Benefits: Access and portability - Issue paper

From: Employment and Social Development Canada

Disclaimer: This paper is one of a series of papers prepared by the Secretariat to the Expert Panel on Modern federal labour standards as background information to stimulate the Panel's discussions. The papers do not necessarily reflect the views of the Government of Canada.

On this page

- Issue

- Background

- Benefits and the Canada Labour Code

- Situation in the federally regulated private sector

- What the research says

- Stakeholder perspectives

- Policy responses in Canada and other jurisdictions

- Private sector and worker responses in Canada and other jurisdictions

- Issues for the panels’s consideration

- Annex A

- Selected bibliography

Issue

Benefits, including statutory minimums such as annual vacations and leaves as well as employer-provided benefits such as medical and retirement savings plans, make crucial contributions to the personal and financial security of Canadian workers. Access to benefits has traditionally been based on full-time long-term employment with one employer. Workers who change jobs frequently and those who spend part of their working life in non-standard work may not have access to them. Should the federal government take steps to enhance access to benefits in the federally regulated private sector and/or improve portability? If so, what measures should be considered?

Background

The persistence and potential future growth in the share of workers in non-standard work, combined with the insecurity that non-standard jobs tend to entail, have placed a spotlight on the issue of whether there is a need to enhance access to benefits and make them more portable for workers, especially those who move jobs often or work in non-standard work.

There are two key types of benefits:

- statutory minimums, such as annual vacation and leaves

- employer-provided benefits, such as medical, dental and vision insurance, pensions and retirement savings plans

Traditionally, access to statutory minimums in the federally regulated private sector (FRPS) has been limited to employees covered under Part III of the Canada Labour Code (the Code) who have completed an eligibility period. Though employees in standard work are more likely to have access to these benefits and be able to keep them, this access is contingent on remaining with the same employer for long periods of time. If employees in standard work change jobs, they cannot transfer the statutory minimums to which they were entitled to their new job and instead must start over with no continuous employment period. In addition, entitlements such as annual vacation and severance pay increase as an employee stays longer in their job.

Workers in non-standard work, on the other hand, are less likely to meet the requirements for statutory minimums in the first place. Temporary employees in short-term relationships with multiple employers, for example, may not meet the length of service requirements with one employer and, like other employees, generally cannot “carry” what they have acquired with them when they change employers. Workers who are not considered employees (for example independent contractors) are not entitled to any statutory minimums under Part III.

Access to employer-provided benefits is traditionally available to employees who meet prescribed eligibility criteria, including length of service and hours worked. While employees in standard work can usually access the benefits offered by their employer, options for portability are limited if they exist at all (for example pension transfer agreements). Therefore, those who are interested in changing employers within their field or transitioning to a new type of work may have to consider the potential loss of their accumulated benefits against their professional goals and aspirations.

Workers in non-standard work are often treated differently when it comes to employer-provided benefits. For example, temporary and part-time employees may not be eligible for the same insurance plans and pensions as permanent, full-time employees. They also often have difficulty meeting requirements such as working a certain number of hours in a given period. Workers who are not employees (for example dependent and independent contractors) are unlikely to be able to access any employer-provided benefits. Workers who are employed by small businesses, in either standard or non-standard work, are less likely than those working for medium or large businesses to have access to employer-provided benefits.

Benefits security is another concern. In certain circumstances, workers (in standard or non-standard work) as well as retirees may be at risk of losing any benefits to which they are entitled. For example, if an employer goes bankrupt, workers and retirees may lose their coverage under any uninsured benefit plans that were offered by the employer.

For employers, providing benefits to employees has advantages and costs. Total compensation packages—consisting of wages and benefits—are key elements in employers’ efforts to recruit and retain employees and foster loyalty, as well as important factors influencing employees’ job choices. Employers may also choose to offer more than the statutory minimums, such as more annual vacation. However, benefits are often costly for employers to provide, which is one reason why some employers offer access only to employees in standard work. Insuring benefit plans can further increase costs to employers.

Access to and portability of both types of benefits has implications for Canada’s overall system of social protection. The public programs in place to protect and support people are similarly based on longer-term standard work with one employer. Even if workers meet the eligibility requirements, the level of available support is often limited. For example, this year, the maximum monthly payment amount for the Canada Pension Plan (CPP) for someone at age 65 is $1,134.17 (Government of Canada, 2018) and the maximum monthly Old Age Security (OAS) payment regardless of marital status is $600 (Government of Canada, 2018), while retirees in Canada spend nearly double these amounts combined every month ($2,611) on average (Sun Life Financial, 2016). Workers who spend part of their career in part-time work, have employment gaps between contracts or earn a lower income would likely not meet maximum contribution or benefit amountsFootnote 1. Given that they are also less likely to have access to employer-provided retirement savings plans, they are at an even greater risk of an underfunded retirement or being unable to retire at all.

The broader social protection system is also at risk as people engage in non-standard work. In scenarios developed by Policy Horizons (2016) where the nature of work continues to change, potentially lower incomes and more unemployment would contribute to reduced income tax revenues and higher social transfer needs, which would in turn strain the existing system of social protection system.

Limits on access to employer-provided benefits and the portability of these benefits can be major factors contributing to insecurity for workers and their families, as well as weakening of Canada’s social protection system. In addition, they can have economic impacts on the efficiency of the labour market (for example mobility, employer costs), as well as social impacts in areas such as public health and poverty.

While there is growing awareness that benefits access and portability are closely connected to the future of Canada’s social protection system, there is no consensus on how to move forward. The issue raises important questions about benefits and the role of governments, employers, workers, insurance companies and others in paying for and administering them.

Overall, research, policy work and public debate about improving access to statutory and employer-provided benefits and enhancing portability, especially for workers in non-standard work, are in the early stages. There is a need to address key knowledge gaps, crystallize policy thinking and raise awareness and generate dialogue amongst stakeholders, experts, the public and policy-makers. The Expert Panel’s work, though done in the context of labour standards in the FRPS, could help strengthen future thinking about Canada’s social protection regime.

Benefits and the Canada Labour Code

Statutory minimums

Eligibility periods: Part III (Labour Standards) of the Code sets out continuous employment eligibility requirements for certain labour standards. This means that an employee must have worked for the same employer for a certain period of time before being entitled to certain rights and protections. Annex A provides a table of current and new eligibility requirements for annual vacation, holiday pay and leaves.

- Changes to the eligibility requirements for some Part III provisions were introduced in fall 2018 as part of the Budget Implementation Act, 2018, No. 2 (BIA II), which received Royal Assent in December 2018. To address the fact that employees who change jobs often have difficulty meeting eligibility requirements, eligibility periods for a number of leaves will be eliminated and the eligibility period for a third week of annual vacation will be reduced from six years to five years once the changes come into force over the coming months. Employees with 10 years or more of continuous employment will also be eligible for an additional fourth week of annual vacation.

Continuous employment: Per section 189(1) of the Code, when an employee is transferred from one federally regulated employer to another as a result of a sale, lease or merger (or is “otherwise” transferred), their employment before and after the transfer is deemed to be continuous with one employer.

- BIA II included changes that, once in effect, will preserve continuity of employment by ensuring that employees’ length of service is treated as continuous when their employment is transferred from one employer to another through contract retendering within the FRPS or through the transfer of a provincially regulated business to a federally regulated employer, or when an employer’s work, undertaking or business is transferred from the provincial or territorial jurisdiction to the federal jurisdiction. In addition, the changes will extend equal remuneration protection (section 47.3 of the Code) through regulations under Part I (Labour Relations) to unionized contract employees at airports and airlines that provide the same or similar services following contract retendering. The Labour Program will also study the broader issue of collective bargaining in situations of contract retendering.

Multi-employer employment: Division VI of the Code defines “multi-employer employment” as “employment in any occupation or trade in which, by custom of that occupation or trade, any or all employees would in the usual course of a working month be ordinarily employed by more than one employer”. The Canada Labour Standards Regulations further define “multi-employer employment” as “longshoring employment in any port in Canada where by custom the employee engaged in such employment would in the usual course of a working month be ordinarily employed by more than one employer.” The Regulations authorize the Minister to designate by order an association of employers as a “multi-employer unit” at any port(s) if the association establishes a central pay office through which all the member employers pay their employees. The Regulations provide that an employee engaged in multi-employer employment is deemed to be continuously employed for the purposes of the eligibility requirements for a number of labour standards provisionsFootnote 2.

Employer-provided benefits

Part III of the Code does not impose a general obligation on employers to provide employees with supplementary benefit plans. However, they are required to subscribe to a plan that provides an employee who is absent from work due to work-related illness or injury with wage replacement, payable at an equivalent rate to that provided for under the applicable workers’ compensation legislation in the employee’s province of permanent residence.

Part III also requires the accumulation of pensions, health and disability benefits and seniority to continue during the employee’s absence from work for certain purposes (for example work-related injury or illness).

Changes to Part III related to insuring benefit plans were introduced in the Jobs, Growth and Long-term Prosperity Act, which received Royal Assent in 2012. As a result of these changes, Part III now requires every employer that offers a long-term disability plan to its employees to insure that plan with a licensed insurance company. Part III does not require any other types of benefit plans to be insured.

Situation in the federally regulated private sectorFootnote 3

Statutory minimums

According to the 2015 Federal Jurisdiction Workplace Survey (FJWS), 88% of employees in the FRPS have worked for the same employer for more than a year. There are relatively more low-tenure employees in Canada overall (see Table 1).

According to the 2015 FJWS, 59% of employees in the FRPS have worked for their employer for five years or more and these employees will be entitled to a third week of annual vacation when the changes made through BIA II come into force. Thirty-eight per cent of FRPS employees have worked for their employer for 10 years or more and will be entitled to a fourth week of vacation.

| FRPS/Canada | Less than 1 year | 1–5 years | 5–10 years | 10 years or more |

|---|---|---|---|---|

| Employees in the FRPS (2015) | 12% | 29% | 21% | 38% |

| Employees in Canada (2017) | 20% | 32% | 18% | 30% |

Source: FJWS 2015 for the FRPS; Labour Force Survey 2017 for Canada

A small percentage of employees in the FRPS expect to lose their job in the next year by layoff, termination or non-renewal of a contract. According to the 2014 Longitudinal and International Study of Adults (LISA), about 11% of employees in the FRPS reported having a 26-50% chance and 3% reported having over a 50% chance of job loss within the next year. This is similar to the case in Canada overall, where 11% reported having a 26-50% chance and 4% reported having over a 50% chance of job loss in the next year.

Employer-provided benefits

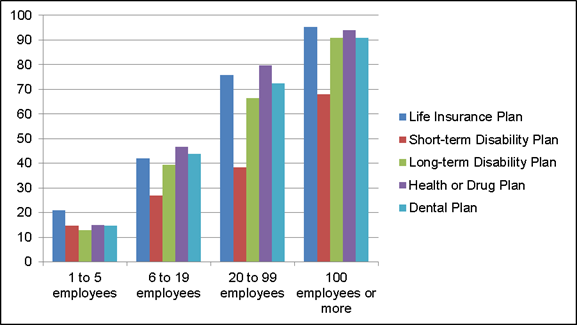

According to the 2015 FJWS, about 47% of FRPS companies reported offering employment-related benefits to their employees in 2015. Companies employing five or fewer employees were about three times less likely to offer benefits than larger companies employing 100 or more employees (35% versus 99%) (see Figure 1).

Figure 1 - Text versionPercentage of employees covered by employer-provided benefits, by firm size, 2015

| Number of employee | Life Insurance Plan | Short-term disability plan | Long-term disability plan | Health or drug plan | Dental plan |

|---|---|---|---|---|---|

| 1 to 5 employees | 21 | 14,7 | 12,9 | 15 | 14,6 |

| 6 to 19 employees | 41,9 | 26,9 | 39,3 | 46,8 | 43,7 |

| 20 to 99 employees | 75,8 | 38,3 | 66,5 | 79,7 | 72,5 |

| 100 employees or more | 95,3 | 68,1 | 91 | 93,9 | 90,9 |

In addition, about 32% of FRPS companies offered pension plans to their employees. There was a similarly significant difference between the percentage of large employers (83%) and small employers (28%) who offered such plans.

According to the 2014 LISA, participation in an employer-provided pension plan is more common in the FRPS than in Canada overall. Approximately 33% of employees in the FRPS participated in an employer-provided Registered Retirement Savings Plan (RRSP), 21% participated in a Deferred Profit Sharing Plan (DPSP) and 53% participated in an employer-provided pension planFootnote 4. In Canada, approximately 20% of employees participated in an RRSP, 5% in a DPSP and 37% in an employer-provided pension plan.

Collective agreements

The Labour Program recently reviewed a representative sample of 231 collective agreements in the FRPS. This review confirmed that individuals in non-standard work such as casual, temporary, seasonal and part-time employees and freelancers are often entitled to less generous benefits under collective agreements than employees in standard work. For instance, the analysis found that:

- part-time employees are usually provided with benefits pro-rated to their hours worked, but a minority of agreements exclude part-time employees from all benefits

- casual and temporary employees typically do not receive benefits such as pension contributions, medical and group insurance and certain leaves

- seasonal employees tend to be entitled to receive benefits only during their time of work, but can elect coverage during their period of seasonal lay-off if they continue to pay the associated costs

In addition, although rare, a few of the agreements in the sample completely exclude workers in non-standard work from any employer-provided benefits and limit the benefits provided to those required pursuant to the Code.

On the other hand, under some of the collective agreements examined, employers offer workers in non-standard work certain benefits based on length of service. For example, contractors working at CBC for more than 13 weeks have access to full benefit plans, excluding pension. Hay River Health and Social Services Authority offers temporary employees working more than four months to be appointed on a term basis, resulting in entitlement to all the benefits provided to term employees. At the Calgary Airport Authority, term employees are eligible for the benefit and life insurance plans provided under the collective agreement if they are initially hired for a period in excess of six months, or when their initial term is extended beyond six months, and are eligible for the pension plan after completing 24 months of continuous work.

Finally, the analysis of the sample agreements found no evidence that any parties negotiated the portability of benefits through collective bargaining.

What the research says

Statutory minimums

While there is a body of research on access to statutory minimums, much of it relates more closely to the changes to the Code made through BIA II in autumn 2018 or to the broader issue of protections for workers in non-standard work (see Issue Paper on Federal labour standards protections for workers in non-standard work).

Some research has been done on the portability of statutory minimums, particularly in Australia, where long service leave is portable in some industries. Some of this research supports the expansion of portable long service leave to other industries or to the entire workforce. For example, in a 2017 McKell Institute Report, Markey et al. make the case for national portable long service leave in Australia in part by arguing that workers are increasingly remaining in the workforce at older ages, and this makes it more important for employees to have a period of recovery (long service leave) part way through their working life. At the same time, they observe that workers are highly mobile and three-quarters stay with their employer for less than 10 years, meaning that only a small portion of workers have access to the leave. They note, too, that women are less likely to be able to access the leave because they are less likely to be employed with one employer for 10 years or more. The authors identify a number of possible benefits of expanding portable long service leave to all workers, including in areas such as worker retention, equity, mobility and flexibility and productivity, but also potential disadvantages such as costs for employer.

While the research in Canada on portability of statutory minimums is limited, some have begun to contemplate the idea. For example, in an article for the Mowat Centre, Thirgood (2017) imagines a scenario where all workers have access to paid leave (for example vacation, sick leave) and other benefits through a portable benefit account funded by employer contributions pro-rated to the hours a worker has put into their organization. She notes that such an idea would require federal-provincial-territorial cooperation in order to work in Canada.

Employer-provided benefits

Workers in non-standard work, particularly those who are non-unionized, are less likely to be able to access employer-provided benefits. According to the Conference Board of Canada’s 2015 Benefits Benchmarking survey, 64% of employers provide benefits to all permanent part-time employees and 29% provide them to some permanent part-time employees. Coverage for permanent part-time workers typically requires that employees work a minimum number of hours per week or meet a percentage of full-time equivalency. Temporary employees (for example contract, term, seasonal, casual employees) were even less likely to have benefits coverage. Only 6% of employers offered benefits to all contingent workers (defined as contract, term, seasonal or casual workers) and 52% offered them to some contingent workers.

Providing benefits is a significant cost to employers. The Conference Board’s 2015 Benefits Benchmarking survey found that employers spent an average of $4,745 per employee in 2014 on group benefits, in addition to legally required payments (in other word CPP, Quebec Pension Plan and EI) which represented an extra cost of approximately $3,585 per employee. Spending on group benefits and required payments averaged about 10% of an employer’s gross annual payroll, excluding the cost of pension and retirement savings plans. Moreover, more than half of employers reported an increase of 6.2% in benefits costs for employees between 2013 and 2014. According to the report, costs per full-time employee for all benefit types have risen since 2011.

The 2015 Benefits Benchmarking survey also found that cost containment remains the top benefits priority for organizations. Employers have taken different approaches to managing costs, such as generic substitution, exclusion of specific drugs from their policy, preferred pharmacy networks, and increasing employees’ shares of benefits premiums. However effective these strategies have proven to be, the report argues that they have not gone to the source of the increase in benefits costs, which includes chronic disease, employee stress and rising obesity rates. As the report notes, in addition to affecting premiums, these factors contribute to higher absenteeism rates which represent an additional cost for employers. The report also notes that as the average age of Canadian workers increases because employees are delaying retirement, employers are seeing the effects on their prescription drug spending and long-term disability rates.

There are also specific challenges associated with providing benefits to workers in the gig economy. In Benefits Canada, Tatelman (2017) highlights challenges including the risk to employers that offering benefits to these workers might “tip the scale” towards them being considered employees, which would have associated costs for employers. She notes, as well, that offering benefits to these workers may also be more costly to insurers if, for example, workers try to maximize benefits before a contract ends.

Some research offers support for portable benefits as a way to expand access to more workers and reduce costs for employers. In a 2016 report for the Aspen Institute, Rolf, Clark and Watterson Bryant argue that the existing social safety net in the United States is insufficient for workers in the 21st century. As a solution, the authors argue for a portable benefits scheme that could take different forms, but should be: portable, pro-rated and universal. A report by Strom and Schmitt (2016) for the Century Foundation similarly points to portable benefits as a solution to gaps in the social safety net and notes that portability models tend to follow a basic outline: portable and universal benefits, likely administered through payroll deduction and likely pro-rated based on the amount of work done for an employer.

While portable benefits are seen as a potential solution, there does not appear to be any consensus in the literature in terms of the ideal model for administering them. Both the Aspen Institute and Century Foundation reports note the many different ways portable benefits could work, with different options for who contributes and how much, whether coverage is voluntary or mandatory, and the scale of portability (for example between employers, within industries, or within a workforce), among other important details (Rolf, Clark and Watterson Bryant, 2016; Strom and Schmitt, 2016).

Research in Canada is also beginning to consider portable benefits. For example, Johal and Thirgood (2016) describe portable benefits as a “transformational change” that Canadian policymakers could consider in rethinking existing approaches to the labour market. A Policy Horizons Canada (2016) report on the changing nature of work also points to portable benefits as one way to update social security programs in the context of the changing nature of work.

Stakeholder perspectives

In the online public survey launched as part of the Modern federal labour standards consultation, 95% of individual respondents said that keeping their benefits was very or somewhat important when changing jobs. About 37% said that employees should be able to keep their benefits when they move jobs.

In written submissions, four unions and labour organizations, one employer organization and two advocacy groups supported the idea of a government-sponsored benefits bank for independent contractors, while two other employer organizations strongly opposed introducing any portable benefits.

Some unions and labour organizations recommended that the Code be amended to eliminate differential treatment with respect to benefits, so that temporary and part-time employees would be entitled to receive the same dental/health care plans, for example, as full-time equivalent employees.

Policy responses in Canada and other jurisdictions

Governments have adopted a range of policy responses to address access to benefits and portability. These generally fall within three categories: providing benefits; requiring or enabling employers to provide or offer benefits; and enabling portability of benefits.

Providing benefits

Typically, this type of policy response has covered only benefits usually provided by employers, particularly health-related benefits such as drug coverage. For example, the purchase of prescription drug coverage has been mandatory in Quebec since 1997. Every person who is permanently settled in Quebec must have prescription drug coverage, either through a private plan or through the public plan administered by the Régie de l’assurance maladie du Québec. The public plan has subsidized premiums for individuals who cannot afford insurance. In British Columbia, the Fair PharmaCare Plan offers prescription drug and designated medical supplies coverage. In Nova Scotia, the Family Pharmacare Program helps Nova Scotians with the cost of their prescription medication.

Some jurisdictions offer access to broad medical coverage beyond prescription drug coverage. The Government of Alberta, for example, offers health insurance through a third-party insurer to all residents younger than 65 and their dependants to cover medical costs not covered by the provincial health care plan. Provided by Alberta Blue Cross, the insurance plan covers prescription drugs, as well as other medical costs such as psychological services, home nursing, prosthetics and hospital accommodation. Albertans are required to pay an annual deductible in addition to monthly premiums. Subsidies for low-income applicants are available.

In the United States, the Patient Protection and Affordable Care Act, also known as Obamacare, aims to extend health insurance coverage to American citizens who do not receive coverage from their employer and are not covered by health programs for the poor and the elderly. The Act requires all Americans to have health insurance while offering subsidies to make coverage more affordable. It also requires businesses with 50 or more full-time equivalent employees to provide affordable health insurance to at least 95% of their full-time employees and dependents up to age 26, or pay a fine. However, on December 22, 2017, the United States Congress enacted the Tax Cuts and Jobs Act (now called An Act to provide for reconciliation pursuant to titles II and V of the concurrent resolution on the budget for fiscal year 2018), which will repeal the individual mandate of Obamacare that requires all Americans to obtain minimally adequate health insurance for themselves and their dependents and penalize those who fail to do so. The elimination of the Obamacare tax penalty will take effect in 2019. All other provisions of Obamacare remain in place.

Requiring or enabling employers to provide or offer benefits

Policy responses of this type require employers to provide benefits directly to employees, or require them to provide benefits in a way that includes employees in non-standard work. For example, under The Saskatchewan Employment Act, employers with 10 or more full-time employees who provide benefits to these employees must also provide benefits to part-time employees if they meet certain eligibility requirements. Benefits include dental plans, group life insurance, accidental death or dismemberment plans, and prescription drug plans. The level of benefits varies depending on the number of hours worked or on annual earnings.

In February 2018, a bill was introduced in the Washington State legislature which would require businesses participating in the gig economy to contribute money to a qualified benefit provider who is responsible for providing benefits to workers. Any employer who employs at least 50 workers in a 12-month period would be required to make contributions. The benefits would follow the worker from job to job, who would be allowed to choose the benefits they want to receive (in other words health insurance, paid time off, retirement benefits, and other benefits determined by the qualified benefit provider).

Similarly, a bill was introduced in California on February 16, 2018 to authorize an organization that is a digital marketplace (such as an app or web-based service) to contribute to a contractor benefit plan established to provide certain employment benefits to marketplace contractors who use the digital marketplace. The bill would require a participating digital marketplace to enter into a written plan agreement with a plan administrator to establish and maintain a benefit plan to provide benefits to the contractors who connect with users through the digital marketplace.

Several states recently passed legislation to create retirement savings programs that employers must offer. For instance, under Illinois’ Secure Choice Retirement Savings Program, businesses with 25 or more employees operating within the state for at least two years will be required to enroll workers into the plan. Employers can only opt out of the plan if they enroll their employees into another retirement savings plan. Employees will contribute 5% of their wages to the plan. Employees can opt out at any time. In California, the CalSavers Secure Choice Retirement Savings Program (formerly Secure Choice) will require employers to register their employees into the savings plan. Employee contribution rates will be 3%, but the administrative board will be able to adjust the rate to within 2% and 4%. Employees will be able to specify a different contribution rate or opt out of the program.

Enabling portability of benefits

Policy responses to enable portability can extend to both statutory minimums and employer-provided benefits. One example of enabling portability of statutory minimums can be found in Australia, where all employees are entitled to long service leave after ten years of employment with one employer. State and territorial laws enable employees in certain sectors (for example building and construction, coal mining, cleaning, community services) to access portable long service leave, which allows them to meet eligibility requirements for long service leave based on continuous service within that sector, rather than with a single employer. Portable long service leave is more common in industries where there is concern about losing skilled workers to other industries. While sector-based portability allows for worker mobility within a sector, it does not encourage broader mobility across sectors or jurisdictions. The specific rules about portable long service leave vary depending on the jurisdiction, though the general principle is that the leave is paid for by contributions from employers in the sector to a central fund, rather than a single employer.

Measures to enable portability of employer-provided benefits are more common. In 2010, Canadian federal, provincial and territorial Finance Ministers agreed to introduce new Pooled Registered Pension Plans (PRPPs) to provide an accessible, large-scale and low-cost pension option to Canadians who do not have access to a workplace pension plan. PRPPs are voluntary and are designed to be portable so that they move with employees from job to job. In 2012, the federal PRPPs regulatory framework came into force. Since then, some provinces have passed legislation providing a regulatory framework for the establishment of PRPPs in their jurisdiction. According to the Office of the Superintendent of Financial Institutions (OSFI), there were five federally-registered PRPPs at the end of 2017, with one reporting it had entered into contracts with five employers and enrolled 111 members, for a total investment of $150,100 (OSFI, 2018).

In Quebec, the construction industry is divided into four sectors for the purposes of negotiating collective agreements, with employer associations designated for each sector. The negotiation of benefits is required as part of the collective bargaining process. Benefit plans are portable to the extent that the employee remains employed by an employer covered under the relevant agreement and the level of protection enjoyed by employees depends on the number of hours worked in a specified period.

In addition, the Act respecting collective agreement decrees allows the Quebec government to order that a collective agreement respecting any trade, industry, commerce or occupation is binding on all employers and employees within a range of application. These decrees have led to the establishment of many fringe benefit schemes for workers in the sectors to which they apply. However, the number of collective agreements extended by decree has declined in recent years.

The 2017 report of the United Kingdom’s Taylor Review of Modern Working Practices looked at the issues surrounding benefits in the context of self-employed workers and people engaged in other non-traditional labour market activities. The Review found that portable benefits schemes tied to the individual as they move from one job to another should be explored. It recommended that the government work with third parties to develop a range of benefits models and platforms in the United Kingdom.

A number of bills have been recently tabled in the United States to enable portability of benefits. For instance, a bill was introduced in the United States Senate on May 25, 2017 proposing to establish a $20-million grant fund within the Department of Labor to incentivize states, local governments and non-profit organizations to experiment with portable benefits models for independent workers such as contractors, temporary workers and self-employed workers. The models would be able to provide a number of work-related benefits, such as workers’ compensation, skills training, disability coverage, health insurance coverage, retirement savings, income security, and short-term savings. However, models focused solely on retirement-related benefits would not be eligible for a grant.

In 2017, the European Council proposed a portable voluntary retirement plan that could be offered to European citizens working across the continent. According to the Council, the proposed “pan-European pension product” (PEPP) would offer more choice, consumer protection, the ability to switch providers and portability to savers, while offering economies of scale, broader reach and cross-border distribution to plan providers (European Council, 2018). The Council agreed on its negotiation stance in June 2018, making it possible for it to negotiate with the European Parliament.

Private sector and worker responses in Canada and other jurisdictions

Some innovative initiatives have been put in place by employers and unions and worker organizations (for example multi-employer benefit plans, group insurance plans). They offer a potentially valuable lens through which to consider potential legislative and non-legislative measures for enhancing access to benefits and portability for FRPS workers, while also contributing to the evidence base for broader public discourse about the future of Canada’s system of social protection.

In the FRPS, employees in the longshoring industry regularly work for different employers in a short span of time. Therefore, and as permitted under the Code, employers in this industry have formed large employer associations that provide centralized payroll processes and allow members to collectively manage benefits for employees. The British Columbia Maritime Employers Association (BCMEA) is an example of this type of association. It collectively bargains on behalf of employers with the International Longshore Workers Association (ILWU), which represents employees working in the industry.

In Quebec, multi-employer plans can be independently established by multiple employers in a geographic area or within the same industry in order to allow them to provide benefits to employees. Generally, only unionized employees are covered by these plans. For example, the Merit Contractors Association offers this type of plan. Employers are required to report the number of hours worked by each employee to the plan administrator. Those hours are then deposited into the employee’s personal hour bank. To pay for benefits, 150 hours are deducted from the worker’s hour bank each month. The remaining hours stay in the bank and accumulate up to a set maximum amount. In order to be eligible for benefits, employees must have at least 300 hours in their bank and must maintain a minimum of 150 hours.

Similarly, artists’ associations and producer associations in Quebec (under the Act Respecting the Professional Status and Conditions of Engagement of Performing, Recording and Film Artists) and in the FRPS (under the Status of the Artist Act) can enter into agreements setting out minimum terms and conditions of employment including benefits. These benefits are paid for with producer and artist contributions made to a shared security fund.

Some unions and worker associations offer benefits directly to members. These benefits can follow the worker rather than the job, as long as the worker maintains membership in the union or association. For example, the Canadian Freelance Union (a community chapter of Unifor) offers health benefits for freelancers and self-employed workers who are members of the association.

Many insurance companies in Canada and other jurisdictions also offer benefit plans that are targeted to workers in non-standard work who do not have access to employer-provided benefits or who need portable benefits because they change jobs often. These are inherently portable because they follow the worker, not the job or membership in an association, and are paid for entirely by individual contributions.

In the United States, some multi-employer benefit plans have been established. For example, the Family Medical Care Plan administered by the National Electrical Contractors Association and the International Brotherhood of Electrical Workers is available to employees of employers who contribute to the plan pursuant to a collective bargaining agreement or as otherwise agreed to by the plan’s board of trustees. Hourly contributions are made to allow employees who accumulate 140 hours per month or 200 hours in two consecutive months to access health benefits and a pension.

In recent years, American companies have adopted new approaches to facilitating access to and portability of benefits for workers in the gig economy. For example, several gig economy companies (including Uber, Etsy and TaskRabbit) have partnered with Stride Health, a company that offers workers the ability to compare and apply for benefits including health, dental and vision. The premiums for benefits are paid entirely by the workers; employers do not contribute.

Issues for the panels’s consideration

- Which benefits should be statutory and/or universal in the FRPS and which should be optional? For whom?

- Who should be responsible for benefits in the FRPS? What should the roles be for the federal government, employers, workers, insurers and others?

- Should the federal government take further steps to enhance access to benefits in the federal private sector and enable portability? If so, are there specific models that should be considered and why?

- Should the federal government take further steps to enhance security of employer-provided benefits in the federal private sector? If so, what steps should be taken?

- How should the federal government proceed on this issue?

Annex A

| Part III provisions | Continuous employment requirement | |||||||

|---|---|---|---|---|---|---|---|---|

| None | 1 month | 3 months | 6 months | 12 months | 5 years | 6 years | 10 years | |

| Annual vacations: two weeks | n/a | n/a | n/a | n/a | X | n/a | n/a | n/a |

| Annual vacations: three weeks | n/a | n/a | n/a | n/a | n/a | X* | n/a | n/a |

| General holidays (pay) | X* | n/a | n/a | n/a | n/a | n/a | n/a | n/a |

| Maternity leave | X* | n/a | n/a | n/a | n/a | n/a | n/a | n/a |

| Parental leave | X* | n/a | n/a | n/a | n/a | n/a | n/a | n/a |

| Compassionate care leave | X* | n/a | n/a | n/a | n/a | n/a | n/a | n/a |

| Leave related to critical illness | X* | n/a | n/a | n/a | n/a | n/a | n/a | n/a |

| Leave related to death or disappearance | X* | n/a | n/a | n/a | n/a | n/a | n/a | n/a |

| Bereavement leave | Unpaid | n/a | Paid | n/a | n/a | n/a | n/a | n/a |

| Sick leave | X* | n/a | n/a | n/a | n/a | n/a | n/a | n/a |

| Leave for members of Reserve Force | n/a | n/a | X* | n/a | n/a | n/a | n/a | n/a |

| New provisions – BIA 2017, No.2 (Not yet in force) | ||||||||

| Traditional Indigenous practices leave | n/a | n/a | X | n/a | n/a | n/a | n/a | n/a |

| Victims of domestic violence leave | Unpaid | n/a | Paid | n/a | n/a | n/a | n/a | n/a |

| New provisions – BIA 2018, No.2 (Not yet in force) | ||||||||

| Annual vacations: four weeks | n/a | n/a | n/a | n/a | n/a | n/a | n/a | X |

| Personal leave | Unpaid | n/a | Paid | n/a | n/a | n/a | n/a | n/a |

| Court leave | X | n/a | n/a | n/a | n/a | n/a | n/a | n/a |

* New continuous employment requirement not yet in force

Selected bibliography

A Second Act to Implement Certain Provisions of the Budget Tabled in Parliament on February 27, 2018 and Other Measures, (c. 27), 2018.

An Act to Add Section 20139 to, and to Add Title 21 (commencing with Section 100000) to, the Government Code, and to add Section 1088.9 to the Unemployment Insurance Code, Relating to Retirement Savings Plans, and Making an Appropriation Therefor, California State Legislature, 2012.

Bernier, J. Social protection for non-standard workers outside the employment relationship, Federal Labour Standards Review Commission, January 10, 2006.

California State Treasurer. CalSavers Secure Choice Retirement Savings Program, 2018.

Canada Labour Code, Government of Canada, 1985,.

Conference Board of Canada. Benefits benchmarking 2015, 2015.

Employment and Social Development Canada (ESDC). Modernizing federal labour standards—what we heard, Government of Canada, 2018.

European Council. Pensions: Council agrees its stance on pan-European pension product [Press release], June 19, 2018.

Government of Canada. Canada Pension Plan - How much could you receive, 2018.

Illinois Secure Choice. Illinois State Treasurer, 2018.

Johal, S., and Thirgood, J. Working without a net, (PDF version, (7.24 Mb) Mowat Centre, 2016.

Lee, J. Europe takes a stab at addressing pension portability with continent-wide product, Benefits Canada, July 31, 2017.

Markey, R., Parr, N., Kyng, T., Muhidin, S., O’Neill, S., Thornthwaite, L., Wright, C., … Ferris, S. The case for a national portable long service leave scheme in Australia, McKell Institute, 2017.

Office of the Superintendent of Financial Institutions Canada. OSFI Annual report 2017-2018, (PDF version, 717.79 Kb) Government of Canada, 2018.

Policy Horizons Canada. Canada and the changing nature of work, Government of Canada, May 1, 2016.

Rolf, D., Clark, S., and Waterson Bryant, C. Portable benefits in the 21st century, (PDF version 2.23 MB) Aspen Institute, June 8, 2016. (2.23 Mb)

Strom, S., and Schmitt, M. Protecting workers in a patchwork economy, Century Foundation, April 7, 2016.

Sun Life Financial. Retirement now, February 17, 2017.

Tatelman, S. The Intricacies of Providing Benefits in the Gig Economy, Benefits Canada, February 21, 2017.

Taylor, M. Good Work: The Taylor Review of Modern Working Practices (PDF version, 3.75 MB), Government of the United Kingdom, July 11, 2017. (3.75 Mb)

Thirgood, J. What if you could take it with you?, Mowat Centre, June 27, 2017.