Report on Public Sector Pension Plans as at March 31, 2022

On this page

About this report

This report provides overviews of the four main public sector pension plans. These overviews are based on information from the most recent annual and actuarial reports for each plan, the Public Sector Pension Investment Board annual report and the Public Accounts of Canada.

Data in this report is for the fiscal year ended March 31, 2022. If data as of this date is not available, data from other years is presented and noted.

About the plans

Pension plans are one component of a total compensation package. They provide a lifetime income to eligible plan members upon retirement, disability or termination. The level of pension received is usually based on the plan member’s salary and years of service. These plans also provide benefits to eligible survivors upon the member’s death.

The Government of Canada sponsors pension plans for the public service, the Royal Canadian Mounted Police (RCMP) and the Canadian Armed Forces (CAF) and its Reserve Force. These plans are contributory defined benefit pension plans established under legislation.Footnote 1 This means that both the employer and employee make contributions.

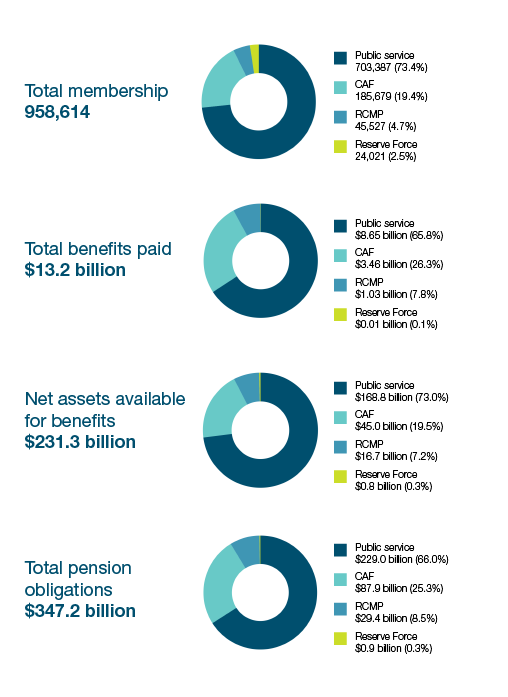

Fiscal year highlights

Fiscal year highlights- Text version

| Pension plan | Number of members | Percentage of total |

|---|---|---|

| Public service | 703,387 | 73.4% |

| Canadian Armed Forces | 185,679 | 19.4% |

| Royal Canadian Mounted Police | 45,527 | 4.7% |

| Reserve Force | 24,021 | 2.5% |

| Total membership (all plans) | 958,614 | 100 % |

| Pension plan | Benefits paid | Percentage of total |

|---|---|---|

| Public service | $8.65 billion | 65.8% |

| Canadian Armed Forces | $3.46 billion | 26.3% |

| Royal Canadian Mounted Police | $1.03 billion | 7.8% |

| Reserve Force | $0.01 billion | 0.1% |

| Total benefits paid (all plans) | $13.2 billion | 100% |

| Pension plan | Net assets held by PSPIB | Percentage of total |

|---|---|---|

| Public service | $168.8 billion | 73.0% |

| Canadian Armed Forces | $45.0 billion | 19.5% |

| Royal Canadian Mounted Police | $16.7 billion | 7.2% |

| Reserve Force | $0.8 billion | 0.3% |

| Total net assets (all plans) | $231.3 billion | 100% |

| Pension plan | Obligations | Percentage of total |

|---|---|---|

| Public service | $229.0 billion | 66.0% |

| Canadian Armed Forces | $87.9 billion | 25.3% |

| Royal Canadian Mounted Police | $29.4 billion | 8.5% |

| Reserve Force | $0.9 billion | 0.3% |

| Total obligations (all plans) | $347.2 billion | 100,1% |

Note: Due to rounding, the individual plan percentages presented do not total 100%.

Members

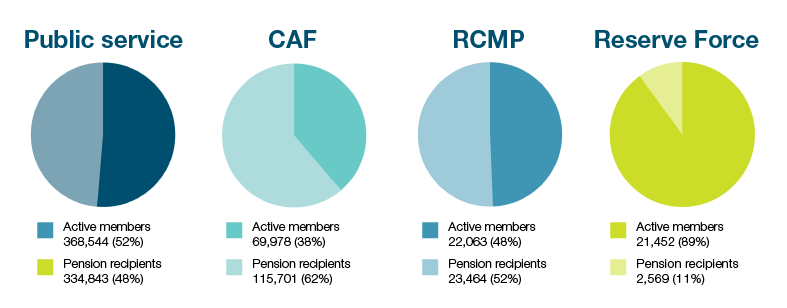

Plan members are classified as either active members or pension recipients (which includes survivors and deferred annuitants). The breakdown of members for each pension plan appears in Figure 1.

Figure 1 - Text version

Individual plan membership breakdown by type of member

| Number of members | Percentage of total | |

|---|---|---|

| Active members | 368,544 | 52% |

| Pension recipients | 334,843 | 48% |

| Total members | 703,387 | 100% |

| Number of members | Percentage of total | |

|---|---|---|

| Active members | 22,063 | 48% |

| Pension recipients | 23,464 | 52% |

| Total members | 45,527 | 100% |

| Number of members | Percentage of total | |

|---|---|---|

| Active members | 69,978 | 38% |

| Pension recipients | 115,701 | 62% |

| Total members | 185,679 | 100% |

| Number of members | Percentage of total | |

|---|---|---|

| Active members | 21,452 | 89% |

| Pension recipients | 2,569 | 11% |

| Total members | 24,021 | 100% |

Benefits

A plan member’s benefits are based on their years of pensionable service and on their pensionable salary, and are calculated using a formula set out in the applicable legislation.Footnote 1

Members may receive their benefits in one of the following ways: immediate or deferred pensions, annual allowances, or disability retirement benefits. Eligible survivors and children may receive survivor benefits and child allowances, respectively.

All benefits are indexed annually to cover increases in the cost of living, as determined by the Consumer Price Index (CPI). The CPI is a measure of price changes published by Statistics Canada based on retail prices of about 300 goods and services, including food, housing, transportation, clothing and recreation.

The indexation rate was 2.4% for calendar year 2022 and 1% for calendar year 2021.

Table 1 shows the average pension paid to retired members and their eligible survivors for fiscal year ended March 31, 2022.

| Pension plan | Average pension |

|---|---|

| Public service | $34,682 |

| CAF – Regular Force | $34,247 |

| RCMP | $45,091 |

| CAF – Reserve Force | $5,142 |

Contributions

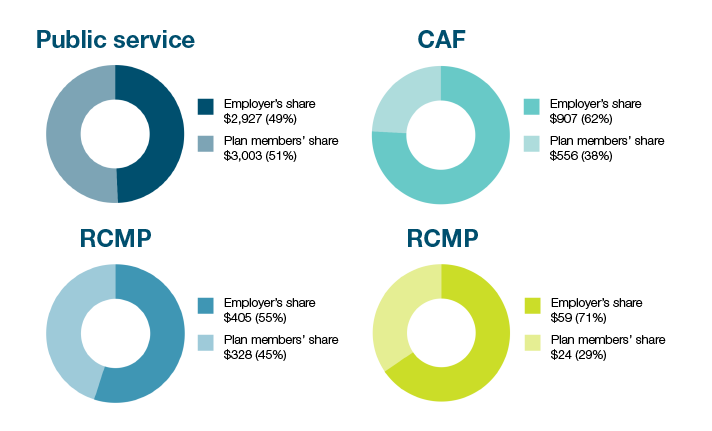

Public sector pension plan benefits are funded by contributions from active plan members and the Government of Canada (as the employer), as well as from investment earnings.

Contributions include current service and past service contributions (for example, service buybacks) received during the year and do not include special employer contributions, which are special payments the Government of Canada is required to make to fund actuarial deficits.

For fiscal year ended March 31, 2022, total contributions were $8.2 billion. Figure 2 shows a breakdown of the contributions.

Figure 2 - Text version

| Employers’ share | Plan members’ share | Total | |||

|---|---|---|---|---|---|

| Millions ($) | Percentage (%) | Millions ($) | Percentage (%) | Millions ($) | |

| Public service | $2,927 | 49% | $3,003 | 51% | $5,930 |

| Royal Canadian Mounted Police | $405 | 55% | $328 | 45% | $733 |

| Canadian Armed Forces | $907 | 62% | $556 | 38% | $1,463 |

| Reserve Force | $59 | 71% | $24 | 29% | $83 |

| Total contributions (all plans) | $8,209 | ||||

Plan members’ contributions are a percentage of their salary and are collected through payroll deductions. Refer to Appendix: Contribution rates.

Pension obligations

Pension obligations measure, in today’s dollars, the benefits that will be paid to members in the future.

The amount of pension obligations is based on a plan’s actuarial valuation that is conducted each year for accounting purposes by the Office of the Chief Actuary. The valuation uses economic assumptions, such as future rates of return on investments, and demographic assumptions, such as life expectancy and retirement age.

Investment returns

Net assets consist mainly of net investments managed by the Public Sector Pension Investment Board (PSPIB) on behalf of the plans.

Since April 1, 2000, (March 1, 2007, for the Reserve Force pension plan), plan member and employer contributions, net of benefit payments and other charges to the plans, have been transferred to the PSPIB for investment.

Returns on these investments are key to funding plan benefits. The contribution transfers are over and above benefit payments and administrative costs. As the plans mature, the quantity of assets that come from investment returns is expected to continue growing.

Since 2018, the cumulative net investment returns have exceeded the cumulative net contribution transfers sent to the PSPIB.

Administrative expenses

Under legislation, authorized government organizations and the PSPIB charge eligible administrative expenses to the public sector pension plans.

Expenses by government departments are for the administration of the public sector pension plans. Expenses incurred by the PSPIB are for operating costs to invest pension assets. Investment management fees are either paid directly by the PSPIB or offset against distributions received from the investments.

For the fiscal year ended March 31, 2022, total administrative expenses for the public sector pension plans were $770 million (see Table 2).

| Paid by | Amount |

|---|---|

| Government organizations | $183 million |

| Public Sector Pension Investment Board | $587 million |

| Total | $770 million |

Impact on public finances

Pension expenses are calculated based on Canadian public sector accounting standards and are included in the Public Accounts of Canada 2022.

- Pension expense includes employers’ contributions and recognized actuarial valuation gains and losses and other adjustments

- Net interest expense is calculated based on the average accrued pension obligations (benefits earned by members under their pension plan for pensionable service)

Table 3 shows a summary of transactions for the plans that resulted in expenses for the Government of Canada in fiscal year ended March 31, 2022.

| Pension plan | Pension expense | Net interest expense | Total expense |

|---|---|---|---|

| Public service | 3,754 | 938 | 4,692 |

| CAF | 2,103 | 886 | 2,989 |

| RCMP | 663 | 272 | 935 |

| Reserve Force | 54 | 1 | 55 |

| Total expenses | 6,574 | 2,097 | 8,671 |

Pension plan funding

Key measures to support sustainability

The governance framework of the public sector pension plans includes key measures that help ensure that the plans remain sustainable and affordable for plan members and taxpayers. These measures include:

- actuarial valuations, which provide an estimate of expenses and obligations

- reviews of the funded status of the plans

- annual reports on the plans

Each plan also has an advisory committee that comprises representatives of the employer, active plan members and retired plan members. These committees provide additional oversight, accountability and transparency by reviewing administration, design and funding of benefits.

The sustainability of the plans is supported by the Funding Policy for the Public Sector Pension Plans and a strong governance framework that was put in place in response to the 2014 Auditor General of Canada’s performance audit of the public sector pension plans. As part of the implementation of the Funding Policy for the Public Sector Pension Plans, which TBS, the RCMP and National Defence approved in 2018, a sustainability review of the plans is currently underway.

Actuarial valuations

An actuarial valuation is an actuarial analysis that provides information on the financial condition of a pension plan. Such valuations are performed regularly to support the administration of the pension plans. The Office of the Chief Actuary performs two types of actuarial valuations:

- Actuarial valuations for accounting purposes are conducted as at March 31 of each fiscal year to measure and report on the pension expense and obligations in the Public Accounts of Canada, and to provide the necessary information to prepare the plans’ financial statements.

- Actuarial valuations for funding purposes are conducted at least once every three years to determine the contribution rates, actuarial liability and the funded status of the plans. These valuations help the President of the Treasury Board make informed decisions on the financing of the pension plans. Assessments of the funded status of the pension plans are done annually, in consultation with the Office of the Chief Actuary.

Methodology and assumptions used in actuarial valuations

Assumptions underlying the actuarial valuation for accounting purposes are based on management’s best estimates. The Office of the Chief Actuary determines the best estimate assumptions used in actuarial valuations for funding purposes.

Actuarial assumptions refer to economic and demographic assumptions, such as future expected rates of return, inflation, salary levels, retirement ages and mortality rates, that actuaries use when carrying out an actuarial valuation or calculation.

Economic assumptions are set in order to conduct actuarial valuations. Population characteristics and benefit provisions are specific to each pension plan. As part of the economic assumptions, discount rates are used to determine the present value of the future pension payments (the accrued benefit obligation or the actuarial liability), the costs of benefits earned and the interest expenses.

Discount rates are set as follows:

For accounting purposes:

- For funded pension benefits (post-March 2000), the discount rates are the streamed expected rates of return on funds invested by the PSPIB.

- For unfunded pension benefits (pre-April 2000), the discount rates are the government’s cost of borrowing. That cost is derived from the yields on the actual zero-coupon yield curve for Government of Canada bonds, which reflect the timing of the expected future cash flows.

For funding purposes:

- For funded pension benefits (post-March 2000), the discount rates are the streamed expected rates of return on funds invested by the PSPIB.

- For unfunded pension benefits (pre-April 2000), the discount rates are the streamed weighted average of Government of Canada long-term bond rates. This average is a calculated 20-year weighted moving average of Government of Canada long-term bond rates projected over time. The streamed rates account for historical Government of Canada long-term bond rates and, over time, reflect expected Government of Canada long-term bond rates.

Table 4 presents some of the key economic assumptions used in the most recent actuarial valuations.

| Actuarial report | Long-term discount rate | Long-term rate | ||

|---|---|---|---|---|

| Funded pension benefits (post-March 2000)table 4 note * |

Unfunded pension benefits (pre-April 2000) |

Salary increase | Pension indexation | |

| For accounting purposes (as at March 31, 2021) |

5.9% | 1.8% to 1.85% (equivalent flat discount rate) | 2.6% | 2.0% |

| For funding purposes | ||||

| Public service (as at March 31, 2020) |

5.9% | 4.1% | 2.7% | 2.0% |

| CAF (as at March 31, 2019) | 6.0% | 4.5% | 2.7% | 2.0% |

| RCMP (as at March 31, 2021) | 5.9% | 4.0% | 2.6% | 2.0% |

| Reserve Force (as at March 31, 2019) |

6.0% | n/a | 2.7% | 2.0% |

Table 4 Notes

|

||||

Actuarial valuation report: financial position

Tables 5 and 6 show the results of the superannuation account and the pension fund of each pension plan as of the last triennial funding valuation.

| Balance | Public service (2020) |

RCMP (2021) |

CAF (2019) Regular Force |

|---|---|---|---|

| Account balance | 91,537 | 13,359 | 45,630 |

| Actuarial liability | 98,837 | 14,503 | 48,057 |

| Actuarial excess (shortfall) | (7,300) | (1,144) | (2,427) |

| Balance | Public service (2020) |

RCMP (2021) |

CAF (2019) | |

|---|---|---|---|---|

| Regular Force | Reserve Force | |||

| Actuarial value of assetstable 6 note * | 125,409 | 13,802 | 31,586 | 538 |

| Actuarial liability | 110,909 | 12,720 | 31,007 | 711 |

| Actuarial surplus (deficit) | 14,500 | 1,082 | 579 | (173) |

Table 6 Notes

|

||||

Source documents

- Report on the Public Service Pension Plan for the Fiscal Year Ended March 31, 2022

- Royal Canadian Mounted Police Pension Plan Annual Report, 2021–2022

- Canadian Armed Forces Pension Plan Annual Report, 2021–2022

- Public Sector Pension Investment Board annual report (2022)

- Public Accounts of Canada (2022)

- Actuarial Report on the Pension Plan for the Public Service of Canada as at 31 March 2020

- Actuarial Report on the Pension Plan for the Royal Canadian Mounted Police as at 31 March 2021

- Actuarial Report on the Pension Plan for the Canadian Forces: Regular Force and Reserve Force as at 31 March 2019

Glossary

- contributions

- Sums credited or paid by the employer and plan members to finance future pension benefits. Each year, the employer contributes amounts sufficient to fund the future benefits earned by employees in respect of that year, as determined by the President of the Treasury Board.

- deferred pension (also known as “deferred annuity”)

- A pension option that allows a member with at least two years of pensionable service to postpone their pension payments until a later date if they leave the public service before the retirement age applicable to them (60 or 65 years).

- disability

- A physical or mental impairment that prevents an individual from engaging in any employment for which the individual is reasonably suited by virtue of their education, training or experience and that can reasonably be expected to last for the rest of the individual’s life.

- pension obligation

- The value, discounted in accordance with actuarial assumptions, of all future payable benefits accrued as of the valuation date in respect of all previous pensionable service.

- pensionable service

- Periods of service to the credit of a public sector pension plan member. This service includes any complete or partial periods of purchased service (for example, service buyback or elective service).

- Public Sector Pension Investment Board

- A Crown corporation established on September 14, 1999, under the Public Sector Pension Investment Board Act. It manages the amounts transferred to it by the Government of Canada for the funding of benefits earned by members of the federal public sector pension plans. The board operates under the commercial name of PSP Investments.

- service buyback

- A legally binding agreement under which a member purchases a period of prior service to increase their pensionable service.

- survivor

For the purposes of the public service pension plan, a survivor is a person who, at the time of a plan member’s death, was married to the plan member before their retirement or was cohabiting with the plan member in a conjugal relationship prior to the member’s retirement and for at least one year prior to the date of death.

For the purposes of the pension plans for the CAF and RCMP, a survivor is a person who, at the time of a plan member’s death, was married to the plan member, or was cohabiting with the plan member in a conjugal relationship for at least one year prior to the plan member’s retirement, or if retired, prior to the member’s 60th birthday.

Appendix: Contribution rates

Contribution rates in the table below, effective January 1, apply to:

- public service pension plan members who were contributing to the before January 1, 2013

- public service pension plan members who are employed or deemed to be employed in operational service with Correctional Service Canada

- Canadian Armed Forces–Regular Force pension plan members

- Royal Canadian Mounted Police pension plan members

| From your salary… | In 2021 you contributed… | In 2022 you contributed… |

|---|---|---|

| On earnings up to the maximum covered by the Canada Pension Plan or Quebec Pension Plan ($61,600 in 2021 and $64,900 in 2022) | 9.83% | 9.36% |

| On earnings over the maximum covered by the Canada Pension Plan or Quebec Pension Plan | 12.26% | 12.48% |

|

Note: Contribution rates are reduced to 1% of salary for all plan members who reach the maximum 35 years of pensionable service. If you accumulate deemed operational service, you make an additional contribution of 0.62% of your salary to the pension plan for that service. |

||

| From your salary… | In 2021 you contributed… | In 2022 you contributed… |

|---|---|---|

| On earnings up to the maximum covered by the Canada Pension Plan or Quebec Pension Plan ($61,600 in 2021 and $64,900 in 2022) | 8.89% | 7.95% |

| On earnings over the maximum covered by the Canada Pension Plan or Quebec Pension Plan | 10.59% | 11.82% |

|

Note: Contribution rates are reduced to 1% of salary for all plan members who reach the maximum 35 years of pensionable service. |

||