Calculate second additional CPP contributions (CPP2) deductions

Beginning January 1, 2024, you must begin to calculate the second additional CPP contribution (CPP2) on earnings above the annual maximum pensionable earnings.

You may be looking for: Second additional CPP contribution (CPP2) rates and maximums

How to use the CPP2 contributions tables and how to manually calculate the amount to withhold.

If the employee's province of employment is Quebec, you are required to deduct the second Quebec Pension Plan (QPP) contributions and not the CPP2 contributions, refer to: Québec Pension Plan Contributions | Revenu Québec

On this page

Calculation methods

Reminder: There is an online calculator that will calculate the CPP2 deductions for you.

Calculate CPP2 deductions based on the type of payment:

- Any payments (CPP2 tables)

- Any payments (manual calculation)

- Verification – Year-end or multiple pay periods

Any payments (CPP2 tables)

CPP2 contributions tables calculate the required CPP2 contributions for you on given ranges of income for a specified pay period.

Steps

Determine if you can use CPP2 contributions tables

CPP2 contributions tables can be used in most common situations.

Use when

- The payment is for remuneration paid in one of the common or uncommon pay periods for which tables are provided

- If the payment is made to a First Nations worker and you received Form TD1-IN, only use these tables on the portion of their income which is taxable

Do not use when

- You are doing a year-end verification of your CPP2 contributions, use: Verification – Year-end or multiple pay periods

- The employee already reached their CPP2 maximum contributions for the year

Determine if your employee exceeded the first maximum annual pensionable earnings ceiling

- Employee's gross pay for the year to date

- plus Employee's taxable benefits and allowances for the year to date

- minus Employee's non-pensionable earnings for the year to date

What are non-pensionable earnings

Non-pensionable earnings are:

- Received before and including the month they turned 18

- Received after the month they turned 70

- Received after the effective date of their completed and signed Form CPT30 to elect to stop contributing to the CPP

- Received before and including the month where the employee provided you a completed and signed Form CPT30 to restart contributing to the CPP

- Received while the employee is considered to be disabled under the CPP or QPP

- Employment income, benefits, and payments from which you are not required to deduct CPP

- equals This amount is the pensionable earnings for the year to date

- minus Employee's maximum pensionable earnings

How to calculate prorated maximum pensionable earnings

- Maximum annual pensionable earnings

- multiply by Number of months the employee has pensionable employment

- equals Result of first step of proration calculation

- divide by 12 months

- equals Maximum pensionable earnings after prorating

- equals A positive amount confirms your employee exceeded the first maximum annual pensionable earnings ceiling

Calculation example

Joseph receives a biweekly salary of $5,500 and $500 in taxable benefits per pay period. You have paid him for 14 pay periods so far in 2026 ($77,000 and $7,000, to a total of $84,000). Joseph has a pensionable employment for the full year of 2026.

- $77,000 is Joseph's gross pay for the year to date

- plus $7,000 is Joseph's taxable benefits for the year to date

- equals $84,000 is Joseph's pensionable earnings for the year to date

- minus $0 because all of Joseph's earnings require CPP contributions

- minus $74,600 the maximum annual pensionable earnings

- equals $9,400 is Joseph's pensionable earnings that exceeded the first maximum pensionable earnings ceiling

You must continue to calculate Joseph's CPP2 contributions because the amount is positive.

Do not continue to next step if the amount is zero or negative.

You do not deduct CPP2 contributions in this situation.

You must continue to: Calculate CPP contributions deductions.

- Continue to next step if the amount is positive.

Determine if your employee reached the CPP2 maximum contribution

Use the applicable calculation if your employee has a pensionable employment for the full year or only for part of the year (prorate)

Employee has more than one employer

You must withhold CPP2 contributions until the employee reaches the maximum without taking into account deductions made by another employer.

Calculation – Employee has a pensionable employment for full year

- Maximum annual employee CPP2 contributions in their employment with you

- minus Employee's CPP2 contributions to date for the year in their employment with you

- equals This amount is the maximum CPP2 contribution that you can deduct from your employee's pay for the rest of the year

Calculation example

Joseph's has a pensionable employment for the year 2026. You have already deducted $100 in CPP2 from his earnings with you this year.

- $416 is the maximum 2026 annual CPP2 contribution in his employment with you

- minus $100 is the amount for Joseph CPP2 contributions to date for the year in his employment with you

- equals $316 is the maximum CPP2 contributions that you can deduct from Joseph's pay for the rest of the year

Calculation – Employee has a pensionable employment only for part of the year (prorate)

- Additional maximum annual pensionable earnings

- minus Maximum annual pensionable earnings

- equals Additional maximum pensionable earnings

- multiply by Number of months the employee has pensionable employment

- equals Result of first part of proration calculation

- divide by 12 months

- equals Additional maximum pensionable earnings after prorating

- multiply by 4% (CPP2 rate )

- equals This amount is the maximum CPP2 contribution after prorating in their employment with you

- minus Employee's CPP2 contributions to date for the year in their employment with you

- equals This amount is the maximum CPP2 contributions that you can deduct from your employee's pay for the rest of the year

Calculation example

Joseph turns 70 on February 24, 2026 and has pensionable employment for 2 months. You have already deducted $10 in CPP2 from his earnings with you this year.

- $85,000 is the additional maximum annual pensionable earnings

- minus $74,600 is the maximum annual pensionable earnings

- equals $10,400 is Joseph's additional maximum pensionable earnings

- multiply by 2 months that Joseph is pensionable

- equals $20,800 is the result of first part of proration calculation

- divide by 12 months

- equals $1,733.33 is Joseph's additional maximum pensionable earnings after prorating

- multiply by 4% is the CPP2 rate

- equals $69.33 is Joseph's maximum CPP2 contributions after prorating in his employment with you

- minus $10 is the amount for Joseph CPP2 contributions to date for the year in his employment with you

- equals $59.33 is the maximum CPP2 contributions that you can deduct from Joseph's pay for the rest of the year

No CPP2 contributions should be deducted after the end of February 2026.

- Do not deduct CPP2 contributions if they have reached the maximum.

- Continue to next step if they have not reached the CPP2 maximum.

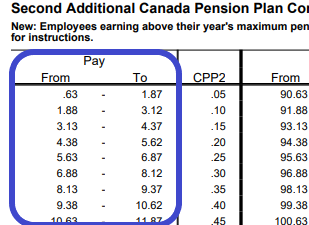

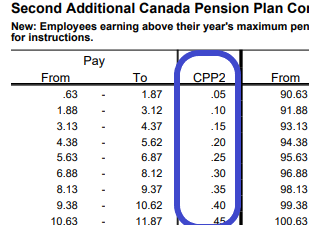

Get the CPP2 contributions tables

2026 tax year

Use the CPP2 contributions tables.

Second additional CPP contributions table [PDF]

Previous years

Previous years

- 2025 tax year – Second additional CPP contributions table [PDF]

- 2024 tax year – Second additional CPP contributions table [PDF]

The 2024 CPP2 table is the first tax year they are published.

Determine the pay range

Find the range that includes your employee's gross remuneration (including any taxable benefits) in the "Pay" column.

If the maximum CPP contribution is reached during the pay period, use only the part of their pensionable earnings for the pay period above the first maximum annual pensionable earnings ceiling (step 2) to determine the pay range to use.

Get the amount of CPP2 contributions to deduct

Find the amount under the "CPP2" column that corresponds with the range that includes your employee’s pay for the pay period.

Calculate the amount of CPP2 contributions you have to withhold

Use one of the following amount that applies to your situation:

- If the amount in step 6 is less than step 3, withhold the amount from step 6.

- If the amount in step 6 is greater than step 3, withhold the amount from step 3.

Calculate the amount of CPP2 contributions you have to remit

- CPP2 contributions you have to withhold from your employee (step 7)

- multiply by 2 (matching employer CPP2 contribution)

- equals This is the total amount you have to remit (your employee's share and your share of the CPP2 contribution)

Calculation example

You have reviewed the CPP2 contributions tables and found that the required CPP2 contributions for Joseph’s earnings in this pay period is $40.40. You have also confirmed that this amount is not more than the remaining CPP2 contributions that you can deduct for the rest of the year.

- $40.40 is Joseph's CPP2 contributions you have to withhold (step 7)

- multiply by 2 (your matching CPP2 contribution)

- equals $80.80 is the total CPP2 contributions to remit (Joseph's share and your share of the CPP2 contribution)

Any payments (manual calculation)

You can use the manual calculation method to calculate the CPP2 contributions that must be withheld for any payments made to your employees in a pay period without using the CPP2 tables.

Steps

Determine if your employee exceeded the first maximum annual pensionable earnings ceiling

- Employee's gross pay for the year to date

- plus Employee's taxable benefits and allowances for the year to date

- minus Employee's non-pensionable earnings for the year to date

What are non-pensionable earnings

Non-pensionable earnings are:

- Received before and including the month they turned 18

- Received after the month they turned 70

- Received after the effective date of their completed and signed Form CPT30 to elect to stop contributing to the CPP

- Received before and including the month where the employee provided you a completed and signed Form CPT30 to restart contributing to the CPP

- Received while the employee is considered to be disabled under the CPP or QPP

- Employment income, benefits, and payments from which you are not required to deduct CPP

- equals This amount is the pensionable earnings for the year to date

- minus Employee's maximum pensionable earnings

How to calculate prorated maximum pensionable earnings

- Maximum annual pensionable earnings

- multiply by Number of months the employee has pensionable employment

- equals Result of first step of proration calculation

- divide by 12 months

- equals Maximum pensionable earnings after prorating

- equals A positive amount confirms your employee exceeded the first maximum annual pensionable earnings ceiling

Calculation example

Joseph receives a biweekly salary of $5,500 and $500 in taxable benefits per pay period. You have paid him for 14 pay periods so far in 2026 ($77,000 and $7,000, to a total of $84,000). Joseph has a pensionable employment for the full year of 2026.

- $77,000 is Joseph's gross pay for the year to date

- plus $7,000 is Joseph's taxable benefits for the year to date

- equals $84,000 is Joseph's pensionable earnings for the year to date

- minus $0 because all of Joseph's earnings require CPP contributions

- minus $74,600 the maximum annual pensionable earnings

- equals $9,400 is Joseph's pensionable earnings that exceeded the first maximum pensionable earnings ceiling

You must continue to calculate Joseph's CPP2 contributions because the amount is positive.

Do not continue to next step if the amount is zero or negative.

You do not deduct CPP2 contributions in this situation.

You must continue to: Calculate CPP contributions deductions.

- Continue to next step if the amount is positive.

Determine if your employee reached the CPP2 maximum contribution

Use the applicable calculation if your employee has a pensionable employment for the full year or only for part of the year (prorate) .

Employee has more than one employer

You must withhold CPP2 contributions until the employee reaches the maximum without taking into account deductions made by another employer.

Calculation – Employee has a pensionable employment for full year

- Maximum annual employee CPP2 contributions in their employment with you

- minus Employee's CPP2 contributions to date for the year in their employment with you

- equals This amount is the maximum CPP2 contribution that you can deduct from your employee's pay for the rest of the year

Calculation example

Joseph has a pensionable employment for the year 2026. You have already deducted $100 in CPP2 from his earnings with you this year.

- $416 is the maximum 2026 annual CPP2 contribution in his employment with you

- minus $100 is the amount for Joseph CPP2 contributions to date for the year in his employment with you

- equals $316 is the maximum CPP2 contributions that you can deduct from Joseph's pay for the rest of the year

Calculation – Employee has a pensionable employment only for part of the year (prorate)

- Additional maximum annual pensionable earnings

- minus Maximum annual pensionable earnings

- equals Additional maximum pensionable earnings

- multiply by Number of months the employee has pensionable employment

- equals Result of first part of proration calculation

- divide by 12 months

- equals Additional maximum pensionable earnings after prorating

- multiply by 4% (CPP2 rate )

- equals This amount is the maximum CPP2 contribution after prorating in their employment with you

- minus Employee's CPP2 contributions to date for the year in their employment with you

- equals This amount is the maximum CPP2 contributions that you can deduct from your employee's pay for the rest of the year

Calculation example

Joseph turns 70 on February 24, 2026 and has pensionable employment for 2 months. You have already deducted $10 in CPP2 from his earnings with you this year.

- $85,000 is the additional maximum annual pensionable earnings

- minus $74,600 is the maximum annual pensionable earnings

- equals $10,400 is Joseph's additional maximum pensionable earnings

- multiply by 2 months that Joseph is pensionable

- equals $20,800 is the result of first part of proration calculation

- divide by 12 months

- equals $1,733.33 is Joseph's additional maximum pensionable earnings after prorating

- multiply by 4% is the CPP2 rate

- equals $69.33 is Joseph's maximum CPP2 contributions after prorating in his employment with you

- minus $10 is the amount for Joseph CPP2 contributions to date for the year in his employment with you

- equals $59.33 is the maximum CPP2 contributions that you can deduct from Joseph's pay for the rest of the year

No CPP2 contributions should be deducted after the end of February 2026.

- Do not deduct CPP2 contributions if they have reached the maximum.

- Continue to next step if they have not reached the CPP2 maximum.

Calculate the total CPP2 pensionable income

- Employee's gross pay for the pay period

- plus Employee's taxable benefits and allowances for the pay period

- minus Employee’s non-pensionable earnings for the pay period

- equals This is the total CPP2 pensionable income for the pay period

If the maximum CPP contribution is reached during the pay period, use only the part of their pensionable earnings for the pay period above the first maximum annual pensionable earnings ceiling (step 2) to determine their total CPP2 pensionable income for the pay period.

Calculation example

Joseph receives a weekly salary of $500 and $50 in taxable benefits. He passed the maximum pensionable earnings ceiling for the year in July 2026 and this is your second calculation after he passed that ceiling.

- $500 is Joseph's gross pay for the pay period

- plus $50 is Joseph's taxable benefits for the pay period

- minus $0 because all of Joseph's earnings for the pay period require CPP2 contributions

- equals $550 is Joseph's total CPP2 pensionable income for the pay period

Determine the amount of CPP2 contributions to deduct

- Total CPP2 pensionable income for the pay period (step 3)

- multiply by 4% (CPP2 rate )

- equals This amount is the CPP2 contributions to deduct

Calculation example

The total of Joseph’s gross pay and taxable benefits for the weekly pay period is $550. All of Joseph's earnings require CPP2 contributions. He passed the maximum pensionable earnings for the year in July 2026 and this is your second calculation after he passed that ceiling.

- $550 is Joseph's total pensionable income for the pay period (step 3)

- multiply by 4% is the CPP2 rate

- equals $22 is the amount of CPP2 contributions to deduct

Calculate the amount of CPP2 contributions you have to withhold

Use one of the following amount that applies to your situation:

- If the amount in step 4 is less than step 2, withhold the amount from step 4.

- If the amount in step 4 is greater than step 2, withhold the amount from step 2.

Calculate the amount of CPP2 contributions you have to remit

- CPP2 contributions you have to withhold from your employee (step 5)

- multiply by 2 (matching employer CPP2 contribution)

- equals This is the total amount you have to remit (your employee's share and your share of the CPP2 contribution)

Calculation example

You have calculated the required CPP2 contributions for Joseph's earnings in the pay period is $22. You have also confirmed that this amount is not more than the remaining CPP2 contributions that you can deduct for the rest of the year.

- $22 is Joseph's contributions you have to withhold (step 5)

- multiply by 2 (your matching CPP2 contribution)

- equals $44 is the total CPP2 contributions to remit (Joseph's share and your share of the CPP2 contribution)

Verification – Year-end or multiple pay periods

Use this calculation to verify an employee’s CPP2 contributions at year-end or for multiple pay periods at any time of year. This verification is used to determine if you have deducted properly, under deducted or over deducted CPP2 contributions.

Steps

Determine if your employee exceeded the first maximum annual pensionable earnings ceiling

The following calculation must include only pensionable earnings in their employment with you:

- Employee's gross pay for the total period of employment which will be included in box 14 of their T4 slip

- plus Employee's taxable benefits and allowances for the total period of employment which will be included in box 14 of their T4 slip

- minus Employee's non-pensionable earnings

What are non-pensionable earnings

Non-pensionable earnings are:

- Received before and including the month they turned 18

- Received after the month they turned 70

- Received after the effective date of their completed and signed Form CPT30 to elect to stop contributing to the CPP

- Received before and including the month where the employee provided you a completed and signed Form CPT30 to restart contributing to the CPP

- Received while the employee is considered to be disabled under the CPP or QPP

- Employment income, benefits, and payments from which you are not required to deduct CPP

- equals This amount is the pensionable earnings for the period of employment

- minus Employee's maximum pensionable earnings

How to calculate prorated maximum pensionable earnings

- Maximum annual pensionable earnings

- multiply by Number of months the employee has pensionable employment

- equals Result of first step of proration calculation

- divide by 12 months

- equals Maximum pensionable earnings after prorating

- equals A positive amount confirms your employee exceeded the first maximum annual pensionable earnings ceiling

Calculation example

Your employee Joseph was pensionable for the whole year of 2026. You are about to prepare his T4 and are reviewing your payroll records to confirm that you have deducted enough CPP2 from his earnings this year. He has pensionable employment for the entire year.

- $90,000 is Joseph’s total salary, wages benefits, and allowances for the total period of employment which will be included in box 14 of their T4 slip

- minus $0 is Joseph’s non-pensionable earnings. These are earnings:

- Received before and including the month they turned 18

- Received after the month they turned 70

- Received after the effective date of their completed and signed Form CPT30 to elect to stop contributing to the CPP

- Received before and including the month where the employee provided you a completed and signed Form CPT30 to restart contributing to the CPP

- Received while the employee is considered to be disabled under the CPP or QPP

- Employment income, benefits, and payments from which you are not required to deduct CPP

- equals $90,000 is Joseph's pensionable earnings for the period of employment

- minus $74,600 is the maximum annual pensionable earnings for the period of employment

- equals $15,400 is Joseph's pensionable earnings that exceeded the first maximum pensionable earnings ceiling

You must continue to calculate Joseph's CPP2 contributions because the amount is positive.

Do not continue to next step if the amount is zero or negative.

You do not deduct CPP2 contributions in this situation.

You must continue to: Calculate CPP contributions deductions.

- Continue to next step if the amount is positive.

Confirm the amount of CPP2 pensionable earnings for the period of employment

- Employee's additional maximum annual pensionable

earnings - minus Employee's maximum annual pensionable earnings

- equals Result

Calculation example

Your employee Joseph had pensionable employment for the whole year of 2026. You are about to prepare his T4 and are reviewing your payroll records to confirm that you have deducted enough CPP2 from his earnings this year. He was pensionable for the entire year and his total earnings were $90,000.

- $85,000 is the additional maximum pensionable earnings

- minus $74,600 is the maximum annual pensionable earnings

- equals $10,400 is the result

The result in step 1 is $15,400 and is more than $10,400. Use $10,400 to calculate step 3.

- If the amount in step 1 is more than your result, use this result as the CPP2 pensionable earnings for the period of employment.

- If the amount in step 1 is less than your result, use the amount from step 1 as the CPP2 pensionable earnings for the period of employment.

- Employee's additional maximum annual pensionable

Determine the amount of required CPP2 contributions for the period of employment

- CPP2 pensionable earnings for the period of employment (step 2)

- multiply by 4% (CPP2 rate )

- equals This amount is the employee's required CPP2 contributions for the period of employment

Calculation example

Joseph was paid monthly during the year of 2026 in his employment with your company. As his income ($90,000) was above both the maximum pensionable earnings and additional maximum pensionable earnings for the year, his CPP2 contributory earnings are the additional maximum pensionable earnings $10,400.

- $10,400 is Joseph's CPP2 pensionable earnings for the period of employment (step 2)

- multiply by 4% is the CPP2 rate

- equals $416 is the amount for your employee's required CPP2 contributions for the period of employment

Determine if you have under or over remitted for the period of employment

- Employee's required CPP2 contributions for the period of employment (step 3)

- minus CPP2 contributions you deducted from the employee for the period of employment

- equals This amount should be $0 if you have deducted correctly

Calculation example

You confirmed in your payroll records that a total of $416 in CPP2 was deducted from Joseph’s pay during the year of 2026.

- $416 is Joseph's required CPP2 contributions for the period of employment (step 2)

- minus $416 is the CPP2 contributions you deducted from Joseph for the period of employment

- equals $0 is the amount, this means you have deducted correctly

- If the amount is positive you have under deducted for the period of employment.

- If the amount is negative you have over deducted for the period of employment.

To correct a deduction error:

- If you have not filed the information return, refer to: Make corrections before filing

- If you already filed the information return, refer to: Make corrections after filing

References

Related

- Administration of the Canada Pension Plan and the Employment Insurance Act

- Canada Pension Plan enhancement

Multimedia

- Webinar – Enhanced CPP & You | 45 minutes

- Webinar – How to use the payroll deductions tables | 18 minutes

Legislation

- CPP: 8

- Contributions by employees in respect of pensionable employment

- CPP: 9

- Contributions by employers in respect of pensionable employment

- CPP: 11.1

- Contribution rate

- CPP: 11.2

- First and second additional contribution rates

- CPP: 12

- Contributory salary and wages

- CPP: 17.1

- Additional maximum pensionable earnings

- CPP: 18.1

- Year’s additional maximum pensionable earnings

- CPP: 21(2)

- Amount to be deducted and remitted by employer

- CPP: Schedule 2

- First and second additional contribution rates

- CPP Reg: 4

- Computation of employee's contribution

- CPP Reg: 5.1(1)

- Computation of employee's contribution

- CPP Reg: 7

- Employer's contribution