Report on the Administration of the Members of Parliament Retiring Allowances Act for the Fiscal Year Ended March 31, 2015

© Her Majesty the Queen in Right of Canada,

represented by the President of the Treasury Board, 2016

ISSN: 1487-1815

Catalogue No. BT1-11E-PDF

His Excellency the Right Honourable David Johnston, C.C., C.M.M., C.O.M., C.D.,

Governor General of Canada

Excellency:

I have the honour to submit to Your Excellency the Report on the Administration of the “Members of Parliament Retiring Allowances Act” for the Fiscal Year Ended .

Respectfully submitted,

Original signed by

The Honourable Scott Brison, P.C., M.P.

President of the Treasury Board

Table of Contents

Introduction

The Members of Parliament pension plan (the plan) is a contributory defined benefit pension plan, serving Senators and Members of the House of Commons. The plan was established in 1952 and is governed by the Members of Parliament Retiring Allowances Act (MPRAA) and the Members of Parliament Retiring Allowances Regulations.

This report provides a summary of the plan’s main provisions; presents information for the fiscal year 2014–15 on the transactions recorded in the pension plan accounts; and provides information about membership, benefits paid, and historical data.

In this report, “Members of Parliament” refers to Senators and Members of the House of Commons, and “plan members” refers to both active and retired Members of Parliament. Where necessary, Senators and Members of the House of Commons are referred to separately.

Year at a Glance: 2014‒15

- A total of 393 plan members (401 plan members in 2014) contributed to the plan. There were 18 vacant seats in the Senate and 2 vacant seats in the House of Commons.

- A total of 714 plan members received retirement allowances (718 retirement allowances in 2014).

- The average retirement allowance in pay under the plan, including indexation, was $73,273 ($69,931 in 2014) for retired Senators, and $61,176 ($59,974 in 2014) for retired Members of the House of Commons.

Changes to the Members of Parliament Pension Plan

The Pension Reform Act was tabled before Parliament on October 19, 2012, and received royal assent on . A number of amendments have been made to the MPRAA:

- Effective , contribution rates to the Members of Parliament pension plan are being increased over time to bring the current service cost-sharing ratio to 50 per cent by 2017. Contribution rates for the calendar years 2013 to 2015 were set in the MPRAA. Contribution rates starting , are being set by the Chief Actuary of Canada.

- The age at which a retirement allowance may be paid without a reduction has been raised from age 55 to age 65 for pensionable service accrued on or after . A plan member can elect to receive a retirement allowance at age 55, but the allowance will be reduced by 1 per cent for each year the plan member is under the age of 65. Changes to the Prime Minister’s retirement allowance are described in the “Plan Provisions” section of this report.

- Effective , benefits under the plan for pensionable service accrued on or after , are being coordinated with the Canada/Québec Pension Plan (CPP/QPP). As a result, plan members’ benefits will be reduced at age 60 by a formulated amount.

- Effective , contribution rates no longer distinguish between Senators and Members of the House of Commons.

- Effective , the rate of interest to be credited to the Members of Parliament Retiring Allowances (MPRA) Account and the Members of Parliament Retirement Compensation Arrangements (MPRCA) Account has been modified. The changes are described in the “Interest” section of this report.

- Effective , the President of the Treasury Board, on the basis of actuarial advice, has been authorized to debit amounts from the MPRA and MPRCA accounts if the amounts to the credit of the accounts exceed the costs of all benefits payable from the accounts.

Demographic Highlights

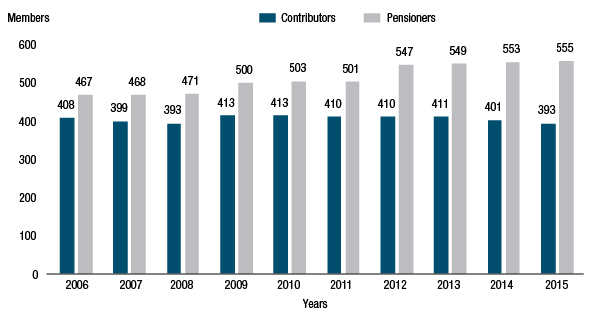

This figure demonstrates the number of contributors relative to the number of pensioners from 2006 to 2015.

Figure 1 - Text version

| 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | |

|---|---|---|---|---|---|---|---|---|---|---|

| Contributors | 408 | 399 | 393 | 413 | 413 | 410 | 410 | 411 | 401 | 393 |

| Pensioners | 467 | 468 | 471 | 500 | 503 | 501 | 547 | 549 | 553 | 555 |

The 10-year annual average growth rate for contributors was -0.3 per cent (0.1 per cent in 2014) compared with 2.3 per cent for pensioners (3.9 per cent in 2014).

| Membership Profile | Number of Plan Members 2011 | Per Cent of Total 2011 | Number of Plan Members 2015 | Per Cent of Total 2015 | Per Cent Change 2011–15 |

|---|---|---|---|---|---|

| Senate contributors | 105 | 9.7 | 87 | 7.9 | -17.1 |

| House of Commons contributors | 305 | 28.3 | 306 | 27.7 | 0.3 |

| Senate pensioners | 64 | 5.9 | 83 | 7.5 | 29.7 |

| House of Commons pensioners | 437 | 40.5 | 472 | 42.6 | 8.0 |

| Survivors | 161 | 15.0 | 153 | 13.8 | -5.0 |

| Children | 6 | 0.6 | 6 | 0.5 | 0.0 |

| Total | 1,078 | 100.0 | 1,107 | 100.0 | 2.7 |

Pension Objective

The objective of the MPRAA is to provide a source of lifetime retirement income for retired and disabled Members of Parliament. Upon a plan member’s death, the plan provides an income for eligible survivors.

Membership Eligibility

All Members of Parliament must contribute to the plan. Membership has been mandatory since 1965 for all Senators, and since 2000 for all Members of the House of Commons.

Plan Provisions for Members

The plan is a contributory defined benefit pension plan, which provides benefits that are calculated using a defined formula. The formula is based on a plan member’s pensionable service and his or her annual sessional indemnity over the five consecutive years of highest-paid pensionable service.

Formula 1 - Text version

The benefit accrual rate multiplied by the average annual sessional indemnity calculated based on five consecutive years of highest-paid service multiplied by the years of pensionable service equals the retirement allowance.

Benefit Accrual Rate

The benefit accrual rate is the rate at which a plan member’s retirement allowance for the year is accumulated.

The benefit accrual rate for Senators is 3 per cent per year of service, to a maximum of 75 per cent of the average sessional indemnity.

The benefit accrual rate for Members of the House of Commons, to a maximum of 75 per cent of the average sessional indemnity, is as follows:

- 3 per cent per year of service effective ;

- 4 per cent per year of service from , to ; and

- 5 per cent per year of service up to and including .

A pro rata is applied on these rates if the additional allowances and salaries differ from the sessional indemnity received in that year. There is no limit to the accrual of benefits on additional allowances and salaries.Footnote 1

The age at which a retirement allowance may be paid without a reduction has been raised from age 55 to age 65 for pensionable service accrued on or after . A plan member can elect to receive a retirement allowance at age 55, but the allowance will be reduced by 1 per cent for each year the plan member is under age 65.

Retirement Allowance

- Effective , a retirement allowance is based on a plan member’s average sessional indemnity for the best five consecutive years.

- Prior to 2001, the average sessional indemnity was based on the six highest consecutive years of service.

Table 2 shows when benefit options are available to plan members who have six or more years of pensionable service. The availability of a benefit depends on when the pensionable service is accrued and at what age the pension benefit is taken.

| If the pensionable service is accrued… | The benefit option is… | Payable at… |

|---|---|---|

| Before | An immediate unreduced retirement allowance | Any age |

| , to | An immediate unreduced retirement allowance | Age 55 |

| Before and after | An immediate unreduced retirement allowance for service accrued before | Age 55 |

| and An immediate and permanently reduced retirement allowance for service accrued after |

Age 55 | |

| or An immediate unreduced retirement allowance for service accrued after |

Age 65 | |

| On or after | An immediate and permanently reduced retirement allowance | Age 55 |

| or An immediate unreduced retirement allowance |

Age 65 |

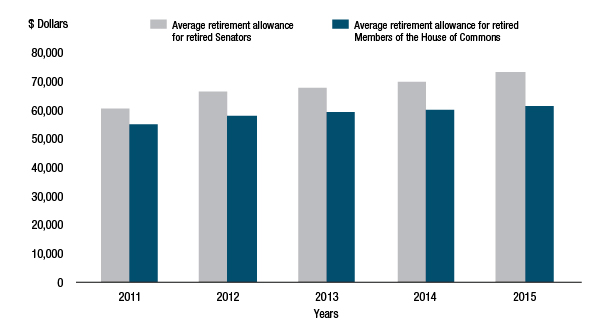

This figure presents the average retirement allowance, including indexation, paid to retired Senators and retired Members of the House Commons from 2011 to 2015. As at , the average retirement allowance paid to retired Senators was $73,273 ($69,931 in 2014); the average retirement allowance paid to retired Members of the House of Commons was $61,176 ($59,974 in 2014).

Figure 2 - Text version

| 2011 | 2012 | 2013 | 2014 | 2015 | |

|---|---|---|---|---|---|

| Average retirement allowance for retired Senators | 60,599 | 66,218 | 67,461 | 69,931 | 73,273 |

| Average retirement allowance for retired Members of the House of Commons | 55,102 | 58,051 | 59,307 | 59,974 | 61,176 |

The retirement allowance of a retired plan member is suspended if that person is re-employed as a Senator or a Member of the House of Commons. If the retired plan member receives remuneration of at least $5,000 in any one-year period as a federal public service employee or pursuant to a federal service contract, all retirement allowances under the MPRAA to that retired plan member in that year will be reduced by one dollar for each dollar of remuneration received in that year.Footnote 2

Withdrawal Allowance

If a plan member ceases to be a member prior to completing six years of contributory service, or if the plan member is disqualified from the Senate or expelled from the House of Commons, the plan member becomes entitled to a withdrawal allowance (also known as a return of contributions). The withdrawal allowance is a reimbursement of all the plan member’s contributions plus interest at a rate set by the Members of Parliament Retiring Allowances Regulations.

Survivor Allowance

Upon a plan member’s death, eligible survivors and children may receive retirement benefits.

| At the time of death, if the member had… | The pension plan may pay… | The benefit is… |

|---|---|---|

| A spouse | a survivor allowance | A monthly allowance equal to 60 per cent of the plan member’s unreduced basic retirement allowance. This amount is payable immediately, for the lifetime of the spouse. |

| Dependent children | a child allowance | A monthly allowance equal to 10 per cent of the plan member’s unreduced retirement allowance, payable to each child until age 18, or age 25 if the child is a full-time student. |

| Dependent children, but no spouse | a child allowance | A monthly allowance equal to 20 per cent of the plan member’s unreduced retirement allowance, payable to each child until age 18, or age 25 if the child is a full-time student. |

| No eligible survivor, or children | a lump sum payment | A minimum benefit equal to the return of contributions (plus interest) exceeding any allowances already paid. The benefit is payable to the plan member’s estate. |

If the plan member did not have six years of pensionable service and was therefore not eligible for a retirement allowance, a withdrawal allowance will be paid to the estate. This lump sum payment is equal to the total of the plan member’s contributions, plus interest compounded annually at 4 per cent for each full year of service.

Indexing

Retirement allowances and survivor allowances are indexed annually to take into account increases in the cost of living. This adjustment corresponds to the percentage increase in the average of the Consumer Price Index (CPI) for the 12-month period ended September 30 over the CPI average for the same 12-month period of the previous year. If there is no change in the CPI, or if it decreases, the allowances will not be adjusted that year. In , the indexing increase was 1.7 per cent (0.9 per cent in ).

Retirement allowances are not indexed until the plan member reaches age 60. However, once indexing begins, payments reflect the cumulative increase in the CPI since the plan member left Parliament.

Survivor allowances and disability pensions are indexed as soon as they start to be paid.

Plan Provisions for the Prime Minister

Retirement Allowance

If a Prime Minister holds office for at least four years, then he or she is entitled to a special retirement allowance in addition to the benefits received as a plan member of the Members of Parliament pension plan. As of , a former Prime Minister has been able to receive a retirement allowance at age 67 or upon ceasing to hold office, whichever is later.

The basic formula for calculating the retirement allowance is:

Formula 2 - Text version

3 percent multiplied by the Prime Minister’s salary upon date of payment which is age 67 or later multiplied by the years of service as a Prime Minister equals the retirement allowance.

Note: The retirement allowance cannot exceed two thirds (2/3) of the Prime Minister’s salary at the time the payment of the retirement allowance begins.

Prior to , payment of the retirement allowance began when the Prime Minister reached age 65 or ceased to be a plan member, whichever was later. The retirement allowance was equal to two thirds of the Prime Minister’s salary at the time the payment of the allowance began.

Survivor Allowance

An eligible survivor receives a survivor allowance equal to 50 per cent of the retirement allowance payable to the former Prime Minister for service as Prime Minister. The survivor allowance is only paid to a spouse, and there is no child’s allowance payable.

Funding

Accounts

Two accounts are maintained in the Public Accounts of Canada to record transactions under the plan: the MPRA Account and the MPRCA Account.

The MPRA Account records the transactions related to the benefits payable under the plan when these benefits are permitted under the Income Tax Act (ITA) for registered pension plans. The MPRCA Account records the transactions related to the benefits payable under the plan when the benefits exceed the limits established by the ITA.

The MPRCA Account is registered with the Canada Revenue Agency (CRA); transfers are recorded annually between the MPRCA Account and the CRA either to remit a 50-per-cent refundable tax in respect of the net contributions and interest credits or to credit a reimbursement based on the net benefit payments. For the fiscal year ended , the MPRCA Account remitted $4.3 million ($10.0 million in 2014) to the CRA.

Statements 1 to 4 in the “Account Transaction Statements”Footnote 3 section of this report present current and historical data on the MPRA and MPRCA accounts.

Actuarial Funding Valuation

As required by the Public Pensions Reporting Act, the President of the Treasury Board directs the Chief Actuary of Canada to conduct an actuarial funding valuation of the pension arrangements established under the MPRAA at least every three years, to be tabled in Parliament by the President. The actuarial valuation presents an estimate of the balance sheet on an actuarial basis—the value of assets and liabilities and any resulting excess or shortfall. In addition, the actuarial valuation also projects the current service cost for each of the next three years following the valuation date. The most recent valuation, the Actuarial Report on the Pension Plan for the Members of Parliament as at , was tabled before Parliament on .

Members’ Contributions

Plan members are required to pay regular monthly contributions to the Members of Parliament pension plan for as long as they remain a Member of Parliament. On , an increase in plan members’ contribution rates began in order to bring the plan members’ share of the pension plan’s current service cost to 50 per cent by 2017. The initial increase was phased in over three years and resulted in contribution rates rising by 1 per cent of salary in to 8 per cent; by another 1 per cent in to 9 per cent; and by 1 per cent in 2015 to 10 per cent; for the second phase, contribution rates for 2016 and 2017 are being set by the Chief Actuary of Canada.

The following table shows plan members’ contribution rates for the calendar years 2015 to 2017.

| Calendar Year | 2015 | 2016table 4 note a | 2017table 4 note b |

|---|---|---|---|

Table 4 Notes

|

|||

| Contribution rates | 10.00% | 15.79% | 21.59% |

Plan members make contributions on their sessional indemnities based on the rates shown above, until they reach the maximum benefit accrual rate of 75 per cent. Once they have accrued a 75 per cent maximum benefit, the contribution rate drops to 1 per cent of salary for the remainder of their service.

Some plan members, such as the speakers, Cabinet ministers, leaders of the opposition and parliamentary secretaries, receive additional allowances and salaries. They make contributions on these additional amounts based on the rates indicated.

The Prime Minister must contribute at the applicable contribution rate of the salary paid to him or her as Prime Minister. This is in addition to the Prime Minister’s contributions as a Member of the House of Commons.

If eligible, a plan member can elect to make contributions on prior service in Parliament, in which case the member must pay interest on past service contributions.

Retirement Compensation Arrangement (RCA)

Retirement compensation arrangements provide benefits that exceed the allowable limits for a registered pension plan under the ITA. The ITA defines the maximum pensionable earnings for which benefits can be accrued during a calendar year. The earnings limit for 2015 is $140,944.50 ($138,500.00 for 2014).

Plan members, who have not reached the age of 71, contribute a portion of their sessional indemnity up to the earnings limit for that year to the MPRA and MPRCA accounts, until they have accrued a retirement allowance equal to 75 per cent of the average sessional indemnity. Once a plan member has reached the earnings limit for the calendar year, the member contributes a certain percentage to the MPRCA Account as established under the MPRAA.

Government Contributions

Each month, the government is required to contribute an amount to the MPRA and MPRCA accounts, after taking into account plan members’ contributions, to fund the costs of all future benefits that members have earned during that month. The government contribution rate for each account varies from year to year and can be expressed as a percentage of the pensionable payroll.

The government’s current service contribution rates for the calendar years 2014 and 2015 are as follows:

| 2014 | 2015 | |

|---|---|---|

| MPRA Account | 13.38% | 12.77% |

| MPRCA Account | 26.45% | 23.67% |

Interest

Every quarter, the government credits interest on the balance of each account at a rate set by the Members of Parliament Retiring Allowances Regulations. Effective , the interest rate to be credited to the MPRA and the MPRCA accounts is the effective quarterly rate derived from the valuation interest rate used in the most recently tabled valuation report from the Chief Actuary of Canada. For the fiscal year ended , interest was credited at 1.082 per cent per quarter for the three quarters ended , and 0.839 per cent for the quarter ended .

Credits and Debits to the Accounts

When the government identifies an unfunded actuarial liability in either the MPRA Account or the MPRCA Account following the tabling of an actuarial valuation report in Parliament, the government must, over a prescribed period, credit to the account such amounts that, after the prescribed period, would cover the unfunded actuarial liability identified.

The Pension Reform Act amended the MPRAA to permit the government, on the basis of actuarial advice from the Chief Actuary, to debit amounts from the MPRA and the MPRCA accounts if the amounts to the credit of the accounts exceed the total costs of all retirement allowances and other benefits payable under the plan. For the fiscal year ended , there was no debit or credit recorded to the accounts.

Roles and Responsibilities

Overall responsibility for the MPRAA lies with the President of the Treasury Board, who is supported by the Treasury Board of Canada Secretariat (as the administrative arm of the Treasury Board), Public Services and Procurement CanadaFootnote 4 and the Senate of Canada.

Treasury Board of Canada Secretariat

The President of the Treasury Board is responsible for the overall management of the plan and acts as the plan’s sponsor. In support of the Treasury Board’s role, the Secretariat is responsible for policy development in respect of the funding, design and governance of the Members of Parliament retirement programs and arrangements.

Public Services and Procurement Canada and the Senate of Canada

Public Services and Procurement Canada and the Senate of Canada are responsible for the day-to-day administration of the plan. This includes developing and maintaining the plan’s pension systems, books of accounts, records, and internal controls, as well as preparing Account Transaction Statements for reporting in the Public Accounts of Canada.

Office of the Chief Actuary

The Office of the Chief Actuary, an independent unit within the Office of the Superintendent of Financial Institutions Canada, provides a range of actuarial services and advice to the Government of Canada, including services and advice for the Members of Parliament pension plan. The Office of the Chief Actuary is responsible for conducting an annual actuarial valuation of the plan for accounting purposes as well as a triennial (i.e., once every three years) funding valuation. It also sets contribution rates and coordination factors for the plan, and recommends credits and debits to the accounts.

Account Transaction Statements

| 2015 | 2014 | |

|---|---|---|

| Members of Parliament Retiring Allowances Account, Opening Balance (A) | 496,467 | 755,806 |

| Receipts and Other Credits | ||

|

Plan members’ contributions, current

|

1,974 | 2,015 |

|

Government contributions, current

|

8,856 | 8,917 |

|

Plan members’ contributions, arrears on principal, interest, and mortality insurance

|

12 | 14 |

|

Government contributions on amounts payable (elections)

|

0 | 0 |

|

Interest

|

20,367 | 36,078 |

|

Transfer from the Supplementary Retirement Benefits Account

|

0 | 0 |

|

Actuarial liability adjustment

|

0 | 0 |

| Total Receipts (B) | 31,209 | 47,024 |

| Payments and Other Charges | ||

|

Retirement allowances

|

26,641 | 26,330 |

|

Withdrawal allowances including interest

|

14 | 33 |

|

Pension division payments

|

0 | |

|

Transfers to the Public Service Superannuation Account

|

0 | 0 |

|

Actuarial adjustment

|

280,000 | |

| Total Payments (C) | 26,655 | 306,363 |

| Excess of Receipts Over Payments (B - C) = (D) | 4,554 | (259,339) |

| Members of Parliament Retiring Allowances Account, Closing Balance (A + D) | 501,021 | 496,467 |

| 2015 | 2014 | |

|---|---|---|

Table 7 Notes

|

||

| Members of Parliament Retirement Compensation Arrangements Account, Opening Balance (A) | 224,403 | 243,993 |

| Receipts and Other Credits | ||

|

Plan members’ contributions, current

|

4,149 | 3,427 |

|

Government contributions, current

|

17,062 | 17,500 |

|

Plan members’ contributions, arrears on principal, interest, and mortality insurance

|

27 | 32 |

|

Interest

|

9,436 | 11,878 |

|

Actuarial liability adjustment

|

0 | 0 |

| Total Receipts (B) | 30,674 | 32,837 |

| Payments and Other Charges | ||

|

Retirement allowances

|

12,912 | 12,355 |

|

Withdrawal allowances plus interest

|

46 | 71 |

|

Pension division payments

|

0 | 0 |

|

Transfer to other pension funds

|

0 | 0 |

|

Refundable tax

table 7 note 1

|

4,305 | 10,001 |

|

Other

table 7 note 2

|

30,000 | |

| Total Payments (C) | 17,263 | 52,427 |

| Excess of Receipts over Payments (B - C) = (D) | 13,411 | (19,590) |

| Members of Parliament Retirement Compensation Arrangements Account, Closing Balance (A + D) | 237,814 | 224,403 |

| Period / Fiscal Year | Members’ Contributions ($)table 8 note a | Government Contributions ($) | Interest ($) | Actuarial and Other Accounting Adjustments ($) | Total Receipts ($) | Annual Allowances ($) | Withdrawal Allowances ($) | Transfers to PSStable 8 note d Account ($) | Othertable 1 note e | Total Payments ($) | Account Balance ($) |

|---|---|---|---|---|---|---|---|---|---|---|---|

Table 8 Notes

|

|||||||||||

| 1952–1989 | 26,299,441 | 25,786,913 | 22,917,200 | 0 | 75,003,554 | 41,114,724 | 4,365,056 | 269,623 | 0 | 45,749,403 | 29,254,221 |

| 1989–90 | 2,267,074 | 2,082,958 | 2,960,449 | 0 | 7,310,481 | 6,197,822 | 124,942 | 24,593 | 0 | 6,347,357 | 30,217,345 |

| 1990–91 | 2,305,080 | 2,175,581 | 3,059,384 | 0 | 7,540,045 | 6,368,934 | 27,364 | 0 | 0 | 6,396,298 | 31,361,092 |

| 1991–92 | 2,060,258 | 2,220,659 | 3,440,449 | 167,941,788table 8 note b | 175,663,154 | 7,187,271 | 7,339 | 0 | 0 | 7,194,610 | 199,829,636 |

| 1992–93 | 1,042,520 | 2,131,335 | 20,493,768 | 0 | 23,667,623 | 9,813,446 | 17,221 | 0 | 0 | 9,830,667 | 213,666,592 |

| 1993–94 | 1,048,643 | 2,064,761 | 21,882,703 | 0 | 24,996,107 | 12,084,079 | 1,852,076 | 0 | 0 | 13,936,155 | 224,726,544 |

| 1994–95 | 1,070,539 | 1,884,100 | 22,861,864 | 0 | 25,816,503 | 15,432,287 | 58,833 | 0 | 0 | 15,491,120 | 235,051,927 |

| 1995–96 | 990,505 | 1,685,476 | 23,933,398 | 0 | 26,609,379 | 14,947,496 | 936,723 | 0 | 0 | 15,884,219 | 245,777,087 |

| 1996–97 | 876,577 | 1,561,870 | 25,029,451 | 0 | 27,467,898 | 15,000,643 | 138,516table 8 note c | 0 | 0 | 15,139,159 | 258,105,826 |

| 1997–98 | 941,060 | 1,707,658 | 26,262,499 | 0 | 28,911,217 | 15,251,902 | 840,524table 8 note c | 0 | 0 | 16,092,426 | 270,924,617 |

| 1998–99 | 1,081,944 | 2,261,589 | 27,620,578 | 0 | 30,964,111 | 15,211,454 | 673,914table 8 note c | 0 | 0 | 15,885,368 | 286,003,360 |

| 1999–2000 | 1,054,926 | 2,673,500 | 29,409,145 | 0 | 33,137,571 | 15,311,534 | 680,015table 8 note c | 0 | 0 | 15,991,549 | 303,149,382 |

| 2000–01 | 1,582,118 | 2,882,101 | 31,014,334 | 0 | 35,478,553 | 15,514,009 | 405,499table 8 note c | 0 | 0 | 15,919,508 | 322,708,427 |

| 2001–02 | 1,366,802 | 3,847,838 | 33,226,180 | 0 | 38,440,820 | 15,993,470 | 154,314table 8 note c | 0 | 0 | 16,147,784 | 345,001,463 |

| 2002–03 | 1,340,110 | 4,395,891 | 35,221,387 | 0 | 40,957,388 | 16,623,728 | 846,514table 8 note c | 0 | 0 | 17,470,242 | 368,488,609 |

| 2003–04 | 1,100,713 | 4,557,315 | 37,822,796 | 0 | 43,480,824 | 16,551,392 | 862,213table 8 note c | 0 | 0 | 17,413,605 | 394,555,828 |

| 2004–05 | 1,361,109 | 4,780,613 | 40,502,434 | 0 | 46,644,156 | 18,108,177 | 566,431table 8 note c | 0 | 0 | 18,674,608 | 422,525,376 |

| 2005–06 | 1,600,703 | 5,226,747 | 43,384,988 | 0 | 50,212,438 | 18,977,081 | 311,777table 8 note c | 188,576 | 0 | 19,477,434 | 453,260,380 |

| 2006–07 | 1,653,756 | 5,355,841 | 46,554,638 | 0 | 53,564,235 | 20,017,711 | 149,303table 8 note c | 0 | 0 | 20,167,014 | 486,657,601 |

| 2007–08 | 1,635,495 | 5,592,419 | 50,003,648 | 0 | 57,231,562 | 20,530,863 | 260,000table 8 note c | 0 | 0 | 20,790,863 | 523,098,300 |

| 2008–09 | 1,690,181 | 6,065,645 | 53,771,144 | 0 | 61,526,970 | 21,404,062 | 559,833table 8 note c | 0 | 0 | 21,963,895 | 562,661,375 |

| 2009–10 | 1,821,235 | 6,800,618 | 57,879,875 | 0 | 66,501,728 | 22,448,720 | 0table 8 note c | 0 | 0 | 22,448,720 | 606,714,383 |

| 2010–11 | 1,840,317 | 7,618,115 | 62,459,846 | 0 | 71,918,278 | 22,996,056 | 0table 8 note c | 0 | 0 | 22,996,056 | 655,636,605 |

| 2011–12 | 1,964,975 | 9,002,051 | 67,506,190 | 0 | 78,473,216 | 24,682,295 | 1,172,223table 8 note c | 206,238 | 0 | 26,060,756 | 708,049,065 |

| 2012–13 | 1,973,869 | 8,999,607 | 62,794,895 | 0 | 73,768,371 | 25,766,262 | 245,281table 8 note c | 0 | 0 | 26,011,543 | 755,805,893 |

| 2013–14 | 2,029,259 | 8,916,866 | 36,078,041 | 0 | 47,024,166 | 26,329,938 | 33,367 | 0 | 280,000,000 | 306,363,305 | 496,466,754 |

| 2014–15 | 1,986,298 | 8,855,514 | 20,367,021 | 0 | 31,208,833 | 26,640,665 | 14,145 | 0 | 0 | 26,654,810 | 501,020,777 |

| Fiscal Year | Members’ Contributions ($) | Government Contributions ($) | Interest ($) | Actuarial and Other Accounting Adjustments ($) | Total Receipts ($) | Annual Allowances ($) | Withdrawal Allowances ($) | Refundable Tax ($) | Transfer to Other Pension Funds | Othertable 9 note c | Total Payments ($) | Account Balance ($) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

Table 9 Notes

|

||||||||||||

| 1992–93 | 1,944,720 | 13,837,316 | 806,119 | 0 | 16,588,155 | 71,198 | 3,901 | 6,516,391 | 0 | 0 | 6,591,490 | 9,996,665 |

| 1993–94 | 1,553,821 | 10,394,866 | 1,487,793 | 0 | 13,436,480 | 391,546 | 571,762 | 6,637,345 | 0 | 0 | 7,600,653 | 15,832,492 |

| 1994–95 | 1,610,329 | 9,058,349 | 2,025,049 | 0 | 12,693,727 | 727,802 | 27,755 | 5,807,226 | 0 | 0 | 6,562,783 | 21,963,436 |

| 1995–96 | 1,246,927 | 5,971,846 | 2,563,705 | 0 | 9,782,478 | 762,478 | 574,632table 9 note a | 4,808,645 | 0 | 0 | 6,145,755 | 25,600,159 |

| 1996–97 | 1,074,385 | 4,944,660 | 2,853,534 | 0 | 8,872,579 | 772,012 | 57,167table 9 note a | 3,884,619 | 0 | 0 | 4,713,798 | 29,758,940 |

| 1997–98 | 1,147,880 | 5,410,244 | 3,257,976 | 0 | 9,816,100 | 954,739 | 718,385table 9 note a | 3,982,375 | 0 | 0 | 5,655,499 | 33,919,541 |

| 1998–99 | 1,353,367 | 6,816,386 | 3,769,294 | 0 | 11,939,047 | 976,109 | 113,933table 9 note a | 5,101,490 | 0 | 0 | 6,191,532 | 39,667,056 |

| 1999–2000 | 1,248,721 | 7,397,670 | 4,458,146 | 0 | 13,104,537 | 1,017,774 | 464,361table 9 note a | 5,790,772 | 0 | 0 | 7,272,907 | 45,498,686 |

| 2000–01 | 1,812,679 | 7,831,603 | 5,031,774 | 0 | 14,676,056 | 1,113,039 | 207,462table 9 note a | 6,460,747 | 0 | 0 | 7,781,248 | 52,393,494 |

| 2001–02 | 2,448,630 | 15,269,084 | 6,396,263 | 0 | 24,113,977 | 1,368,096 | 448,629table 9 note a | 10,049,942 | 0 | 0 | 11,866,667 | 64,640,804 |

| 2002–03 | 2,571,907 | 15,859,000 | 7,248,223 | 9,773,275 | 35,452,405 | 1,445,396 | 412,384table 9 note a | 10,982,904 | 0 | 0 | 12,840,684 | 87,252,525 |

| 2003–04 | 2,925,422 | 16,921,883 | 9,979,113 | 9,773,275 | 39,599,693 | 1,529,508 | 523,313table 9 note a | 17,926,813 | 0 | 0 | 19,979,634 | 106,872,584 |

| 2004–05 | 2,629,785table 9 note b | 16,297,793 | 11,702,344 | 9,645,766 | 40,275,688 | 3,254,354 | 441,259table 9 note a | 17,944,084 | 0 | 0 | 21,639,697 | 125,508,575 |

| 2005–06 | 2,755,607table 9 note b | 16,529,339 | 13,591,352 | 5,708,760 | 38,585,058 | 4,113,948 | 980,709table 9 note a | 18,223,501 | 0 | 0 | 23,318,158 | 140,775,475 |

| 2006–07 | 2,663,652table 9 note b | 16,178,865 | 15,103,392 | 0 | 33,945,909 | 5,886,618 | 211,517table 9 note a | 13,540,275 | 0 | 0 | 19,638,410 | 155,082,974 |

| 2007–08 | 2,579,374table 9 note b | 16,480,107 | 16,501,512 | 0 | 35,560,993 | 6,281,662 | 43,987table 9 note a | 18,318,531 | 0 | 0 | 24,644,180 | 165,999,787 |

| 2008–09 | 2,644,227table 9 note b | 17,921,071 | 17,734,300 | 600,000 | 38,899,598 | 7,431,275 | 801,124table 9 note a | 15,438,016 | 0 | 0 | 23,670,415 | 181,228,970 |

| 2009–10 | 2,710,973table 9 note b | 18,071,572 | 19,272,737 | 600,000 | 40,655,282 | 8,697,147 | 30,562table 9 note a | 15,693,048 | 0 | 0 | 24,420,757 | 197,463,495 |

| 2010–11 | 2,705,797table 9 note b | 19,084,944 | 20,980,723 | 600,000 | 43,371,464 | 8,985,433 | (4,123)table 9 note a | 16,820,431 | 0 | 0 | 25,801,741 | 215,033,218 |

| 2011–12 | 2,757,757table 9 note b | 20,398,894 | 22,706,928 | 600,000 | 45,863,579 | 11,268,702 | 1,541,549table 9 note a | 16,792,406 | 477,875 | 0 | 30,080,532 | 231,416,266 |

| 2012–13 | 2,816,628table 9 note b | 19,212,077 | 20,884,907 | 0 | 42,913,612 | 12,013,724 | 354,656table 9 note a | 17,368,459 | 0 | 600,000 | 30,336,839 | 243,993,039 |

| 2013–14 | 3,459,061table 9 note b | 17,500,384 | 11,878,044 | 0 | 32,837,489 | 12,355,325 | 70,619 | 10,001,484 | 0 | 30,000,000 | 52,427,428 | 224,403,100 |

| 2014–15 | 4,176,493table 9 note b | 17,061,626 | 9,435,453 | 0 | 30,673,572 | 12,912,355 | 45,747 | 4,304,614 | 0 | 0 | 17,262,716 | 237,813,956 |

Statistical Tables

Statistical Table 1

New and Past Retirement Allowances for the Fiscal Year 2014–15

The following 23 new retirement allowances became payable:

- 7 to former Senators

- 1 to the survivor of a former Senator

- 6 to former Members of the House of Commons

- 0 to a former Member of the House of Commons whose retirement allowance was reinstated

- 6 to survivors of former Members of the House of Commons

- 3 to former Members of the House of Commons reinstated in accordance with An Act to Amend the “Members of Parliament Retiring Allowances Act.”

Withdrawal allowances (i.e., return of plan members’ contributions with interest) were paid in respect of two Senators.

The following 26 retirement allowances ceased to be payable:

- to 23 plan members who died during the fiscal year:

- 0 Senators

- 2 former Senators

- 2 survivors of former Senators

- 10 former Members of the House of Commons

- 9 survivors of former Members of the House of Commons

- to 3 plan members for the reasons given below:

- 1 regarding a former Member of the House of Commons suspended in accordance with An Act to Amend the “Members of Parliament Retiring Allowances Act.”

- 2 regarding suspension of the student allowance of a former Member of the House of Commons

Since the MPRAA came into force on , a total of 1,586 retirement allowances and 961 withdrawal allowances have been authorized.

The distribution of retirement allowances in pay (including applicable indexation) at , was as follows:

Statistical Table 2

Distribution of Retirement Allowances in Pay

| Amount of Allowance (dollars) | Former Plan Members | Survivors | Dependent Children/Students | Total 2015 | Total 2014 |

|---|---|---|---|---|---|

| 90,000 and over | 108 | 2 | 0 | 110 | 101 |

| 85,000–89,999 | 18 | 0 | 0 | 18 | 20 |

| 80,000–84,999 | 22 | 0 | 0 | 22 | 19 |

| 75,000–79,999 | 19 | 2 | 0 | 21 | 19 |

| 70,000–74,999 | 28 | 1 | 0 | 29 | 23 |

| 65,000–69,999 | 38 | 0 | 0 | 38 | 46 |

| 60,000–64,999 | 23 | 4 | 0 | 27 | 27 |

| 55,000–59,999 | 37 | 6 | 0 | 43 | 43 |

| 50,000–54,999 | 24 | 3 | 0 | 27 | 32 |

| 45,000–49,999 | 43 | 12 | 0 | 55 | 50 |

| 40,000–44,999 | 44 | 24 | 0 | 68 | 75 |

| 35,000–39,999 | 35 | 8 | 0 | 43 | 42 |

| 30,000–34,999 | 42 | 18 | 0 | 60 | 57 |

| 25,000–29,999 | 28 | 23 | 0 | 51 | 54 |

| 20,000–24,999 | 20 | 16 | 0 | 36 | 34 |

| 15,000–19,999 | 12 | 14 | 0 | 26 | 27 |

| Up to 14,999 | 14 | 20 | 6 | 40 | 49 |

| Totals | 555 | 153 | 6 | 714 | 718 |

Glossary of Terms

- accrued pension benefits

- Benefits earned by plan members under the Members of Parliament pension plan for pensionable service to date.

- accrual rate

- The rate at which a plan member’s retirement benefits for the year are accumulated in a defined benefit plan.

- actuarial valuation

- An actuarial analysis that provides information on the financial condition of a pension plan.

- additional allowances and salary

- The additional remuneration of, and salaries payable to, Members of Parliament who occupy certain offices or positions, such as the Prime Minister, Cabinet ministers, speakers, and leaders of the opposition.

- Canada Pension Plan

- A mandatory earnings-related pension plan, implemented on , to provide basic retirement income to Canadians who work in all the provinces and territories except Quebec. Quebec operates the Québec Pension Plan for persons who work in that province; it is similar to the Canada Pension Plan.

- child

- A dependant who may be entitled to a children’s allowance under the Members of Parliament pension plan, upon the death of a plan member. To be eligible for an allowance, a child must be under 18 years of age. Children between 18 and 25 may receive allowances if they are enrolled in school or another educational institution full-time and have attended continuously since the age of 18 or the date of the plan member’s death, whichever occurs later.

- Consumer Price Index

- A measure of price changes published by Statistics Canada on a monthly basis. The Consumer Price Index measures the retail prices of a “shopping basket” of about 300 goods and services, including food, housing, transportation, clothing and recreation. The index is weighted, meaning that it gives greater importance to price changes for some products than others—more to housing, for example, than to entertainment—in an effort to reflect typical spending patterns. Increases in the Consumer Price Index are also referred to as increases in the cost of living.

- contributions

- Sums credited or paid by the employer (i.e., the Government of Canada) and plan members to finance future pension benefits. Each year, the employer contributes amounts sufficient to fund the future benefits earned by plan members in respect of that year, as determined by the President of the Treasury Board and the Office of Chief Actuary.

- coordination of the Members of Parliament pension plan with the Canada Pension Plan or the Québec Pension Plan

- For pensionable service accrued on or after , Members of Parliament pension plan benefits will be coordinated with the benefits paid under the Canada Pension Plan or the Québec Pension Plan. As a result, Members of Parliament pension plan benefits will be reduced at age 60 by a formulated amount.

- defined benefit pension plan

- A type of pension plan that promises a certain level of pension usually based on the plan member’s salary and years of service. The Members of Parliament pension plan is a defined benefit pension plan.

- indexation

- The automatic adjustment of pensions in pay or accrued pension benefits (i.e., deferred annuities) in accordance with changes in the Consumer Price Index. Under the Members of Parliament pension plan, pensions are indexed in January of each year in order to maintain their purchasing power.

- Members of Parliament pension plan

- A pension plan, established in 1952, that governs pension arrangements for Members of Parliament and provides benefits to their survivors and children payable after death. This plan is defined by the Members of Parliament Retiring Allowances Act and the Members of Parliament Retiring Allowances Regulations.

- Members of Parliament Retiring Allowances Account

- An account established by the Members of Parliament Retiring Allowances Act to record pension transactions relating to benefits payable under the plan.

- Members of Parliament Retiring Allowances Act

- An Act to provide pension benefits to eligible Members of Parliament.

- minimum benefit

- A benefit that is equal to the return of contributions plus interest paid on prior service contributions that exceed allowances already paid to a plan member. It is payable to his or her estate.

- pensionable service

- Periods of service credited to a member of the Members of Parliament pension plan. This service includes any complete or partial periods of purchased service (e.g., service buyback or elective service).

- Québec Pension Plan

- A pension plan, similar to the Canada Pension Plan, that covers individuals working in the province of Quebec. It is administered by the Régie des rentes du Québec.

- retirement allowance

- A benefit payable on a periodic basis to a plan member until the member’s death, unless payment of the benefit is suspended.

- return of contributions

- A benefit that is available to contributors who have less than six years of pensionable service under the Members of Parliament pension plan when they cease to be a plan member. It includes plan member’s contributions plus interest, if applicable.

- sessional indemnity

- An annual amount, equivalent to a salary, payable monthly.

- survivor

- The person who, at the time of the plan member’s death, was married to the plan member before his or her retirement, or was cohabiting in a relationship of a conjugal nature with the plan member prior to retirement and for at least one year prior to the date of death.

- survivor allowance

- A pension benefit paid to the survivor upon a plan member’s death.