FHSA taxes payable, assessments and reassessments

You have to file a return and pay the taxes owing when you have taxes payable on your first home savings account (FHSA). If you do not file the return on time, the Canada Revenue Agency (CRA) may assess your taxes owing based on its records and send you a notice of assessment.

You may contact the CRA if you disagree with the notice of assessment or notice of reassessment that you receive about your FHSAs.

Tax payable on FHSAs

In certain circumstances, there might be taxes payable with respect to your FHSA. For more information on when or, how these taxes are payable, and by whom, go to:

- Tax payable on excess FHSA amount

- Tax payable on non-qualified investments

- Tax payable on prohibited investments

- Refund of taxes paid on non-qualified or prohibited investments

- Tax payable on an advantage

Where one or more FHSA taxes are payable, an RC728, First Home Savings Account (FHSA) Return must be completed and filed by June 30 of the year following the calendar year in which the tax arose.

FHSA payment of taxes

Most FHSA holders have no tax payable related to their FHSAs, and no RC728 return has to be filed.

However, when FHSA taxes are applicable for a year, you have to file an RC728 return and pay the taxes owing no later than June 30 after the end of the year in which there are FHSA taxes payable.

When an individual dies before the due date of an RC728 return, both the filing and the balance due dates will be the later of:

- June 30

- 6 months after the date of death

If you do not file by this due date, a penalty and interest charge will apply, and the CRA will continue to charge interest until you pay the balance owing.

Exception to the due date:

When a due date falls on a Saturday, Sunday, or public holiday recognized by the CRA, an exception to the due date will apply. For more information, go to Filing due dates for the 2025 tax return.

Completing your Form RC728 - Schedule A, Excess FHSA Amounts

You must complete the Form RC728 - Schedule A, Excess FHSA Amounts if you have excess FHSA amount and attach the completed schedule to your RC728 return. Refer to the schedule for instructions on how to complete it.

The explanation and examples below refer to the 2025 tax year. If you need to file an RC728 for a previous year, refer to Form RC728, 2024 First Home Savings Account (FHSA) Return.

-

Example: How to complete your RC728 - Schedule A, 2025 Excess FHSA Amounts

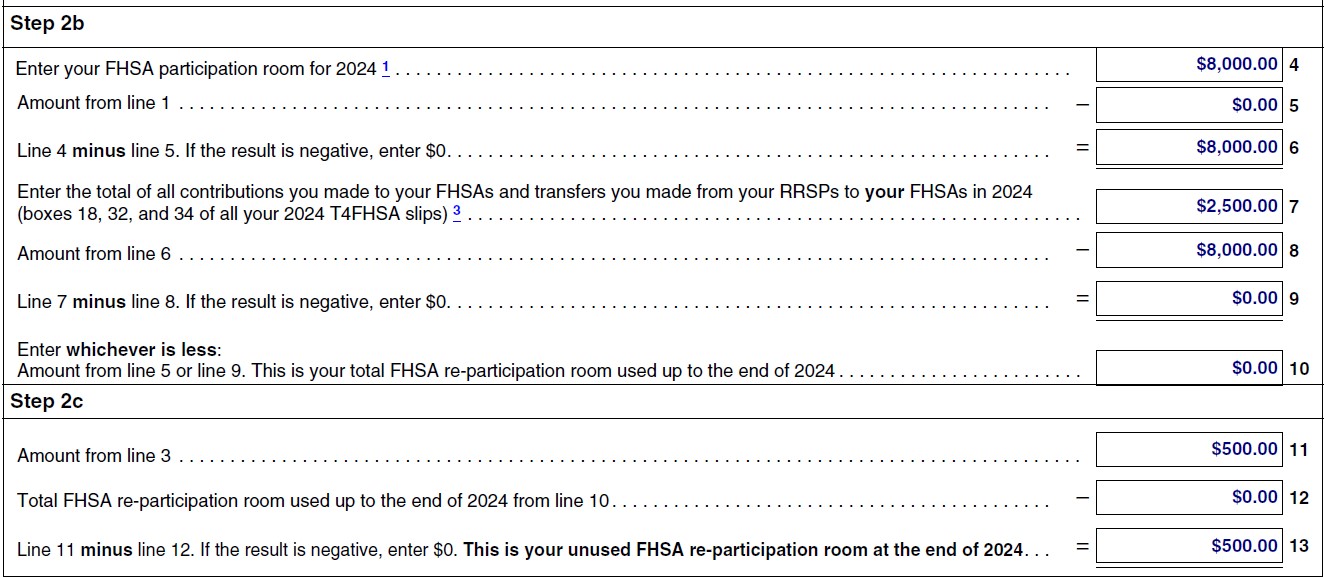

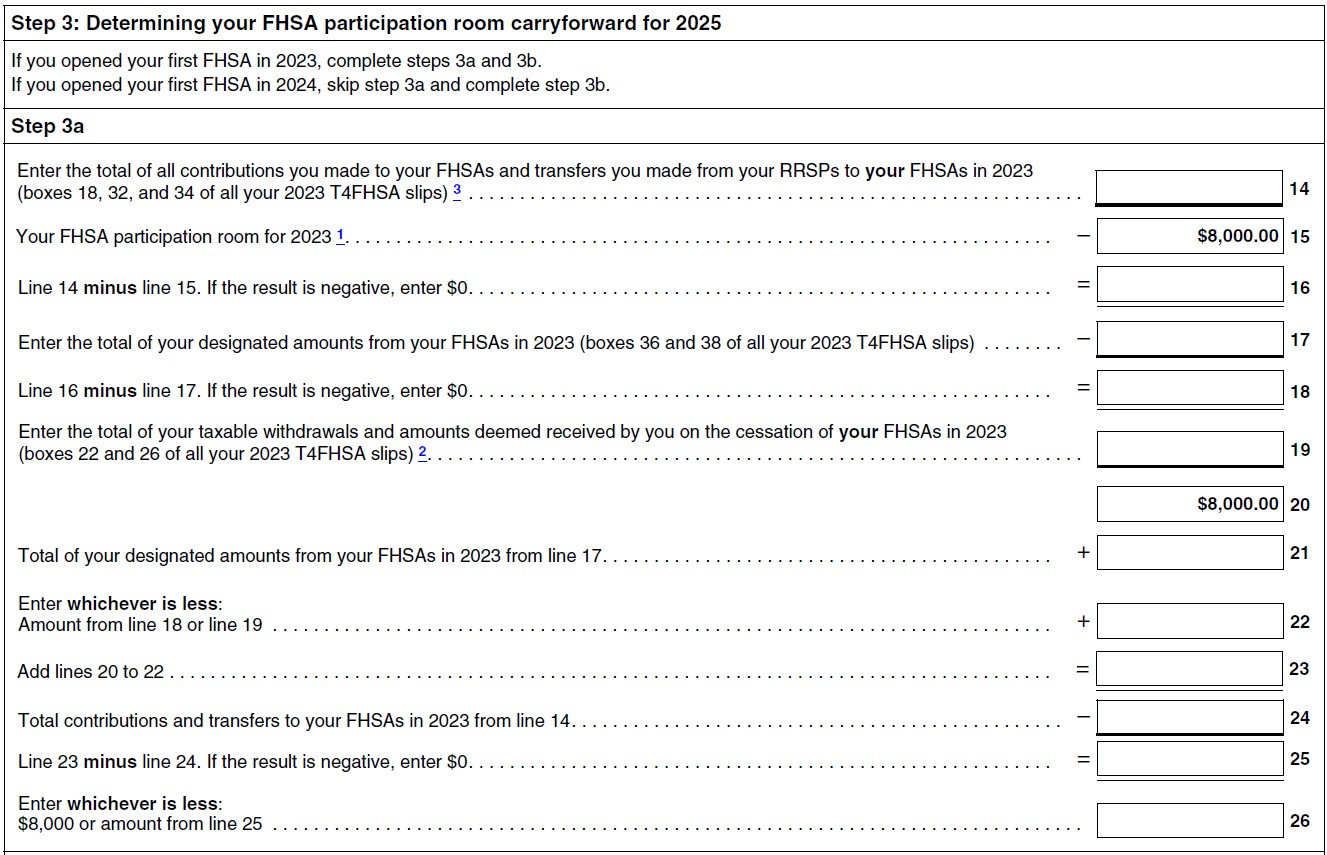

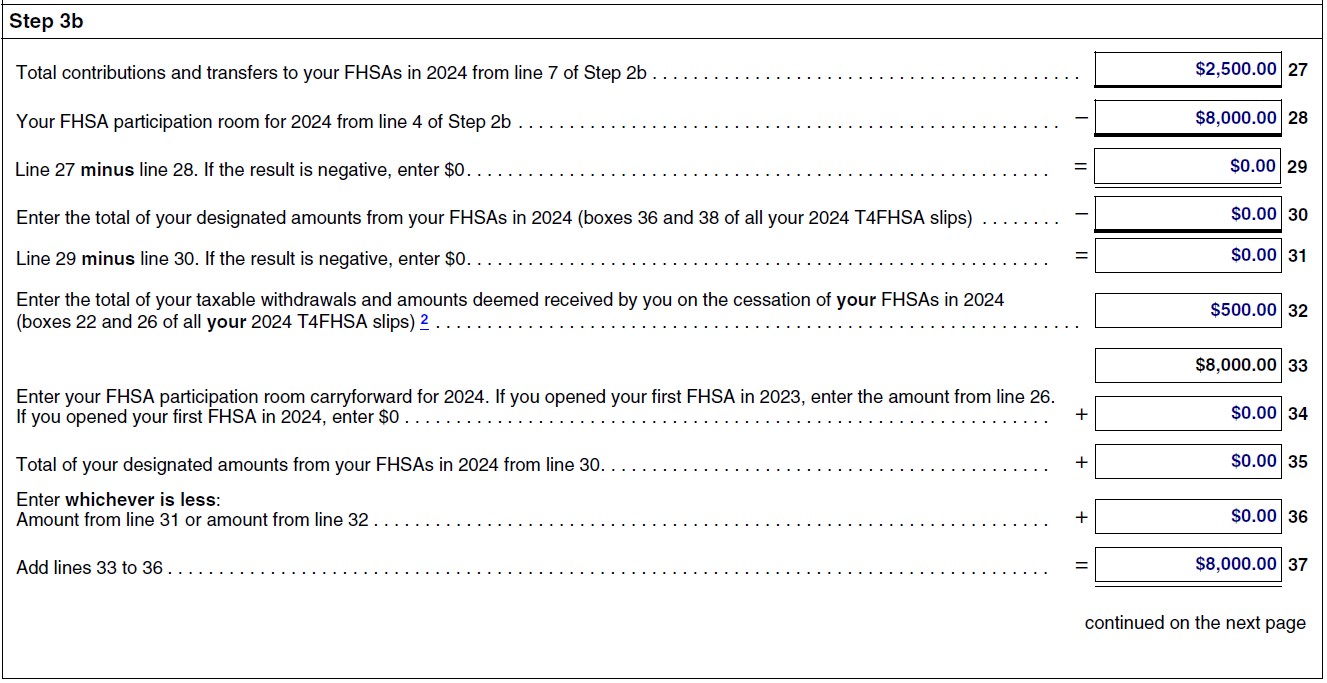

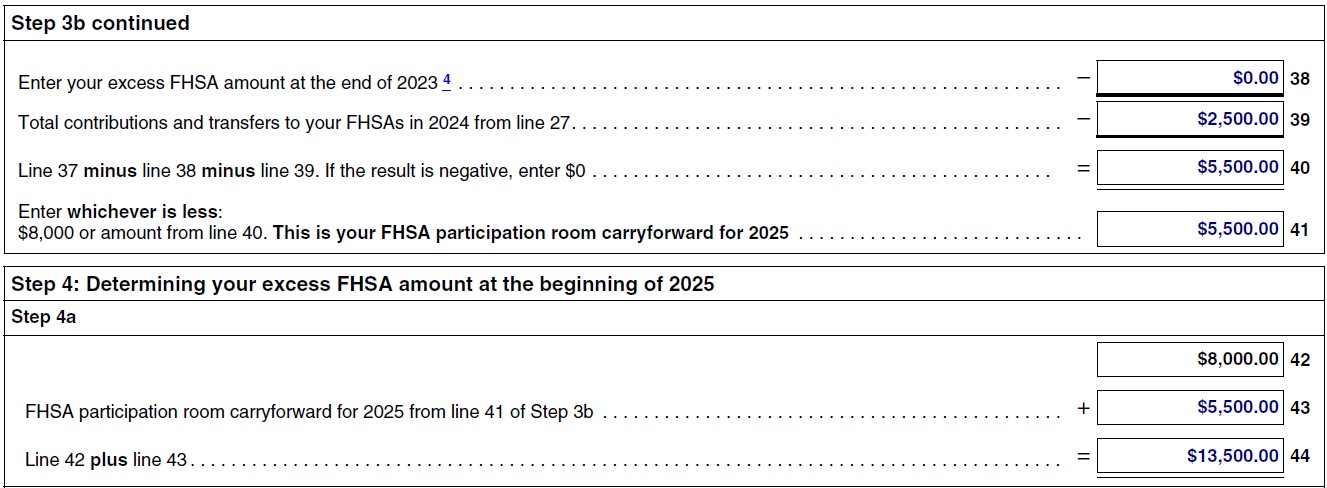

Luffy opens an FHSA on May 5, 2024. Luffy’s FHSA participation room for 2024 is $8,000 because this is the first year he opened an FHSA.

Luffy makes the following FHSA transactions in 2024:

May 15, 2024: $2,500 contribution

December 24, 2024: $500 taxable withdrawal

Luffy’s FHSA participation room for 2025 is $14,000. For more information on calculating the FHSA participation room, go to How to calculate your FHSA participation room.

Luffy makes the following FHSA transactions in 2025:

January 31, 2025: $8,000 contribution

August 9, 2025: $7,000 transfer from his RRSP to his FHSA

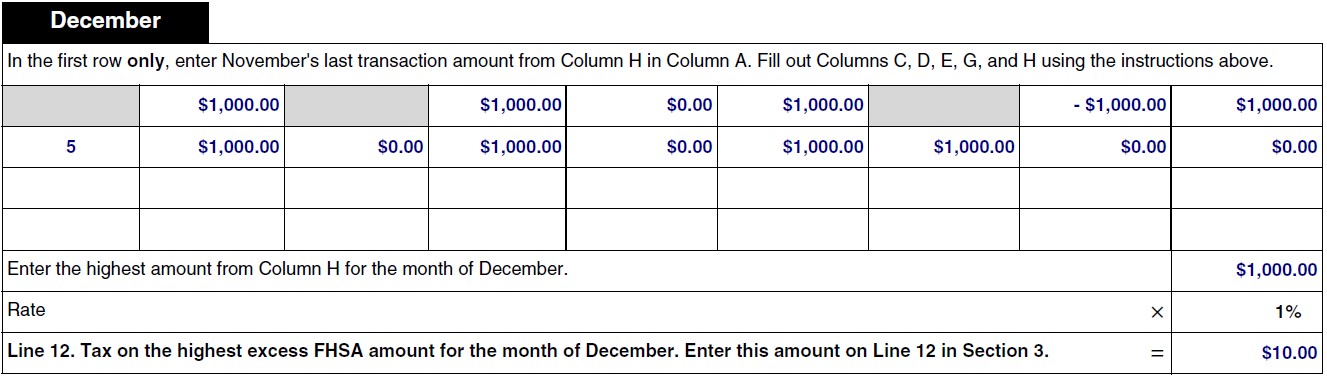

On December 5, 2025, Luffy realizes that he has an excess FHSA amount. That same day, he fills out Form RC727, Designate an Excess FHSA Amount as a Withdrawal from your FHSA or as a Transfer to your RRSP or RRIF and gives the form to his FHSA issuer. The designated withdrawal of $1,000 is completed on the same day.

Since Luffy has excess FHSA amount in 2025, he must fill out Form RC728 - Schedule A, 2025 Excess FHSA Amounts, and attach it to his RC728 return.

This is how Luffy fills out his Form RC728 - Schedule A for 2025.

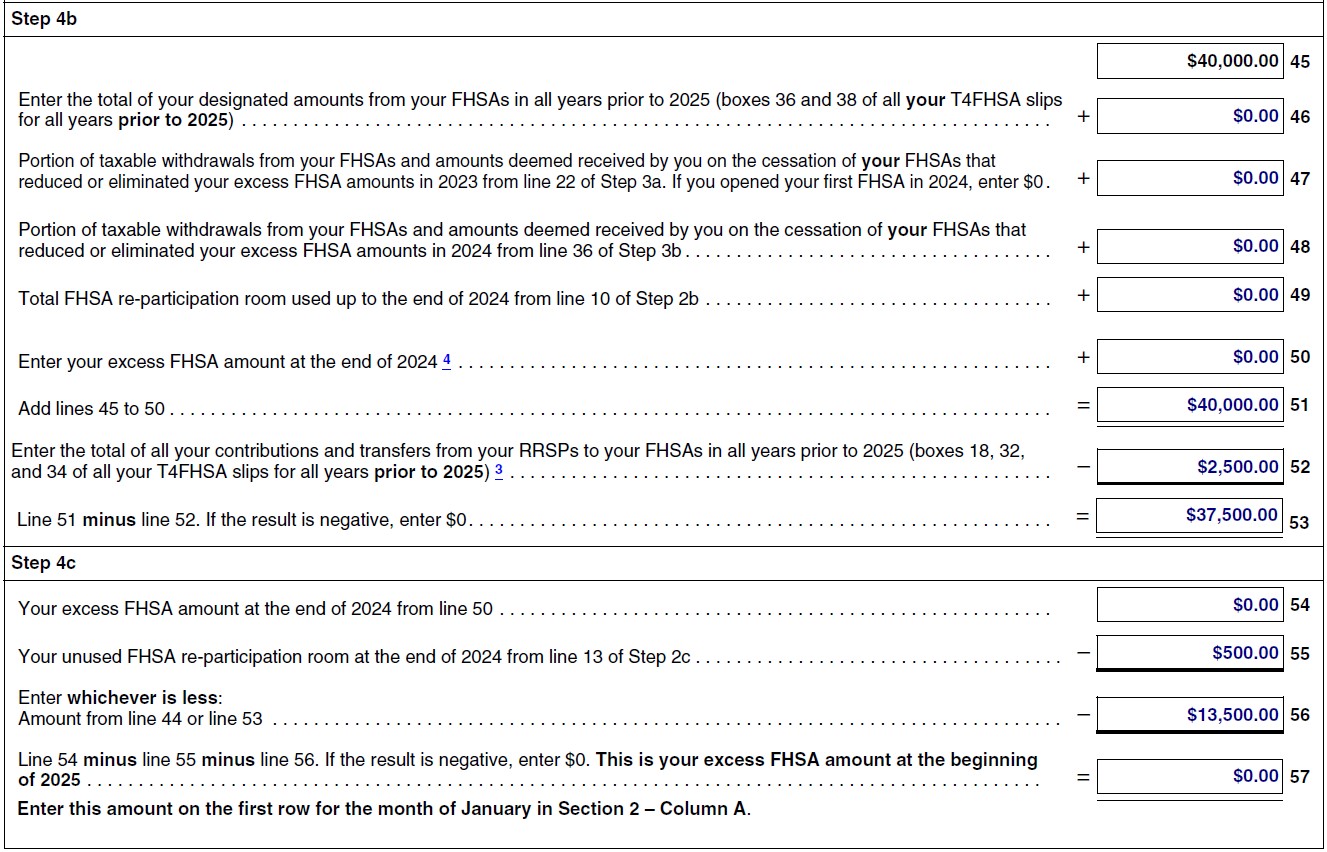

Section 1:

Luffy completes Section 1 to determine his excess FHSA amount and his FHSA participation room at the beginning of 2025.

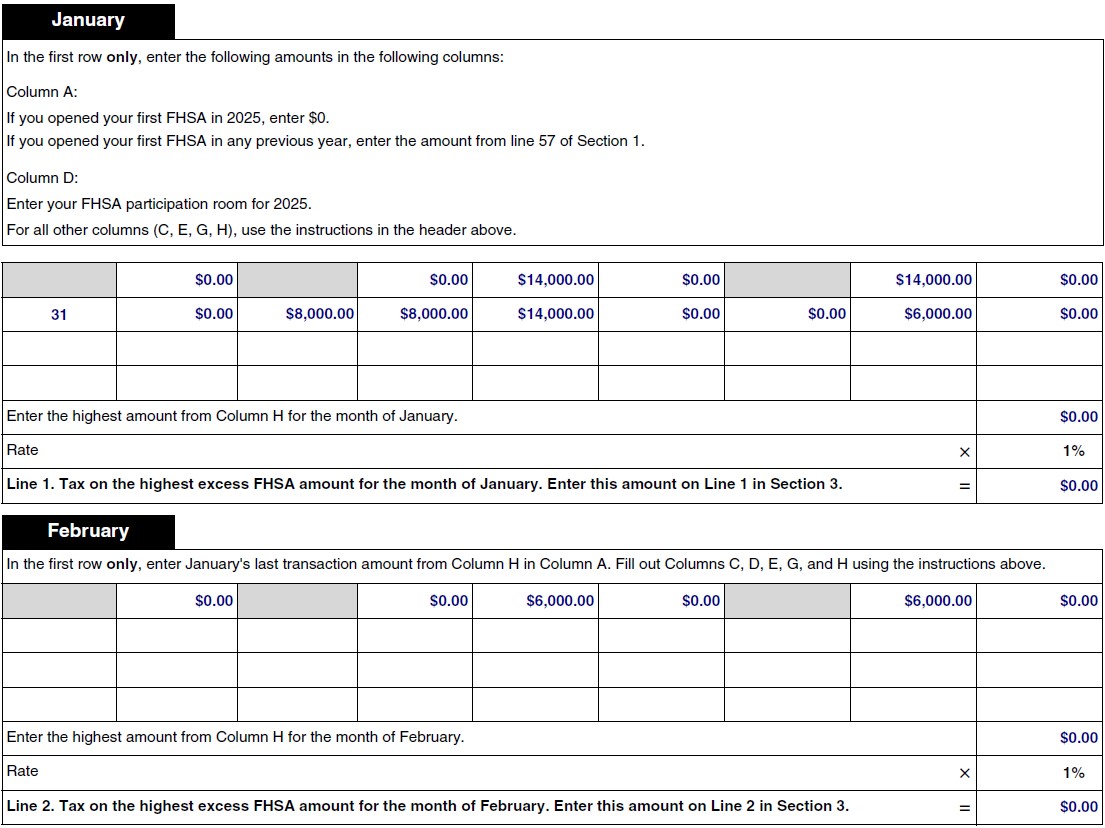

He enters his excess FHSA amount at the beginning of 2025 on the first row for the month of January in Column A of Section 2 and his FHSA participation room at the beginning of 2025 on the first row for the month of January in Column D of Section 2.

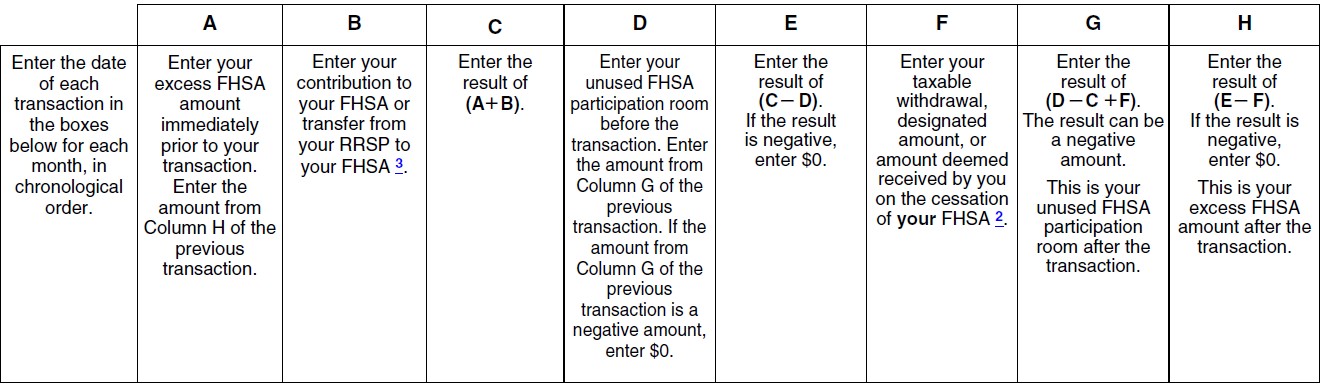

Section 2:

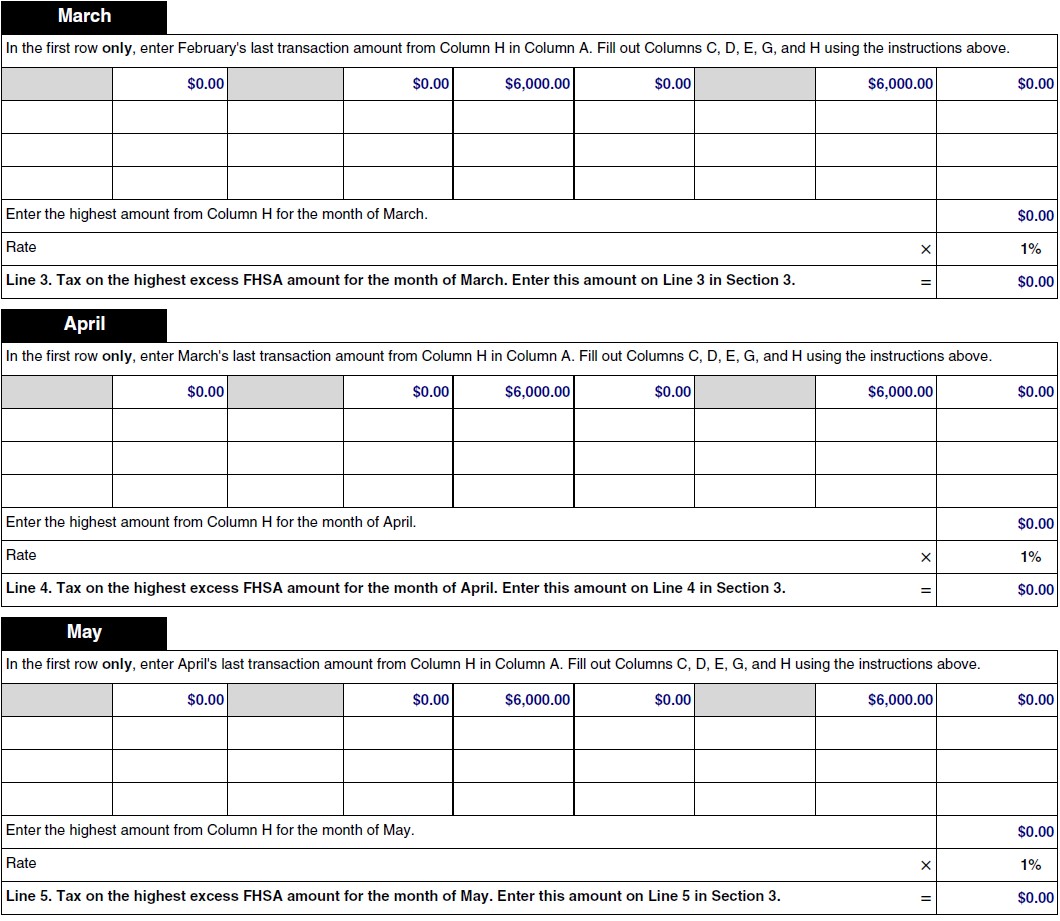

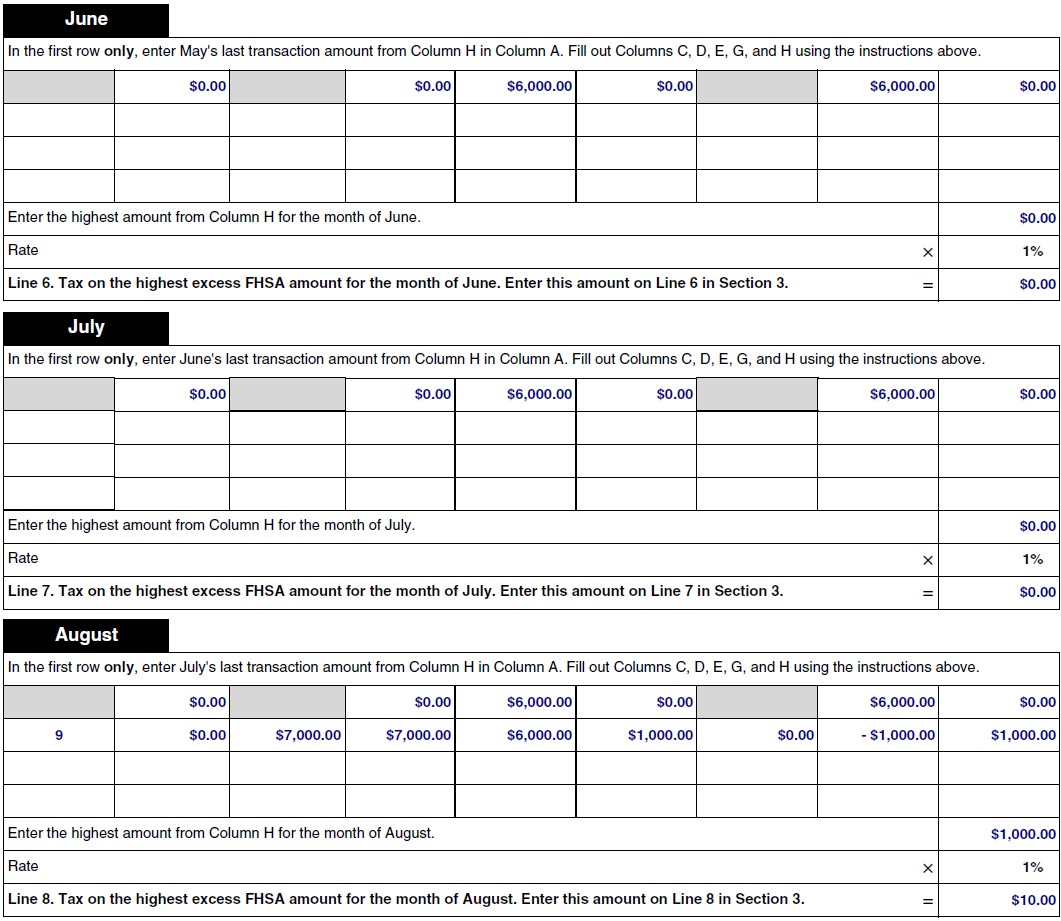

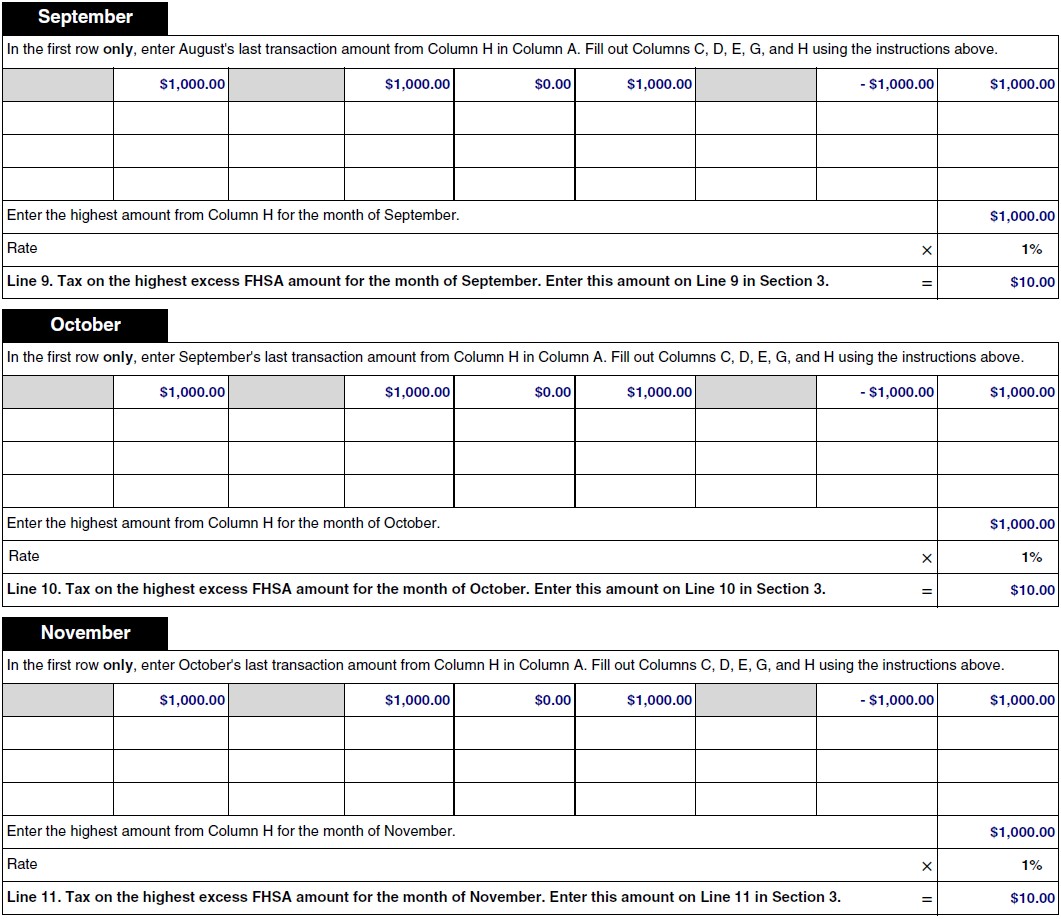

Luffy completes the chart from January to December even though he only made FHSA transactions in January, August, and December.

In Column A of the first row for the month of January, he entered the result of the calculation from line 57 of Section 1.

In Column D of the first row for the month of January, he entered his FHSA participation room for 2025 from his 2025 FHSA participation room statement.

Luffy completes the chart from January to December even though he only made FHSA transactions in January, August, and December.

In Column A of the first row for the month of January, he entered the result of the calculation from line 37 of Section 1.

In Column D of the first row for the month of January, he entered his FHSA participation room for 2025 from his 2025 FHSA participation room statement.

Section 3:

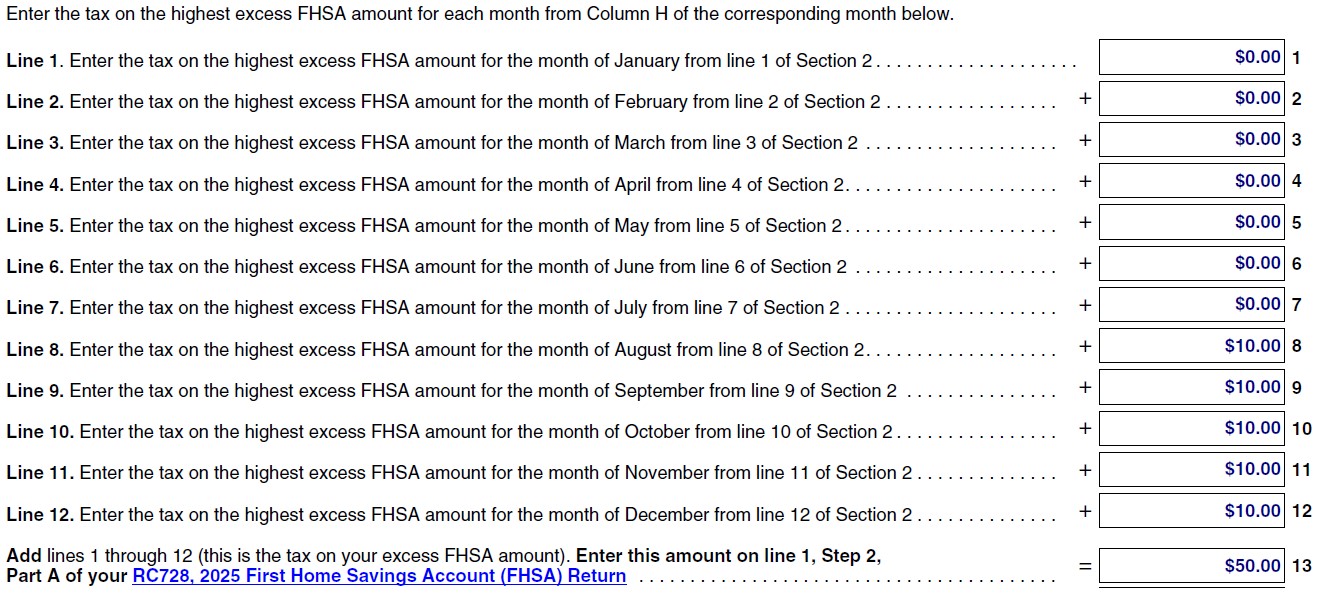

Luffy enters the tax on the highest excess FHSA amount for each month on lines 1 to 12.

Luffy adds the total of lines 1 through 12 and enters it on line 13. This is the tax on Luffy’s excess FHSA amount.

Luffy enters $50 on line 1 in Step 2, Part A of his RC728 return.

FHSA assessments and reassessments

If an RC728 return is required but has not been filed, we may use information provided by your issuers to calculate any tax payable by you.

Once the CRA has assessed your RC728 return, the CRA will send you a notice of assessment showing the amount of taxes payable, and any related penalties and interest.

Once your RC728 return has been assessed, the CRA may reassess your return and send you a notice of reassessment at any time within three years of the date of your notice of assessment. The CRA can do this in either of the following circumstances:

- You bring to the CRA’s attention new information or an error in your return or assessment

- The CRA finds an error during a review of your return, or a return related to yours

What to do if you disagree with your FHSA notice of assessment or reassessment

If you disagree with the assessment or reassessment of your FHSA taxes payable, you may ask for an explanation by contacting the Canada Revenue Agency (CRA).

Also, you can ask for an adjustment by sending a signed letter to the FHSA Processing Unit at one of the addresses listed below:

If your residential address is based in Ontario, Prince Edward Island, Newfoundland and Labrador, Yukon, Nunavut, Northwest Territories and the following Quebec cities: Montreal, Quebec City, Laval, Sherbrooke, Gatineau, and Longueuil, send the signed letter to:

Canada Revenue Agency

Sudbury Tax Centre

FHSA Processing Unit

Post Office Box 20000, Station A

Sudbury ON P3A 5C1

If your residential address is based in Manitoba, Saskatchewan, Alberta, British Columbia, Nova Scotia, New Brunswick and the remaining areas of the province of Quebec not listed under the Sudbury Tax Centre, send the signed letter to:

Canada Revenue Agency

Winnipeg Tax Centre

FHSA Processing Unit

Post Office Box 14000, Station Main

Winnipeg MB R3C 3M2

If you send the CRA a letter, include all necessary documents to support your request (if you did not already provide them) and state the changes you want the CRA to make. Also, give the CRA your social insurance number, address, phone number, and the tax year(s) you want the CRA to adjust.

You can also submit your request by fax at 418-566-6335 or online by logging into your CRA account. For more details on how to submit documents online, go to Submit documents online.

You can also register a formal dispute within 90 days of the date of the notice of assessment or reassessment. For more information or to register a formal dispute, go to Objections, appeals, disputes, and relief measures.

Requesting a waiver or cancellation of your FHSA taxes

The Minister may use discretion to waive or cancel all or part of the taxes payable on excess FHSA amounts if:

- your excess FHSA amounts on which the tax is based arose due to a reasonable error

- you have taken steps or are taking immediate steps to remove the excess FHSA amount, including any income that is reasonably attributable to it, from your FHSAs

The Minister may also waive or cancel all or part of the taxes payable by you on the non-qualified or prohibited investments held in your FHSAs, as well as advantages, if it is determined that it is fair to do so after reviewing all factors, including:

- the tax arose because of a reasonable error

- the extent to which the transaction or series of transactions that gave rise to the tax also gave rise to another tax under the Income Tax Act

- the extent to which payments have been made from the FHSAs

To request a waiver or cancellation of the taxes payable on your excess FHSA amount only, you need to fill out Form RC729, Request for Waiver or Cancellation of Tax on your Excess FHSA Amount. Submit all relevant documents that support your request for the waiver or cancellation of tax such as copies of your FHSA transaction statements which show the dates when the excess FHSA amount occurred, as well as the dates when you removed your excess FHSA amount. Also include copies of any document that would support the explanation of the reasonable error that caused the excess FHSA amount.

To request a waiver or cancellation of the taxes payable on your non-qualified or prohibited investments, as well as advantages, you need to write a letter explaining why the tax liability arose, and why it would be fair to cancel or waive all or part of the tax.

The waiver for taxes payable on non-qualified or prohibited investments, as well as advantages is limited to tax paid under the anti-avoidance rules and not taxes paid under any other part of the Income Tax Act.

Send the completed form, signed letter, and any supporting documents to one of the following tax centres:

If your residential address is based in Ontario, Prince Edward Island, Newfoundland and Labrador, Yukon, Nunavut, Northwest Territories and the following Quebec cities: Montreal, Quebec City, Laval, Sherbrooke, Gatineau, and Longueuil, send your request to:

Canada Revenue Agency

Sudbury Tax Centre

FHSA Processing Unit

Post Office Box 20000, Station A

Sudbury ON P3A 5C1

If your residential address is based in Manitoba, Saskatchewan, Alberta, British Columbia, Nova Scotia, New Brunswick and the remaining areas of the province of Quebec not listed under the Sudbury Tax Centre, send the request to:

Canada Revenue Agency

Winnipeg Tax Centre

FHSA Processing Unit

Post Office Box 14000, Station Main

Winnipeg MB R3C 3M2

You can also send the completed form, signed letter, and any supporting documents to the FHSA Processing Unit by fax at 418-566-6335 or online by logging in to your CRA account. For more details on how to submit documents online, go to Submit documents online.

Cancel or waive penalties and interest

The CRA administers legislation, commonly called "taxpayer relief provisions," that gives the CRA discretion to cancel or waive penalties and interest when taxpayers cannot meet their tax obligations due to circumstances beyond their control.

The CRA's discretion is limited to any period that ends within 10 calendar years before the year the request is made.

Penalties

The CRA will consider your request only if it relates to a tax year or fiscal period ending in any of the 10 calendar years before the year you make your request. For example, your request made in 2025 must relate to a penalty for a tax year or fiscal period ending in 2015 or later.

Interest on a balance owing

The CRA will consider only the amounts that accrued during the 10 calendar years before the year you make your request. For example, your request made in 2025 must relate to interest that accrued in 2015 or later.

Taxpayer relief requests can be made online using the CRA's My Account, My Business Account, or Represent a Client digital services.

You can also fill out Form RC4288, Request for Taxpayer Relief – Cancel or Waive Penalties and Interest, and send it:

- online using My Account, My Business Account, or Represent a Client

- by mail or courier to the designated office, as shown on the last page of the form, based on your place of residence

For information about submitting documents online, go to Submit documents online.

For more information about cancelling or waiving penalties and interest, go to Cancel or waive penalties and interest at the CRA.