Quarterly Financial Report - For the quarter ended December 31, 2022

Table of contents

1 Introduction

This quarterly financial report should be read in conjunction with the 2022-23 Main Estimates, the 2022-23 Supplementary Estimates (A) and the 2022-23 Supplementary Estimates (B). This report has been prepared by management as required by section 65.1 of the Financial Administration Act and in the form and manner prescribed by the Treasury Board. It has not been subject to an external audit or review.

1.1 Authority, mandate and programs

Shared Services Canada (SSC) is responsible for digitally enabling government programs and services by providing information technology (IT) services in the domains of networks and network security, data centers and cloud offerings, digital communications and providing IT tools that the public service needs to do its job. As a service provider to over 40 government departments and agencies, SSC is focussed on moving toward an IT service delivery model that encourages sharing common solutions and platforms across departments in an effort to reduce the variety of IT solutions across the government. In taking this enterprise approach, SSC is working to solidify network capacity and security, equip and empower employees to collaborate, and support partners in the design and delivery of their digital service offering to Canadians. The Minister of Public Services and Procurement Canada is the Minister responsible for Shared Services Canada.

In carrying out its mandate, SSC is supporting the Digital Operations Strategic Plan: 2021-2024 and the Government of Canada Cloud Adoption Strategy, as well as working in partnership with public and private sector stakeholders, implementing enterprise-wide approaches for managing IT infrastructure services, and employing effective and efficient business management processes.

The Shared Services Canada Act and related Orders-in-Council set out the powers, duties and functions of the Minister responsible for SSC. Amendments to the Act in June 2017 allow the Minister to delegate to other Ministers the power to procure certain items, thereby making it easier for federal departments to buy some of the most frequently purchased IT goods and services. SSC remains responsible for setting up IT contracts, standing offers and supply arrangements, and will continue to ensure only trusted IT equipment and software are used. The Minister responsible for SSC may also, in exceptional circumstances, authorize another Minister to obtain services from within their own department or from a source other than SSC. However, this authorization cannot be used to exempt the entire department from using SSC’s services.

Further details on SSC’s authority, mandate, responsibilities and programs may be found in the 2022-23 Main Estimates and in SSC’s 2022-23 Departmental Plan.

1.2 Basis of presentation

This quarterly financial report has been prepared by management using an expenditure basis of accounting. The accompanying statement of authorities includes the department's spending authorities granted by Parliament, and those used by the department consistent with the 2022-23 Main Estimates, the 2022-23 Supplementary Estimates (A), the 2022-23 Supplementary Estimates (B) and the 2021-22 Carry Forward. This quarterly report has been prepared using a special purpose financial reporting framework designed to meet financial information needs with respect to the use of spending authorities.

The authority of Parliament is required before money can be spent by the government. Approvals are given in the form of annually approved limits through appropriation acts or through legislation in the form of statutory spending authority for specific purposes.

When Parliament is dissolved for the purposes of a general election, section 30 of the Financial Administration Act authorizes the Governor General, under certain conditions, to issue a special warrant authorizing the government to withdraw funds from the Consolidated Revenue Fund. A special warrant is deemed to be an appropriation for the fiscal year in which it is issued.

The department uses the full accrual method of accounting to prepare and present its annual departmental financial statements that are part of the departmental results reporting process. However, the spending authorities voted by Parliament remain on an expenditure basis. The main difference between the quarterly financial report and the departmental financial statements is the timing of when revenues and expenses are recognized. The quarterly financial report presents revenues only when the money is received and expenses only when the money is paid out. The departmental financial statements report revenues when they are earned and expenses when they are incurred. In the latter case, revenues are recorded even if cash has not been received and expenses are incurred even if cash has not yet been paid out.

1.3 Shared Services Canada financial structure

SSC has a financial structure composed mainly of voted budgetary authorities, namely Vote 1 - Operating expenditures, including Vote netted revenues, and Vote 5 - Capital expenditures, including Vote netted revenues. The statutory authorities consist of contributions to the Employee Benefit Plan (EBP).

At the end of the third quarter of 2022-23, 93% of the department’s budget was devoted to supporting its IT consolidation and standardization goals. This ensured that current and future IT infrastructure services offered to the Government of Canada are maintained in an environment of operational excellence. The remaining 7% was devoted to internal services, which are services in support of SSC’s programs and/or required to meet SSC’s corporate obligations.

Total Vote netted revenue authority for 2022-23 is $861.2 million, which consists of respendable revenue for IT infrastructure services provided by SSC to organizations on a cost-recovery basis.

2 Highlights of fiscal quarter and fiscal year-to-date results

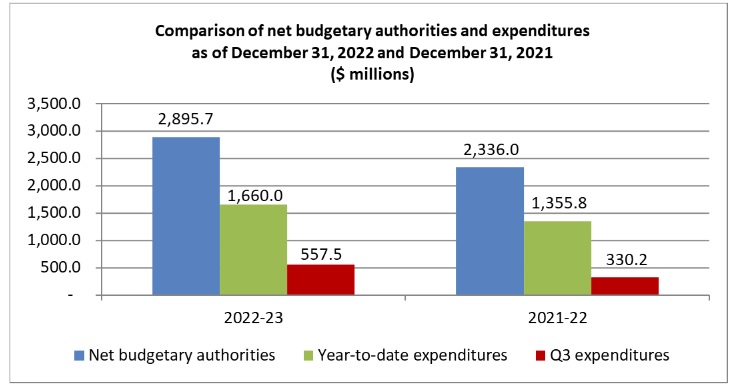

The following graph provides a comparison of the net budgetary authorities available for spending, the year-to-date expenditures, and the expenditures for the quarters ended December 31, 2022, and December 31, 2021, for the department’s combined Vote 1 - Operating expenditures, Vote 5 - Capital expenditures, and statutory authorities.

Text description – Comparison of net budgetary authorities and expenditures

The graph shows total net budgetary authorities available for spending of $2,895.7 million as of December 31, 2022 and $2,336.0 million as of December 31, 2021. It also shows year-to-date expenditures totalling $1,660.0 million as of December 31, 2022 compared to $1,355.8 million as of December 31, 2021. Finally, it shows total expenditures of $557.5 million for the third quarter ended December 31, 2022 compared to $330.2 million for the third quarter ended December 31, 2021.

2.1 Significant changes to authorities

For the period ended December 31, 2022, the authorities available to the department include the Main Estimates, the Supplementary Estimates (A), the Supplementary Estimates (B) and the 2021-22 Carry Forward. Authorities available for spending in 2022-23 are $2,895.7 million at the end of the third quarter, compared to $2,336.0 million at the end of the third quarter of 2021-22, representing an increase of $559.7 million, or 24.0%. This total increase is a combination of an increase of $448.4 million in Vote 1 – Gross operating expenditures, an increase of $19.1 million in Vote 5 – Gross capital expenditures, a decrease in Vote netted revenues of $88.8 million and an increase in Budgetary statutory authorities (EBP) of $3.4 million.

| Net authorities available ($ millions) | 2022-23 | 2021-22 | Variance |

|---|---|---|---|

| Vote 1 - Operating expenditures | 3,215.5 | 2,767.1 | 448.4 |

| Vote 5 - Capital expenditures | 423.7 | 404.6 | 19.1 |

| Statutory (EBP) | 117.7 | 114.3 | 3.4 |

| Total gross authorities | 3,756.9 | 3,286.0 | 470.9 |

| Vote netted revenues | (861.2) | (950.0) | 88.8 |

| Total net authorities | 2,895.7 | 2,336.0 | 559.7 |

Vote 1 – Gross operating expenditures

The department’s Vote 1 increased by $448.4 million, compared to the third quarter of 2021-22, mainly due to:

- an increase of $208.4 million related to the following projects and initiatives:

- incremental cost of providing core IT services to client departments and agencies ($65.9 million)

- Next Generation Human Resources and Pay Solution ($63.2 million)

- Service Integrity Mission-Critical Projects ($44.7 million)

- Cyber and Information Technology Security ($33.9 million)

- Operating Budget Carry Forward ($0.7 million)

- a net increase of $177.7 million related to the implementation of various Budget 2021 initiatives:

- Workload Modernization and Migration Program ($101.2 million)

- Network Modernization and Implementation Fund ($40.5 million)

- Secure Cloud Enablement and Defence Evolution and Departmental Connectivity ($36.0 million)

- a net increase of $158.8 million related to the department’s implementation of the IT Enterprise Service Model

- a net increase of $35.6 million due to a realignment of funding authority from Vote 5 to Vote 1

- a decrease of $88.8 million related to the decrease in Vote netted revenues in 2022-23

- a decrease of $43.3 million related to the following projects and initiatives:

- Workload Migration and Cloud Architecture Programs ($22.1 million)

- other projects and initiatives ($20.0 million)

- collective agreements and other compensation adjustments ($1.2 million)

Vote 5 – Gross capital expenditures

The department’s Vote 5 increased by $19.1 million, compared to the third quarter of 2021-22, mainly due to:

- an increase of $85.9 million related to the implementation of various Budget 2021 initiatives:

- Workload Modernization and Migration Program ($65.7 million)

- Network Modernization and Implementation Fund ($20.2 million)

- an increase of $4.0 million related to other projects and initiatives

- a net decrease of $35.6 million due to a realignment of funding authority from Vote 5 to Vote 1

- a decrease of $35.2 million related to the following projects and initiatives:

- Workload Migration and Cloud Architecture Programs ($21.9 million)

- Cyber and Information Technology Security ($7.9 million)

- Capital Budget Carry Forward ($5.4 million)

Vote netted revenues

The department’s Vote netted revenues (VNR) authority decreased by $88.8 million compared to the third quarter of 2021-22. At the end of 2021-22, SSC’s VNR authority was $950.0 million, compared to the total authority of $861.2 million at the end of the third quarter of 2022-23. SSC’s VNR authority at the end of the third quarter of 2022-23 is lower than the 2021-22 year-end VNR authority due to the implementation of the IT Enterprise Service Model.

Statutory (EBP)

The department’s EBP authority increased by $3.4 million, compared to the third quarter of 2021-22, mainly due to:

- an increase of $3.4 million related to other projects and initiatives

2.2 Explanations of significant variances from previous year expenditures

Compared to the previous year, the total net year-to-date expenditures for the period ended December 31, 2022, have increased by $304.2 million, from $1,355.8 million to $1,660.0 million as per the table below. This represents an increase of 22.4% against expenditures recorded for the same period in 2021-22.

| Net year-to-date expenditures ($ millions) | 2022-23 | 2021-22 | Variance |

|---|---|---|---|

| Vote 1 - Operating expenditures | 1,847.5 | 1,660.7 | 186.8 |

| Vote 5 - Capital expenditures | 145.2 | 97.6 | 47.6 |

| Statutory (EBP) | 88.3 | 72.3 | 16.0 |

| Total gross year-to-date expenditures | 2,081.0 | 1,830.6 | 250.4 |

| Vote netted revenues | (421.0) | (474.8) | 53.8 |

| Total net year-to-date expenditures | 1,660.0 | 1,355.8 | 304.2 |

Vote 1 - Increase of $186.8 million

The net increase in operating expenditures, compared to the third quarter of 2021-22, is mainly attributed to:

- transportation and communications expenditures increased by $58.6 million. This increase is mainly attributable to expenditures related to data and voice communications services.

- rentals expenditures increased by $45.8 million. This increase is mainly attributable to expenditures for licence and maintenance fees for software.

- repair and maintenance expenditures increased by $45.7 million. This increase is mainly attributable to expenditures in repair and maintenance of computer equipment as well as repair and maintenance of office buildings.

- personnel expenditures increased by $30.0 million. This is mainly due to an increase in the number of SSC employees in 2022-23. This increase is partially offset by a decrease related to payments in 2021-22 of retroactive pay and compensation related to the Phoenix pay system.

- increase of $6.7 million in other various expenditures.

Vote 5 - Increase of $47.6 million

The net increase in capital expenditures, compared to the third quarter of 2021-22, is mainly attributed to:

- acquisitions of machinery and equipment increased by $32.1 million. This is mainly due to an increase in expenditures related to the acquisitions of computer equipment.

- acquisitions of land, buildings and works increased by $13.1 million. This is mainly due to a payment to IBM Canada Ltd for leasehold improvements to supercomputer facilities.

- increase of $2.4 million in other various expenditures.

Vote netted revenues - Decrease of $53.8 million

The decrease in the collected Vote netted revenues, compared to the third quarter of 2021-22, is mainly due to the implementation of the IT Enterprise Service Model, Part A services, that has appropriated services in 2022-23 that were previously cost recovered as Vote netted revenues.

3 Risks and uncertainty

As the collective public service and Shared Services Canada look to a post-pandemic world—one in which employees across the Government of Canada will need to be supported with the enterprise tools and network infrastructure critical for the delivery of government programs and services—there are certain risk exposures and emerging trends that could potentially impact departmental outcomes. Namely, the unprecedented transition to a mix of in-office and telework arrangements will likely bring unique risks related to the organizational management and engagement of employees; the effective management of complex enterprise IT projects to continue digital transformation; and increasing and sophisticated cybersecurity incidents exacerbated by increasing reliance on digital services. Looking to external factors, Shared Services Canada is operating within a continually evolving landscape, including global supply chain disruptions, shifting global socio-economic, political and/or environmental conditions, and the ever-changing industry standards and best practices related to IT service delivery.

Considering the host of internal and external risks, the department strives to employ best practice Enterprise Risk Management and Operational Risk Management methodology throughout its project and program operations, internal services and financial governance activities. Shared Services Canada promotes a risk-informed culture through the Corporate Risk Management division, whereby the function continuously seeks to strengthen the department’s risk management processes and procedures, systems, governance structures, service delivery model, tools, analytics capacity and controls to ensure high standards of practice. Within this context, Shared Services Canada has also revised its Enterprise Risk Profile to capture the foremost risk exposures faced by the organization and to ensure strategic alignment with its enterprise approach and the Digital Operations Strategic Plan: 2021-2024.

Further, an Integrated Business Planning framework has been developed to effectively drive a consolidated vision to mature strategic planning and reporting to ensure the fulfillment of key priorities and interweave risk management methodology through all facets of the organization. The department has also undertaken several initiatives related to proactive workforce resourcing strategies to retain, recruit and train personnel and provide progressive mental health resources to support employees throughout the COVID-19 pandemic. Lastly, Shared Services Canada promotes effective financial management practices and financial sustainability to ensure that it has the financial resources, systems and funding mechanisms in place to maintain and enhance mission-critical systems while funding modernization initiatives.

The Key Enterprise Risks can be found in SSC’s 2022-23 Departmental Plan.4 Significant changes in relation to operations, personnel and programs

On November 14, 2022, Scott Davis was appointed Assistant Deputy Minister and Chief Financial Officer, to replace Samantha Hazen who left SSC on November 25, 2022.

Approval by senior officials

Original signed by

Sony Perron

President

Original signed by

Scott Davis, CPA

Assistant Deputy Minister and Chief Financial Officer

Ottawa, Canada

February 17, 2023

5 Statement of authorities (unaudited) (in thousands of dollars)

| Fiscal year 2022-23 | Fiscal year 2021-22 | |||||

|---|---|---|---|---|---|---|

| Total available for use for the year ending March 31, 2023Footnote * | Used during the quarter ended December 31, 2022 | Year-to-date used at quarter-end | Total available for use for the year ending March 31, 2022Footnote * | Used during the quarter ended December 31, 2021 | Year-to-date used at quarter-end | |

| Vote 1 - Operating expenditures | ||||||

| Gross operating expenditures | 3,215,496 | 647,599 | 1,847,569 | 2,767,052 | 580,901 | 1,660,746 |

| Vote netted revenues | (791,215) | (171,896) | (419,778) | (880,000) | (319,912) | (474,803) |

| Net operating expenditures | 2,424,281 | 475,703 | 1,427,791 | 1,887,052 | 260,989 | 1,185,943 |

| Vote 5 - Capital expenditures | ||||||

| Gross capital expenditures | 423,729 | 53,613 | 145,158 | 404,619 | 44,236 | 97,573 |

| Vote netted revenues | (70,000) | (1,237) | (1,237) | (70,000) | – | – |

| Net capital expenditures | 353,729 | 52,376 | 143,921 | 334,619 | 44,236 | 97,573 |

| (S) Contributions to employee benefit plan | 117,709 | 29,427 | 88,282 | 114,344 | 24,972 | 72,308 |

| Total budgetary authorities | 2,895,719 | 557,506 | 1,659,994 | 2,336,015 | 330,197 | 1,355,824 |

6 Departmental budgetary expenditures by standard object (unaudited) (in thousands of dollars)

| Fiscal year 2022-23 | Fiscal year 2021-22 | |||||

|---|---|---|---|---|---|---|

| Planned expenditures for the year ending March 31, 2023Note de bas de page * | Expended during the quarter ended December 31, 2022 | Year-to-date used at quarter-end | Planned expenditures for the year ending March 31, 2022Note de bas de page * | Expended during the quarter ended December 31, 2021 | Year-to-date used at quarter-end | |

| Expenditures: | ||||||

| Personnel (includes EBP) | 920,151 | 248,404 | 703,274 | 883,413 | 221,369 | 657,064 |

| Transportation and communications | 843,469 | 147,784 | 375,811 | 828,845 | 127,826 | 316,397 |

| Information | 3,991 | 253 | 643 | 2,237 | 720 | 1,120 |

| Professional and special services | 476,290 | 114,036 | 268,665 | 358,422 | 110,910 | 261,790 |

| Rentals | 622,105 | 82,869 | 377,906 | 540,303 | 85,554 | 332,722 |

| Repair and maintenance | 266,923 | 61,481 | 169,313 | 215,408 | 43,310 | 121,332 |

| Utilities, materials and supplies | 9,842 | 1,223 | 3,226 | 11,625 | 1,159 | 2,869 |

| Acquisition of land, buildings and works | 11,705 | 946 | 15,832 | 14,438 | 912 | 2,710 |

| Acquisition of machinery and equipment | 594,185 | 79,478 | 164,352 | 424,290 | 55,743 | 125,455 |

| Transfer payments | – | – | – | – | – | – |

| Public debt charges | 8,177 | 1,993 | 6,244 | 5,654 | 2,471 | 6,431 |

| Other subsidies and payments | 96 | (7,828) | (4,257) | 1,380 | 135 | 2,737 |

| Total gross budgetary expenditures | 3,756,934 | 730,639 | 2,081,009 | 3,286,015 | 650,109 | 1,830,627 |

| Less revenues netted against expenditures: | ||||||

| Vote netted revenues | 861,215 | 173,133 | 421,015 | 950,000 | 319,912 | 474,803 |

| Total revenues netted against expenditures | 861,215 | 173,133 | 421,015 | 950,000 | 319,912 | 474,803 |

| Total net budgetary expenditures | 2,895,719 | 557,506 | 1,659,994 | 2,336,015 | 330,197 | 1,355,824 |

7 Glossary

- Appropriations/Authorities

-

Expenditure authorities are approvals from Parliament for individual government organizations to spend up to specific amounts. Expenditure authority is provided in two ways: annual appropriation acts that specify the amounts and broad purposes for which funds can be spent; and other specific statutes that authorize payments and set out the amounts and time periods for those payments. The amounts approved in appropriation acts are referred to as voted amounts, and the expenditure authorities provided through other statutes are called statutory authorities.

-

Vote 1 - Operating expenditures

A vote that covers most day-to-day expenses, such as salaries, utilities and minor capital expenditures.

-

Vote 5 - Capital expenditures

Capital expenditures are those made for the acquisition or development of items that are classified as tangible capital assets as defined by government accounting policies. This vote is generally used for capital expenditures that exceed $10,000.

-

- Capital Budget Carry Forward

-

Treasury Board centrally managed vote that permits departments to bring forward eligible lapsing funds from one fiscal year to the next in an amount up to 20% of their year-end allotments in the capital expenditures Vote as reflected in Public Accounts.

- Cash method of accounting

-

The cash method recognizes revenues when they are received and expenses when they are paid for.

- Collective agreement

-

A collective agreement means an agreement in writing entered into under the Public Service Staff Relations Act between the employer and a bargaining agent and containing provisions covering terms and conditions of employment and related matters.

- Departmental Plan

-

The Departmental Plan is an expenditure plan for each department and agency (excluding Crown corporations). It describes departmental priorities, expected results and associated resource requirements covering a three-year period, beginning with the year indicated in the title of the report.

- Employee Benefit Plan (EBP)

-

A statutory item that includes employer contributions for the Public Service Superannuation Plan, the Canada and the Quebec Pension Plans, Death Benefits, and the Employment Insurance accounts. Expressed as a percentage of salary, the EBP rate is changed every year as directed by the Treasury Board Secretariat.

- Expenditure basis of accounting

-

An accounting method that combines elements of the two major accounting methods: the cash method and the accrual method. The expenditure basis of accounting method recognizes revenues when cash is received and expenses when liabilities are incurred or cash is paid out.

- Frozen allotments

-

Frozen allotments are used to prohibit the spending of funds previously appropriated by Parliament. There are two types of frozen allotments:

- permanent: where the Treasury Board has directed that funds lapse at the end of the fiscal year

- temporary: where an appropriation is frozen until such time as conditions have been met

- Full accrual method of accounting

-

An accounting method that measures the performance and position of an organization by recognizing economic events regardless of when cash transactions occur. Therefore, the full accrual method of accounting recognizes revenues when they are earned (for example, when the terms of a contract are fulfilled) and expenses when they are incurred.

- Main Estimates

-

Each year, the government prepares estimates in support of its request to Parliament for authority to spend public funds. This request is formalized through the introduction of appropriation bills in Parliament. In support of the Appropriation Act, the Main Estimates identify the spending authorities (Votes) and amounts to be included in subsequent appropriation bills. Parliament is asked to approve these Votes to enable the government to proceed with its spending plans.

- Operating Budget Carry Forward

-

Treasury Board centrally managed vote that permits departments to bring forward eligible lapsing funds from one fiscal year to the next in an amount up to 5% of their Main Estimates gross operating budget allotment.

- Standard objects

-

A system in accounting that classifies and summarizes expenditures by category, such as type of goods or services acquired, for monitoring and reporting.

- Supplementary Estimates

-

The President of the Treasury Board tables up to 3 Supplementary Estimates usually in May, in late October or early November and in February to obtain the authority of Parliament to adjust the government's expenditure plan set out in the estimates for that fiscal year. Supplementary Estimates serve two purposes. First, they seek authority for revised spending levels that Parliament will be asked to approve in an Appropriation Act. Second, they provide Parliament with information on changes in the estimated expenditures to be made under the authority of statutes previously passed by Parliament. Each Supplementary Estimates document is identified alphabetically (A, B and C).

- Vote netted revenues authority

-

The authority by which Shared Services Canada has permission to collect and spend revenue earned and collected from the provision of IT services within the government.