Parliamentary committee appearance binder for the Comptroller General of Canada before the Standing Committee on Public Accounts (PACP) on November 18 and 22nd, 2022 regarding the Public Accounts of Canada 2022

Notice to readers

This report contains either personal or confidential information, or information related to security, which has been redacted in accordance with the Access to Information Act.

On this page

Meeting Agenda and PAC Membership

A. Summary on Public Accounts 2022

Public Accounts 2022

Issue / Question:

The Public Accounts of Canada for fiscal year 2021-2022 were tabled in Parliament by the President of the Treasury Board in October 2022.

Suggested Response:

- The Government of Canada is committed to responsible financial management and oversight.

- The Public Accounts include the audited consolidated financial statements of the Government.

- For the 24th year in a row, the Government of Canada received a clean audit opinion on its consolidated financial statements.

- This demonstrates the high quality of Canada's financial reporting.

Background:

- Production and finalization of the Public Accounts of Canada is a joint responsibility between the Receiver General, the Office of the Comptroller General and the Department of Finance.

- The Public Accounts reflect the Government’s audited consolidated financial statements and other detailed financial information for the fiscal year 2021-2022 that ended March 31, 2022.

- Volume I – includes the audited consolidated financial statements of the Government; the unmodified audit report from the Auditor General; a financial statements discussion and analysis, which presents 10-year comparative financial information; as well as details on certain financial statement components.

- Volume II – includes financial operations of the departments, including the reconciliations of authorities granted and spent.

- Volume III – includes other supplementary information such as losses, claims against the Crown, ex gratia payments and Ministers’ Office expenditures.

- The Auditor General also simultaneously tables in Parliament, through the Speaker of the House, her observations on key financial audits. This year's observations focus on the pandemic measures enacted by the government, pay administration and National Defence's inventory and asset pooled items.

- The Public Accounts are tabled in the House of Commons and undergo a review by the Public Accounts Committee.

- The Public Accounts show a deficit of $90.2B compared to the projected $154.7B deficit in Budget 2021. To note, Budget 2022 revised the projection to $113.8B.

B. Opening remarks

Notes for remarks by Roch Huppé, Comptroller General of Canada, at the Standing Committee on Public Accounts

October 2022

Ottawa

Check against delivery

Introduction

Thank you, Mr. Chair, and members of the Committee.

I’m pleased to have the opportunity to discuss the Public Accounts of Canada 2022.

Before I begin, I would like to acknowledge that I am speaking here today from the traditional unceded territory of the Algonquin Anishnaabeg People.

I am joined by two of my colleagues from the Treasury Board of Canada Secretariat:

- Monia Lahaie, Assistant Comptroller General of the Financial Management Sector; and

- Diane Peressini, Executive Director, Government Accounting Policy, and Reporting.

- As this committee knows, the Public Accounts include the audited consolidated financial statements for the 2021- 2022 fiscal year, which ended on March 31, 2022, in addition to other unaudited financial information.

I’m pleased to note that, for the 24th consecutive year, the Auditor General has issued an unmodified or “clean” audit opinion on these financial statements.

I would like to thank the financial management community of the Government of Canada, the Department of Finance and the Receiver General, and the Office of the Auditor General for helping prepare the Public Accounts.

Highlights

Let me now turn to some of the highlights in this year’s documents.

Total revenues in these Public Accounts amounted to $413.3 billion in 2022, which represents an increase of $96.8 billion, or 30.6%, from 2021.

Total expenses amounted to $503.5 billion in 2022, which is down $140.7 billion, or 21.8%, from 2021.

As expected, the pandemic continues to have a significant impact on the financial statements.

The total impact of the key COVID-19 response measures on fiscal year 2022 is estimated at over $70 billion.

These include:

- The Canada Emergency Wage Subsidy at $22.3 billion;

- The Canada Recovery Benefit, Canada Recovery Sickness Benefit, Canada Recovery Caregiving Benefit, and the Canada Worker Lockdown Benefit, totaling $16.5 billion; and

- The Canada Emergency Rent Subsidy, totaling $3.7 billion.

Tabling Date

Mr. Chair, one additional point which tends to come up that I would like to clarify is the timing of the tabling of the Public Accounts.

The Financial Administration Act requires the President of the Treasury Board to table the Public Accounts, while Parliament is sitting, each year by December 31.

While the end date is set by legislation, the actual tabling date will vary from year to year within this timeframe.

For instance, during fall election years, the tabling usually takes place closer to the end of the calendar year.

There are also other factors that impact the timeline.

After the Auditor General approves the Public Accounts, several weeks are required to prepare them for publication.

This includes an online version which is required by law to meet accessibility requirements.

Timing of tabling for this year was within typical timelines of mid to late October in a non-election year.

I want to assure this committee that we are looking for ways to help boost our efficiency throughout the production process to achieve the optimal timeline for the tabling of the Public Accounts of Canada.

Mr. Chair, I’d also like to acknowledge we are currently reviewing this committee’s recent report on the 2021 Public Accounts.

In particular, we are assessing the committee’s recommendations including the one recommendation concerning tabling timelines. .

Modernization

Mr. Chair, we are continuously looking for opportunities to improve how government operates, and this includes the modernization of the Public Accounts.

Based on recommendations of this committee, the government committed to study potential improvements, and I’m pleased to report that this work is underway.

To identify possible streamlining opportunities, we reviewed the existing content of the public accounts to identify information that is available through other means, not required by legislation and some with thresholds that have not changed for decades.

In addition, we have received feedback from the Library of Parliament on opportunities to improve the presentation and format of the Public Accounts of Canada.

At the same time, we have engaged key stakeholders on additional potential improvements through a survey.

The purpose of the survey is to better understand how the Public Accounts of Canada are being used, and to gather feedback on opportunities to improve and modernize them.

This feedback is critical to ensure that any changes to the Public Accounts provides information that is relevant, timely, and useful for accountability purposes.

I would like to reiterate that any proposed changes will be carefully examined to ensure the government’s financial information continues to support transparency and accountability to parliamentarians and Canadians.

As this project advances, the government will continue to work closely with parliamentarians, stakeholders, and this committee, Mr. Chair.

Thank you for your attention.

This concludes my remarks.

C. Presentation deck

Public Accounts of Canada 2022

October 2022

Agenda

- Background Information

- Current Reporting Cycle for Government Expenditures

- Public Accounts of Canada

- Roles and Responsibilities

- Accounting Standards

- Financial Results

- Appropriation Information

- Observations

- Annex - Definitions

Current reporting Cycle for Government Expenditures

- Before Fiscal Year

- January to March

- Final Supplementary Estimates of Prior Year

- Appropriation Act

- Tabling of Main Estimates

- Appropriation Act (Interim Supply)

- Departmental Plans

- Budget

- Final Supplementary Estimates of Prior Year

- January to March

- During Fiscal Year

- April to June

- Appropriation Act (Full Supply)

- Supplementary Estimates (A)

- Appropriation Act

- September to December

- Economic and Fiscal Update

- Supplementary Estimates (B)

- Appropriation Act

- January to March

- Final Supplementary Estimates (C)

- Appropriation Act

- April to June

- After Fiscal Year

- September to December

- Annual Financial Report

- Tabling of Public Accounts

- Departmental Results Reports, including departmental financial statements

- September to December

Other Key Documents

- Quarterly Financial Reports

- Monthly Fiscal Monitor

- Annual Debt Management Strategy and Debt Management Report

- Annual Tax Expenditure Report

- Crown Corporation Corporate Plan Summaries and Annual Reports

GC InfoBase

Public Accounts of Canada

- The Annual Report of the Government of Canada for the fiscal year ending March 31.

- The source of authority is under the Financial Administration Act (FAA) Section 64 (1) and (2).

- Financial statements discussion and analysis

- Audited consolidated financial statements of the Government

- Auditor General Report on the consolidated financial statements

Accrual

- Details of financial operations by ministries and departments:

- Appropriations

- Revenues

- Expenditures

Modified Cash

- Additional information and analyses

- For example:

- Losses of Public Money and Property (Section 2)

- Payments of claims against the Crown and Ex Gratia payments (Section 8)

Accrual/Modified Cash

Roles and Responsibilities

Public Accounts of Canada

- Receiver General

- Compile the data received from departments, agencies and Crown corporations

- Publish the Public Accounts of Canada

- Office of the Comptroller General

- Develop and interpret accounting policies

- Determine related disclosure requirements

- Department of Finance

- Draft the Financial Statements Discussion and Analysis

- Produce and release the Annual Financial Report

- Office of the Auditor General

- Audit the Government’s consolidated financial statements in the Public Accounts of Canada

- Provide a separate audit opinion on Crown Corporations and other agencies

- Commentary on Financial Audits

- Tabling in the House of Commons by the President of Treasury Board

Public Accounts Committee Review

Accounting Standards

Image - Text version

The Government of Accounting Handbook identifies where a policy choice, requirement, interpretation, or other further direction has been issued to supplement Public Sector Accounting Standards

Note: Certain Crown corporations use International Financial Reporting Standards (IFRS)

2021-2022 Financial Results

| (in billions of dollars) | Budget 2021-2022 |

Actual 2021-2022 |

Actual 2020-2021 |

|---|---|---|---|

| Total revenue | 355.1 | 413.3 | 316.4 |

| Program expenses | 475.6 | 468.8 | 608.5 |

| Public debt charges | 22.1 | 24.5 | 20.4 |

| Total expenses, excluding net actuarial losses | 497.6 | 493.3 | 628.9 |

| Annual deficit before net actuarial losses | (142.5) | (80.0) | (312.4) |

Net actuarial losses |

(12.2) | (10.2) | (15.3) |

| Annual deficit | (154.7) | (90.2) | (327.7) |

| Other comprehensive income (loss) | - | 4.5 | 0.3 |

| Accumulated deficit at end of year | (1,203.5) | (1,134.5) | (1,048.7) |

| Totals may not add due to rounding. | |||

| (in billions of dollars) | 2021-2022 | 2020-2021 |

|---|---|---|

| Accounts payable and accrued liabilities | 260.3 | 207.4 |

| Pensions and other future benefits | 327.4 | 312.9 |

| Unmatured debt and other liabilities | 1,251.0 | 1,131.9 |

| Total liabilities | 1,838.7 | 1,652.2 |

| Cash and accounts receivable | 280.0 | 224.2 |

| Foreign exchange amounts | 104.0 | 92.6 |

| Loans, investments and advances | 207.0 | 179.3 |

| Public sector pension assets | 9.2 | 6.3 |

| Total financial assets | 600.3 | 502.4 |

| Net debt | (1,238.4) | (1,149.8) |

| Total non-financial assets | 103.9 | 101.1 |

| Accumulated deficit | (1,134.5) | (1,048.7) |

| Totals may not add due to rounding. | ||

2021-2022 Financial Results - Impact of the Economic Response Plan

| (in billions of dollars) | Impact 2021-2022 |

|---|---|

Table 3 Notes

|

|

| Economic Response Plan impact on the Government of Canada expenses: | |

| Canada Emergency Wage Subsidy (CEWS) | 22.3 |

| COVID-19 income support for workerstable 3 note * | 15.6 |

| Canada Emergency Rent Subsidy | 3.7 |

| Canada Worker Lockdown Benefit | 0.9 |

| Total impact of some key Economic Response Plan measures on the Government of Canada expenses | 42.5 |

2021-2022 Financial Results

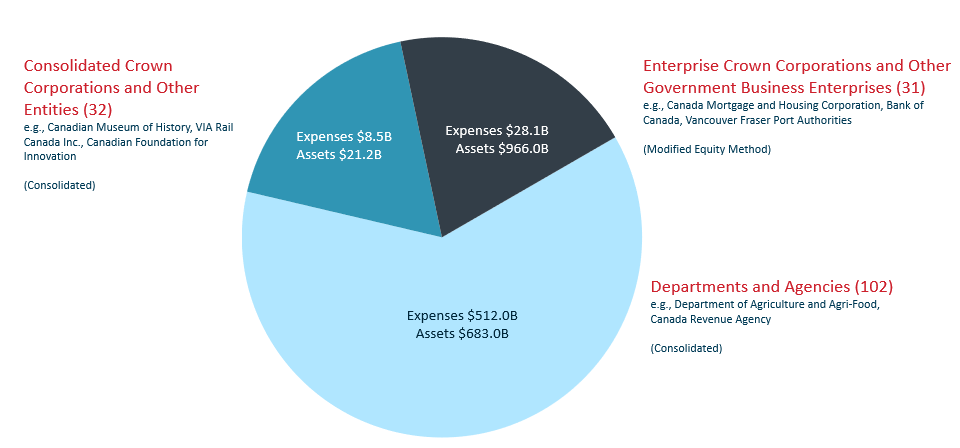

Government of Canada Reporting Entity - Text version

Consolidated Crown Corporations and Other Entities (32)

e.g., Canadian Museum of History, VIA Rail Canada Inc., Canadian Foundation for Innovation

(Consolidated)

Expenses $8.5B

Assets $21.2B

Enterprise Crown Corporations and Other Government Business Enterprises (31)

e.g., Canada Mortgage and Housing Corporation, Bank of Canada, Vancouver Fraser Port Authorities

(Modified Equity Method)

Expenses $28.1B

Assets $966.0B

Departments and Agencies (102)

e.g., Department of Agriculture and Agri-Food, Canada Revenue Agency

(Consolidated)

Expenses $512.0B

Assets $683.0B

2021-2022 Total Voted Budget – Used in Current Year

| National Defence $62,697M | Indigenous Services $18,287M | Health $15,739M | Public Safety $11,307M | Intergovermental Affairs, Infrastructure and Communities $9,296M | Innovation, Science and Industry $9,165M | Other Ministries $23,256M | |

|---|---|---|---|---|---|---|---|

| Budget (%) | 41.9 | 12.2 | 10.5 | 7.6 | 6.2 | 6.1 | 15.5 |

2021-2022 Total Voted Budget - Significant Lapses

- Health

- Total Lapse of $11,176M

Frozen Allotments: $5,560M

Net Lapse: $5,616M

- Total Lapse of $11,176M

- Indigenous Services

- Total Lapse of $3,451M

Frozen Allotments: $3,162M

Net Lapse: $289M

- Total Lapse of $3,451M

- Intergovernmental Affairs, Infrastructure and Communities

- Total Lapse of $3,436M

Frozen Allotments: $2,261M

Net Lapse: $1,175M

- Total Lapse of $3,436M

- National Defence

- Total Lapse of $2,555M

Frozen Allotments: $1,709M

Net Lapse: $846M

- Total Lapse of $2,555M

- Crown-Indigenous Relations and Northern Affairs

- Total Lapse of $2,244M

Frozen Allotments: $2,223M

Net Lapse: $21M

- Total Lapse of $2,244M

- Innovation, Science and Industry

- Total Lapse of $2,241M

Frozen Allotments: $1,009M

Net Lapse: $1,231M

- Total Lapse of $2,241M

Total Lapses $38.201M

Totals may not add due to rounding.

Observations of the Auditor General of Canada

Pay Administration

- Despite pay errors, the consolidated financial statements were presented fairly.

- A significant amount of work remains to resolve current payroll data quality problems, including backlog, in order to accurately pay employees.

National Defence

- Errors persist in both quantities and value of inventory and asset pooled items.

- Progress has been made over the past year to review how to classify items as inventory or asset pooled items.

Annex - Definitions

Accounting

- Accrual Accounting

- Transactions are recognized when revenue is earned, rather than when cash is received, and expenses are recognized when they are incurred, rather than when they are paid.

- Appropriation

- Any authority of Parliament to pay money out of the Consolidated Revenue Fund.

- Expenditure Basis of Accounting/Modified Cash Accounting (Appropriation Accounting)

- Transactions are recognized when money is paid out of the Consolidated Revenue Fund (CRF), as well as a limited number of transactions which do not affect the CRF until a later date for goods and services received just prior to year-end. Non-cash transactions (e.g., amortization) are not recognized. This is also sometimes called modified cash accounting.

- Modified Equity Accounting

- The cost of the Government’s equity is reduced by dividends received and adjusted to include the annual profits and losses of corporations, after elimination of unrealized inter-organizational gains and losses. Applies to Crown Corporations and other entities who can sustain their operations without government appropriations.

- Unmodified Audit Opinion

- Independent auditor's opinion that the financial statements are fairly presented, and in accordance with the accounting policies of the Government which conform with Canadian Public Sector Accounting Standards.

Government Concepts

- Special Revenue Spending Authorities

- Special revenue spending authorities from Parliament allows departments to use a certain amount of their revenues to finance their directly related expenditures. Those authorities include Revolving Funds and Net Voting and both of these reduce dependence on appropriations from general revenues.

- Net Voting

- Net voted operations may or may not be self-sustaining and usually the scale of operations is less significant than is the case for revolving funds. The aim of net voting provides that certain revenues offset related expenditures within a fiscal year (e.g., Shared Services Canada).

- Revolving Funds

- Generally appropriate for large, distinct, self-sustaining activities that provide client-oriented services. The aim of a revolving fund is to achieve self-sufficiency over its business cycle, therefore appropriations are non-lapsing (e.g., Passport Canada).

- Specified Purpose Accounts (SPAs)

- A broad classification of accounts established in the accounts of Canada and reported in the Public Accounts. SPAs, record transactions, and expenditures for money payable out of the Consolidated Revenue Fund (CRF) under statutory authorities established for specified purposes. For accounting purposes, SPAs are classified as either a consolidated SPA (Employment Insurance Operating Account), a non-consolidated SPA (Insurance and Death Benefit Accounts) or deferred revenue SPA (Spectrum Licence Fees).

- Frozen Allotments

- Used to prohibit the spending of funds previously appropriated by Parliament. There are two types of frozen allotments: permanent and temporary.

- Permanent Frozen Allotments

- Used where the Treasury Board has directed that funds lapse at the end of the fiscal year.

- Temporary Frozen Allotments

- Used where an appropriation is frozen until such time as a condition (conditions) has (have) been met.

- Special Purpose Allotments (SPAs)

- Used to set apart a portion of an organization’s voted appropriation for a specific initiative or item. Such an allotment is established when the Board wishes to impose special expenditure controls.

D. PAC overview note

Master Overview of the Committee

Standing Committee on Public Accounts (PACP)

Mandate of the Committee

When the Speaker tables a report by the Auditor General in the House of Commons, it is automatically referred to the Public Accounts Committee. The Committee selects the chapters of the report it wants to study and calls the Auditor General and senior public servants from the audited organizations to appear before it to respond to the Office of the Auditor General’s findings. The Committee also reviews the federal government’s consolidated financial statements – the Public Accounts of Canada – and examines financial and/or accounting shortcomings raised by the Auditor General. At the conclusion of a study, the Committee may present a report to the House of Commons that includes recommendations to the government for improvements in administrative and financial practices and controls of federal departments and agencies.

Government policy, and the extent to which policy objectives are achieved, are generally not examined by the Public Accounts Committee. Instead, the Committee focuses on government administration – the economy and efficiency of program delivery as well as the adherence to government policies, directives and standards. The Committee seeks to hold the government to account for effective public administration and due regard for public funds.

Pursuant to Standing Order 108(3) of the House of Commons, the mandate of the Standing Committee on Public Accounts is to review and report on:

- The Public Accounts of Canada;

- All reports of the Auditor General of Canada;

- The Office of the Auditor General’s Departmental Plan and Departmental Results Report; and,

- Any other matter that the House of Commons shall, from time to time, refer to the Committee.

The Committee also reviews:

- The federal government’s consolidated financial statements;

- The Public Accounts of Canada;

- Makes recommendations to the government for improvements in spending practices;

- Considers the Estimates of the Office of the Auditor General.

Other Responsibilities:

- The economy, efficiency and effectiveness of government administration;

- The quality of administrative practices in the delivery of federal programs; and,

- Government’s accountability to Parliament with regard to federal spending.

Committee Members

| Name and Role | Party | Riding | PACP Member Since |

|---|---|---|---|

| Chair | |||

| John Williamson | Conservative | New Brunswick Southwest | February 2022 |

| Vice-chair | |||

| Jean Yip | Liberal | Scarborough—Agincourt | January 2018 |

| Nathalie Sinclair-Desgagné Critic for Public Accounts; Pandemic Programs; Economic Development Agencies |

Bloc Québécois | Terrebonne | December 2021 |

| Members | |||

| Garnett Genuis Critic for International Development |

Conservative | Sherwood Park—Fort Saskatchewan | October 2022 |

| Michael Kram | Conservative | Regina—Wascana | October 2022 |

| Kelly McCauley |

Conservative | Edmonton West | October 2022 |

| Blake Desjarlais Critic for TBS; Diversity and Inclusion; Youth; Sport and PSE |

New Democratic Party | Edmonton Greisbach | December 2021 |

| Valerie Bradford | Liberal | Kitchener South – Hespeler | December 2021 |

| Han Dong | Liberal | Don Valley North | December 2021 |

| Peter Fragiskatos Parliamentary Secretary National Revenue |

Liberal | London North Centre | December 2021 |

| Brenda Shanahan | Liberal | Châteauguay—Lacolle | December 2021; and Jan 2016 – Jan 2018 |

Anticipated TBS-Related Activity – 44th Parliament

- Briefing from the Canada Audit and Accountability Foundation

- Introductory briefings from the Auditor General; Comptroller General of Canada; others.

- Public Accounts of Canada

- Reports of the Auditor General of Canada

TBS Related Committee Activity – 43rd Parliament

- Public Accounts of Canada (Link to study)

- Government Response provided: link

- Reports of the Auditor General of Canada:

- Oversight of Government of Canada Advertising (Link to study)

- Government Response provided: Link

- Procuring Complex Information Technology Solutions (Link to study)

- Investing in Canada Plan (Link to study)

- Call Centres (Link to study)

- Government Response provided: Link

- National Shipbuilding Strategy (Link to study)

- Oversight of Government of Canada Advertising (Link to study)

- Public Service Culture (Link to study)

- No report

Interest in TBS Portfolio

Conservative Party of Canada (CPC)

- Spending Oversight and Accountability

- Conservative MPs consider the government is spending too much, and without proper oversight and accountability. This criticism amplified since the election of the CPC’s new leader, MP Pierre Poilievre. Since the return of Parliament in September, most of the party’s interventions during Question Period have been about government spending.

- More broadly, Conservatives have been using the Public Accounts as an example of wasteful spending and government incompetence. MP Andrew Scheer (not a committee member) claimed that “we are constantly poring through Public Accounts to find wasteful spending and, lo and behold, we find them all the time.”

- October 28, 2022, Debate on Bill C-9

- MP Kelly McCauley recently presented the Conservatives' dissenting report on the 2021 Public Accounts report, in which the CPC claimed that should the government revise the public accounts after they are finalized, they recommend that the secretary of the Treasury Board and the comptroller general report their rationale for doing so to PACP, that the Auditor General present their views to the committee and that all three appear at PACP to discuss the matter.

- October 20, 2022, Routine Proceedings

- In the past, MPs Pat Kelly (not a committee member) and Kelly McCauley have criticized the way the government produced the 2021 Public Accounts, suggesting that the audited Public Accounts were re-opened for political gain; showed concerns that the late tabling made it impossible to hold the government accountable for “out of control spending”.

- December 8, 2021, Committee of the Whole – Supplementary Estimates (B) 2021-22; December 10, 2021, Question Period; February 3, 2022, Debate on Bill C-8; March 1, 2022, OGGO – Supplementary Estimates (C) 2021-22

- Public Service and Public Servants

- MP Philip Lawrence (no longer a committee member) claims that he is frustrated by the fact that when he was a member of PACP, the studies have always focused on the same topic ands reports that do not necessarily get implemented. He wants to focus more on improving the performance of the public sector.

- May 5, 2022, PACP – Main Estimates 2022-23 (OAG)

- MP Philip Lawrence (no longer a committee member) claims that he is frustrated by the fact that when he was a member of PACP, the studies have always focused on the same topic ands reports that do not necessarily get implemented. He wants to focus more on improving the performance of the public sector.

- Diversity & Inclusion, GBA+

- Conservative MPs have supported GBA+ in recent Parliaments, often criticizing the Government for claiming to be feminist while supposedly doing very little to enforce GBA+ practices. On multiple occasions, Conservative MPs have accused Government MPs and officials of not taking the GBA+ training that is offered to them seriously.

- February 27, 2020, FEWO – Meeting #3; June 9, 2021, Private Member’s Business

- Throughout the pandemic, Conservatives have been very vocal over the Government’s “failure to apply the GBA+ on all the COVID-19 programs”. During Question Period and in committees, several MPs, including Raquel Dancho, Jag Sahota and Karen Vecchio (not committee members) have asked questions about the lack of GBA+ analysis in COVID-related policies, claiming that it ended up isolating women and leaving them vulnerable during lockdowns.

- May 25, 2020, Statement by Members; March 12, 2021, Question Period; June 15, 2021, FEWO – Meeting #42

- More recently, in PACP meetings from the 44th Parliament, MPs Eric Duncan, Philip Lawrence and Jeremy Patzer (no longer committee members) again insisted on how quarantine measures disadvantaged women. They expressed to the Auditor General that they are “very surprised that this has not raised a red flag in any way as being worthy of an audit, particularly when it comes to a GBA+ lens”. They also asked questions to the Auditor General on ways to make National Defence more inclusive for women.

- Conservative MPs have supported GBA+ in recent Parliaments, often criticizing the Government for claiming to be feminist while supposedly doing very little to enforce GBA+ practices. On multiple occasions, Conservative MPs have accused Government MPs and officials of not taking the GBA+ training that is offered to them seriously.

- April 5, 2022, PACP – Meeting #13; June 2, 2022, PACP – Meeting #22

- Environment and Greening Government

- MP Philip Lawrence (no longer a committee member) believes that investments in many sectors of government need to be made, specifically about data management and climate change resilience. He mentioned that he would like more information on what the government is doing on that front.

- March 3, 2022, PACP – Meeting #8

- MP Philip Lawrence (no longer a committee member) believes that investments in many sectors of government need to be made, specifically about data management and climate change resilience. He mentioned that he would like more information on what the government is doing on that front.

- Order Paper Questions

- MPs Scott Aitchinson and Tom Kmiec (not committee members) respectively requested parliamentary returns on Expenditures on Transportation Machinery and Equipment listed in the 2021 Public Accounts (Q-297, January 2022) and on Losses of public money and property as listed in the 2021 Public Accounts (Q-323, February 2022)

Bloc Québécois (BQ)

- Spending Oversight and Accountability

- MP Sinclair-Desgagné criticized on multiple occasions the ‘’fiscal imbalance’’ in the Public Accounts, particularly when it comes to healthcare transfers to Quebec and other provinces from the federal government.

- October 27, 2022, Debate on Bill C-31

- MP Sinclair-Desgagné suggested that the President of the Treasury Board is happy that workers from the Office of the Auditor General are on strike because it means they are no longer able to produce reports that “embarrass the government” and that they can no longer ensure accountability.

- March 31, 2022, Statement by Members

- MP Sinclair-Desgagné showed concerns that Crown corporations make it impossible to correctly track government spending. With Crown corporations, “it is impossible to know how much money is being handed over”. She believes that the current situation is unacceptable. More recently, in a PACP meeting, she asked a TBS official what legislative changes would be needed for crown corporations to disclose information the same way departments do.

- November 1, 2022, PACP – Meeting #36 (Briefing on the Office of the Auditor General); May 9, 2022, Debate on Budget 2022

- MP Sinclair-Desgagné criticized on multiple occasions the ‘’fiscal imbalance’’ in the Public Accounts, particularly when it comes to healthcare transfers to Quebec and other provinces from the federal government.

- Public Service and Public Servants

- MP Sinclair-Desgagné showed support for employees working at the Office of the Auditor General that are on strike, saying they deserve better pay equity.

- March 31, 2022, Statement by Members

- MP Sinclair-Desgagné showed support for employees working at the Office of the Auditor General that are on strike, saying they deserve better pay equity.

- Diversity & Inclusion, GBA+

- Bloc MPs have been historically in favor of GBA+ while being repeatedly critical over the lack of results and the lack of data indicating its effectiveness. MP Andréanne Larouche (not a committee member) has been the most vocal Bloc MP on this issue, claiming on multiple occasions that GBA+ must be considered in every department and in government economic responses, with better outcomes.

- June 15, 2020, HUMA – Meeting #19; February 25, 2021, FEWO – Meeting #18

- More recently, in PACP meetings, MP Sinclair-Desgagné was interested in the Auditor General's findings on the shortcomings of the government's implementation of GBA+. She also reiterated her concern about the lack of focus on outcomes, saying that there is a lack of information to determine whether concrete improvements are being made to reduce barriers. She wonders if the problem is “with the data or the process”.

- June 2, 2022, PACP – Meeting #22

- Bloc MPs have been historically in favor of GBA+ while being repeatedly critical over the lack of results and the lack of data indicating its effectiveness. MP Andréanne Larouche (not a committee member) has been the most vocal Bloc MP on this issue, claiming on multiple occasions that GBA+ must be considered in every department and in government economic responses, with better outcomes.

- Environment and Greening Government

- MP Sinclair-Desgagné criticizes the fact that, regarding greening government, Crown corporations are held to lower environmental standards. More notably, she criticized some of the Public Sector Pension Investment Board’s environmental practices.

- February 15, 2022, PACP – Meeting #6

- MP Sinclair-Desgagné believes Government funding should be cut off to sectors where positive environmental results are lacking, such as the oil sector

- February 8, 2022, PACP – Meeting #4

- MP Sinclair-Desgagné criticizes the fact that, regarding greening government, Crown corporations are held to lower environmental standards. More notably, she criticized some of the Public Sector Pension Investment Board’s environmental practices.

New Democratic Party (NDP)

- Spending Oversight and Accountability

- MP Daniel Blaikie (not a committee member) reminded the House several times about the Parliamentary Budget Officer’s remarks about how the government has been filing the Public Accounts too late. He and the NDP believes that “…additional financial reporting (is) warranted…” and that “normally, in the countries of most of our allies and trading partners, that happens on a six-month timetable after the end of the fiscal year, so tabling them in December was very late. I think it is true, especially when the government is spending large sums of money, that accountability and transparency become that much more important”.

- February 2, 2022, March 23, 2022 & March 28, 2022, Debate on the Economic and Fiscal Update Implementation Act, 2021

- MP Daniel Blaikie (not a committee member) reminded the House several times about the Parliamentary Budget Officer’s remarks about how the government has been filing the Public Accounts too late. He and the NDP believes that “…additional financial reporting (is) warranted…” and that “normally, in the countries of most of our allies and trading partners, that happens on a six-month timetable after the end of the fiscal year, so tabling them in December was very late. I think it is true, especially when the government is spending large sums of money, that accountability and transparency become that much more important”.

- Public Service and Public Servants

- MP Blake Desjarlais criticized the Pheonix Pay System, saying that the Treasury Board not consulting with public servants resulted in a direct impact on workers. He claims that years later, the Government continues to fail with Phoenix.

- May 3, 2022, PACP – Meeting #17

- MP Blake Desjarlais criticized the Pheonix Pay System, saying that the Treasury Board not consulting with public servants resulted in a direct impact on workers. He claims that years later, the Government continues to fail with Phoenix.

- Diversity and Inclusion, GBA+

- The NDP has been one of the most vocal parties about the importance of GBA+. They believe that GBA+ analyses should be applied systematically to the “development, implementation or oversight” of every government program. NDP MPs have been particularly critical about the Government for allegedly breaking its commitment to make GBA+ an indispensable tool. They partially attribute the non-compliance of recruitment and retention targets for underrepresented groups as a result of the “failure” to implement GBA+.

- May 27, 2021, PACP – Meeting #34; June 9, 2021, Private Member’s Business

- In PACP meetings, MP Desjarlais has been a strong advocate for GBA+. He believes that shortcomings in the government's implementation of GBA+ constitute an “extreme situation” that undermines the confidence of people in marginalized communities, such as Indigenous women, in their government.

- June 2, 2022, PACP – Meeting #22

- MP Desjarlais believes more work needs to be done in the public sector and with Crown corporations when it comes to ensuring diversity inclusion and equity. He believes stronger targets and indicators should be put in place so we can see the tangible results and progress.

- February 15, 2022, PACP – Meeting #6; March 31, 2022, PACP – Meeting #12; March 31, 2022, Debate on Bill S-214

- The NDP has been one of the most vocal parties about the importance of GBA+. They believe that GBA+ analyses should be applied systematically to the “development, implementation or oversight” of every government program. NDP MPs have been particularly critical about the Government for allegedly breaking its commitment to make GBA+ an indispensable tool. They partially attribute the non-compliance of recruitment and retention targets for underrepresented groups as a result of the “failure” to implement GBA+.

- Environment and Greening Government

- MP Desjarlais often criticizes the lack of “real climate action” by the Government. He believes the government should be held accountable on the lack of progress on that front. He believes climate actions should play an integral part in the action plans of Government departments.

- December 1, 2021, Reply to the Speech of the Throne; March 1, 2022, PACP – Meeting #7; April 7, 2022, Statement by Members

- Other NDP MPs, like Laurel Collins (not a committee member) showed concerns over the fact that when it comes to the greening government, Crown corporations are not required to report on their emissions.

- May 3, 2022, ENVI – Meeting #15

- MP Desjarlais often criticizes the lack of “real climate action” by the Government. He believes the government should be held accountable on the lack of progress on that front. He believes climate actions should play an integral part in the action plans of Government departments.

Relevant Meeting Summaries

Meeting 1 – December 16, 2021

Election of Chair

Full transcript: Evidence – PACP (44) – No. 1

The Standing Committee on Public Accounts (PACP) held its first meeting of the 44th Parliament to elect a chair. Tom Kmiec (CPC) was nominated and elected as Chair of the Committee. Jean Yip (LPC) and Nathalie Sinclair-Desgagné (Bloc) were nominated and elected as Vice Chairs of the Committee.

The Committee adopted several routine motions for the committee (e.g. steering committee membership, publication of committee proceedings, research staff, travel etc.)

A motion from Blake Desjarlais (NDP) proposed to establish limits to when and how the Committee can move to meet in camera. The motion failed in a recorded division 9-1.

A motion from Jean Yip (LPC) proposed that the Committee receive a briefing from the Canadian Audit and Accountability Foundation for one meeting, which was adopted unanimously.

At 11:51, the meeting adjourned.

Next Steps

There are no future meetings scheduled for the committee. A one-meeting briefing session with the Canadian Audit and Accountability Foundation is expected to take place when the committee next meets, likely in the new year.

Meeting 2 – February 1, 2022

Briefing with Canadian Audit and Accountability Foundation

Full transcript: Evidence – PACP (44-1) – No. 2

Officials from the Canadian Audit and Accountability Foundation (CAAF) presented a briefing to the Committee during the first hour of the meeting (a briefing usually held for the committee at the beginning of every Parliament). The briefing outlined the role of the CAAF, the role of PACP as a committee, and the importance of parliamentary oversight and accountability. The briefing also discussed how to interpret OAG performance and financial audits, and the Public Accounts. CAAF officials emphasized the importance of the relationship between committee members and the OAG/ public servants, including the type of questions that are asked. Officials put a particular emphasis on the importance of non-partisanship and to approach committee meetings with a shared purpose and goal.

Committee Members agreed that regular rounds of questioning based on party would be suspended so Members were not limited in time. Members asked technical questions about the performance audits by the Auditor General. Members also showed concern about the approach with files and departments that are consistently re-appearing with very little or no improvement (Shipbuilding and clean drinking water were specifically named as reoccurring files) - in response, officials emphasized the importance of key clear recommendations with deadlines in reports, follow-ups from the committee and targeted questioning on actions being taken by the responsible departments. When responding to a question about research, the Library of Parliament analysts commented on the trickiness of using GCInfobase without experience.

At 12:06, the meeting went in camera to discuss committee business.

Meeting 6 – February 15, 2022

Public Sector Pension Investment Board

Full transcript: Evidence – PACP (44-1) – No. 6

The meeting started late due to a vote in the House of Commons.

The Deputy Auditor General began the meeting with his opening remarks on the audit. The Financial Administration Act requires a special examination be carried out every ten years, but he confirmed that they did not find any deficiencies. The OAG did find issues with performance indicators on issues such as diversity and inclusion. The OAG also noted that improvements for risk mitigation, risk monitoring and reporting were needed, such as in human resources planning. The corporation has agreed with the recommendations and has prepared an action plan.

Mr. Glynn, Chair of the Board for PSPIB explained the audit in his opening remarks and confirmed that no material deficiencies were found. Mr. Glynn explained that PSP as a crown corporation operates at arm’s length from the Government of Canada and explained the operations of PSP. Mr. Glynn gave an overview of the actions already taken by PSP to implement the recommendations by the OAG and confirmed that PSP has made significant progress. Mr. Glynn also announced the retirement of Mr. Cunningham (President and CEO) next year.

All Members were pleased with the results of the audit and commended the witnesses on the results. Members asked questions about the specifics of the audits and the workings of PSPIB in terms of investments and risks. Members had concerns about the specific targets being put in place to address bigger issues such as diversity and inclusion along with climate change, which the witnesses provided the updates on recent actions and updated targets as recommended by the OAG.

Next Steps

The committee is scheduled to meet for its work on Thursday, February 17, 2022.

Meeting 15 – April 26, 2022

Public Accounts of Canada 2021 (TBS Appearance)

Full transcript: Minutes – PACP (44-1) – No. 15 (in camera)

Meeting 17 – May 3, 2022

Public Accounts of Canada 2021 (TBS Appearance)

Full transcript: Evidence – PACP (44-1) – No. 17

Witnesses

Treasury Board Secretariat

- Roch Huppé, Comptroller General of Canada

- Monia Lahaie, Assistant Comptroller General, Financial Management Sector

- Diane Peressini, Executive Director, Government Accounting Policy and Reporting, Office of the Comptroller General

Office of the Auditor General

- Karen Hogan, Auditor General of Canada

- Etienne Matte, Principal

- Chantale Perreault, Principal

Department of Finance

- Michael J. Sabia, Deputy Minister

- Nicholas Leswick, Associate Deputy Minister

- Evelyn Dancey, Assistant Deputy Minister, Economic and Fiscal Policy Branch

Highlights

The meeting began late, due to votes in the House of Commons. Members agreed to extend proceedings to 1:30pm.

The Auditor General began the meeting with her opening remarks on the Public Accounts of Canada 2021 (PAC), and the process involved in auditing the accounts. She confirmed that the document met with her approval. She outlined why there was an amendment to the PAC, and the process that her office undertook to assess and complete the revision. The AG also review the exceptional spending related to the pandemic. She described the comments section of her review, and also touched on the state of affairs in the PS pay administration file, as well as the review of DND’s inventory control problems. Other issues mentioned included cybersecurity and data management.

Mr. Huppé provided the Committee an overview of the PAC, stressing the ‘clean’ audit the GC has received for the 23rd straight year. He highlighted the deficit numbers, and compared it favourably to initial projections. He reviewed why the PAC was re-opened last year, as well as the process of revision that led to the publishing delay beyond the norm, though still well within the statutory requirement. He reviewed the study of potential modernization of the Public Accounts, committing to work closely with parliamentarians and Canadians as the process advances.

The Committee posed a wide range of questions including a particularly sharp focus on the reopening of the PAC last fall (CPC); the gap in transparency of financial reporting between Crown Corporations and the rest of government (BQ); and the progress of the government on the Phoenix pay system problems (NDP). A full accounting of questions is included in the summary.

Follow-Ups

Will be verified against the transcript and tasked out accordingly by TBS Parliamentary Affairs

- Request for an official opinion on the options available to achieve the objective of closing the gap in financial transparency between Crown Corporations and the rest of government, specifically in creating a requirement for the jurisdictional destination of Crown Corporation funding decisions to be publicly available. - Mme. Nathalie Sinclair-Desgagné (BQ)

Next Steps

The Committee’s next meeting is Thursday, May 5, where it is expected to hear from the AG on the Main Estimates, 2022-23.

Meeting 18 – May 5, 2022

Main Estimates 2022-23 (OAG)

Full transcript: Evidence – PACP (44-1) – No. 18

Witnesses

Office of the Auditor General

- Karen Hogan, Auditor General of Canada

- Jerry V. DeMarco, Commissioner of the Environment and Sustainable Development

- Andrew Hayes, Deputy Auditor General

- Lissa Lamarche, Assistant Auditor General and Chief Financial Officer

- Paule-Anny Pierre, Assistant Auditor General

Highlights

The meeting began late, due to votes in the House of Commons. The Committee moved to in camera at the end of the meeting to consider drafting instructions for a report not related to TBS.

The Auditor General provided the Committee with an overview of her resources and the requests in the Main Estimates 2022-23 and the steps the office is taking to digitize their office, she also emphasized the efforts the Office of the Auditor General has taken after the strike.

Members were focused on the repetitive nature of the reports and wanted to understand how resources in the Office of the Auditor General to follow-up on its recommendations. CPC Members brought forward the examples of the multiple follow-ups needed with the clean drinking water and the National shipbuilding reports. MP Nathalie Sinclair-Desgagné (BQ) was concerned with overall oversight on crown corporations, which the Auditor General agreed with.

MP Blake Desjarlais (NDP) passionately questioned the Auditor General on improvements being made to the culture within the work environment after the strike and expressed concern that employees may be facing disciplinary action. The Auditor General assured the Member that she had not been made aware of any disciplinary actions and reiterated the importance of the Code of Conduct that employees must follow.

MP Jeremy Patzer (CPC) asked if there were plans to conduct an audit on the overall productivity of public servants working from home, and in response, the Auditor General confirmed that it was not in the current plans.

The Committee adopted the referred votes of the Main Estimates 2022-23 for the Office of the Auditor General (on division).

Meeting 22 – June 2, 2022

Briefing on the 2022 Reports 1 to 4 of the Auditor General of Canada

Full transcript: Evidence – PACP (44-1) – No. 22

Witnesses

Office of the Auditor General

- Karen Hogan, Auditor General of Canada

- Carey Agnew, Principal

- Carol McCalla, Principal

- Nicholas Swales, Principal

Highlights

The Auditor General appeared before the Committee to brief members on the four audit reports tabled earlier this week. In her opening remarks, she provided an overview of the reports’ findings, including on Report 3: Follow-up on Gender-Based Analysis Plus (GBA+). She indicated that while GBA+ analyses are completed, there has not been an observable impact on outcomes. She said that the Privy Council Office (PCO), Treasury Board Secretariat (TBS) and Women and Gender Equality (WAGE) need to better collaborate and ensure organizations fully integrate GBA+ in a way that produces real results.

During questioning, Brenda Shanahan (LPC) asked how departments were doing with regards to implementing GBA+. Ms. Hogan said that it was a mixed bag, with some departments using GBA+ usefully and improving outcomes, while others see it as more of an obligation. Ms. Shanahan later gave examples of improvements in gender equality in Canada, and asked Ms. Hogan to comment. Ms. Hogan repeated that results were mixed, as reporting and measuring are inconsistent across government.

Valerie Bradford (LPC) asked about the OAG process for following up with departments after audits. In her response, Ms. Hogan referenced TBS requirements that departmental audit committees to follow up on any recommendations their organizations receive.

Blake Desjarlais (NDP) said that shortcomings with the government’s implementation of GBA+ is hurting the confidence of people in marginalized communities in their government. Ms. Hogan replied that the Government seems to be more focused on process rather than outcomes.

Nathalie Sinclair-Desgagné (BQ) asked Ms. Hogan to elaborate on her findings on the shortcomings of the government’s implementation of GBA+. The Auditor General said that there was a lack of capacity, skills and data to do the analysis. She also repeated her concern about a lack of focus on outcomes, saying a lot of information was missing to determine whether concrete improvements are being made to reduce barriers.

Ziad Aboultaif (CPC) said that while the federal public service had expanded, productivity was down and outcomes are not being achieved. He asked if there needs to be a restructuring of the public service. Ms. Hogan noted her concern that the government was focused on process rather than outcomes, but said there needed to be a balance, as some controls and vetting are needed to ensure accountability.

Meeting 26 – June 16, 2022

Follow-up study on Report 9, Investing in Canada Plan (TBS Appearance)

Full transcript: Not available yet

Witnesses

Canada Mortgage and Housing Corporation

- Romy Bowers, President and Chief Executive Officer

- Nadine Leblanc, Senior Vice President, Policy

Department of Indigenous Services

- Christiane Fox, Deputy Minister

- Rory O'Connor, Director General

Office of Infrastructure of Canada

- Kelly Gillis, Deputy Minister

- Gerard Peets, Assistant Deputy Minister

- Sean Keenan, Director General

Office of the Auditor General

- Karen Hogan, Auditor General of Canada

- Gabriel Lombardi, Director

Privy Council Office

- Laurie Goldmann, Director of Operations

Treasury Board Secretariat

- Ritu Banerjee, Executive Director, Results Division, Expenditure Management Sector

Highlights

Note: The Secretary of the Treasury Board previously appeared on this subject on May 11, 2021. He did not receive any questions.

The Auditor General confirmed that no new audit work has been completed since March 2021. She stressed the importance of clear and meaningful reporting for success, especially with so many departments involved in the Plan. In her opening remarks, the Deputy Minister from Infrastructure Canada explained the improvements the department has made in reporting requirements and working collaboratively with their partners on the Investing in Canada Plan. Ms. Gillis also pointed to the fact that Infrastructure Canada works very closely with TBS and PCO on reporting requirements.

The TBS official did not respond to any questions.

MP Eric Duncan (CPC) expressed concerns about the issuing of performance pay to CMHC employees, Ms. Bowers (CMHC) explained the compensation structure as a crown corporation.

MP Alain Therrien (BQ) moved two motions unrelated to TBS.

Meeting 27 – June 21, 2022

Public Accounts of Canada 2021

Full transcript: Evidence – PACP (44-1) – No. 27

Meeting 28 – June 23, 2022

Public Accounts of Canada 2021

Full transcript: Minutes – PACP (44-1) – No. 28 (in camera)

Meeting 29 – September 27, 2022

Public Accounts of Canada 2021

Full transcript: Minutes – PACP (44-1) – No. 29 (in camera)

Meeting 32 – October 18, 2022

Report 2, Greening Government Strategy (TBS Appearance)

Full transcript: Evidence – PACP (44-1) – No. 32

Witnesses

Treasury Board Secretariat

- Graham Flack, Secretary of the Treasury Board of Canada

- Jane Keenan, Acting Executive Director, Centre for Greening Government

- Malcolm Edwards, Senior Engineer, Centre for Greening Government

Office of the Auditor General

- Jerry V. DeMarco, Commissioner of the Environment and Sustainable Development

- Milan Duvnjak, Principal

Department of National Defence

- Bill Matthews, Deputy Minister

- Nancy Tremblay, Associate Assistant Deputy Minister, Material

- Saleem Sattar, Director General, Environment and Sustainable Management

Department of Transport

- Michael Keenan, Deputy Minister

- Ross Ezzeddin, Director General, Air, Marine and Environmental Programs

Highlights

The meeting was delayed by votes in the House.

In his opening remarks, Commissioner of the Environment and Sustainable Development, Jerry DeMarco outlined the history of the Greening Government Strategy and the targets that were set and revised since the launch in 2017. He told the Committee that the audit focused on TBS’s leadership in supporting departmental progress; as well as how DND and Transport implemented controls to reduce GHG emissions. He concluded that TBS’s efforts to reduce emissions are not as complete as they could be, and that important information on greening government was hard to find, unclear or insufficient – including a lack of detail on costs and savings. He cited concerns that indirect emissions have not been reported, and that Crown corporations were outside the reach of the strategy. He said that neither DND nor Transport made it clear how they would meet the 2050 target. He concluded that the lack of info makes it difficult to track targets, and to determine if Canada is being the global leader it has set out to be. He told the Committee that of the five recommendations for TBS in the report, only one wasn’t fully agreed with. Finally, the Commissioner noted that he tabled a fall report on October 4 on the 2021 progress report on the Federal Sustainable Development Strategy.

In his opening remarks, Deputy Minister of Transport Canada, Michael Keenan, told the Committee that Transport Canada fully accepted the Commissioners recommendation and is fully committed to the GHG reduction targets. He said that Transport Canada’s emission largely result from its fleet, rather than from buildings, so its implementation plan is somewhat unique. He said that TC’s roadmap will continue to evolve and be updated, and that mechanisms would be put in place to assess risks and track reductions of emissions.

In his opening remarks, the Secretary of the Treasury Board, Graham Flack, outlined how the Government is greening its activities with a target of net-zero GHG emission by 2050, and an interim target of 40% reduction by 2025 for the conventional fleet of vehicles and federal facilities. He also reviewed the leadership role of the Centre for Greening Government (CGG) at TBS, in terms of the strategy to green buildings, vehicles and procurement by the government. This includes developing low-carbon real property portfolio plans; building new zero-carbon buildings; retrofitting existing buildings to be energy efficient and low-carbon; including environmental factors in their procurement; buying hybrid or zero-emission vehicles and clean electricity; and adopting clean technologies, such as smart building technologies, clean fuels, and renewable electricity. After touching on the top lines of the Commissioners report, the Secretary said that TBS agrees with all the recommendations of the report, other than the notion that TBS has not developed an approach to tracking costs and savings. He told the Committee that CGG uses life-cycle costing analysis and total cost of ownership methodologies to inform decision makers on the best value options to decarbonize government operations. He also said that other governments have reached out to ours on implementing a costing methodology. Finally, he said that TBS would do more to communicate the cost-effective approach to accounting for costs and emissions to Parliamentarians and Canadians.

In his remarks, DND deputy minister, Bill Matthews outlined the size and scale of DND’s operating environment. He said the department is making progress, meeting shorter term targets, but that there remains a great deal of work to achieve the Government’s long-term net-zero targets. He said that DND accepted the recommendations of the Commissioner.

Following opening statements, the Committee suspended proceedings due to additional votes in the House. The witnesses were released but are expected to be recalled for questioning at a subsequent date.

The Committee returned to meet in camera on Committee Business following the votes in the House.

Meeting 35 – October 28, 2022

Report 2, Greening Government Strategy (TBS Appearance)

Full transcript: Not available yet

Witnesses

Treasury Board Secretariat

- Graham Flack, Secretary of the Treasury Board of Canada

- Malcolm Edwards, Senior Engineer, Centre for Greening Government

Office of the Auditor General

- Jerry V. DeMarco, Commissioner of the Environment and Sustainable Development

- Milan Duvnjak, Principal

Department of National Defence

- Bill Matthews, Deputy Minister

- Nancy Tremblay, Associate Assistant Deputy Minister, Material

- Saleem Sattar, Director General, Environment and Sustainable Management

Department of Transport

- Michael Keenan, Deputy Minister

- Ross Ezzeddin, Director General, Air, Marine and Environmental Programs

Highlights

The Committee met to study Report 2, Greening Government Strategy, of the 2022 Reports 1 to 5 of the Commissioner of the Environment and Sustainable Development, and to question witnesses. Officials did not make opening statements as they had already done so during the meeting on October 18, which was interrupted due to votes in the House of Commons.

Today’s meeting was largely polite and cordial. Topics of discussion of interest to TBS included:

- TBS’s role in the Greening Government Strategy, including reporting, enforcement, and international cooperation.

- Costs associated with achieving the government’s greenhouse gas (GHG) emissions reduction goals.

- The government’s ability to provide comprehensive reporting on its GHG emissions.

- The impact of the COVID-19 pandemic on government GHG emissions

- The OAG’s recommendation that Crown corporations also report their progress, and TBS’s consultations with Crown corporations.

- Any current and future plans to purchase carbon offsets by the government.

- GHG emissions produced by ministerial travel.

The officials from DND and Transport also responded to questions regarding their own plans and progress in reducing their departments’ emissions. Mr. Matthews, from DND, made reference to tools and guidance provided to them by TBS. After the conclusion of witness testimony, the Committee met in camera to discuss committee business.

Meeting 36 – November 1, 2022

Briefing on the Office of the Auditor General (TBS Appearance)

Full transcript: Not available yet

Witnesses

Treasury Board Secretariat (TBS)

- Stephen Diotte, Executive Director, Employment Relations and Total Compensation, Strategic Compensation Management, Office of the Chief Human Resources Officer

Office of the Auditor General (OAG)

- Karen Hogan, Auditor General of Canada

- Andrew Hayes, Deputy Auditor General

Department of Finance (FIN)

- Nicholas Leswick, Associate Deputy Minister

Highlights

Pursuant to the motion adopted on October 21, 2022, the Committee received a briefing on the Office of the Auditor General.

In her opening remarks, the Auditor General (AG) emphasized the importance of considering the workload in proportion with the amount of funding the OAG receives when requesting additional audits. The AG considers the current funding model problematic due to the fact that the Department of Finance (FIN) and Treasury Board Secretariat (TBS) are organizations audited by the OAG and presents challenges to maintain independence from the Government. The AG addressed the previous strike and the resulting challenges in attracting and maintaining personnel. The AG concluded by assuring the Committee that they will continue to pursue conversations with employees to foster a better working environment.

Members showed considerable concern with the independence of the OAG in the current funding model and questioned whether or not they were appropriately resourced. All Members pointed out the increasing expression of mistrust in Government institutions and emphasized the importance of the role of the OAG in maintaining that trust. MP Blake Desjarlais (NDP) questioned all witnesses on the roles of each organization in the events during the OAG employee strike last Fall. Government Members clarified how collective bargaining mandates work and asked TBS to identify the risk in expanding the mandate in terms of the existing agreements.

Follow-Ups

- What legislative changes would be needed for crown corporations to disclose information the same way departments do? – MP Nathalie Sinclair-Desgagné

Next Steps

The Committee is expected to meet next on Friday, November 4, 2022 to discuss Committee Business. The Chair also indicated that the Committee will have a briefing with the Auditor General on the upcoming performance reports on November 15th (in camera). The Chair also indicated that the Committee will invite officials to appear on the Public Accounts 2022 on November 18th.

Bios of the Committee Members

John Williamson (New Brunswick Southwest) Conservative Chair

- Elected as MP for New Brunswick Southwest in 2011, he was then defeated in 2015 and re-elected in 2019 & 2021.

- Currently also serves as a Member of the Liaison Committee and Chair of the Subcommittee on Agenda and Procedure of the Standing Committee on Public Accounts

- Previously served on many committees, including PACP for a brief time in 2013

- Prior to his election, M. Williamson occupied different positions. He was an editorial writer for the National Post from 1998 to 2001, then joined the Canadian Taxpayers Federation until 2008. In 2009, he was hired by Stephen Harper as director of communications in the PMO.

Jean Yip (Scarborough - Agincourt) Liberal First Vice-Chair

- Elected as MP for Scarborough—Agincourt in a by-election on December 11, 2017, and re-elected in 2019 & 2021.

- Has served on Public Accounts (since 2018), as well as Government Operations and Canada-China committees in the past.

- Vice-Chair of the Subcommittee on Agenda and Procedure of the Standing Committee on Public Accounts

- Before her election, Ms. Yip was an insurance underwriter and constituency assistant.

Nathalie Sinclair-Desgagné (Terrebonne) Bloc Québécois Second Vice-Chair

- Elected as MP for Terrebonne in the 2021 federal election.

- BQ Critic for Public Accounts; Pandemic Programs; and Federal Economic Development Agencies.

- Vice-Chair of the Subcommittee on Agenda and Procedure of the Standing Committee on Public Accounts

- Worked at the European Investment Bank and at PWC London.

- Return to Quebec in 2017 to pursue a career in the Quebec business world.

Garnett Genuis (Sherwood Park—Fort Saskatchewan) Conservative

- Elected as MP for Sherwood Park—Fort Saskatchewan in 2015, re-elected ion 2019 and 2021

- Conservative Shadow Minister for International Development

- Also serves on the Standing Committee on Foreign Affairs and International Development

- Served on multiple standing committees in the past, including Citizenship and Immigration, Canada-China Relations and Scrutiny of Regulations

- Prior to his election, Mr. Genuis was an assistant to former Prime Minister Stephen Harper and adviser on the staff of former minister Rona Ambrose.

Michael Kram (Regina—Wascana) Conservative

- Elected as MP for Regina—Wascana in 2019, and re-elected in 2021.

- Served as Vice-Chair of the Standing Committee on Industry and Technology, as well as a Member of the standing committees on Transpart, Infrastration and Communities and International Trade

- Prior to his election, Mr. Kram worked for 20 years in the information technology sector, including a number of contract positions with the Department of National Defence.

Kelly McCauley Edmonton West) Conservative

- Elected as the Member of Parliament in 2015 for Edmonton West, re-elected in 2019 and 2021

- Also serves as Chair of the Standing Committee on Government Operations and Estimates

- Former Conservative Shadow Minister for Treasury Board

- Previously served on the COVID-19 Pandemic committee as well as the Subcomittee on Agenda and Procedure of OGGO in 2020

- Before his election in 2015, Mr. McCauley was a hospitality executive specialized in managing hotels and convention centres

- He has a graduate of BCIT in the Hospitality Management program

- He has a history of advocacy for seniors and veterans

Blake Desjarlais (Edmonton Greisbach) NDP

- Elected as MP for Edmonton Greisbach in 2021.

- NDP Critic for Treasury Board; Diversity and Inclusion; Youth; Sport; and Post-secondary Education.

- Also a member of the Subcommittee on Agenda and Procedure of the Standing Committee on Public Accounts

- First openly Two-Spirit person to be an MP, and Alberta’s only Indigenous Member of Parliament.

Valerie Bradford (Kitchener South – Hespeler) Liberal

- Elected as MP for Kitchener South – Hespeler in 2021.

- Also sits on the Science and Research committee and the Subcommittee on Agenda and Procedure of the Standing Committee on Science and Research

- Director of the Canada-Africa Association

- Prior to her election, Ms. Bradford worked as an economic development professional for the City of Kitchener.

Han Dong (Don Valley North) Liberal

- Elected as MP for Don Valley North in 2019, and re-elected in 2021.

- Also sits on the Industry and Technology committee.

- Has served on the Ethics, and Human Resources committees in the past.

- Co-Chair of the Canada-China Legislative Association

- Prior to his election, Mr. Dong worked with Toronto-based high-tech company dedicated to building safer communities and served as the leader of the Chinatown Gateway Committee established by Mayor John Tory.

Peter Fragiskatos (London North Centre) Liberal

Parliamentary Secretary to the Minister of National Revenue

- Elected as MP for London North Centre in 2015, and re-elected in 2019 & 2021.

- Serves as Parliamentary Secretary to the Minister of National Revenue.

- Has served on the Finance, Canada-China, Human Resources, Public Safety, and Foreign Affairs committees in the past.

- Served as a member of the National Security and Intelligence Committee of Parliamentarians (NSICOP).

- Prior to his election, Mr. Fragiskatos was a political science professor at Huron University College and King’s University College, as well as a frequent media commentator on international issues.

Brenda Shanahan (Châteauguay—Lacolle) Liberal

- Elected as MP for Châteauguay—Lacolle in 2015, and re-elected in 2019 & 2021.

- Caucus Chair of the Liberal Party

- Has served on Public Accounts (2016-2018), as well as Ethics, Government Operations, and MAID committees in the past.

- Has served as a member of the National Security and Intelligence Committee of Parliamentarians (NSICOP).

- Prior to her election, Ms. Shanahan was a banker and social worker, who has also been involved in a number of organizations such as Amnesty International and the Canadian Federation of University Women.

Volume I

Variances

Public Accounts 2022

Issue / Question:

The Public Accounts of Canada for fiscal year 2021-2022 were tabled in Parliament by the President of the Treasury Board in October 2022.

Suggested Response:

- The Government of Canada is committed to responsible financial management and oversight.

- The Public Accounts include the audited consolidated financial statements of the Government.

- For the 24th year in a row, the Government of Canada received a clean audit opinion on its consolidated financial statements.

- This demonstrates the high quality of Canada's financial reporting.

Background:

- Production and finalization of the Public Accounts of Canada is a joint responsibility between the Receiver General, the Office of the Comptroller General and the Department of Finance.

- The Public Accounts reflect the Government’s audited consolidated financial statements and other detailed financial information for the fiscal year 2021-2022 that ended March 31, 2022.

- Volume I – includes the audited consolidated financial statements of the Government; the unmodified audit report from the Auditor General; a financial statements discussion and analysis, which presents 10-year comparative financial information; as well as details on certain financial statement components.

- Volume II – includes financial operations of the departments, including the reconciliations of authorities granted and spent.

- Volume III – includes other supplementary information such as losses, claims against the Crown, ex gratia payments and Ministers’ Office expenditures.

- The Auditor General also simultaneously tables in Parliament, through the Speaker of the House, her observations on key financial audits. This year's observations focus on the pandemic measures enacted by the government, pay administration and National Defence's inventory and asset pooled items.

- The Public Accounts are tabled in the House of Commons and undergo a review by the Public Accounts Committee.

- The Public Accounts show a deficit of $90.2B compared to the projected $154.7B deficit in Budget 2021. To note, Budget 2022 revised the projection to $113.8B.

Provision for contingent liabilities

Issue / Question:

Why has the Government of Canada's provision for contingent liabilities increased in the year?

Suggested Response:

- The Government of Canada is committed to honouring its obligations and settling claims which impacts the contingent liability balance.

- The contingent liabilities amount changes annually as estimates are revised for existing liabilities, new claims are filed against the Crown, and settlements are reached.

- This year's increase is mainly due to efforts to advance reconciliation with Indigenous People.

- The Government of Canada's contingent liabilities are reviewed on a quarterly basis as required by Treasury Board's Directive on Accounting Standards to ensure that they fairly represent the financial position of Canada.

Background:

- The agreement-in-principle ($20B) was reached in December 2021 on a global resolution related to compensation for those harmed by underfunding of the First Nations Child and Family Services program and Jordan's Principle. This resulted in an increase to the pending and threatened litigation and other claims balance of $4B during the year. This amount was offset by a decrease of $2B for the settlement of Safe Drinking Water.

- Pending and threatened litigation and other claims has also increased by an additional $2,705M due to claims reassessed as likely or for reassessments of existing accrued contingent liabilities. [This information has been redacted]

In any given year, factors that could increase the provision include:

- Recent Court and Tribunal rulings and precedent setting outcomes from settlements of past grievances and claims with the Government can influence others to bring claims forward against the Government of Canada.

- Social activism such as the “Me too” movement against discrimination, sexual harassment and assault can influence individuals to bring forward claims against the Government of Canada for past injustices.

- A provision is also made when it is likely that a payment will be made to honour a guarantee and when the amount of the anticipated loss can be reasonably estimated. The way the Government structures future funding arrangements with third parties which include a Government guarantee also has the potential to increase the liability.

Other Employee and Veteran Future Benefit Liabilities

Variance Analysis

Issue / Question:

Why are there significant increases in the liabilities for 'other employee and veteran future benefits' on a year over year basis?

Suggested Response :

- Each year, adjustments are made to the liabilities for other employee and veteran future benefits to:

- add the costs of benefits earned by employees during the year and the accrued interest; and

- deduct benefit payments made to employees, retirees and veterans.

- In the 2021-22 FY, these adjustments resulted in a net increase in the liabilities of $8.4B.

- In addition, a portion of previously unrecognized net actuarial losses were expensed this fiscal year, increasing the liabilities by $7.1B.

Background:

- Other employee and veteran future benefit liabilities include:

- Veterans and Royal Canadian Mounted Police disability and other future benefits

- Pensioners’ health care and dental benefits

- Severance and other benefits

- Accumulated sick leave entitlements

- Workers' compensation

- Significant other future benefits sponsored by consolidated Crown corporations and other entities.

- The liabilities are adjusted to record:

- Any plan amendments, curtailments or settlements – In 2022, an amendment was made to introduce new mental health benefits providing immediate coverage to veterans for treatment of certain mental health conditions. The goal is to support veterans’ mental health while their disability benefits application is being processed. This amendment resulted in a one-time past service cost of $102M.

- Recognition of actuarial gains and losses – Consistent with the accounting standards, gains and losses related to experience and changes in actuarial assumptions used to estimate the liabilities are not recorded immediately, rather they are recognized over the average remaining service life of the employee group or the average remaining life expectancy of the benefit recipients under wartime veteran plans.

- Recognition of interest expense – Consistent with the accounting for other long-term liabilities, the Government uses a present value technique to estimate the current value of all future payments to be made under the benefit plans. The interest expense reflects the time value of money and the fact that we are one year closer to making these payments.

- The liabilities for other employee and veteran future benefits are subject to significant volatility. The payments for these benefit plans are made many years into the future and are dependent upon the evolution of factors such as wage increases, workforce composition, retirement rates and mortality rates. The Government estimates these liabilities based upon its historical experience, current facts and circumstances, and expected future developments. Annual changes to the estimates, and changes to the discount rates used to present value the liabilities result in unrealized gains and losses that are recorded as an expense over the average remaining service life of the employee group or the average remaining life expectancy of the benefit recipients under wartime veteran plans.

Enterprise Crown corporations

Issue / Question: