Wage Earner Protection Program for trustees or receivers: Eligibility

2. Eligibility

Obtaining payroll information

Trustees/receivers require access to payroll information to help identify individuals and calculate eligible wages. Payroll officer(s) or any person in possession of payroll records must provide assistance within 10 days of your request for information.

When payroll information is not available, use “due diligence” in locating for the information needed. You should call the WEPP information line at 1-866-683-6516 (TTY: 1-800-926-9105) if you encounter issues or have questions.

Types of eligible wages

The following amounts are considered eligible wages under the WEPP:

- wages (salaries, commissions, compensation for services rendered, gratuities accounted for by the former employer, production bonuses and shift premiums) that were earned during the eligibility period

- disbursements of a travelling salesperson properly incurred in and about the business of the former employer earned during the eligibility period

- vacation pay earned during the eligibility period

- termination pay and severance pay for employment that ended either during the eligibility period or prior to the discharge of the trustee/receiver

Calculating eligible wages

Wages, vacation pay and disbursements of a travelling salesperson are restricted to amounts earned during the eligibility period. For example, if an employee is entitled to 2 weeks of vacation per year (in other words 10 days), the amount they could receive for vacation pay under the WEPP would be only the portion of the vacation pay that was earned during the eligibility period. If the eligibility period is for 6 months, then in this example only 1 week of vacation pay would be eligible, and not the full year.

To calculate termination pay and severance pay, refer to the applicable Federal, Provincial or Territorial Labour Standards legislation. Alternatively, these entitlements may also be set out in an employment contract or a collective agreement.

For each individual, you must determine eligible wages owed, inform them of the WEPP and submit a Trustee Information Form (TIF) including in circumstances where:

- an individual is on maternity, parental or sick leave at the time of the bankruptcy or receivership because the employment relationship does not generally end as a result of being on leave

- an individual worked for a sole proprietorship or partnership

- an individual was a manager, an officer or a director of their former employer

- an individual had a controlling interest in the business of their former employer payment or non-payment of wages by their former employer

- an individual was not dealing at arm's length with any person who would be ineligible according to any of the previous criteria

Other WEPP qualifying insolvency proceedings

As per the changes to the WEPP Regulations, 3 other WEPP qualifying insolvency proceedings have been introduced:

- proposal under the Bankruptcy & Insolvency Act (BIA) (Division 1 Part III). Note: this also includes a Notice of Intention to file a proposal under the BIA (Division 1 Part III)

- certain Companies’ Creditors Arrangement Act (CCAA) proceedings

- certain foreign proceedings

For these other proceedings, the former employer must have terminated all of its employees, in Canada, other than any retained to wind down its business operations. The trustee/receiver appointed may be required to provide Court documents to validate these proceedings.

For foreign proceedings, if you do not have an Estate ID (that is, Office of the Superintendent of bankruptcy number), please contact the WEPP information line at 1-866-683-6516 for help.

Eligibility period

The wages, other than termination pay and severance pay, owed to the individual must have been earned during the eligibility period. The WEPP eligibility period is the 6-month period before the bankruptcy or receivership, or other qualifying insolvency proceeding.

WEPP qualifying restructuring proceedings

WEPP qualifying restructuring proceedings are:

- Notice of Intention (NOI) to make a proposal under Division I Part III of the BIA, and/or

- a proposal under Division I Part III of the BIA, and/or

- proceedings under the CCAA

If the bankruptcy, receivership, or other WEPP qualifying insolvency proceeding is preceded by a WEPP qualifying restructuring proceeding, then the eligibility period would be:

- the period starting 6 months before the restructuring proceeding, and

- ending on the date of the bankruptcy, receivership, or date the court determined that all former employees in Canada had been terminated, other than any retained to wind down its business operations

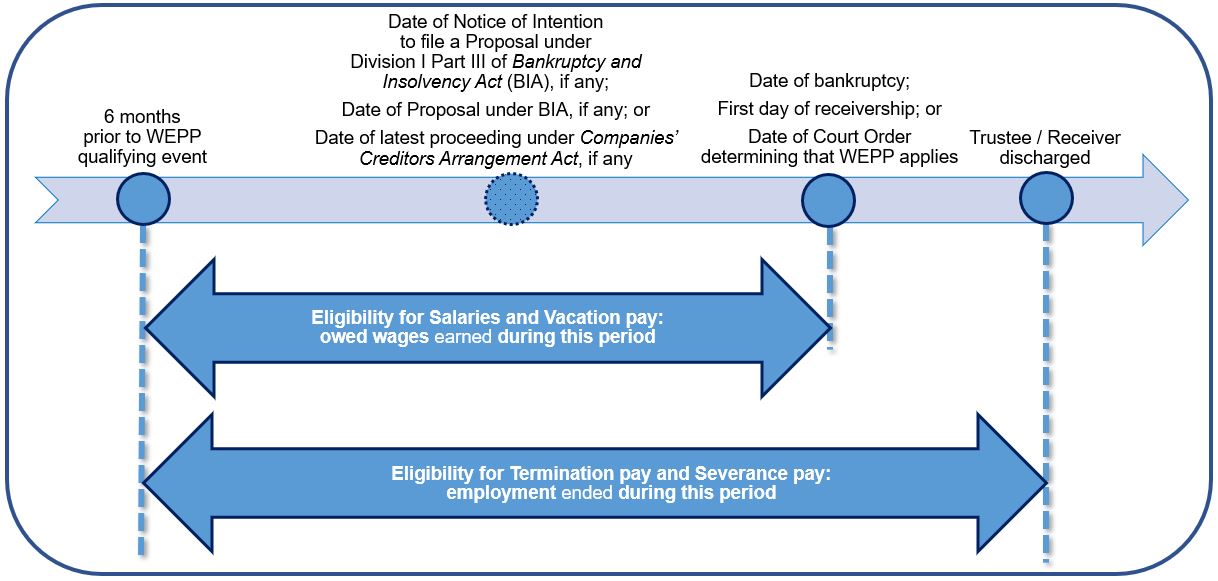

Text description

Timeline showing that the eligibility period for wages starts 6 months prior to the WEPP qualifying event, which may be the date of:

- notice of intention to file a proposal under Division I of Part III of the Bankruptcy and Insolvency Act (BIA)

- actual proposal under the BIA

- latest proceeding under the Companies’ Creditors Arrangement Act

- actual bankruptcy

- first day of receivership, or

- WEPP qualifying court order

The eligibility period for wages terminates on the date of:

- actual bankruptcy

- first day of receivership, or

- WEPP qualifying court order

An arrow is showing that wages (such as salaries and vacation pay) earned between these two dates may be eligible for payment.

Another arrow is showing that the eligibility period for termination pay and severance pay, also starts 6 months prior to the WEPP qualifying event and extends until the discharge of the trustee or receiver. If the applicant’s employment ends during this period, they may be eligible to WEPP payment for termination pay and severance pay.

Continued to work for the trustee/receiver after the date of the bankruptcy, receivership, or other WEPP qualifying insolvency proceeding

Employees sometimes continue to work after the date of the bankruptcy/receivership/ date the court determined that all former employees in Canada had been terminated, other than any retained to wind down its business operations. These individuals are eligible for WEPP when their employment ends, as long as it is prior to the trustee/receiver being discharged.

For WEPP enquiries, call the information line at 1-866-683-6516 (TTY: 1-800-926-9105) or visit a Service Canada Centre.

Employee entitlements in the case of an employer subject to 2 WEPP qualifying insolvency proceedings

The Wage Earner Protection Program Act provides that when 2 WEPP qualifying insolvency proceedings occur (for example, bankruptcy and receivership), the amount to be paid is the greater amount.

The trustee/receiver is required to provide a Trustee Information Form for each employee under both proceedings. Service Canada will then determine the most beneficial payment.

Income tax

Income tax is not deducted directly from WEPP payments. However, individuals will be informed by Service Canada that they are required to report their WEPP payment as taxable income on their annual tax return. Service Canada will issue to WEPP recipients, a T4A slip and a Relevé 1 for Quebec residents by February 28th of the year following the payment.

Statement of crown debt repaid

In the event of an overpayment, the amount reported on T4A/T4AQ would not change.

When the debt is re-paid, a separate document called a Statement of crown debt repaid will be issued.

Definitions

-

Employee

The term "employee" is not defined in the Wage Earner Protection Program Act. Where there is uncertainty as to whether an individual is an employee for the purposes of the legislation, trustees/receivers may contact the Labour and Employment Standards office in the relevant jurisdiction.

-

Managerial position

A “managerial position” is defined in the Wage Earner Protection Program Regulations as one where the individual's responsibilities included making binding financial decisions which affected the business or regarding the payment or non-payment of wages by the former employer.

However, simply because an employee is given the title of "manager", it does not mean that the individual is automatically excluded from WEPP. A trustee/receiver information form must be filed for the individual.