Chapter 2: Impact and effectiveness of Employment Insurance benefits (Part I of the Employment Insurance Act)

From: Employment and Social Development Canada

Official title: Employment Insurance Monitoring and Assessment Report for fiscal year beginning April 1, 2018 and ending March 31, 2019: Chapter 2: Impact and effectiveness of Employment Insurance benefits (Part I of the Employment Insurance Act)

In chapter 2

- List of abbreviations

- Introduction – Chapter 2

- 2.1 Employment Insurance benefits overview

- 2.2 Employment Insurance regular benefits

- 2.3 Employment Insurance support while on training

- 2.4 Employment Insurance fishing benefits

- 2.5 Employment Insurance Work-Sharing benefits

- 2.6 Employment Insurance special benefits

- 2.7 Employment Insurance financial information

List of abbreviations

This is the complete list of abbreviations for the Employment Insurance Monitoring and Assessment Report for the fiscal year beginning April 1, 2018 and ending March 31, 2019.

Abbreviations

- ASETS

- Aboriginal Skills and Employment Training Strategy

- ATSSC

- Administrative Tribunals Support Service of Canada

- B/C Ratio

- Benefits-to-Contributions ratio

- B/U Ratio

- Benefits-to-Unemployed ratio

- B/UC Ratio

- Benefits-to-Unemployed Contributor ratio

- BDM

- Benefit Delivery Modernization

- CANSIM

- Canadian Socio-Economic Information Management System

- CAWS

- Citizen Access Workstation Services

- CCAJ

- Connecting Canadians with Available Jobs

- CCB

- Canada Child Benefit

- CCDA

- Canadian Council of Directors of Apprenticeship

- CEIC

- Canada Employment Insurance Commission

- COLS

- Community Outreach and Liaison Service

- CSO

- Citizen Service Officer

- CPI

- Consumer Price Index

- CPP

- Canada Pension Plan

- CRA

- Canada Revenue Agency

- CRF

- Consolidated Revenue Fund

- CUSMA

- Canada-United States-Mexico Agreement

- CX

- Client Experience

- EBSMs

- Employment Benefits and Support Measures

- ECC

- Employment Contact Centre

- EF

- Enabling Fund

- EI

- Employment Insurance

- EI PAAR

- Employment Insurance Payment Accuracy Review

- EI PRAR

- Employment Insurance Processing Accuracy Review

- EICS

- Employment Insurance Coverage Survey

- eROE

- Electronic Record of Employment

- ESDC

- Employment and Social Development Canada

- FLMM

- Forum of Labour Market Ministers

- FY

- Fiscal Year

- G7

- Group of Seven

- GDP

- Gross Domestic Product

- HCCS

- Hosted Contact Centre Solution

- HRSDC

- Human Resources and Social Development Canada

- IQF

- Individual Quality Feedback

- IVR

- Interactive Voice Response

- LFS

- Labour Force Survey

- LMDA

- Labour Market Development Agreements

- LMI

- Labour Market Information

- LMP

- Labour Market Partnerships

- MIE

- Maximum Insurable Earnings

- MSCA

- My Service Canada Account

- NAICS

- North American Industry Classification System

- NAFTA

- North American Free Trade Agreement

- NAS

- National Apprenticeship Survey

- NERE

- New-Entrant/Re-Entrant

- NESI

- National Essential Skills Initiative

- NIS

- National Investigative Services

- NOS

- National Occupational Standards

- NQCP

- National Quality and Coaching Program for Call Centres

- OAS

- Old Age Security

- OECD

- Organization for Economic Co-operation and Development

- PPEs

- Clients who are Premiums Paid Eligible

- P/Ts

- Provinces and Territories

- PPTS

- Percentage points

- PRP

- Premium Reduction Program

- QPIP

- Quebec Parental Insurance Plan

- RAIS

- Registered Apprenticeship Information System

- ROE

- Record of Employment

- RSOS

- Red Seal Occupational Standards

- SA

- Social Assistance

- SCC

- Service Canada Centres

- SDP

- Service Delivery Partner

- SEPH

- Survey of Employment, Payrolls and Hours

- SIN

- Social Insurance Number

- SIR

- Social Insurance Registry

- SME

- Small and medium sized enterprises

- SO

- Scheduled Outreach

- SST

- Social Security Tribunal

- STDP

- Short-term disability plan

- SUB

- Supplemental Unemployment Benefit

- UV

- Unemployed-to-job-vacancy ratio

- VBW

- Variable Best Weeks

- VER

- Variable Entrance Requirement

- WWC

- Working While on Claim

Introduction – Chapter 2

This chapter of the Employment Insurance Monitoring and Assessment Report assesses income support provided by Employment Insurance (EI) Part I benefits:

- regular benefits

- fishing benefits

- Work-Sharing benefits

- special benefits

This chapter includes several key indicators, such as the number of new claims established, total amount paid, level of benefits, maximum duration and actual duration of benefits as well as the exhaustion of benefits. Throughout the chapter, key EI program provisions and recent changes made to the EI program are discussed. Indicators related to level of claims and level of benefits are presented for claims established within the fiscal year for which at least 1 dollar in EI benefits was paid. Meanwhile, indicators like maximum and actual duration are based on claims completedFootnote 1 during the fiscal year for which at least 1 dollar was paid in EI benefits. Indicators related to amount of EI benefits paid are presented on a cash basis, which means the expenses are accounted for during the fiscal year in which they are paid. More information on the definitions of the indicators presented throughout this chapter can be found in Annex 2.1 of this report.

This chapter relies on several sources of information to provide a comprehensive analysis of the EI program. EI administrative data, generally based on a 10% sample, underpins the majority of the analysis in this chapter. Some sections of this chapter also make use of tax data provided by the Canada Revenue Agency related to T4 tax slips with employment income or T1 returns. Statistics Canada's Employment Insurance Coverage Survey provides the basis for deeper analysis of coverage, eligibility and access of EI benefits for unemployed people. Throughout the chapter, data for the FY1819 is compared with data from previous years and, in some instances, long-term trends are discussed.

Annex 2 of the report presents additional statistical information on benefits analyzed in this chapter and Annex 7 provides an overview of major changes to the EI program between April 1996 and December 2019.

2.1 Employment Insurance benefits overview

In this section

- 2.1.1 Employment Insurance claims, amount paid and level of benefits

- 2.1.2 Combined Employment Insurance claims

- 2.1.3 Benefits-to-contributions ratios

The Employment Insurance (EI) program provides temporary income support to partially replace employment income for eligible unemployed contributors to the program while they look for new employment or upgrade their skills, and for those who are absent from work due to specific life circumstances, such as:

- sickness

- pregnancy

- providing care to a newborn or newly adopted child

- providing care and support to a critically ill family member, or

- providing end-of-life care to a family member with significant risk of death

In this chapter, EI benefits refer to regular benefits, special benefits, fishing benefits and Work-Sharing benefits (see Table 1). Special benefits include maternity benefits, parental benefits, sickness benefits, family caregiver benefits for adults or children, and compassionate care benefits. All EI benefit types are paid at a benefit rate of 55% of average weekly insurable earnings up to the maximum weekly benefit rate, except for extended parental benefits, which are paid at 33%. Subsection 2.1.1 covers the number of new claims established in the fiscal year, total amount paid over the fiscal year and benefit levels of claims established. Subsection 2.1.2 examines combined (or mixed) benefit claims. Subsection 2.1.3 provides an analysis of the usage of EI benefits relative to EI contribution premiums.

| Benefit type | Circumstance | Insurable employment entrance requirement | Maximum entitlement |

|---|---|---|---|

| Regular | Unemployed with a valid reason for separation and searching for suitable employment or retraining in certain cases | 420 to 700 hours depending on the Variable Entrance Requirement | 14 to 45 weeks, depending on insurable employment and regional unemployment rate1 |

| Fishing | Self-employed fishers without available work | Value of a catch between $2,500 and $4,200 depending on the Variable Entrance Requirement | 26 weeks per season (summer or winter) |

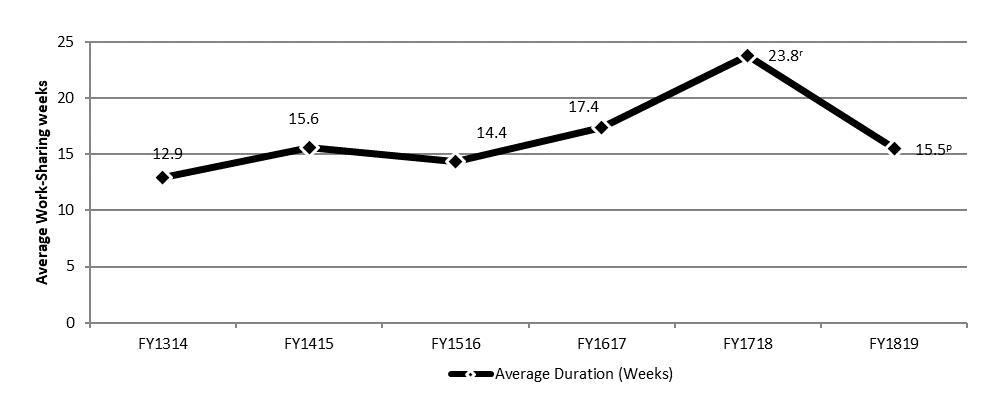

| Work-Sharing | Firm avoiding layoffs during a slowdown in business activity for reasons beyond the firm’s control with a recovery plan and a Work-Sharing agreement in place | 420 to 700 hours depending on the Variable Entrance Requirement and must be a year-round employee | 6 to 26 weeks, with the possibility of an extension by 12 weeks if warranted2 |

| Special3 - Maternity | Unavailable to work because of pregnancy or has recently given birth | 600 hours | 15 weeks |

| Special - Parental | Caring for a newborn or a newly adopted child | 600 hours | Standard parental: 35 weeks plus 5 additional weeks when benefits are shared4 Extended parental (at a lower replacement rate5): 61 weeks plus 8 additional weeks when benefits are shared4 |

| Special - Sickness | Unavailable to work because of illness, injury or quarantine | 600 hours | 15 weeks |

| Special - Family caregiver for children (formerly Parents of Critically Ill Children)7 | Providing care or support to a critically ill or injured child under the age of 18 | 600 hours | 35 weeks6 |

| Special - Family caregiver for adults | Providing care or support to a critically ill or injured person 18 years or older | 600 hours | 15 weeks6 |

| Special - Compassionate care | Providing care to a person of any age who requires end-of-life care | 600 hours | 26 weeks6 |

- 1 Budget Implementation Act, 2016, No. 1 extended the duration of EI regular benefits up to a maximum of 70 weeks of regular benefits for some claimants (see subsection 2.2.4 for further details on the measure).

- 2 Temporary Work-Sharing special measures were announced to support employers affected by the downturn in the forestry sector and the steel and aluminum sector. These measures extend the duration of Work-Sharing agreements across Canada from a maximum of 38 weeks to 76 weeks. The temporary special measure for the forestry sector came into effect on July 30, 2017 and will continue until March 28, 2020. The temporary special measure for the steel and aluminum sector came into effect on August 19, 2018 and will continue until March 27, 2021.

- 3 Self-employed workers (other than fishers) who have opted into EI special benefits must meet an insurable earnings threshold for the calendar year preceding the claim. The threshold was $6,947 for claims established in 2018 and $7,121 for claims established in 2019.

- 4 Since March 17, 2019, the EI parental sharing benefit provides 5 additional weeks to standard parental benefits and 8 additional weeks to extended parental benefits when parental benefits are shared between eligible parents.

- 5 As of December 3, 2017 parents can choose between standard parental benefits at a 55% replacement rate and extended parental benefits at a 33% replacement rate.

- 6 Benefits can be shared between eligible claimants. That is:

- parents, or

- family members

- 7 As of December 3, 2017 benefits for Parents of Critically Ill Children were improved and renamed "the family caregiver benefit for children". Since then child's parents and any qualifying members of the immediate and extended family who are eligible can claim the family caregiver benefit for children. Prior to that date, only parents could receive those benefits.

2.1.1 Employment Insurance claims, amount paid and level of benefits

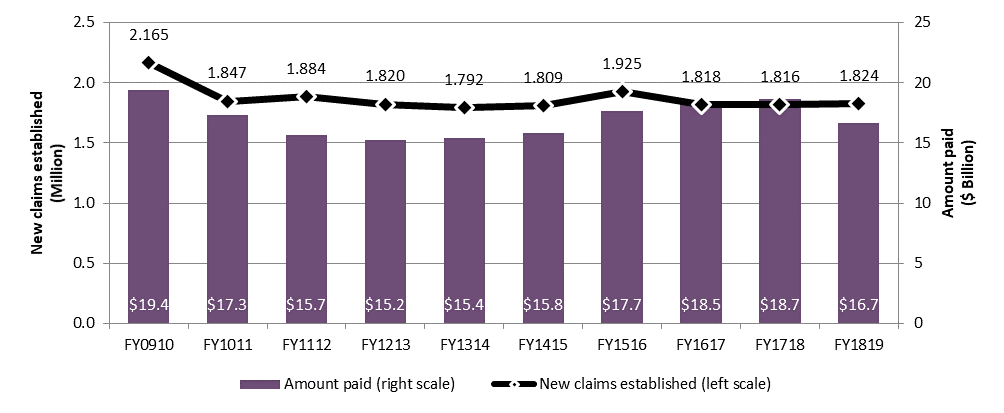

For the period beginning April 1, 2018, and ending March 31, 2019 (FY1819), the number of new EI claims edged up 0.5% (+8,790) to just over 1.8 million new claims. Total EI benefit payments decreased by nearly $2 billion, or -10.6%, to $16.7 billion. This was the lowest level recorded since FY1415 (see Chart 1). This decline is partly due to generally improving labour market conditions and relatively low unemployment rates.

Text description of Chart 1

| Fiscal year | Employment Insurance claims (millions) (left scale) | Amount paid in Employment Insurance benefits ($ billion) (right scale) |

|---|---|---|

| FY0910 | 2.165 | $19.4 |

| FY1011 | 1.847 | $17.3 |

| FY1112 | 1.884 | $15.7 |

| FY1213 | 1.820 | $15.2 |

| FY1314 | 1.792 | $15.4 |

| FY1415 | 1.809 | $15.8 |

| FY1516 | 1.925 | $17.7 |

| FY1617 | 1.818 | $18.5 |

| FY1718 | 1.816 | $18.7 |

| FY1819 | 1.824 | $16.7 |

- Note: Includes all claims for which at least $1 of Employment Insurance benefits was paid.

- Source: Employment and Social Development Canada, Employment Insurance (EI) administrative data. Data are based on a 10% sample of EI administrative data.

According to Statistics Canada, there were 717,600 beneficiaries receiving EI benefits on average each month in FY1819, a decrease of 7.5% from 775,800 beneficiaries during the previous reporting period.Footnote 2

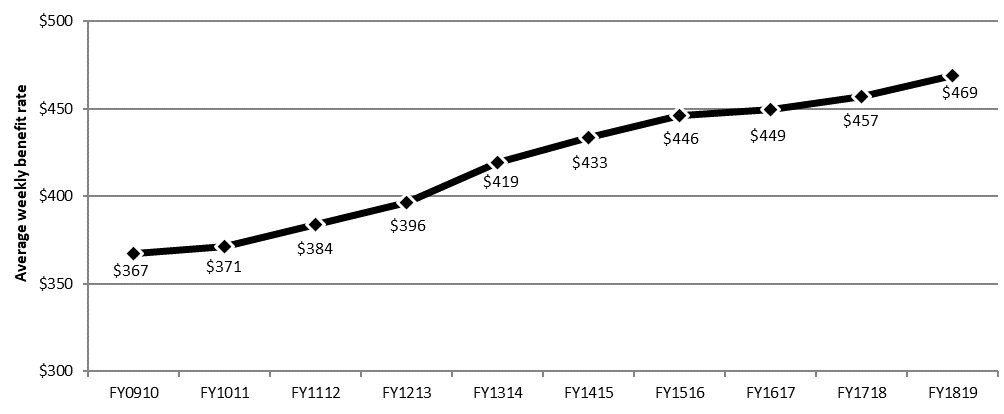

The average weekly benefit rate increased by 2.6% from $454 in FY1718 to $465 to FY1819.Footnote 3,Footnote 4 The proportion of claimants receiving the maximum weekly benefit increased from 46.5% in FY1718 to 48.0% in FY1819.

New Employment Insurance claims established

The slight increase in the number of new EI claims observed during the reporting period is largely due to an increase in claims for sickness and parental benefits, which was partially offset by a decrease in the number of claims for regular, compassionate care and maternity benefits (see Table 2).

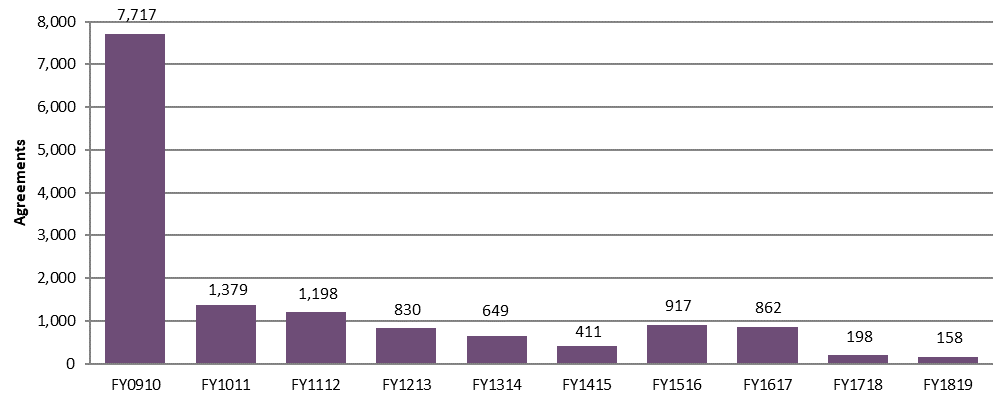

| Type of Employment Insurance benefit | New claims established FY1718 | New claims established FY1819 | Change in new claims established (# and %) | Amount paid ($ millions) FY1718 | Amount paid ($ millions) FY1819 | Change in amount paid (%) |

|---|---|---|---|---|---|---|

| Regular | 1,299,710 | 1,292,710 | -7,000 (-0.5%) | $12,640.5 | $10,673.8 | -15.6% |

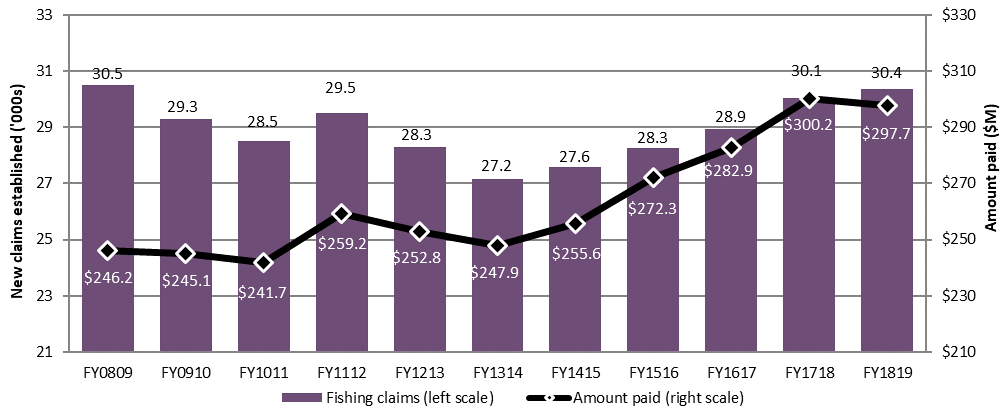

| Fishing | 30,055 | 30,367 | +312 (+1.0%) | $300.2 | $297.7 | -0.8% |

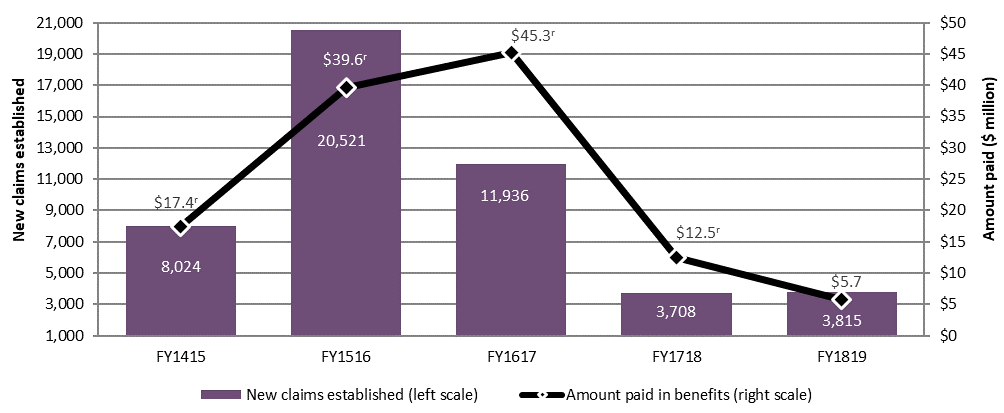

| Work-Sharing | 3,708 | 3,815 | +107 (+2.9%) | $12.5r1 | $5.7 | -53.9% |

| Special | 597,090 | 606,540 | +9,450 (+1.6%) | $5,739.7r | $5,792.7 | +0.9% |

| Maternity | 171,470 | 170,010 | -1,460 (-0.9%) | $1,150.3 | $1,164.1 | +1.2% |

| Parental | 198,050 | 200,030 | +1,980 (+1.0%) | $2,778.1 | $2,728.0 | -1.8% |

| Sickness | 411,870 | 420,840 | +8,970 (+2.2%) | $1,712.0 | $1,769.6 | +3.4% |

| Family caregiver for children | 4,921r | 5,475 | +554 (+11.3%) | $30.4r | $36.8 | +20.9% |

| Family caregiver for adults | 2,671r,* | 10,106 | n/a* | $7.8r,* | $48.3 | n/a* |

| Compassionate care | 11,010 | 8,385 | -2,625 (-23.8%) | $61.1 | $45.8 | -25.0% |

| Canada | 1,815,540 | 1,824,330 | +8,790 (+0.5%) | $18,654.7 | $16,685.3 | -10.6% |

- Notes: Totals may not add up due to rounding. Includes all claims for which at least $1 of Employment Insurance benefits was paid. The sum of claims by benefit type does not add up as multiple benefit types can be combined in 1 single claim.

- r1 Data has been revised, given that the amount paid in Work-Sharing benefits is now based on a 100% sample of EI administrative data.

- r Revised data.

- * EI family caregiver benefits for adults came into effect on December 3, 2017. Given the short period during which benefits for family caregivers for adults were offered in FY1718, few claims were made. Consequently, the data from FY1819 are not comparable to the previous year's data.

- Source: Employment and Social Development Canada, Employment Insurance (EI) administrative data. Data are based on a sample of 10% of the EI administrative data, except for family caregiver, Work-Sharing and compassionate care benefits as well as claims for fishing benefits (100%).

Most provinces and territories experienced modest declines in the number of new EI claims established between FY1718 and FY1819. However, Alberta (+18,600 or +10.9%), Newfoundland and Labrador (+4,980 or +6.1%), Saskatchewan (+2,960 or +5.8%) and Manitoba (+2,580 or +4.2%) recorded increases over the reporting period (see Table 3).

| Category | New claims established FY1718 | New claims established FY1819 | Change in new claims established (%) | Amount paid ($ millions) FY1718 | Amount paid ($ millions) FY1819 | Change in amount paid (%) |

|---|---|---|---|---|---|---|

| Newfoundland and Labrador | 81,090 | 86,070 | +6.1% | $1,185.2 | $1,022.9 | -13.7% |

| Prince Edward Island | 22,720 | 22,480 | -1.1% | $248.1 | $231.1 | -6.9% |

| Nova Scotia | 85,300 | 84,570 | -0.9% | $892.2 | $845.1 | -5.3% |

| New Brunswick | 91,130 | 89,820 | -1.4% | $954.0 | $869.6 | -8.9% |

| Quebec | 482,990 | 473,060 | -2.1% | $3,558.2 | $3,106.0 | -12.7% |

| Ontario | 562,570 | 556,900 | -1.0% | $5,657.7 | $5,240.4 | -7.4% |

| Manitoba | 61,440 | 64,020 | +4.2% | $631.3 | $619.2 | -1.9% |

| Saskatchewan | 51,250 | 54,210 | +5.8% | $700.9 | $624.7 | -10.9% |

| Alberta | 170,270 | 188,870 | +10.9% | $2,655.3 | $2,171.0 | -18.2% |

| British Columbia | 200,820 | 198,240 | -1.3% | $2,089.5 | $1,878.1 | -10.1% |

| Yukon | 2,200 | 2,310 | +5.0% | $27.8 | $25.0 | -9.8% |

| Northwest Territories | 2,420 | 2,310 | -4.5% | $30.9 | $31.1 | +0.9% |

| Nunavut | 1,340 | 1,470 | +9.7% | $23.6 | $21.0 | -11.1% |

| Men | 974,660 | 988,250 | +1.4% | $9,678.0 | $8,416.6 | -13.0% |

| Women | 840,880 | 836,080 | -0.6% | $8,976.6 | $8,268.7 | -7.9% |

| 24 years old and under | 172,810 | 170,480 | -1.3% | $1,443.0 | $1,284.6 | -11.0% |

| 25 to 44 years old | 876,270 | 882,780 | +0.7% | $9,908.0 | $9,038.7 | -8.8% |

| 45 years to 54 years old | 363,410 | 352,640 | -3.0% | $3,431.5 | $2,883.7 | -16.0% |

| 55 years old and over | 403,050 | 418,430 | +3.8% | $3,872.1 | $3,478.3 | -10.2% |

| Canada | 1,815,540 | 1,824,330 | +0.5% | $18,654.7 | $16,685.3 | -10.6% |

Notes: Totals may not add up to the total due to rounding. Includes claims for which at least $1 of EI benefits was paid.

Source: Employment and Social Development Canada, Employment Insurance (EI) administrative data. Data are based on a sample of 10% of the EI administrative data.

The number of new claims established by men increased slightly during FY1819, while it decreased for women. Men established 54.2% of all new claims. Levels of new EI claims decreased for young workers aged 24 years old and under and for workers aged 45 to 54 years old.

Total amount paid in Employment Insurance benefits

The amount paid for all types of EI benefits combined reached $16.7 billion in FY1819, a decrease of $2 billion or -10.6%. This decline was largely attributable to the decrease in the amount paid in EI regular benefits ($2 billion or -15.6%).

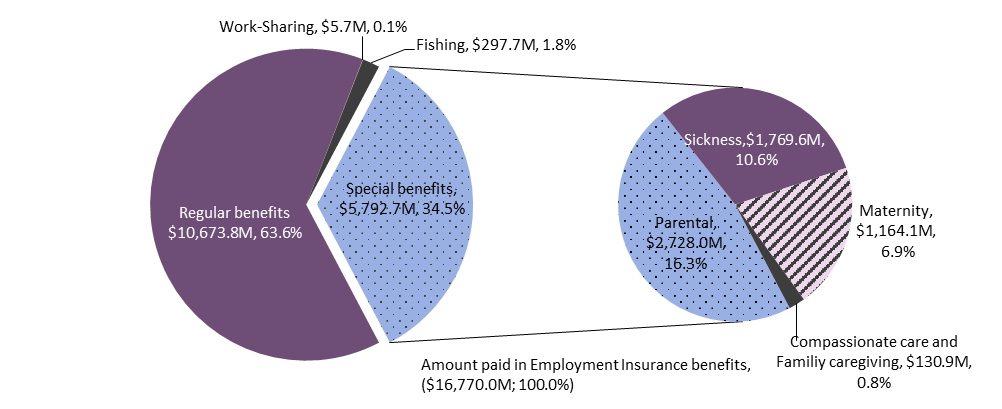

The share of EI benefits paid by benefit type remains relatively unchanged compared to the previous reporting period. However, the share of regular benefits fell slightly between FY1718 and FY1819 from 67.6% to 63.6%, while the share of special benefits climbed from 30.7% to 34.5%. Fishing and Work-Sharing benefits represented less than 2.0% of total EI benefits paid (see Chart 2).

Text description of Chart 2

| Benefits | $ million | % share |

|---|---|---|

| Regular benefits | $10,673.8 | 63.6% |

| Work-Sharing benefits | $5.7 | 0.1% |

| Fishing benefits | $297.7 | 1.8% |

| Special benefits | $5,792.7 | 34.5% |

| Parental benefits | $2,728.0 | 16.3% |

| Sickness benefits | $1,769.6 | 10.6% |

| Maternity benefits | $1,164.1 | 6.9% |

| Compassionate care and Family caregiving benefits | $130.9 | 0.8% |

- *The total amount paid reported in Chart 2 does not correspond to the total reported in Tables 2 and 3 because data on compassionate care benefits and family caregiver benefits can only be reported on a 100% sampling bases on an aggregate level.

- Source: Employment and Social Development Canada, Employment Insurance (EI) administrative data. Data are based on a sample of 10% of the EI administrative data, except for Work-Sharing, family caregiver and compassionate care benefits (100%).

The amount paid in EI benefits decreased in all provinces and territories, except for Northwest Territories. Alberta (-18.2%), Newfoundland and Labrador (-13.7%) and Quebec (-12.7%) recorded the largest declines in benefits paid (see Table 3).

EI benefits received by both men and women declined from the previous fiscal year, with men having experienced a greater decline than women. The amount paid in EI benefits also decreased for each age group.

Levels of benefits

For all claims, excluding those for extended parental benefitsFootnote 5, the average weekly benefit rate increased by 2.6% nationally to $465 over the reporting period (see Annex 2.3.2). This rise is comparable to the 2.7% increase in maximum insurable earnings between 2018 and 2019 (see Section 2.7). All provinces and territories recorded increases, with the exception of Nunavut. Northwest Territories continued to have the highest average weekly benefit rate ($520), while Prince Edward Island and Nova Scotia posted the lowest average rates ($437 each).

Northwest Territories also had the highest proportion of claimants receiving the maximum weekly benefit rate (79.4%) for FY1819, while Prince Edward Island and New Brunswick had the lowest proportions of claimants receiving the maximum rate (35.1% and 35.4%, respectively).

The average weekly benefit rate increased for male and female claimants to $492 and $433, respectively. Men (59.5%) were proportionally more likely to receive the maximum weekly benefit rate compared to women (33.9%) in FY1819.

The average weekly benefit rate also increased for all age groups compared to FY1718. Claimants aged 25 to 44 still received the highest average weekly benefit rate ($478) and were more likely to collect the maximum weekly benefit rate (52.7%). Claimants under 25 years of age received, on average, the lowest amount of weekly benefits ($421), and only 30.0% of them received the maximum weekly benefit rate in FY1819.

Calculating the weekly benefit rate: Variable Best Weeks (VBW)

Since April 7, 2013 under the VBW provision the weekly benefit rate is calculated based on an EI claimant's highest (best) weeks of insurable earnings during the qualifying period. The number of weeks used to calculate the weekly benefit rate ranges from 14 to 22, depending on the monthly regional unemployment rate.*

| Unemployment rate* | Number of weeks |

|---|---|

| 6.0% and under | 22 |

| 6.1% to 7.0% | 21 |

| 7.1% to 8.0% | 20 |

| 8.1% to 9.0% | 19 |

| 9.1% to 10.0% | 18 |

| 10.1% to 11.0% | 17 |

| 11.1% to 12.0% | 16 |

| 12.1% to 13.0% | 15 |

| More than 13.0% | 14 |

- *The monthly regional unemployment rates used for the EI program are a moving average of seasonally adjusted rates of unemployment produced by Statistics Canada, as per section 17 of the Employment Insurance Regulations.

Impacts of Variable Best Weeks on benefit amounts

Prior to the implementation of the Variable Best Weeks (VBW) in April 2013, 2 methods for calculating the weekly benefit rate were in place: the Small Weeks provision and the Best 14 Weeks pilot project. The VBW method aims to strengthen incentives to accepting available work.

A recent departmental study* examined the impacts of the April 2013 change, among other things, on benefit rates by comparing benefits rates based on the VBW method with hypothetical rates that would have been obtained if the 2 previous methods had still been in effect. The analysis covered the period from April 2013 to August 2018.

The results of the study indicate that of the 9.7 million of claims established during the period covered by the study, 75.4% were not impacted by the change (because they would have received the same weekly benefit amounts if the old calculation methods had still been in effect), while 6.8% (0.7 million of claims) resulted in a lower benefit rate, and 17.8% (1.7 million of claims) received a higher benefit rate.

For claims established in regions that were subject to the Best 14 Weeks pilot project and negatively affected by the change, the benefit rate would have been higher by an average of $13 to $19 per week with the Best 14 Weeks method. This represents a decrease of about 5% of the benefit rate following the implementation of Variable Best Weeks.

For claims established in regions that were subject to the Small Weeks Provision and benefited from the change, the benefit rate would have been lower by an average of $43 to $49 per week if the previous Small Weeks method had still been in effect. This represents an increase of about 11% of their benefit rate following the implementation of Variable Best Weeks.

In general, claims established by claimants aged 15 to 24, men and claimants with less than 700 hours of insurable employment, and claims from the goods-producing industries, were the most impacted by the change in the benefit rate calculation method, both for claims established in the Best 14 Weeks pilot project regions and for those established in the Small Weeks provision regions.

- * ESDC, Impacts of Variable Best Weeks on benefit amounts (ESDC, Employment Insurance Policy Directorate, Ottawa, 2020)

Family supplement provision

The Family supplement provision, which targets low-income families, provides additional benefits to EI claimants with children under the age of 18 who have an annual family net income equal to or less than $25,921. The claimant must also receive the Canada Child Benefit. Under the Family supplement provision, which is available to claims in all benefit types, the weekly amount of family supplement can increase a claimant's benefit rate from 55% to a maximum of 80% of his or her weekly insurable earnings, subject to the maximum weekly benefit. The supplement provided to eligible claimants is determined by the claimant's family net income, the number of children in the claimant's family, and the age of the claimant's children.Footnote 6

In FY1819, low-income families received a total of $77.0 million in additional benefits through the Family supplement provision. A total of 72,900 claims received the family supplement in FY1819, a decrease of 4.0% from FY1718. The number of EI claims receiving the family supplement has now decreased for 17 consecutive years from a high of 187,300 claims in FY0102. Women (79.5%) and claimants aged 25 to 44 (72.2%) continue to be the main demographic groups benefitting from the Family supplement provision. The average weekly family supplement was $44 in FY1819 and has remained relatively unchanged over the years (see Annex 2.23 for more statistics on the Family Supplement provision).

2.1.2 Combined Employment Insurance claims

Under certain provisions of the EI program, a claimant may receive multiple types of benefits as part of a single claim, assuming that the claimant meets each benefit type's eligibility requirements.Footnote 7 A "pure" claim is 1 in which an EI claimant receives a single benefit type, while a "combined" claim is 1 in which the claimant receives more than 1 benefit type. Pure claims represented 81.8% of all completed claims in FY1819 (see Table 4).

| Benefit type* | Number of total claims (‘000s) | Number of pure claims (‘000s) |

Share of pure claims (%) | Number of combined claims (‘000s) |

Share of combined claims (%) | Benefit type most often combined with (share of combined claims) |

|---|---|---|---|---|---|---|

| Regular | 1,423.8 | 1,242.0 | 87.2% | 181.8 | 12.8% | Sickness (93.3%) |

| Fishing | 30.2 | 26.1 | 86.5% | 4.1 | 13.5% | Sickness (85.0%) |

| Work-Sharing | 3.3 | 2.3 | 68.9% | 1.0 | 31.1% | Regular (76.7%) |

| Maternity | 166.2 | 2.5 | 1.5% | 163.6 | 98.5% | Parental (98.1%) |

| Parental** | 196.3 | 31.1 | 15.8% | 165.2 | 84.2% | Maternity (97.2%) |

| Sickness | 439.6 | 236.8 | 53.9% | 202.8 | 46.1% | Regular (83.7%) |

| Compassionate care | 10.0 | 5.8 | 58.5% | 4.1 | 41.5% | Sickness (61.4%) |

| All claims*** | 1,891.3 | 1,546.7 | 81.8% | 344.6 | 18.2% | n/a |

- Note: Data may not add up to the total due to rounding. Includes claims for which at least $1 of EI benefits was paid. Completed claims include those that are terminated and those that are dormant and remained inactive as of August the following fiscal year. The sum of claims by benefit type for the “Total claims” and “Combined claims” columns does not add up to the total because more than 1 benefit type can be part of the same claim. This does not apply to pure claims that include only 1 benefit type.

- *Excludes Family Caregiver Benefits for children and adults.

- **Parental benefits include benefits for biological parents and adoptive parents.

- *** The total number of claims is based on claims completed during the fiscal year. This explains why the total number of claims here is different from the total numbers of claims in Tables 2 and 3 which are based on established claims.

- Source: Employment and Social Development Canada, Employment Insurance (EI) administrative data. Data are based on a 10% sample of EI administrative data.

Women were more likely to claim more than 1 type of EI benefit (28.0%) than men (10.1%) mostly due to their high probability of claiming both maternity and parental benefits.

In fact, maternity benefits were the benefits most often combined with other types of benefits, usually parental benefits. However, a significant proportion also claimed sickness benefits with maternity benefits (17.4%), resulting in the claimant starting her leave before becoming eligible for maternity benefits (available 12 weeks prior to the child’s expected date of birth).Footnote 8 The combination of maternity, parental and sickness benefits was the most common among claims with 3 or more benefit types (26,900 claims representing 16.2% of completed claims for maternity benefits in FY1819).

Claims for parental benefits were combined at a slightly lower rate than maternity, as only 11.4% of men who claimed parental also received another benefit payment. Of those male claimants, 86.9% received regular benefits and 17.4% claimed sickness benefits. Among women, virtually all (99.5%) who combined parental benefits with other types of benefits combined them with maternity benefits.

Sickness benefits were the third most likely to be combined with other benefit types, mostly with regular benefits. Men combined their sickness benefits predominantly with regular benefits (96.5%), while sickness claims from women were most often combined with regular (71.3%), maternity (27.7%) and parental benefits (26.3%). Sickness also represented the greatest share of combined regular claims.

When combined, compassionate care benefits are most often shared with sickness benefits (61.4%) or regular benefits (52.2%). Men tended to combine compassionate care benefits with regular benefits (63.3%) more often than women (47.2%). Women were most likely to combine compassionate care benefits with sickness benefits (67.5%) compared to men (47.7%).

One third of all Work-Sharing claims were combined with other benefit types, predominantly regular benefits. This is attributable to the fact that both benefit types are typically used during a downturn in business activity, which increases the risk of layoffs (Work-Sharing benefits) and actual layoffs (regular benefits). Regular benefits are usually claimed following Work-Sharing benefits, reflecting a continued downturn in a participating firm’s activity that eventually leads to a downsizing of the firm’s labour force.

While fishers do have the possibility of sharing fishing benefits with other benefit types (under some restrictions), only 13.5% of fishing claims were combined claims. Of those claims, 85.0% were combined with sickness benefits. No fishing claims were shared with maternity, parental, compassionate care or Work-Sharing benefits during the reporting period.

2.1.3 Benefits-to-contributions ratios

The benefits-to-contributions ratio (B/C ratio) is a measure of EI benefits paid by the program as a share of the contributions paid. It provides an estimate of the use of the EI program by claimants compared to the premiums paid. This section examines 2 different ratios: the total benefits-contributions ratio (total B/C ratio) and the regular benefits-contributions ratio (regular B/C ratio) for 2017.Footnote 9 As EI contributions are not assigned to a specific benefit type, the regular B/C ratio accounts for reductions in EI contributions related to special benefits.Footnote 10

This subsection presents adjusted ratios that are normalized, with Canada’s ratio set at 1.0. This provides a benchmark for examining the ratios based on certain sociodemographic characteristics. An adjusted ratio higher than 1.0 means that the underlying sub-population (such as province or territory, industry) is a net beneficiary of the EI program, while those with an adjusted ratio lower than 1.0 are net contributors to the program relative to Canada as a whole.

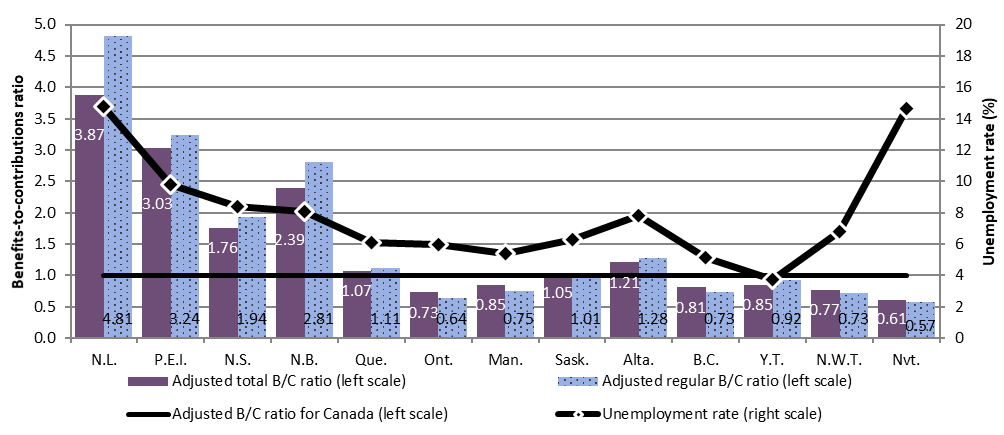

ProvincesFootnote 11 with high numbers of seasonal claimants generally exhibit adjusted total B/C ratios that are above the national average. In 2017, Newfoundland and Labrador, Prince Edward Island, Nova Scotia and New Brunswick received more in EI benefits than they contributed, when compared to the national average (see Chart 3), highlighting these provinces’ greater usage of regular benefits compared to other regions. On the other hand, Ontario, Manitoba, British Columbia and the Territories received fewer EI benefits and regular benefits per dollar contributed in premiums than the national average.

Text description of Chart 3

| Region | Adjusted total benefits-to-contributions ratio (left scale) | Adjusted regular benefits-to-contributions ratio (left scale) | Adjusted total benefits-to-contributions ratio for Canada (1.0) (left scale) | Unemployment rate (right scale) |

|---|---|---|---|---|

| Newfoundland and Labrador | 3.87 | 4.81 | 1.0 | 14.8 |

| Prince Edward Island | 3.03 | 3.24 | 1.0 | 9.8 |

| Nova Scotia | 1.76 | 1.94 | 1.0 | 8.4 |

| New Brunswick | 2.39 | 2.81 | 1.0 | 8.1 |

| Quebec | 1.07 | 1.11 | 1.0 | 6.1 |

| Ontario | 0.73 | 0.64 | 1.0 | 6.0 |

| Manitoba | 0.85 | 0.75 | 1.0 | 5.4 |

| Saskatchewan | 1.05 | 1.01 | 1.0 | 6.3 |

| Alberta | 1.21 | 1.28 | 1.0 | 7.8 |

| British Columbia | 0.81 | 0.73 | 1.0 | 5.2 |

| Yukon | 0.85 | 0.92 | 1.0 | 3.8 |

| Northwest Territories | 0.77 | 0.73 | 1.0 | 6.8 |

| Nunavut | 0.61 | 0.57 | 1.0 | 14.6 |

- Sources: Canada Revenue Agency (CRA), T4 slips with employment income (for data on contributions); Employment and Social Development Canada (ESDC), Employment Insurance (EI) administrative data (for data on benefits); and Statistics Canada, Labour Force Survey, Tables 14-10-0287-01 and 14-10-0292-01 (for data on unemployment rates). CRA data are based on a 10% sample of T4 slips with employment income, and ESDC data are based on a 10% sample of EI administrative data.

In 2017, women continued to receive more in EI benefits than they contributed in premiums compared to male claimants, with adjusted total B/C ratios of 1.03 and 0.97 respectively (see Table 5). Women aged 25 to 44 in particular receive more in benefits than they contribute with an adjusted total B/C ratio of 1.42, compared to women aged 45 to 54 with the lowest ratio (0.65) among women. This is likely due to the fact that women aged 25 to 44 claim maternity and/or parental benefits – their adjusted regular B/C ratio is much lower at 0.65.

| Age category | Adjusted total B/C ratio for men | Adjusted total B/C ratio for women | Adjusted total B/C ratio | Adjusted regular B/C ratio for men | Adjusted regular B/C ratio for women | Adjusted regular B/C ratio |

|---|---|---|---|---|---|---|

| 24 years old and under | 1.26 | 0.84 | 1.08 | 1.55 | 0.50 | 1.09 |

| 25 to 44 years old | 0.90 | 1.42 | 1.13 | 1.13 | 0.65 | 0.92 |

| 45 to 54 years old | 0.89 | 0.65 | 0.78 | 1.15 | 0.78 | 0.98 |

| 55 years old and over | 1.12 | 0.70 | 0.93 | 1.46 | 0.85 | 1.19 |

| Total | 0.97 | 1.03 | 1.00 | 1.23 | 0.71 | 1.00 |

- Sources: Canada Revenue Agency (CRA), T4 slips with employment income (for data on contributions);

- Employment and Social Development Canada (ESDC), Employment Insurance (EI) administrative data (for data on benefits). CRA data are based on a 10% sample of T4 slips with employment income, and ESDC data are based on a 10% sample of EI administrative data.

With respect to regular B/C ratios, the gender gap is reversed: men (ratio of 1.23) received more EI regular benefits than they contributed compared to women (ratio of 0.71). This is true for all age groups.

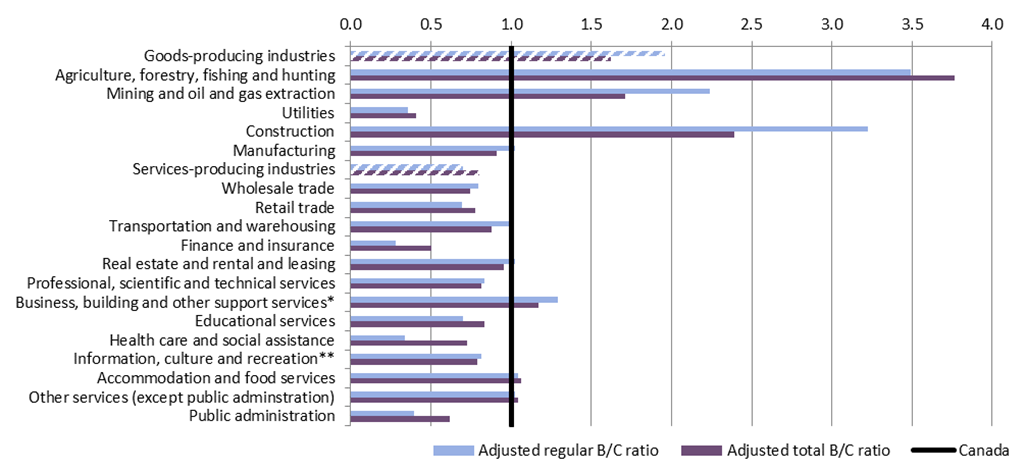

In 2017, claimants working in goods-producing industries were net beneficiaries of EI benefits with adjusted B/C ratios above the national average, while those in service-producing industries were, overall, net contributors (see Chart 4). The greater use of EI regular benefits by workers in goods-producing industries compared to those in service-producing industries may be related to the higher proportion of seasonal employment in these industries, particularly the construction and the agriculture, forestry, fishing and hunting industries. The difference between the adjusted B/C ratios of goods-producing industries compared to those of service-producing industries is smaller for the total B/C ratio. This may be explained in part by the fact that certain industries, such as the health care and social assistance industry and the educational services industry, have a large proportion of female workers who can claim maternity or parental benefits.

Text description of Chart 4

| Industry | Adjusted total benefits-to-contributions ratio | Adjusted regular benefits-to-contributions ratio |

|---|---|---|

| Goods-producing industries | 1.62 | 1.96 |

| Agriculture, forestry, fishing and hunting | 3.76 | 3.49 |

| Mining and oil and gas extraction | 1.71 | 2.24 |

| Utilities | 0.41 | 0.36 |

| Construction | 2.39 | 3.22 |

| Manufacturing | 0.91 | 1.02 |

| Services-producing industries | 0.80 | 0.70 |

| Wholesale trade | 0.75 | 0.79 |

| Retail trade | 0.78 | 0.70 |

| Transportation and warehousing | 0.88 | 0.99 |

| Finance and insurance | 0.50 | 0.28 |

| Real estate and rental and leasing | 0.96 | 1.03 |

| Professional, scientific and technical services | 0.82 | 0.83 |

| Business, building and other support services | 1.17 | 1.29 |

| Educational services | 0.84 | 0.70 |

| Health care and social assistance | 0.73 | 0.34 |

| Information, culture and recreation | 0.79 | 0.82 |

| Accommodation and food services | 1.06 | 1.04 |

| Other services (except public administration) | 1.05 | 1.03 |

| Public administration | 0.62 | 0.40 |

| Canada | 1.00 | 1.00 |

- * Includes management of companies and enterprises and administrative support, waste management and remediation services.

- ** Includes information and cultural industries and arts, entertainment and recreation services.

- Sources: Canada Revenue Agency (CRA), T4 slips with employment income (for data on contributions); Employment and Social Development Canada (ESDC), Employment Insurance (EI) administrative data (for data on benefits). CRA data are based on a 10% sample of T4 slips with employment income, and ESDC data are based on a 10% sample of EI administrative data.

Implicit income redistribution and the Employment Insurance program

Due to differences in income support provided by the EI program across socio-economic sub-populations, the program can act as an implicit income redistribution mechanism in Canada, providing greater income support (relative to contributions) to individuals in the lower part of the income distribution as compared to those with greater earnings. A 2012 evaluation study* showed that the benefit and contribution aspects of the program tend to be redistributive and that the impact of the program on the redistribution of earnings increased substantially during the late 2000s recession.

Moreover, a study on the financial impact of receiving EI benefits** concluded that the EI program has a considerable positive income redistribution effect, with lower income families having a higher adjusted total benefits-to-contributions ratio than higher income families. In fact, families with after-tax incomes below the median received 34% of total EI benefits and paid 18% of all premiums, representing an adjusted total benefits-to-contributions ratio of close to 2.0.

- *Ross Finnie and Ian Irvine, The Redistributional Impact of Employment Insurance 2007 to 2009 (Ottawa: HRSDC, Evaluation Directorate, 2013).

- **Constantine Kapsalis, Financial of Receiving Employment Insurance (Ottawa: Data Probe Economic Consulting Inc., 2010).

2.2 Employment Insurance regular benefits

In this section

- 2.2.1 Employment Insurance regular claims and amount paid

- 2.2.2 Coverage, eligibility and access to Employment Insurance regular benefits for the unemployed population

- 2.2.3 Level of Employment Insurance regular benefits

- 2.2.4 Employment Insurance regular benefit entitlement

- 2.2.5 Employment Insurance regular benefits and seasonal claimants

- 2.2.6 Exhaustion of Employment Insurance regular benefits

- 2.2.7 Working while on claim

2.2.1 Employment Insurance regular claims and amount paid

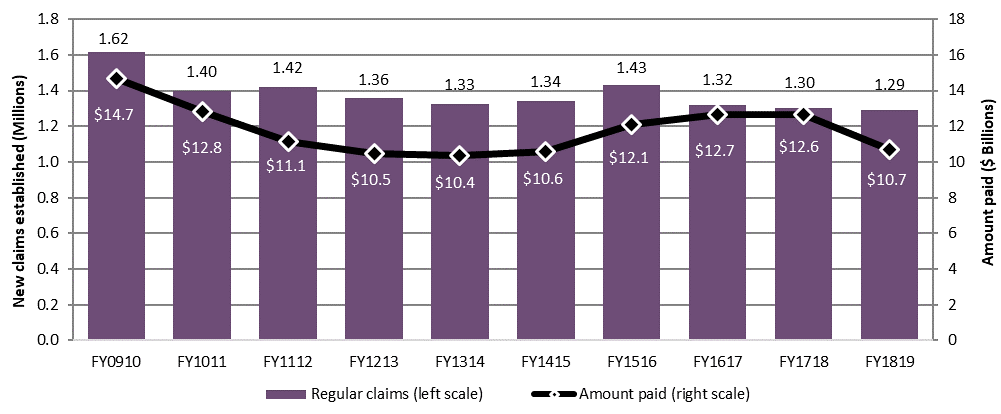

As shown in Chart 5, the number of new EI regular claims established in FY1819 remained relatively stable at 1.29 million from 1.3 million in FY1718, representing a slight decrease of 0.5%. This decline was largely attributable to the notable decline in new claims established in Quebec (-14,580 claims) and Ontario (-9,510 claims), offsetting the increases in Alberta (+14,690 claims) and Newfoundland and Labrador (+4,510 claims).

Over the same period, the total amount of EI regular benefits paid significantly decreased by 15.6% from $12.6 billion in FY1718 to $10.7 billion in FY1819, which is close to the total amount paid prior to FY1516. This decrease follows a 2 year downward trend in total amount paid, and is attributable in part to many factors, including a continued employment growth, a decrease in the national unemployment rate and the number of beneficiaries receiving EI regular benefits, the conclusion of the extension of EI regular benefits for workers in regions affected by the downturn in commodity prices,Footnote 12 a decrease in the average duration of EI regular weeks paid (-2 weeks) and a lower exhaustion rate.

Text description of Chart 5

| Fiscal year | Regular claims (millions) (left scale) | Amount paid ($ billions) (right scale) |

|---|---|---|

| FY0910 | 1.62 | $14.7 |

| FY1011 | 1.40 | $12.8 |

| FY1112 | 1.42 | $11.1 |

| FY1213 | 1.36 | $10.5 |

| FY1314 | 1.33 | $10.4 |

| FY1415 | 1.34 | $10.6 |

| FY1516 | 1.43 | $12.1 |

| FY1617 | 1.32 | $12.7 |

| FY1718 | 1.30 | $12.6 |

| FY1819 | 1.29 | $10.7 |

- Note: Includes claims for which at least $1 of EI regular benefits was paid.

- Source: Employment and Social Development Canada, Employment Insurance (EI) administrative data. Data are based on a 10% sample of EI administrative data.

The number of new claims established tends to be influenced by labour market conditions and overall economic cycles. During periods of economic growth and robust labour market conditions, fewer claims for EI regular benefits are established, while the opposite is true during periods of economic stagnation and unfavourable labour market conditions. This is evident in Chart 5—over the last decade, the number of new claims established was highest at 1.6 million in FY0910 following the recession in FY0809. As discussed in Chapter I, the Canadian economy experienced a moderate growth in FY1819 as GDP increased by 1.7% compared to the previous year, while the labour force increased by 1.1% during the same time period. The national unemployment rate slightly decreased from 6.1% in FY1718 to 5.8% in FY1819 as the number of unemployed individuals moderately declined by 3.9% during the same time period, leading to the corresponding slight decrease in the volume of new claims established for EI regular benefits (-0.5%) in FY1819.

In FY1819, on average, the number of people receiving EI regular benefits each month significantly decreased by 11.4% to 453,400, down from 511,800 in the previous year and continuing the downward trend that began in FY1617.Footnote 13 FY1819 marks the first time since the recession of FY0809 that the number of EI regular beneficiaries has dropped below 500,000.

As the number of monthly beneficiaries is related to the number of new claims established previously, these 2 measures tend to move in similar directions, with the count of monthly beneficiaries usually lagging behind the number of new claims established when there are changes in the average duration of benefits or a sudden and significant increase or decrease in new claims. To illustrate this, suppose there is an increase in the number of claims established for EI regular benefits after an economic shock. The number of monthly beneficiaries will increase following the increase in new claims. However, the count of monthly beneficiaries can still remain elevated even after the volume of new claims established has subsided once the labour market conditions improve, as payments continue to be made on previously established new claims until benefits are exhausted or the claimants have found employment.

Employment Insurance regular claims and amount paid by province or territory, gender and age

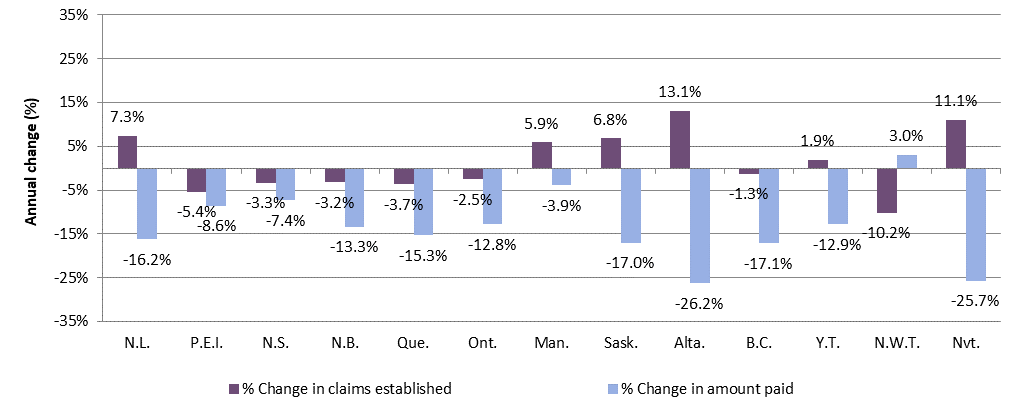

As illustrated in Chart 6, on a year-over-year basis, 7 out of 13 provinces and territories experienced a decline in the number of new claims established for EI regular benefits, including Northwest Territories (-10.2% or -180 claims), Prince Edward Island (-5.4% or -890 claims), Quebec (-3.7% or -14,580 claims), Nova Scotia (-3.3% or-2,080 claims), New Brunswick (-3.2% or -2,290 claims), Ontario (-2.5% or -9,510 claims) and British Columbia (-1.3% or -1,550 claims). These decreases partly offset the significant increases in Prairies provinces.

Text description of Chart 6

| Province/territory | % Change claims established | % Change amount paid |

|---|---|---|

| British Columbia | -1.3% | -17.1% |

| Alberta | 13.1% | -26.2% |

| Saskatchewan | 6.8% | -17.0% |

| Manitoba | 5.9% | -3.9% |

| Ontario | -2.5% | -12.8% |

| Quebec | -3.7% | -15.3% |

| New Brunswick | -3.2% | -13.3% |

| Nova Scotia | -3.3% | -7.4% |

| Prince Edward Island | -5.4% | -8.6% |

| Newfoundland and Labrador | 7.3% | -16.2% |

| Yukon | 1.9% | -12.9% |

| Northwestern Territories | -10.2% | -10.2% |

| Nunavut | 11.1% | -25.7% |

- Note: Includes claims for which at least $1 of EI regular benefits was paid.

- Source: Employment and Social Development Canada, Employment Insurance (EI) administrative data. Data are based on a 10% sample of EI administrative data.

In terms of the total EI regular benefits paid in FY1819, it decreased in all provinces and territories (see Chart 6) except in the Northwest Territories as compared to the previous year. The largest percentage decreases in the amount of EI regular benefits paid were observed in Alberta (-26.2%), followed by Nunavut (-25.7%), British Columbia (-17.1%), and Saskatchewan (-17.0%).Footnote 14 The percentage decreases in terms of EI regular benefits payments in Ontario and Quebec were lower than the national percentage decrease, and these 2 provinces continued to account for half (50.2%) of the total of all EI regular benefits paid in FY1819.

Table 6 outlines the number of new EI regular claims established and the total amount paid by gender and age groups. The number of new claims established by men remained relatively stable, while new claims established by women decreased slightly in the reporting period compared to the previous year (+0.3% and -1.8%, respectively). The share of claims established by gender remained stable year-over-year.

In terms of the total amount paid in EI regular benefits, the share of benefits paid to both men and women remained stable in FY1819 compared to the previous year, men accounted for 66.0% and women 34.0% of the total benefits paid.

| Category | Number of claims FY1718 |

Number of claims FY1819 |

Number of claims change (%) |

Amount paid ($ millions) FY1718 |

Amount paid ($ millions) FY1819 |

Amount paid ($ millions) change (%) |

|---|---|---|---|---|---|---|

| Men | 788,880 | 791,220 | +0.3% | $8,359.3 | $7,072.5 | -15.4% |

| Women | 510,830 | 501,490 | -1.8% | $4,281.2 | $3,601.3 | -15.9% |

| 24 years old and under | 118,750 | 113,780 | -4.2% | $1,076.1 | $922.7 | -14.3% |

| 25 to 44 years old | 571,930 | 568,800 | -0.5% | $5,449.7 | $4,585.2 | -15.9% |

| 45 to 54 years old | 289,420 | 278,900 | -3.6% | $2,876.7 | $2,335.9 | -18.8% |

| 55 years old and over | 319,610 | 331,230 | +3.6% | $3,238.0 | $2,830.0 | -12.6% |

| Canada | 1,299,710 | 1,292,710 | -0.5% | $12,640.5 | $10,673.8 | -15.6% |

- Note: Data may not add up to the total due to rounding. Percentage change is based on unrounded numbers. Includes claims for which at least $1 of EI regular benefits was paid.

- Source: Employment and Social Development Canada, Employment Insurance (EI) administrative data. Data are based on a 10% sample of EI administrative data.

The number of new EI regular claims established decreased for all age groups, except individuals aged 55 years old and over, while at the same time the total amount paid for all age groups decreased during the reporting period compared to the previous year. Like in the previous year, claimants who were between 25 and 44 years old continued to account for the largest shares of new regular claims and total amount paid in FY1819, while the smallest shares were for younger claimants aged less than 25 years.

One notable trend that has been observed over the past few years is that, while the shares of new claims established by different age groups has been relatively stable, the share of new claims established by older claimants aged 55 years and over has increased slowly but steadily over the past several years. The trends observed for older claimants are likely attributable in part to Canada’s aging population and the labour force composition. Individuals in this age category accounted for 21.4% of the labour force in FY1819, up from 21.1% in FY1718 (+0.3 percentage points).Footnote 15

Employment Insurance regular claims and amount paid by industry

As outlined in Table 7, there is a slight increase in the number of new claims established for EI regular benefits for the goods-producing industries (+3,120 claims or +0.6%), while for the service producing industries the number of new claims remained stable. Among the goods-producing industries, the Construction industry accounted for more than half (57.9%) of all new claims established, and had an increase of +1.3% compared to the previous year. On the other hand, the largest relative increase was observed in the Mining and oil and gas extraction industry where the number of new claims increased by 17.1%. Among the services-producing industries, the Educational services industry accounted for the largest share of claims in FY1819 (21.3%). On a year-over-year basis, the largest percentage decrease in the number of new claims established in the services-producing sector was observed for the Finance and insurance industry (-15.9%), while the largest increase was for both Transportation and warehousing, and Other services (excluding Public administration) industry, with 4.1% increase for both.

| Industry | Number of claims (% share of all claims) FY1718 |

Number of claims (% share of all claims) FY1819 |

Number of claims change (%) |

Amount paid - $ millions (% share of total amount paid) FY1718 |

Amount paid - $ millions (% share of total amount paid) FY1819 |

Amount paid - $ millions change (%) |

|---|---|---|---|---|---|---|

| Goods-producing industries | 502,080 (38.6%) | 505,200 (39.1%) | +0.6% | $5,343.6 (42.3%) | $4,473.4 (41.9%) | -16.3% |

| Agriculture, forestry, fishing and hunting | 53,760 (4.1%) | 52,440 (4.1%) | -2.5% | $578.2 (4.6%) | $496.8 (4.7%) | -14.1% |

| Mining and oil and gas extraction | 21,340 (1.6%) | 24,980 (1.9%) | +17.1% | $310.0 (2.5%) | $274.2 (2.6) | -11.5% |

| Utilities | 4,150 (0.3%) | 4,150 (0.3%) | 0.0% | $48.2 (0.4%) | $36.4 (0.3) | -24.6% |

| Construction | 288,870 (22.2%) | 292,720 (22.6%) | +1.3% | $3,113.4 (24.6%) | $2,640.3 (24.7) | -15.2% |

| Manufacturing | 133,960 (10.3%) | 130,910 (10.1%) | -2.3% | $1,293.7 (10.2%) | $1,025.7 (9.6%) | -20.7% |

| Services-producing industries | 764,150 (58.8%) | 764,220 (59.1%) | 0.0% | $6,998.6 (55.4%) | $5,995.6 (56.2%) | -14.3% |

| Wholesale trade | 39,790 (3.1%) | 38,920 (3.0%) | -2.2% | $492.3 (3.9%) | $402.6 (3.8%) | -18.2% |

| Retail trade | 79,090 (6.1%) | 69,330 (5.4%) | -12.3% | $763.4 (6.0%) | $620.9 (5.8%) | -18.7% |

| Transportation and warehousing | 60,190 (4.6%) | 62,640 (4.8%) | +4.1% | $533.3 (4.2%) | $466.0 (4.4%) | -12.6% |

| Finance and insurance | 15,020 (1.2%) | 12,630 (1.0%) | -15.9% | $193.9 (1.5%) | $155.0 (1.5%) | -20.0% |

| Real estate, rental and leasing | 17,720 (1.4%) | 18,270 (1.4%) | +3.1% | $207.3 (1.6%) | $175.4 (1.6%) | -15.4% |

| Professional, scientific and technical services | 52,690 (4.1%) | 50,950 (3.9%) | -3.3% | $601.1 (4.8%) | $479.4 (4.5%) | -20.2% |

| Business, building and other support services* | 86,380 (6.6%) | 88,130 (6.8%) | +2.0% | $871.4 (6.9%) | $768.8 (7.2%) | -11.8% |

| Educational services | 157,110 (12.1%) | 163,030 (12.6%) | +3.8% | $850.0 (6.7%) | $774.6 (7.3%) | -8.9% |

| Health care and social assistance | 46,590 (3.6%) | 45,870 (3.5%) | -1.5% | $424.0 (3.4%) | $349.6 (3.3%) | -17.5% |

| Information, culture and recreation** | 39,080 (3.0%) | 40,250 (3.1%) | +3.0% | $377.7 (3.0%) | $324.7 (3.0%) | -14.0% |

| Accommodation and food services | 63,840 (4.9%) | 63,280 (4.9%) | -0.9% | $559.9 (4.4%) | $487.2 (4.6%) | -13.0% |

| Other services (excluding Public administration) | 40,340 (3.1%) | 42,010 (3.2%) | +4.1% | $421.5 (3.3%) | $371.7 (3.5%) | -11.8% |

| Public administration | 66,310 (5.1%) | 68,910 (5.3%) | +3.9% | $702.7 (5.6%) | $619.7 (5.8%) | -11.8% |

| Unclassified*** | 33,480 (2.6%) | 23,290 (1.8%) | -30.4% | $298.4 (2.4%) | $204.8 (1.9%) | -31.4% |

| Canada | 1,299,710 (100.0%) | 1,292,710 (100.0%) | -0.5% | $12,640.5 (100.0%) | $10,673.8 (100.0%) | -15.6% |

- Note: Data may not add up to the total due to rounding. Percentage change is based on unrounded numbers. Includes claims for which at least $1 of EI regular benefits was paid.

- * This industry sector comprises the industries with codes 55 (Management of companies and enterprises) and 56 (Administration and support, waste management and remediation services).

- ** This industry sector comprises the industries with codes 51 (Information and cultural industries) and 71 (Arts, entertainment and recreation).

- *** For some claims, this information was not available in the data.

- Source: Employment and Social Development Canada, Employment Insurance (EI) administrative data. Data are based on a 10% sample of EI administrative data.

The total amount of benefits paid to claimants in both the goods-producing sector and the services-producing sector decreased by $870.2 million (-16.3%) and $1,003 million (-14.3%), respectively, in the reporting period compared to the previous year. The decline in the total amount paid to claimants in the goods-producing industries was mainly attributable to the large decrease in the Construction industry (-$473.1 million or -15.2%) and in the Manufacturing industry (-$268.1 million or -20.7%). As for the services-producing sector, the decrease in total amount paid was in most part driven by the declines in the Retail trade industry (-$142.5 million or -18.7%), the Professional, scientific and technical services industry (-$121.7 million or -20.2%), and the Business, building and other support services industry (-$102.6 million or -11.8%).

Benefit repayments in the 2017 tax year*

EI benefit payments are taxable income, regardless of the type of benefits. In accordance with the Employment Insurance Act, claimants must repay a percentage of EI benefits they have received if their net income** in a given year exceeds 1.25 times the maximum yearly insurable earnings. In the 2017 taxation year, claimants whose net income exceeded $64,125*** were required to repay 30% of the lesser of:

- the net income in excess of $64,125

- the total regular benefits, including regular fishing benefits, paid in the taxation year

However, claimants who received special benefits or less than 1 week of either regular or fishing benefits in the preceding 10 taxation years were exempt from the benefit repayment requirement.

In the 2017 taxation year, around 189,200 EI claimants repaid a total of $285.5 million in EI benefits. On average, each EI claimant subject to the benefit repayment provision repaid $1,509 in 2017, while they received $6,373 in EI benefits in the same year. Compared to the previous year, the increases in both the number of claimants who repaid benefits (+19,900 or +11.8%) and the total amount repaid (+$34.9 million or + 13.9%) were substantial in 2017. However, the average amount of benefit repaid (+$29 or +1.9%) and the average benefit received (-$8 or -0.1%) by these EI claimants remained relatively unchanged in 2017 compared to 2016.

In 2017, 2 out of 3 (66.7%) claimants who repaid benefits lived in Quebec, Ontario and Alberta. Together, these claimants accounted for 58.4% of the total amount repaid in EI benefits. In comparison, Atlantic provinces represented 16.3% of the total number of claimants who repaid benefits, accounting for 25.7% of the total amount repaid.

Benefit repayments also vary by industry. In 2017, around two-thirds (66.5%) of claimants who repaid benefits had worked in the goods-producing industries, unchanged from 2016. These claimants accounted for 67.2% of the total amount repaid. On the other hand, services-producing industries accounted for 28.9% claimants who repaid benefits and 29.7% of total amount repaid. These proportions have remained stable since 2011.

- * The most recent taxation year for which data are available is 2017.

- ** Net income includes employment income and EI benefits received during the taxation year.

- *** The maximum insurable earnings in 2017 was $51,300.

Employment Insurance regular benefits and firms

According to the 2017 tax dataFootnote 16 available from the Canada Revenue Agency (CRA), the number of firms operating in Canada slightly increased (+1.0%) compared to 2016. Among the 1.21 million of firms, 309,100 (representing 25.5% of all firms) employed at least 1 employee who had received EI regular benefits.

Table 8 outlines the number of firms, employment and EI regular claimants by sizeFootnote 17 of firms. The proportion of firms which employed at least 1 employee receiving EI regular benefits varied widely by firm size, with smaller firms being less likely to be the last employer of a claimant. For example, 20.0% of small-sized firms in 2017 had at least 1 former employee who received EI regular benefits, compared to 74.3% of small-to-medium sized firms, 95.1% of medium-to-large sized firms and 99.4%of large-sized firms.

However, when the number of claimants for EI regular benefits is compared with distribution of workforce by firm size, employees from smaller firms are found to be over-represented among EI regular claimants. As shown in Table 8, smaller firms accounted for 21.5% of the total workforce while they represented 26.6% of the total EI regular benefit claimants in 2017. Similarly, employees in the small-to-medium sized firms were also over-represented among EI regular claimants—these firms accounted for 19.8% of the total employees and 24.3% of the total EI regular claimants. This gap between the share of employment and the share of EI regular claimants narrows for the medium-to-large sized firms. For the large-sized firms, however, the opposite was observed—these firms represented 42.6% of the total workforce in Canada in 2017 but accounted for only 31.6% of the total EI regular claimants. The higher proportion of usage of EI regular benefits among employees in the smaller-sized firms suggest that smaller firms are more vulnerable to difficult business or economic conditions than larger firms, and need to make broader adjustments to their workforces, resulting in a larger share of their employees claiming EI regular benefits as a result of layoffs. Moreover, this trend can also be influenced by industry-related characteristics such as the greater prevalence of seasonal jobs in small-sized firms that are generally more likely to rely on EI, relative to the national average in some industries.Footnote 18

| Firm size | Number of all firms | Number of firms with at least 1 employee receiving EI regular benefits | Employment distribution** (% share) |

EI claimant distribution*** (% share) |

|---|---|---|---|---|

| Small | 1,096,760 | 219,460 | 21.5% | 26.6% |

| Small-medium | 95,710 | 71,080 | 19.8% | 24.3% |

| Medium-large | 16,120 | 15,340 | 16.1% | 17.5% |

| Large | 3,240 | 3,220 | 42.6% | 31.6% |

| Canada | 1,211,830 | 309,090 | 100.0% | 100.0% |

- Note: Data may not add up due to rounding.

- * The categories of firm size reflect those found in Business Dynamics in Canada, a Statistics Canada publication. Small-sized firms are defined as those that employ 1 to 19 employees. Small-to-medium sized firms employ 20 to 99 employees. Medium-to-large sized firms employ 100 to 499 employees. Large-sized firms employ 500 employees or more.

- ** The number of workers in a firm is the number of individuals with employment income in that firm, as indicated on a T4 form. The number of workers is adjusted so that each individual in the labour force is only counted once and individuals who work for more than 1 firm are taken into account. For example, if an employee that earned $25,000 in firm 1 and $25,000 in firm 2, then he or she was recorded as 0.5 employees at the first firm and 0.5 employees at the second firm.

- *** These are based on the number of people receiving EI regular benefits in 2017.

- Source: Employment and Social Development Canada, Employment Insurance (EI) administrative data. Data are based on a 100% sample of EI administrative data. Canada Revenue Agency, CRA administrative data. CRA data are based on a 100% sample.

Employment Insurance regular claims and amount paid by EI claimant category

Table 9 outlines the number of new claims established for EI regular benefits and total amount paid by EI claimant category.Footnote 19 In FY1819, both the number of new claims established by and the total amount paid to long-tenured workers decreased by 5.0% and 26.2%, respectively, compared to the previous year. On the other hand, the number of new claims established by occasional claimants remained relatively unchanged (+0.2%) in FY1819, while the total amount paid decreased by 12.2% compared to the previous year. Lastly, the number of new claims established by frequent claimants had a moderate increase (+2.5%) in the reporting period; while the total amount paid to the claimants in this category fell by 10.7% from FY1718.

In FY1819, long-tenured workers accounted for 22.8% of all new regular claims established while they received 23.1% of the total amount paid. Occasional claimants, on the other hand, proportionally benefited less—they accounted for 54.2% of all new claims established in FY1819 but received 51.6% of the total amount paid. Frequent claimants accounted for 23.0% of total new regular claims in the reporting year and received 25.3% of the total amount paid.

| Claimant category | Number of claims (% share of all EI regular claims) FY1718 |

Number of claims (% share of all EI regular claims) FY1819 |

Number of claims change (%) |

Amount paid - $ millions (% share of total amount paid for EI regular benefits) FY1718 |

Amount paid – $ millions (% share of total amount paid for EI regular benefits) FY1819 |

Amount paid - $ millions change (%) |

|---|---|---|---|---|---|---|

| Long-tenured workers | 310,270 (23.9%) | 294,820 (22.8%) | -5.0% | $3,343.6 (26.5%) | $2,467.4 (23.1%) | -26.2% |

| Occasional claimants | 699,370 (53.8%) | 700,580 (54.2%) | +0.2% | $6,272.5 (49.6%) | $5,505.2 (51.6%) | -12.2% |

| Frequent claimants | 290,070 (22.3%) | 297,310 (23.0%) | +2.5% | $3,024.4 (23.9%) | $2,701.2 (25.3%) | -10.7% |

| Canada | 1,299,710 (100.0%) | 1,292,710 (100.0%) | -0.5% | $12,640.5 (100.0%) | $10,673.8 (100.0%) | -15.6% |

- Note: Data may not add up to the total due to rounding. Percentage change is based on unrounded numbers. Includes claims for which at least $1 of EI regular benefits was paid.

- * See Annex 2.1 for definitions of EI claimant categories referenced in this table.

- Source: Employment and Social Development Canada, Employment Insurance (EI) administrative data. Data are based on a 10% sample of EI administrative data.

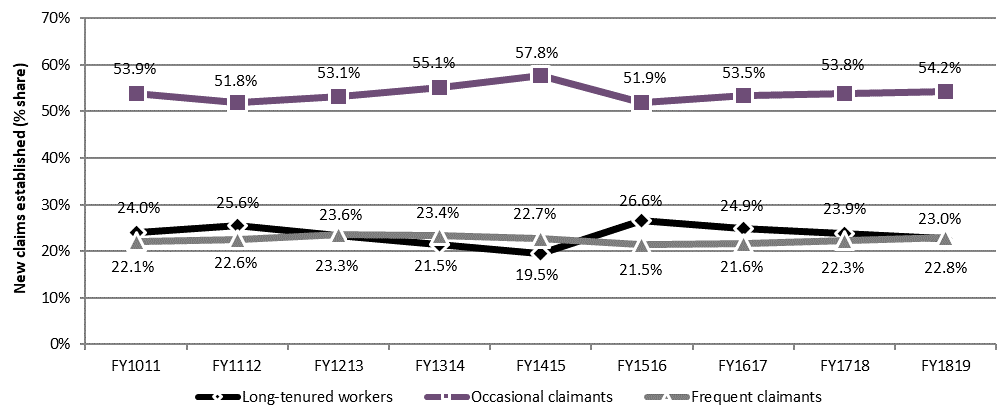

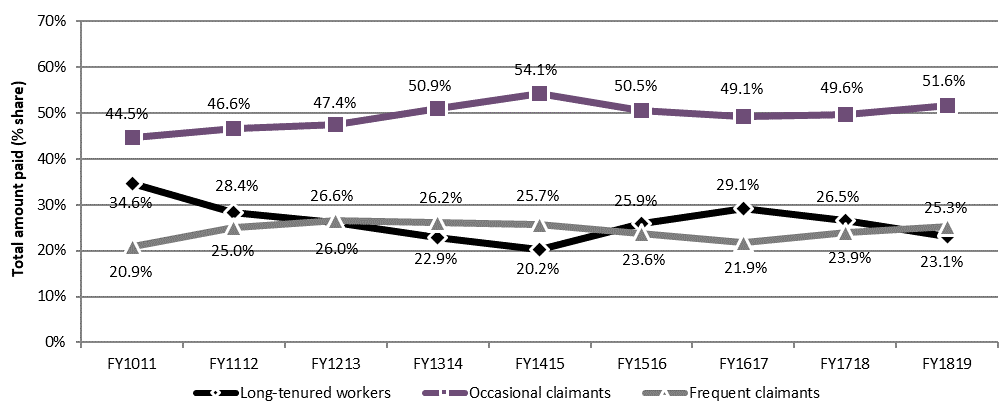

Chart 7 and Chart 8 show the share of new EI regular claims established and the share of total amount paid by claimant categories from FY1011 to FY1819.

Text description of Chart 7

| Claimants | FY1011 | FY1112 | FY1213 | FY1314 | FY1415 | FY1516 | FY1617 | FY1718 | FY1819 |

|---|---|---|---|---|---|---|---|---|---|

| Long-tenured workers | 24.0% | 25.6% | 23.3% | 21.5% | 19.5% | 26.6% | 24.9% | 23.9% | 22.8% |

| Occasional claimants | 53.9% | 51.8% | 53.1% | 55.1% | 57.8% | 51.9% | 53.5% | 53.8% | 54.2% |

| Frequent claimants | 22.1% | 22.6% | 23.6% | 23.4% | 22.7% | 21.5% | 21.6% | 22.3% | 23.0% |

- Note: Includes claims for which at least $1 of EI regular benefits was paid.

- Source: Employment and Social Development Canada, Employment Insurance (EI) administrative data. Data are based on a 10% sample of EI administrative data.

Text description of Chart 8

| Claimants | FY1011 | FY1112 | FY1213 | FY1314 | FY1415 | FY1516 | FY1617 | FY1718 | FY1819 |

|---|---|---|---|---|---|---|---|---|---|

| Long-tenured workers | 34.6% | 28.4% | 26.0% | 22.9% | 20.2% | 25.9% | 29.1% | 26.5% | 23.1% |

| Occasional claimants | 44.5% | 46.6% | 47.4% | 50.9% | 54.1% | 50.5% | 49.1% | 49.6% | 51.6% |

| Frequent claimants | 20.9% | 25.0% | 26.6% | 26.2% | 25.7% | 23.6% | 21.9% | 23.9% | 25.3% |

- Note: Includes claims for which at least $1 of EI regular benefits was paid.

- Source: Employment and Social Development Canada, Employment Insurance (EI) administrative data. Data are based on a 10% sample of EI administrative data.

Employment Insurance regular claims by hours of insurable employment and unemployment rate in the Employment Insurance economic region of establishment

One of the eligibility conditions for EI regular benefits is the accumulation of enough hours of insurable employment during the qualifying period. The number of required hours depends on the unemployment rate in the EI economic region where the claimant resides and is known as the Variable Entrance Requirement (VER). The higher the unemployment rate in a given region, the lower the number of hours needed to qualify for EI regular benefits (see Annex 2.2 for the full breakdown of required number of hours of insurable employment with corresponding regional rate of unemployment). A detailed discussion is provided in subsection 2.2.2 on eligiblity and access to EI regular benefits.

Variable entrance requirement

In order to qualify for EI regular benefits, a worker must accumulate between 420 and 700 hours of insurable employment in the qualifying period, depending on the applicable regional rate of unemployment where the claimant resides. As outlined below, a higher regional unemployment rate corresponds to a lower required number of hours of insurable employment.

| EI regional unemployment rate | Variable entrance requirement |

|---|---|

| 6.0% and under | 700 hours |

| 6.1% to 7.0% | 665 hours |

| 7.1% to 8.0% | 630 hours |

| 8.1% to 9.0% | 595 hours |

| 9.1% to 10.0% | 560 hours |

| 10.1% to 11.0% | 525 hours |

| 11.1% to 12.0% | 490 hours |

| 12.1% to 13.0% | 455 hours |

| More than 13.0% | 420 hours |

Table 10 outlines the distribution of EI regular claims for the past 5 years by the number of hours of insurable employment used to qualify for EI regular benefits. Consistent with previous years, claimants who accumulated more than 1,820 hours of insurable employment accounted for the largest share (25.0%) of total new EI regular claims established in FY1819. This was relatively unchanged from the previous year. On the other hand, claimants with less than 700 hours of insurable employment represented the smallest share (4.7%), decreasing by 0.4 percentage points compared to the previous year. All of the categories shown in Table 10 experienced a change in their share in FY1819 that was less than 1.0 percentage point compared to the previous year.

| Number of hours of insurable employment in the qualifying period | FY1415 | FY1516 | FY1617 | FY1718 | FY1819 |

|---|---|---|---|---|---|

| Less than 700 hours | 64,390 (4.8%) | 67,170 (4.7%) | 76,340 (5.8%) | 66,150 (5.1%) | 60,150 (4.7%) |

| 700 to 979 hours | 203,690 (15.2%) | 207,610 (14.5%) | 216,650 (16.4%) | 215,600 (16.6%) | 212,640 (16.4%) |

| 980 to 1,259 hours | 256,210 (19.1%) | 264,500 (18.5%) | 242,610 (18.4%) | 234,850 (18.1%) | 239,650 (18.5%) |

| 1,260 to 1,539 hours | 245,530 (18.3%) | 260,870 (18.2%) | 239,030 (18.1%) | 239,600 (18.4%) | 243,490 (18.8%) |

| 1,540 to 1,819 hours | 218,840 (16.3%) | 235,120 (16.4%) | 207,440 (15.7%) | 211,880 (16.3%) | 213,480 (16.5%) |

| 1,820 hours and more | 353,950 (26.4%) | 395,820 (27.7%) | 339,060 (25.7%) | 331,630 (25.5%) | 323,300 (25.0%) |

| Canada | 1,342,610 (100.0%) | 1,431,090 (100.0%) | 1,321,130 (100.0%) | 1,299,710 (100.0%) | 1,292,710 (100.0%) |

- Note: Data may not add up to the total due to rounding. Includes claims for which at least $1 of EI regular benefits was paid.

- Source: Employment and Social Development Canada, Employment Insurance (EI) administrative data. Data are based on a 10% sample of EI administrative data.

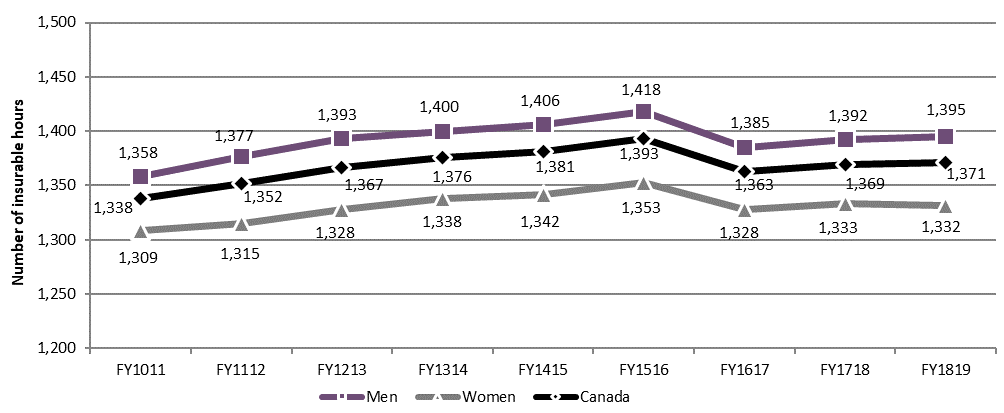

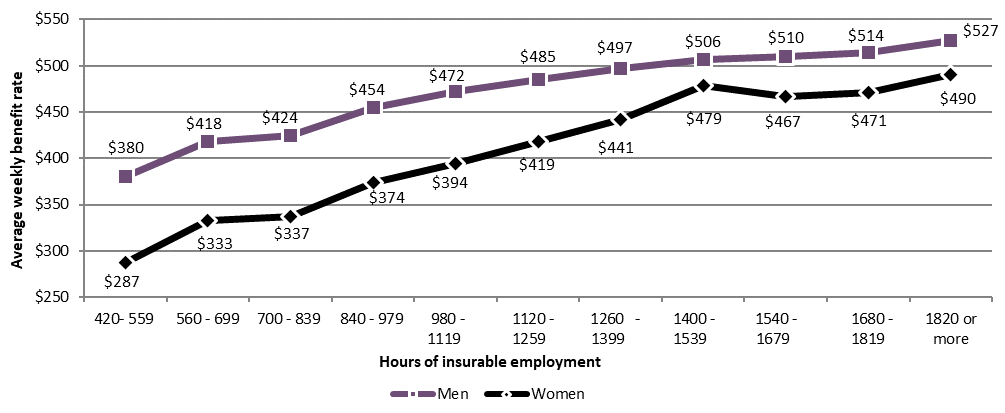

Chart 9 shows the average number of hours of insurable employment per claim receiving EI regular benefits from FY1011 to FY1819 by gender. In the reporting period, on average in Canada, claimants had accumulated 1,371 hours of insurable employment during their qualifying period, up from 1,369 hours in FY1718. The difference between the average number of hours of insurable employment for men and women has stayed around 60 hours over the years. In FY1819, men on average had 63 more hours of insurable employment than women. This can be attributable to the fact that a higher proportion of women work in part-time and/or temporary jobs than men, and thus accumulate fewer hours of insurable employment on average.

Text description of Chart 9

| Claimants | FY1011 | FY1112 | FY1213 | FY1314 | FY1415 | FY1516 | FY1617 | FY1718 | FY1819 |

|---|---|---|---|---|---|---|---|---|---|

| Men | 1,358 | 1,377 | 1,393 | 1,400 | 1,406 | 1,418 | 1,385 | 1,392 | 1,395 |

| Women | 1,309 | 1,315 | 1,328 | 1,338 | 1,342 | 1,353 | 1,328 | 1,333 | 1,332 |

| Canada | 1,338 | 1,352 | 1,367 | 1,376 | 1,381 | 1,393 | 1,363 | 1,369 | 1,371 |

- Note: Includes claims for which at least $1 of EI regular benefits was paid.

- Source: Employment and Social Development Canada, Employment Insurance (EI) administrative data. Data are based on a 10% sample of EI administrative data.

In FY1819, claimants who were aged between 25 and 44 years accumulated the highest number of hours of insurable employment during their qualifying period (1,406 hours), followed by those who were 45 to 54 years old (1,395 hours). Older claimants (that is, 55 years old and above), on the other hand, accumulated the lowest number of hours of insurable employment (1,308 hours) in FY1819, closely followed by younger claimants aged less than 25 years (1,315 hours).

Furthermore, the average number of hours of insurable employment per claim during the qualifying period in FY1819 varied by province and territory as well. Generally, the number of hours of insurable employment per claim in the Atlantic provinces and the territories tend to be lower than other regions. This trend continued in the reporting period—the lowest average hours of insurable employment per claim among all provinces and territories was observed in Newfoundland and Labrador (1,126 hours), followed by Nunavut (1,180 hours), Prince Edward Island (1,182 hours) and New Brunswick (1,236 hours). On the other hand, the highest average hours of insurable employment per claim in FY1819 was observed in Alberta (1,462 hours), followed by Ontario (1,436 hours) and British Columbia (1,403 hours).

Table 11 outlines the number and distribution of new claims established for EI regular benefits as well as the labour force and the unemployed population by regional unemployment rate. The share of new regular claims established in EI economic regions where the unemployment rate was between 0.1% and 7.0% was higher (+80,450 claims) in FY1819 compared to previous fiscal years. This increase can be mainly attributable to the increase in the number of EI regular claims established in EI economic regions of Alberta (+71,990 claims) and Newfoundland and Labrador (+ 15,080 claims) where the unemployment rate thresholds were less than or equal to 7%. Table 11 also shows that, in FY1819, EI regular claims established and the unemployed population were similarly spread across regional unemployment rate categories.

| Unemployment rate | EI regular claims established (,000) (% share of total claims) FY1415 |

EI regular claims established (,000) (% share of total claims) FY1516 |

EI regular claims established (,000) (% share of total claims) FY1617 |

EI regular claims established (,000) (% share of total claims) FY1718 |

EI regular claims established (,000) (% share of total claims) FY1819 |

Labour force (,000) (% share of labour force) FY1819 |

Number of unemployed (,000) (% share of unemployed) FY1819 |

|---|---|---|---|---|---|---|---|

| 0.1% to 6% | 273.4 (20.4%) | 218.0 (15.2%) | 171.4 (13.0%) | 384.2 (29.6%) | 411.2 (31.8%) | 8,222.6 (40.9%) | 411.7 (31.9%) |

| 6.1% to 7% | 158.1 (11.8%) | 363.7 (25.4%) | 363.2 (27.5%) | 425.6 (32.7%) | 479.0 (37.1%) | 8,389.4 (41.7%) | 533.4 (41.3%) |

| 7.1% to 8% | 329.9 (24.6%) | 279.0 (19.5%) | 299.0 (22.6%) | 134.8 (10.4%) | 129.4 (10.0%) | 1,735.0 (8.6%) | 129.1 (10.0%) |

| 8.1% to 9% | 236.5 (17.6%) | 216.3 (15.1%) | 169.3 (12.8%) | 110.9 (8.5%) | 40.8 (3.2%) | 527.7 (2.6%) | 43.8 (3.4%) |

| 9.1% to 10% | 78.5 (5.8%) | 75.7 (5.3%) | 65.5 (5.0%) | 31.7 (2.4%) | 13.9 (1.1%) | 175.9 (0.9%) | 16.7 (1.3%) |

| 10.1% to 11% | 56.0 (4.2%) | 50.4 (3.5%) | 35.4 (2.7%) | 8.0 (0.6%) | 37.0 (2.9%) | 378.6 (1.9%) | 40.2 (3.1%) |

| 11.1% to 12% | 44.4 (3.3%) | 16.7 (1.2%) | 21.4 (1.6%) | 60.1 (4.6%) | 49.0 (3.8%) | 174.6 (0.9%) | 20.0 (1.5%) |

| 12.1% to 13% | 7.7 (0.6%) | 43.9 (3.1%) | 35.3 (2.7%) | 13.4 (1.0%) | 4.1 (0.3%) | 32.7 (0.2%) | 4.2 (0.3%) |

| 13.1% to 14% | 0.5 (0.0%) | 16.9 (1.2%) | 11.4 (0.9%) | 28.2 (2.2%) | 7.0 (0.5%) | 28.8 (0.1%) | 3.8 (0.3%) |

| 14.1% to 15% | 25.9 (1.9%) | 23.7 (1.7%) | 38.2 (2.9%) | 24.0 (1.8%) | 17.9 (1.4%) | 58.0 (0.3%) | 8.6 (0.7%) |

| 15.1% to 16% | 25.1 (1.9%) | 32.0 (2.2%) | 25.4 (1.9%) | 10.3 (0.8%) | 25.0 (1.9%) | 75.7 (0.4%) | 11.8 (0.9%) |

| 16% or higher | 107.0 (8.0%) | 94.8 (6.6%) | 85.8 (6.5%) | 68.6 (5.3%) | 78.6 (6.1%) | 319.7 (1.6%) | 69.0 (5.3%) |

| Canada | 1,342.6 (100.0%) | 1,431.1 (100.0%) | 1,321.1 (100.0%) | 1,299.7 (100.0%) | 1,292.7 (100.0%) | 20,118.6 (100.0%) | 1,292.3 (100.0%) |

- Note: Data may not add up to the total due to rounding. Includes claims for which at least $1 of EI regular benefits was paid.

- * Unemployment rates used for the Employment Insurance program are a moving average of seasonally adjusted rates of unemployment produced by Statistics Canada, as per section 17 of the Employment Insurance Regulations.

- Source: Employment and Social Development Canada, Employment Insurance (EI) administrative data and Statistics Canada, special tabulations from the Labour Force Survey. EI data are based on a 10% sample of EI administrative data.

Claimant obligations to search for and accept suitable employment