Canadian Armed Forces Pension Plans Annual Report for the Fiscal Year ended 31 March 2024

On this page

- Message from the Deputy Commander of Military Personnel Command (MILPERSCOM)

- About this report

- About the plans and its members

- Financial overview

- Fiscal year highlights

- Investment performance

- Administrative expenses

- Governance and oversight

- Financial Statements of the Canadian Forces Pension Plan

- Financial statements of the Reserve Force Pension Plan

- Account Transaction Statements

- Glossary

- Contact Information

Message from the Deputy Commander of Military Personnel Command (MILPERSCOM)

I am pleased to present the Annual Report on the Canadian Armed Forces Pension Plans for the fiscal year ended 31 March 2024. This report provides plan members, parliamentarians, and the Canadian public with insight into how the plans were managed in the last fiscal year.

Canadian Armed Force (CAF) members and the Government of Canada contribute to a pension plan that provides a strong foundation on which to build a secure financial future when CAF members retire. The CAF pension is a key part of the overall CAF compensation package and, along with personal savings, investments, and benefits from the Canada Pension Plan (CPP)/Québec Pension Plan (QPP) and Old Age Security, provide the basis for financially stable retirement years.

As Chair of the Canadian Forces Pension Advisory Committee (CFPAC), my responsibilities include the administration, policy development, and improvement of the CAF pension plans. The CAF will continue to recruit Canada’s best, and work hard to enable their lasting service in the CAF. We will continue to care for those who are ill or injured, whether physically or mentally. We will care for our military families, who have such a central role to play in keeping us strong. Service to Canada is highly valued, and the government’s investment in CAF pension plans reflects the importance it places on that service.

Major General Erick Simoneau

Deputy Commander Military Personnel Command / Assistant Chief Military Personnel

About this report

This report provides information on the Canadian Forces Pension Plan (CFPP) and Reserve Force Pension Plan (RFPP) for the fiscal year ended 31 March 2024. It is prepared and tabled in Parliament in accordance with section 57 of the Canadian Forces Superannuation Act (CFSA). The report includes the plans’ annual financial statements prepared in accordance with the stated accounting policies set out in Note 2 to the statements.

About the plans and its members

First established in 1901 under the Militia Pension Act, the CAF pension plans are administered in accordance with the provisions of CFSA and its supporting regulations.

The CAF pension plans cover all members of the Regular Force component of the CAF and Reserve Force members who have sufficient qualifying service. Regular Force members are members of the CFPP, while Reserve Force members who have sufficient qualifying service and pensionable earnings are members of either the CFPP or the RFPP, depending on their employment status and earnings.

Both CFPP and RFPP are contributory defined benefit pension plans. A contributory defined benefit plan is one to which both the employer and the employee make payments, and in which the benefits payable on death, disability, termination of service, and retirement are specified in the plan document—in this case, the CFSA and its Regulations. The benefits are directly related to the employee's earnings and years of pensionable service.

The plans provide survivor benefits for a member’s eligible spouse, common-law partner, and eligible children.

Plan contributions

For Fiscal Year 2023-2024, CFPP members contributed 9.35% of their pensionable earnings for the first nine months and 9.35% for the last three months, up to the Canada Pension Plan Yearly Maximum Pensionable Earnings (YMPE). Contributions on earnings in excess of the YMPE were made at the rate of 12.37% for the first nine months and 12.25% for the last three months. The YMPE was $66,600 in calendar year 2023 and increased to $68,500 for calendar year 2024.

For FY 2023-2024, part-time members of the Reserve Force who participated in the RFPP contributed 5.2% of salary for the year (unchanged from the prior year) in respect of basic pension benefits and their indexation.

Each year the Government, as the employer, contributes an amount that ensures sufficient future funds will be available for the benefits earned by employees in respect of that year, as determined by the President of the Treasury Board.

Plan benefits

Regular Force members and qualified full-time members of the Reserve Force who retire with 25 years or the equivalent of 9,131 days or more of CAF service are eligible for an immediate annuity.

An immediate annuity is based on the pension plan member’s average salary during the best five consecutive years of pensionable earnings, multiplied by the number of years of pensionable service to a maximum of 35 years times 2%, which includes a bridge benefit to age 65.

In general, Reserve Force members who participate in the RFPP and who retire with at least 9,131 days of CAF service are eligible for an immediate annuity based on the total pensionable years of service, age, and other factors (section 43 of the Reserve Force Pension Plan Regulations).

RFPP pension is based on cumulative pensionable earnings only. The basic benefit formula is 2% multiplied by indexed pensionable earnings, which includes a bridge benefit to age 65. Those Reserve Force members with sufficient qualifying service are automatically converted to membership under the CFPP.

Annuities and member and survivor annual allowances are subject to cost-of-living increases pursuant to the CFSA.

Financial overview

The CFPP and RFPP financial statements provide a comprehensive presentation of the plans’ financial positions. These statements were prepared in accordance with accounting policies of the Canadian accounting standards for pension plans in Part IV of the Chartered Professional Accountants (CPA) Canada Handbook. The Office of the Auditor General of Canada (OAG) audits the financial statements.

The Superannuation Account has been established in the accounts of Canada under the CFSA. It represents a tracking of all contributions, benefit payments, interest revenue, charges, and transfers that pertain to service prior to April 1, 2000. The Account portrays a notional portfolio of bonds, and as such, does not hold any investment assets. The amount of interest credited on the Account is as though net cash flows were invested quarterly in 20-year Government bonds issued at prescribed rates and held to maturity. For service accrued after 31 March 2000, contributions and benefit payments in respect of pensionable service accrued after are recorded in the CFPP in the accounts of Canada, in accordance with the Canadian accounting standards for pension plans. Contributions net of current benefits and administration expenses are regularly transferred to the Public Sector Pension Investment Board (PSPIB) for investment in capital markets to build assets to pay future benefits.

The RFPP is governed by the CFSA and its RFPP Regulations. The RFPP provides pension benefits for all eligible members of the Reserve Force. As with the CFPP, contributions net of current benefits and administration expenses are transferred to PSPIB to be invested in capital markets.

Fiscal year highlights

| CFPP | RFPP | |

|---|---|---|

| Active contributors | 69,298 | 19,235 |

| Retired members | 94,185 | 2,826 |

| Deferred annuitants | 7,748 | 16,349 |

| Survivors receiving benefits | 22,242 | 229 |

| CFPP | RFPP | |

|---|---|---|

| Net assets available for benefits ($millions) | 50,897 | 929 |

| Total Annuity Payments ($millions) | 3,809 | 15 |

| Average Annuity Payment per Member ($) | 38,040 | 5,516 |

| Death Benefits paid ($thousands) | 34,421 | 207 |

| Assets under investment with PSPIB ($millions) | 57,798 | 1,233 |

Investment performance

CFPP and RFPP funds are invested in private and public markets in accordance with the Public Sector Pension Investment Board Act (PSPIBA). PSPIB manages invested pension funds in the best interests of plan contributors and beneficiaries and maximizes returns without undue risk of loss, taking into account the funding, policies, and requirements of the pension plans and the ability of those pension plans to meet their financial obligations. Pension funds are diversified across a variety of investment vehicles.

Asset Mix

Image description

A circular graph indicating that the pension fund’s assets are composed of:

- 21.0 percent Public Market Equities,

- 23.9 percent Government Fixed Income,

- 15.3 percent Private Equity,

- 10.3 percent Real Estate,

- 13.0 percent Infrastructure,

- 9.9 percent Credit Investments,

- 5.7 percent Natural Resources,

- 0.9 percent Complementary Portfolio.

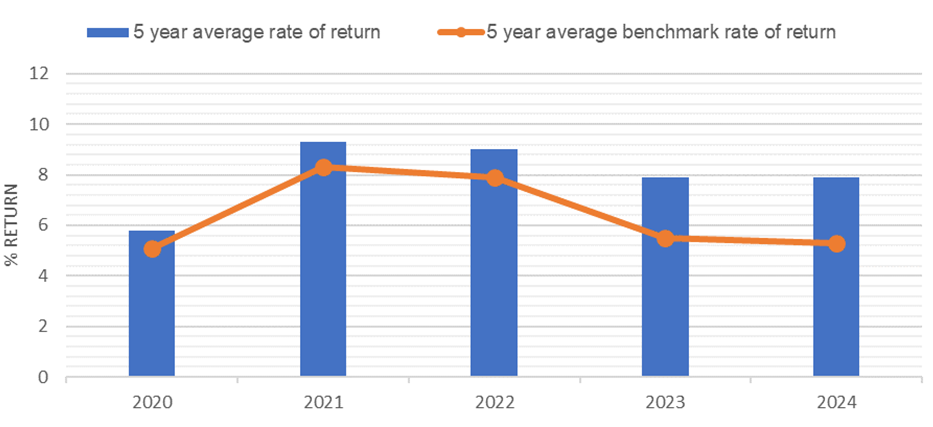

5 year average benchmark rate of return

The investment gain reflects a consolidated 5-year net annual rate of return of 7.9% in FY 2023-2024. The 5-year average rate of return for the plan, as compared to the 5-year average benchmark rate, shows the plan consistently outperforming the comparable benchmark.

Further details and analysis of the investment performance and the overall state of investment markets are available in the 2024 Annual Report of PSPIB.

Image description

This bar graph compares the five year average rate of return of the pension fund against the five year average benchmark rate of return. Overall, the pension fund's performance slightly exceeded the benchmark for each year:

- For year 2020 the average rate of return was 5.8 percent compared to a 5.1 percent average benchmark rate of return

- For year 2021 the average rate of return was 9.3 percent compared to a 8.3 percent average benchmark rate of return

- For year 2022 the average rate of return was 9 percent compared to a 7.9 percent average benchmark rate of return

- For year 2023 the average rate of return was 7.9 percent compared to a 5.5 percent average benchmark rate of return.

- For year 2024 the average rate of return was 7.9 percent compared to a 5.3 percent average benchmark rate of return.

Administrative expenses

Under CFSA legislation, authorized government organizations and the PSPIB charge eligible administrative expenses to the plans. These are expenses that departments incur for plan administration and for the operating expenses of the PSPIB.

While many aspects of the two pension plans are administered jointly, the CFPP and the RFPP each issue independent financial statements. Where expenses incurred can be specifically attributed to the CFPP or RFPP, they are charged accordingly. Expenses which cannot be specifically attributed to one of the pension plans, such as office supplies, are shared between each of the pension plans based on an appropriate allocation method.

| CFPP | RFPP | Total | |

|---|---|---|---|

| Public Services and Procurement Canada (PSPC) | |||

| Salaries and employee benefits | $27,982 | $4,263 | $32,245 |

| Operation and maintenance | 11,627 | 1,771 | 13,398 |

| Subtotal—PSPC | $39,609 | $6,034 | $45,643 |

| Department of National Defence (DND) | |||

| Salaries and employee benefits | $3,024 | $460 | $3,484 |

| Operation and maintenance | 1,089 | 166 | 1,255 |

| Subtotal—DND | $4,113 | $626 | $4,739 |

| Office of the Chief Actuary—Actuarial fees | 936 | 143 | 1,079 |

| Total - Government Departments | $44,658 | $6,803 | $51,461 |

| Public Service Pension Investment Board (PSPIB) | |||

| Salaries and employee benefits | $85,000 | $1,850 | $86,850 |

| Operation and maintenance | 22,000 | 572 | 22,572 |

| Professional and consulting fees | 22,000 | 471 | 22,471 |

| Other | 5,000 | 5,000 | |

| Total - PSPIB | $134,000 | $2,893 | $136,893 |

| Total administrative expenses | $178,658 | $9,696 | $188,354 |

Governance and oversight

Minister of National Defence (MND): The Minister of National Defence is responsible for the oversight of the pension plans. Within the Department of National Defence (DND), the Directorate of Pension Policy and Social Programs (DPSP) oversees the financial analysis, program and policy advice and interpretation, including amendments to the CFSA and its Regulations, on behalf of the MND. DPSP also prepares the Annual Report of the Canadian Armed Forces pension plans.

Treasury Board of Canada Secretariat (TBS): TBS is responsible for the overall pension policy for the four major federal public sector pension plans. The CFSA requires the President of the Treasury Board to consult with the MND on funding matters. TBS provides general guidance to the DND on the accounting for the pension plans through the Office of the Comptroller General.

Canadian Forces Pension Advisory Committee (CFPAC): Chaired by the Deputy Commander Military Personnel Command, CFPAC is an advisory committee to the Minister of National Defence, comprised of up to ten members—one pensioner, three members representing active Regular Force contributors, one member representing Reserve Force personnel, and five other members—all appointed by the Minister of National Defence. CFPAC reviews and provides advice and recommendations to the Minister on pension issues and considers any pension-related matters that the Minister may refer to it.

Public Services and Procurement Canada (PSPC): Under the direction of its Minister, PSPC has assumed the day-to-day administration of the pension plans, alongside the Public Service Pension Plan and Royal Canadian Mounted Police Pension Plan. This includes benefit calculation, and member communications and support. As Receiver General for Canada, the Minister of PSPC is responsible for the central treasury and payments functions.

Public Sector Pension Investment Board (PSPIB): PSPIB is a Crown corporation that reports to Parliament through the President of the Treasury Board. In accordance with the Public Sector Pension Investment Board Act and its Regulations, net pension contributions are transferred to PSPIB and invested in equities, fixed income securities, real estate, private equity, and infrastructure. The relevant financial results of PSPIB are included in the pension plans’ financial statements.

Office of the Superintendent of Financial Institutions (OSFI): OSFI performs an actuarial valuation of the pension plans every three years. This triennial valuation, which is tabled in Parliament by the President of the Treasury Board, is used to compare the pension plans’ assets and liabilities and estimate the contribution rates required to ensure the pension plans’ ongoing financial sustainability. For accounting purposes, the triennial actuarial valuation is updated annually using management’s best estimate assumptions, and actual data on annuitants and contributors.

Office of the Auditor General (OAG): The OAG is responsible for the annual audit of the pension plans’ year-end financial statements to provide assurance that the financial statements are presented fairly, in accordance with Canadian accounting standards for pension plans and that the CAF pension plans comply with the key legislative authorities.

Financial Statements of the Canadian Forces Pension Plan for the fiscal year ended 31 March 2024

Statement of Responsibility

Responsibility for the integrity and fairness of the financial statements of the Canadian Forces Pension Plan (the pension plan) rests with the management of the Department of National Defence. In support of this responsibility, management has developed and maintained books, records, internal controls and management practices designed to provide reasonable assurance as to the reliability of the financial information and to ensure that transactions are in accordance with the Canadian Forces Superannuation Act and regulations, as well as the Financial Administration Act and regulations.

The financial statements of the pension plan for the year ended 31 March 2024, have been prepared in accordance with the stated accounting policies set out in Note 2 to the financial statements, which are based on Canadian accounting standards for pension plans, and on a basis consistent with that of the preceding year. The information included in the financial statements is based on management’s best estimates and judgement, with due consideration given to materiality.

Additional information is obtained as required, from the Public Sector Pension Investment Board (PSPIB) to meet accounting and reporting requirements. PSPIB maintains its own systems of financial management and internal controls to account for the funds managed on behalf of the pension plan in accordance with the Public Sector Pension Investment Board Act, regulations and by-laws.

These financial statements have been audited by the Auditor General of Canada, the independent auditor for the Government of Canada.

Approved by:

Original signed by

Stefanie Beck

Deputy Minister

Major General Erick Simoneau

Deputy Commander MILPERSCOM

Ottawa, Canada

Independent Auditor’s Report

To the Minister of National Defence

Report on the Audit of the Financial Statements

Opinion

We have audited the financial statements of the Canadian Forces Pension Plan (the pension plan), which comprise the statement of financial position as at 31 March 2024, and the statement of changes in net assets available for benefits and statement of changes in pension obligations for the year then ended, and notes to the financial statements, including a summary of significant accounting policies.

In our opinion, the accompanying financial statements present fairly, in all material respects, the financial position of the pension plan as at 31 March 2024, and the changes in its net assets available for benefits and changes in its pension obligations for the year then ended in accordance with Canadian accounting standards for pension plans.

Basis for Opinion

We conducted our audit in accordance with Canadian generally accepted auditing standards. Our responsibilities under those standards are further described in the Auditor’s Responsibilities for the Audit of the Financial Statements section of our report. We are independent of the pension plan in accordance with the ethical requirements that are relevant to our audit of the financial statements in Canada, and we have fulfilled our other ethical responsibilities in accordance with these requirements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion.

Other Information

Management is responsible for the other information. The other information comprises the information included in the annual report, but does not include the financial statements and our auditor’s report thereon.

Our opinion on the financial statements does not cover the other information and we do not express any form of assurance conclusion thereon.

In connection with our audit of the financial statements, our responsibility is to read the other information and, in doing so, consider whether the other information is materially inconsistent with the financial statements or our knowledge obtained in the audit, or otherwise appears to be materially misstated. If, based on the work we have performed, we conclude that there is a material misstatement of this other information, we are required to report that fact. We have nothing to report in this regard.

Responsibilities of Management and Those Charged with Governance for the Financial Statements

Management is responsible for the preparation and fair presentation of the financial statements in accordance with the stated accounting policies set out in Note 2 of the financial statements, which are based on Canadian accounting standards for pension plans, and for such internal control as management determines is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error.

In preparing the financial statements, management is responsible for assessing the pension plan’s ability to continue as a going concern, disclosing, as applicable, matters related to going concern and using the going concern basis of accounting unless management either intends to liquidate the pension plan or to cease operations, or has no realistic alternative but to do so.

Those charged with governance are responsible for overseeing the pension plan’s financial reporting process.

Auditor’s Responsibilities for the Audit of the Financial Statements

Our objectives are to obtain reasonable assurance about whether the financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditor’s report that includes our opinion. Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance with Canadian generally accepted auditing standards will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of these financial statements.

As part of an audit in accordance with Canadian generally accepted auditing standards, we exercise professional judgment and maintain professional skepticism throughout the audit. We also:

- Identify and assess the risks of material misstatement of the financial statements, whether due to fraud or error, design and perform audit procedures responsive to those risks, and obtain audit evidence that is sufficient and appropriate to provide a basis for our opinion. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control

- Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the pension plan’s internal control

- Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates and related disclosures made by management

- Conclude on the appropriateness of management’s use of the going concern basis of accounting and, based on the audit evidence obtained, whether a material uncertainty exists related to events or conditions that may cast significant doubt on the pension plan’s ability to continue as a going concern. If we conclude that a material uncertainty exists, we are required to draw attention in our auditor’s report to the related disclosures in the financial statements or, if such disclosures are inadequate, to modify our opinion. Our conclusions are based on the audit evidence obtained up to the date of our auditor’s report. However, future events or conditions may cause the pension plan to cease to continue as a going concern

- Evaluate the overall presentation, structure and content of the financial statements, including the disclosures, and whether the financial statements represent the underlying transactions and events in a manner that achieves fair presentation

- Obtain sufficient appropriate audit evidence regarding the financial information of the entities or business activities within the pension plan to express an opinion on the financial statements. We are responsible for the direction, supervision, and performance of the group audit. We remain solely responsible for our audit opinion

We communicate with those charged with governance regarding, among other matters, the planned scope and timing of the audit and significant audit findings, including any significant deficiencies in internal control that we identify during our audit.

Report on Compliance with Specified Authorities

Opinion

In conjunction with the audit of the financial statements, we have audited transactions of the Canadian Forces Pension Plan coming to our notice for compliance with specified authorities. The specified authorities against which compliance was audited are the Canadian Forces Superannuation Act and regulations, the Public Sector Pension Investment Board Act and regulations, and the by-laws of the Public Sector Pension Investment Board.

In our opinion, the transactions of the Canadian Forces Pension Plan that came to our notice during the audit of the financial statements have complied, in all material respects, with the specified authorities referred to above.

Responsibilities of Management for Compliance with Specified Authorities

Management is responsible for the Canadian Forces Pension Plan’s compliance with the specified authorities named above, and for such internal control as management determines is necessary to enable the Canadian Forces Pension Plan to comply with the specified authorities.

Auditor’s Responsibilities for the Audit of Compliance with Specified Authorities

Our audit responsibilities include planning and performing procedures to provide an audit opinion and reporting on whether the transactions coming to our notice during the audit of the financial statements are in compliance with the specified authorities referred to above.

Original signed by

Mimma Venema, CPA, CA, CGA

Principal

for the Auditor General of Canada

Ottawa, Canada

26 February 2025

CFPP Financial Statements

| As at 31 March 2024 | As at 31 March 2023 | |

|---|---|---|

| Assets | ||

| Canadian Forces Pension Fund (Note 4) | $79 | $25 |

| Investments (Note 5) | 57,798 | 54,514 |

| Contributions receivable | ||

| From plan members (Note 8) | 92 | 86 |

| From employer (Note 8) | 150 | 137 |

| Transfers receivable from Reserve Force (Note 4 and Note 8) | 59 | 61 |

| Other assets | 36 | 36 |

| Total assets | $58,214 | $54,859 |

| Liabilities | ||

| Investment-related liabilities (Note 5) | 2,064 | 3,023 |

| Accounts payable and other liabilities | 95 | 101 |

| Borrowings (Note 5 and Note 9) | 5,158 | 4,624 |

| Total liabilities | $7,317 | $7,748 |

| Net assets available for benefits | $50,897 | $47,111 |

| Pension obligations | ||

| Funded (Note 12) | $41,431 | $39,256 |

| Unfunded (Note 12 and Note 20) | $43,956 | $46,838 |

| Total pension obligations | $85,387 | $86,094 |

| Deficit to be financed by the Government of Canada (Note 13) | $(34,490) | $(38,983) |

Table 4 NoteCommitments (Note 23) The accompanying notes are an integral part of these financial statements. |

||

| 2024 | 2023 | |

|---|---|---|

| Net assets available for benefits, beginning of year | $47,111 | $44,987 |

| Increase in net assets available for benefits | ||

| Investment income, excluding changes in fair values of investment assets and investment liabilities (Note 14) | 1,525 | 1,265 |

| Changes in fair values of investment assets and investment liabilities, realized and unrealized gains (Note 14) | 2,381 | 1,075 |

| Contributions | ||

| From plan members (Note 15) | 669 | 547 |

| From employer (Note 15) | 1,073 | 893 |

| Transfers from other pension plans (Note 4) | 45 | 73 |

| Total increase in net assets available for benefits | $5,693 | $3,853 |

| Decrease in net assets available for benefits | ||

| Benefits paid with respect to service after 31 March 2000 (Note 17) | 1,204 | 1,072 |

| Change in transfers receivable from Reserve Force | 2 | 12 |

| Refunds and transfers (Note 17) | 159 | 241 |

| Investment-related expenses (Note 18) | 370 | 236 |

| Administrative expenses (Note 19) | 172 | 168 |

| Total decrease in net assets available for benefits | $1,907 | $1,729 |

| Net increase in net assets available for benefits | $3,786 | $2,124 |

| Net assets available for benefits, end of year | $50,897 | $47,111 |

Table 5 NoteThe accompanying notes are an integral part of these financial statements. |

||

| 2024 Funded | 2024 Unfunded | 2024 Total | 2023 Funded | 2023 Unfunded | 2023 Total | |

|---|---|---|---|---|---|---|

| Pension obligations, beginning of year | $39,256 | $46,838 | $86,094 | $37,552 | $50,316 | $87,868 |

| Increase in pension obligations | ||||||

| Interest on pension obligations | 2,436 | 1,384 | 3,820 | 2,072 | 1,172 | 3,244 |

| Benefits earned | 1,436 | 0 | 1,436 | 1,477 | 0 | 1,477 |

| Experience losses (Note 12) | 260 | 287 | 547 | 642 | 1,118 | 1,760 |

| Cost of new elections | 16 | 0 | 16 | 17 | 0 | 17 |

| Transfers from other pension plans | 45 | 0 | 45 | 73 | 0 | 73 |

| Total increase in pension obligations | $4,193 | $1,671 | $5,864 | $4,281 | $2,290 | $6,571 |

| Decrease in pension obligations | ||||||

| Benefits paid (Note 17) | $1,204 | $2,605 | $3,809 | $1,072 | $2,525 | $3,597 |

| Changes in actuarial assumptions: gains (Note 12) | 617 | 1,932 | 2,549 | 1,240 | 3,214 | 4,454 |

| Refunds and transfers (Note 17) | 159 | 10 | 169 | 241 | 13 | 254 |

| Administrative expenses included in the service cost (Note 19 and Note 20) | 38 | 6 | 44 | 24 | 16 | 40 |

| Total decrease in pension obligations | $2,018 | $4,553 | $6,571 | $2,577 | $5,768 | $8,345 |

| Net increase (decrease) in pension obligations | $2,175 | $(2,882) | $(707) | $1,704 | $(3,478) | $(1,774) |

| Pension obligations, end of year | $41,431 | $43,956 | $85,387 | $39,256 | $46,838 | $86,094 |

Table 6 NoteThe accompanying notes are an integral part of these financial statements. |

||||||

1. Description of the Canadian Forces Pension Plan

The Canadian Forces Pension Plan (the pension plan), governed by Part I of the Canadian Forces Superannuation Act (CFSA), provides pension benefits for all members of the Regular Force component and eligible members of the Reserve Force component of the Canadian Forces. Established in 1901 under the Militia Pension Act, the present-day version of the pension plan is administered in accordance with the CFSA.

The main provisions of the pension plan are summarized below.

(A) General

The pension plan is a contributory defined benefit plan covering all members of the Regular Force component and eligible members of the Reserve component of the Canadian Forces. Membership in the pension plan is compulsory for all members of the Regular Force regardless of length of service. Members of the Reserve Force component of the Canadian Forces contribute to the pension plan when they meet eligibility criteria.

The Government of Canada (the government) is the sole sponsor of the pension plan. The Minister of National Defence is the Minister responsible for the CFSA. The Department of National Defence is responsible for the management of the pension plan and maintains the books of account, while Public Services and Procurement Canada (PSPC) provides the day-to-day administration. The Office of the Chief Actuary (OCA), an independent unit within the Office of the Superintendent of Financial Institutions (OSFI), performs periodic actuarial valuations of the pension plan.

Until 1 April 2000, separate invested funds were not set aside to provide for payment of pension benefits. Instead, transactions relating to the pension plan were recorded in a Canadian Forces Superannuation Account (superannuation account) created by legislation in the accounts of Canada. Pursuant to the CFSA, as amended by the Public Sector Pension Investment Board Act, transactions relating to service since 1 April 2000 are now recorded in the Canadian Forces Pension Fund (pension fund). While the pension plan matures, an amount equal to contributions in excess of benefit payments and administrative costs is transferred regularly to the Public Sector Pension Investment Board (PSPIB) for investment. PSPIB is a Crown corporation whose statutory objectives are to manage the funds transferred to it for investment and to maximize investment returns without undue risk of loss, having regard to the funding, policies and requirements of the three main public sector pension plans (public service, Royal Canadian Mounted Police (RCMP) and Canadian Armed Forces). When the pension plan is mature to a state where benefit payments are greater than incoming contributions, which is the normal state for any mature pension plan, PSPIB will transfer amounts to the Consolidated Revenue Fund (CRF) for benefit payments and administrative costs, or as required under the circumstance of a non-permitted surplus (refer to CFSA subsection 55.4 (5) for the definition of non-permitted surplus).

(B) Funding policy

The pension plan is funded from plan member and employer contributions, and from investment earnings. For the fiscal year, members of the pension plan contributed 9.35% (9.36% in 2023) for the first nine months and 9.35% (9.35% in 2023) for the last three months of pensionable earnings, up to the maximum covered by the Canada Pension Plan (CPP) or Québec Pension Plan (QPP), and 12.37% (12.48% in 2023) for the first nine months and 12.25% (12.37% in 2023) for the last three months of pensionable earnings above that maximum.

The government’s contribution is made monthly to provide for the cost (net of plan member contributions) of the benefits that have accrued in respect of that month at a rate determined by the President of the Treasury Board. The contribution rates are determined based on actuarial valuations for funding purposes, which are performed triennially.

The CFSA provides that all pension obligations arising from the pension plan be met by the government. The CFSA requires that any actuarial deficit in the pension fund be dealt with by transferring equal instalments to the pension fund over a period of up to 15 years, starting in the year in which the actuarial report is tabled in Parliament. The CFSA also allows any surplus to be lowered by reducing employer and plan member contributions. In addition, if there is an amount considered to be a non-permitted surplus related to the pension fund, no further government pension contributions are permitted, while plan member contributions under the pension fund may be reduced and amounts managed by PSPIB may be transferred to the government’s CRF.

(C) Benefits

The pension plan provides pension benefits based on the number of years of pensionable service up to a maximum of 35 years. Benefits are determined by a formula set out in the legislation; they are not based on the financial status of the pension plan. The basic benefit formula is 2 % per year of pensionable service multiplied by the average salary of the five consecutive years of highest paid service. To reflect the Income Tax Act restrictions on registered pension plan benefits, separate retirement compensation arrangements (RCAs) have been implemented to provide benefits that exceed the limits established in the Income Tax Act. Since the RCAs are covered by separate legislation, their account balances in the accounts of Canada are not consolidated in these financial statements; however, condensed information is presented in Note 21.

Pension benefits are coordinated with the CPP and QPP and are reduced when the plan member reaches age 65 or earlier if the member receives a disability benefit from the CPP or QPP. The pension reduction factor is 0.7% for members born before 1943, declining gradually for members born from 1943 to 1946 until it reaches 0.625% for members born after 1946. Benefits are fully indexed to the annual increase in the Consumer Price Index.

Other benefits include survivor pensions, deferred annuities, annual allowances, transfer values, cash termination allowances or minimum benefits in the event of death, unreduced early retirement pensions, and disability pensions.

2. Significant accounting policies

The significant accounting policies that have been applied in the preparation of these financial statements are summarized below.

(A) Basis of presentation

These financial statements present information on the pension plan on a going-concern basis. They are prepared to assist plan members and others in reviewing the activities of the pension plan for the year, not to portray the funding requirements of the pension plan.

These financial statements are prepared in Canadian dollars, the pension plan’s functional currency, in accordance with the accounting policies stated below, which are based on Canadian accounting standards for pension plans in Part IV of the Chartered Professional Accountants (CPA) Canada Handbook (Section 4600). Section 4600 provides specific accounting guidance on investments and pension obligations. For accounting policies that do not relate to either investments or pension obligations, the pension plan complies with International Financial Reporting Standards (IFRS) in Part I of the CPA Canada Handbook. To the extent that IFRS in Part I are inconsistent with Section 4600, Section 4600 takes precedence. The presentation and results using the stated accounting policies do not result in any significant differences from Canadian accounting standards for pension plans.

PSPIB is a Crown corporation whose statutory objectives are to manage the funds transferred to it for investment and to maximize investment returns without undue risk of loss. PSPIB qualifies as an investment entity as defined under IFRS 10 Consolidated Financial Statements and forms part of the pension plan reporting entity. Pursuant to Section 4600, PSPIB’s subsidiaries that are formed to hold investments or those that provide PSPIB with services that relate to its investment activities are consolidated, since these entities are not considered investment assets. PSPIB’s investment in subsidiaries, associates, and joint ventures that are considered investment assets are measured at fair value in accordance with Section 4600. Financial liabilities are also measured at fair value in accordance with Section 4600.

The financial statements for the year ended 31 March 2024 were authorized for issue by the signatories on 26 February 2025.

(B) Interests in other entities

Management, through the activities of PSPIB, assesses control, joint control and significant influence with respect to the investees disclosed in Note 6 as follows:

(I) Control and significant influence

A subsidiary is an entity which is controlled by PSPIB. PSPIB determines that it controls an investee when it has power over the investee, is exposed, or has rights, to variable returns from its investment in the investee and has the ability to affect those returns through its power over the investee.

An associate is an entity over which PSPIB has significant influence, as in certain cases, PSPIB does not have control over an investee but has the power to participate in the financial and operating policy decisions of the investee. In such cases, PSPIB determines that it has significant influence over the investee.

In the context of control or significant influence, power over an investee is obtained through voting rights conveyed by PSPIB’s ownership interest, other contractual arrangements, or a combination thereof.

(II) Joint control

PSPIB determines that it is party to a joint venture arrangement when it has joint control over an investee and has rights to the net assets of the investee. Such investees are reported as jointly controlled. Joint control is established through a contractual arrangement which requires the unanimous consent of the parties sharing control for the activities that significantly affect the returns of the arrangement.

Generally, decision-making regarding such activities is governed through voting rights conveyed by the ownership interest of each party. In certain cases, it is governed solely through contractual arrangements or in conjunction with the ownership interest of each party.

(C) Financial instruments

(I) Classification

Financial assets representing investments are managed, together with related financial liabilities, according to the entity’s business model to maximize the rate of return. The performance of such financial instruments is evaluated on a fair value basis and they are classified at fair value through profit or loss (FVTPL). They are described in detail in Note 5(A).

Borrowings, as described under Note 9, are financial liabilities that are designated to be measured at FVTPL since they are part of the portfolios of investments that are managed together and whose performance is evaluated on a fair value basis.

(II) Recognition

Financial assets and financial liabilities are recorded at the date upon which PSPIB becomes a party to the associated contractual provisions. In the case of traded financial assets, they are recorded as of the trade date.

(III) Initial and subsequent measurement

All financial assets and financial liabilities are recorded in the statement of financial position at fair value and continue to be measured as such on a recurring basis. After initial measurement, subsequent changes in the fair value of financial assets and financial liabilities classified at FVTPL are recorded in the statement of changes in net assets available for benefits.

(IV) Derecognition

A financial asset (or, where applicable, a part thereof) is derecognized when the following conditions are met:

- The rights to receive cash flows from the asset have expired, or

- PSPIB has transferred its rights to receive cash flows from the asset or has assumed an obligation to pay the received cash flows to a third party, and

- PSPIB has transferred substantially all the risks and rewards of the asset, or

- In cases where PSPIB has neither transferred nor retained substantially all the risks and rewards of the asset, it has transferred control of the asset

A financial liability is derecognized when the obligation under the liability is discharged, cancelled or expired.

(D) Determination of fair value

Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date.

At initial recognition, PSPIB evaluates the facts and circumstances related to a transaction to confirm that the transaction price represents the fair value of an asset or a liability. At each subsequent reporting date, market prices are used to determine fair value where an active market exists (such as a recognized securities exchange), as they reflect actual and regularly occurring market transactions on an arm’s length basis. If quoted market prices are not available, then fair value is estimated using valuation techniques based on inputs existing at the end of the reporting period that are derived from observable market data.

Valuation techniques are generally applied to investments in private markets, alternative investments, over-the-counter (OTC) derivatives and certain fixed income securities. The values derived from applying these techniques are impacted by the choice of valuation model and the underlying assumptions made concerning factors such as the amounts and timing of future cash flows, discount rates, volatility and credit risk. In certain cases, such assumptions are not supported by market observable data.

The determination of fair value of all financial assets and financial liabilities is described in Note 5.

(E) Foreign currency translation

Foreign currency transactions during the period, including purchases and sales of securities, income and expenses, are translated at the rate of exchange prevailing on the date of the transaction.

Monetary assets and liabilities that are denominated in foreign currencies are translated at the functional currency rate of exchange prevailing at the end of the reporting period.

Foreign currency transaction gains and losses on all monetary assets and liabilities are included in investment income.

(F) Securities lending and securities borrowing and related collateral

PSPIB participates in securities lending and borrowing programs whereby it lends and borrows securities in order to enhance portfolio returns. Lending and borrowing transactions including related collateral under such programs do not transfer the risks or rewards of ownership of the securities to the counterparty. Consequently, PSPIB does not derecognize securities lent or pledged as collateral or recognize securities borrowed or received as collateral. Cash amounts received are recognized as described in Note 5(A) (IX).

The securities lending and borrowing programs require collateral in cash, high-quality debt instruments or securities. Collateral transactions are conducted under terms that are usual and customary in standard securities lending and borrowing programs. PSPIB and its counterparties are authorized to sell, repledge or otherwise use collateral held. The same securities or equivalent securities must be returned to the counterparty at the end of the contract, unless an event of default occurs.

(G) Securities sold under repurchase agreements and purchased under reverse repurchase agreements and related collateral

PSPIB is party to repurchase and reverse repurchase agreements. Such agreements involve the sale of securities by one counterparty with a simultaneous agreement to repurchase such securities at a specified price and at a specified future date.

Securities sold or purchased under the repurchase and reverse repurchase agreements respectively, including related collateral, are not derecognized or recognized as all risks and rewards of ownership related to such securities are not transferred. As such, in the case where PSPIB is the counterparty selling securities under such agreements, all income (loss) related to such securities continues to be reported in investment income, and obligations to repurchase the securities sold are accounted for as investment-related liabilities.

The difference between the fair value of the securities sold and the repurchase price is recorded as interest expense within investment-related expenses. In the case where PSPIB is the counterparty purchasing securities under such agreements, no income (loss) related to such securities is recognized, and obligations to resell the securities are accounted for as investment-related receivables. The difference between the fair value of the securities purchased and resale price is recorded in investment income.

Transactions under repurchase and reverse repurchase agreements involve pledging collateral consisting of cash or securities deemed acceptable by the counterparties. Collateral transactions are conducted under terms that are usual and customary in standard repurchase arrangements. Such terms require the relevant counterparty to pledge additional collateral based on the changes in the fair value of the existing collateral pledged, as well as the related securities sold or purchased. The counterparties are authorized to sell, repledge or otherwise use collateral held. The securities pledged as collateral must be returned to the relevant counterparty at the end of the contract, unless an event of default occurs.

(H) Offsetting of financial instruments

Financial assets and financial liabilities are offset with the net amount reported in the statement of financial position only if PSPIB has a current legally enforceable right to offset the recognized amounts and the intent to settle on a net basis, or to realize the assets and settle the liabilities simultaneously.

(I) Pension obligations

The present value of accrued pension benefits is calculated by the OCA on behalf of the pension plan sponsor, the government, using the projected benefit method prorated on service, based on management’s best estimate of streamed expected rates of return on invested funds for funded pension benefits, and the government’s cost of borrowing derived from the yields on the actual zero-coupon yield curve for Government of Canada bonds, which reflect the timing of the expected future cash flows for unfunded pension benefits.

(J) Investment income

Investment income is made up of interest, dividends, gains (losses) on the disposal of financial assets and financial liabilities, as well as gains (losses) which reflect the change in unrealized appreciation (depreciation) of financial assets held and financial liabilities outstanding at the end of the reporting period. Interest is recognized, on a consistent basis, using the prescribed rates until maturity. Dividends are recognized when the right to receive them has been obtained, generally on the ex-dividend date.

(K) Contributions

Contributions for current service are recorded in the year in which the related payroll costs are incurred. Contributions for past service that are receivable over a period in excess of one year are recorded at the estimated net present value of the contributions to be received.

(L) Benefits earned, benefits paid, and refunds and transfers

Benefits earned are accrued as employees render pensionable services.

The funded and unfunded benefits paid are recognized as a reduction of pension obligations when the payments are made. The funded benefits paid are recognized as a reduction of net assets available for benefits when the payments are made.

Benefit payments, refunds to former members and transfer payments to other plans are recorded in the period in which they are paid.

(M) Investment-related expenses

Investment-related expenses are made up of interest expense, transaction costs, external investment management fees and other (net).

Transaction costs are incremental costs directly attributable to the acquisition, due diligence, issue, or disposal of a financial asset or financial liability, and they are expensed as incurred.

External investment management fees are directly attributable to the external management of assets on behalf of PSPIB. These fees are paid directly by PSPIB and comprise base fees accrued as a percentage of the fair value of the assets managed externally and performance fees accrued as a function of various performance indicators. This excludes amounts not paid directly by PSPIB for certain pooled fund investments classified under alternative investments and for investments in private markets as outlined in Note 18.

(N) Significant accounting judgments, estimates and assumptions

In preparing the financial statements, management makes certain judgments, estimates and assumptions that can affect the amounts reported therein. Significant judgments include those related to the determination of the investment entity status of PSPIB as described in Note 2(A).

Management also makes estimates and assumptions in the measurement, risk assessment and related disclosures surrounding investments in private markets, certain fixed income securities and the pension obligations.

The main assumptions made by management regarding measurement of financial instruments are outlined in Note 5(C) (III), and those regarding the assessment of risk are outlined in Note 7.

The pension obligations are actuarially determined, and the actual experience may differ significantly from the assumptions used in the calculation of the pension obligations. The significant actuarial assumptions used in measuring the pension obligations are found in Note 12.

The economic environment continues to be subject to global uncertainty and heightened geopolitical tensions, which could impact the actuarial assumptions used to measure the present value of the pension obligations and the market value of PSPIB’s portfolio. The pension obligations and the investments held by PSPIB, as at 31 March 2024, as well as the return on investments for the year, reflect the impacts resulting from these events to the extent known and estimable at the reporting date.

Although assumptions reflect management’s best estimates, actual results may differ from such estimates due to the uncertainties involved in using them.

3. Current and future changes in accounting standards

Management has determined that there is no anticipated material impact on the financial statements arising from new standards, amendments and interpretations that have been issued by the IASB but that are not yet effective.

4. Canadian Forces Pension Fund

The government has a statutory obligation to pay benefits relating to the pension plan. This pension obligation is to plan members and their beneficiaries.

In 1999, the pension legislation was amended to allow the government to invest funds in order to provide for the pension obligation. This legislation created the PSPIB to manage and invest amounts that are transferred regularly to it from the CRF related to service since 1 April 2000. The transactions are recorded in the Canadian Forces Pension Fund. The Canadian Forces Pension Fund is a flow through account. At year-end, the balance in the Canadian Forces Pension Fund represents net contributions transferable to the PSPIB, and would also reflect any amounts transferred from the PSPIB. PSPIB investment assets and investment related liabilities are reflected directly in the pension plan’s financial statements.

In order for the government to track the transactions related to contributions, benefit payments, interest and transfers for service prior to 1 April 2000, the government established the Canadian Forces Superannuation Account in the accounts of Canada. The Canadian Forces Superannuation Account has no capacity to pay pensions and is not considered an asset of the pension plan. All cash receipts and disbursements go to or come from the CRF. The details of the transactions of the Canadian Forces Superannuation Account are provided in Note 20.

Related Party—Reserve Force Pension Plan

The Canadian Forces Pension Plan is related, through common legislation (the CFSA), to the Reserve Force Pension Plan. Transactions with the Reserve Force Pension Plan related to member service and contributions are considered to be in the normal course of operations, in accordance with the Section 83 of the Reserve Force Pension Plan Regulations (RFPPR) and are recorded at the exchange amount as required by that section. For the year ended 31 March 2024, $45 million (2023—$73 million) was transferred between the fund accounts. The value of the pensionable service due between the pension plans has been estimated at 31 March 2024 to be $59 million (2023—$61 million).

5. Financial assets and financial liabilities

(A) Classes of financial assets and financial liabilities

Financial assets and financial liabilities are aggregated in the following table, in classes that reflect their respective exposure as well as in investment sectors.

| 2024 | 2023 | |

|---|---|---|

| Investments Public markets |

||

| Canadian equity | $535 | $862 |

| Foreign equity | 8,022 | 6,787 |

| Private markets | ||

| Real estate | 7,106 | 7,914 |

| Private equity | 7,565 | 6,907 |

| Infrastructure | 7,794 | 6,915 |

| Natural resources | 4,154 | 3,590 |

| Fixed income | ||

| Cash and cash equivalentstable 7 note 1 | 677 | 1,346 |

| Money market securitiestable 7 note 1 | 1,617 | 1,604 |

| Government and corporate bonds | 5,150 | 4,466 |

| Inflation-linked bonds | 3,431 | 2,200 |

| Private debt securities | 5,694 | 5,840 |

| Alternative investments | 4,940 | 4,789 |

| Total Investments | $56,685 | $53,220 |

| Investment-related assets | ||

| Amounts receivable from pending trades | $244 | $488 |

| Interest receivable | 121 | 97 |

| Dividends receivable | 52 | 40 |

| Securities purchased under reverse repurchase agreements | 437 | 246 |

| Derivative-related assets | 259 | 423 |

| Total investment-related assets | $1,113 | $1,294 |

| Investments representing financial assets at FVTPLtable 7 note 2 | $57,798 | $54,514 |

| Investment-related liabilities | ||

| Amounts payable from pending trades | $(103) | $(209) |

| Interest payable | (32) | (22) |

| Securities sold short | (613) | (480) |

| Collateral payable | (128) | (184) |

| Securities sold under repurchase agreements | (1,001) | (1,814) |

| Derivative-related liabilities | (187) | (314) |

| Investment-related liabilities representing financial liabilities at FVTPL | $(2,064) | $(3,023) |

| Borrowings | ||

| Capital market debt financing | $(5,158) | $(4,624) |

| Borrowings representing financial liabilities designated at FVTPL | $(5,158) | $(4,624) |

| Net investments | $50,576 | $46,867 |

Table 7 Notes

|

||

(I) Public markets

Public markets consist of Canadian and foreign investments in the following securities: common shares, American depository receipts, global depository receipts, participation notes, preferred shares, income trust units, exchange traded funds units, pooled funds units, and securities convertible into common shares of publicly listed issuers.

Valuation techniques

Direct investments in Canadian and foreign equities are measured at fair value using quoted prices in active markets and are based on the most representative price within the bid-ask spread.

In the case of investments in pooled funds, fair value is measured using unit values obtained from each of the funds’ administrators, which are derived from the fair value of the underlying investments in each pooled fund. PSPIB reviews the fair value received, and where necessary, the impact of restrictions on the sale or redemption of such investments is taken into consideration.

(II) Private markets

Private markets consist of investments in real estate, private equity, infrastructure and natural resources.

Real estate investments are comprised of direct equity positions in various private entities, fund investments, as well as properties in the real estate sector. Real estate investments focus on partnerships, companies and properties operating mainly in the retirement and residential, office, retail, and industrial sectors, as well as private funds invested in real estate assets. Real estate investments are presented net of all third-party financing.

Private equity investments are comprised of fund investments with similar objectives, co-investments in private entities, as well as direct equity positions.

Infrastructure investments are comprised of direct equity positions, fund investments and co-investments in various private entities. Infrastructure investments focus on entities engaged in the management, ownership or operation of assets in energy, transportation and other regulated businesses. Infrastructure investments are presented net of all third-party financing.

Natural resources investments are comprised of direct equity positions, fund investments and co-investments in various private entities. Natural resources investments focus on entities engaged in the management, ownership or operation of assets in timberlands, agriculture and upstream oil and gas. Natural resources investments are presented net of all third-party financing.

Valuation techniques

The process for fair value measurement of private markets investments is described in Note 5(C) (II) and the valuation techniques, together with the significant inputs used, are described in Note 5(C) (III).

(III) Fixed income

Cash and cash equivalents

Cash includes demand deposits with financial institutions.

Cash equivalents include treasury bills, certificates of deposit, bankers’ acceptances and other fixed-income securities with maturities of 90 days or less that are held to meet short-term financial commitments. Such instruments are readily convertible into known amounts of cash and have an insignificant risk of change in value.

Money market securities, bonds and private debt securities

Fixed income consists of money market securities, government and corporate bonds, inflation-linked bonds and private debt securities. Money market securities include instruments having a maximum term to maturity of one year, such as treasury bills, certificates of deposit and bankers’ acceptances.

Government and corporate bonds include Canadian and foreign, federal, provincial, territorial and municipal bonds, floating rate notes, asset-backed term notes and mortgage-backed securities. Inflation-linked bonds are fixed income securities that earn inflation-adjusted returns.

Private debt securities are fixed income securities of private companies held directly or through private funds. Such debt securities take the form of senior debt, mezzanine and distressed debt and primary and secondary investments in leveraged loans. Private debt securities also include third-party loans such as junior and senior debts, construction loans, bridge loans, income-participating loans, as well as other structured finance products in the real estate sector.

Valuation techniques

Treasury bills are valued based on prices obtained from third-party pricing sources. Such prices are determined using the most representative price within a spread of dealer quotations. Certificates of deposit and bankers’ acceptances are recorded at cost plus accrued interest, which approximates their fair value given their short-term nature.

Fair values of government and most corporate bonds, inflation-linked bonds and mortgage-backed securities are based on prices obtained from third-party pricing sources. Such prices are determined using either an appropriate interest rate curve with a spread associated with the credit quality of the issuer or other generally accepted pricing methodologies.

The fair values of certain corporate bonds, private debt securities and asset-backed term notes are determined using valuation techniques. Such techniques, together with the significant inputs used, are described in Note 5(C) (III).

The fair value measurement of fund investments included as part of private debt securities is described in Note 5(C) (II).

(IV) Alternative investments

Alternative investments consist mainly of units of funds that hold a mix of equity, fixed income and derivative instruments, as well as hedge funds.

Valuation techniques

The fair value of these investments is determined based on the fair values reported by the funds’ administrators or general partners and reflects the fair value of the underlying equity, fixed income or derivative instruments, as applicable. PSPIB reviews the fair value received and, where necessary, the impact of restrictions on the sale or redemption of such investments is taken into consideration.

(V) Amounts receivable and payable from pending trades

Amounts receivable from pending trades consist of proceeds on sales of investments, excluding derivative financial instruments, which have been traded but remain unsettled at the end of the reporting period.

Amounts payable from pending trades consist of the cost of purchases of investments, excluding derivative financial instruments, which have been traded but remain unsettled at the end of the reporting period.

Valuation techniques

The fair value of amounts receivable and payable from pending trades reflects the value at which their underlying original sale or purchase transactions were undertaken.

(VI) Interest and dividends receivable

Interest and dividends are recorded at the amounts expected to be received at the end of the reporting period, which due to their short-term maturity, approximates fair value.

(VII) Interest payable

With respect to the borrowings described in Note 5(A) (XI), interest is accrued at the amount expected to be paid at the end of the reporting period, which approximates fair value.

(VIII) Securities sold short

Securities sold short reflect PSPIB’s obligation to purchase securities pursuant to short selling transactions. In such transactions, PSPIB sells securities it does not own with an obligation to purchase similar securities on the market to cover its position.

Valuation techniques

Using quoted market prices that are based on the most representative price within the bid-ask spread, the fair value of securities sold short is measured using the same method as the similar long positions presented within public markets and fixed income.

(IX) Collateral payable

As part of securities lending and certain OTC derivative transactions, when cash is received, it is recognized as collateral payable. The payable balance reflects the obligation of the transferee to return the amount to the transferor at the end of the transaction in the absence of an event of default by the transferor.

(X) Securities sold under repurchase agreements and purchased under reverse repurchase agreements

As described in Note 2(G), PSPIB is party to repurchase and reverse repurchase agreements.

Valuation techniques

Obligations to repurchase or resell the securities sold or purchased under such agreements are recorded at cost plus accrued interest, which due to their short-term maturity, approximates fair value.

(XI) Borrowings under the capital market debt program

PSPIB’s capital market debt program is described in Note 9(B).

Valuation techniques

Short-term promissory notes are recorded at cost plus accrued interest, which due to their short-term maturity, approximates fair value. The fair value of PSPIB’s medium-term notes is based on prices that are obtained from third-party pricing sources. Such prices are determined using an interest rate curve with a spread consistent with PSPIB’s credit quality.

(B) Derivative-related assets and liabilities

Derivative financial instruments are financial contracts that are settled at a future date. The value of such instruments is derived from changes in the value of the underlying assets, interest or exchange rates. Derivative financial instruments do not, typically, require an initial net investment. In certain cases, they require an initial net investment that is less than what would be required to hold the underlying position directly. Derivative financial instruments can be listed or traded OTC. OTC instruments consist of those that are bilaterally negotiated and settled, and those that are cleared (OTC-cleared) by a central clearing party (CCP).

PSPIB uses derivative financial instruments to enhance returns or to replicate investments synthetically. Derivatives are also used to reduce the risk associated with existing investments.

PSPIB uses the following types of derivative financial instruments:

(I) Swaps

Swaps are transactions whereby two counterparties exchange cash flow streams with each other based on predetermined conditions that include a notional amount and a term. Swaps are used to increase returns or to adjust exposures of certain assets without directly purchasing or selling the underlying assets.

(II) Futures

Futures are standardized contracts to take or make delivery of an asset (buy or sell) at a predefined price and predefined future date. Futures are used to adjust exposures to specified assets without directly purchasing or selling the underlying assets.

(III) Forwards

Forwards are contracts involving the sale by one party and the purchase by another party of a predefined amount of an underlying instrument, at a predefined price and at a predefined date in the future. Forwards are used to adjust exposures to specified assets without directly purchasing or selling the underlying assets.

(IV) Options

Options are contracts where the seller gives the purchaser the right, but not the obligation, to buy or sell a given amount of an underlying security, index, commodity, currency, interest rate, credit or other financial instrument, at an agreed-upon price stipulated in advance, either at a determined date or at any time before the predefined maturity date.

(V) Warrants and rights

Warrants are options to purchase an underlying asset which is in the form of a transferable security and which can be listed on an exchange or traded OTC.

Rights are securities giving shareholders entitlement to purchase new shares issued by a corporation at a predetermined price (normally less than the current market price) in proportion to the number of shares already owned. Rights are issued only for a short period of time, after which they expire.

Valuation techniques

(i) Determination of fair value of derivative financial instruments

Listed derivative financial instruments are recorded at fair value using quoted market prices that are based on the most representative price within the bid-ask spread. OTC-cleared derivatives are recorded at fair value using prices obtained from the CCP. OTC derivatives are valued using appropriate valuation techniques such as discounted cash flows. These techniques use significant inputs that are observable in the market such as current market yields.

(ii) Notional values and fair values of derivative-related assets and liabilities

Notional values of derivative financial instruments are not recorded as assets or liabilities as they represent the face amount of the contract. Except for credit derivatives, notional values do not represent the potential gain or loss associated with the market or credit risk of such transactions disclosed below. Rather, they serve as the basis upon which the cash flows and the fair value of the contracts are determined.

| 2024 | 2023 | |||||

|---|---|---|---|---|---|---|

| Notional value | Fair value | Notional value | Fair value | |||

| Assets | Liabilities | Assets | Liabilities | |||

| Equity and commodity derivatives | ||||||

| Listed: Futures | $1,071 | $0 | $0 | $710 | $0 | $0 |

| Listed: Options: Purchased | 30 | 0 | 0 | 175 | 6 | 0 |

| Written | 0 | 0 | 0 | 230 | 0 | (3) |

| OTC | ||||||

| Swaps | 4,256 | 94 | (41) | 3,979 | 127 | (44) |

| Options: Purchased | 0 | 0 | 0 | 16 | 0 | 0 |

| Currency derivatives | ||||||

| Listed: Futures | 72 | 0 | 0 | 44 | 0 | 0 |

| OTC | ||||||

| Forwards | 11,191 | 42 | (66) | 20,670 | 136 | (160) |

| Swaps | 236 | 0 | (6) | 686 | 17 | (6) |

| Options: Purchased | 174 | 1 | 0 | 396 | 2 | 0 |

| Written | 202 | 0 | (1) | 512 | 0 | (2) |

| Interest rate derivatives | ||||||

| Listed: Futures | 2,080 | 0 | 0 | 423 | 0 | 0 |

| Listed: Options: Purchased | 7,994 | 4 | 0 | 9,334 | 1 | 0 |

| Written | 8,255 | 0 | (3) | 8,548 | 0 | (1) |

| OTC | ||||||

| Forwards | 153 | 0 | (1) | 272 | 2 | (1) |

| Swaps | 467 | 1 | (4) | 670 | 6 | (3) |

| Options: Purchased | 10,247 | 114 | 0 | 12,623 | 123 | 0 |

| Written | 13,315 | 0 | (62) | 14,735 | 0 | (92) |

| OTC‑cleared | ||||||

| Swaps | 12,591 | 0 | 0 | 15,559 | 0 | 0 |

| Credit derivatives | ||||||

| OTC | ||||||

| Credit default swaps: | ||||||

| Purchased | 119 | 0 | (3) | 108 | 0 | (2) |

| Writtentable 8 note 1 | 382 | 3 | 0 | 232 | 3 | 0 |

| OTC-cleared | ||||||

| Credit default swaps: | ||||||

| Purchased | 565 | 0 | 0 | 389 | 0 | 0 |

| Total | - | $259 | $(187) | - | $423 | $(314) |

Table 8 Note

|

||||||

| 2024 | 2023 | |||||

|---|---|---|---|---|---|---|

| Notional value | Fair value | Notional value | Fair value | |||

| Assets | Liabilities | Assets | Liabilities | |||

| Listed derivatives | $19,452 | $4 | $(3) | $19,464 | $7 | $(4) |

| OTC derivatives | 40,742 | 255 | (184) | 54,899 | 416 | (310) |

| OTC-cleared derivatives | 13,156 | 0 | 0 | 15,948 | 0 | 0 |

| Total | - | $259 | $(187) | - | $423 | $(314) |

| 2024 | 2023 | |

|---|---|---|

| Less than 3 months | $32,936 | $44,180 |

| 3 to 12 months | 21,558 | 28,656 |

| Over 1 year | 18,856 | 17,475 |

(C) Fair value hierarchy

(I) Classification

Financial assets and financial liabilities described under Note 5(A) are classified within the fair value hierarchy, described as follows, based on the lowest level of input that is significant to the fair value measurement as a whole.

- Level 1 inputs are quoted prices (unadjusted) in active markets for identical assets or liabilities that PSPIB can access at the end of the reporting period

- Level 2 inputs are inputs other than quoted prices included within Level 1 that are observable for the asset or the liability, either directly or indirectly. Level 2 inputs include:

- quoted prices for similar assets or liabilities in active markets

- quoted prices for identical or similar assets or liabilities in markets that are not active

- inputs other than quoted prices that are observable for the asset or liability

- market-corroborated inputs

- Level 3 inputs are unobservable inputs for the asset or liability that are used within model-based techniques. They reflect PSPIB’s assessment of the assumptions that market participants would use in pricing the assets or liabilities

The classification within the levels of the hierarchy is established at the time of the initial determination of fair value of the asset or liability and reviewed at the end of each reporting period. PSPIB determines whether a transfer between levels has occurred and recognizes such transfers at the beginning of the reporting period.

| Level 1 | Level 2 | Level 3 | Total fair value | |

|---|---|---|---|---|

| Investments Public markets |

||||

| Canadian equity | $185 | $350 | $0 | $535 |

| Foreign equity | 7,478 | 98 | 446 | 8,022 |

| Private markets | ||||

| Real estate | 0 | 0 | 7,106 | 7,106 |

| Private equity | 0 | 0 | 7,565 | 7,565 |

| Infrastructure | 0 | 0 | 7,794 | 7,794 |

| Natural resources | 0 | 0 | 4,154 | 4,154 |

| Fixed income | ||||

| Cash and cash equivalents | 256 | 421 | 0 | 677 |

| Money market securities | 1,487 | 130 | 0 | 1,617 |

| Government and corporate bonds | 1,329 | 3,820 | 1 | 5,150 |

| Inflation-linked bonds | 3,410 | 21 | 0 | 3,431 |

| Private debt securities | 0 | 0 | 5,694 | 5,694 |

| Alternative investments | 0 | 3,030 | 1,910 | 4,940 |

| Total investments | $14,145 | $7,870 | $34,670 | $56,685 |

| Investment-related assets | ||||

| Amounts receivable from pending trades | $0 | $244 | $0 | $244 |

| Interest receivable | 0 | 121 | 0 | 121 |

| Dividends receivable | 0 | 52 | 0 | 52 |

| Securities purchased under reverse repurchase agreements | 0 | 437 | 0 | 437 |

| Derivative-related assets | 4 | 255 | 0 | 259 |

| Total investment-related assets | $4 | $1,109 | $0 | $1,113 |

| Investments representing financial assets at FVTPL | $14,149 | $8,979 | $34,670 | $57,798 |

| Investment-related liabilities | ||||

| Amounts payable from pending trades | $0 | $(103) | $0 | $(103) |

| Interest payable | 0 | (32) | 0 | (32) |

| Securities sold short | (613) | 0 | 0 | (613) |

| Collateral payable | 0 | (128) | 0 | (128) |

| Securities sold under repurchase agreements | 0 | (1,001) | 0 | (1,001) |

| Derivative-related liabilities | (3) | (184) | 0 | (187) |

| Investment-related liabilities representing financial liabilities at FVTPL | $(616) | $(1,448) | $0 | $(2,064) |

| Borrowings | ||||

| Capital market debt financing | $0 | $(5,158) | $0 | $(5,158) |

| Borrowings representing financial liabilities designated at FVTPL | $0 | $(5,158) | $0 | $(5,158) |

| Net investments | $13,533 | $2,373 | $34,670 | $50,576 |

| Level 1 | Level 2 | Level 3 | Total fair value | |

|---|---|---|---|---|

| Investments Public markets |

||||

| Canadian equity | $529 | $333 | $0 | $862 |

| Foreign equity | 6,400 | 199 | 188 | 6,787 |

| Private markets | ||||

| Real estate | 0 | 0 | 7,914 | 7,914 |

| Private equity | 0 | 0 | 6,907 | 6,907 |

| Infrastructure | 0 | 0 | 6,915 | 6,915 |

| Natural resources | 0 | 0 | 3,590 | 3,590 |

| Fixed income | ||||

| Cash and cash equivalentstable 12 note 1 | 635 | 711 | 0 | 1,346 |

| Money market securitiestable 12 note 1 | 1,459 | 145 | 0 | 1,604 |

| Government and corporate bonds | 1,563 | 2,902 | 1 | 4,466 |

| Inflation-linked bonds | 2,200 | 0 | 0 | 2,200 |

| Private debt securities | 0 | 0 | 5,840 | 5,840 |

| Alternative investments | 0 | 2,963 | 1,826 | 4,789 |

| Total investments | $12,786 | $7,253 | $33,181 | $53,220 |

| Investment-related assets | ||||

| Amounts receivable from pending trades | $0 | $488 | $0 | $488 |

| Interest receivable | 0 | 97 | 0 | 97 |

| Dividends receivable | 0 | 40 | 0 | 40 |

| Securities purchased under reverse repurchase agreements | 0 | 246 | 0 | 246 |

| Derivative-related assets | 7 | 416 | 0 | 423 |

| Total investment-related assets | $7 | $1,287 | $0 | $1,294 |

| Investments representing financial assets at FVTPL | $12,793 | $8,540 | $33,181 | $54,514 |

| Investment-related liabilities | ||||

| Amounts payable from pending trades | $0 | $(209) | $0 | $(209) |

| Interest payable | 0 | (22) | 0 | (22) |

| Securities sold short | (449) | (31) | 0 | (480) |

| Collateral payable | 0 | (184) | 0 | (184) |

| Securities sold under repurchase agreements | 0 | (1,814) | 0 | (1,814) |

| Derivative-related liabilities | (4) | (310) | 0 | (314) |

| Investment-related liabilities representing financial liabilities at FVTPL | $(453) | $(2,570) | $0 | $(3,023) |

| Borrowings | ||||

| Capital market debt financing | $0 | $(4,624) | $0 | $(4,624) |

| Borrowings representing financial liabilities designated at FVTPL | $0 | $(4,624) | $0 | $(4,624) |

| Net investments | $12,340 | $1,346 | $33,181 | $46,867 |

Table 12 Note

|

||||