Report on the Administration of the Members of Parliament Retiring Allowances Act for the Fiscal Year Ended March 31, 2019

On this page

Her Excellency the Right Honourable Julie Payette, C.C., C.M.M., C.O.M., C.Q., C.D.

Governor General of Canada

Excellency:

I have the honour of submitting to Your Excellency the Report on the Administration of the Members of Parliament Retiring Allowances Act for the Fiscal Year Ended .

Respectfully,

Original signed by

The Honourable Jean-Yves Duclos, P.C., M.P.

President of the Treasury Board

Introduction

The Members of Parliament Pension Plan is a defined benefit pension plan that is funded by contributions from plan members and from the Government of Canada. The plan offers a source of lifetime retirement income for eligible retired and disabled parliamentarians.Footnote 1

The plan was established in 1952 and is governed by the Members of Parliament Retiring Allowances Act (MPRAA). Membership has been mandatory since 1965 for members of the Senate, and since 2000 for members of the House of Commons. Since January 1, 2016, plan member contribution rates have been set by the Chief Actuary of Canada. The employer-member cost-sharing ratio of 50:50, which is required under the Pension Reform Act, was achieved in 2017.

Overall responsibility for the plan lies with the President of the Treasury Board, supported by the Treasury Board of Canada Secretariat, the administrative arm of the Treasury Board. The Secretariat:

- develops policy for the funding, design and governance of the plan

- provides strategic direction, program advice and interpretation

- develops legislation

- communicates with plan members

- liaises with plan stakeholders

Public Services and Procurement Canada and the Senate of Canada handle the day-to-day administration of the plan.

Fiscal year at a glance

Plan member and employer contributions

Benefits paid to retired plan members and survivors

Average annual retirement allowance

Plan benefits

The benefits provided under the Members of Parliament Pension Plan are calculated using a formula that is based on a plan member’s pensionable service and their annual pensionable earnings during their 5 highest-paid consecutive years.

Overview of benefits

- Members who have 6 or more years of pensionable service are entitled to receive a retirement allowance

- Members who cease to be parliamentarians are entitled to a withdrawal allowance if they

- have not completed 6 years of pensionable service

- are disqualified from the Senate or expelled from the House of Commons

- When a plan member dies, eligible survivors and children are entitled to survivor benefits.

Retirement allowance

Table 1 shows how a plan member’s retirement allowance is calculated.

| Lifetime pension benefit (maximum 75% accrualTable 1 footnote 1) | ||||

|---|---|---|---|---|

| For pensionable service accrued before January 1, 2016 | ||||

| 3% (or applicable rate) |

× | Highest average sessional indemnityTable 1 footnote 2 | × | Years of credited pre-2016 service |

| For pensionable service accrued after December 31, 2015 | ||||

| 2.6% up to AMPETable 1 footnote * 3% above AMPE |

× | Highest average pensionable earningsTable 1 footnote 2 | × | Years of credited post-2015 service |

| Bridge benefit (payable on post-2015 service until age 60) | ||||

| 0.4% | × | Average pensionable earnings up to AMPE | × | Years of credited post-2015 service |

A plan member must have at least 6 years of pensionable service to be entitled to receive a retirement allowance.

Eligibility for a benefit depends on when the pensionable service is accrued and at what age the pension benefit is taken.

Table 2 shows benefit options that are available to plan members who have 6 or more years of pensionable service.

| If the pensionable service is accrued… | the benefit is… | payable at… |

|---|---|---|

| on or before July 12, 1995 | an immediate unreduced retirement allowance | any age |

| from July 13, 1995, to December 31, 2015 | an immediate unreduced retirement allowance | age 55 |

| on or after January 1, 2016 | an immediate and permanently reduced retirement allowance | age 55 |

| or an immediate unreduced retirement allowance |

age 65 |

For fiscal year ended March 31, 2019:

- 36 new retirement allowances became payable

- 38 retirement allowances ceased to be paid

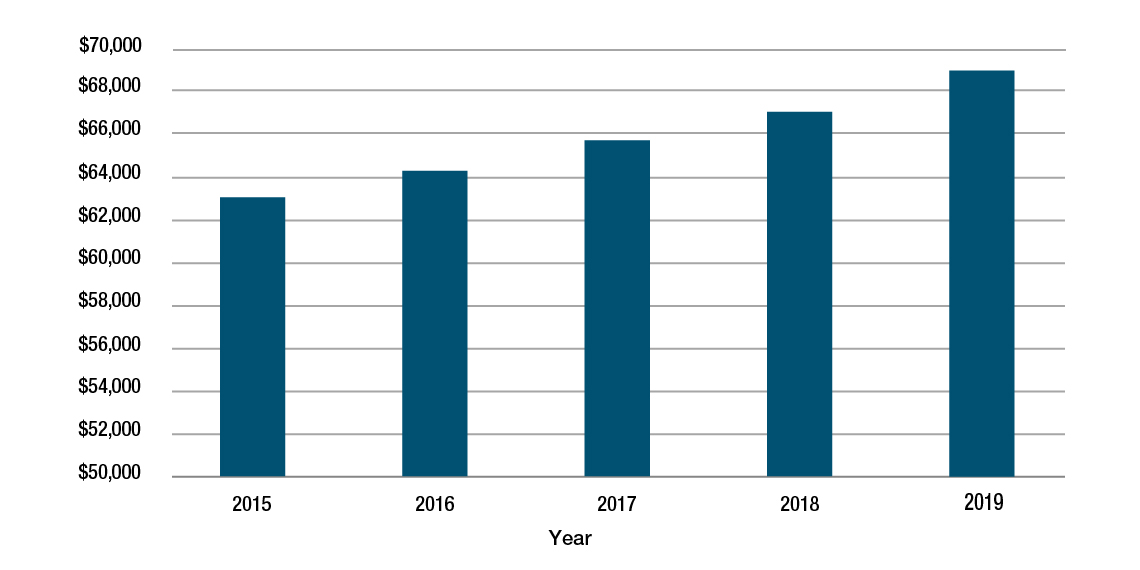

The average retirement allowance paid in fiscal year ended March 31, 2019, was $69,081 ($66,960 in the previous fiscal year).

Figure 1 shows the average retirement allowance, including indexation, paid to retired plan members from 2015 to 2019.

Figure 1 - Text version

| 2015 | 2016 | 2017 | 2018 | 2019 | |

|---|---|---|---|---|---|

| Average retirement allowance | $62,985 | $64,202 | $65,668 | $66,960 | $69,081 |

The age at which a retirement allowance may be paid without a reduction is 65 for pensionable service accrued on or after January 1, 2016. A plan member can elect to start receiving a retirement allowance at age 55, but the allowance will be reduced by 1% for every year the member is under age 65.

Benefits for pensionable service accrued on or after January 1, 2016, have been coordinated with the Canada Pension Plan (CPP) and the Québec Pension Plan (QPP). As a result, a plan member’s retirement allowance now consists of 2 separate components:

- a lifetime pension benefit, payable until the plan member’s death

- a temporary bridge benefit, payable until the plan member reaches age 60

The retirement allowance of a plan member who reaches age 60 (or who starts receiving a retirement allowance after age 60) is reduced by a percentage of the average maximum pensionable earnings (AMPE) for CPP and QPP purposes, multiplied by their years of pensionable service.

Withdrawal allowance

Plan members who cease to be parliamentarians before they have completed 6 years of pensionable service or who are disqualified from the Senate or expelled from the House of Commons are entitled to a withdrawal allowance (also known as a return of contributions).

The withdrawal allowance is a reimbursement of all the member’s contributions paid under Part I and Part II of the MPRAA, plus interest, calculated at the rate of 4%, compounded annually.

Survivor benefits

When a plan member dies, eligible survivors and children may receive a benefit.

Table 3 provides an overview of the different benefits available to survivors when a member has at least 6 years of pensionable service at the time of death.

| At the time of death, if the member had… | the plan may pay… | and the benefit is… |

|---|---|---|

| a spouse or common-law partner | a survivor allowance | a monthly allowance equal to 60% of the plan member’s basic retirement allowance, payable immediately, for the lifetime of the spouse or common-law partner |

| dependent children | a child allowance | a monthly allowance equal to 10% of the plan member’s retirement allowance, payable to each child until age 18, or until age 25 if the child is a full-time student. |

| dependent children, but no spouse or common-law partner | a child allowance | a monthly allowance equal to 20% of the plan member’s retirement allowance, payable to each child until age 18, or until age 25 if the child is a full-time student |

| no eligible survivor or dependent children | a lump-sum payment | a minimum benefit, payable to the plan member’s estate, equal to the return of contributions (plus interest) exceeding any allowances already paid |

Table 3 - Text version

If, at the time of death, the member had a spouse or common-law partner, the pension plan may pay a survivor allowance. This is a monthly allowance equal to 60% of the plan member’s unreduced basic retirement allowance. It is payable immediately, for the lifetime of the spouse or common-law partner.

If, at the time of death, the member had dependent children, the pension plan may pay a child allowance. This is a monthly allowance equal to 10% of the plan member’s unreduced retirement allowance. It is payable to each child until age 18, or until age 25 if the child is a full-time student.

If, at the time of death, the member had dependent children but no spouse or common-law partner, the pension plan may pay a child allowance. This is a monthly allowance equal to 20% of the plan member’s unreduced retirement allowance. It is payable to each child until age 18, or until age 25 if the child is a full-time student.

If, at the time of death, the member had no eligible survivor or dependent children, the pension plan may pay a lump-sum payment to the plan member’s estate. This benefit is a minimum benefit equal to the return of contributions (plus interest) exceeding any allowances already paid.

If the plan member did not have 6 years of pensionable service and was therefore not eligible for a retirement allowance, a withdrawal allowance is paid. If there is no person to whom an allowance or other benefit may be paid, it is paid to the estate.

This lump-sum payment is equal to the total of the plan member’s contributions, plus interest, calculated at the rate of 4%, compounded annually.

Benefit accrual rate

The benefit accrual rate is the rate at which a plan member’s retirement allowance for the year accumulates. It applies to retirement allowances and survivor benefits, but not to withdrawal allowances.

The current benefit accrual rate for plan members is 3% per year of service.

For service before January 1, 2016, the benefit accrual rate for members of the Senate is 3% per year of service; and the benefit accrual rate for members of the House of Commons is as follows:

- 3% per year of service effective January 1, 2001

- 4% per year of service from July 13, 1995, to December 31, 2000

- 5% per year of service up to and including July 12, 1995

Indexation

Retirement allowances, survivor allowances and disability pensions under the plan are indexed annually, in January, to take into account the cost of living, which is based on increases in the Consumer Price Index.

Retirement allowances are not indexed until the member reaches age 60. However, once indexing begins, payments reflect the cumulative increase in the Consumer Price Index since the plan member left Parliament.

Survivor allowances and disability pensions are indexed as soon as they start to be paid.

In 2019, the indexation rate was 2.2% (1.6% in 2018).

Membership statistics

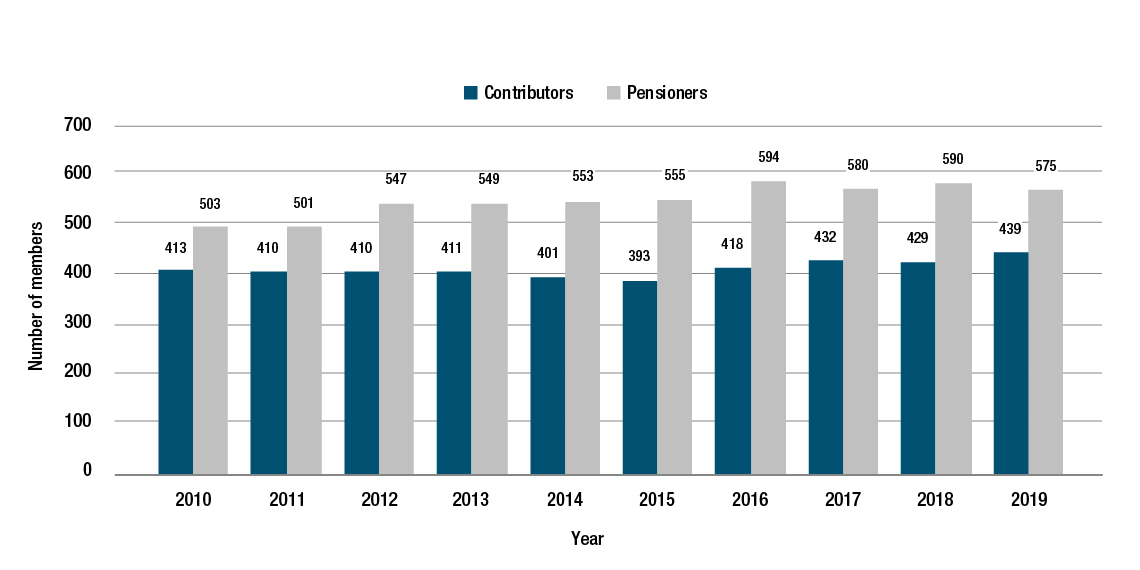

Figure 2 shows the number of contributors and the number of pensioners from 2010 to 2019.

Figure 2 - Text version

| 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | |

|---|---|---|---|---|---|---|---|---|---|---|

| Contributors | 413 | 410 | 410 | 411 | 401 | 393 | 418 | 432 | 429 | 439 |

| Pensioners | 503 | 501 | 547 | 549 | 553 | 555 | 594 | 580 | 590 | 575 |

The 10-year average annual growth rateFootnote 2 for contributors was 0.6% (0.9% in 2018) and 1.4% for pensioners (2.3% in 2018).

Table 4 shows the breakdown of membership by type in 2015 and 2019.

| Member type | Members 2015 | Share of total membership 2015 (%) | Members 2019 | Share of total membership 2019 (%) | Change from 2015 to 2019 (%) |

|---|---|---|---|---|---|

| Contributors | 393 | 35.5 | 439 | 36.8 | 29.9 |

| Pensioners | 555 | 50.1 | 575 | 48.2 | 12.1 |

| Survivors | 153 | 13.8 | 174 | 14.6 | 13.7 |

| Children | 6 | 0.5 | 5 | 0.4 | (16.7) |

| Total | 1,107 | 100.0 | 1,193 | 100.0 | 7.8 |

Plan provisions for prime ministers

-

In this section

Retirement allowance

A prime minister who holds office for at least 4 years is entitled to a special retirement allowance in addition to their Members of Parliament Pension Plan benefit. As of February 6, 2006, former prime ministers can receive a retirement allowance at age 67 or upon ceasing to hold office, whichever is later.

Table 5 shows the basic formula for calculating a prime minister’s retirement allowance.

| 3% | × | The prime minister’s salary when payment of the allowance begins (age 67 or later) | × | Years of service as prime minister |

Table 5 Notes

|

||||

Before February 6, 2006, payment of the retirement allowance began when the prime minister reached age 65 or ceased to be a plan member, whichever was later. The retirement allowance was equal to two thirds of the prime minister’s salary at the time the payment of the allowance began.

Survivor allowance

An eligible survivor receives a survivor allowance equal to 50% of the retirement allowance payable to the former prime minister for service as prime minister. The survivor allowance is paid to a spouse only; there is no child’s allowance.

Financial overview

Accounts

Two accounts are maintained in the Public Accounts of Canada to record transactions under the plan:

- Members of Parliament Retiring Allowances (MPRA) Account

- Members of Parliament Retirement Compensation Arrangements (MPRCA) Account

The MPRA Account records the transactions related to the benefits payable under the plan when these benefits are permitted under the Income Tax Act for registered pension plans. The MPRCA Account records the transactions related to the benefits payable under the plan when the benefits exceed the limits established by the Income Tax Act.

The MPRCA Account is registered with the Canada Revenue Agency. Transactions are recorded annually between the MPRCA Account and the Canada Revenue Agency either to remit a 50% refundable tax in respect of the net contributions and interest credits or to credit a reimbursement based on the net benefit payments. For the fiscal year ended March 31, 2019, the MPRCA Account recorded a refundable tax credit of $58.6 million.Footnote 3 For the fiscal year ended March 31, 2018, the MPRCA Account recorded a refundable tax credit of $3.5 million and remitted $4.7 million to the Canada Revenue Agency.

The Account transaction statements section of this report presents the data on the MPRA and MPRCA accounts for the fiscal years ended March 31, 2018, and March 31, 2019.

Actuarial funding valuation

As required by the Public Pensions Reporting Act, the President of the Treasury Board directs the Chief Actuary of Canada to conduct an actuarial funding valuation of the pension arrangements established under the MPRAA at least every 3 years. The President tables the actuarial valuation in Parliament. This valuation presents an estimate of the balance sheet on an actuarial basis, which means that it presents the account balances and liabilities and any resulting excess or shortfall. The actuarial valuation also projects the current service cost for each of the 3 years following the valuation date. The most recent actuarial funding valuation for the plan, entitled Actuarial Report on the Pension Plan for the Members of Parliament as at 31 March 2016, which has a valuation date of March 31, 2016, was tabled in Parliament on November 3, 2017.

Members’ contributions

Plan members are required to make regular monthly contributions to the plan for as long as they remain parliamentarians. To ensure the sustainability of the plan, contribution rates have been at the 50:50 employer-member cost-sharing ratio since 2017. Contribution rates have been set by the Chief Actuary of Canada since January 1, 2016.

The coordination of benefits with the CPP and QPP, which started in 2016, means that plan members pay different contribution rates on different portions of their pensionable earnings. They pay one rate on the portion that is below the year’s maximum pensionable earnings (YMPE), another rate on the portion that is at or above the YMPE up to the maximum pensionable earnings (MPE), and another rate on the portion that is above the MPE.

The YMPE is the maximum earnings for which contributions can be made to the CPP or QPP during a calendar year. The MPE is the maximum earnings for which pension benefits can be accrued during a calendar year, as defined by the Income Tax Act.

Table 6 shows plan members’ contribution rates to the MPRA Account for the calendar years from 2018 to 2020.

| Calendar year | Under age 71 | Age 71 and above | ||

|---|---|---|---|---|

| Below YMPE | YMPE to MPE | Above MPE | ||

| 2018 | 11.13% | 14.22% | 0.00% | 0.00% |

| 2019 | 11.19% | 14.29% | 0.00% | 0.00% |

| 2020 | 11.30% | 14.43% | 0.00% | 0.00% |

Plan members make contributions on their pensionable earnings at the rates shown above, until they reach the maximum benefit accrual rate of 75%. Once they have reached that maximum, the contribution rate drops to 1% of their salary for the remainder of their service.

Some plan members, such as the speakers, Cabinet ministers, leaders of the opposition and parliamentary secretaries, receive additional allowances and salaries. They make contributions on these additional amounts at the rates indicated.

Prime ministers must contribute at the applicable contribution rate of their salary received as prime minister, in addition to their contributions as a member of the House of Commons.

If eligible, a plan member can elect to make contributions on prior service in Parliament, in which case the member must pay interest on past service contributions.

Retirement compensation arrangement

Retirement compensation arrangements provide benefits that exceed the allowable limits for a registered pension plan under the Income Tax Act. The Income Tax Act defines the maximum pensionable earnings (MPE) for which benefits can be accrued during a calendar year. On January 1, 2016, the earnings limit formula was revised to reflect the coordination with the CPP and QPP.

Table 7 shows the basic formula for calculating the MPE.

| Defined benefit limit | − | % fixed by the Office of the Chief Actuary | × | YMPE | ÷ | 0.02 | + | YMPE |

The MPE are $154,700 for 2018, $159,000 for 2019, and $162,500 for 2020.

Plan members who have not reached the age of 71 contribute to the MPRA and MPRCA accounts a portion of their sessional indemnity up to the MPE for that year, until they have accrued a retirement allowance equal to 75% of the average sessional indemnity. Once a plan member has reached the MPE for the calendar year, the member contributes a certain percentage to the MPRCA Account as established under the MPRAA.

Table 8 shows plan members’ contribution rates to the MPRCA Account for the calendar years from 2018 to 2020.

| Calendar year | Under age 71 | Age 71 and above | |

|---|---|---|---|

| Below MPE | Above MPE | ||

| 2018 | 6.31% | 19.41% | 19.41% |

| 2019 | 6.35% | 19.52% | 19.52% |

| 2020 | 6.40% | 19.70% | 19.70% |

Government of Canada contributions

Every month, the Government of Canada is required to contribute an amount to the MPRA and MPRCA accounts, after taking into account plan members’ contributions, to fund the costs of all future benefits that members have earned during that month. The government’s contributions for each account, which match plan members’ contributions, vary from year to year and can be expressed as a percentage of the pensionable payroll.

Table 9 shows the Government of Canada’s current service contribution rates for the calendar years from 2018 to 2020.

| Account | 2018 | 2019 | 2020 |

|---|---|---|---|

| MPRA Account | 10.69% | 10.81% | 10.94% |

| MPRCA Account | 8.72% | 8.71% | 8.76% |

Interest

Every quarter, the Government of Canada credits interest on the balance of each account at a rate set under the Members of Parliament Retiring Allowances Regulations. Effective January 1, 2013, the interest rate to be credited to the MPRA and the MPRCA accounts is the effective quarterly rate derived from the valuation interest rate used in the most recently tabled valuation report from the Chief Actuary of Canada. For the fiscal year ended March 31, 2019, interest was credited quarterly at a rate of 0.72%.

Credits and debits to the accounts

If there is an unfunded actuarial liability in either the MPRA Account or the MPRCA Account, the MPRA Account or the MPRCA Account must be credited with such amounts that, in the opinion of the President of the Treasury Board, on the basis of actuarial advice, would be necessary to meet the total costs of all the allowances and other benefits payable under the plan. Conversely, if there is an excess of the balance of the accounts over the actuarial liability, the President of the Treasury Board has the authority, on the basis of actuarial advice, to debit amounts from the MPRA Account or the MPRCA Account.

For the fiscal year ended March 31, 2019, no actuarial adjustment was required to meet the total costs of all the allowances and other benefits payable under the plan.

Roles and responsibilities

President of the Treasury Board

The President of the Treasury Board is responsible for the overall management of the plan on behalf of the Government of Canada, the plan’s sponsor.

Treasury Board of Canada Secretariat

The Treasury Board of Canada Secretariat helps the President of the Treasury Board carry out their role by developing policy for the funding, design and governance of the plan and of retirement allowances for parliamentarians. It also provides strategic direction, program advice and interpretation; develops legislation; liaises with stakeholders; communicates with plan members; and prepares an annual report on the administration of the plan.

Public Services and Procurement Canada and the Senate of Canada

Public Services and Procurement Canada and the Senate of Canada are responsible for the day-to-day administration of the plan. This includes developing and maintaining the plan’s pension systems, books of accounts, records, and internal controls, as well as preparing account transaction statements for reporting in the Public Accounts of Canada.

Office of the Chief Actuary

The Office of the Chief Actuary, an independent unit within the Office of the Superintendent of Financial Institutions Canada, provides a range of actuarial services and advice to the Government of Canada on the plan. The Office of the Chief Actuary is responsible for conducting an annual actuarial valuation of the plan for accounting purposes, and for performing a funding valuation once every 3 years. It also sets contribution rates and coordination factors for the plan, and recommends credits and debits to the accounts.

Account transaction statementsFootnote 4

| 2019 | 2018 | |

|---|---|---|

| Opening balance (A) | 557,559 | 509,482 |

| Receipts and other credits | ||

|

Plan members’ contributions, current

|

8,005 | 7,964 |

|

Government contributions, current

|

8,005 | 7,952 |

|

Plan members’ contributions, arrears on principal, interest, and mortality insurance

|

21 | 22 |

|

Interest

|

15,497 | 20,997 |

|

Actuarial adjustment

|

0 | 40,700 |

| Total receipts (B) | 31,528 | 77,635 |

| Payments and other charges | ||

|

Retirement allowances

|

29,048 | 29,347 |

|

Withdrawal allowances, including interest

|

49 | 103 |

|

Pension division payments

|

34 | 108 |

| Total payments (C) | 29,131 | 29,558 |

| Excess of receipts over payments (B - C) = (D) | 2,397 | 48,077 |

| Closing balance (A + D) | 559,956 | 557,559 |

| 2019 | 2018 | |

|---|---|---|

| Opening balance (A) | 142,830 | 254,930 |

| Receipts and other credits | ||

|

Plan members’ contributions, current

|

7,038 | 6,689 |

|

Government contributions, current

|

7,038 | 6,718 |

|

Plan members’ contributions, arrears on principal, interest, and mortality insurance

|

40 | 42 |

|

Interest

|

3,959 | 10,866 |

|

Refundable taxtable 10 note 1

|

58,589 | 3,500 |

| Total receipts (B) | 76,664 | 27,815 |

| Payments and other charges | ||

|

Retirement allowances

|

16,830 | 16,041 |

|

Withdrawal allowances, including interest

|

0 | 138 |

|

Pension division payments

|

19 | 106 |

|

Refundable taxtable 10 note 1

|

1 | 4,730 |

|

Actuarial adjustment

|

0 | 118,900 |

| Total payments (C) | 16,850 | 139,915 |

| Excess of receipts over payments (B - C) = (D) | 59,814 | (112,100) |

| Closing balance (A + D) | 202,644 | 142,830 |

Table 10 Notes

|

||

Statistical table

| Amount of allowance ($) | Former plan members | Survivors | Dependent children or students | Total 2019 | Total 2018 |

|---|---|---|---|---|---|

| 90,000 and over | 150 | 4 | 0 | 154 | 95 |

| 85,000 to 89,999 | 19 | 1 | 0 | 20 | 10 |

| 80,000 to 84,999 | 18 | 1 | 0 | 19 | 22 |

| 75,000 to 79,999 | 24 | 2 | 0 | 26 | 23 |

| 70,000 to 74,999 | 29 | 0 | 0 | 29 | 14 |

| 65,000 to 69,999 | 30 | 3 | 0 | 33 | 39 |

| 60,000 to 64,999 | 32 | 8 | 0 | 40 | 28 |

| 55,000 to 59,999 | 27 | 6 | 0 | 33 | 24 |

| 50,000 to 54,999 | 31 | 6 | 0 | 37 | 12 |

| 45,000 to 49,999 | 43 | 15 | 0 | 58 | 72 |

| 40,000 to 44,999 | 34 | 27 | 0 | 61 | 43 |

| 35,000 to 39,999 | 68 | 16 | 0 | 84 | 39 |

| 30,000 to 34,999 | 20 | 15 | 0 | 35 | 79 |

| 25,000 to 29,999 | 25 | 26 | 0 | 51 | 96 |

| 20,000 to 24,999 | 12 | 12 | 0 | 24 | 29 |

| 15,000 to 19,999 | 9 | 15 | 0 | 24 | 51 |

| Up to 14,999 | 4 | 17 | 5 | 26 | 80 |

| Totals | 575 | 174 | 5 | 754 | 756 |

Glossary

- actuarial valuation

- An actuarial analysis that provides information on the financial condition of a pension plan.

- average maximum pensionable earnings

- The average of the year’s maximum pensionable earnings as set by the Canada Pension Plan and the Québec Pension Plan for the year of retirement and the 4 preceding years.

- benefit accrual rate

- The rate at which a plan member’s retirement allowance for the year accumulates.

- Canada Pension Plan

- A mandatory earnings-related pension plan, implemented on January 1, 1966, to provide basic retirement income to Canadians who work in all the provinces and territories except Quebec, which has its own pension plan (see Québec Pension Plan).

- child

- For the purpose of benefits under the Members of Parliament Pension Plan, a dependant who may be entitled to a children’s allowance under the plan, in the event of a plan member’s death. To be eligible for an allowance, a child must be under 18 years of age. Children between 18 and 25 may receive allowances if they are enrolled in school or another educational institution full-time and have attended continuously since the age of 18 or the date of the plan member’s death, whichever occurs later.

- Consumer Price Index

- A measure of price changes published by Statistics Canada on a monthly basis. The Consumer Price Index measures the retail prices of about 300 goods and services, including food, housing, transportation, clothing and recreation. The index is weighted, meaning that it gives greater importance to price changes for some products than others (for example, more to housing, for example, than to entertainment) in an effort to reflect typical spending patterns. Increases in the Consumer Price Index are also referred to as “cost-of-living increases.”

- defined benefit pension plan

- A type of pension plan that offers eligible members a certain level of pension, which is usually based on their salary and years of service.

- disability

- Impairment or limitation due to a physical, mental, cognitive or developmental condition.

- indexation

- The automatic adjustment of pensions in pay or accrued pension benefits (deferred annuities) in accordance with changes in the Consumer Price Index.

- maximum pensionable earnings

- The maximum earnings for which pension benefits can be accrued during a calendar year, as defined by the Income Tax Act.

- minimum benefit

- A benefit that is payable to a deceased plan member’s estate. It is equal to the withdrawal allowance plus interest paid on prior service contributions that exceed allowances already paid to a plan member.

- pensionable earnings

- The cumulative total of the sessional indemnity, annual allowances and any salary payable during the calendar year.

- pensionable service

- Periods of service credited to a member of the Members of Parliament Pension Plan. This service includes any complete or partial periods of purchased service (for example, service buyback).

- Québec Pension Plan

- A pension plan similar to the Canada Pension Plan that covers individuals working in the province of Quebec. It is administered by Retraite Québec.

- retirement allowance

- An allowance payable on a monthly basis to a plan member until the member’s death, unless payment of the benefit is suspended.

- sessional indemnity

- An annual amount, equivalent to a salary, payable monthly.

- survivor

- The person who, at the time of a plan member’s death, was married to the plan member before their retirement or was cohabiting with the plan member in a conjugal relationship before retirement and for at least 1 year before the date of death.

- survivor allowance

- An allowance paid to the survivor upon a plan member’s death.

- withdrawal allowance

- An allowance that is available to contributors who have less than 6 years of pensionable service under the Members of Parliament Pension Plan when they cease to be a plan member. It includes plan member’s contributions plus interest, if applicable.

- year’s maximum pensionable earnings

- The maximum earnings for which contributions can be made to the Canada Pension Plan and the Québec Pension Plan during the year.

Further information

Additional information on the plan is available on the following sites:

© Her Majesty the Queen in Right of Canada, represented by the President of the Treasury Board, 2020,

ISSN: 1487-1815