Greenhouse gas and air pollutant emissions projections – 2025

Download the alternative format

(PDF format, 4.67 MB, 181 pages)

Executive Summary

ES.1 Context

This report presents Canada’s updated projections of greenhouse gas (GHG) and air pollutant emissions through 2035 under two core scenarios: With Measures (WM) and With Additional Measures (WAM). It includes historical emissions data, projected trends by sector and gas type, and the accounting contribution from land-use, land-use change and forestry (LULUCF), nature-based climate solutions (NBCS), and agriculture measures. The report also provides sensitivity, uncertainty, emissions embodied in trade, and individual policy analyses, methodological details, and a comprehensive list of policies and measures included in each scenario.

Canada’s legislative foundation for these projections is the Canadian Net-Zero Emissions Accountability Act, which commits Canada to net-zero emissions by 2050. The Act sets interim targets for 2030, 2035, 2040, and 2045, and mandates the development of Emissions Reduction Plans for each of the milestone years and oversight by an independent advisory body. Canada’s 2030 Emissions Reduction Plan, released in 2022, targeted a 40% to 45% reduction below 2005 levels by 2030. The Plan also included several economy-wide and sector-specific measures to reach the 2030 target.

Canada’s international climate and air pollutant emissions commitments also shape its emissions reduction efforts. Under the United Nations Framework Convention on Climate Change (UNFCCC) and Paris Agreement, Canada has pledged to reduce GHG emissions. For air pollutants such as sulphur dioxide (SO2), nitrogen oxides (NOX), volatile organic compounds (VOCs), fine particulate matter (PM2.5), and black carbon, Canada has taken on emission reduction commitments in several international fora including under the United Nations Economic Commission for Europe’s (UNECE) Air Convention, the Arctic Council and the Canada–United States Air Quality Agreement. Canada has established commitments under the Gothenburg Protocol and supports the Arctic Council’s black carbon reduction goals, while continuing to align with evolving international standards.

Building on these legislative and international frameworks, the report models future emissions using the WM and WAM scenarios. The WM scenario reflects current legislative, regulatory and financial conditions as of November 2025, while the WAM scenario includes additional announced initiatives not yet fully implemented, along with NBCS and agriculture measures. Both scenarios incorporate the LULUCF accounting contribution.

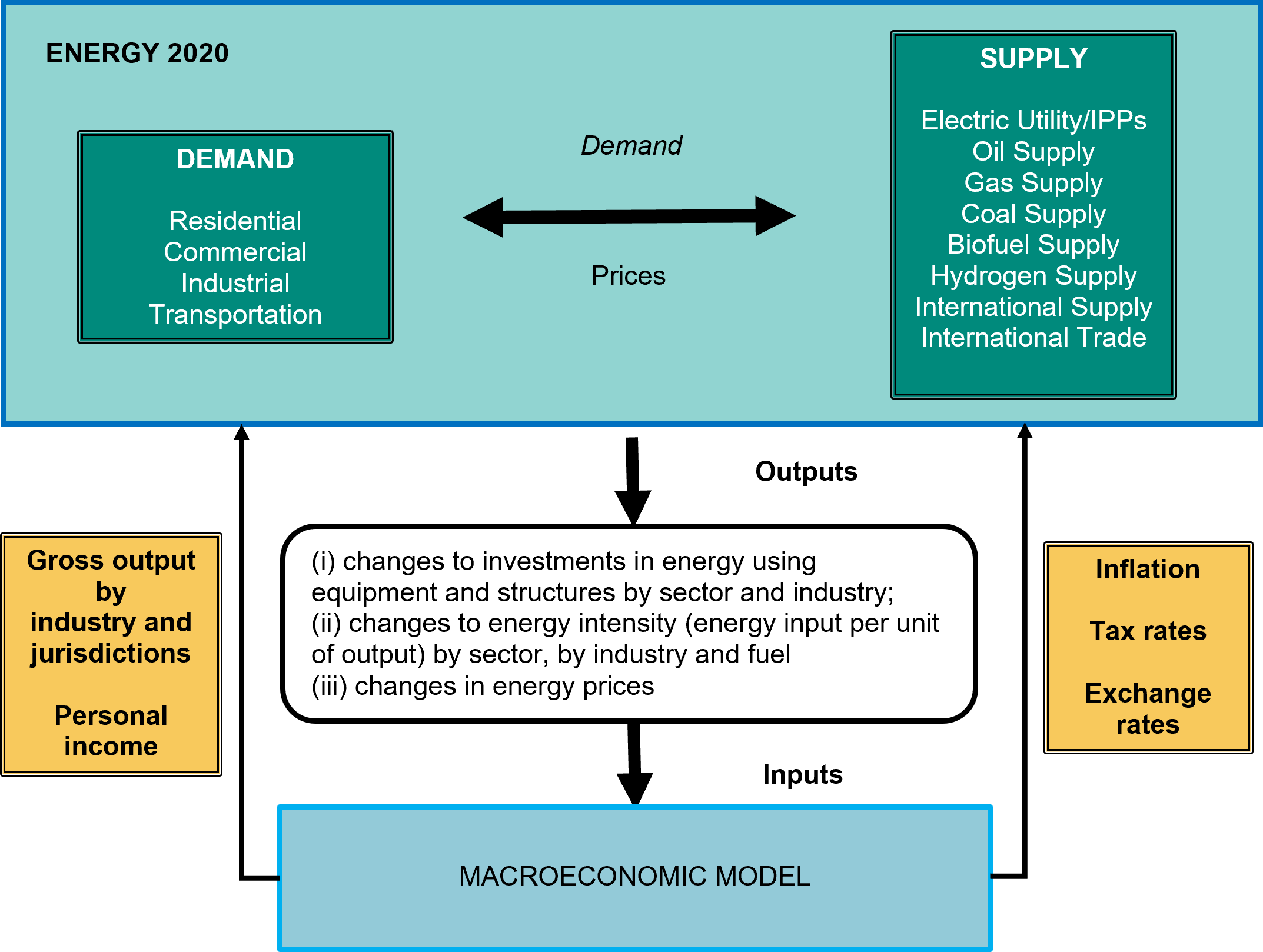

To develop these projections, Environment and Climate Change Canada (ECCC) uses the Energy, Emissions and Economy Model for Canada (E3MC). This integrated modelling framework combines ENERGY 2020 and the North America Economic Model to simulate energy supply and demand, macroeconomic activity, and policy impacts. E3MC draws on data from Statistics Canada, the Canada Energy Regulator (CER), Natural Resources Canada (NRCan), and ECCC’s National Inventory Report (NIR). Projections are updated annually using the latest historical data and input from federal, provincial, and territorial partners.

Results are organized by economic sector and gas type, as well as aligned with Intergovernmental Panel on Climate Change (IPCC) categories for international reporting. This report includes historical data for 1990, 2005, and 2023, along with projections for 2026, 2030 and 2035. Energy model data span 1990 to 2023 historically, and 2024 to 2035 for projections, while macroeconomic historical estimates extend to 2024 with projections starting in 2025. Complete time series data are available through the Government of Canada’s open data portal, and interactive visualizations can be accessed via Canada’s Greenhouse Gas Emissions Projections website.

The report is organized into three main sections and two annexes:

- section 1 outlines the legislative and policy context, including Canada’s international commitments

- it also describes the methodological framework used to develop the projections and defines the WM and WAM scenarios

- section 2 presents detailed GHG emissions projections under the WM and WAM scenarios

- it includes sensitivity analyses that examine the effects of varying economic and energy assumptions such as gross domestic product (GDP), growth, population trends, and oil and gas prices

- it also includes uncertainty analysis around WM estimates and the individual impacts of selected key policies

- section 3 provides projections of air pollutant emissions under both scenarios

- annex 1 contains technical details on the modelling approach, assumptions, and data sources used throughout the report

- annex 2 contains a detailed list of policies and measures included in the projections

ES.2 Greenhouse gas emissions projections

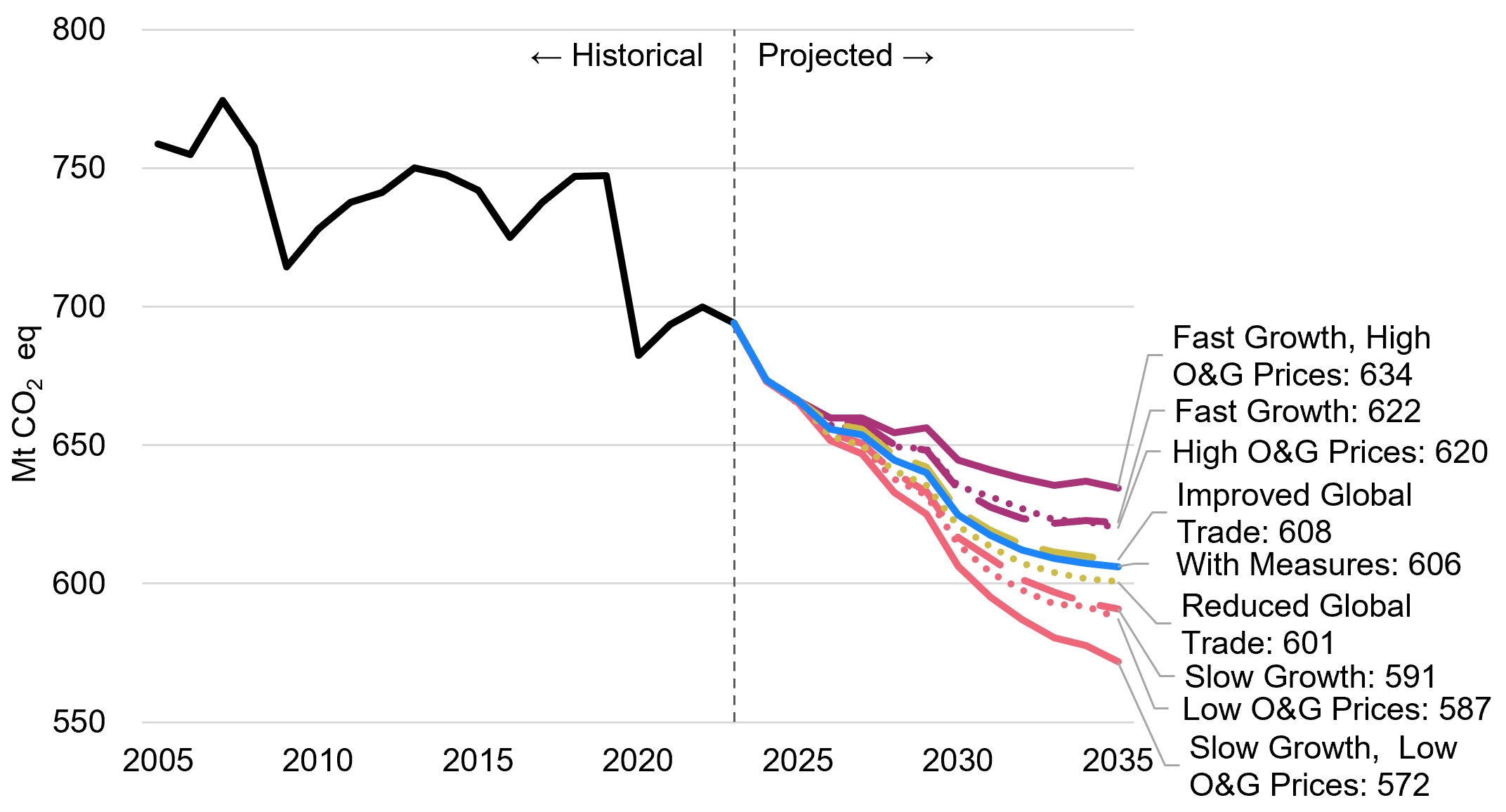

Between 2005 and 2023, Canada’s total GHG emissions (excluding the LULUCF accounting contribution) declined by 8.5%, reaching 694 megatonnes (Mt) of carbon dioxide equivalents (CO2 eq) in 2023. The Electricity sector had the largest decline, as electricity emissions fell by 58% due to the phase out of coal and increased reliance on non-emitting sources. Emissions from the Oil and Gas sector increased modestly since 2005 but have declined from their 2014 peak. Emissions intensity, GHG emissions per unit of GDP, has dropped by 44% since 1990. This reflects improvements in energy efficiency and a shift towards cleaner energy sources.

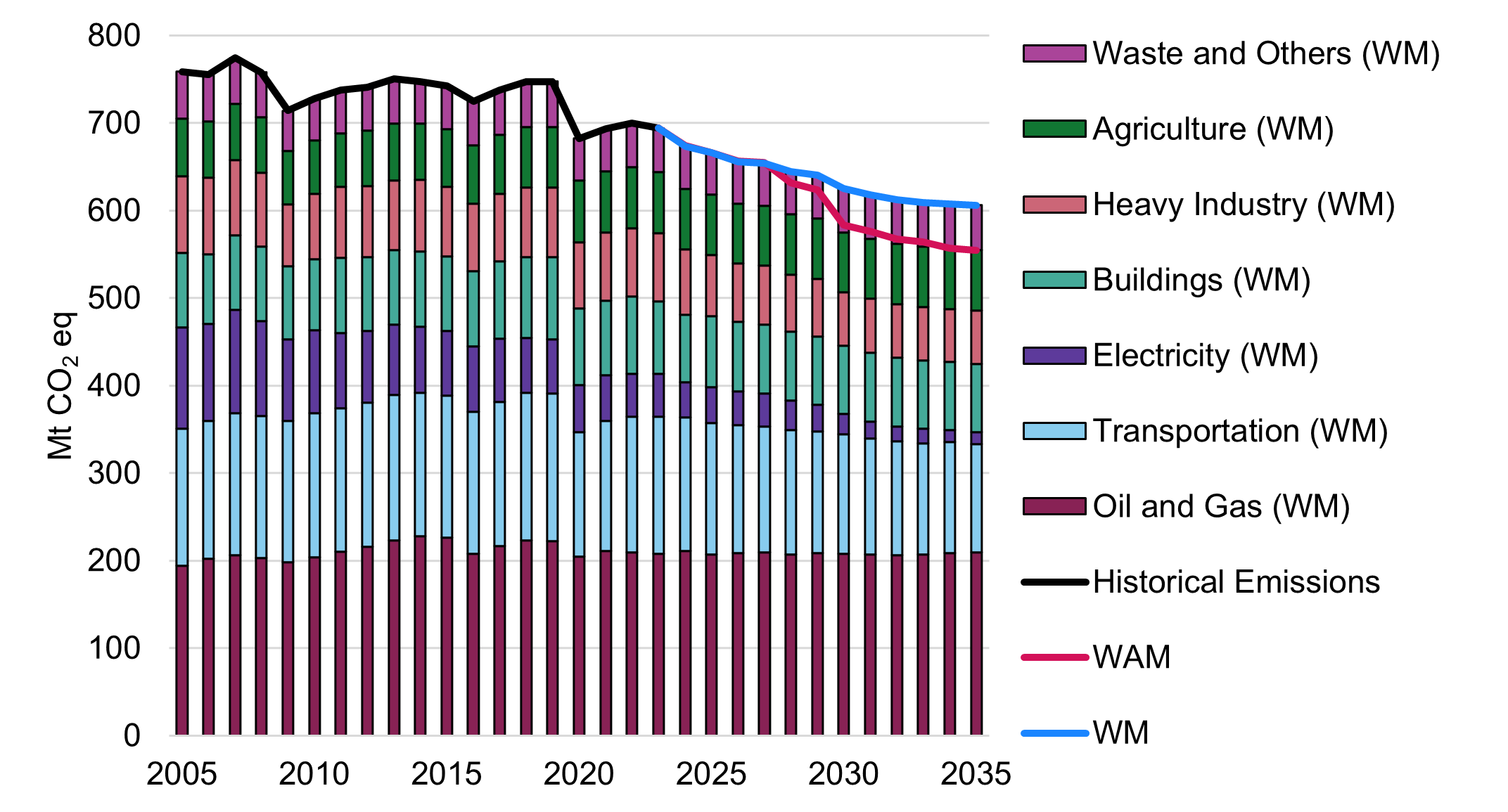

Under the WM scenario, GHG emissions are projected to decline to 625 Mt in 2030. Including the LULUCF sector accounting contribution, 2030 emissions are projected to be 600 Mt in the WM scenario. Post-2030, emissions projected in the WM scenario continue to decline, reaching 577 Mt in 2035, including the LULUCF accounting contribution.

Under the WAM scenario, emissions in 2030 decline to 546 Mt, including LULUCF, NBCS, and agriculture measures. Post-2030, emissions projected in the WAM scenario (including LULUCF, NBCS, and agriculture measures) continue to decline, reaching 513 Mt in 2035.

Both the WM and WAM scenarios project continued reductions in emissions across all major sectors:

- Oil and Gas:

- Despite continued increases in production, emissions are expected to stay flat in the WM scenario with methane regulations, industrial carbon pricing, clean fuel requirements, and increased deployment of carbon capture and storage (CCS) technologies.

- The WAM scenario includes further reductions through the Enhanced Oil and Gas Methane Regulations , announced CCS projects, and increases in efficiency.

- Transportation:

- Emissions will decrease as zero-emission vehicles become more prevalent, supported by Electric Vehicle Availability Standards for light-duty vehicles.

- Light-duty and medium and heavy-duty vehicle standards continue to lead to declines in projected emissions over time.

- Electricity:

- The sector will continue to decarbonise, with the Clean Electricity Regulations and increasing adoption of renewable generation and storage technologies.

- By 2035, wind energy is projected to account for up to 24% of generation.

- Heavy Industry:

- Emissions will decline through fuel switching, electrification, CCS, and modernization of facilities.

- Buildings:

- Emissions are projected to fall due to electrification, heat pump adoption, and more stringent building codes.

- Despite growth in residential and commercial space, efficiency gains will drive reductions.

- Agriculture:

- Emissions remain stable in the WM scenario and decline slightly in WAM due to improved land-use practices and nitrogen management.

- NBCS and agriculture measures are projected to contribute up to 12 Mt CO2 eq in annual reductions by 2035.

- Waste and Others:

- GHG emissions in the Waste and Others sector remain near 2023 levels in the WM scenario with a slight post-2030 increase from light manufacturing.

- The WAM scenario achieves deeper reductions, especially in solid waste and light manufacturing, through measures like the Landfill Methane Regulations and carbon revenue returns, keeping emissions below or equal to 2023 levels.

| Sector | 1990 | 2005 | 2023 | 2026Footnote a | 2030Footnote a | 2035Footnote a | 2026Footnote b | 2030Footnote b | 2035Footnote b |

|---|---|---|---|---|---|---|---|---|---|

| Oil and Gas | 117 | 194 | 208 | 209 | 207 | 209 | 208 | 175 | 177 |

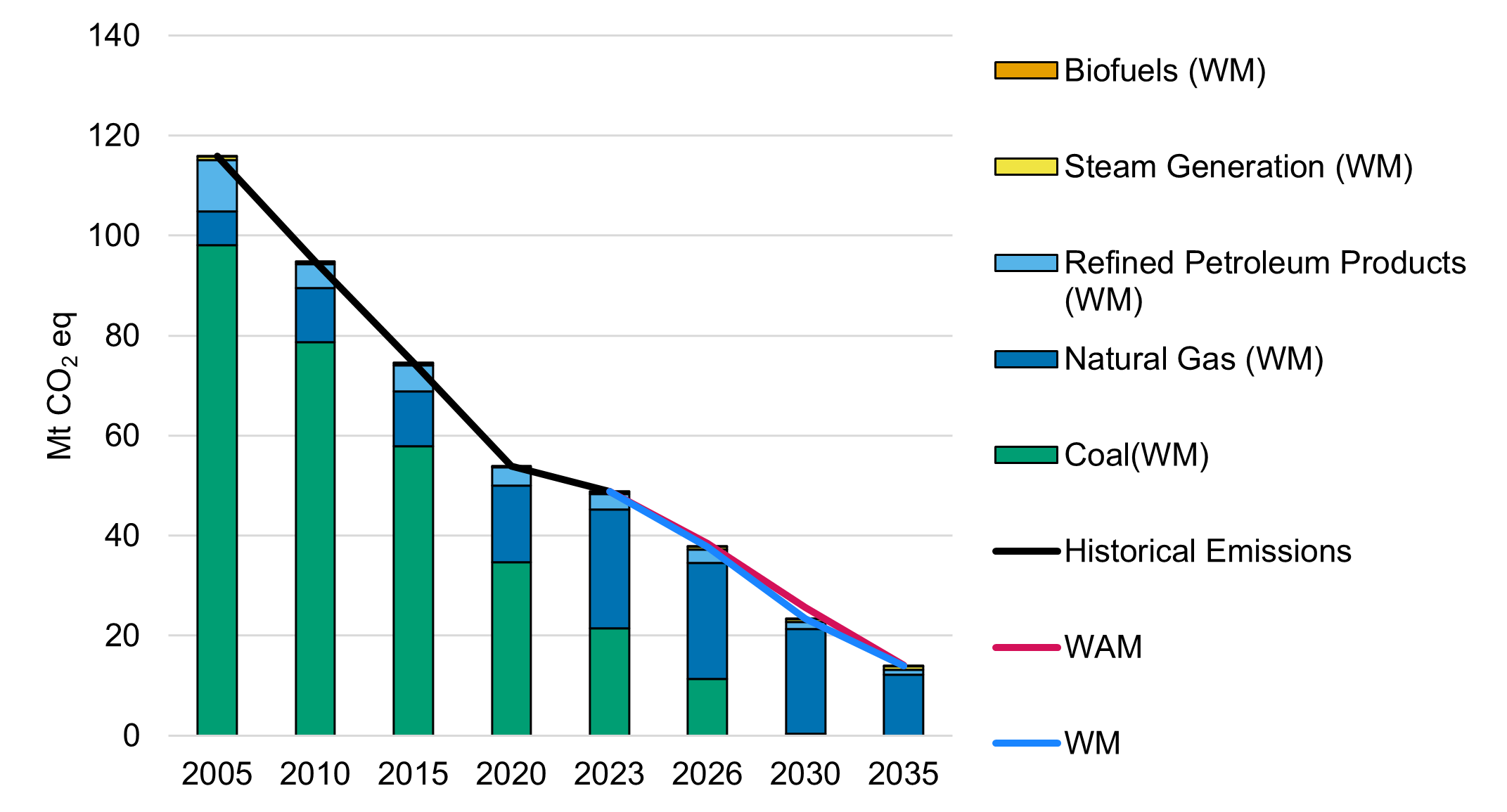

| Electricity | 94 | 116 | 49 | 38 | 23 | 14 | 39 | 26 | 14 |

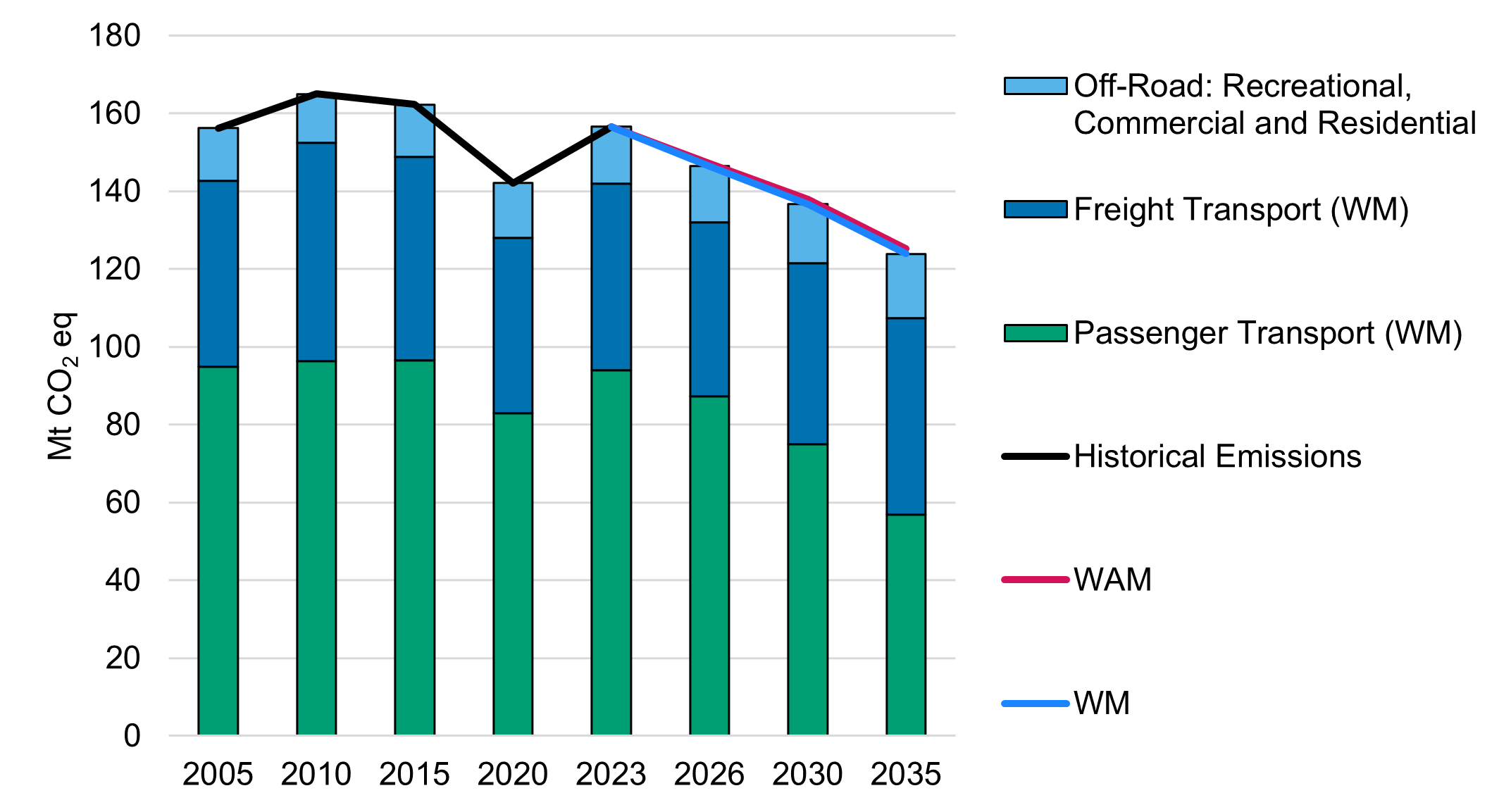

| Transportation | 118 | 156 | 157 | 146 | 137 | 124 | 147 | 138 | 125 |

| Heavy Industry | 97 | 88 | 78 | 67 | 61 | 60 | 67 | 59 | 57 |

| Buildings | 72 | 85 | 83 | 80 | 78 | 78 | 79 | 76 | 69 |

| AgricultureFootnote * | 51 | 66 | 69 | 69 | 69 | 69 | 69 | 68 | 69 |

| Waste and Others | 57 | 54 | 50 | 48 | 50 | 51 | 48 | 41 | 42 |

| Subtotal | 606 | 759 | 694 | 656 | 625 | 606 | 656 | 583 | 554 |

| LULUCF Accounting Contribution | 27 | 0 | -39 | -21 | -25 | -30 | -21 | -25 | -30 |

| NBCS and Agriculture Measures | NA | NA | NA | NA | NA | NA | NA | -12 | -12 |

| Total | 633 | 759 | 655 | 635 | 600 | 577 | 636 | 546 | 513 |

| WCI CreditsFootnote ** | NA | NA | -10 | NA | NA | NA | -6 | -4 | 0 |

Note: Totals may not match due to rounding. Historical data up to 2023 are sourced from NIR2025. Data from 2024 to 2035 are modelled projections developed using ECCC’s analytical framework. Access more data on the open data portal .

Note: *Historical emissions include data from NIR2023 and NIR2025, and also include LULUCF accounting contribution. Access more data on the open data portal.

- WM25: Current With Measures scenario.

- WAM25: Current With Additional Measures scenario.

- WM23: With Measures scenario published in the 2023 Emissions Projections Report (EPR 2023).

- WAM23: With Additional Measures scenario published in EPR2023 in 2023.

Long description

| Year | 2023 NIR* | WM23 | WAM23 (incl. NBCS + Ag. Measures) | 2025 NIR* | 2025 WM | 2025 WAM | 2025 WAM (incl. NBCS/Ag Measures) |

|---|---|---|---|---|---|---|---|

| 2005 | 732 | - | - | 759 | - | - | - |

| 2006 | 722 | - | - | 752 | - | - | - |

| 2007 | 751 | - | - | 778 | - | - | - |

| 2008 | 733 | - | - | 760 | - | - | - |

| 2009 | 675 | - | - | 700 | - | - | - |

| 2010 | 712 | - | - | 738 | - | - | - |

| 2011 | 727 | - | - | 755 | - | - | - |

| 2012 | 719 | - | - | 742 | - | - | - |

| 2013 | 719 | - | - | 747 | - | - | - |

| 2014 | 692 | - | - | 721 | - | - | - |

| 2015 | 725 | - | - | 746 | - | - | - |

| 2016 | 695 | - | - | 715 | - | - | - |

| 2017 | 693 | - | - | 719 | - | - | - |

| 2018 | 707 | - | - | 730 | - | - | - |

| 2019 | 697 | - | - | 722 | - | - | - |

| 2020 | 629 | - | - | 660 | - | - | - |

| 2021 | 637 | 637 | 637 | 665 | - | - | - |

| 2022 | - | 688 | 686 | 709 | - | - | - |

| 2023 | - | 637 | 632 | 655 | 655 | 655 | - |

| 2024 | - | 630 | 616 | - | 667 | 667 | - |

| 2025 | - | 624 | 602 | - | 642 | 642 | - |

| 2026 | - | 615 | 577 | - | 635 | 636 | - |

| 2027 | - | 608 | 554 | - | 632 | 633 | - |

| 2028 | - | 590 | 528 | - | 621 | 609 | - |

| 2029 | - | 577 | 506 | - | 618 | 602 | - |

| 2030 | - | 560 | 468 | - | 600 | 558 | 546 |

| 2031 | - | 556 | 457 | - | 592 | 551 | 539 |

| 2032 | - | 550 | 448 | - | 586 | 541 | 529 |

| 2033 | - | 548 | 442 | - | 584 | 538 | 527 |

| 2034 | - | 544 | 435 | - | 580 | 530 | 518 |

| 2035 | - | 541 | 423 | - | 577 | 525 | 513 |

ES.3 Air pollutant emissions projections

Canada’s air pollutant reporting is guided by its commitments (including voluntary) under international agreements and national environmental policies, as outlined in Section 1. Air pollutant emissions projections for NOX, SOX, VOCs, particulate matter, black carbon, carbon monoxide, mercury, and ammonia through 2035 are available by pollutant under both the WM and WAM scenarios. These projections are based on historical data from 1990 to 2023. Historical data are reported in Canada's Air Pollutant Emissions Inventory Report 2025 (APEI2025) and Canada's Black Carbon Inventory Report 2025.

The projections indicate that Canada remains on track to meet its international air emissions reduction commitments under both scenarios, driven by cleaner fuels, electrification, and regulatory improvements. This underscores the country’s leadership in environmental stewardship and cross-border collaboration.

Table ES.2 summarises historical and projected emissions by pollutant. Open data Tables A37 through A46 provide detailed national emissions data by economic sector and pollutant.

| Pollutant | 1990 | 2005 | 2023 | 2026 Footnote a | 2030 Footnote a | 2035 Footnote a | 2026 Footnote b | 2030 Footnote b | 2035 Footnote b |

|---|---|---|---|---|---|---|---|---|---|

| Nitrogen Oxides | 2 236 | 2 259 | 1 228 | 1 006 | 963 | 950 | 1 004 | 960 | 944 |

| Sulphur Oxides | 3 010 | 2 095 | 608 | 544 | 443 | 458 | 542 | 442 | 451 |

| Volatile Organic Compounds | 2 200 | 2 256 | 1 368 | 1 174 | 1 184 | 1 202 | 1 174 | 989 | 1 000 |

| Total Particulate MatterFootnote * (excl. Open SourcesFootnote †) | 1 080 | 633 | 528 | 500 | 497 | 507 | 499 | 494 | 499 |

| Total Particulate MatterFootnote * (incl. Open SourcesFootnote †) | 19 976 | 21 161 | 26 804 | 28 550 | 31 508 | 33 946 | 28 575 | 31 455 | 33 961 |

| PM10Footnote ** (excl. Open SourcesFootnote †) | 640 | 386 | 278 | 262 | 258 | 260 | 262 | 256 | 254 |

| PM10Footnote ** (incl. Open SourcesFootnote †) | 6 528 | 6 809 | 8 172 | 8 650 | 9 477 | 10 158 | 8 656 | 9 461 | 10 159 |

| PM2.5Footnote *** (excl. Open SourcesFootnote †) | 458 | 271 | 160 | 149 | 144 | 142 | 149 | 142 | 136 |

| PM2.5Footnote *** (incl. Open SourcesFootnote †) | 1 609 | 1 364 | 1 370 | 1 415 | 1 515 | 1 597 | 1 416 | 1 510 | 1 592 |

| Carbon Monoxide | 13 082 | 9 006 | 4 518 | 4 320 | 4 276 | 4 202 | 4 322 | 4 264 | 4 112 |

| Mercury (Kilograms) | 33 541 | 7 947 | 3 131 | 2 713 | 2 482 | 2 531 | 2 707 | 2 470 | 2 507 |

| Ammonia | 395 | 490 | 495 | 490 | 520 | 550 | 490 | 520 | 551 |

| Black Carbon | NA | NA | 21.6 | 19.8 | 18.4 | 17.9 | 19.7 | 18.3 | 17.4 |

Note: Historical data up to 2023 are sourced from APEI2025 and Canada's Black Carbon Inventory Report 2025. Data from 2024 to 2035 are modelled projections developed using ECCC’s analytical framework. Access more data on the open data portal. Following international reporting standards, emissions from international aviation at cruise altitude and international marine navigation are excluded from national totals.

Acknowledgments

The Analysis and Modelling Division (AMD) of Environment and Climate Change Canada wishes to acknowledge the individuals and organisations that contributed to the Canada's Greenhouse Gas and Air Pollutant Emissions Projections Report 2025. Although the list of all organisations and individuals who provided technical support is too long to include here, the Division would like to highlight the contributions of the following authors and reviewers.

Overall coordination of Canada's Greenhouse Gas and Air Pollutant Emissions Projections Report 2025 was led by Alexandre Dumas with Glasha Obrekht providing overall direction, and with support from Shuvo Barman, Brock Batey, Elise Coffey, Noah Conrad, Thomas Dandres, Doruk Kaymak, Richard Laferrière, Michelle Lasota, Matthew Lewis, Yang Li, Izu Maduekwe, Ata Malfuzi, Levi Mitchell, Milad Naeimi, Howard Park, Bryn Parsons, Serena Rawn, Frédéric Roy-Vigneault, Benjamin Sas Trakinsky, John St-Laurent O'Connor, Timothy Timothy, Jocelyn Tong, Robert Sand Ty, Alice Umuhoza, Marshal Wang, Samantha Wiedrich, Robin White, and Robert Xu. Development of the projections also benefited from support from Systematic Solutions, Inc and Oxford Economics.

AMD acknowledges the valuable contributions of its federal partners, whose input was essential to the development of these projections. The following departments provided key data and expertise:

- Agriculture and Agri-Food Canada (AAFC)

- Canada Energy Regulator (CER)

- Environment and Climate Change Canada (ECCC)

- Finance Canada

- Natural Resources Canada (NRCan)

- Statistics Canada

- Transport Canada

Details on each group’s contribution are provided in Annex 1.

1 Context

This section provides the context for Canada’s 2025 greenhouse gas (GHG) and air pollutant emissions projections. It outlines the legislative and policy framework established by the Canadian Net-Zero Emissions Accountability Act, details Canada’s international climate and air pollutant emissions commitments, and explains the country’s domestic and international reporting obligations.

It also introduces the emissions scenarios used throughout the report and describes the assumptions, scope, and rationale behind their development. These scenarios are developed using a consistent, transparent modelling framework that integrates the latest economic, energy, and policy data to estimate future emissions trajectories. Together, these elements establish the basis for the projections presented in subsequent sections.

1.1 Purpose and scope of the report

The purpose of this report is to present Canada’s updated projections of GHG and air pollutant emissions through 2035. The projections fall under two main policy scenarios: the With Measures (WM) scenario and the With Additional Measures (WAM) scenario. These projections are developed by Environment and Climate Change Canada (ECCC), using the Energy, Emissions, and Economy Model for Canada (E3MC), in alignment with international reporting standards and domestic legislative requirements.

The report aims to:

- provide a comprehensive overview of Canada’s expected emissions trajectory under current and announced climate policies

- inform policy development and decision-making at federal, provincial, and territorial levels

- support Canada’s commitment to transparency and accountability under the Canadian Net-Zero Emissions Accountability Act

- contribute to the country’s obligations under the United Nations Framework Convention on Climate Change (UNFCCC)

- uphold international obligations under agreements such as the Gothenburg Protocol and the Canada–United States Air Quality Agreement (AQA)

- facilitate stakeholder engagement and public understanding of Canada’s climate and air quality policy framework

- highlight methodological improvements and updates to modelling frameworks and assumptions since the previous report

The projections presented in this report reflect the most recent historical data available as of November 2025 and incorporate input from extensive consultations with federal, provincial, and territorial partners. They should not be viewed as forecasts of expected outcomes, but rather scenario-based projections that illustrate potential outcomes under defined assumptions and policies.

This report is organized to provide a comprehensive and transparent overview of Canada’s GHG and air pollutant emissions projections through 2035. It is structured to support both technical analysis and policy development, while ensuring accessibility for a broad range of stakeholders.

All data tables referenced in this report are available through the Government of Canada’s open data portal, which also provides additional tables covering the full range of historical and projection years included in the report. Annex tables are identified by the prefix “A.” While tables A1 to A16 are printed in this document, tables A17 to A46 are only accessible through the open data portal. Links to the open data portal are provided throughout the document.

The report is divided into the following main sections:

- section 1: context

- introduces the legislative and policy framework guiding Canada’s climate and air pollutant emissions commitments, including international agreements and reporting obligations

- it also defines the emissions scenarios used throughout the report

- section 2: greenhouse gas emissions projections

- presents detailed GHG emissions projections by economic sector, Intergovernmental Panel on Climate Change (IPCC) category, and gas type

- it includes historical trends, comparisons to previous projections, decomposition analyses, and assessments of key mitigation measures

- emissions from land use, land-use change, and forestry (LULUCF), nature-based climate solutions (NBCS), and agriculture measures (Ag. Measures) are reported separately

- section 3: air pollutant emissions projections

- provides projections for key air pollutants under the WM and WAM scenarios

- it includes sectoral breakdowns and evaluates Canada’s progress toward international air emissions reduction targets

- annex 1

- provides detailed information on the modelling framework, key assumptions, data sources, and methodological improvements

- it also includes projections, uncertainty analyses, as well as detailed results

- annex 2

- provides a detailed list of all modelled policies

Supporting materials such as the Executive Summary, the List of Figures, the List of Tables, the List of Abbreviations, and the List of Chemical Formulas and Units provide additional context and facilitate navigation of the report.

1.2 Legislative framework

The Canadian Net-Zero Emissions Accountability Act, enacted in June 2021, legally enshrines Canada’s commitment to achieve net-zero GHG emissions by 2050.

The Act establishes a framework for accountability and transparency and mandates the Government of Canada to:

- set emissions reduction targets for 2030, 2035, 2040, and 2045

- develop and table Emissions Reduction Plans for each target year

- report on progress through biennial progress reports and final assessment reports

- establish an independent advisory body to provide expert advice and engage Canadians on pathways to net-zero

- table progress reports and final assessments in Parliament, ensuring public accountability

Canada’s 2030 Emissions Reduction Plan, released in March 2022, is the first climate plan developed under the Act. It outlines a sector-by-sector roadmap to reduce GHG emissions by 40% to 45% below 2005 levels by 2030. The 2030 Emissions Reduction Plan includes:

- an interim objective of a 20% reduction by 2026

- detailed measures across all major economic sectors

- commitments to transparency in modelling and analytical approaches

In addition to domestic legislation, Canada’s climate strategy is shaped by its participation in international agreements, detailed in the following sections.

In 2023, ECCC published the first progress report on the Emissions Reduction Plan, which included:

- updates on emissions trends and progress toward the 2030 target

- a status update on each federal climate measure

- findings from an expert review of ECCC’s modelling framework, the Action Plan and the status update on progress made to address proposed recommendations

Annex 1 includes an update to the progress made in implementing the Independent Modelling Review Action Plan since the last progress update, which was released in 2024 as part of Canada’s First Biennial Transparency Report under the Paris Agreement (BTR1).

1.3 International climate and air pollution reduction commitments

Canada’s international climate and air pollution reduction commitments are grounded in a series of multilateral agreements and protocols. While reducing GHG emissions is central to Canada’s climate strategy, improving air quality remains a parallel priority, both for public health and environmental protection. The following sections outline Canada’s obligations and actions related to GHG emissions and air pollutant emissions under these frameworks.

1.3.1 Greenhouse gas emissions

Canada has been actively engaged in international climate action since signing the UNFCCC in 1992. The country set its first national GHG emissions target in 2000 and has since strengthened its commitments through successive agreements. In 2016, Canada ratified the Paris Agreement, and in 2021, it submitted an enhanced 2030 emissions reduction target. That same year, Canada passed the

1.3.2 Air pollutant emissions

Air quality is important and influences the daily life of all Canadians. It affects not only human health, but also the delicate balance of the natural environment, the integrity of buildings and infrastructure, crop production, and the overall state of the economy. Projections of air pollutant emissions play a pivotal role in guiding both domestic and international efforts aimed at improving air quality.

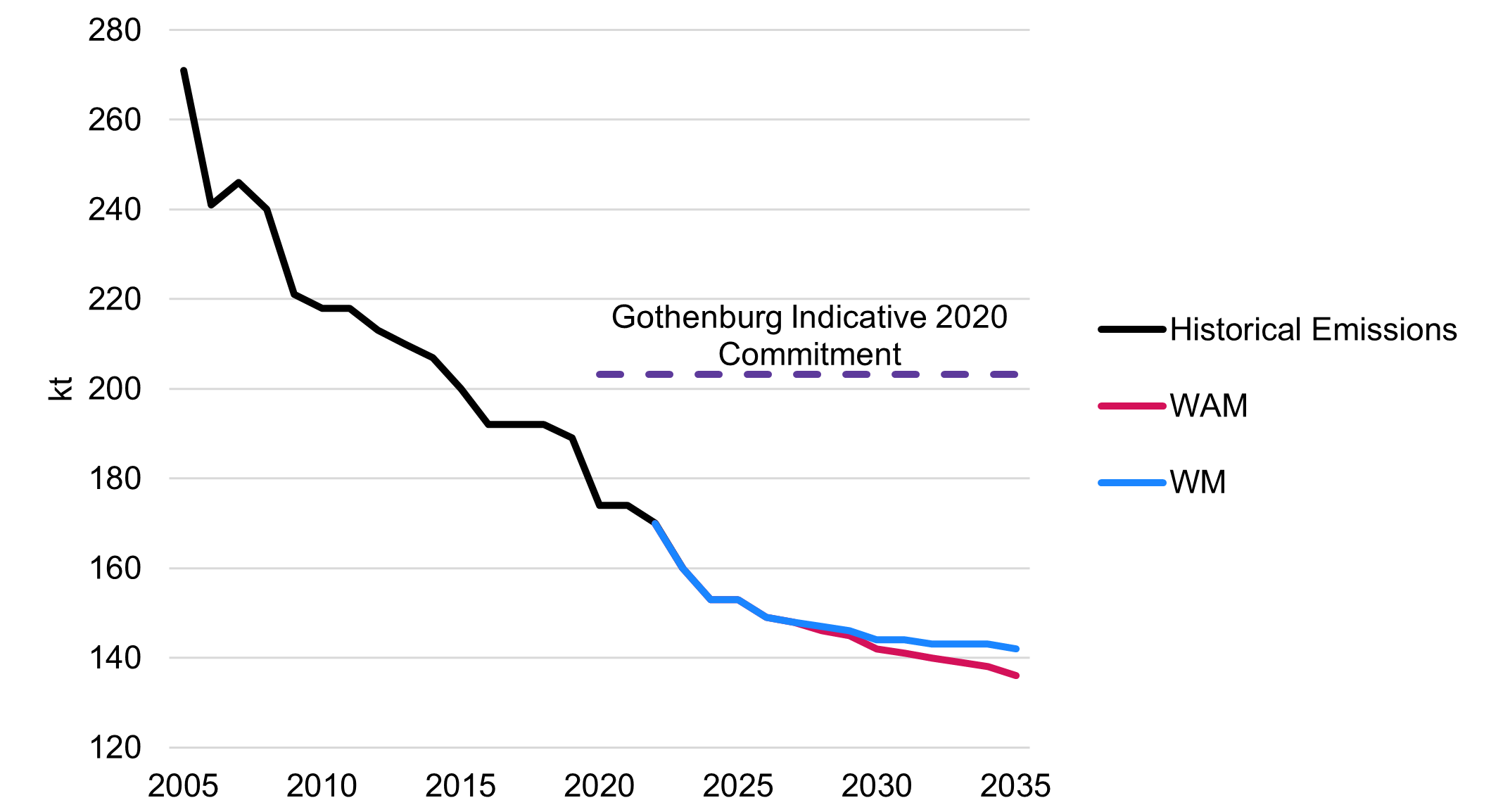

Canada actively collaborates with other countries to address transboundary air pollution, recognizing its significant impact on national air quality. Canada is party to three major international agreements: the Canada–United States Air Quality Agreement, the Arctic Council’s Framework for Action on Enhanced Black Carbon and Methane Emissions Reductions, and the United Nations Economic Commission for Europe’s Convention on Long-range Transboundary Air Pollution (CLRTAP or Air Convention), and its Gothenburg Protocol. Negotiations to revise the Gothenburg Protocol are underway, and expected to continue over the near-term, while negotiations to revise the AQA and develop a new goal for black carbon under the Arctic Council may resume in the coming years. These updates aim to incorporate evolving scientific knowledge, technological advancements, and policy developments.

The Gothenburg Protocol is the most active of the eight protocols under the Air Convention. It targets pollutants that contribute to acidification, eutrophication, and ground-level ozone. In 2012, the Protocol was amended to include fine particulate matter (PM2.5) and updated emissions reduction commitments to be met in 2020 and maintained. Canada ratified the amended Gothenburg Protocol in November 2017, and it entered into force domestically in October 2018. Under this agreement, Canada committed to specific emission reductions for key pollutants.

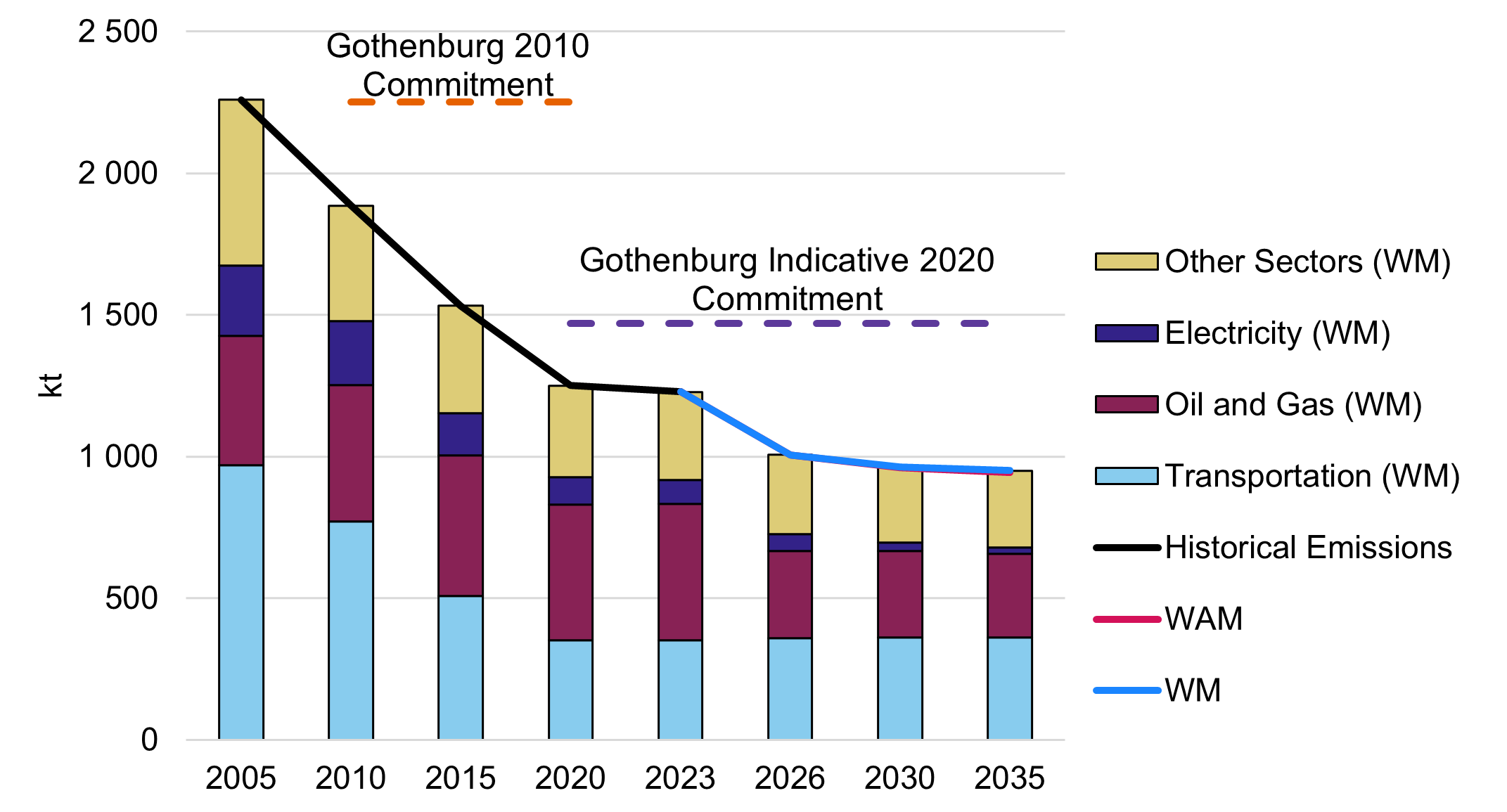

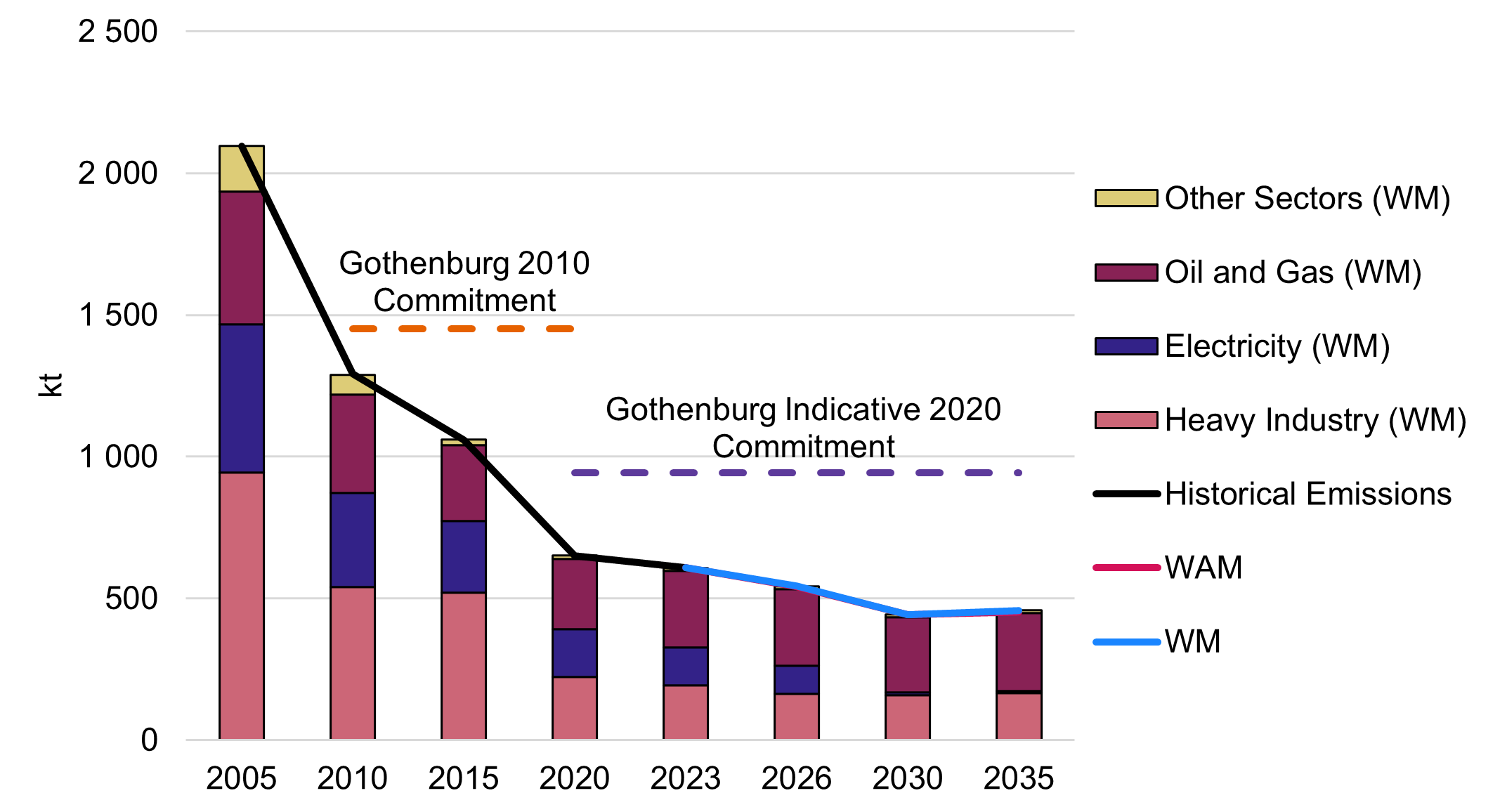

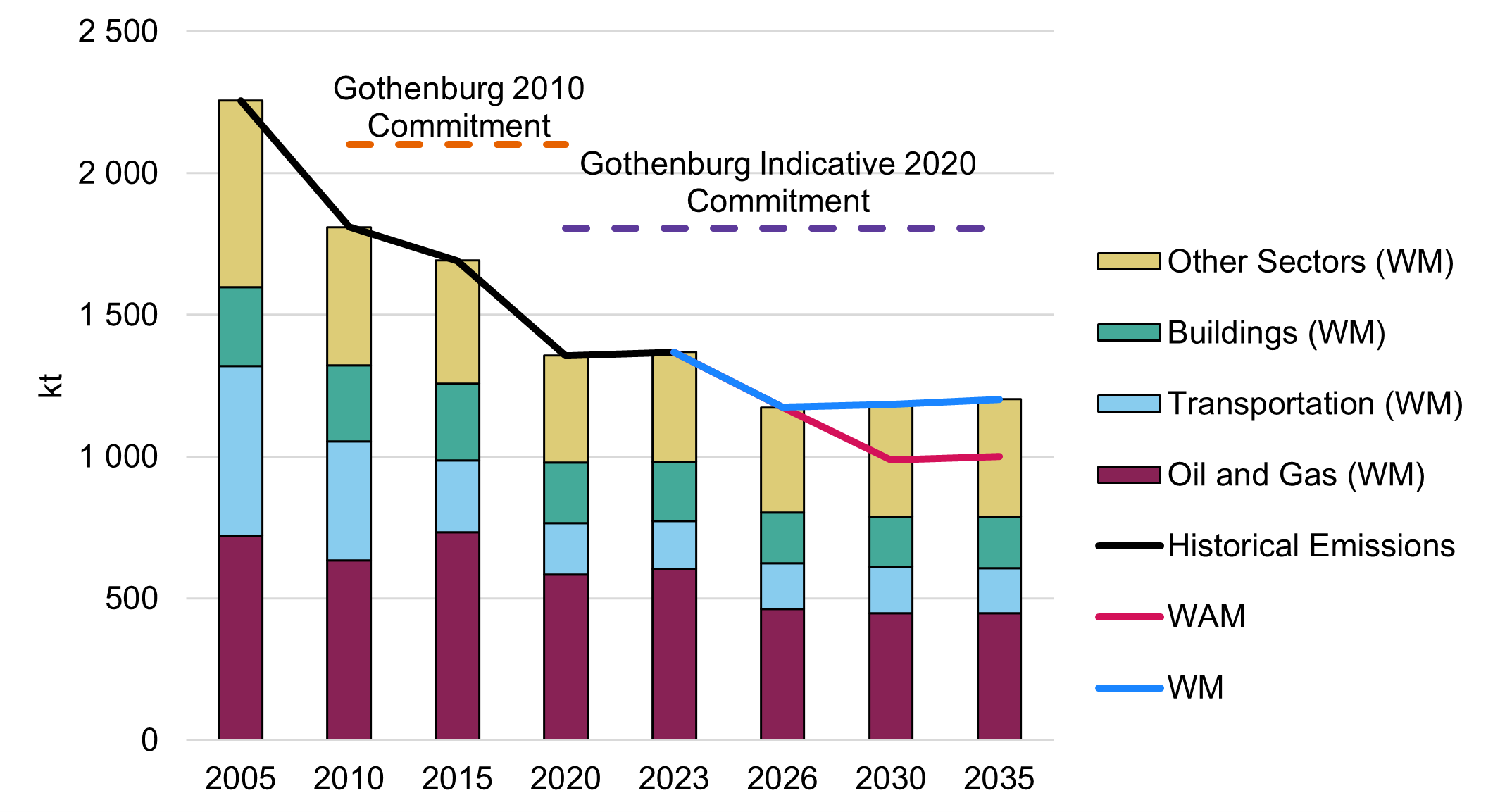

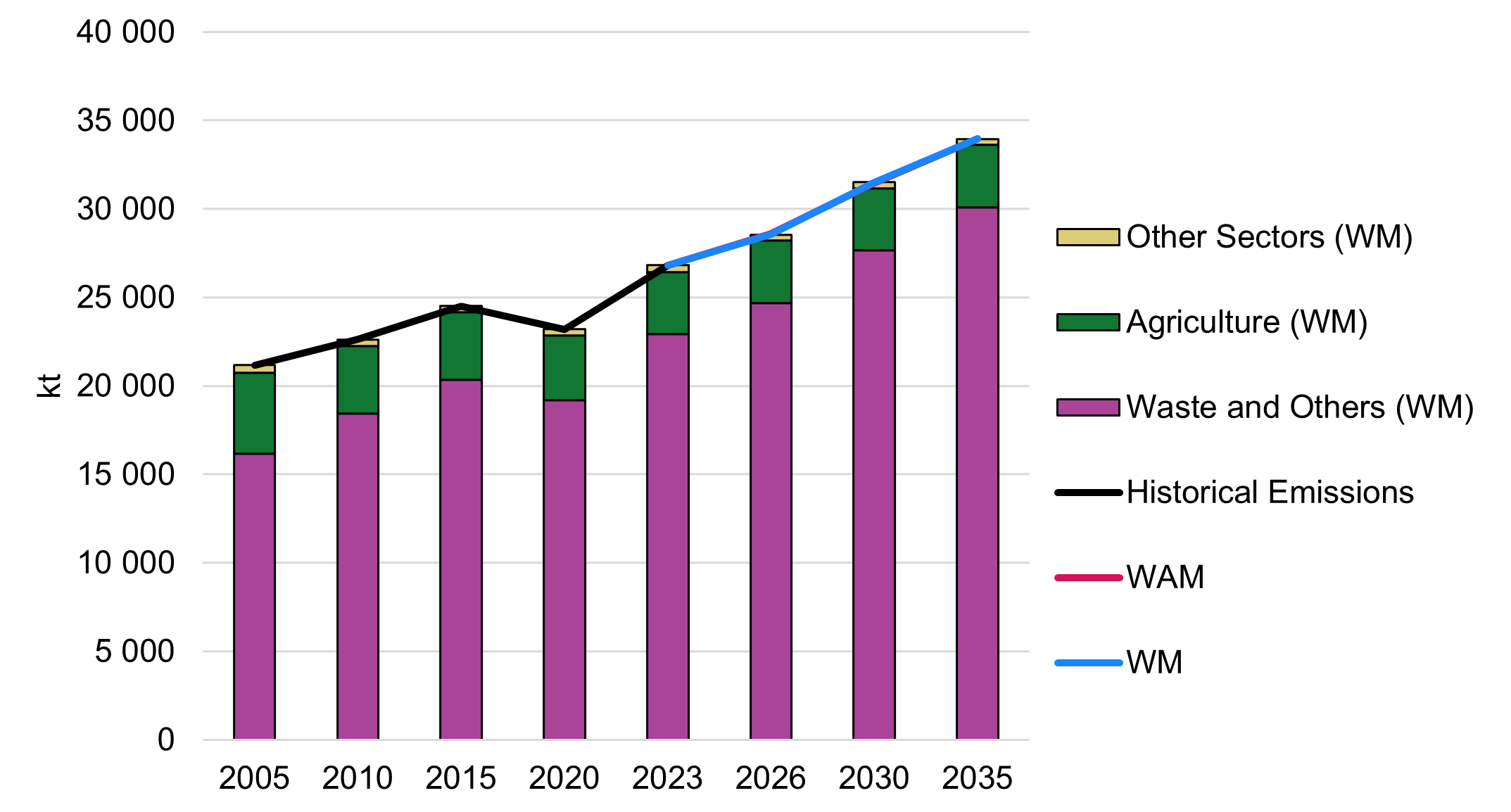

| Pollutant | 2010 Emissions Ceiling (kt) | 2020 Commitment (% below 2005) | 2020 Commitment Level (kt)Footnote * |

|---|---|---|---|

| Sulphur dioxide (SO2) | 1 450 | 55% | 943 |

| Nitrogen oxides (NOX) | 2 250 | 35% | 1 468 |

| Volatile organic compounds (VOCS) | 2 100 | 20% | 1 805 |

| Fine particulate matter, excluding emissions from open sources (PM2.5) | NA | 25% | 203 |

In addition to its Air Convention commitments, Canada also has commitments under the AQA, which focus on reducing emissions of SO₂, NOₓ, and VOCs to control transboundary air pollution.

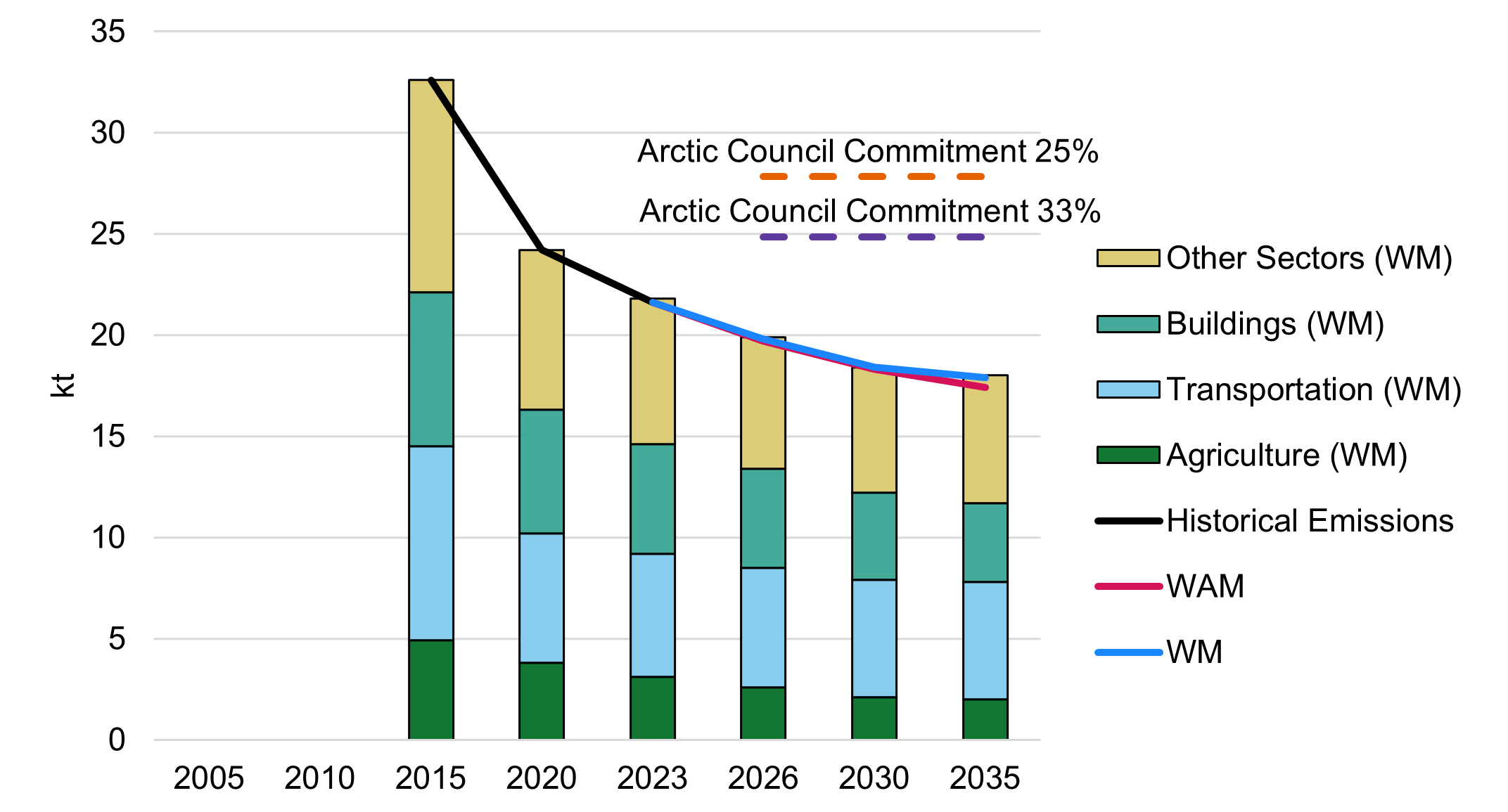

Black carbon is an air pollutant and a short-lived climate pollutant with significant warming potential and health impacts. Under the Arctic Council’s Framework for Action on Enhanced Black Carbon and Methane Emissions Reductions, Canada and other Arctic States agreed to an aspirational goal of reducing collective emissions of black carbon by 25% to 33% below 2013 levels by 2025.

Canada has met its emissions reduction commitments under the Gothenburg Protocol and the AQA, and has reduced its black carbon emissions in line with the Arctic Council’s collective black carbon goal. Section 3 discusses how Canada is expected to continue meeting, or even exceeding, its Gothenburg Protocol obligations through 2035.

1.4 Reporting obligations and methodological overview

ECCC plays a central role in fulfilling Canada’s climate reporting obligations under both domestic legislation and international agreements. These reporting activities promote transparency, accountability, and align with global best practices.

Canada’s emissions projections are developed in accordance with the Modalities, Procedures and Guidelines adopted by the UNFCCC. To ensure consistency with international reporting, Canada has adopted the UNFCCC naming convention for emissions scenarios. As of this report, the scenarios previously referred to as the “Reference Case” and “Additional Measures Scenario” in previous domestic reports are now called the WM and WAM scenarios, respectively. While the modelling approaches remain unchanged, this terminology shift improves comparability across reporting platforms.

ECCC develops GHG and air pollutant emissions projections using E3MC, a comprehensive modelling framework that integrates two core components: ENERGY 2020 and the North America Economic Model (NAEM). ENERGY 2020 simulates energy supply, demand, and pricing across sectors and regions while NAEM captures macroeconomic activity and its interaction with energy use. Together, these models enable a market-based analysis of energy and emissions, balancing supply and demand and reflecting policy, price, and technology dynamics. E3MC incorporates data from authoritative sources such as Statistics Canada, the Canada Energy Regulator (CER), Natural Resources Canada (NRCan), and ECCC’s National Inventory Report (NIR), and supports both forecasting and analysis. It produces detailed outputs on energy consumption, production, prices, and macroeconomic indicators including gross domestic product (GDP) and employment, ensuring consistency with international reporting standards and enabling robust scenario analysis. More information about E3MC is available in Annex 1.

Projections are updated annually to reflect the most recent historical data and current economic and energy market trends. These projections represent potential outcomes that may vary year to year depending on economic, social, and policy developments.

ECCC collaborates with other federal government departments, provinces, and territories to develop the data and assumptions used in emissions modelling. Through comprehensive consultations, most recently completed in August 2025, ECCC ensures that the projections reflect a wide range of policies and measures across all orders of government.

The current projections are based on data available as of November 2025, including the most recent historical data from Canada’s National Inventory Report 1990–2023: Greenhouse Gas Sources and Sinks in Canada 2025 (NIR2025). Projections extend from 2024 through 2035.

Since 2011, ECCC has published annual GHG emissions projections through various platforms including:

- federal climate plans and Progress Reports:

- Pan-Canadian Framework on Clean Growth and Climate Change (2015)

- Canada's Strengthened Climate Plan (2020)

- Canada’s 2030 Emissions Reduction Plan (2022)

- 2023 Progress Report on the 2030 Emissions Reduction Plan (2023)

- biennial submissions to the UNFCCC:

- Canada's Sixth National Report on Climate Change (2013)

- Canada's Second Biennial Report on Climate Change (2015)

- Canada's Seventh National Communication and Third Biennial Report on Climate Change (2017)

- Canada's Fourth Biennial Report on Climate Change (2019)

- Canada's Eight National Communication and Fifth Biennial Report (2022)

- Canada's First Biennial Transparency Report under the Paris Agreement (2024)

- standalone domestic reports:

- Canada's Emissions Trends (2011)

- Canada's Emissions Trends (2012)

- Canada's Emissions Trends (2014)

- Canada's 2016 Greenhouse Gas Emissions Reference Case (2016)

- Canada's Greenhouse Gas and Air Pollutant Emissions Projections (2018)

- Canada's Greenhouse Gas and Air Pollutant Emissions Projections (2020)

- Canada's Greenhouse Gas and Air Pollutant Emissions Projections (2023)

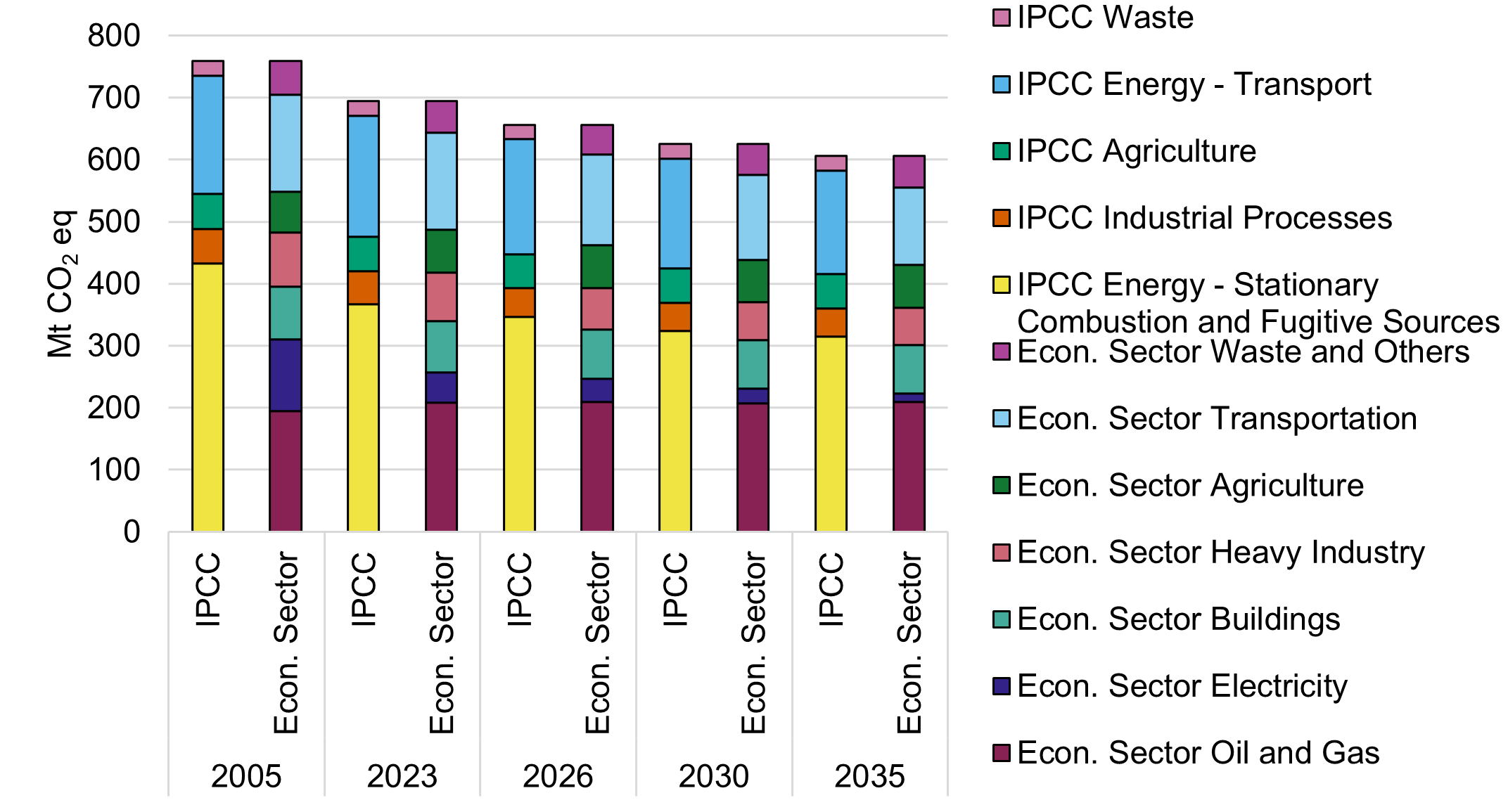

Canada’s emissions projections follow a consistent and transparent approach aligned with international reporting standards. Projections are presented by both sector and gas type, with and without the accounting contribution from the LULUCF sector and emissions reduction from NBCS and agriculture measures. For domestic policy analysis, emissions are classified by economic sector rather than by IPCC categories. This reclassification does not alter the total emissions reported under UNFCCC guidelines but provides a more practical framework for domestic analysis. Unless otherwise noted, the term “sector” in this report refers to these economic sectors. While most results are organized using this economic sector framework, Section 2.3 also presents projections by IPCC category and explains how these align with Canada’s classifications.

To support transparency and IPCC reporting requirements, all projections are presented relative to historical inventory data using both graphical and tabular formats. Historical data are shown for 1990, 2005, and 2023 (except for black carbon, available from 2013 onward). Projections are provided for 2026, 2030, and 2035. Some tables and figures also compare current projections with those from previous reports. Complete time series data are available through the Government of Canada’s open data portal, and interactive visualizations can be accessed via Canada’s Greenhouse Gas Emissions Projections website.

This report presents two primary GHG and air pollutant emissions scenarios, the WM and WAM scenarios. These scenarios provide insight into Canada’s expected emissions trajectory under current and anticipated climate policies. GHG emissions projections are presented in Section 2, while air pollutant projections appear in Section 3.

1.5 Continuous modelling excellence and continuous updates improvements

The Government of Canada possesses long-standing and comprehensive modelling capacity that supports the development of GHG emissions projections. These projections adhere to internationally recognized best practices and rigorous methodologies, aligned with reporting requirements under the UNFCCC. As mentioned in Section 1.4, ECCC employs E3MC, an integrated framework combining ENERGY 2020 and NAEM to simulate energy supply, demand, pricing, and macroeconomic interactions. This approach ensures consistency with international reporting standards and enables robust scenario analysis.

The modelling process draws on authoritative data sources, including Statistics Canada, the CER, NRCan, and ECCC’s NIR, and is informed by expert input on key drivers such as economic growth and energy trends. Importantly, the ENERGY 2020 model has been peer-reviewed by leading external experts in economic modelling and the model inputs are vetted with stakeholders to ensure transparency and credibility. Canada’s projections have been published regularly since 2011 in federal climate plans, biennial submissions to the UNFCCC, and standalone domestic reports, demonstrating Canada’s proven and internationally aligned modelling capability.

Building on this strong foundation, ECCC is committed to continuous improvement of its modelling framework to enhance transparency, stakeholder engagement, and methodological robustness.

In the 2030 Emissions Reduction Plan (released in 2022), ECCC committed to improving transparency in modelling and reporting. ECCC undertook a two-phase consultation process between 2022 and 2023. Phase 1 gathered input from prominent Canadian modelling experts on objectives, scope, and milestones for a formal consultation process, which led to the development of an Independent Modelling Review Action Plan. Phase 2 expanded consultation on the proposed plan. The final version of the action plan was released in Canada's 2023 Greenhouse Gas and Air Pollutant Emissions Projections Report. A progress update was later included in Canada’s First Biennial Transparency Report under the Paris Agreement, submitted to the UNFCCC in 2024. The projections presented in this report continue to address items identified in this action plan.

Key technical advancements in 2025 include modernizing the ENERGY 2020 model by transitioning it from the legacy PROMULA programming language to the modern, high-performance Julia language. Validation of the updated model confirmed consistency with previous outputs. This transition improves model runtime and maintainability and supports integration with advanced development tools including AI-assisted coding and version control tools. Model documentation will be updated to reflect the changes associated with the transition to the Julia programming language and will be made publicly available in 2026.

ECCC has also developed a methodology to isolate the contributions to emissions reductions of certain key individual climate policies, enhancing transparency and supporting strategic decision-making. Additionally, scenario analyses have been expanded to include trade uncertainty and tariff impacts, providing a broader understanding of potential emissions trajectories.

Additional details regarding modelling assumptions, provincial-level data for emissions from the LULUCF sector, and sensitivity scenarios have been added to the open data portal. Finally, a Multi-Model Comparison Forum was set up under the umbrella of the Energy Modelling Hub. Over 2024 and 2025, the Forum established foundational workflows that are poised to enhance collaboration and comparisons across Canadian models. In December 2025, the Annual Forum brought together Canada’s leading energy modellers, policymakers, and system experts to foster collaboration and develop actionable strategies for the future.

Planned future enhancements focus on optimizing model runtimes, enabling cross-platform functionality, leveraging cloud computing efficiencies, and exploring parallel computing. These efforts aim to support more efficient scenario development and policy analysis.

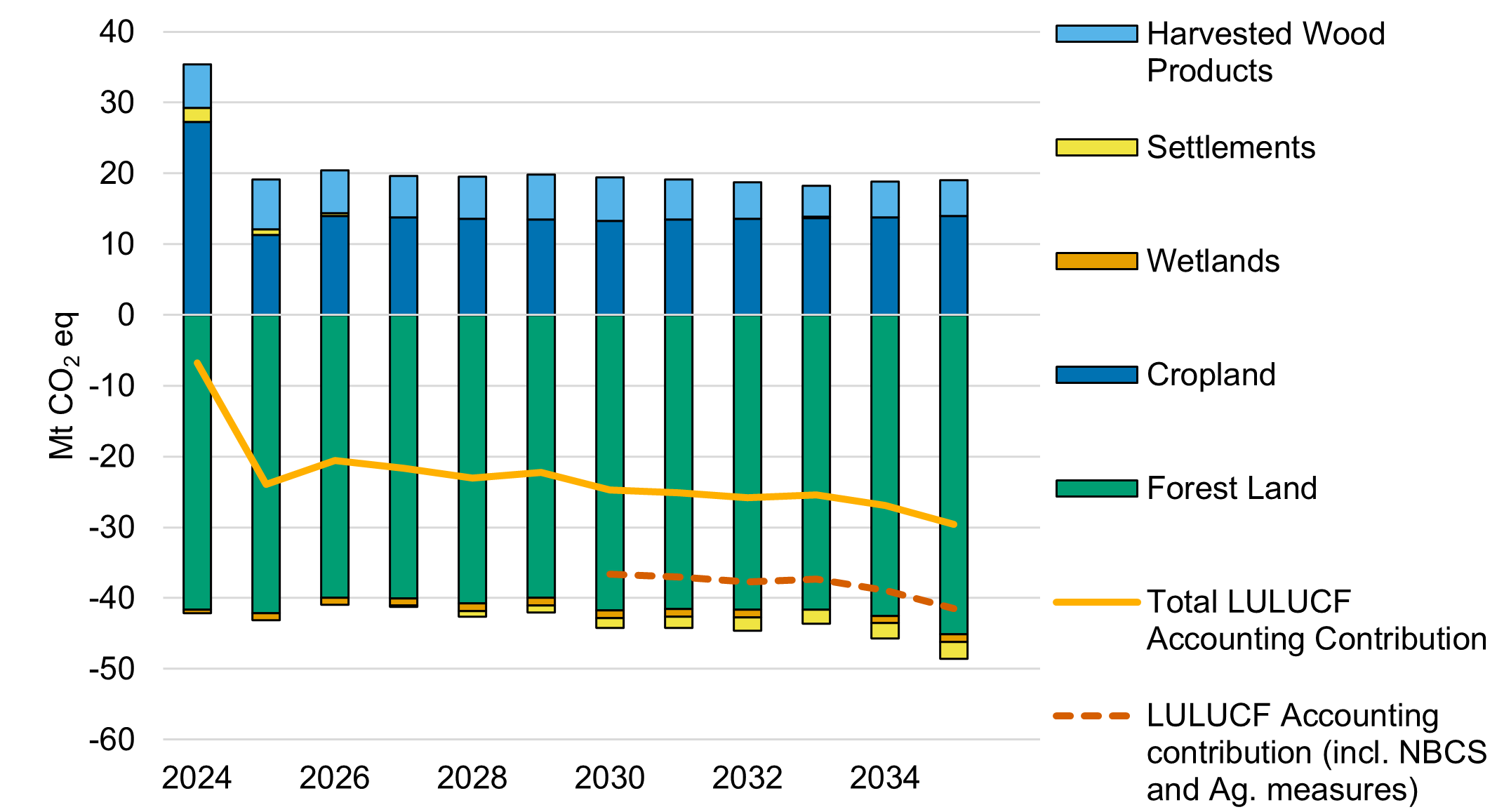

In the LULUCF sector, ECCC continues to improve data and methods based on peer-reviewed science and international reporting protocols. Planned improvements for forest land and harvested wood products (HWP) are detailed in the NIR and related improvement plans.

In 2023 and 2024, Canada conducted a review of its GHG accounting approach for the LULUCF sector, with specific focus on Forest Land remaining Forest Land (FLFL) and associated HWP accounting. As part of this process, NRCan and ECCC sought input from experts and stakeholders to inform Canada’s decision on its LULUCF accounting approach. Based on internal analysis and on feedback received from stakeholders and experts, the Government of Canada made the decision to maintain the current approach that applies reference level accounting to FLFL and the associated HWP and net-net accounting to all other land categories, while continuing to monitor developments related to LULUCF accounting.

Methodological revisions since the previous report include updates to historical data, policy coverage, and modelling approaches to reflect the latest scientific understanding and policy developments. These updates ensure that projections remain accurate and relevant for informing Canada’s climate commitments and policy decisions. Additional information about improvements to the data and methodology can be found in Section A1.9.

1.6 Scenario definitions

1.6.1 With measures scenario

The WM scenario includes federal, provincial, and territorial policies and measures that were in place as of November 2025 and assume no further government action. This scenario was previously referred to as “Reference Case” in previously published domestic reports. Policies and measures in the WM scenario must:

- reflect current legislative, regulatory, and financial conditions

- have sufficient quantifiable information for its impact to be estimated

- be expected to produce meaningful and material reductions by at least 100 kilotonnes (kt) of carbon dioxide equivalents (CO2 eq) annually

Unless otherwise specified, this scenario also includes the accounting contribution from the LULUCF sector. A full list of policies and measures included in the WM scenario is provided in Table A10 and Table A11. Changes to the policy coverage of the WM scenario since the release of Canada’s 2023 Emissions Projections Report (EPR2023) are discussed in Section A1.9.4.

1.6.2 With additional measures scenario

The WAM scenario builds on the WM scenario by including all federal, provincial, and territorial policies and measures that have been announced but not yet fully implemented. It also accounts for the effects of NBCS and agriculture measures. However, it excludes measures still in development or planning stages where insufficient information prevents accurate modelling. This scenario was previously referred to as “Additional Measures” in previously published domestic reports.

The Enhanced Oil and Gas Methane Regulations and the Landfill Methane Regulations were finalized on December 16, 2025. These regulations were completed too late for inclusion in the WM scenario; however, they were included in the WAM scenario and will be incorporated in WM scenario in future updates.

The list of policies and measures included in the WAM scenario, which includes a description of their underlying assumptions, can be found in Table A12. Changes to the policies included in the WAM scenario since the release of EPR2023 are discussed in Section A1.9.4.

As new measures are developed and implemented, their emissions reductions will be assessed and included in future projections.

From 2017 to 2024, Canada included emissions reductions from the Western Climate Initiative (WCI) in its WAM scenario and counted them toward its 2030 target in both domestic and international reports. The WCI is a regional cap-and-trade program that uses market-based mechanisms to reduce GHG emissions. Currently, Québec and California operate linked cap-and-trade systems under the WCI, with Washington state considering participation. Since 2013, these jurisdictions have exchanged allowances and offsets, known as WCI credits, as interchangeable compliance units.

Under Article 6 of the Paris Agreement, countries can trade emissions reductions as internationally transferred mitigation outcomes (ITMOs) if both parties are signatories to the Agreement and have established a bilateral agreement to authorize the exchange. However, the recent United States of America’s (US) withdrawal from the Paris Agreement means it can no longer authorize ITMO trades, preventing Canada from establishing a bilateral agreement with the US to count WCI credit flows as ITMOs.

Going forward, Canada will continue working with Québec to monitor and track WCI credit flows but will no longer formally count them toward its NDC target. Instead, Canada will highlight these net flows in public reports, including this report and the Second Biennial Transparency Report in 2026, to acknowledge their role in a credible and well-documented emissions trading system.

1.6.3 Alternative scenarios

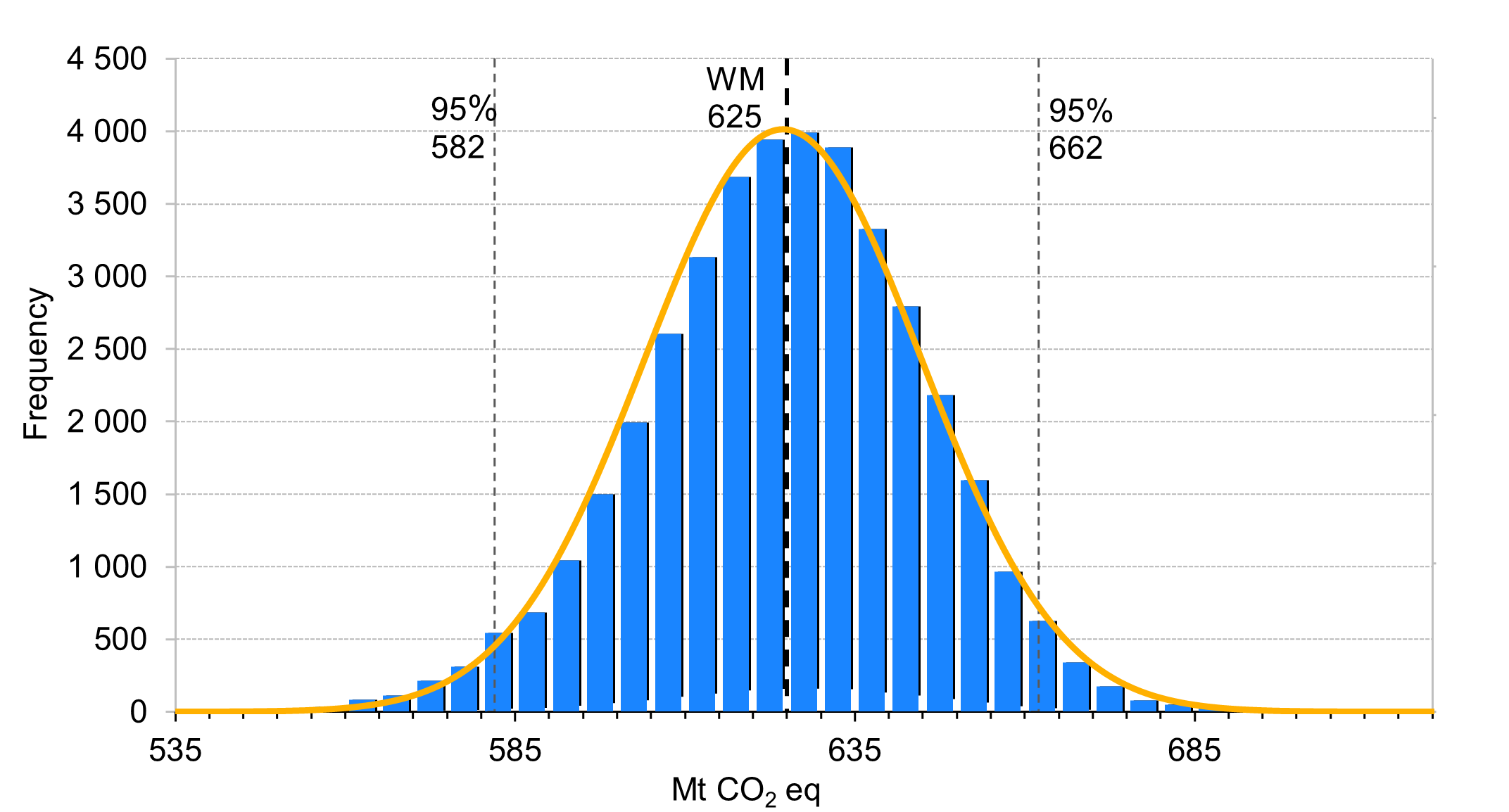

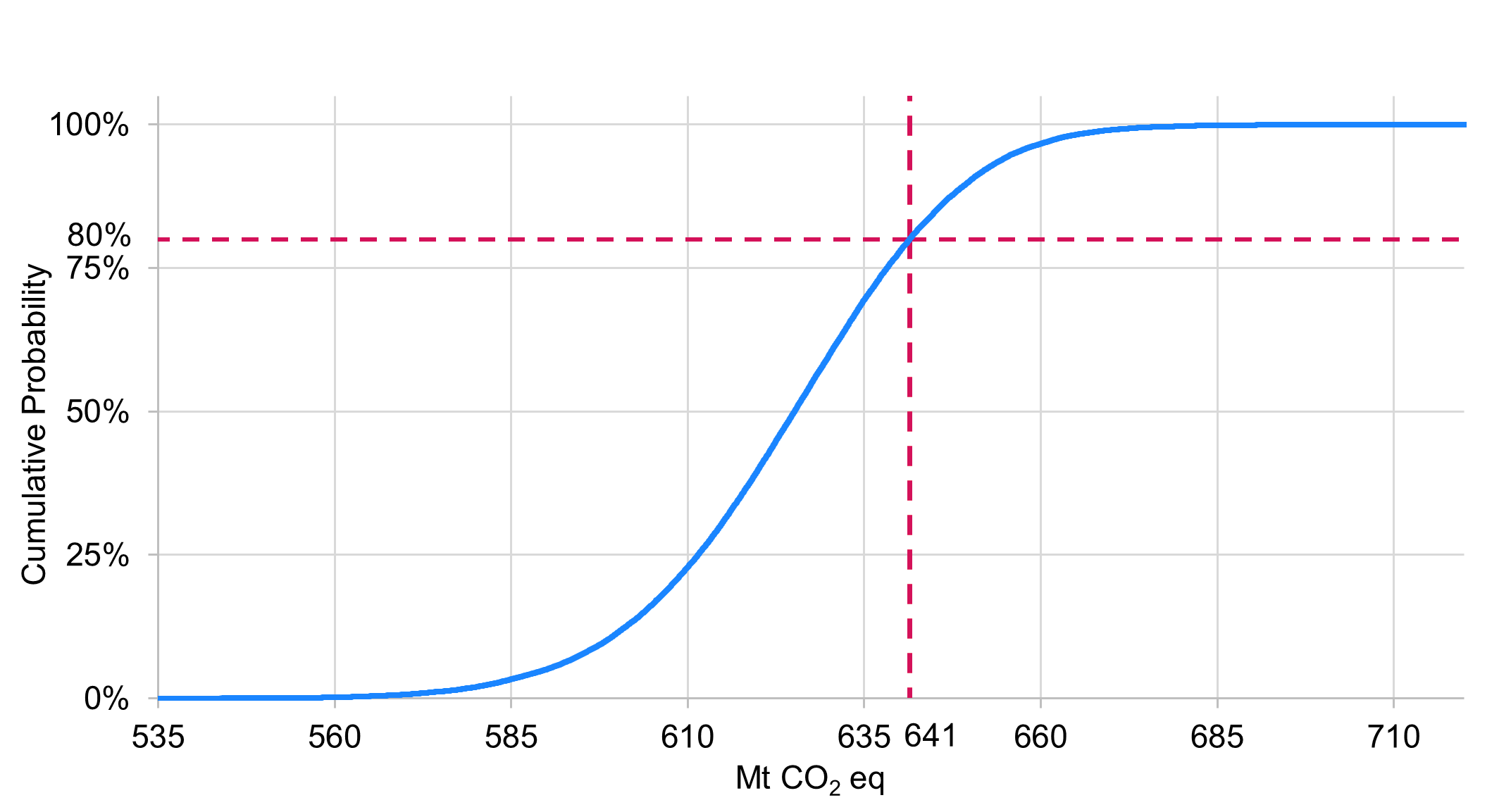

All projections are subject to uncertainty. The WM and WAM scenarios represent plausible outcomes based on current knowledge, but future developments, such as changes in economic growth, energy prices, or technology, could significantly alter emissions trajectories.

Section 2.5 presents alternative scenarios to explore the sensitivity of projections to these key drivers. It also includes an analysis of the uncertainty associated with the WM scenario.

These scenarios do not consider the impact of the LULUCF accounting contribution, NBCS, and agriculture measures.

2 Greenhouse gas emissions projections

2.1 Summary of historical and projected emissions

This section provides a high-level overview of Canada’s GHG emissions trajectory, combining historical data with projections. It highlights key trends, summarizes expected outcomes under current and additional policy measures, and explains the drivers behind projected changes. Together, these elements provide essential context for understanding Canada’s progress toward its climate targets. Historical emissions data from 2005 to 2023 are sourced from NIR2025, while projections from 2024 to 2035 are developed using ECCC’s modelling framework.

Please note that the tables starting with ‘A’ referenced in Sections 2 and 3 are exclusively available on the Government of Canada’s open data portal. Further information on revisions (historical data, policies, and methodological), can be found in sections A1.9.3 to A1.9.5, in Annex 1. A complete list of policies included in the modelling can be found in Table A10 through Table A12.

2.1.1 Historical trends

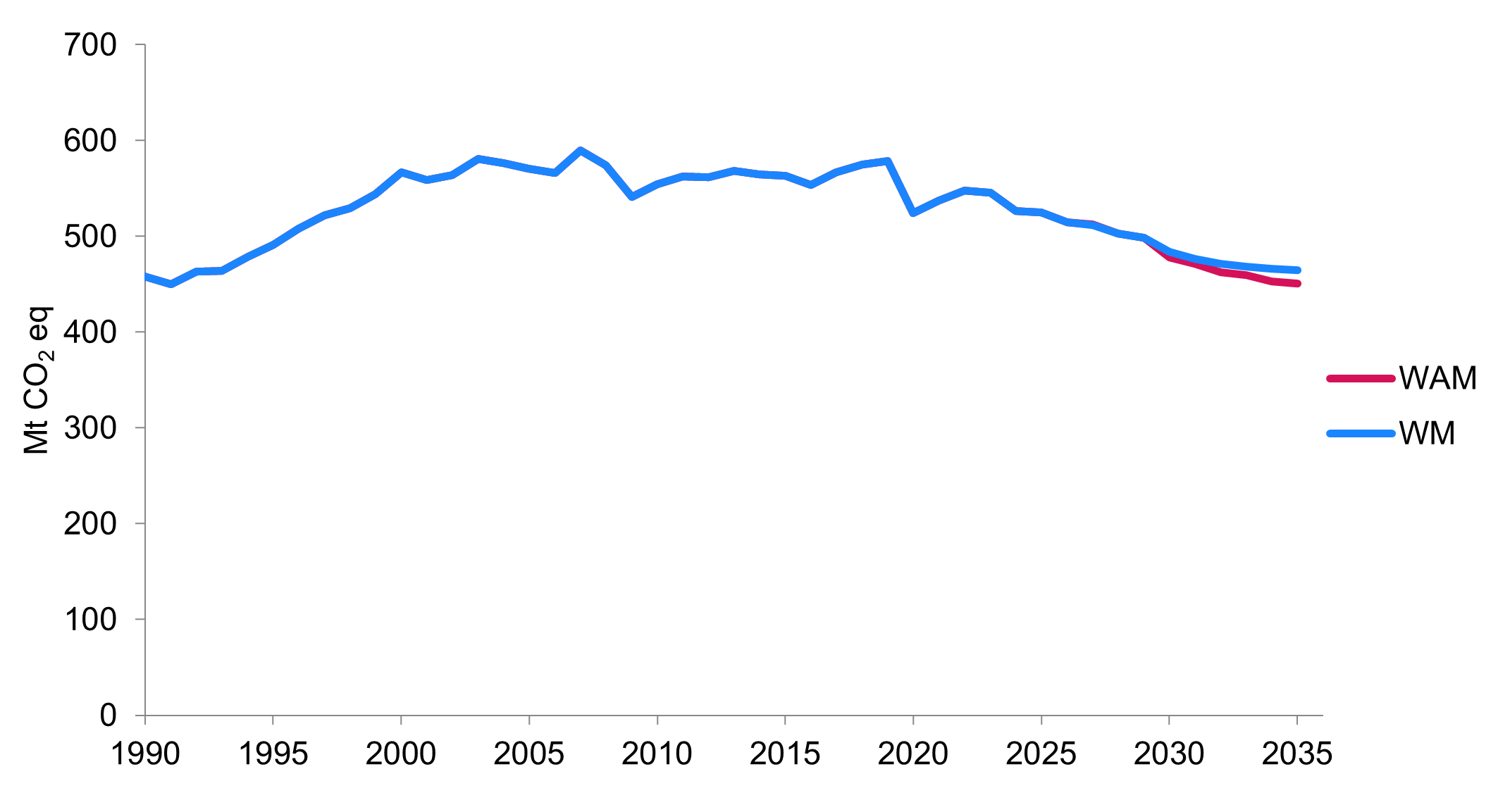

In 2023, Canada’s GHG emissions were 694 megatonnes (Mt), a decrease of 65 Mt (8.5%) from 2005 (excluding the LULUCF sector), and a decrease of 6.0 Mt (0.9%) from 2022.

Emissions from Electricity decreased by 67 Mt (58%), between 2005 and 2023, driven by the phase out of coal-fired electricity generation. Oil and Gas emissions increased by 13 Mt (7%). Oil and Gas emissions peaked in 2014 at 228 Mt and have since decreased by 20 Mt (9%) to 208 Mt in 2023. This is consistent with measured decreases of fugitive methane sources in recent years.

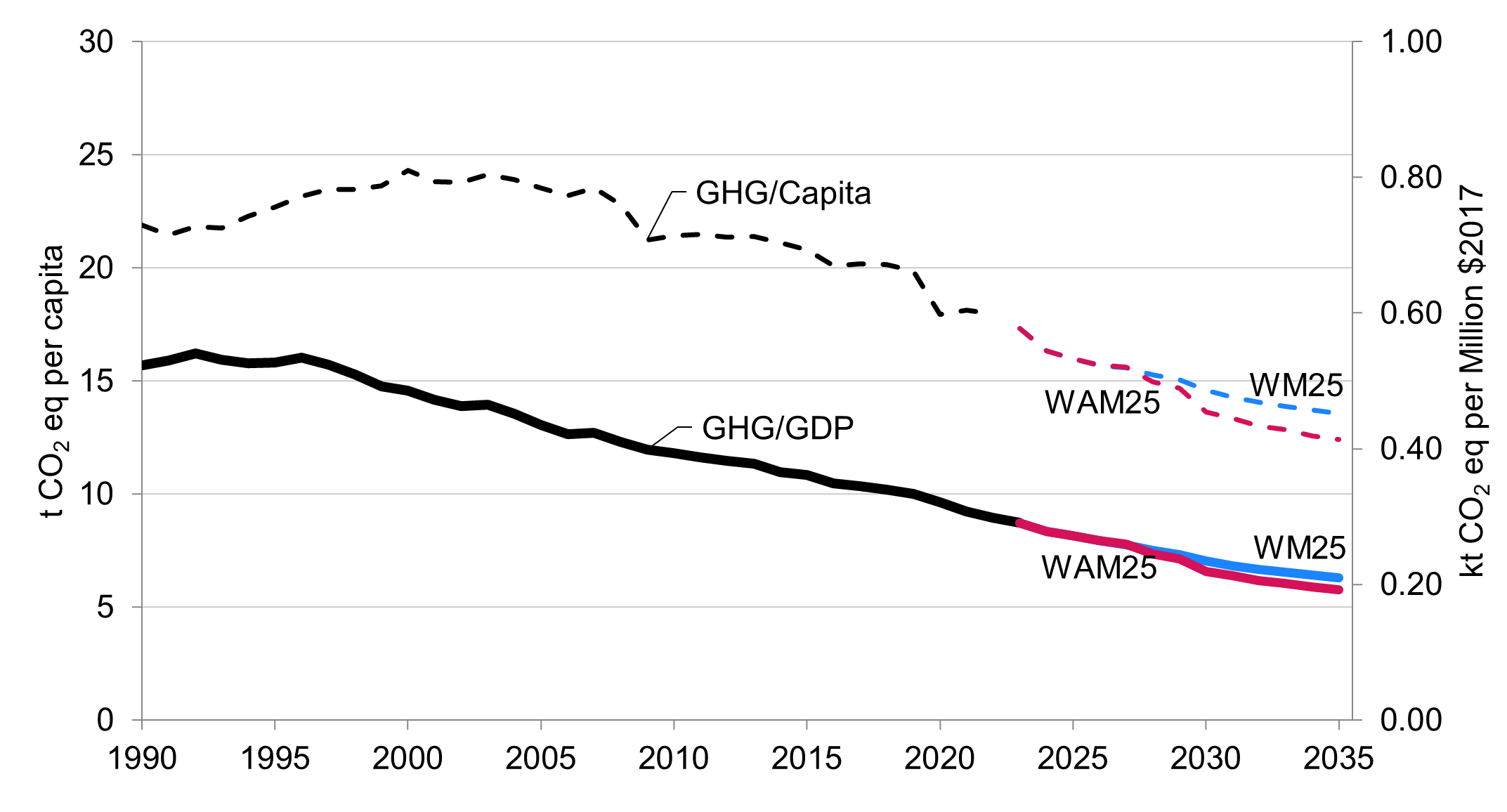

The emissions intensity, GHG per GDP, for the entire Canadian economy has continued to decline. In 2023 it had declined by 44% since 1990 and by 33% since 2005.

As with every NIR edition, improvements have been implemented in NIR2025 resulting in revisions to previously published data. Overall, NIR2025 incorporates downward revisions of 2.8 Mt in 2005 and 7.9 Mt in 2022, relative to the previously published inventory in 2024.

2.1.2 Projections summary

Building on the historical trends outlined above, this section summarizes projected emissions under the WM and WAM scenarios.

Under the WM scenario, GHG emissions are projected to decline to 625 Mt in 2030. With the LULUCF sector accounting contributions included, 2030 emissions are projected to be 600 Mt in the WM scenario. Post-2030, emissions projected in the WM scenario continue to decline, reaching 577 Mt in 2035 (including the LULUCF accounting contribution).

Under the WAM scenario, emissions in 2030 decline to 546 Mt, including LULUCF, NBCS, and agriculture measures. Post-2030, emissions projected in the WAM scenario (including LULUCF, NBCS, and agriculture measures) continue to decline, reaching 513 Mt in 2035.

Table 2 and Figure 1 illustrate projected trends in GHG emissions by economic sector, while Table 16 presents the same projections organized by IPCC categories. Figure 2 compares emissions projections under the WM and WAM scenarios, alongside those published in EPR2023. For further detail, Section 2.2 provides sector-level projections, and Section 2.3 offers a comparative analysis of emissions categorized by both IPCC and Canadian economic sector frameworks.

| Sector | 1990 | 2005 | 2023 | 2026Footnote a | 2030Footnote a | 2035Footnote a | 2026Footnote b | 2030Footnote b | 2035Footnote b |

|---|---|---|---|---|---|---|---|---|---|

| Oil and Gas | 117 | 194 | 208 | 209 | 207 | 209 | 208 | 175 | 177 |

| Electricity | 94 | 116 | 49 | 38 | 23 | 14 | 39 | 26 | 14 |

| Transportation | 118 | 156 | 157 | 146 | 137 | 124 | 147 | 138 | 125 |

| Heavy Industry | 97 | 88 | 78 | 67 | 61 | 60 | 67 | 59 | 57 |

| Buildings | 72 | 85 | 83 | 80 | 78 | 78 | 79 | 76 | 69 |

| AgricultureFootnote * | 51 | 66 | 69 | 69 | 69 | 69 | 69 | 68 | 69 |

| Waste and Others | 57 | 54 | 50 | 48 | 50 | 51 | 48 | 41 | 42 |

| Subtotal | 606 | 759 | 694 | 656 | 625 | 606 | 656 | 583 | 554 |

| LULUCF Accounting Contribution | 27 | 0 | -39 | -21 | -25 | -30 | -21 | -25 | -30 |

| NBCS and Agriculture Measures | NA | NA | NA | NA | NA | NA | NA | -12 | -12 |

| Total | 633 | 759 | 655 | 635 | 600 | 577 | 636 | 546 | 513 |

| WCI CreditsFootnote ** | NA | NA | -10 | NA | NA | NA | -6 | -4 | 0 |

Note: Totals may not match due to rounding. Historical data up to 2023 are sourced from NIR2025. Data from 2024 to 2035 are modelled projections developed using ECCC’s analytical framework. Access more data on the open data portal.

Note: Numbers may not sum to the total due to rounding. Historical emissions data come from NIR2025. Access more data on the open data portal.

Long description

| Year | Agriculture (WM) | Buildings (WM) | Electricity (WM) | Heavy Industry (WM) | Oil and Gas (WM) | Transportation (WM) | Waste and Others (WM) | Historical Emissions | WM | WAM |

|---|---|---|---|---|---|---|---|---|---|---|

| 2005 | 66 | 85 | 116 | 88 | 194 | 156 | 54 | 759 | - | - |

| 2006 | 64 | 79 | 111 | 88 | 202 | 157 | 53 | 755 | - | - |

| 2007 | 64 | 85 | 118 | 86 | 207 | 162 | 53 | 774 | - | - |

| 2008 | 64 | 85 | 108 | 84 | 203 | 163 | 51 | 758 | - | - |

| 2009 | 61 | 84 | 93 | 71 | 198 | 161 | 46 | 714 | - | - |

| 2010 | 61 | 81 | 95 | 75 | 203 | 165 | 48 | 728 | - | - |

| 2011 | 61 | 86 | 86 | 81 | 210 | 164 | 50 | 738 | - | - |

| 2012 | 63 | 84 | 82 | 81 | 216 | 164 | 50 | 741 | - | - |

| 2013 | 65 | 85 | 80 | 80 | 223 | 167 | 50 | 750 | - | - |

| 2014 | 64 | 86 | 75 | 82 | 228 | 164 | 48 | 747 | - | - |

| 2015 | 66 | 85 | 74 | 80 | 226 | 162 | 49 | 742 | - | - |

| 2016 | 67 | 86 | 75 | 77 | 208 | 162 | 51 | 725 | - | - |

| 2017 | 67 | 88 | 73 | 78 | 216 | 165 | 51 | 738 | - | - |

| 2018 | 69 | 92 | 63 | 80 | 223 | 169 | 52 | 747 | - | - |

| 2019 | 69 | 94 | 62 | 79 | 222 | 169 | 52 | 747 | - | - |

| 2020 | 70 | 88 | 54 | 75 | 204 | 142 | 48 | 682 | - | - |

| 2021 | 69 | 85 | 52 | 78 | 211 | 149 | 49 | 694 | - | - |

| 2022 | 70 | 88 | 49 | 78 | 209 | 155 | 50 | 700 | - | - |

| 2023 | 69 | 83 | 49 | 78 | 208 | 157 | 50 | 694 | 694 | 694 |

| 2024 | 69 | 77 | 40 | 75 | 211 | 153 | 49 | - | 673 | 674 |

| 2025 | 68 | 81 | 41 | 70 | 207 | 150 | 48 | - | 666 | 666 |

| 2026 | 69 | 80 | 38 | 67 | 209 | 146 | 48 | - | 656 | 656 |

| 2027 | 69 | 79 | 38 | 67 | 209 | 144 | 48 | - | 654 | 655 |

| 2028 | 69 | 78 | 34 | 66 | 207 | 142 | 49 | - | 645 | 632 |

| 2029 | 69 | 78 | 30 | 66 | 208 | 139 | 49 | - | 640 | 624 |

| 2030 | 69 | 78 | 23 | 61 | 207 | 137 | 50 | - | 625 | 583 |

| 2031 | 69 | 78 | 20 | 62 | 207 | 132 | 50 | - | 618 | 576 |

| 2032 | 69 | 79 | 17 | 62 | 206 | 130 | 50 | - | 612 | 567 |

| 2033 | 69 | 78 | 17 | 61 | 207 | 127 | 51 | - | 609 | 564 |

| 2034 | 69 | 78 | 13 | 60 | 209 | 127 | 51 | - | 607 | 557 |

| 2035 | 69 | 78 | 14 | 60 | 209 | 124 | 51 | - | 606 | 554 |

Note: *Historical emissions include data from NIR2023 and NIR2025, and also include LULUCF accounting contribution. Access more data on the open data portal.

- WM25: Current With Measures scenario.

- WAM25: Current With Additional Measures scenario.

- WM23: With Measures scenario published in EPR2023.

- WAM23: With Additional Measures scenario published in EPR2023 in 2023.

Long description

| Year | 2023 NIR* | WM23 | WAM23 (incl. NBCS + Ag. Measures) | 2025 NIR* | 2025 WM | 2025 WAM | 2025 WAM (incl. NBCS/Ag Measures) |

|---|---|---|---|---|---|---|---|

| 2005 | 732 | - | - | 759 | - | - | - |

| 2006 | 722 | - | - | 752 | - | - | - |

| 2007 | 751 | - | - | 778 | - | - | - |

| 2008 | 733 | - | - | 760 | - | - | - |

| 2009 | 675 | - | - | 700 | - | - | - |

| 2010 | 712 | - | - | 738 | - | - | - |

| 2011 | 727 | - | - | 755 | - | - | - |

| 2012 | 719 | - | - | 742 | - | - | - |

| 2013 | 719 | - | - | 747 | - | - | - |

| 2014 | 692 | - | - | 721 | - | - | - |

| 2015 | 725 | - | - | 746 | - | - | - |

| 2016 | 695 | - | - | 715 | - | - | - |

| 2017 | 693 | - | - | 719 | - | - | - |

| 2018 | 707 | - | - | 730 | - | - | - |

| 2019 | 697 | - | - | 722 | - | - | - |

| 2020 | 629 | - | - | 660 | - | - | - |

| 2021 | 637 | 637 | 637 | 665 | - | - | - |

| 2022 | - | 688 | 686 | 709 | - | - | - |

| 2023 | - | 637 | 632 | 655 | 655 | 655 | - |

| 2024 | - | 630 | 616 | - | 667 | 667 | - |

| 2025 | - | 624 | 602 | - | 642 | 642 | - |

| 2026 | - | 615 | 577 | - | 635 | 636 | - |

| 2027 | - | 608 | 554 | - | 632 | 633 | - |

| 2028 | - | 590 | 528 | - | 621 | 609 | - |

| 2029 | - | 577 | 506 | - | 618 | 602 | - |

| 2030 | - | 560 | 468 | - | 600 | 558 | 546 |

| 2031 | - | 556 | 457 | - | 592 | 551 | 539 |

| 2032 | - | 550 | 448 | - | 586 | 541 | 529 |

| 2033 | - | 548 | 442 | - | 584 | 538 | 527 |

| 2034 | - | 544 | 435 | - | 580 | 530 | 518 |

| 2035 | - | 541 | 423 | - | 577 | 525 | 513 |

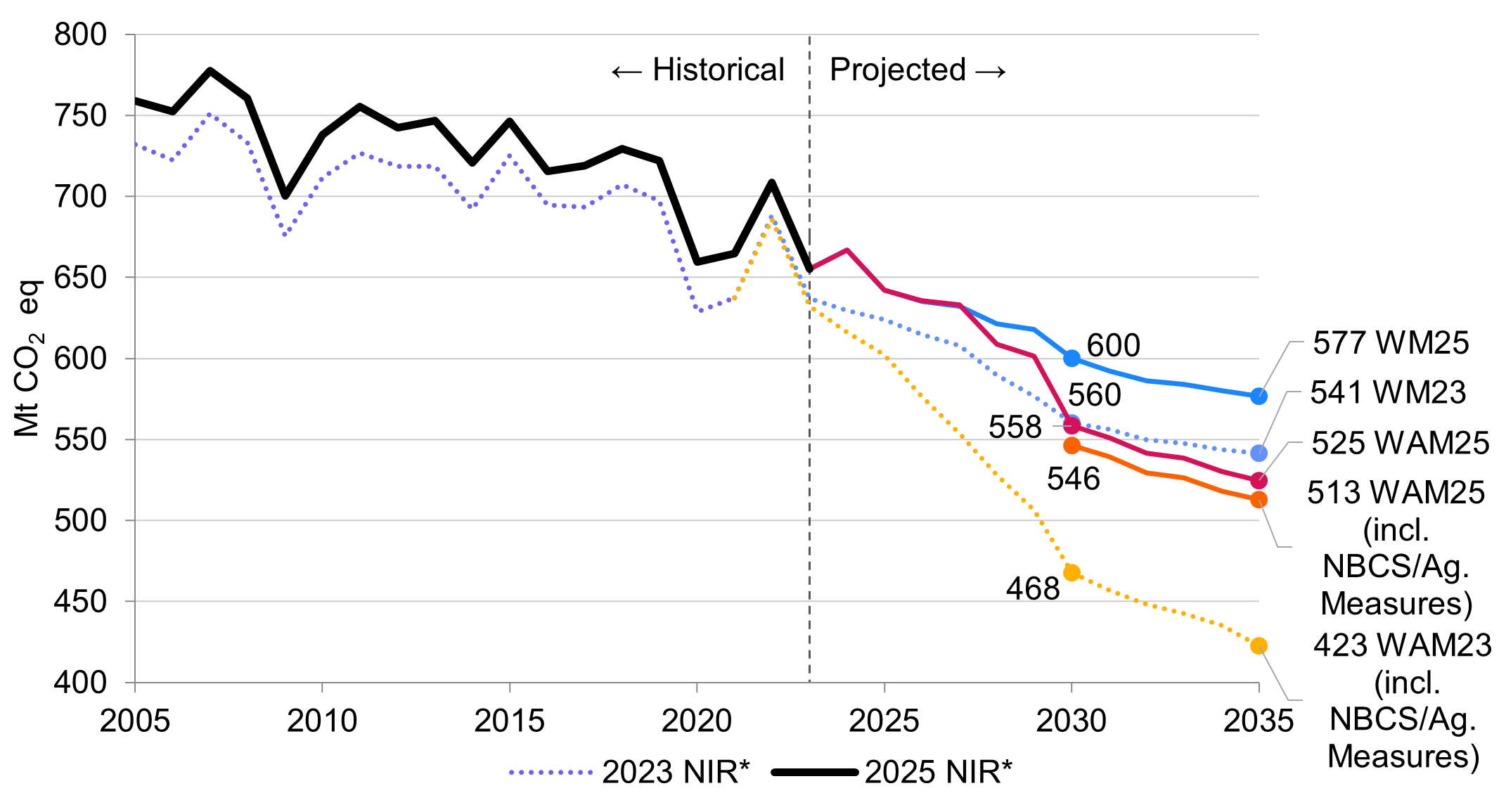

2.1.3 Comparison to previous projections

To assess progress and methodological consistency, this section compares the current projections to those published in EPR2023.

In 2030, Canada's GHG emissions under the WM scenario (including the LULUCF accounting contribution) are projected to be 600 Mt, or 40 Mt above the WM scenario of 560 Mt presented in EPR2023. In the WAM scenario, emissions (including the LULUCF accounting contribution, NBCS, and agriculture measures) are projected to be 546 Mt in 2030, 79 Mt higher than the WAM projections included in EPR2023. These increases are partly offset by declines in emissions from the heavy industry sector, driven by tariff impacts on production.

The projected emissions have changed along with historical emissions because of improvements and refinements to data sources and methodologies, as discussed in more detail in Section A1.9.3. These revisions extend back to 2005 (Figure 2). For example, in 2021, the last year available for NIR2023, total emissions were revised upward by 24 Mt (from 670 Mt to 694 Mt), primarily due to a 22 Mt increase in the Oil and Gas sector, while other sectors only saw increases or decreases of 2 Mt or less. These changes largely reflect the adoption of updated global warming potential (GWP) factors and also significant revisions to estimates of methane emissions that incorporate atmospheric measurement data, starting with NIR2024. Section A1.9.3 provides a detailed description of these historical changes, while Table A10-2 of the 2023 to 2025 editions of the NIR shows sector-by-sector historical GHG emissions estimates for individual years.

Changes to projected emissions also reflect updates to policy coverage and modelling assumptions. Section A1.9.4 lists policies added or removed since EPR2023. Notably, this year’s projections incorporate the removal of the federal fuel charge and of the oil and gas emissions cap. In the Transportation Sector, two key adjustments stand out. First, Canada’s Electric Vehicle Availability Standard (EVAS) was incorporated into the WM case in the BTR1 projections, whereas in EPR2023 full adoption by 2035 was still treated as a WAM policy. Second, updated data shows that previous assumptions about a post-COVID rebound in demand were overstated.

In the agriculture sector, the WAM scenario no longer includes the assumption of meeting the fertilizer emissions target, a voluntary federal target to reduce emissions by 30% below 2020 levels by 2030. The projected GHG impact of existing programs targeting nitrogen management is now included in the WM scenario.

Projected LULUCF accounting contribution declined from 32 Mt in EPR2023 to 25 Mt in EPR2025 due to revisions to projected harvest rates from provinces and territories.

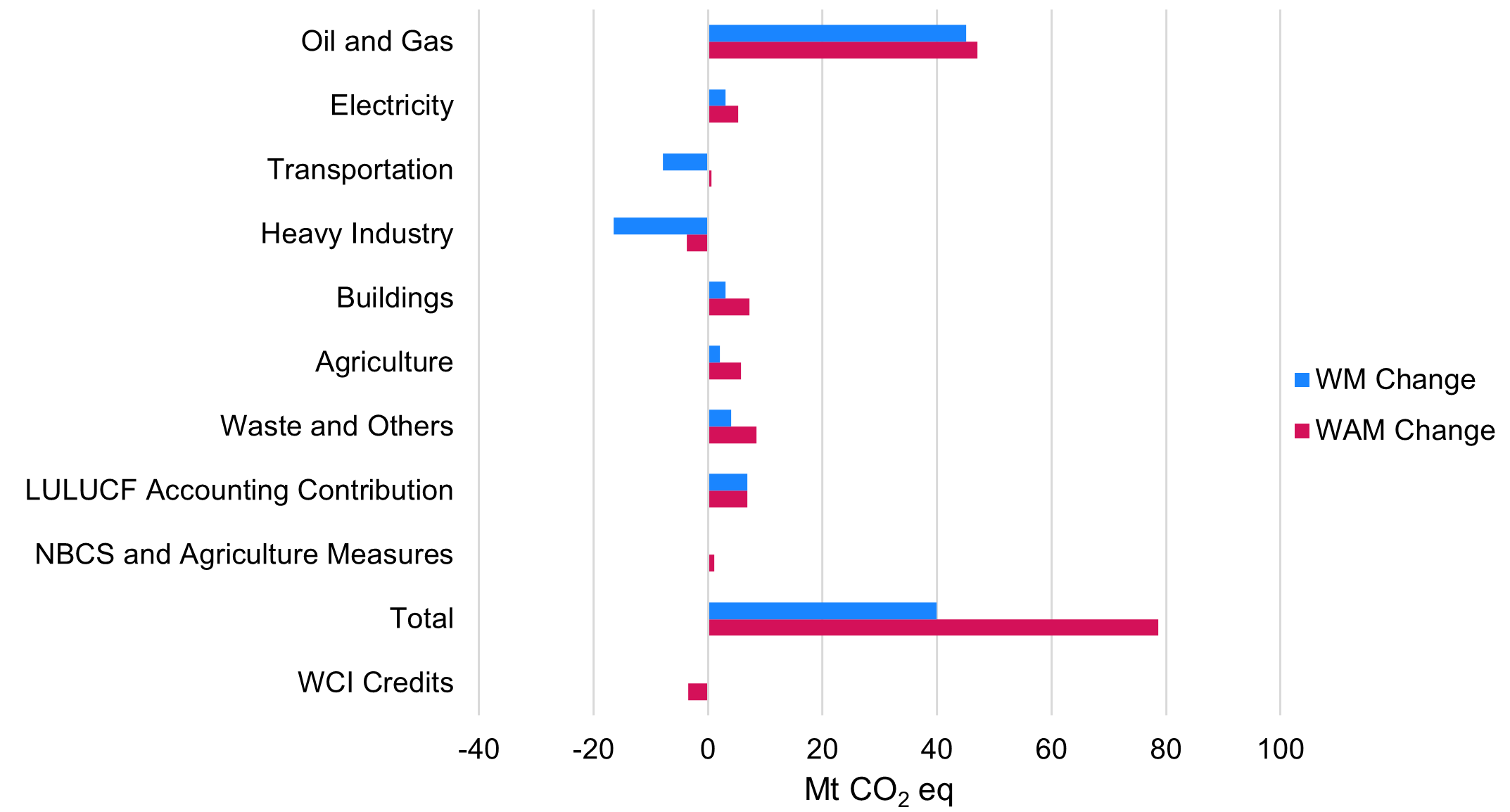

Table 3 presents changes at the economic sector level between the WM and WAM scenarios. Figure 3 illustrates the projected emissions reductions of each sector in 2030.

Oil and Gas

| Sectors | WM – EPR2023 | WM – EPR2025 | Change in WM Scenario (2023 vs 2025) | WAM – EPR2023 | WAM – EPR2025 | Change in WAM Scenario (2023 vs 2025) |

|---|---|---|---|---|---|---|

| Oil and gas | 162 | 207 | 45 | 128 | 175 | 47 |

| Electricity | 20 | 23 | 3 | 20 | 26 | 5 |

| Transportation | 144 | 137 | -8 | 137 | 138 | 1 |

| Heavy Industry | 77 | 61 | -16 | 63 | 59 | -4 |

| Buildings | 75 | 78 | 3 | 69 | 76 | 7 |

| Agriculture* | 67 | 69 | 2 | 63 | 68 | 6 |

| Waste and Others | 46 | 50 | 4 | 32 | 41 | 8 |

| LULUCF Accounting Contribution | -32 | -25 | 7 | -32 | -25 | 7 |

| NBCS and Agriculture Measures | NA | NA | NA | -13 | -12 | 1 |

| Total | 560 | 600 | 40 | 467 | 546 | 79 |

| WCI Credits** | NA | NA | NA | -1 | -4 | -4 |

Note: Numbers may not sum to the total due to rounding. Access more data on the open data portal.

* Additional emissions reductions in the WAM scenario occurring on agricultural lands are represented in the NBCS and Agriculture Measures row.

** As a result of the United States’ withdrawal from the Paris Agreement the United States is unable to participate in cooperative approaches under Article 6 of the Paris Agreement. Therefore, the net flow of WCI allowances and offset credits (imported from California into Québec) could not be considered as potential ITMOs under Article 6 of the Paris Agreement. Consequently, these net flows are excluded from the totals presented in this table. Nonetheless, Canada continues to monitor and document WCI credit flows in recognition of their contribution to a credible, transparent, and well-functioning emissions trading system.

Note: As a result of the United States’ withdrawal from the Paris Agreement, the net flow of WCI allowances and offset credits (imported from California into Québec) cannot be reported by Canada as ITMOs under Article 6 of the Paris Agreement. Consequently, these flows are excluded from the totals in the current WAM projections shown in this figure, but they were included in previous projections, as they were counted at the time of their release. Nonetheless, Canada continues to monitor and document WCI credit flows in recognition of their contribution to a credible, transparent, and well-functioning emissions trading system.

Long description

WAM Change| Scenario | Sector | Emissions |

|---|---|---|

| WM Change | Oil and Gas | 45 |

| WM Change | Electricity | 3 |

| WM Change | Transportation | -8 |

| WM Change | Heavy Industry | -16 |

| WM Change | Buildings | 3 |

| WM Change | Agriculture | 2 |

| WM Change | Waste and Others | 4 |

| WM Change | WCI Credits | NA |

| WM Change | LULUCF Accounting Contribution | 7 |

| WM Change | NBCS and Agriculture Measures | NA |

| WM Change | Total | 40 |

| WAM Change | Oil and Gas | 47 |

| WAM Change | Electricity | 5 |

| WAM Change | Transportation | 1 |

| WAM Change | Heavy Industry | -4 |

| WAM Change | Buildings | 7 |

| WAM Change | Agriculture | 6 |

| WAM Change | Waste and Others | 8 |

| WAM Change | WCI Credits | -4 |

| LULUCF Accounting Contribution | 7 | |

| WAM Change | NBCS and Agriculture Measures | 1 |

| WAM Change | Total | 79 |

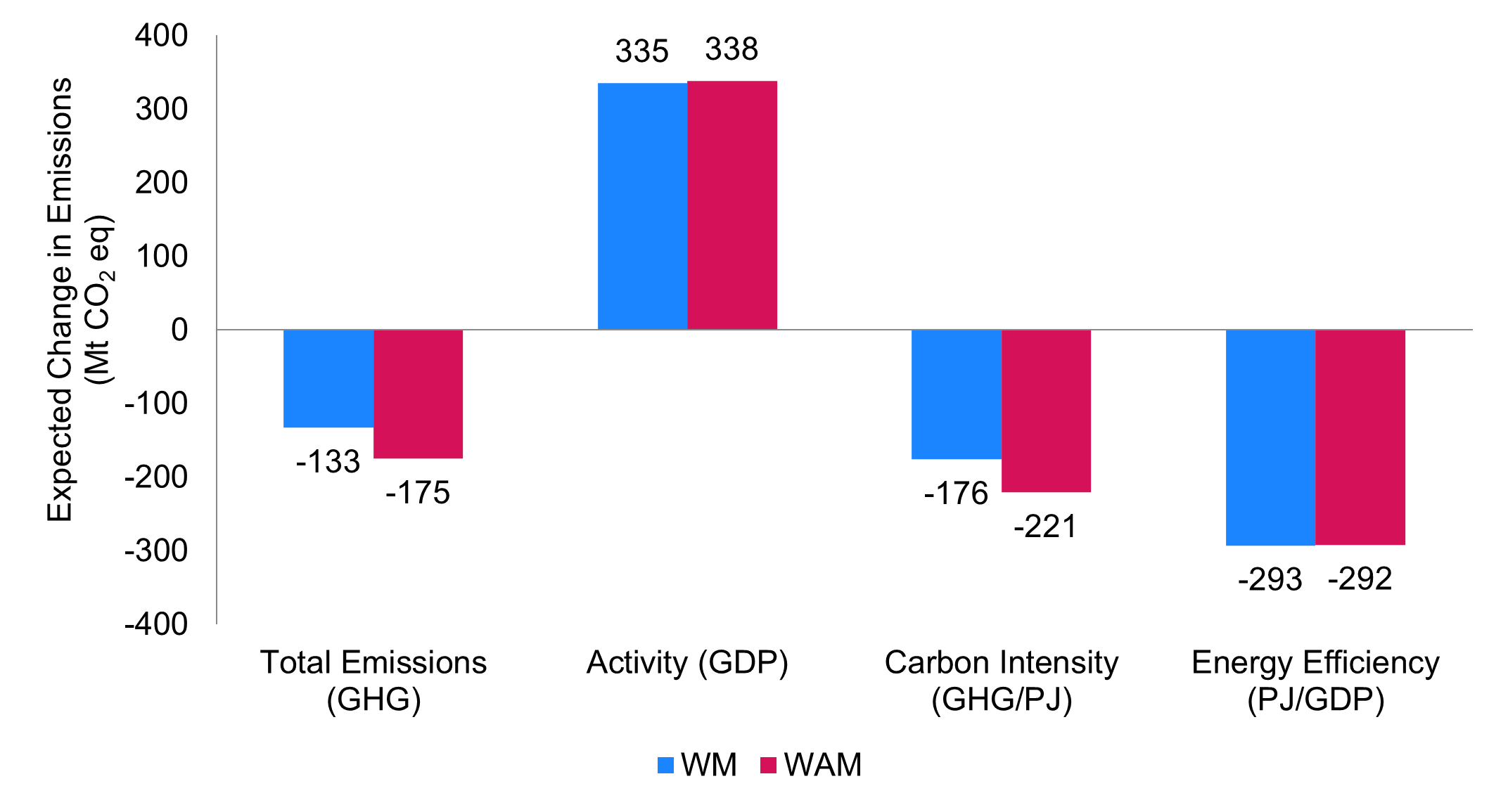

2.1.4 Decomposition of projected change in Canada's GHG emissions

This decomposition analysis explores how different factors contribute to trends in Canada’s historical and projected GHG emissions under the WM and WAM scenarios (Figure 4).

In both scenarios from 2005 to 2030, there is a significant decoupling of economic growth and combustion emissions. Upward pressure on GHG emission projections arising from GDP growth is offset by the switch to cleaner and more efficient energy use. In the WAM scenario, the impact of economic activity adds 338 Mt. This is more than offset by a combined reduction of 513 Mt from lower carbon intensity and greater energy efficiency.

- The Activity Effect measures the impact of economic growth, which is estimated to be 53% over the 2005 to 2030 period

- On its own, this growth is projected to lead to 335 Mt of additional GHG emissions in 2030 in the WM scenario and 338 Mt in the WAM scenario

- The Carbon Intensity Effect measures changes in the carbon emission coefficient of energy

- The shift to cleaner fuels such as the replacement of coal-fired electricity with cleaner sources, as well as measures to reduce fugitive and process emissions, are projected to have a significant impact, reducing emissions by 176 Mt in 2030 in the WM scenario and 221 Mt in the WAM scenario

- The Energy Efficiency Effect measures changes in energy efficiency at the subsector level

- The analysis shows that the uptake of energy-efficient technologies, induced by policies, consumer responses to energy prices, and stock turnover, reduces emissions by 293 Mt in 2030 in the WM scenario and 292 Mt in the WAM scenario

Note: Numbers may not sum to the total due to rounding.

Long description

| Category | 2030 Expected Change in Emissions, WM (Mt CO2 eq) | 2030 Expected Change in Emissions, WAM (Mt CO2 eq) |

|---|---|---|

| Total Emissions (GHG) | -133 | -175 |

| Activity (GDP) | 335 | 338 |

| Carbon Intensity (GHG/PJ) | -176 | -221 |

| Energy Efficiency (PJ/GDP) | -293 | -292 |

2.2 Sectoral emissions analysis

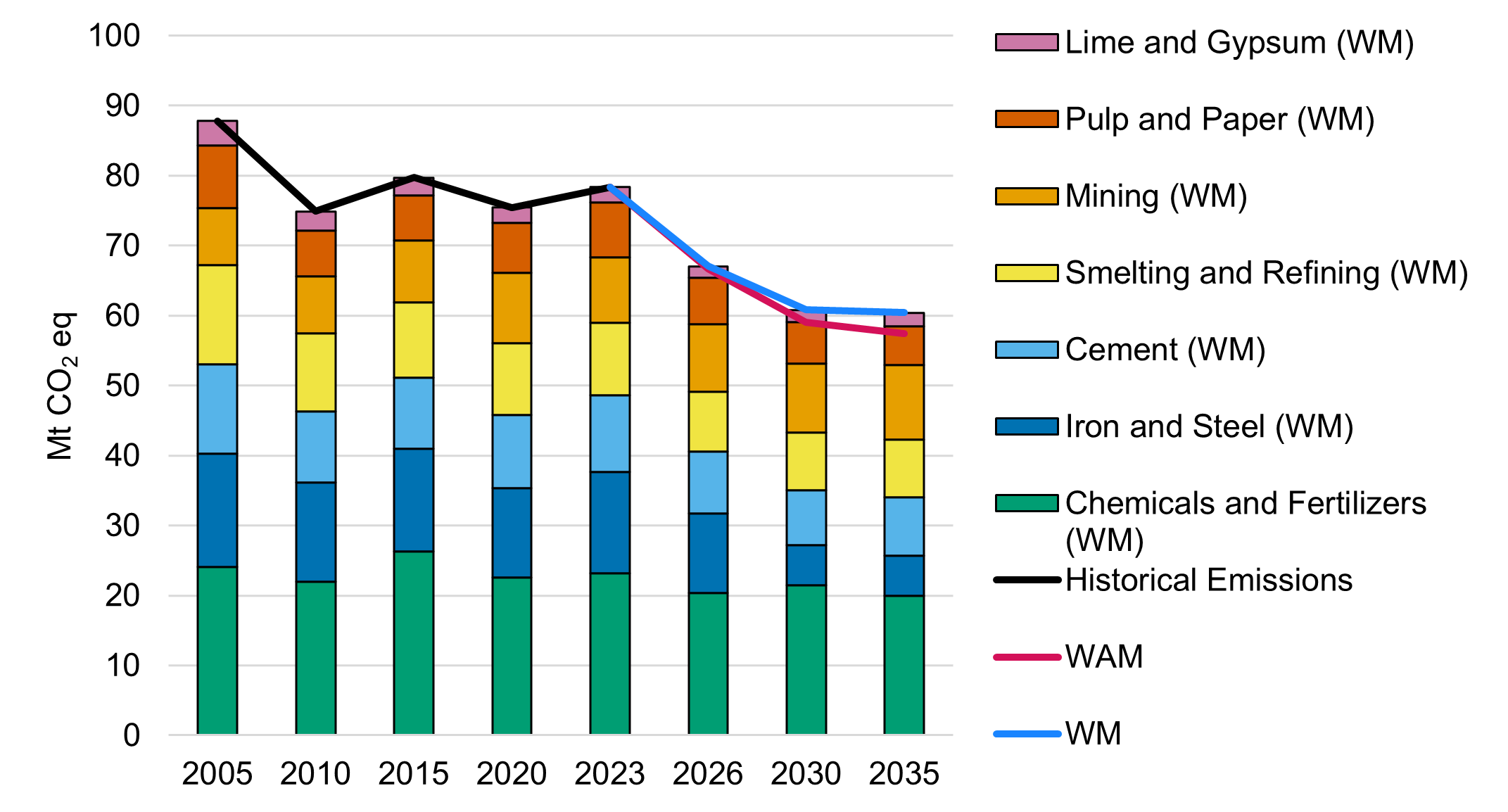

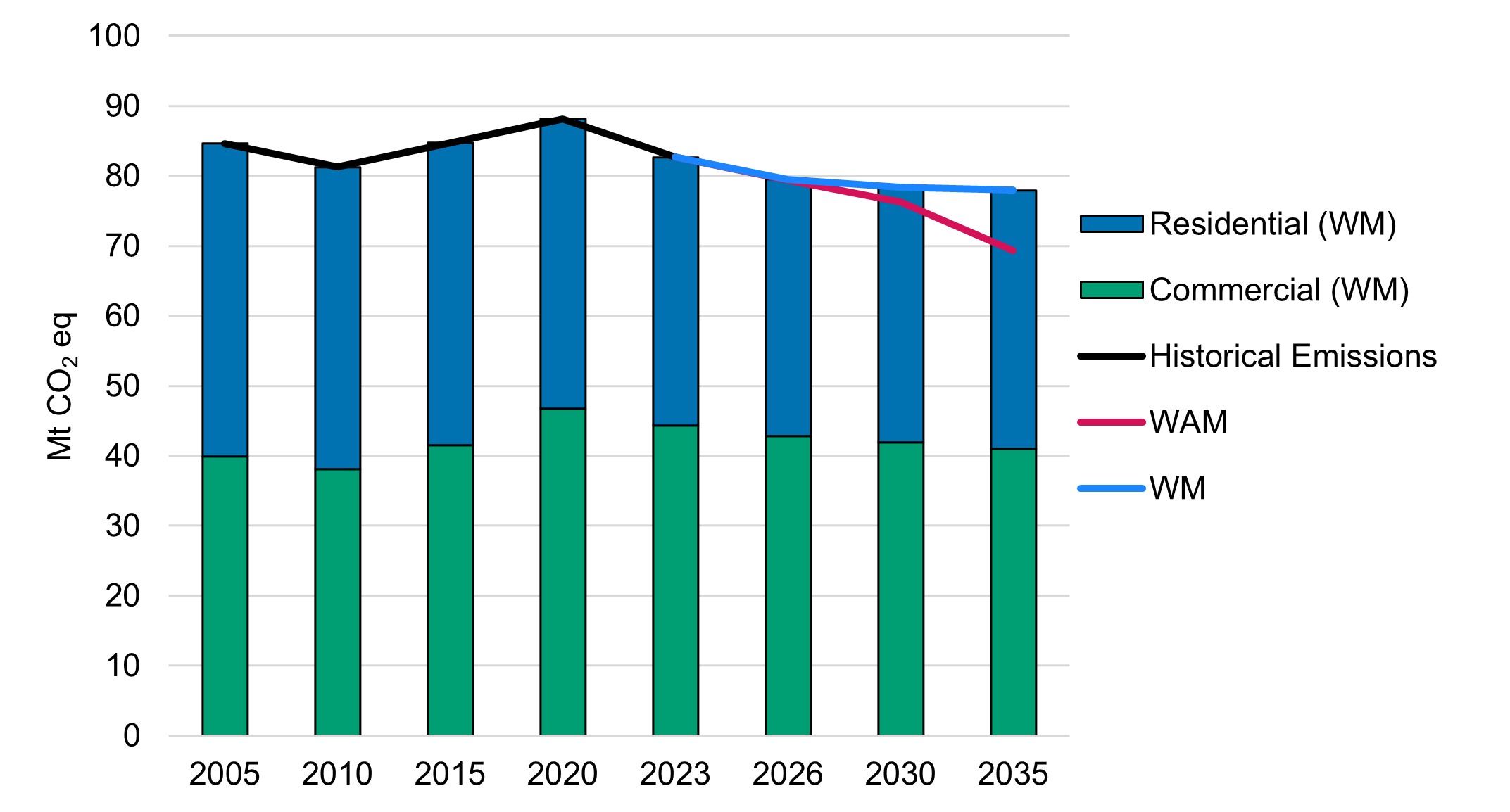

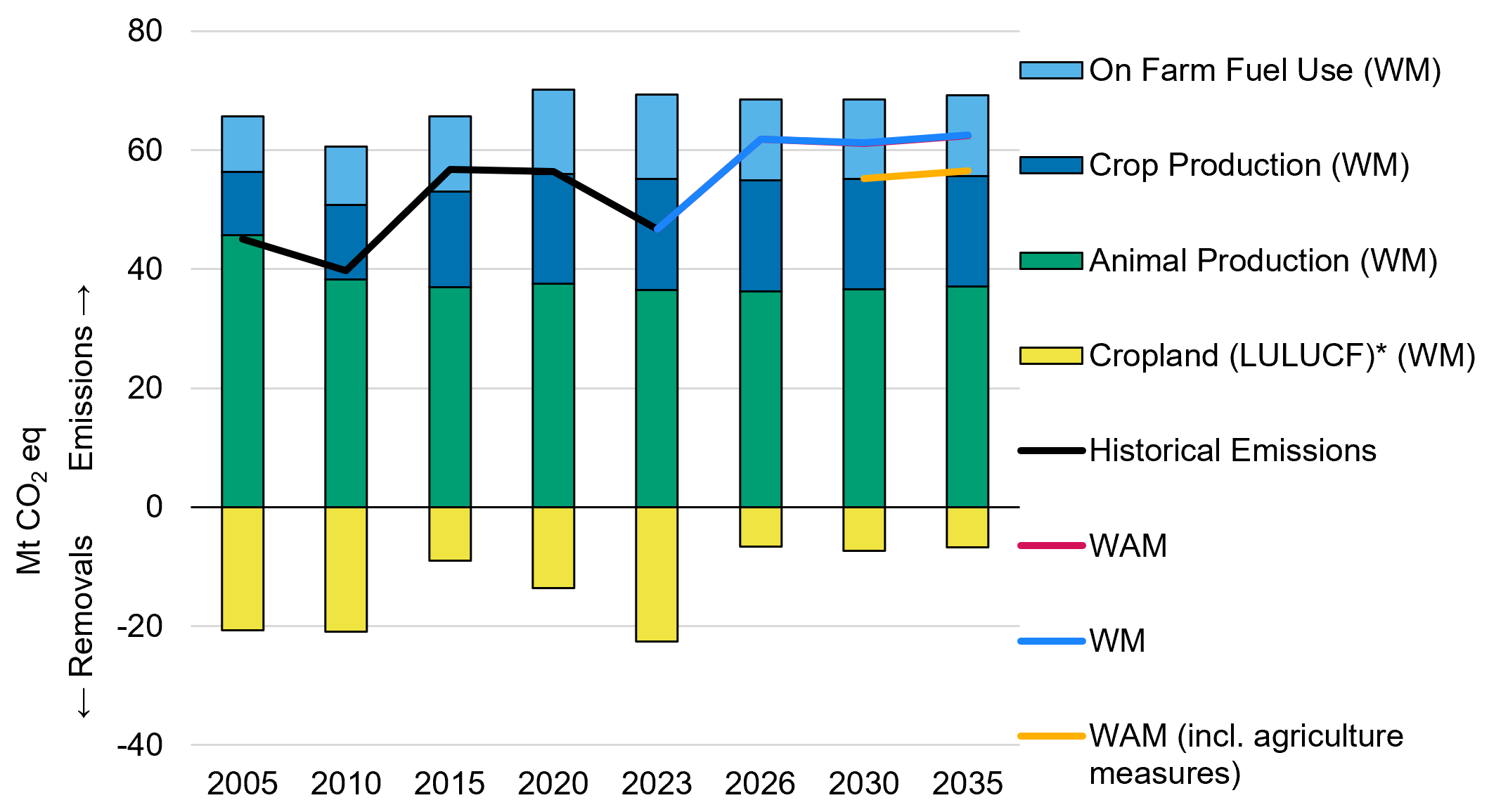

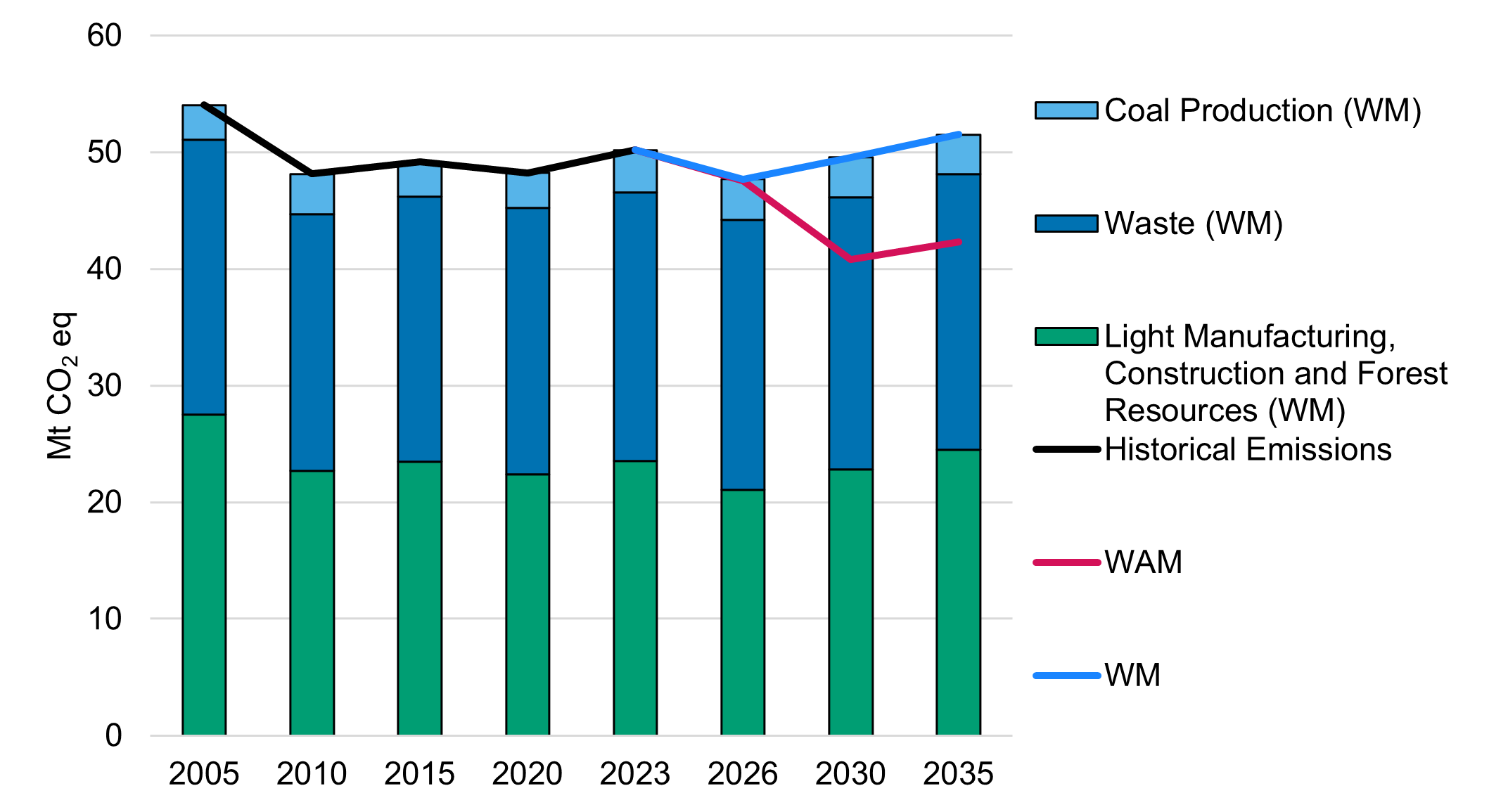

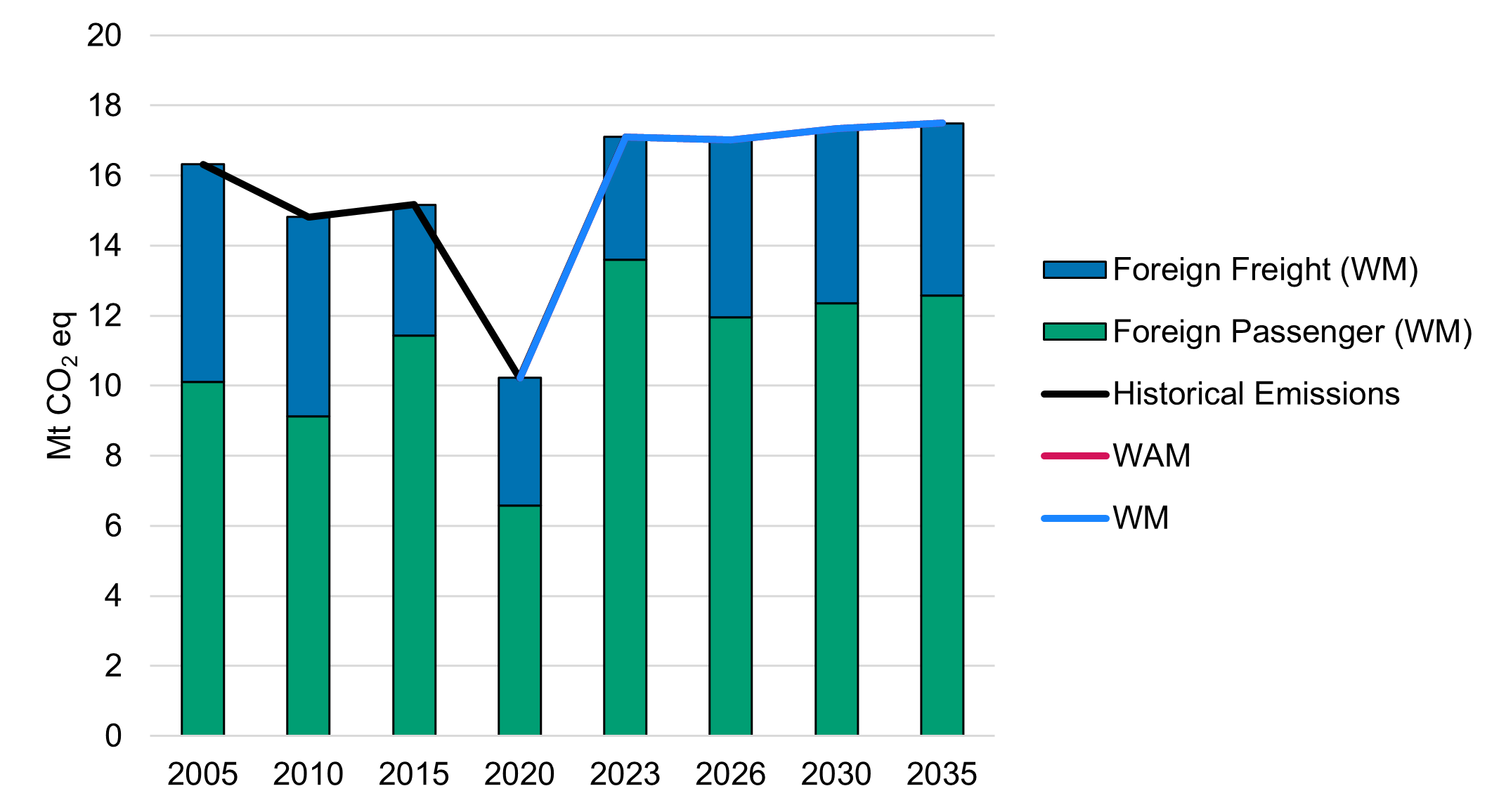

This section presents Canada’s emissions broken down by the following economic sectors: Oil and Gas (including details on emissions attributable to oil and gas exports), Transportation, Electricity, Heavy Industry, Buildings, Agriculture, and Waste and Others (Others includes coal production, light manufacturing, construction and forest resources). Details about emissions reductions resulting from carbon capture and storage (CCS) are presented at the sector level in Section 2.2.8. Finally, foreign passenger and foreign freight emissions are not included in the national total, consistent with the 2006 IPCC Guidelines for National Greenhouse Gas Inventories. They are, however, presented separately in Section 2.2.9.

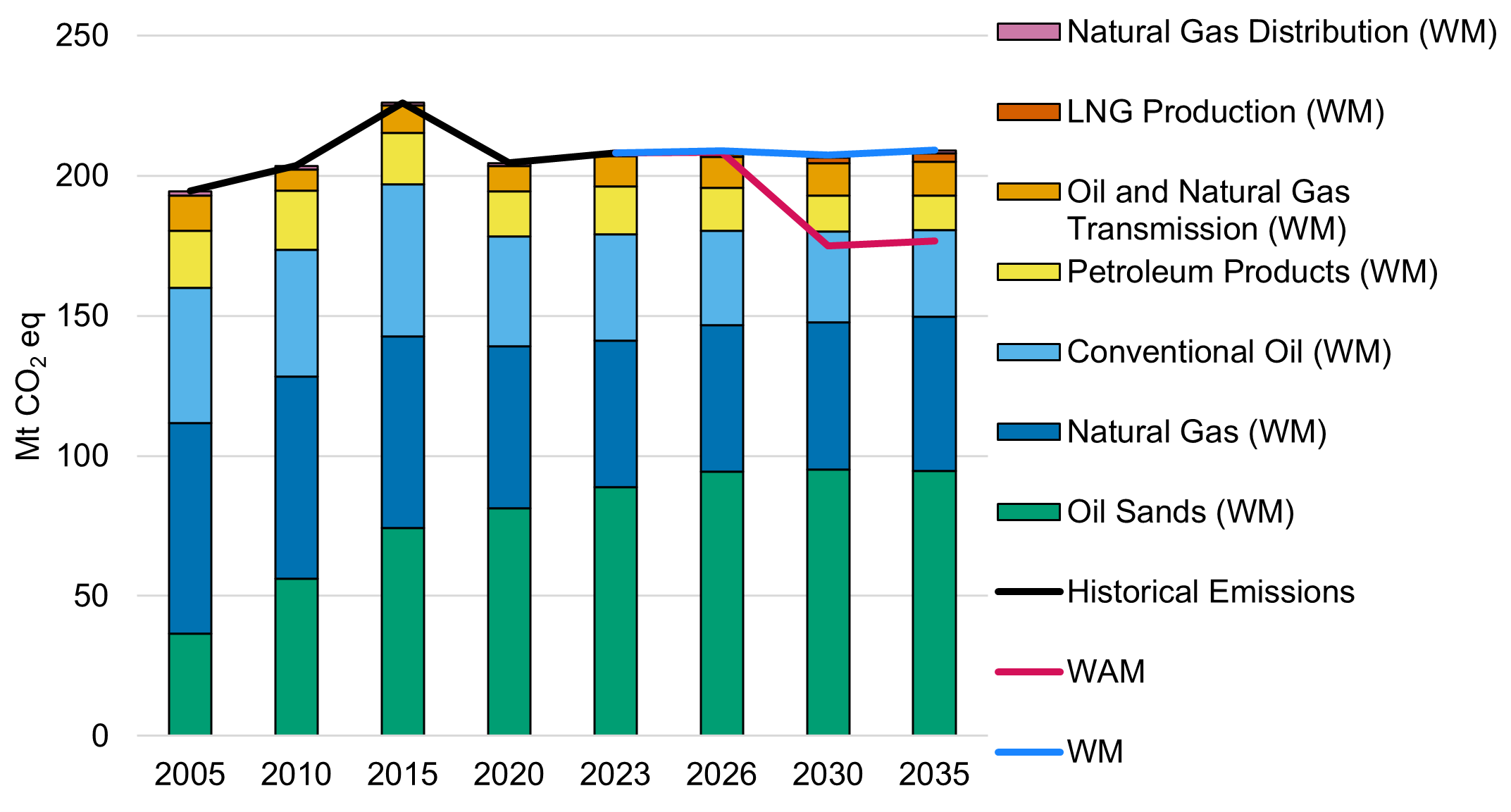

2.2.1 Oil and Gas

Production, pipeline transportation, processing, refining, and distribution of oil and gas products all contribute to emissions in the Oil and Gas sector. In 2023, this sector was the largest source of GHG emissions in Canada, accounting for 30% of the national total, excluding the LULUCF accounting contribution. Oil and Gas emissions have increased 91 Mt since 1990, largely due to oil sands expansion. Although emissions peaked in 2014, they declined by 14 Mt between 2019 and 2023, reflecting the impact of federal and provincial methane regulations introduced in 2020.

The sector’s emissions are driven by oil and gas production forecasts from the CER. This year’s production and price forecasts use a preliminary version of the Current Measures scenario from the CER’s 2026 Energy Future (EF2026) outlook.

In the WM scenario, over the projection period, emissions from increasing production of oil sands, natural gas, and liquefied natural gas (LNG) are partly offset by declining emission intensities across subsectors. Measures such as regulations on methane emissions in the upstream Oil and Gas sector, the industrial fuel charge, the Clean Fuel Regulations (CFR), and CCS technologies are projected to constrain emissions.

The WAM scenario reflects an ambitious policy environment, with substantial emissions abatement due to enhanced decarbonization, energy efficiency, and methane reductions. A breakdown of emissions by subsector is provided below.

It is important to note that the Enhanced Oil and Gas Methane Regulations targeting 75% reduction in methane emissions from the oil and gas sector by 2030 from 2012 levels, were finalized on December 16, 2025, which was too late for inclusion in the WM scenario, and thus they were included only in the WAM scenario.

Across all subsectors, emissions are shaped by production trends, technological adoption, and policy measures. While output continues to grow, emissions are increasingly constrained by federal and provincial initiatives. Table 4 provides detailed subsector data, and Figure 5 to Figure 9 illustrate emissions and intensity trends under the WM and WAM scenarios.

| Subsector | 1990 | 2005 | 2023 | 2026a | 2030a | 2035a | 2026b | 2030b | 2035b |

|---|---|---|---|---|---|---|---|---|---|

| Natural Gas Production and Processing | 38 | 75 | 52 | 52 | 53 | 55 | 52 | 40 | 39 |

| Conventional Oil | 32 | 48 | 38 | 34 | 32 | 31 | 34 | 21 | 20 |

| Light Oil Production | 19 | 22 | 21 | 19 | 19 | 17 | 19 | 10 | 9 |

| Heavy Oil Production | 13 | 25 | 16 | 13 | 12 | 11 | 13 | 9 | 9 |

| Frontier Oil Production | 0 | 2 | 1 | 2 | 2 | 2 | 2 | 2 | 2 |

| Oil Sands | 15 | 37 | 89 | 94 | 95 | 95 | 94 | 89 | 92 |

| In-Situ | 5 | 13 | 47 | 49 | 53 | 53 | 49 | 50 | 52 |

| Mining and Extraction | 3 | 7 | 17 | 20 | 20 | 20 | 20 | 20 | 20 |

| Upgraders | 8 | 17 | 24 | 25 | 23 | 22 | 25 | 20 | 20 |

| Oil and Natural Gas Transmission | 12 | 12 | 11 | 11 | 12 | 12 | 11 | 10 | 10 |

| Downstream Oil and Gas | 20 | 22 | 18 | 16 | 14 | 13 | 16 | 13 | 13 |

| Petroleum Products | 18 | 20 | 17 | 15 | 13 | 12 | 15 | 12 | 12 |

| Natural Gas Distribution | 2 | 2 | 1 | 1 | 1 | 1 | 1 | 1 | 1 |

| LNG Production | 0 | 0 | 0 | 1 | 2 | 3 | 1 | 2 | 3 |

| Total | 117 | 194 | 208 | 209 | 207 | 209 | 208 | 175 | 177 |

Note: Numbers may not sum to the total due to rounding. Historical data up to 2023 are sourced from NIR2025. Data from 2024 to 2035 are modelled projections developed using ECCC’s analytical framework. Access more data on the open data portal.

a Projections under the WM scenario.

b Projections under the WAM scenario.

Note: Historical emissions data come from NIR2025. Access more data on the open data portal.

Long description

| Year | Conventional Oil (WM) | LNG Production (WM) | Natural Gas Distribution (WM) | Natural Gas (WM) | Oil and Natural Gas Transmission (WM) | Oil Sands (WM) | Petroleum Products (WM) | Historical Emissions | WM | WAM |

|---|---|---|---|---|---|---|---|---|---|---|

| 2005 | 48 | 0 | 2 | 75 | 12 | 37 | 20 | 194 | - | - |

| 2010 | 45 | 0 | 1 | 72 | 7 | 56 | 21 | 203 | - | - |

| 2015 | 54 | 0 | 1 | 68 | 10 | 74 | 18 | 226 | - | - |

| 2020 | 39 | 0 | 1 | 58 | 9 | 81 | 16 | 204 | - | - |

| 2023 | 38 | 0 | 1 | 52 | 11 | 89 | 17 | 208 | 208 | 208 |

| 2026 | 34 | 1 | 1 | 52 | 11 | 94 | 15 | - | 209 | 208 |

| 2030 | 32 | 2 | 1 | 53 | 12 | 95 | 13 | - | 207 | 175 |

| 2035 | 31 | 3 | 1 | 55 | 12 | 95 | 12 | - | 209 | 177 |

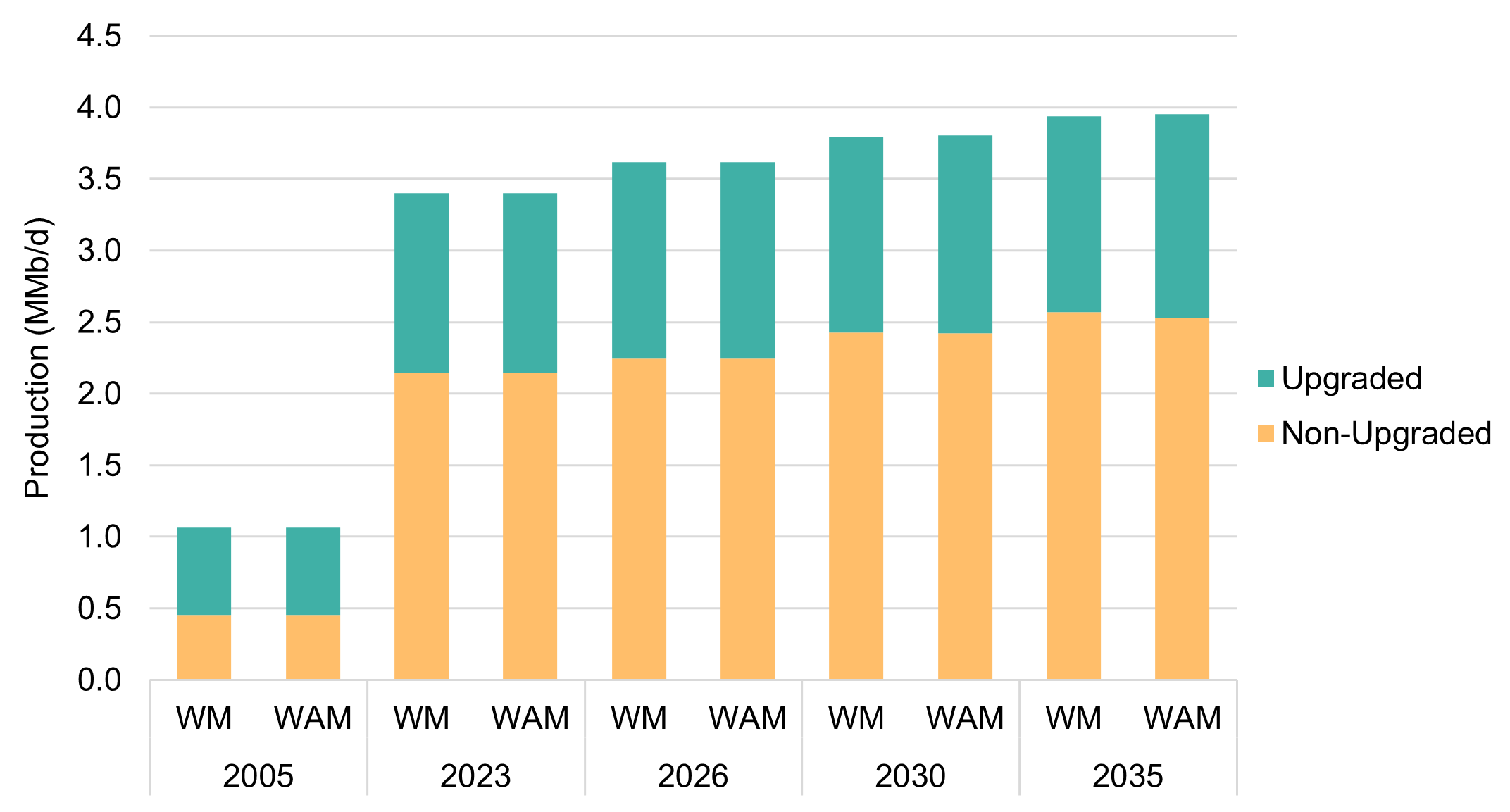

2.2.1.1 Upstream oil and gas production

This subsector includes extraction, production, and processing of conventional and unconventional oil and gas. Emissions in this sector are primarily influenced by two opposing trends: increasing production and declining emissions intensity (open data Table A17). Oil sands and natural gas output are projected to grow steadily, supported by market conditions and investment. Under the WM scenario, emissions intensity declines due to the industrial fuel charge, CFR, and CCS deployment. Additional reductions are driven by technological advancements, provincial regulations, such as the CleanBC plan, and by federal and provincial methane regulations.

In the WAM scenario, further reductions are achieved through Enhanced Oil and Gas Methane Regulations and funding programs (such as the Canada Growth Fund and carbon revenue recycling mechanisms). The Enhanced Oil and Gas Methane Regulations, effective in 2028, target a 75% reduction from 2012 levels, mostly in conventional operations.

Lower CFR credit prices in the WAM scenario reduce compliance costs, encouraging development. Figure 6 illustrates the shift toward in-situ production in the forecast, while Figure 7 shows non-upgraded oil sands representing a dominant portion of oil sands production in the forecast period.

Long description

| Year | Scenario | Sector | Production (MMb/d) |

|---|---|---|---|

| 2005 | WM | In-Situ | 0.29 |

| 2005 | WM | Oil Sands Mining | 0.63 |

| 2005 | WM | Primary Oil Sands | 0.15 |

| 2023 | WM | In-Situ | 1.55 |

| 2023 | WM | Oil Sands Mining | 1.65 |

| 2023 | WM | Primary Oil Sands | 0.20 |

| 2026 | WM | In-Situ | 1.68 |

| 2026 | WM | Oil Sands Mining | 1.72 |

| 2026 | WM | Primary Oil Sands | 0.22 |

| 2030 | WM | In-Situ | 1.83 |

| 2030 | WM | Oil Sands Mining | 1.74 |

| 2030 | WM | Primary Oil Sands | 0.23 |

| 2035 | WM | In-Situ | 1.90 |

| 2035 | WM | Oil Sands Mining | 1.79 |

| 2035 | WM | Primary Oil Sands | 0.24 |

| 2005 | WAM | In-Situ | 0.29 |

| 2005 | WAM | Oil Sands Mining | 0.63 |

| 2005 | WAM | Primary Oil Sands | 0.15 |

| 2023 | WAM | In-Situ | 1.55 |

| 2023 | WAM | Oil Sands Mining | 1.65 |

| 2023 | WAM | Primary Oil Sands | 0.20 |

| 2026 | WAM | In-Situ | 1.68 |

| 2026 | WAM | Oil Sands Mining | 1.72 |

| 2026 | WAM | Primary Oil Sands | 0.22 |

| 2030 | WAM | In-Situ | 1.83 |

| 2030 | WAM | Oil Sands Mining | 1.74 |

| 2030 | WAM | Primary Oil Sands | 0.23 |

| 2035 | WAM | In-Situ | 1.91 |

| 2035 | WAM | Oil Sands Mining | 1.80 |

| 2035 | WAM | Primary Oil Sands | 0.24 |

Long description

| Year | Scenario | Sector | Production (MMb/d) |

|---|---|---|---|

| 2005 | WM | Upgraded | 0.61 |

| 2023 | WM | Upgraded | 1.26 |

| 2026 | WM | Upgraded | 1.37 |

| 2030 | WM | Upgraded | 1.37 |

| 2035 | WM | Upgraded | 1.37 |

| 2005 | WM | Non-Upgraded | 0.45 |

| 2023 | WM | Non-Upgraded | 2.15 |

| 2026 | WM | Non-Upgraded | 2.25 |

| 2030 | WM | Non-Upgraded | 2.43 |

| 2035 | WM | Non-Upgraded | 2.57 |

| 2005 | WAM | Upgraded | 0.61 |

| 2023 | WAM | Upgraded | 1.26 |

| 2026 | WAM | Upgraded | 1.37 |

| 2030 | WAM | Upgraded | 1.38 |

| 2035 | WAM | Upgraded | 1.42 |

| 2005 | WAM | Non-Upgraded | 0.45 |

| 2023 | WAM | Non-Upgraded | 2.15 |

| 2026 | WAM | Non-Upgraded | 2.25 |

| 2030 | WAM | Non-Upgraded | 2.42 |

| 2035 | WAM | Non-Upgraded | 2.53 |

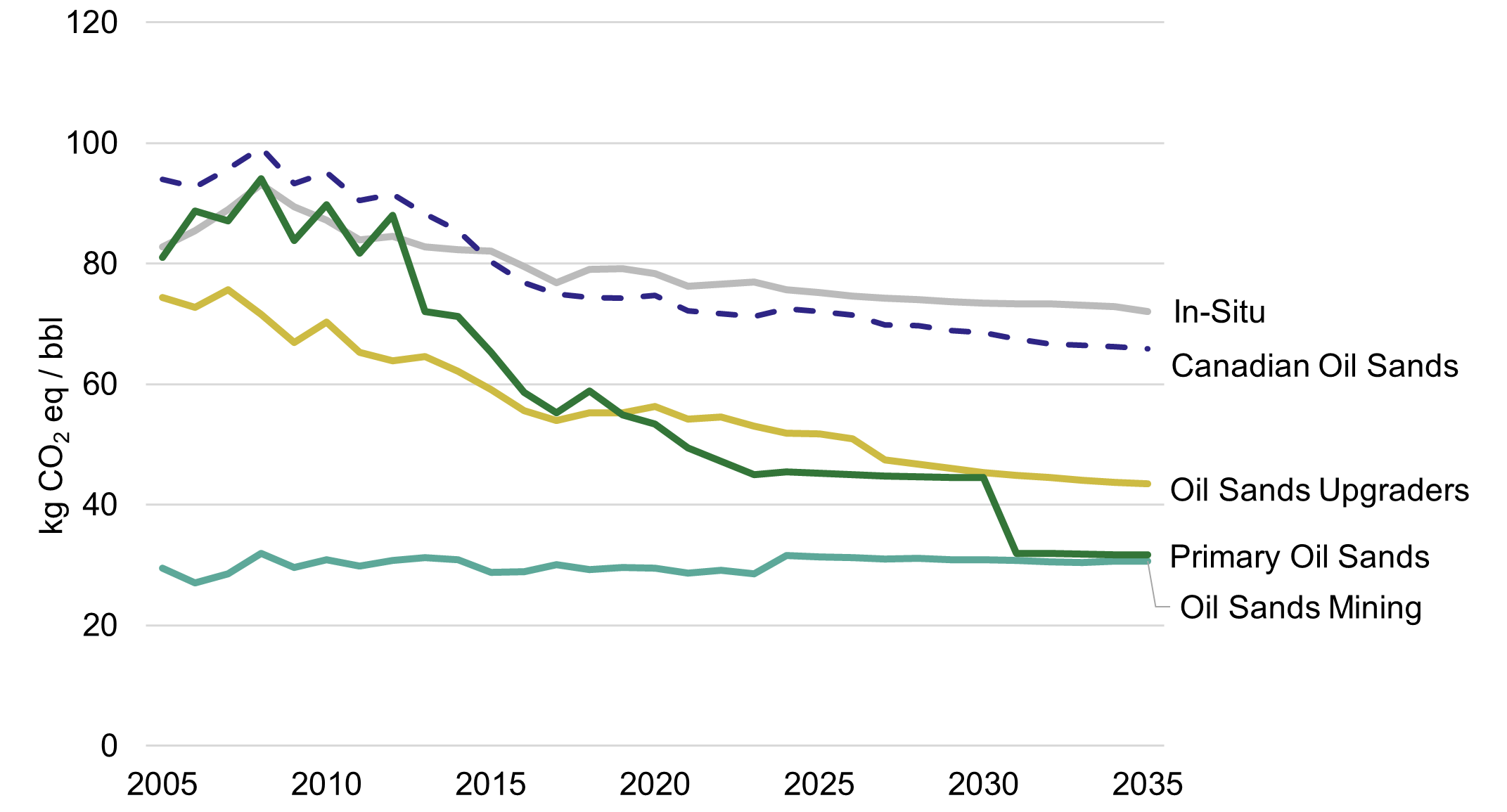

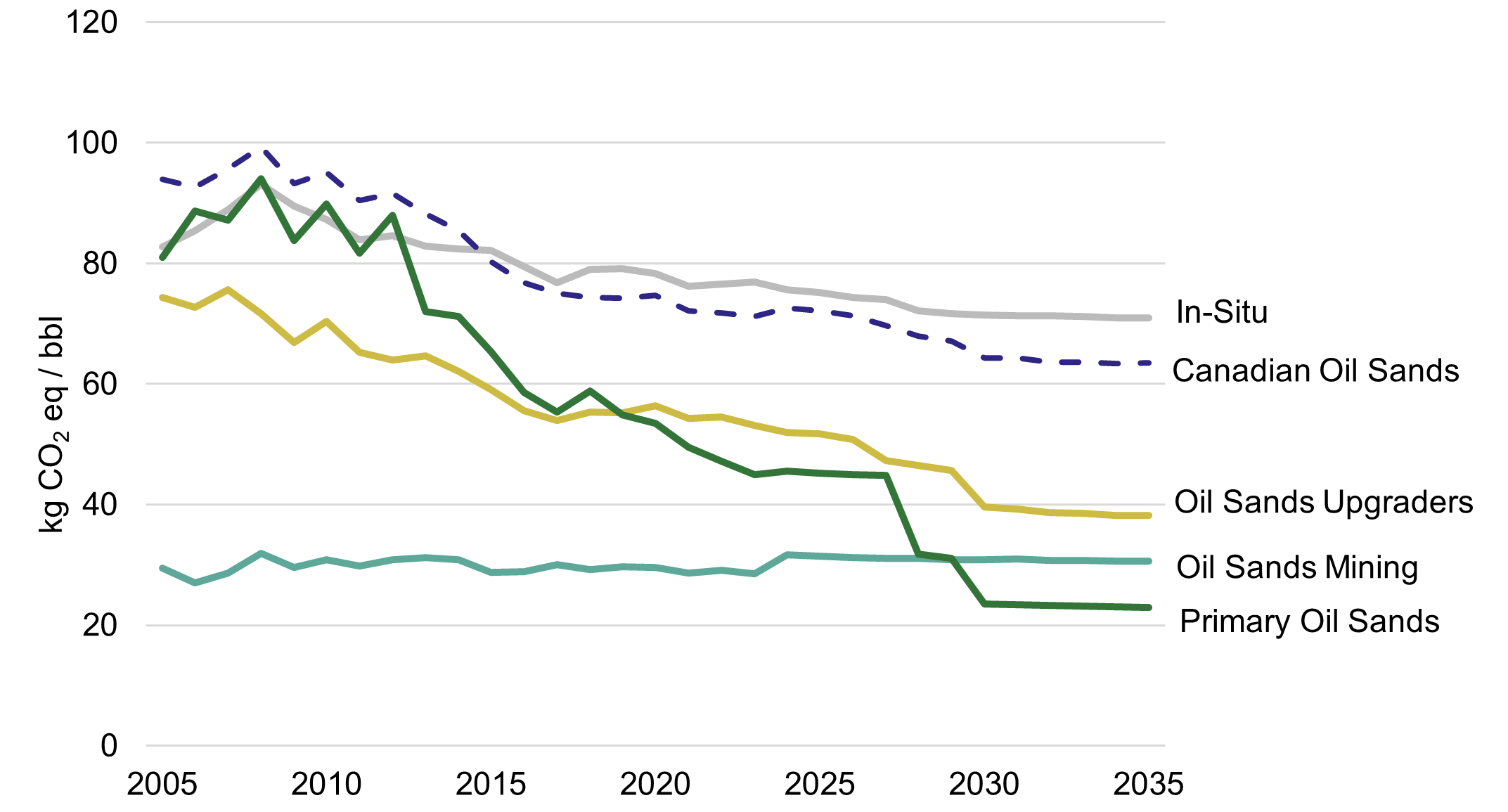

Emissions intensity in the oil sands is influenced by extraction method, infrastructure age, and reservoir quality. In-situ extraction, where bitumen is separated underground, is generally more emissions-intensive than surface mining, as shown in Figure 8. As production grew significantly between 2005 and 2023, intensity remained relatively stable. Starting in 2024, emissions from mining operations are expected to rise due to the replacement of petroleum coke-fired boilers with high-efficiency natural gas cogeneration units at Suncor’s Base Plant. While this upgrade improves energy efficiency, it also increases reported cogeneration emissions.

Additional upward pressure on emissions intensity is expected from declining reservoir quality, aging infrastructure, and a continued shift towards in-situ operations. Future production growth is projected to come from brownfield expansions and new greenfield developments that incorporate more energy-efficient technologies. These newer facilities are also more likely to adopt emerging technologies within the unconventional crude oil sector, helping to offset some of the intensity increases.

Emissions intensity is projected to decline under both the WM and WAM scenarios, driven by stronger policy measures and technology adoption. Key drivers include the CFR, Enhanced Oil and Gas Methane Regulations, the industrial fuel charge, and the carbon capture, utilization and storage (CCUS) investment tax credit (ITC). These measures aim to reduce emissions while supporting continued production growth.

Figure 8 and Figure 9 illustrate projected emissions intensity trends under the WM and WAM scenarios, reflecting the combined influence of policy, technology, and operational changes across the oil sands sector.

Note: Historical emissions data come from NIR2025. In-situ includes production from cyclic steam stimulation (CSS) and steam assisted gravity drainage (SAGD). Canadian oil sands include emissions from oil sands upgraders, but not the barrels of synthetic crude oil produced by upgraders, as this would lead to double counting of bitumen that is first extracted and then upgraded.

Long description

| Year | In-Situ | Canadian Oil Sands | Oil Sands Mining | Oil Sands Upgraders | Primary Oil Sands |

|---|---|---|---|---|---|

| 2005 | 82.8 | 94.0 | 29.5 | 74.4 | 81.0 |

| 2006 | 85.4 | 93.0 | 27.0 | 72.7 | 88.7 |

| 2007 | 88.9 | 96.0 | 28.6 | 75.6 | 87.1 |

| 2008 | 93.1 | 99.0 | 32.0 | 71.6 | 94.1 |

| 2009 | 89.5 | 93.0 | 29.6 | 66.9 | 83.8 |

| 2010 | 87.3 | 95.0 | 30.9 | 70.3 | 89.8 |

| 2011 | 83.9 | 90.0 | 29.8 | 65.3 | 81.7 |

| 2012 | 84.6 | 91.6 | 30.8 | 63.9 | 88.0 |

| 2013 | 82.8 | 88.0 | 31.2 | 64.6 | 72.1 |

| 2014 | 82.3 | 85.0 | 30.8 | 62.1 | 71.2 |

| 2015 | 82.1 | 80.0 | 28.8 | 59.1 | 65.3 |

| 2016 | 79.5 | 77.0 | 28.9 | 55.6 | 58.6 |

| 2017 | 76.8 | 75.0 | 30.0 | 54.0 | 55.3 |

| 2018 | 79.0 | 74.0 | 29.3 | 55.3 | 58.8 |

| 2019 | 79.2 | 74.0 | 29.6 | 55.3 | 54.9 |

| 2020 | 78.4 | 75.0 | 29.5 | 56.3 | 53.4 |

| 2021 | 76.3 | 72.1 | 28.7 | 54.3 | 49.5 |

| 2022 | 76.6 | 71.8 | 29.1 | 54.6 | 47.2 |

| 2023 | 76.9 | 71.2 | 28.6 | 53.1 | 45.0 |

| 2024 | 75.6 | 72.5 | 31.6 | 51.9 | 45.5 |

| 2025 | 75.2 | 72.1 | 31.3 | 51.7 | 45.2 |

| 2026 | 74.6 | 71.4 | 31.2 | 50.9 | 45.0 |

| 2027 | 74.3 | 69.8 | 31.0 | 47.5 | 44.8 |

| 2028 | 74.1 | 69.7 | 31.1 | 46.8 | 44.7 |

| 2029 | 73.7 | 68.9 | 30.9 | 46.0 | 44.6 |

| 2030 | 73.4 | 68.5 | 30.9 | 45.4 | 44.5 |

| 2031 | 73.4 | 67.6 | 30.7 | 44.9 | 32.0 |

| 2032 | 73.3 | 66.7 | 30.5 | 44.5 | 31.9 |

| 2033 | 73.1 | 66.5 | 30.5 | 44.1 | 31.8 |

| 2034 | 72.8 | 66.3 | 30.6 | 43.7 | 31.7 |

| 2035 | 72.1 | 65.9 | 30.6 | 43.4 | 31.7 |

Note: Historical emissions data come from NIR2025. In-situ includes production from CSS and SAGD. Canadian oil sands include emissions from oil sands upgraders, but not the barrels of synthetic crude oil produced by upgraders, as this would lead to double counting of bitumen that is first extracted and then upgraded.

Long description

| Year | In-Situ | Canadian Oil Sands | Oil Sands Mining | Oil Sands Upgraders | Primary Oil Sands |

|---|---|---|---|---|---|

| 2005 | 82.8 | 94.0 | 29.5 | 74.4 | 81.0 |

| 2006 | 85.4 | 93.0 | 27.0 | 72.7 | 88.7 |

| 2007 | 88.9 | 96.0 | 28.6 | 75.6 | 87.1 |

| 2008 | 93.1 | 99.0 | 32.0 | 71.6 | 94.1 |

| 2009 | 89.5 | 93.0 | 29.6 | 66.9 | 83.8 |

| 2010 | 87.3 | 95.0 | 30.9 | 70.3 | 89.8 |

| 2011 | 83.9 | 90.0 | 29.8 | 65.3 | 81.7 |

| 2012 | 84.6 | 91.6 | 30.8 | 63.9 | 88.0 |

| 2013 | 82.8 | 88.0 | 31.2 | 64.6 | 72.1 |

| 2014 | 82.3 | 85.0 | 30.8 | 62.1 | 71.2 |

| 2015 | 82.1 | 80.0 | 28.8 | 59.1 | 65.3 |

| 2016 | 79.5 | 77.0 | 28.9 | 55.6 | 58.6 |

| 2017 | 76.8 | 75.0 | 30.0 | 54.0 | 55.3 |

| 2018 | 79.0 | 74.0 | 29.3 | 55.3 | 58.8 |

| 2019 | 79.2 | 74.0 | 29.6 | 55.3 | 54.9 |

| 2020 | 78.4 | 75.0 | 29.5 | 56.3 | 53.4 |

| 2021 | 76.3 | 72.1 | 28.7 | 54.3 | 49.5 |

| 2022 | 76.6 | 71.8 | 29.1 | 54.6 | 47.2 |

| 2023 | 76.9 | 71.2 | 28.6 | 53.1 | 45.0 |

| 2024 | 75.7 | 72.6 | 31.6 | 51.9 | 45.5 |

| 2025 | 75.2 | 72.2 | 31.4 | 51.7 | 45.2 |

| 2026 | 74.4 | 71.3 | 31.2 | 50.8 | 45.0 |

| 2027 | 74.0 | 69.7 | 31.0 | 47.3 | 44.8 |

| 2028 | 72.1 | 68.0 | 31.0 | 46.4 | 31.8 |

| 2029 | 71.7 | 67.1 | 30.9 | 45.7 | 31.1 |

| 2030 | 71.4 | 64.3 | 30.9 | 39.6 | 23.6 |

| 2031 | 71.4 | 64.3 | 30.9 | 39.3 | 23.4 |

| 2032 | 71.3 | 63.6 | 30.7 | 38.7 | 23.3 |

| 2033 | 71.2 | 63.6 | 30.7 | 38.6 | 23.2 |

| 2034 | 71.0 | 63.4 | 30.6 | 38.2 | 23.0 |

| 2035 | 71.0 | 63.5 | 30.6 | 38.2 | 22.9 |

2.2.1.2 Transmission and distribution of oil and gas

Emissions from transmission and distribution of oil and gas are projected to remain relatively stable under the WM scenario, as shown in Table 4. This reflects the CER’s assumptions regarding incremental infrastructure development. Under the WAM scenario, emissions decline modestly due to the Enhanced Oil and Gas Methane Regulations.

2.2.1.3 Petroleum refining and upgrading

Emissions from petroleum refining and upgrading decline in both the WM and WAM scenarios (open data Table A18), primarily due to CCS deployment. Projects such as Shell Quest and the Alberta Carbon Trunk Line contribute significantly. Refining and upgrading offer low-cost CCS opportunities, with over 3 Mt of capacity expected by 2030. Under the WAM scenario, emissions decline further due to additional investments from the Canada Growth Fund and Output-Based Pricing System (OBPS) revenues.

2.2.1.4 Upstream emissions attributable to exports

Canada’s GHG projections follow territorial accounting. All extraction, processing, upgrading and transmission emissions occur in Canada and are already included in the Oil and Gas sector totals. This subsection provides additional information on decomposition of emissions associated with production of oil and gas products for domestic consumption versus for exports. Importantly, the national totals reported elsewhere in this report remain unchanged.

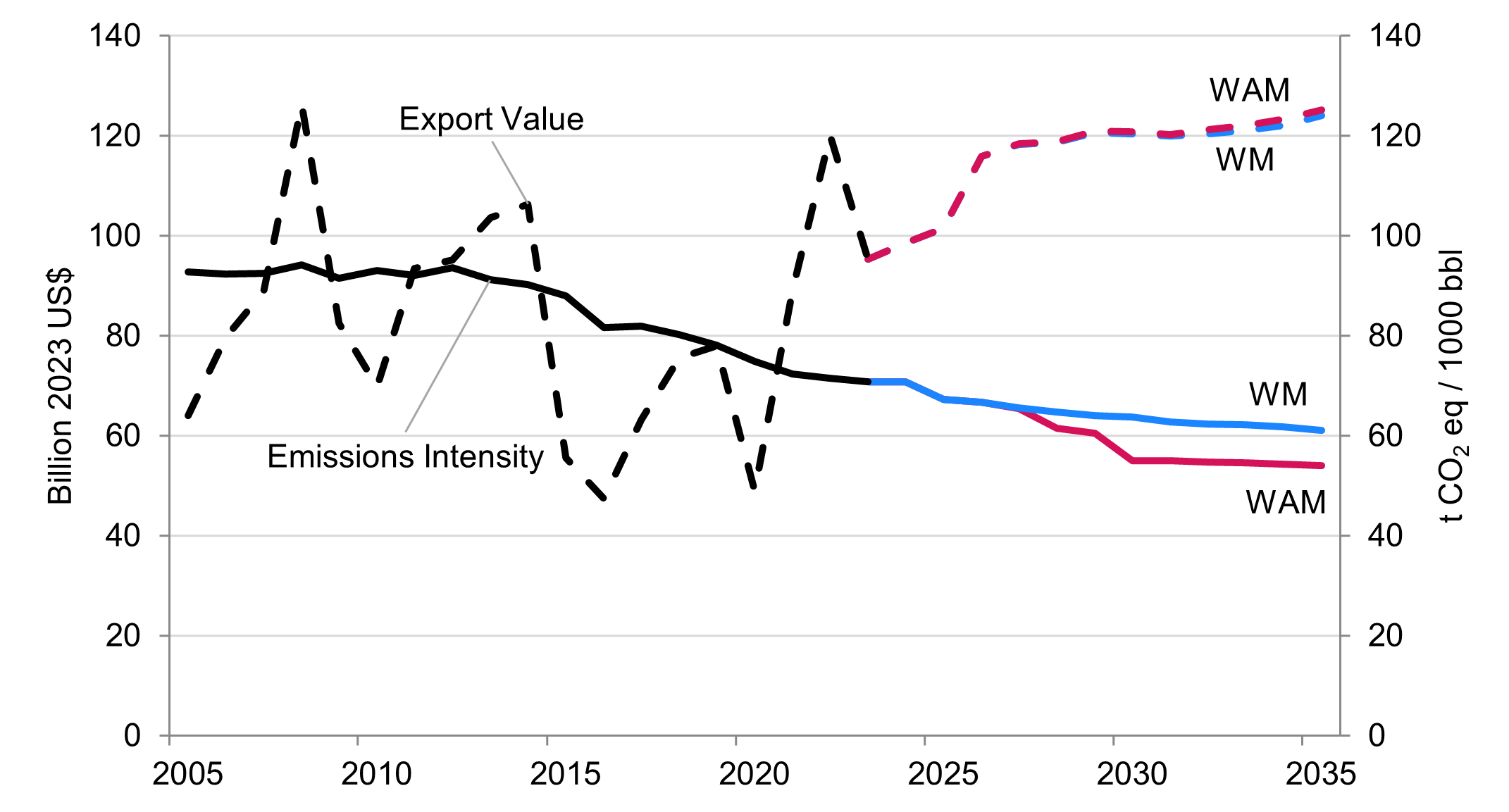

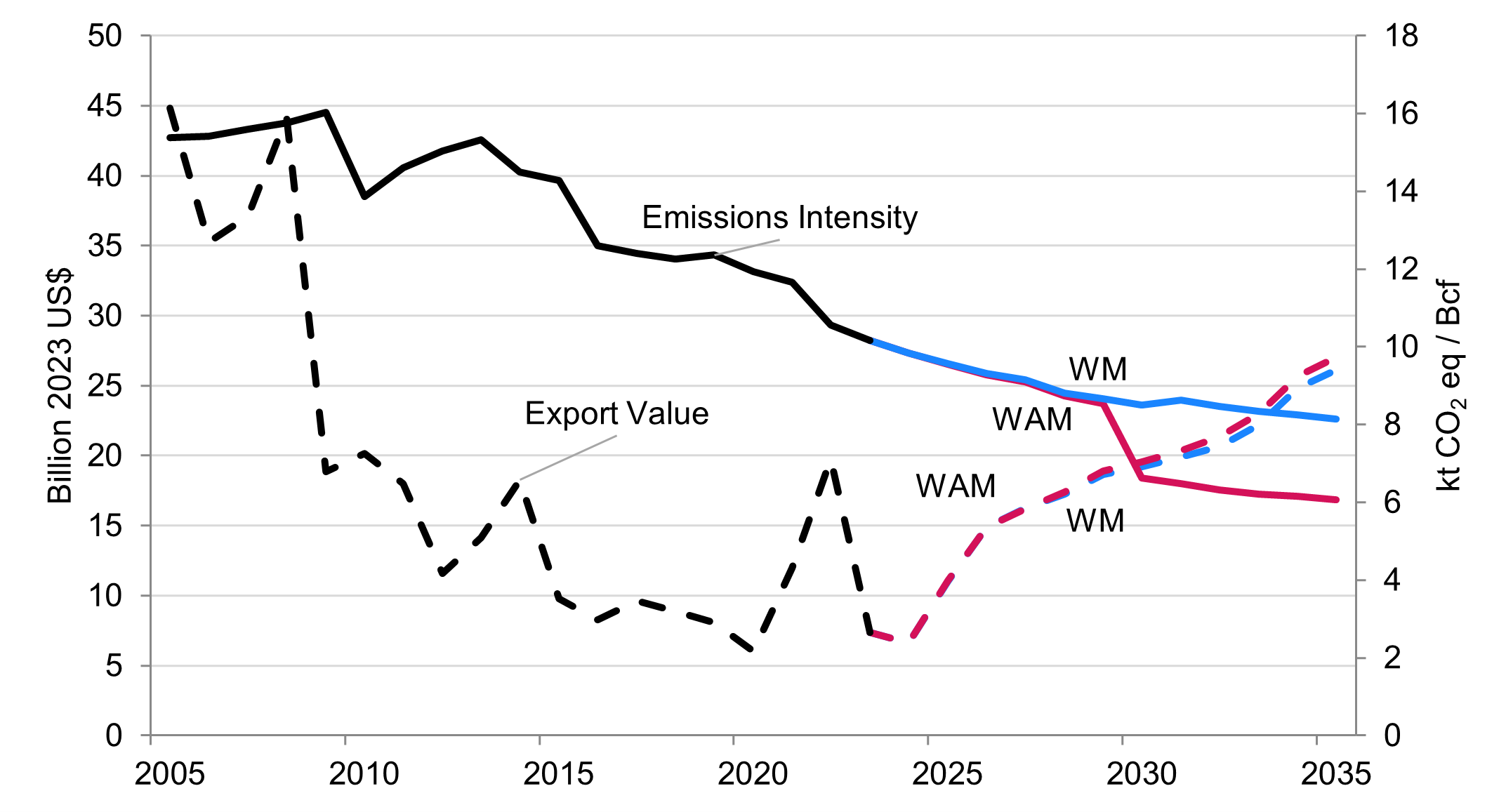

As outlined in the Climate Competitiveness Strategy, the Government of Canada “will develop and communicate new metrics to show how companies and households are reducing their carbon footprint, how the clean economy is growing, and how exports are tracking to achieve world-leading emissions intensity.”

This first round of reporting focuses on emissions associated with oil and gas produced to meet international demand. Future iterations will progressively expand to other traded emissions sources, such as heavy industries, low-carbon fuels, and electricity. The decision to report on this sector first is based on the data that are currently available. Moving forward, Canada will continue to refine and expand its methodology for reporting on the emissions embodied in trade, notably from oil and gas, and will monitor how clean energy and technology exports support global decarbonization. Details about the methodology are provided in Section A1.5.

Figure 10 and Figure 11 show that between 2005 and 2035, emissions intensity of production for oil and gas decline, while the value of exports increases for oil in both the WM and WAM scenarios.