Annual Report 2016–2017: Fairness: A right, not a privilege

Publication Date: November 22, 2017

Our reports and publications are available in alternate and accessible formats

Office of the Taxpayers’ Ombudsman

600-150 Slater Street, Ottawa, ON K1A 1K3

Tel: 613-946-2310 | Toll-free: 1-866-586-3839

Fax: 613-941-6319 | Toll-free: 1-866-586-3855

© Minister of Public Works and Government Services Canada 2017

Cat. No.: Rv6

ISSN: 1924-5076

* This publication is also available in electronic format at canada.ca/en/taxpayers-ombudsman/.

Taxpayer Bill of Rights

The Taxpayer Bill of Rights defines 16 rights describing the treatment to which taxpayers are entitled when dealing with the Canada Revenue Agency (CRA). The Taxpayer Bill of Rights also sets out the CRA’s Commitment to Small Business to ensure interactions with the CRA are conducted as efficiently and effectively as possible. Within the Taxpayer Bill of Rights, the Taxpayers’ Ombudsman is responsible to uphold eight of these rights. These include rights 5, 6, 9, 10, 11, 13, 14, and 15 (in bold below).

- You have the right to receive entitlements and to pay no more and no less than what is required by law.

- You have the right to service in both official languages.

- You have the right to privacy and confidentiality.

- You have the right to a formal review and a subsequent appeal.

- You have the right to be treated professionally, courteously, and fairly.

- You have the right to complete, accurate, clear, and timely information.

- You have the right, unless otherwise provided by law, not to pay income tax amounts in dispute before you have had an impartial review.

- You have the right to have the law applied consistently.

- You have the right to lodge a service complaint and to be provided with an explanation of our findings.

- You have the right to have the costs of compliance taken into account when administering tax legislation.

- You have the right to expect us to be accountable.

- You have the right to relief from penalties and interest under tax legislation because of extraordinary circumstances.

- You have the right to expect us to publish our service standards and report annually.

- You have the right to expect us to warn you about questionable tax schemes in a timely manner.

- You have the right to be represented by a person of your choice.

- You have the right to lodge a service complaint and request a formal review without fear of reprisal.

Commitment to Small Business

- The CRA is committed to administering the tax system in a way that minimizes the costs of compliance for small businesses.

- The CRA is committed to working with all governments to streamline service, minimize cost, and reduce the compliance burden.

- The CRA is committed to providing service offerings that meet the needs of small businesses.

- The CRA is committed to conducting outreach activities that help small businesses comply with the legislation we administer.

- The CRA is committed to explaining how we conduct our business with small businesses.

Message from the Taxpayers’ Ombudsman

Overseeing service in a service-oriented society

Proactive service delivery

Proactive service delivery is important and is a culture. Being proactive with service delivery means constantly seeking ways to give the best service possible and to make improvements and changes before there are problems. During the past fiscal year, we worked on being proactive. We proactively worked on improving our processes so we can improve our service. While we deal reactively with individual complaints we receive about the service provided by the CRA, we proactively seek opportunities to find out about service issues. We do this by reaching out to taxpayers and those who assist taxpayers to learn about issues they face. We monitor media and external sources for changes and issues that may have an impact on service from the CRA. We communicate proactively with the CRA about initiatives they have or changes being made that could affect service. We created a new mechanism to request a change in service, called a Request for Service Improvement, which will allow us to raise potential service improvements that are not specifically part of an individual complaint, do not require a systemic examination and recommendation to the Minister of National Revenue, but may impact more taxpayers.

In the future, it will be important that my Office continues to foster collaborative relationships with organizations supporting taxpayers who have difficulty accessing services, the tax professional community of tax lawyers and accountants, and the CRA. These relationships will allow my Office to monitor changes and initiatives that may affect the service provided by the CRA, and to continue to find out about issues or potential issues as early as possible. We will also be monitoring recommendations previously made by my Office, to work toward ensuring effective changes were made and the issues identified do not climb to the forefront of current issues affecting taxpayers.

Reaching taxpayers across Canada

I am pleased to say that in the 2016-2017 fiscal year, I completed the first phase of my outreach tour, visiting every province and territory in the country. I am proud of the effort made by my Office to reach out to taxpayers and the organizations helping them. Serving taxpayers in the resolution of disputes between them and the CRA is a significant undertaking, but a challenge I am happy to accept.

Reaching out to taxpayers has provided me with insight on the issues affecting taxpayers in the various regions across Canada, and to hear their stories and bring information back to my Office to conduct preliminary research. This outreach, as well as speaking engagements at conferences, has increased the visibility of my Office and the understanding taxpayers have of my role as the Taxpayers’ Ombudsman. We are working to continue to diversify our engagement opportunities to raise awareness about my Office and to hear about service issues affecting taxpayers. By establishing open lines of communication with taxpayers and our stakeholders, we can better address the service provided by the CRA, and ensure fairness is a right, not a privilege, for all taxpayers.

Sherra Profit

Taxpayers' Ombudsman

About us

The mandate of the Taxpayers’ Ombudsman

As outlined in the Order in Council P.C. 2007-0828, the Taxpayers’ Ombudsman’s (the Ombudsman) mandate is to assist, advise, and inform the Minister of National Revenue (the Minister) about any matter relating to services provided to a taxpayer by the Canada Revenue Agency (CRA).

The Ombudsman:

- reviews and addresses any request for a review about a service matter or a matter arising from the application of sections 5, 6, 9, 10, 11, 13, 14, and 15 of the Taxpayer Bill of Rights;

- identifies and reviews emerging and systemic issues related to service matters that impact taxpayers negatively;

- facilitates access by taxpayers to the proper redress mechanisms within the CRA to address service matters; and

- provides information to taxpayers about the mandate of the Ombudsman.

The Ombudsman reviews service issues at the request of the Minister, on receipt of a complaint from a taxpayer or their representative, or on her own initiative.

The Ombudsman does not review:

- matters that arose before February 21, 2007, unless the request is made by the Minister;

- the administration or enforcement of CRA program legislation, unless the review relates to service matters;

- Government of Canada legislation, policy, or CRA policy, unless the review relates to service matters;

- the CRA’s administrative interpretation of a provision within its program legislation;

- matters before the courts or court decisions;

- legal advice provided to the Government of Canada; and

- confidences of the Queen’s Privy Council for Canada.

Our mission

Our mission is to increase awareness about our services, influence positive changes to the services provided by the CRA, and to ensure taxpayers have access to trusted, fair, and independent resolution of complaints about the CRA’s service.

Our guiding principles

Independence

Our Office operates at arm’s length from the CRA and the Ombudsman is accountable to the Minister, not the CRA. The Ombudsman is free to form her own opinion, independent of the CRA’s opinions. This freedom allows her to make the recommendations she believes are necessary to resolve a service issue, and to choose the audience(s) that will receive the greatest benefit from her outreach activities.

Impartiality

Our role is not to be an advocate for taxpayers or a defender of the CRA. We collect the facts from the taxpayer, the CRA, and any other relevant source. We examine those facts in a neutral and objective manner. Based upon the facts, we determine whether there is a service issue and identify a solution or make recommendations to correct it.

Fairness

Our Office reviews each service complaint on a case-by-case basis. We take into consideration all factors affecting the taxpayer and their situation. We act on the information in an unbiased manner and ensure the CRA applies its policies and procedures in a manner to ensure consistent outcomes for everyone.

Confidentiality

We do not disclose any confidential information to anyone, including the CRA, without the taxpayer’s consent. Likewise, the CRA will only disclose information to our Office with the taxpayer’s consent.

Who we serve

We serve taxpayers, whom we define as individuals, businesses, corporations, charities, and other legal entities that are subject to Canadian tax statutes, eligible to receive an amount as a benefit, or provided a service by the CRA. The Ombudsman also provides service to the Minister, by advising her on any matter relating to the service provided to taxpayers by the CRA and making recommendations to correct or improve a service issue.

Our services

One of the objectives of the service complaint process is to resolve complaints at the lowest possible level. Our Office assesses whether taxpayers have followed the steps of the CRA’s service complaint process and if not, provides the taxpayer with information on how to seek a resolution for their particular issue. If our Office receives a complaint that is not within our mandate, we refer the taxpayer and facilitate their access to the appropriate area for redress.

Image description

The steps in the service complaint process are:

- Step 1 - attempt to resolve the complaint with the CRA employee or their supervisor.

- Step 2 - file a service complaint with the CRA Service Complaint Program.

- Step 3 - if the taxpayer is not satisfied with the CRA’s decision, submit the service complaint to our Office for review.

Examinations of service issues come in two forms: individual examinations and systemic examinations. Our Office receives complaints from taxpayers relating to specific service issues they have experienced during their interactions with the CRA. If we receive a complaint, or several complaints, that may negatively impact a segment of the population or a large number of taxpayers, the Ombudsman may initiate a systemic examination of these issues. Systemic issues may also be brought to the attention of the Ombudsman through outreach, environmental scanning, or by request of the Minister.

Our mandate allows us to examine a service complaint only after the CRA’s internal redress mechanisms have been exhausted, unless there are compelling circumstances. A compelling circumstance may exist when:

- the taxpayer’s complaint raises a systemic issue;

- following all the steps of the service complaint process may cause undue personal or financial hardship to the taxpayer; or

- following all the steps of the service complaint process is unlikely to resolve the complaint within a period of time the Ombudsman considers reasonable.

Our accountability and our governance

Reporting annually

Under subsection 9(2) of Order in Council P.C. 2007-0828, the Ombudsman is required to submit to the Minister and the Chair of the Board of Management before December 31 of each year an annual report on the activities of the Office for the preceding fiscal year. The Minister tables the annual report in each House of Parliament. Under subsection 9(3), the Ombudsman publishes the annual report as soon as it is tabled by the Minister.

Governance

Our Office is functionally independent and operates at arm’s length from the CRA. However, our governance framework for the management of financial and human resources is rooted within the CRA’s governance framework.

Financial authorities

The Ombudsman and employees of our Office are required to comply with the financial management policies issued by the Treasury Board of Canada Secretariat (TBS) under the Financial Administration Act, and the CRA policy framework reflecting those policies.

Proactive disclosure

Compliance with the TBS and CRA financial management policies requires the mandatory publication of the Ombudsman’s travel and hospitality expenses. It also requires disclosure of contracts entered into by our Office for amounts over $10,000.

The disclosure is published on our website and the TBS website, which includes a link to our Office’s information under its "Proactive disclosure by department or agency"Footnote 1 webpage.

Human resources authorities

The Commissioner of the CRA, who is authorized by the Canada Revenue Agency Act to exercise human resources related powers, duties, and functions, formally delegated the authority and management of human resources to the Ombudsman.

In accordance with subsection 3 of the Order in Council, employees of our Office are employed pursuant to the Canada Revenue Agency Act. Therefore, the Ombudsman and employees of the Office are bound by the CRA’s human resources policies and programs.

Year in review

Measuring our performance

Our Office has established key performance indicators for the 2016-2017 Performance Measurement Framework.Footnote 2 As our business matures and our internal processes change, we review and adjust the language of the indicators, when necessary, to determine the overall success of these changes and ensure we are reporting on current processes.

| Key performance indicators for 2016-2017 | Target | Actual |

|---|---|---|

| Percentage of recommendations raised by the Taxpayers’ Ombudsman that will be acted upon by the Canada Revenue Agency | 90% | 100% |

| Percentage of taxpayer complaints acknowledged within two business days | 95% | 95% |

| Percentage of service-related complaints resolved prior to investigationFootnote 3 | 75% | 74% |

| Percentage of requests for action or information from the Office of the Taxpayers’ Ombudsman that are acted upon by the CRA | 90% | 100% |

Figure 4.1 Performance indicators for the Office of the Taxpayers’ Ombudsman, including our target and actual performance.

We did not meet our third performance indicator due to a change in our process during the year. Previously, when a taxpayer had not first filed their complaint with the Canada Revenue Agency’s Service Complaints Program (CRA-SC), and there were no compelling circumstances, our intake officers would refer the complaint to the CRA-SC and close our file. In our case tracking system, this was closed as resolved prior to examination. If the taxpayer was not satisfied with the result of the CRA-SC review of their complaint, we would reopen the file and have an examination officer address the complaint.

To provide better service to taxpayers, we made the decision to keep these files open when they were sent to the CRA-SC and to follow-up to ensure whether the taxpayer was satisfied with the result of the CRA-SC review of their complaint. Once those complaints are reviewed by the CRA-SC, if the taxpayer is satisfied with the result, our file is closed as resolved prior to examination. If the taxpayer is not satisfied with the result, the file is transferred to an examination officer. Therefore, where all of those files would have previously been recorded as resolved prior to examination and then reopened, they are remaining open through to the completion of the examination.

| Expenditures | 2016-2017 ($000) |

|---|---|

| Salaries | 2,125 |

| Professional services | 40 |

| Non-professional services | 29 |

| Training and education | 29 |

| Travel | 36 |

| Office equipment | 24 |

| Printing and publishing | 7 |

| Office expenses | 15 |

| Total annual operating expenses | 2,305 |

Figure 4.2 Summary of financial expenditures for the 2016 2017 fiscal year.

Examining individual complaints

Our officers conduct independent, impartial reviews of the service complaints we receive. They review the facts provided by the taxpayer, the CRA, or any other relevant source to facilitate a resolution of the issue(s).

For ongoing examinations, we provide regular updates to the taxpayer on the status of the examination. When the examination reveals the service provided by the CRA was not adequate, we work with the taxpayer and the CRA to find a resolution. Sometimes, resolution is achieved simply, by re-establishing communication or clarifying information from the CRA. When the examination is completed, we inform the taxpayer of our findings and the actions we took, if any, to resolve the service issue.

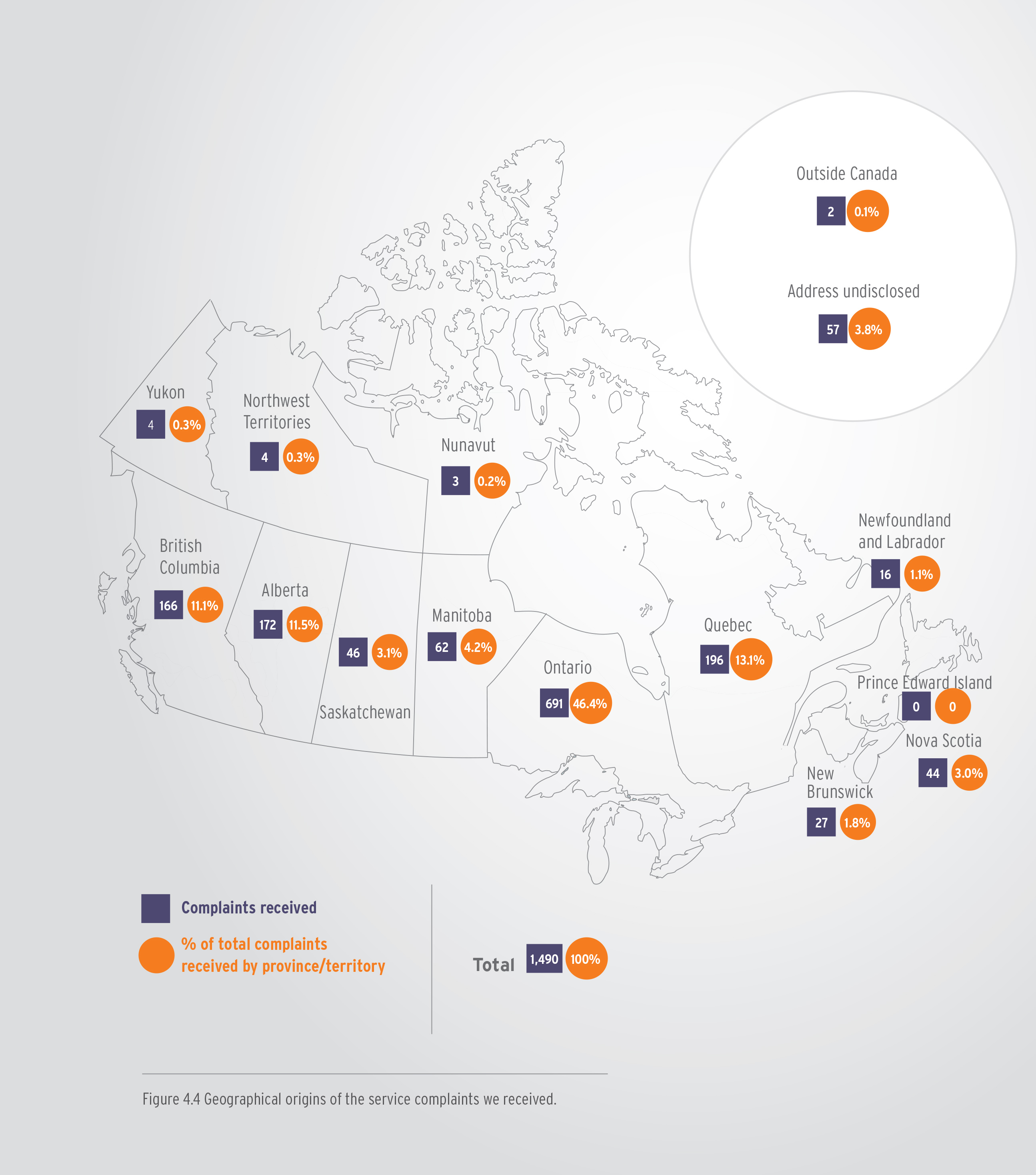

Regardless of the method used to contact our Office, these service complaints come to us from across Canada and internationally. Learning about the geographic origins of complaints helps us to identify possible outreach opportunities to increase the public’s awareness of our services. Of the 1,490 complaint files opened during the 2016-2017 fiscal year, 46.4% of those complaints came from Ontario, 13.1% from Québec, and 11.5% from Alberta.

Image description

| Location | Complaints received | % of total complaints received by province/territory |

% of Canadian population by province/territory |

|---|---|---|---|

| Alberta | 172 | 11.5 | 11.7 |

| British Colombia | 166 | 11.1 | 13.1 |

| Manitoba | 62 | 4.2 | 3.6 |

| New Brunswick | 27 | 1.8 | 2.1 |

| Newfoundland and Labrador | 16 | 1.1 | 1.5 |

| Northwest Territories | 4 | 0.3 | 0.1 |

| Nova Scotia | 44 | 3.0 | 2.6 |

| Nunavut | 3 | 0.2 | 0.1 |

| Ontario | 691 | 46.4 | 38.6 |

| Prince Edward Island | 0 | 0 | 0.4 |

| Québec | 196 | 13.1 | 22.9 |

| Saskatchewan | 46 | 3.1 | 3.2 |

| Yukon | 4 | 0.3 | 0.1 |

| Address undisclosed | 57 | 3.8 | N/A |

| Outside Canada | 2 | 0.1 | N/A |

| Total | 1,490 | 100 | 100 |

Figure 4.4 Geographical origins of the service complaints we received.Footnote 4

How we resolved the issues

When closing files, we close each issue separately. Some files have more than one issue. During the 2016-2017 fiscal year, 1,611 issues were closed. Following is a breakdown of the issues closed in the 2016-2017 fiscal year.

We often receive complaints from taxpayers as a first attempt at resolving their service issue. In 2016-2017, 964 issues within our mandate were brought to our attention, but had not first been addressed by the CRA-SC. We referred 369 of those issues to the CRA-SC on the taxpayer’s behalf. Another 202 issues were referred to the CRA for its urgent action; mainly as a result of compelling circumstances, such as financial hardship. Our Office closed 129 issues because taxpayers did not respond to our requests for additional information, 95 issues were withdrawn by the taxpayer, and 87 issues were awaiting resolution by a third party (taxpayer relief, audit, or appeals, for example). We learned of 34 issues already resolved through a CRA recourse mechanism requiring no further action by our Office. Taxpayers may copy our Office on correspondence sent to another area to raise our awareness of an issue, but the complaint is not formally filed with our Office. These awareness raising complaints accounted for 35 issues in total. Examples of the remaining issues included requests about general enquiries, and the inability of our Office to reach taxpayers for a follow-up due to incorrect contact information.

An issue with merit is one where the taxpayer submitted their original complaint to the CRA and received a reply with which they were unsatisfied, we did an examination of the complaint, and determined there was a service issue on the part of the CRA. Issues with merit are resolved by our Office making a recommendation to the CRA (15), the CRA taking corrective action upon being made aware of the service issue (21), or our Office submitting a request to the CRA asking for an action to be taken (9). In some circumstances, the issues are resolved without our Office making formal recommendations to the CRA. The CRA may provide clarifying information to the taxpayer, we help re-establish contact between the taxpayer and the CRA, or our raising of the issue with the CRA facilitates a resolution (76).

Case summaries

The following case summaries provide examples of the types of complaints submitted by taxpayers.Footnote 5

Case summary #1 – Influencing the coordination of reassessments

Taxpayer A filed a personal income tax return and a Goods and services tax (GST)/Harmonized sales tax (HST) return for their business. They were subject to a review of their personal income tax return, resulting in a reassessment of the return. As a result of personal income tax return reviews, their GST/HST returns were reassessed as well. They received notices of reassessments for both returns. Taxpayer A disagreed with the CRA and filed an objection for the reassessment of their personal income tax return. They were under the impression that, as a result of filing an objection for their first return, the objection would result in an automatic review of their GST/HST return as the incomes were related, were for the same tax year, and the GST/HST return reassessment was a result of the reassessment of the personal income tax return.

In their service complaint to our Office, Taxpayer A stated they were not previously informed of the need to file objections for both reassessments. Taxpayer A informed our Office it was only later in their discussions with the CRA that it notified them of the need to file a separate objection for the GST/HST reassessment. By the time they were notified of the need for a separate objection, the 90-day period to file an objection for their GST/HST reassessment had passed. As they were not within a year of the expiry of the objection period, an application to extend time to object could not have been granted.

Taxpayer B disagreed with both reassessments. They filed an objection with Revenu Québec, but not with the CRA, as the taxpayer was under the impression the CRA accepted an objection verbally during a telephone conversation. However, during the same telephone call, the CRA misunderstood and thought the objection filed by the taxpayer was not to Revenu Québec, but rather to the CRA. By the time the misunderstandings were cleared up, it was too late for the taxpayer to file the objection with the CRA or apply for an extension of time. Taxpayer B’s objection with Revenu Québec resulted in part of their claim being allowed. The CRA advised our Office that Taxpayer B must submit a request for an adjustment to the CRA so that it could apply the same changes. Taxpayer B claimed to have done so by way of an adjustment request.

We worked with the CRA to facilitate the processing of the reassessment based on Revenu Québec’s reassessment. Once the taxpayer received their new reassessment, we informed Taxpayer B they had 90 days to file an objection with the CRA and to request a review of the full amount of the business loss they originally claimed.

Examining systemic service issues

A systemic examination arises when an issue is identified that may impact a large number of taxpayers or a segment of the population. Our Office conducts reviews of the individual service complaints and telephone calls received, with the goal of identifying possible trends. We engage our Consultative Committee, tax professionals, academia, community support organizations, and continuously scan media sources to assist in identifying systemic issues. Also, the Minister may request we examine a particular systemic issue.

Top systemic trends for the 2016-2017 fiscal year

The trends analysis conducted by our Office was completed based on the issues identified from telephone calls or at the outset of complaints. This analysis does not take into account other issues identified after further discussions between taxpayers and our officers, or how many complaints were later found to be with or without merit.

During the 2016-2017 fiscal year, we identified the following as the most frequently raised systemic issues, either through the submission of taxpayer complaints or telephone calls:

- Inconsistent/incorrect information from the CRA, including unclear and confusing CRA decisions, general enquiries agents providing contradictory information, the CRA requesting the same documentation multiple times, and lack of clarity in the CRA’s correspondence;

- Issues with debt collection programs, including collection officer behaviour, lack of legal warnings, and garnishments;

- Delays in processing income tax and benefit returns;

- Taxpayers having difficulties providing proof of their eligibility for the Canada child benefit;

- Difficulties reaching the CRA via telephone; and

- Delays in processing T1 adjustment requests.

The systemic examination process

Systemic report - Rights and Rulings: Understanding the Decision

Our findings

Our Office found although the rulings letters provide information about the recipient’s right to appeal, they do not provide a sufficient explanation to understand the reasons for the CRA’s decision or the potential consequences resulting from a change in the employment relationship. As a result of preliminary consultations with the CRA, the CPP/EI Rulings Program agreed to improve the information in its rulings letters by adding a reference to its webpage "Have you received a CPP/EI ruling?"

As no explanations are provided in the CPP/EI rulings letters, we found workers or payers have only two ways to receive an explanation: either the worker or payer can call the officer who issued the ruling and request a verbal explanation; or they can request a copy of the CPP/EI Rulings Report. However, for workers or payers to take advantage of these two options, they must be aware these options exist. While the letters provided the contact name and telephone number of the officer who made the rulings decision, there was no mention the worker or payer could request a copy of the CPP/EI Rulings Report.

The Ombudsman’s recommendations

Based on the findings of the examination, the Ombudsman recommended to the Minister that:

- the CRA provide information in the CPP/EI rulings letters indicating to workers and payers that they have the right to request a copy of the CPP/EI Rulings Report, and provide instruction on how to request it;

- where applicable, the CPP/EI rulings letters inform the workers and payers an amount owing or over-contribution may result from the decision;

- the CRA updates the relevant sections of its publications and webpages to clearly communicate with workers and payers involved in a CPP/EI ruling about what they need to do after a ruling is made, including the steps required to pay any outstanding CPP contributions and/or EI premiums;

- the CRA continue to include in its CPP/EI rulings letters:

- the name and telephone number of the rulings officer and an invitation to contact the rulings officer to receive an explanation of the decision;

- a reference to the "Have you received a CPP/EI ruling?" webpage; and

- the CRA determine whether changes can be made to increase efficiencies to allow for the inclusion of an explanation of the relevant factors within each rulings letter.

Open systemic examinations

Examination of the delays in resolving requests for taxpayer relief

In February 2010, the CRA began work on a transformation initiative to centralize the review of taxpayer relief requests to improve governance, consistency, and control. As a result of this initiative, the workload was streamlined as a program under the responsibility of the Appeals Branch. However, after this transformation was completed in April 2012, our Office continued to receive complaints from taxpayers citing delays in the processing of their requests for taxpayer relief. Some taxpayers also stated they were not receiving acknowledgement from the CRA after a relief request was submitted. Taxpayers were uncertain if the CRA received their request or if they should re-submit their request for relief to the CRA. As a result, a systemic examination was opened to look into these issues.

The systemic report is expected to be submitted to the Minister and published in the fall 2017.

Collections procedures pertaining to legal warnings

In February 2017, the Ombudsman notified the Minister our Office was opening a systemic examination into the service issues arising from complaints received about the CRA’s collection procedures with respect to issuing legal warnings to taxpayers.

We heard from taxpayers who alleged the CRA either froze their bank accounts or garnished their wages without first notifying them. Some of these taxpayers expressed their surprise at the extent with which the CRA would go to recover the debts, as these actions may have serious financial or legal consequences for the taxpayer.

Preliminary research into potential systemic issues

During the 2016-2017 fiscal year, our systemic examination officers began preliminary research into various issues brought to our attention through trends analysis of the complaint files submitted to our Office, topics brought to our attention during outreach activities, or at the request of the Minister.

Delays in processing the Canada child benefit applications for newcomers to Canada

Through media attention and a preliminary report from the Senate Human Rights Committee, our Office was alerted to the potential issue of delays in the processing of Canada child benefit (CCB) applications for newcomers to Canada.

We reviewed complaints related to the processing of CCB applications, media reports, and information from the CRA. During our review, we considered the CRA’s timeliness in its processing of CCB applications and related issues, such as the CRA’s approach to fluctuating inventories, which could impact the overall administration of the program.

According to our research, the CRA is exceeding its published service standard for processing times and has processes in place to deal with varying inventories. We found the CRA is also working closely with other government departments to resolve issues, including Immigration, Refugees, and Citizenship Canada. Through its outreach and research activities, the CRA is encouraging new applicants to take full advantage of this benefit. It has also taken measures to make specific messaging and products available about the CCB.

As we have done with other issues and examinations, both opened and closed, our Office will continue to monitor if similar issues are raised in the future or if new issues are brought to our attention.

Female presumption rule and the Canada child benefit

We received complaints from male primary caregivers attempting to claim the CCB, regarding the female presumption rule. The application of this rule automatically defers family benefits to the female partner’s name, even if that person is not the primary caregiver or is the step-parent to the children. These applicants alleged this rule is causing them hardship, as it requires them to prove they are the primary caregiver of their children. They allege this burden of proof does not exist for female benefit recipients.

Upon reaching out to the CRA and receiving additional information, the Ombudsman decided not to open an examination at this time. We will continue to monitor if similar issues are raised in the future or if new issues are brought to our attention.

Northern residents deductions

During the Ombudsman’s outreach to communities in northern Canada, taxpayers conveyed concerns regarding the clarity of the forms used to calculate the Northern residents deductions and the confusion these may cause to some taxpayers. Once they complete and submit these forms to the CRA with their tax returns, claimants allege they are experiencing more frequent reviews, reassessments, or audits than other Canadians.

Our Office requested information from the CRA to better understand the issues related to this credit. Our preliminary research found the CRA has a number of initiatives underway that could potentially remedy the issues we identified. As a result, the Ombudsman decided not to open an examination at this time and will follow-up with the CRA over the next fiscal year to determine whether the CRA’s actions address the issues raised.

Connecting with the CRA through the general enquiries lines

Our Office has received numerous complaints from taxpayers and representatives in recent years, claiming it is very difficult to connect with the CRA’s general enquiries telephone lines. A recurring complaint from taxpayers is they reach a busy signal, regardless of the time of the day they call, forcing them to make multiple calls.

Given the announcement of increased funding for telephone access and initiatives underway by the CRA, our Office is not opening an examination at this time, but we are monitoring this issue.

Communication and outreach: A two-way street

Raising awareness of the role of the Ombudsman and the work conducted by our Office is an important part of the outreach activities being performed. Reaching out to taxpayers across Canada through engagement sessions with community support organizations, or participating at conferences and trade shows by speaking on stage or at our booth are important factors toward making the activities of our Office known.

Connecting with the international ombudsman community

In March 2017, the Ombudsman attended the International Conference on Taxpayer Rights. This presented an opportunity to connect with colleagues who oversee services provided to taxpayers in other jurisdictions. At the conference, she heard about key initiatives and best practices surrounding privacy and transparency, the establishment of frameworks for taxpayer rights, the protection of taxpayer rights in multi-jurisdictional disputes, access to rights and quality service at a time of fiscal responsibility, and building cultures of trust between tax agencies and taxpayers. The information learned and exchanged with colleagues offer our Office insights into issues affecting taxpayers and the services they receive from the CRA.

Modernizing our web presence

Improving the corporate environment

Our corporate services provide support to our Office, in compliance with all the related legislated requirements of the Government of Canada, in corporate planning and reporting, financial management, human resources management, information management, information technology management, and procurement.

To ensure efficient and effective service delivery to taxpayers, the experience, skill sets, and knowledge of our employees is only part of the equation. Employees also need to have the proper training and the necessary tools to manage and complete their work. In 2016-2017, our Office launched a major initiative to replace our complaint case management system. The case management system tracks all taxpayer telephone calls and complaints. Planning, development, and intensive testing took place throughout 2016-2017.

How to contact us

Contacting the Office of the Taxpayers’ Ombudsman

- Within Canada and the United States, call toll-free 1-866-586-3839 or fax us at 1-866-586-3855

- Outside Canada and the United States, call collect +1-613-946-2310 or fax us at +1-613-941-6319.

- Visit our website canada.ca/en/taxpayers-ombudsman

- Write to us

Office of the Taxpayers’ Ombudsman

600-150 Slater Street

Ottawa, ON K1A 1K3

Canada

- Make an appointment for an in-person meeting.

Office hours

Our Office hours are 8:15 a.m. to 4:30 p.m. Eastern Standard Time, Monday to Friday (except holidays).

How to follow us

To stay informed on our activities:

- follow us on Twitter @OTO_Canada;

- subscribe to our electronic mailing list; or

- add our RSS feed to your feed reader.