Report on Public Sector Pension Plans as at March 31, 2017

On this page

Overview

Objective and scope of this report

The Government of Canada sponsors a number of defined benefit pension plans for its employees, including the public service, the Royal Canadian Mounted Police (RCMP), the Canadian Armed Forces and the Reserve Force pension plans (the four public sector pension plans), as well as other retirement compensation arrangements. These plans are one of the benefits the government offers to help recruit and retain the highly skilled workforce that is required to serve Canadians.

The President of the Treasury Board and the Treasury Board of Canada Secretariat have overarching policy responsibility for the four main public sector pension plans, but each plan is managed separately and has its own governance structure and reporting requirements.

This report provides an overview of these plans and complements the annual and actuarial reports of each plan. The appendix contains general information on each plan.

Data in this report is for fiscal year ended March 31, 2017. If data to that date is not available, data from other years is presented and noted. All data presented is from publicly available documents.

Year at a glance, fiscal year ended March 31, 2017

Plan membership

837,619Footnote * members

including active contributors and retired members

Pension obligation

$276.5 billionFootnote *

Total pension obligation

Rates of return

12.8%

Annual net rate of return

6.0%

Annualized net rate of return over the last 10 years

Investments

$135.6 billion

Pension plan assets invested by the Public Sector Pension Investment Board

ContributionsFootnote **

$6,291 million

Employer and employee cash contributions

Expenses

$550 million

Administrative expenses for day-to-day operations of the plans

$11.6 billion

Total pension expenses incurred by the government

Average annual pension paid to retired members

Public service: $30,034

RCMP: $42,649

Canadian Armed Forces (CAF) and Reserve Force (RF): $26,908Footnote *

Roles and responsibilities

The four main public sector pension plans are contributory defined benefit pension plans established under legislation.Footnote 1 The plans provide retirement benefits to eligible plan members upon retirement and survivor benefits to their survivors upon the member’s death.

Pursuant to legislation, the following officials are responsible for the pension plans indicated:

- President of the Treasury Board: the public service pension plan

- Minister of National Defence: the Canadian Armed Forces and the Reserve Force pension plans

- Minister of Public Safety and Emergency Preparedness: Royal Canadian Mounted Police (RCMP)

The President of the Treasury Board is responsible for the funding of all of these plans.

To support their respective ministers, the Treasury Board of Canada Secretariat, the Department of National Defence and the RCMP develop policy and legislation, provide program advice and interpretation, provide financial analysis, and prepare financial statements and annual reports for their pension plans.

Public Services and Procurement Canada (PSPC) handles the day-to-day administration of the plans, including determining eligibility for benefits and calculating and paying benefits for the public service and RCMP pension plans and, as of July 2016, for the Canadian Armed Forces and Reserve Force pension plans.

The Office of the Chief Actuary, an independent unit of the Office of the Superintendent of Financial Institutions, performs periodic actuarial valuations for funding purposes and calculates the yearly pension obligations included in the pension plans’ financial statements.

The Public Sector Pension Investment Board (PSPIB) is responsible for managing the funds transferred to it by the four main public sector pension plan funds and for maximizing investment returns without undue risk of loss, having regard to the funding, policies and requirements of the pension plans. The PSPIB is a Crown corporation established under the Public Sector Pension Investment Board Act that is accountable to Parliament through the President of the Treasury Board. The PSPIB has been investing for the public service, the RCMP and the Canadian Armed Forces pension plans since April 1, 2000, and for the Reserve Force pension plan since March 1, 2007.

Membership

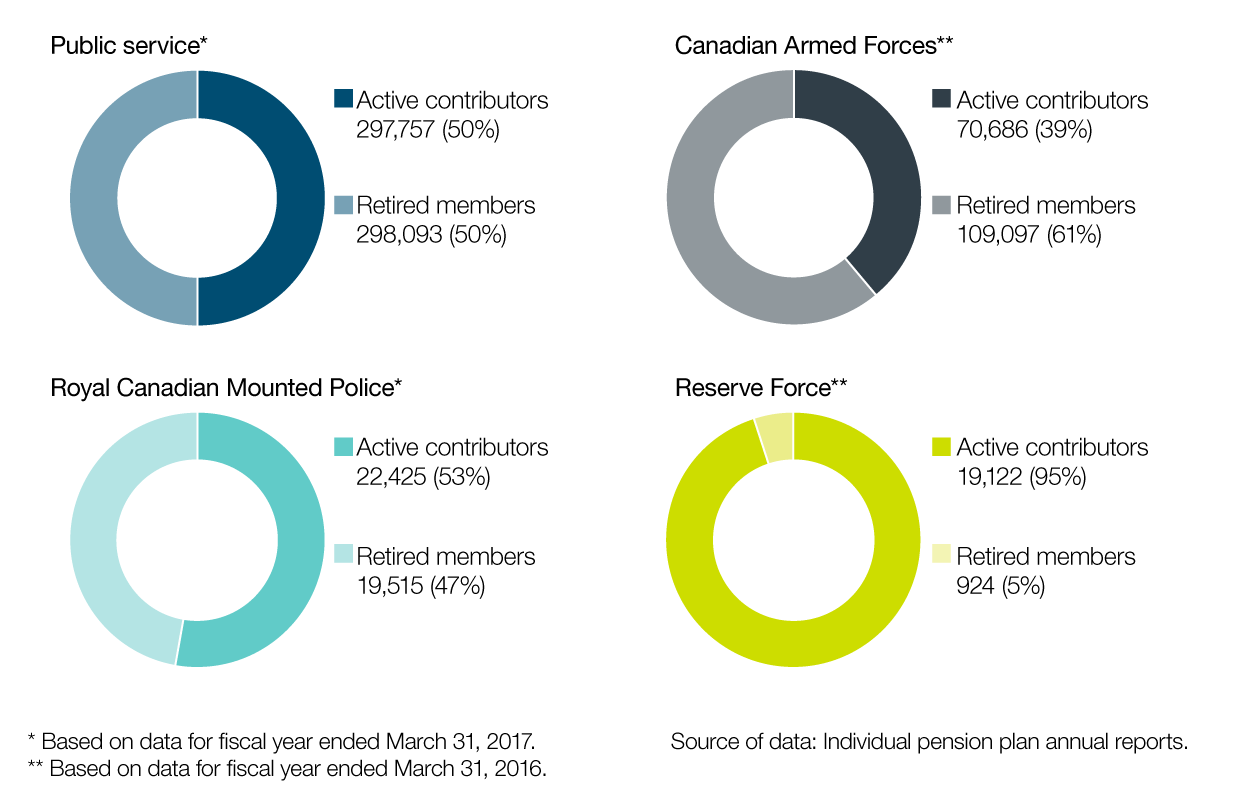

Figure 1 shows the number of active contributors and retired members including survivors and deferred annuitants for each pension plan.

Figure 1 - Text version

| Number | % of total | |

|---|---|---|

Figure 1 Table 1 Notes

Source of data: Individual pension plan annual reports. |

||

| Active contributors | 297,757 | (50%) |

| Retired members | 298,093 | (50%) |

| Public service total | 595,850 | (100%) |

| Number | % of total | |

|---|---|---|

Figure 1 Table 3 Notes

Source of data: Individual pension plan annual reports. |

||

| Active contributors | 70,686 | (39%) |

| Retired members | 109,097 | (61%) |

| Public service total | 179,783 | (100%) |

| Number | % of total | |

|---|---|---|

Figure 1 Table 2 Notes

Source of data: Individual pension plan annual reports. |

||

| Active contributors | 22,425 | (53%) |

| Retired members | 19,515 | (47%) |

| Public service total | 41,940 | (100%) |

| Number | % of total | |

|---|---|---|

Figure 1 Table 4 Notes

Source of data: Individual pension plan annual reports. |

||

| Active contributors | 19,122 | (95%) |

| Retired members | 924 | (5%) |

| Public service total | 20,046 | (100%) |

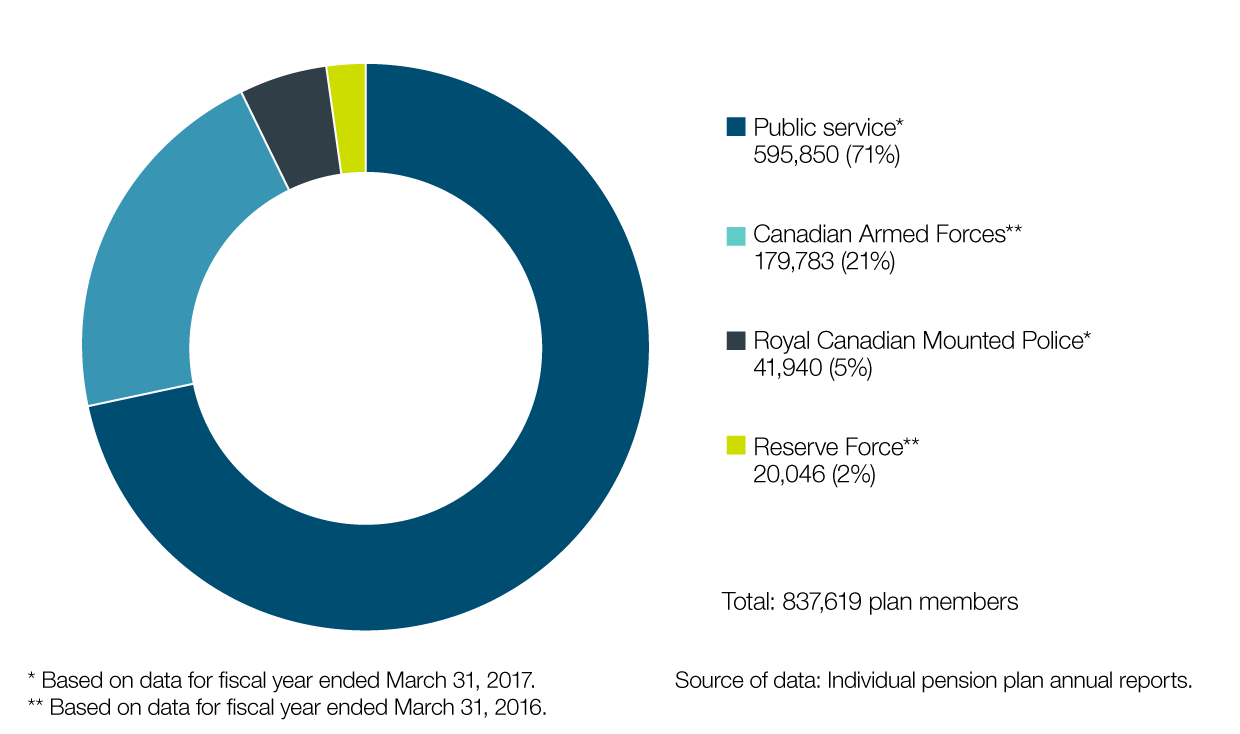

Figure 2 shows the number of active contributors and retired members including survivors and deferred annuitants for each of the four pension plans.

Figure 2 - Text version

| Total | % of total | |

|---|---|---|

Figure 2 Table 1 Notes

Source of data: Individual pension plan annual reports. |

||

| Public servicefigure 2 table 1 note * | 595,850 | (71%) |

| Canadian Armed Forcesfigure 2 table 1 note ** | 179,783 | (21%) |

| Royal Canadian Mounted Policefigure 2 table 1 note * | 41,940 | (5%) |

| Reserve Forcefigure 2 table 1 note ** | 20,046 | (2%) |

| All plans total | 837,619 | (100%) |

Benefits payable to retired members

Figure 3 shows average annual pensions paid to retired members and survivors from 2008 to 2017.

Figure 3 - Text version

| Fiscal years | Public service (dollars) |

Royal Canadian Mounted Police (dollars) |

Canadian Armed Forces and Reserve Force (dollars) |

|---|---|---|---|

Figure 3 Table 1 Notes

Source of data: Individual pension plan annual reports |

|||

| 2008 | 19,273 | 33,533 | 21,002 |

| 2009 | 20,107 | 34,610 | 21,684 |

| 2010 | 20,945 | 35,561 | 22,783 |

| 2011 | 21,584 | 36,114 | 22,970 |

| 2012 | 22,566 | 36,848 | 23,443 |

| 2013 | 22,883 | 37,930 | 24,382 |

| 2014 | 23,746 | 38,940 | 24,851 |

| 2015 | 24,141 | 39,715 | 25,696 |

| 2016 | 29,314 | 40,828 | 26,908 |

| 2017figure 3 table 1 note * | 30,034 | 42,649 | N/A |

The average pension paid to retired members and survivors was as follows:

- Public service: $30,034 (for fiscal year ended March 31, 2017)

- RCMP: $42,649 (for fiscal year ended March 31, 2017)

- Canadian Armed Forces and Reserve Force: $26,908 (for fiscal year ended March 31, 2016)

Contributions

Public sector pension plan benefits are funded through compulsory contributions from the employer and plan members, as well as from investment earnings. Figure 4 shows, for each plan, the share of cash contributions by the employer and by plan members. Cash contributions include current service and past service contributions (for example, service buybacks) and do not include actuarial adjustments.Footnote 2

Figure 4 - Text version

| Public service (in millions)table 4 note * | Public service (in percentage)table 4 note * | Royal Canadian Mounted Police (in millions)table 4 note * | Royal Canadian Mounted Police (in percentage)table 4 note * | Canadian Armed Forces (in millions)table 4 note ** | Canadian Armed Forces (in percentage)table 4 note ** | Reserve Force (in millions)table 4 note ** | Reserve Force (in percentage)table 4 note ** | |

|---|---|---|---|---|---|---|---|---|

Table 4 Notes

|

||||||||

| Employer’s share | $2,330 | 52% | $251 | 56% | $755 | 63% | $72 | 57% |

| Plan members’ share | $2,183 | 48% | $195 | 44% | $450 | 37% | $55 | 43% |

| Total | $4,513 | 100% | $446 | 100% | $1,205 | 100% | $127 | 100% |

Plan members’ contributions are a percentage of their salary and are collected through payroll deductions. Members contribute at a lower rate on salary up to the yearly maximum pensionable earnings (YMPE) that apply under the Canada Pension Plan and the Québec Pension Plan. In 2017, the YMPE was $55,300.

The public service pension plan has 2 groups of plan members:

- Group 1: members who were participating in the plan on or before December 31, 2012

- Group 2: members who began participating in the plan on or after January 1, 2013

The employee contribution rates are approved on calendar basis. Table 1 shows members’ contribution rates as a percentage of their salary for 2017.

| Salary | Public service | Canadian Armed Forces | RCMP | Reserve Forcetable 1 note ** | |

|---|---|---|---|---|---|

| Group 1 | Group 2 | ||||

Table 1 Notes

Source of data: Public Accounts of Canada 2017, section 6 |

|||||

| Up to the YMPE | 9.2% | 8.0% | 9.2% | 9.2% | 5.2% |

| Above the YMPE | 11.2% | 9.5% | 11.2% | 11.2% | |

Since April 1, 2000 (March 1, 2007 for the Reserve Force pension plan), plan member and employer contributions, net of benefit payments and other charges to the plans, have been transferred to the PSPIB for investment.

Before April 1, 2000, employer and plan member contributions were not invested. Contributions, as well as benefit payments, interest, charges and transfers that pertain to service before April 1, 2000, have been tracked in the superannuation accounts in the Public Accounts of Canada.

Financial overview

-

In this section

Figure 5 shows the value of net assets held by the PSPIB for each pension plan, as at March 31, 2017.

Figure 5 - Text version

| Fiscal year | Public service | Canadian Armed Forces | Royal Canadian Mounted Police | Reserve Force | Total |

|---|---|---|---|---|---|

Source of data: Public Sector Pension Investment Board, Annual Report 2017 |

|||||

| 2017 | $98.5 billion (72.7%) | $26.7 billion (19.7%) | $9.8 billion (7.2%) | $0.6 billion (0.4%) | $135.6 billion |

Total value of net assets held by Public Sector Pension Investment Board: $135.6 billion

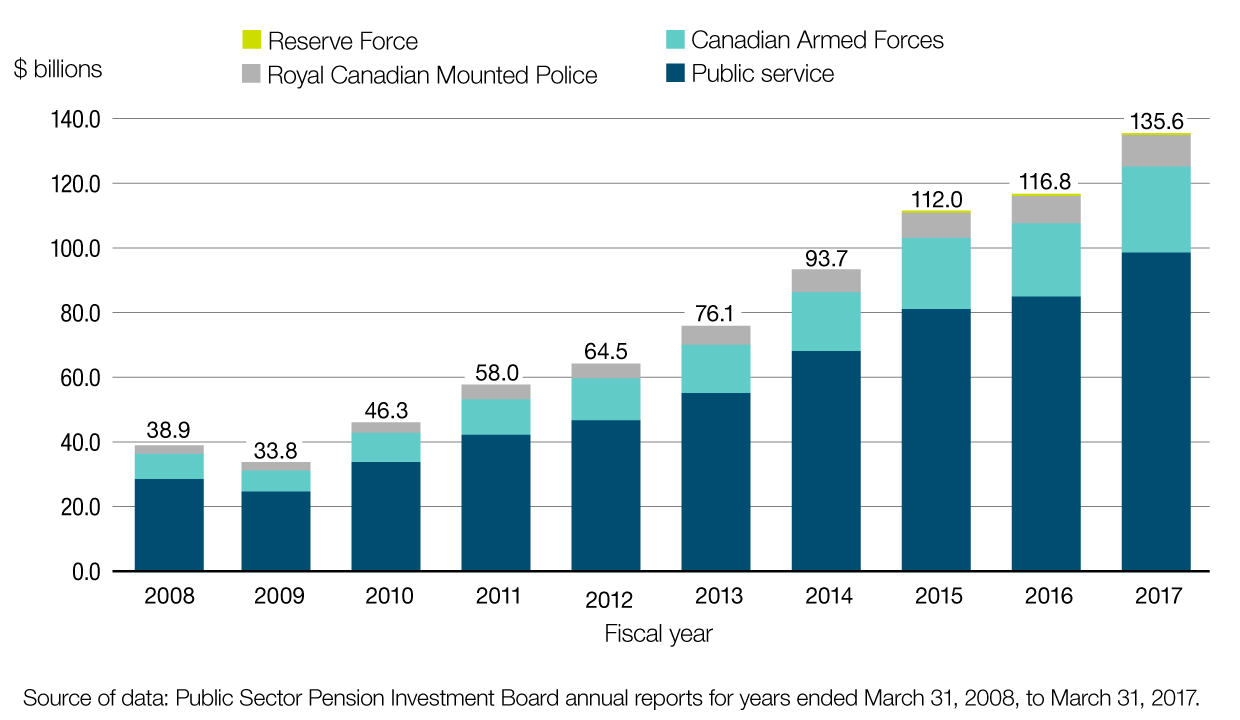

Figure 6 shows the total value of net pension plan assets held by the PSPIB each year over the last 10 years.

Figure 6 - Text version

| Fiscal years | Public service (billions) |

Canadian Armed Forces (billions) |

Royal Canadian Mounted Police (billions) |

Reserve Force (billions) |

Total (billions) |

|---|---|---|---|---|---|

Source of data: Public Sector Pension Investment Board annual reports for years ended March 31, 2008, to March 31, 2017 |

|||||

| 2008 | 28.3 | 7.8 | 2.8 | 0.1 | 38.9 |

| 2009 | 24.5 | 6.8 | 2.4 | 0.1 | 33.8 |

| 2010 | 33.7 | 9.1 | 3.3 | 0.2 | 46.3 |

| 2011 | 42.3 | 11.3 | 4.1 | 0.3 | 58.0 |

| 2012 | 47.1 | 12.4 | 4.6 | 0.4 | 64.5 |

| 2013 | 55.5 | 14.9 | 5.4 | 0.4 | 76.1 |

| 2014 | 68.2 | 18.4 | 6.7 | 0.5 | 93.7 |

| 2015 | 81.3 | 22.0 | 8.1 | 0.6 | 112.0 |

| 2016 | 84.7 | 23.0 | 8.5 | 0.6 | 116.8 |

| 2017 | 98.5 | 26.7 | 9.8 | 0.6 | 135.6 |

Investment asset mix

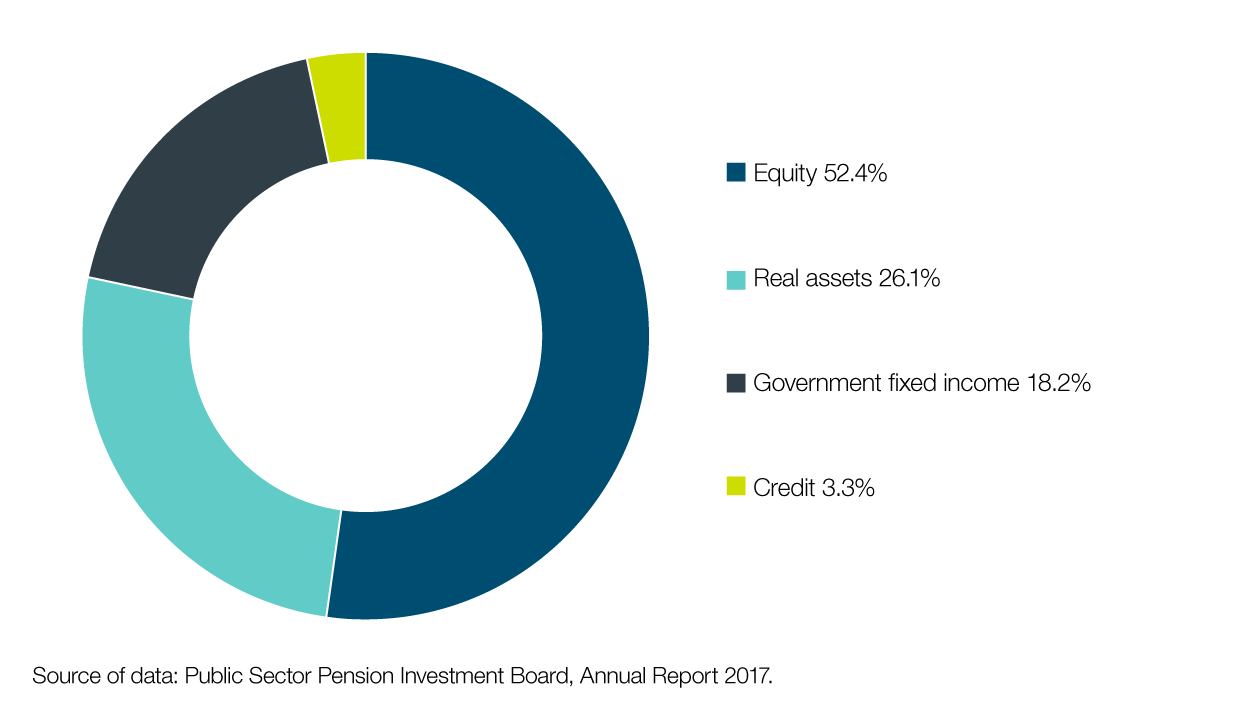

As part of its investment approach, the PSPIB has developed a diverse policy portfolio designed to mitigate risks. The policy portfolio represents the long-term target asset allocation among various asset classes. The PSPIB’s actual investment asset mix is based on the policy portfolio.

Figure 7 shows the PSPIB’s investment asset mix as at March 31, 2017.

Figure 7 - Text version

| PSPIB investment | |

|---|---|

Source of data: Public Sector Pension Investment Board, Annual Report 2017 |

|

| Equity | 52.4% |

| Real assets | 26.1% |

| Government fixed income | 18.2% |

| Credit | 3.3% |

Investment returns

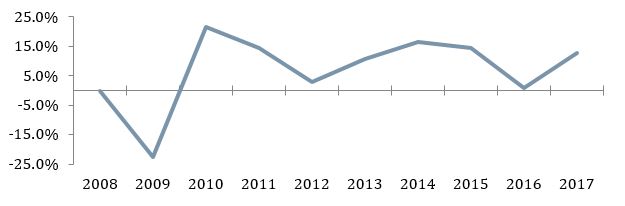

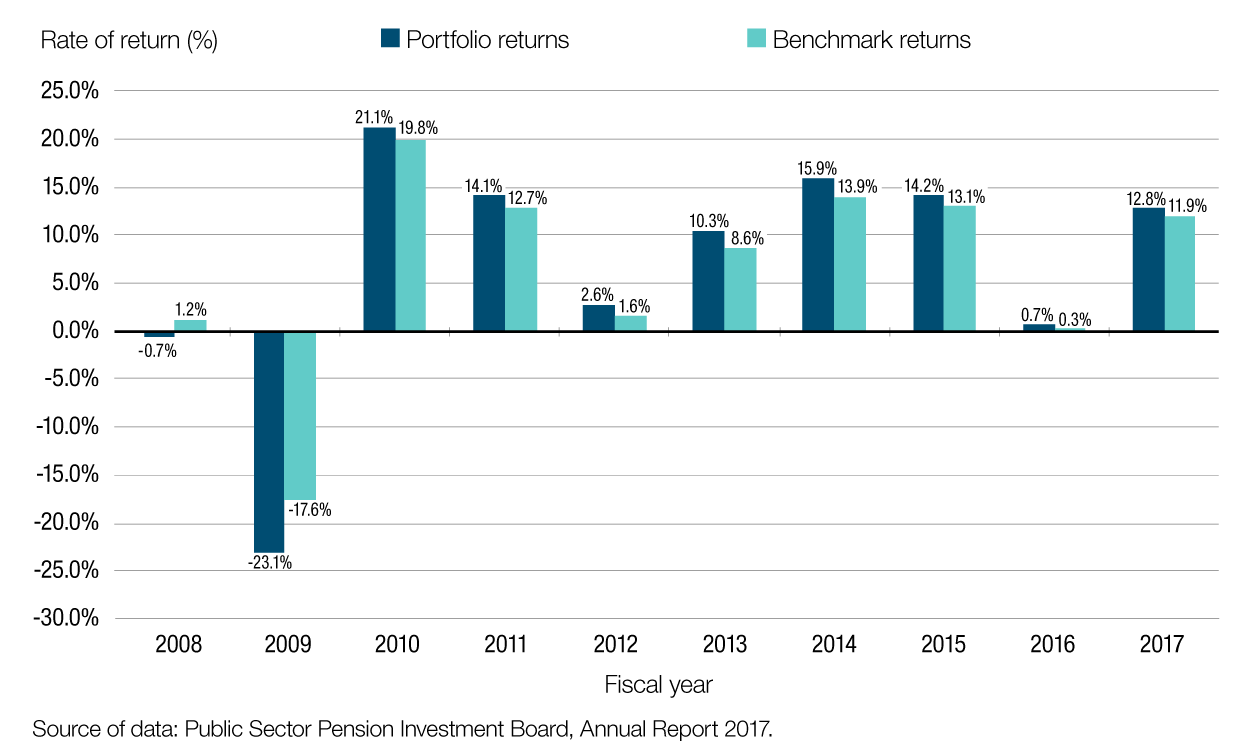

The PSPIB reported a net rate of return of 12.8% for fiscal year ended March 31, 2017, and an annualized net rate of return of 6.0% over the last 10 years, which surpassed the return objective of 5.8% for the same period.

The PSPIB has generated above-benchmark returns in 8 of the past 10 years, including 2017. It has accomplished this by taking a disciplined approach to investment and ensuring an appropriate balance between risks and returns. Responsible corporate governance mechanisms are in place to allow for appropriate control of investment risk and costs.

Figure 8 shows the annual net rate of return on assets held by the PSPIB against its comparative benchmark at year ended March 31.

Figure 8 - Text version

| Fiscal years | Portfolio returns | Benchmark returns |

|---|---|---|

Source of data: Public Sector Pension Investment Board, Annual Report 2017. |

||

| 2008 | -0.7% | 1.2% |

| 2009 | -23.1% | -17.6% |

| 2010 | 21.1% | 19.8% |

| 2011 | 14.1% | 12.7% |

| 2012 | 2.6% | 1.6% |

| 2013 | 10.3% | 8.6% |

| 2014 | 15.9% | 13.9% |

| 2015 | 14.2% | 13.1% |

| 2016 | 0.7% | 0.3% |

| 2017 | 12.8% | 11.9% |

More information on the net rate of return on assets held by the PSPIB and comparative benchmarks is available on the PSPIB’s website.

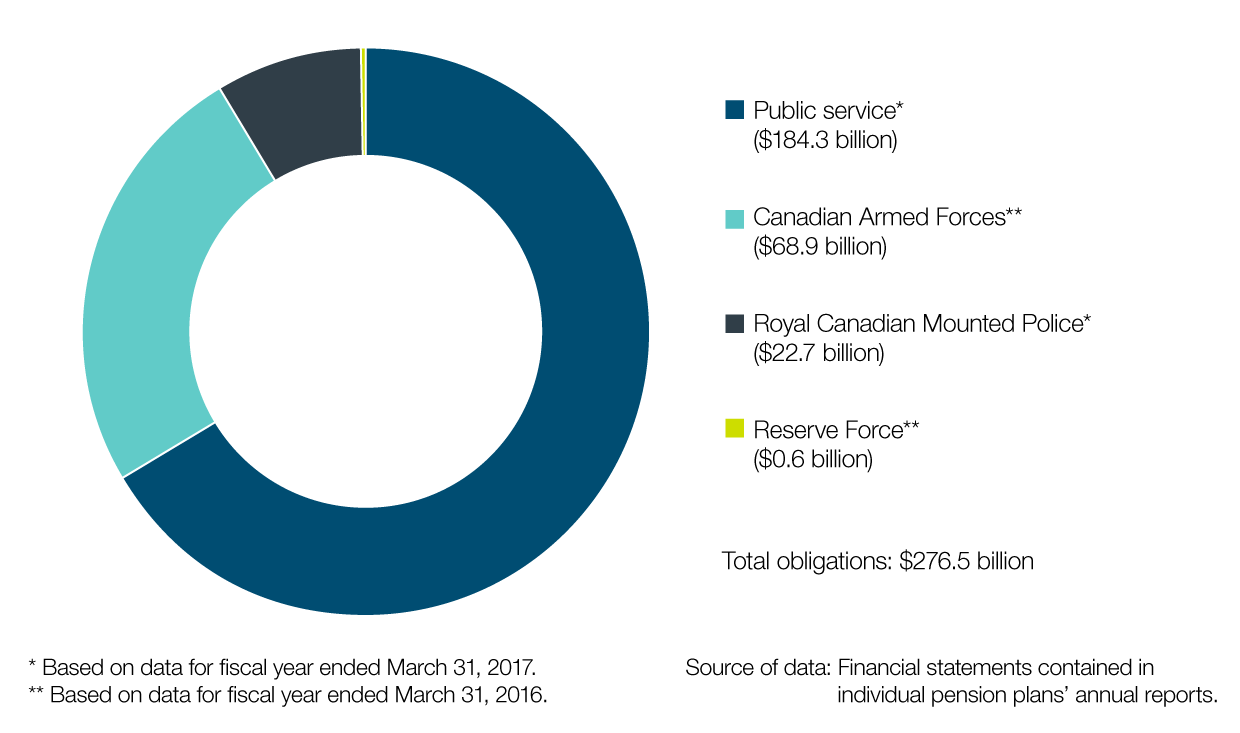

Figure 9 shows the total pension obligations of the four main public sector pension plans. As at March 31, 2017 (for the public service and RCMP pension plans), and as at March 31, 2016 (for the Canadian Armed Forces and the Reserve Force pension plans), total pension obligations were $276.5 billion.

Figure 9 - Text version

| Public servicefigure 9 table 1 note * | Canadian Armed Forcesfigure 9 table 1 note ** | Royal Canadian Mounted Policefigure 9 table 1 note * | Reserve Forcefigure 9 table 1 note ** | Total liabilities | |

|---|---|---|---|---|---|

Figure 9 Table 1 Notes

Source of data: Financial statements contained in individual pension plans’ annual reports. |

|||||

| Obligations (in billions) | 184.3 | 68.9 | 22.7 | 0.6 | 276.5 |

Administrative expenses

The legislation provides for the pension-related administrative expenses of the following government organizations to be charged to the public sector pension plans:

- the Treasury Board of Canada Secretariat

- the Department of National Defence

- the RCMP

- Public Services and Procurement Canada

- Health Canada

- the Office of the Chief Actuary

The administrative expenses of the PSPIB are also charged to the plans.

Figure 10 shows the administrative expenses charged to the plans for the last 10 years as shared between government organizations and the PSPIB (left axis, in $ millions) and the assets held by the PSPIB (right axis, in $ billions). Figure 10 also shows the relation between administrative expenses and increases in the value of assets held by the PSPIB.

Figure 10 - Text version

| Fiscal years | Government organizations (millions) | Public Sector Pension Investment Board (millions) | Total (millions) | Assets held by Public Sector Pension Investment Board (billions) |

|---|---|---|---|---|

Source of data: Public Sector Pension Investment Board annual reports and the Public Accounts of Canada for years ended March 31, 2008 to March 31, 2017 |

||||

| 2008 | 115 | 77 | 192 | 38.9 |

| 2009 | 146 | 87 | 233 | 33.8 |

| 2010 | 163 | 92 | 256 | 46.3 |

| 2011 | 165 | 114 | 279 | 58.0 |

| 2012 | 160 | 148 | 308 | 64.5 |

| 2013 | 179 | 184 | 363 | 76.1 |

| 2014 | 191 | 216 | 407 | 93.7 |

| 2015 | 186 | 243 | 429 | 112.0 |

| 2016 | 191 | 295 | 487 | 116.8 |

| 2017 | 169 | 381 | 549 | 135.6 |

In fiscal year ended March 31, 2017, total administrative expenses for the public sector pension plans were $550 million. Administrative expenses for each pension plan were as follows:

- Public service pension plan: $376 millionFootnote3

- RCMP pension plan: $36 million

- Canadian Armed Forces pension plan: $125 million

- Reserve Force pension plan: $13 million

Impact on public finances

Table 2 shows a summary of transactions for the plans that resulted in expenses for the Government of Canada in the fiscal year ended March 31, 2017. These expenses are calculated based on Canadian public sector accounting standards and are included in the Public Accounts of Canada 2016–17.

The pension expense includes employers’ contributions and recognized actuarial valuation gains and losses and other adjustments.

The net interest expense is calculated based on the average accrued pension obligations (benefits earned by members under their pension plan for pensionable service).

Changes in actuarial assumptions can have a significant impact on the pension expense and obligation. Table 4 shows the impact of changes to certain key assumptions on the pension plans’ obligations.

| Pension plan | Pension expense | Net interest expense | Total expense |

|---|---|---|---|

| Source of data: Public Accounts of Canada 2017, Table 6.16 | |||

| Public service | $3,153 | $4,070 | $7,223 |

| Canadian Armed Forces | 1,435 | 2,008 | 3,443 |

| RCMP | 350 | 579 | 929 |

| Reserve Force | 17 | 1 | 18 |

| Total expenses | $4,955 | $6,658 | $11,613 |

Pension plan funding

Key measures to support sustainability

The governance framework of the public sector pension plans includes key measures that help ensure that the plans remain sustainable and affordable for plan members and taxpayers. These measures include:

- actuarial valuations, which provide an estimate of expenses and obligations

- reviews of the funded status of the plans

- the pension plans’ annual reports

Each plan also has an advisory committee that comprises representatives of the employer, active plan members and retired plan members. These committees provide additional oversight, accountability and transparency by reviewing administration, design and funding of benefits.

In fiscal year ended March 31, 2017, employee contribution rates continued to be increased for the public service pension plan to ensure a more equitable sharing of the cost of the pension plan between the employer and plan members. By the end of 2017, after a 5-year process, the targeted employer-employee cost sharing ratio of 50:50 was reached. Comparable changes to the Canadian Armed Forces and the RCMP pension plans are also being made.

Steps continue to be taken to address the 2014 Auditor General of Canada’s performance audit of the public sector pension plans. Building on the previous year’s benchmarking of pension governance practices, the Treasury Board of Canada Secretariat, in consultation with the RCMP and the Department of National Defence, conducted an in-depth governance review and advanced a funding policy proposal to provide guidance to ensure the long-term sustainability of the public sector pension plans.

Actuarial valuations

Actuarial valuations are performed regularly to support the administration of the pension plans. The Office of the Chief Actuary performs 2 types of actuarial valuations:

- Actuarial valuations for funding purposes are conducted at least once every 3 years to determine the contribution rates, actuarial liability and the funded status of the plans. These valuations help the President of the Treasury Board make informed decisions on the financing of the pension plans. Assessments of the funded status of the pension plans are done annually, in consultation with the Office of the Chief Actuary.

- Actuarial valuations for accounting purposes are performed as at March 31 of each fiscal year to measure and report on the pension expense and obligations in the Public Accounts of Canada, and to provide the necessary information to prepare the plans’ financial statements.

Methodology and assumptions used in actuarial valuations

Economic assumptions are set in order to conduct actuarial valuations. Population characteristics and benefit provisions are specific to each pension plan. Assumptions underlying the actuarial valuation for accounting purposes are based on management’s best estimates. The Office of the Chief Actuary determines the best-estimate assumptions used in actuarial valuations for funding purposes.

As part of the economic assumptions, discount rates are used to determine the present value of the future pension payments (the pension obligation), the costs of benefits earned, and the interest expenses.

Discount rates are set as follows:

- For funded pension benefits (post-March 2000), the discount rates are streamed expected rates of return on funds invested by the PSPIB.

- For unfunded pension benefits (pre-April 2000), the discount rates are the streamed weighted average of Government of Canada long-term bond rates. The streamed weighted average of Government of Canada long-term bond rates is a calculated 20-year weighted moving average of Government of Canada long-term bond rates projected over time. The streamed rates take into account historical Government of Canada long-term bond rates and, over time, reflect expected Government of Canada long-term bond rates.

Table 3 shows some of the key economic assumptions used in the most recent actuarial valuations.

| Actuarial report | Long-term discount rate | Long-term rate | ||

|---|---|---|---|---|

| Unfunded pension benefits (pre-April 2000) | Funded pension benefits (post-March 2000)table 3 note * | Salary increase | Pension indexation | |

Table 3 Notes

Sources: Actuarial reports of the Office of the Chief Actuary and Public Accounts of Canada 2017 |

||||

| For accounting purposes (as at March 31, 2017) |

4.7% | 6.0% | 2.6% | 2.0% |

| For funding purposes | ||||

Canadian Armed Forces (as at March 31, 2016) |

4.7% | 6.0% | 2.8% | 2.0% |

Reserve Force (as at March 31, 2016) |

N/A | 6.0% | 2.8% | 2.0% |

RCMP (as at March 31, 2015) |

4.8% | 6.1% | 2.9% | 2.0% |

Public service (as at March 31, 2014) |

4.8% | 6.1% | 2.9% | 2.0% |

Sensitivity analysis of actuarial assumptions

Changes in actuarial assumptions for valuation sensitivity analysis purposes can result in significantly higher or lower estimates of the accrued pension obligations. Table 4 shows the impact of a 1% increase or decrease to the long-term actuarial assumptions on the four main public sector pension plans, as well as the other pension arrangements for members of Parliament, federally appointed judges, non-career diplomats, the Governor General and lieutenant governors, and retirement compensation arrangements.

| Changes in actuarial assumptions | Unfunded pension benefits (pre-April 2000) |

Funded pension benefits (post-March 2000) |

|---|---|---|

| Source: Public Accounts of Canada 2017, section 2 | ||

| Increase of 1% in discount rates | (6,400) | (20,000) |

| Decrease of 1% in discount rates | 7,700 | 26,100 |

| Increase of 1% in rate of inflation | 21,200 | 17,200 |

| Decrease of 1% in rate of inflation | (17,700) | (14,100) |

| Increase of 1% in general wage increase | 1,100 | 6,500 |

| Decrease of 1% in general wage increase | (800) | (5,800) |

Actuarial valuation report balances

Tables 5 and 6 show the balances of the superannuation account and the pension fund of each pension plan as of the last triennial funding valuation.

| Balance | Canadian Armed Forces 2016 |

Reserve Force 2016 |

RCMP 2015 |

Public Service 2014 |

|---|---|---|---|---|

| Source: Actuarial reports of the Office of the Chief Actuary | ||||

| Account balance | $45,718 | n/a | $13,203 | $96,530 |

| Actuarial liability | $47,385 | n/a | $13,428 | $97,211 |

| Balance | Canadian Armed Forces 2016 |

Reserve Force 2016 |

RCMP 2015 |

Public Service 2014 |

|---|---|---|---|---|

| Source: Actuarial reports of the Office of the Chief Actuary of Canada. | ||||

| Actuarial value of assets | $22,478 | $513 | $7,286 | $63,151 |

| Actuarial liability | $24,048 | $566 | $7,440 | $66,775 |

Source documents

- Report on the Public Service Pension Plan for the Fiscal Year ended March 31, 2017

- Royal Canadian Mounted Police Pension Plan: Annual Report, 2016–17

- 2015–16 Annual Report: Canadian Armed Forces Pension Plans

- Public Sector Pension Investment Board annual reports, 2008 to 2017

- Public Accounts of Canada 2016–17

- Actuarial Report on the Pension Plan for the Public Service of Canada as at 31 March 2014

- Actuarial Report on the Pension Plan for the Royal Canadian Mounted Police as at 31 March 2015

- Actuarial Report on the Pension Plans for the Canadian Forces Regular Force and Reserve Force as at 31 March 2016

Glossary

- actuarial adjustments

- The special payments that the Government of Canada is required to make to fund actuarial deficits.

- actuarial assumptions

- Economic and demographic assumptions, such as future expected rates of return, inflation, salary levels, retirement ages and mortality rates, that are used by actuaries when carrying out an actuarial valuation or calculation.

- actuarial valuation

- An actuarial analysis that provides information on the financial condition of a pension plan.

- actuarial value of assets

- The actuarial value of assets is a method to value the investments of a pension plan using a 5-year smoothed value. Under this method, the expected return on investments is recorded immediately, while the difference between the expected and actual return on investments is recorded over a 5-year period through actuarial gains and losses. The actuarial value of assets is adjusted, if necessary, to ensure that it does not fall outside a limit of plus or minus 10% of the market value of investments at year end. Any difference is recorded immediately through actuarial gains and losses.

- administrative expenses

- Expenses by government departments for the administration of the public sector pension plans and for operating expenses incurred by the PSPIB to invest pension assets. Investment management fees are either paid directly by the PSPIB or offset against distributions received from the investments.

- benchmark

- A standard against which rates of return can be measured, such as stock and bond market indexes developed by stock exchanges and investment managers.

- contributions

- Sums credited or paid by the employer and plan members to finance future pension benefits. Each year, the employer contributes amounts sufficient to fund the future benefits earned by employees in respect of that year, as determined by the President of the Treasury Board.

- defined benefit pension plan

- A type of pension plan that promises a certain level of pension, which is usually based on the plan member’s salary and years of service. the four main public sector pension plans are defined benefit pension plans.

- pension liability/obligation

- Corresponds to the value, discounted in accordance with actuarial assumptions, of all future payable benefits accrued as of the valuation date in respect of all previous pensionable service.

- pensionable service

- Periods of service to the credit of a public sector pension plan member. This service includes any complete or partial periods of purchased service (for example, service buyback or elective service).

- pension transfers

- Transfers made under an agreement negotiated between the Government of Canada and an eligible employer to provide portability of accrued pension credits from one pension plan to the other.

- service buyback

- A service buyback is a legally binding agreement under which a member purchases a period of prior service to increase his or her pensionable service.

- survivor

- A person who, at the time of a plan member’s death, was married to the plan member before his or her retirement or was cohabiting with the plan member in a conjugal relationship prior to the member’s retirement and for at least 1 year prior to the date of death.

- yearly maximum pensionable earnings (YMPE)

- The maximum earnings based on which contributions are made to the Canada Pension Plan and the Québec Pension Plan during the year. In 2017, yearly maximum pensionable earnings were $55,300 ($54,900 in 2016).

Appendix: General information on the plans

| Element | Group 1table appendix 1 note * (pension eligibility at age 60) |

Group 2table appendix 1 note ** (pension eligibility at age 65) |

|---|---|---|

Table Appendix 1 Notes

|

||

| Contributions | A percentage of member’s salary |

|

| Lifetime pension | 2% × average salary × years of pensionable service (maximum 35 years) (calculation includes bridge benefit) |

|

| Bridge benefit | 0.625% × average salary up to the AMPEtable appendix 1 note *** × years of pensionable service (maximum 35 years) |

|

| Immediate annuity |

|

|

| Deferred annuity |

|

|

| Annual allowance |

|

|

| Transfer value | The actuarial value of the member’s pension benefits, payable in a lump sum. This amount must be transferred to another registered pension plan or to a locked-in retirement savings vehicle. |

|

|

|

|

| Return of contributions |

|

|

| Survivor benefit |

|

|

| Child allowance |

|

|

| Indexation | Pension is increased on January 1 of each year to take into account the cost of living, based on increases in the Consumer Price Index. |

|

| Element | Regular members |

|---|---|

Table Appendix 2 Notes

|

|

| Contributions | A percentage of member’s pensionable earnings aligned with Group 1 rates for the public service pension plan |

| Lifetime pension | 2% × average of best 5 consecutive years of salary × years of pensionable service (maximum 35 years) (calculation includes bridge benefit) |

| Bridge benefit | 0.625% × average salary up to the AMPEtable appendix 2 note * × years of pensionable service (maximum 35 years) |

| Immediate annuity |

|

| Deferred annuity | Between 2 years and less than 20 years of service in the Force: An unreduced pension benefit payable at age 60 |

| Annual allowance | A permanently reduced pension, payable based on more than 20 but less than 25 years of service in the Force |

| Transfer value |

|

| Return of contributions |

|

| Survivor benefits |

|

| Child allowance |

|

| Indexation | Pension is increased on January 1 of each year to take into account the cost of living, based on increases in the Consumer Price Index. |

| Element | Regular Force (CFSA, Part I) | Reserve Force (CFSA, Part I.I) |

|---|---|---|

Table Appendix 3 Notes

|

||

| Contributions | A percentage of member’s pensionable earnings aligned with Group 1 rates of the public service pension plan |

Legislated in the Reserve Force Pension Plan Regulations |

| Lifetime pension | 2% × average of best 5 consecutive years of salary × years of pensionable service (maximum 35 years) (calculation includes bridge benefit) |

1.5% × greater of total pensionable earnings and total updated pensionable earnings |

| Bridge benefit | 0.625% × average salary up to the AMPEtable appendix 3 note * × years of pensionable service (maximum 35 years) |

0.5% × greater of total bridge benefit earnings and total updated bridge benefit earnings |

| Immediate annuity |

|

|

|

|

|

| Deferred annuity | At least 2 years of pensionable service: Accrued pension calculated according to the pension formula, payable at age 60 |

|

| Annual allowance | At least 2 years of pensionable service: A permanently reduced pension, payable as early as age 50 and before age 60 |

|

| Transfer value | The actuarial value of the member’s pension benefits, payable in a lump sum. This amount must be transferred to another registered pension plan or to a locked-in retirement savings vehicle. |

|

| Return of contributions |

|

|

| Survivor benefit |

|

|

| Child allowance |

|

|

| Indexation | Pension is increased on January 1 of each year to take into account the cost of living, based on increases in the Consumer Price Index. |

|

© Her Majesty the Queen in Right of Canada, represented by the President of the Treasury Board, 2018,

ISSN: 2561-9047