Health Canada.

†† Based on assumption of one-day plasma exchange.

‡‡ Notice of Compliance issued as of Q3-2019.

Data source: IQVIA MIDAS® Database, 2018 (all rights reserved); US Food and Drug Administration Novel Drugs 2018; European Medicines Agency Human Medicines Highlights 2018; Health Canada Notice of Compliance Database.

D: Spotlight on Canada

This new section reports on sales and prices of medicines that received their first Canadian approval in 2017, and analyzes the market impact of existing medicines that received approval for additional or extended indications in the same year.

Health Canada granted initial market authorization to 36 medicines in 2017, of which 25 had sales by the end of 2018, accounting for 1.6% of the Canadian pharmaceutical market. Table D1 reports on the availability, sales, and pricing of these 36 new-to-Canada medicines as of Q4-2018. Notably, the five highest-selling medicines were also reported in the list of 2017 new medicines in Section B, indicating that they received their first international approval in the same year.

This table also provides foreign-to-Canadian price ratios for each medicine. These ratios compare the median prices in the PMPRB7 countries with those in Canada to reflect how much more or less Canadians would have paid for a new medicine if they had paid the median international price. The average price of the medicine in Canada is set to a value of one and the corresponding foreign median prices are reported relative to this value.

The average ratio reported across all new medicines was 1.58, indicating that foreign prices at Q4-2018 were 58% higher than those in Canada. However, this result is heavily skewed toward prices in the US market. For medicines with prices available in only one foreign country, typically the US, the average foreign-to-Canadian price ratio was 7.91. When medicines with fewer than two comparator countries were excluded, the average ratio dropped to 1.01, indicating that Canadian prices were on par with those internationally for medicines with established international markets. Given the differences in Canadian and international policies for price increases, this ratio is expected to decrease over time.

Table D1 Medicines first approved in Canada in 2017, availability, sales, and prices, ranked by share of sales, Q4-2018

| Medicine (trade name, form, strength, volume)* | Therapeutic class† | Availability | Share of 2017 Canadian new medicine sales | No. of PMPRB7 countries with sales | Price (CAD) | |||

|---|---|---|---|---|---|---|---|---|

| First ale in the PMPRB7 | First sale in Canada | Canada | PMPRB7‡ median | Foreign-to-Canadian price ratio | ||||

| Dupilumab (Dupixent, prefill syrng sc, 150 mg/ml, 2 ml)B | D5X0-Other nonsteroidal products for inflammatory skin disorders | Mar-17 | Feb-18 | 21.1% | 6 | 1,069 | 1,013 | 0.95 |

| Herpes zoster vaccine [recombinant, adjuvanted] (Shingrix Vaccine, vial im, 100 mcg/ml, 0.5 ml)B | J7E2-Varicella vaccines | Dec-17 | Jan-18 | 18.1% | 2 | 119 | 148 | 1.25 |

| Durvalumab (Imfinzi, infus. vial/bottle, 50 mg/ml, 10 ml)B,C | L1G0- Monoclonal antibody antineoplastics | May-17 | Nov-17 | 13.9% | 5 | 4,028 | 3,698 | 0.92 |

| Guselkumab (Tremfya, prefill syrng sc, 100 mg/ml, 1 ml)B | D5B0-Systemic antipsoriasis products | Jul-17 | Nov-17 | 9.9% | 6 | 3,139 | 3,450 | 1.10 |

| Insulin degludec (Tresiba, prefill pen ret., 200 IU/ml 3 ml) | A10C5-Human insulins and analogues, long-acting | Dec-12 | Sept-17 | 8.4% | 6 | 44 | 31 | 0.70 |

| Glecaprevir, pibrentasvir (Maviret, film-ctd tab, 100 mg + 40 mg) | J5D3-Hepatitis C antivirals | Jul-17 | Sept-17 | 6.4% | 7 | 236 | 230 | 0.97 |

| Ocrelizumab (Ocrevus, infus. vial/bottle, 30 mg/ml, 10 ml)B | N7A0-Multiple sclerosis products | Apr-17 | Sept-17 | 6.2% | 7 | 8,446 | 8,506 | 1.01 |

| Voxilaprevir (Vosevi, film-ctd tab, 400 mg + 100 mg + 100 mg) | J5D3-Hepatitis C antivirals | Jul-17 | Sept-17 | 5.7% | 6 | 699 | 854 | 1.22 |

| Lifitegrast (Xiidra, oph u-d liq, 5%, 0.2 ml) | S1K9-Dry eye products, other | Jul-16 | Feb-18 | 2.6% | 1 | 4 | 11 | 2.99 |

| Nusinersen (Spinraza, vial, 2.4 mg/ml, 5 ml)O | N7X0-All other CNS drugs | Feb-17 | Aug-17 | 2.4% | 7 | 120,597 | 113,453 | 0.94 |

| Brexpiprazole (Rexulti, film-ctd tab, 1 mg) | N5A1-Atypical antipsychotics | Jul-15 | Apr-17 | 1.3% | 1 | 4 | 46 | 12.83 |

| Sarilumab (Kevzara, prefill syrng/autoinj, 175 mg/ml, 1.14 ml)B | M1C0-Specific anti-rheumatic agents | May-17 | Feb-17 | 1.0% | 7 | 718 | 711 | 0.99 |

| Midostaurin (Rydapt, capsule, 25 mg)C,O | L1H0-Protein kinase inhibitor antineoplastics | Oct-16 | Sept-17 | 0.8% | 7 | 166 | 166 | 1.00 |

| Eliglustat (Cerdelga, capsule, 84 mg)O | A16A0- Other alimentary tract and metabolism products | Sept-14 | Nov-17 | 0.7% | 5 | 625 | 558 | 0.89 |

| Eluxadoline (Viberzi, film-ctd tab, 100 mg + 40 mg) | A3G0-Gastro-intestinal sensorimotor modulators | Dec-15 | Apr-17 | 0.4% | 3 | 2 | 2 | 1.01 |

| Letermovir (Prevymis, film-ctd tab, 480 mg)O | J5B3-Herpes antivirals | Dec-17 | Dec-17 | 0.3% | 2 | 246 | 249 | 1.01 |

| Olaratumab (Lartruvo, infus. vial/bot., 16 mg/ml, 50 ml)B,C,O | L1G0- Monoclonal antibody antineoplastics | Nov-16 | Dec-17 | 0.3% | 5 | 2,027 | 1,915 | 0.94 |

| Netupitant (Akynzeo, capsule, 300 mg + 500 mcg) | A4A2-NK1 antagonist antiemetics/antinauseants | Oct-14 | Nov-17 | 0.2% | 7 | 138 | 103 | 0.75 |

| Atezolizumab (Tecentriq, infus. vial/bottle, 60 mg/ml, 20 ml)B,C | L1G0-Monoclonal antibody antineoplastics | May-16 | May-17 | 0.2% | 7 | 7,091 | 6,596 | 0.93 |

| Avelumab (Bavencio, infus. vial/bottle, 20 mg/ml, 10 ml)B,C,O | L1G0- Monoclonal antibody antineoplastics | Mar-17 | Dec-17 | 0.1% | 7 | 1,391 | 1,350 | 0.97 |

| Lixisenatide (Soliqua, prefill pen ret., 100 IU/ml + 33 mcg/ml, 3 ml) | A10C9-Other human insulins and analogues | Feb-13 | Sept-17 | 0.1% | 4 | 39 | 42 | 1.09 |

| Obeticholic acid (Ocaliva, film-ctd tab, 5 mg)O | A5A9-Other bile therapy and cholagogues | Jun-16 | Aug-17 | 0.1% | 6 | 104 | 138 | 1.33 |

| Propiverine (Mictoryl, capsule ret., 30 mg) | G4D4-Urinary incontinence products | Jan-81 | Apr-17 | 0.1% | 3 | 1 | 1 | 1.01 |

| Ozenoxacin (Ozanex, cream, 1%, 10 g) | D10A0-Topical anti-acne preparations | – | Jan-18 | <0.1% | 0 | 2 | – | – |

| Neisseria meningitidis B rLP2086 [subfamilies A,B] (Trumenba, prefill im, 120 mcg/ml, 0.5 ml)B | J7D2-Meningococcal vaccines | Nov-14 | Feb-18 | <0.1% | 5 | 101 | 116 | 1.15 |

| Anthrax immune globulin [human] (Anthrasil)B | J6BB19-Anthrax immunoglobulin | – | – | – | – | – | – | – |

| Coagulation Factor IX [recombinant], glycoPEGylated (Rebinyn, vial dry, 2000 IU)B | B2D2-Factors II, VII, IX and X | Jun-17 | – | – | 1 | – | 4 | – |

| Cysteamine bitartrate (Procysbi, capsule, 75 mg)O | A16A0-Other alimentary tract and metabolism products | Mar-98 | – | – | 5 | – | 28 | – |

| Defibrotide (Defitelio, infus. vial/bottle, 80 mg/ml, 2.5 ml)B,O | B1C4-Platelet cAMP enhancing platelet aggregation inhibitors | May-86 | – | – | 5 | – | 556 | – |

| Florbetaben [18F]§ (Neuraceq) | T1G0-Radiodiagnostic agents | – | – | – | – | – | – | – |

| Ioflupane [123i] (Datscan, vial IV, 5 ml) | T1G0-Radiodiagnostic agents | May-05 | – | – | 2 | – | 1,168 | – |

| Migalastat (Galafold, capsule, 123 mg)O | A16A0- Other alimentary tract and metabolism products | May-16 | – | – | 5 | – | 1,661 | – |

| Necitumumab (Portrazza, infus. vial/bottle, 16 mg/ml 50 ml)B,C | L1G0- Monoclonal antibody antineoplastics | Dec-15 | – | – | 2 | – | 3,082 | – |

| Peramivir (Rapivab, infus. bag, 5 mg/ml, 60 ml) | J5B4-Influenza antivirals | Dec-14 | – | – | 1 | – | 405 | – |

| Sebelipase alfa (Kanuma, infus. vial/bottle, 2 mg/ml, 10 ml)B,O | A16A0- Other alimentary tract and metabolism products | Aug-15 | – | – | 4 | – | 9,142 | – |

| Vernakalant (Brinavess, infus. vial/bottle, 20 mg/ml, 25 ml) | C1B0-Anti-arrhythmics | Sept-10 | – | – | 3 | – | 519 | – |

Note: Some medicines with sales may not be reported in IQVIA’s MIDAS Database; for example, although there is no Canadian sales data available in MIDAS for cysteamine bitartrate (Procysbi), it was the subject of a Notice of Hearing issued by the PMPRB in January 2019 for allegations of excessive pricing.

* B: biologic; C: cancer; O: orphan medicines.

† Level 4 of the Anatomical Classification of Pharmaceutical Products, as reported in MIDAS; if unavailable in MIDAS, the reporting is based on the Anatomical Therapeutic Chemical (ATC) Classification System maintained by the World Health Organization (WHO).

‡ France, Germany, Italy, Sweden, Switzerland, the United Kingdom, and the United States.

§ Canadian and international sales are not reported due to limitations in the available data for this medicine.

Data source: IQVIA MIDAS® Database, 2018, all rights reserved; Health Canada Notice of Compliance Database.

Thirty-four previously marketed medicines were granted new or extended indications by Health Canada in 2017. As a group, these medicines grew by 17%, or nearly $600 million, from 2017 to 2018. By comparison, the Canadian pharmaceutical market grew by 4%, or slightly over $1 billion, over the same period. As a result, existing medications with new indications accounted for 55% of total Canadian pharmaceutical sales growth from 2017 to 2018. Of these medicines, velpatasvir, pembrolizumab, and adalimumab made the greatest positive contributions to the sales growth, while ledipasvir had the greatest negative impact. For the full list of medicines with new indications, as well as their change in sales from 2017 to 2018, see Appendix I.

Table D2 Change in sales of existing medicines with new or extended indications in Canada, 2017 to 2018

| 2017 sales | 2018 sales | Net change in sales (% change) | |

|---|---|---|---|

| Existing medicines with new indications in 2017 | $3.50B | $4.09B | $0.59B (17%) |

| Total Canadian market | $27.43B | $28.51B | $1.07B (4%) |