Annual Report 2020

ISSN: 1495-0561

Cat. no.: H78E-PDF

PDF version (2.3 MB)

Table of Contents

- Statistical Highlights 2020

- Letter to the Minister

- Chairperson's Message

- About the Patented Medicine Prices Review Board: Acting in the Interest of Canadians

- Regulating Prices of Patented Medicines: Informing on PMPRB Regulatory Activities

- Key Pharmaceutical Trends: More Expensive Medicines Continue to Influence Sales

- The National Prescription Drug Utilization Information System: Supporting Health Care Decision Making in Canada

- Analysis of Research and Development Expenditures: At a Historical Low

- Appendix 1: Glossary

- Appendix 2: Patented Medicines First Reported to the PMPRB in 2020

- Appendix 3: Pharmaceutical Trends - Sales

- Appendix 4: Research and Development

Statistical Highlights 2020

Regulatory Mandate

- 1,289 patented medicines for human use were reported to the PMPRB, including 79 new medicines.

- 4 Voluntary Compliance Undertakings were accepted as of December 31, 2020.

- $304 thousand in excess revenues were offset by way of payments to the Government of Canada, in addition to price reductions.

Reporting Mandate

Sales Trends:

- Sales of patented medicines in Canada reached $17.5 billion in 2020, a modest increase of 1.6% from the previous year.

- Patented medicines accounted for approximately 54.7% of the sales of all medicines in Canada in 2020.

Price Trends:

- The Consumer Price Index rose by 0.7%, while the national average transaction price for patented medicines increased by 1.6%.

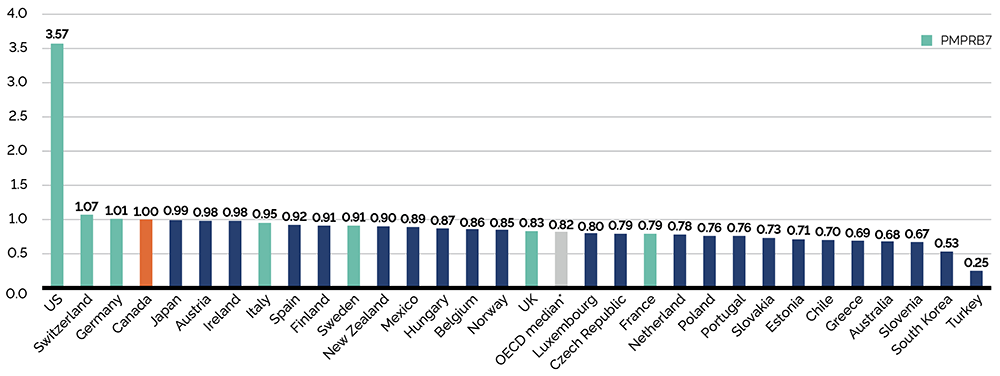

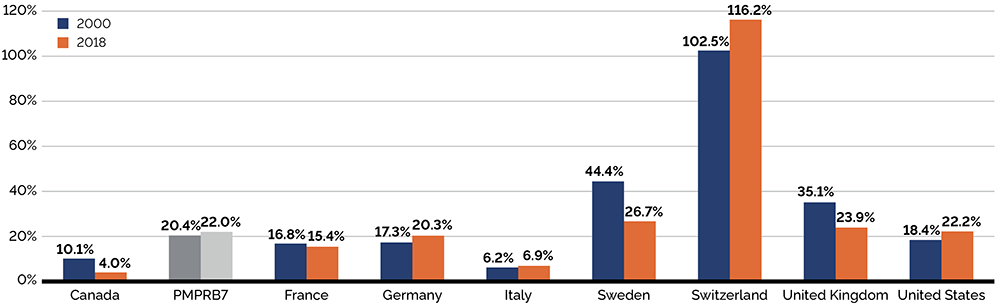

- Canadian list prices were fourth highest among the 31 Organisation for Economic Co-operation and Development (OECD) countries, lower than prices in Germany, Switzerland, and the US.

Research and Development

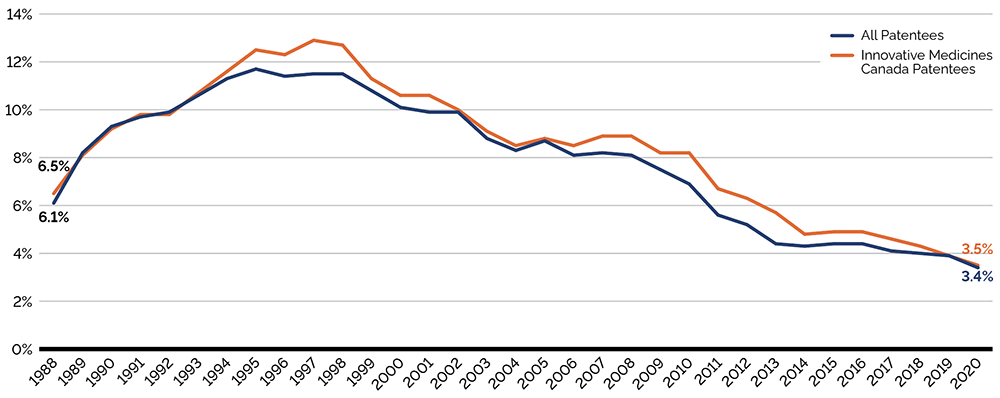

R&D-to-Sales Ratios Decreased in 2020:

- 3.4% for all patentees, a slight decrease from 3.9% in 2019.

- 3.5% for Innovative Medicines Canada members, a decrease from 3.9% in 2019.

R&D Expenditures:

- $822.9 million in total R&D expenditures were reported by patentees, a decrease of 7.9% over 2019.

- $662.8 million in R&D expenditures were reported by Innovative Medicines Canada members, an increase of 1.6% over 2019.

Letter to the Minister

November 5, 2021

The Honourable Jean-Yves Duclos

Minister of Health

House of Commons

Ottawa, Ontario

K1A 0A6

Dear Minister:

I have the pleasure to present to you, in accordance with sections 89 and 100 of the Patent Act, the Annual Report of the Patented Medicine Prices Review Board for the year ended December 31, 2020.

Yours very truly,

Dr. Mitchell Levine

Chairperson

Chairperson’s Message

The Patented Medicine Prices Review Board (PMPRB) is an independent quasi-judicial body established by Parliament in 1987 under the Patent Act (the Act). The PMPRB’s mandate is to protect and inform Canadians by ensuring that the prices of patented medicines sold in Canada are not excessive and by reporting on pharmaceutical trends.

For more than a year now, Canadians have had virtually every aspect of their daily lives disrupted by the ongoing COVID-19 pandemic. As the federal government mobilizes personnel and resources to mitigate the economic and social impact of the pandemic on Canadians, many pre-existing policy priorities have taken a backseat to this all consuming effort. While the PMPRB is eager to turn the page on the multiyear effort to modernize its regulatory framework, we recognize the legitimate desire of our stakeholders to minimize further disruption in the regulatory environment for pharmaceuticals in Canada at this tenous time. As we await the ultimate fate of the Health Canada's amendments to the Patented Medicines Regulations, the PMPRB continues to make the utmost of its existing regulatory tools to protect Canadians from excessively priced patented medicines in an era increasingly marked by extremely high cost drugs. In the eventuality that the regulatory amendments do come into force, the PMPRB is also developing a comprehensive Guideline Monitoring and Evaluation Plan (GMEP) to assess any changes in relevant trends following implementation of the reforms. In the coming year, we will continue to consult with stakeholders as we work to perfect the GMEP.

Further to our reporting mandate and under the broad umbrella of the National Prescription Drug Utilization Information System (NPDUIS) initiative, the PMPRB continues to provide analytical support and expertise to our health partners. Since the release of last year's Annual Report, the PMPRB has published 7 analytical reports, 3 chartbooks, and 2 presentation posters under the NPDUIS banner. These studies continue to highlight the pressures stemming from the increased use of higher-cost medicines in Canada. Over the last five years, sales of patented medicines have grown by an average of 3.0% per year to reach $17.5 billion in 2020. High-cost medicines now account for more than half of these sales. As noted in this year's Annual Report, in 2020, the 20 top selling patented medicines in Canada, which accounted for 36.5% of total patented medicine sales, had a weighted average annual treatment cost of $25,391. These trends lend further credence to longstanding concerns over the sustainability of Canada's pharmaceutical system.

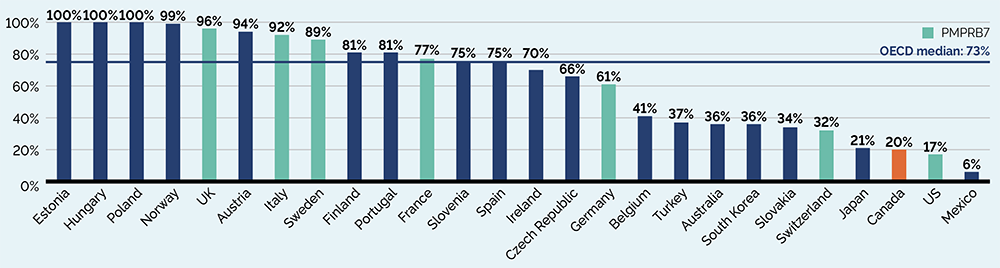

In 2020, Canadian list prices of patented medicines were the fourth highest in the Organisation for Economic Co-operation and Development (OECD), still well behind the US but just marginally lower than Switzerland and Germany. Conversely, the R&D – sales ratio of pharmaceutical patentees in Canada continues its decades-long decline and now stands at 3.4%, its lowest level since the PMPRB first began reporting on pharmaceutical trends in the 1980s.

November 2021 marks the end of my second and final term as a PMPRB Board member, and my tenure as its Chairperson. It has been an honour and a privilege to serve as a Board member and to lead the PMPRB through an important chapter in its more than three decade long history. I would like to thank the Minister for having afforded me this opportunity and to convey my respect and deep appreciation to my fellow Board members who accompanied me on this journey. I would also like to extend my thanks and admiration to the public servants at the PMPRB who I’ve had the pleasure of working alongside during my two terms on the Board. People may come and go but the commitment of staff at the PMPRB to the very highest ideals of public service is unwavering and I am confident it will endure long after my term as Chairperson comes to an end.

Dr. Mitchell Levine

Chairperson

About the Patented Medicine Prices Review Board: Acting in the Interest of Canadians

The Patented Medicine Prices Review Board (PMPRB) is an independent, quasi-judicial body established by Parliament in 1987 under the Patent Act (Act).

The PMPRB is a quasi-judicial administrative agency with a dual regulatory and reporting mandate. Through its regulatory mandate, it ensures that the prices of patented medicines sold in Canada are not excessive. The PMPRB also reports on trends in pharmaceutical sales and pricing for all medicines and on research and development (R&D) spending by patentees. In addition, at the request of the Minister of Health, pursuant to section 90 of the Act, the PMPRB conducts critical analyses of price, utilization, and cost trends for patented and non-patented prescription medicines under the National Drug Utilization Information System (NPDUIS) initiative. Its reporting mandate provides pharmaceutical payers and policy makers with information to make rational, evidence-based reimbursement and pricing decisions.

The PMPRB is part of the Health Portfolio, which includes Health Canada, the Public Health Agency of Canada, the Canadian Institutes of Health Research and the Canadian Food Inspection Agency. The Health Portfolio supports the Minister of Health in maintaining and improving the health of Canadians.

Our Mission

The PMPRB is a respected public agency that makes a unique and valued contribution to sustainable spending on pharmaceuticals in Canada by:

- Providing stakeholders with price, cost, and utilization information to help them make timely and knowledgeable pricing, purchasing, and reimbursement decisions; and

- Acting as an effective check on the prices of patented medicines through the responsible and efficient use of its consumer protection powers.

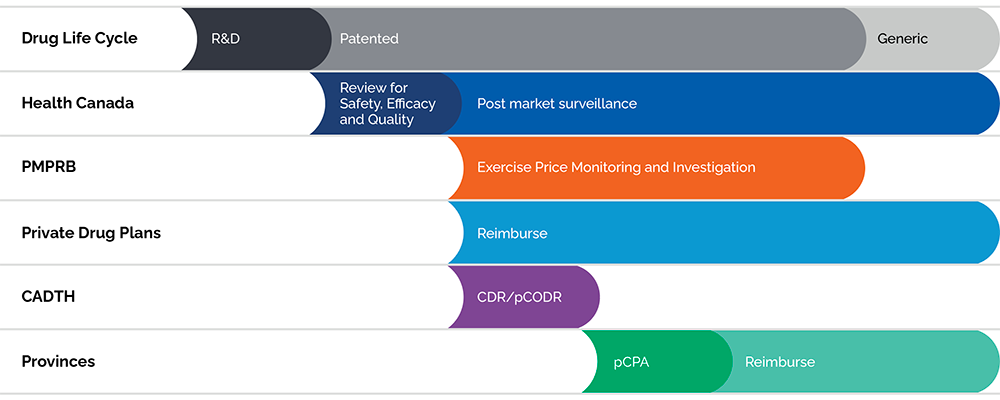

Protecting Consumers in a Complex Marketplace

Figure description

This flowchart illustrates the role of Canadian regulators during the life cycle of a medicine through research and development, the patent period, and post-patent generic period. Health Canada reviews medicines for safety, efficacy, and quality at the start of the patent period and provides subsequent post-market surveillance. The PMPRB exercises price monitoring and investigation during the patent period, after Health Canada’s review. Private drug plans reimburse during and after the patent period, following Health Canada’s review. CADTH conducts the Common Drug Review and pan-Canadian Oncology Drug Review processes after Health Canada’s review. For provinces and territories, the pan-Canadian Pharmaceutical Alliance negotiations begin after CADTH reviews, and reimbursement is after these negotiations.

(CADTH) Canadian Agency for Drugs and Technologies in Health; (CDR) Common Drug Review; (pCODR) pan-Canadian Oncology Drug Review; and (pCPA) pan-Canadian Pharmaceutical Alliance

Data source: PMPRB

Although part of the Health Portfolio, because of its quasi-judicial responsibilities, the PMPRB carries out its mandate at arm’s length from the Minister of Health, who is responsible for the sections of the Act pertaining to the PMPRB. The PMPRB also operates independently of other healthcare-related bodies, such as:

- Health Canada, which approves medicines for marketing in Canada based on their safety, efficacy, and quality;

- federal, provincial and territorial (F/P/T) public drug plans, working collectively as the pCPA, which approve the listing of medicines on their respective formularies for reimbursement purposes; and

- the Common Drug Review and pan-Canadian Oncology Drug Review, administered by the CADTH, which recommend which new medicines should qualify for reimbursement by the pCPA.

The PMPRB is composed of public servants (Staff) who are responsible for carrying out the organization’s day-to-day work, and Board Members, Governor-in-Council appointees who serve as hearing panel members in the event of a dispute between Staff and a patentee over the price of a patented medicine.

Jurisdiction

Regulatory

The PMPRB regulates the maximum ceiling price at which patentees (companies) may sell their products to wholesalers, hospitals, pharmacies and other large distributors. This price is sometimes also known as the “factory gate” (ex-factory) price. The PMPRB does not regulate the prices of non-patented medicines.

The PMPRB’s jurisdiction is not limited to medicines for which the patent is for the active ingredient or for the specific formulation(s) or uses the patentee sells the medicine for in Canada. Rather, its jurisdiction also covers medicines for which a patent “pertains”, including patents for manufacturing processes, delivery systems or dosage forms, indications/use, and any formulations.

Our Vision:

A sustainable pharmaceutical system where payers have the information they need to make smart reimbursement choices and Canadians can afford the patented medicines they need to live healthy and productive lives.

The Act requires patentees (which include any parties who benefit from patents regardless of whether they are owners or licensees under those patents and regardless of whether they operate in the “brand” or “generic” sector of the market) to inform the PMPRB of their intention to sell a new patented medicine. Upon the sale of a new patented medicine, patentees are required to file price and sales information at introduction and, thereafter, until all patents pertaining have expired. Patentees are not required to obtain approval of the price to be able to market their medicines. However, the Act requires the PMPRB to ensure that the prices of patented medicines sold in Canada are not excessive.

Staff review the prices that patentees charge for each individual strength and form of a patented medicine. If the price of a patented medicine appears to be potentially excessive, the patentee may volunteer to lower its price and/or refund its potential excess revenues through a Voluntary Compliance Undertaking (VCU). If this fails, the Chairperson may consider whether a hearing on the matter is in the public interest. At the hearing, a panel composed of Board members acts as a neutral arbiter between Staff and the patentee. If a Hearing Panel concludes, after hearing all of the evidence in light of the factors set out in section 85 of the Act, that the price of a patented medicine is/was excessive in any market, it can order the price be reduced to a non-excessive level. It can also order a patentee to make a monetary payment to the Government of Canada to offset the excess revenues earned and, in cases where the panel determines there has been a policy of excessive pricing, it can double the amount of the monetary payment.

Reporting

As required by the Act, the PMPRB reports annually to Parliament through the Minister of Health on its price review activities, the prices of patented medicines and price trends of all prescription medicines, and on the R&D expenditures reported by pharmaceutical patentees.

In addition, as a result of an agreement by the F/P/T Ministers of Health in 2001, and at the request of the Minister of Health, pursuant to section 90 of the Act, the PMPRB conducts critical analyses of price, utilization, and cost trends for patented and non-patented prescription medicines under the National Prescription Drug Utilization Information System (NPDUIS). The PMPRB publishes the results of NPDUIS analyses in the form of reports, posters, presentations, briefs, and chartbooks. This program provides F/P/T governments and other interested stakeholders with a centralized, objective, and credible source of information on pharmaceutical trends.

Among other initiatives under its reporting mandate, the PMPRB also hosts various forums, such as webinars, research forums, and information sessions, with academics and policy experts to discuss and disseminate research on emerging areas for study on pharmaceutical trends in Canada and internationally.

1,289 Patented medicines were reported to the PMPRB in 2020.

Communications and Outreach

The PMPRB takes a proactive and plain-language approach to its external communication activities. This includes targeted social media campaigns and more conventional (e.g., email and telephone) engagement with domestic, international, and specialized news media. The PMPRB is actively pursuing additional opportunities to leverage new and emerging media to communicate with its stakeholders and the Canadian public.

The PMPRB recognizes the importance of openness and transparency as we continue to work on modernizing the way we carry out our mandate. We communicate regularly, through various channels, about our progress, including projected timelines, and key milestones. Engagement with stakeholders will remain a central part of our multi-faceted communications approach. Reporting on our progress helps ensure we remain focused on delivering results.

Governance

The Board consists of not more than five members who serve on a part-time basis. Board members, including a Chairperson and a Vice-Chairperson, are appointed by the Governor-in-Council. The Chairperson, designated under the Act as the Chief Executive Officer of the PMPRB, has the authority and responsibility to supervise and direct its work. By law, the Vice-Chairperson exercises all the powers and functions of the Chairperson when the Chairperson is absent or incapacitated, or when the office of the Chairperson is vacant.

The members of the Board, including the Chairperson, are collectively responsible for implementing the applicable provisions of the Act. Together, they establish the guidelines, rules, by-laws, and other policies of the PMPRB provided for by the Act (section 96) and consult, as necessary, with stakeholders including provincial and territorial Ministers of Health, representatives of consumer groups, the pharmaceutical industry, and others.

Members of the Board

Chairperson

Mitchell Levine,

BSc, MSc, MD, FRCPC, FISPE, FACP

Dr. Mitchell Levine was appointed Chairperson of the Board on February 13, 2018. He has served as a Member and Vice-Chairperson of the Board since 2011.

Dr. Levine is a professor at McMaster University in Hamilton in the Department of Health Research Methods, Evidence and Impact and in the Department of Medicine, Division of Clinical Pharmacology & Toxicology. He is also an Assistant Dean in the Faculty of Health Sciences and a faculty member of the Centre for Health Economics and Policy Analysis at McMaster.

Dr. Levine received his medical degree from the University of Calgary, which was followed by postgraduate training in Internal Medicine (FRCPC) and in Clinical Pharmacology at the University of Toronto. He received an MSc degree in Clinical Epidemiology from McMaster University.

Dr. Levine is a consultant physician in the fields of internal medicine and clinical pharmacology in Hamilton. On an ad hoc basis, he acts as a clinical pharmacology consultant to the Ontario Ministry of Health and Ministry of Long-Term Care. Prior to his appointment to the Board, Dr. Levine was a member of the PMPRB’s Human Drug Advisory Panel.

This is Dr. Levine’s second term as a Board member. His term ends November 2021.

Vice-Chairperson

Mélanie Bourassa Forcier

LLB., LL.L, MSc, LL.M., DCL

Mélanie Bourassa Forcier was appointed Vice-Chairperson of the Board on June 19, 2019.

Professor Bourassa Forcier is a lawyer and a Full Professor in the Faculty of Law at the Université de Sherbrooke. She directs the Law and Health Policy, and Law and Life Sciences programs. She has expertise in Health governance and Ethics in Health Policy, Intellectual Property, Regulation of Digital Technologies, Technology Transfers and in Pharmaceutical Law and Policies. Over the years she has particularly concentrated her research on policies promoting the development, integration and access to innovation in the health care sector.

Professor Bourassa Forcier has published numerous books and articles on the subject of pharmaceutical regulation and health law. She holds a Ph.D. in Pharmaceutical Patent Law from McGill University, an MSc in International Health Policy from the London School of Economics and Political Science (concentration in Health Economics), a LL.M. in Law and Biotechnologies from the University of Montreal and an LL.L. from the University of Ottawa (summa cum laude).

Members

Carolyn Kobernick,

B.C.L., LL.B.

Carolyn Kobernick was appointed Member of the Board on June 13, 2014.

Ms. Kobernick is a lawyer and former public servant. Prior to her retirement in 2013, Ms. Kobernick had been Assistant Deputy Minister of Public Law for the Department of Justice since 2006. As principal counsel to the Minister of Justice and Attorney General of Canada, Ms. Kobernick was instrumental in the development and delivery of policy for the Department of Justice. In addition to identifying key strategic, legal, and operational matters, she tackled cross-cutting national issues as the liaison between the Department of Justice and other government organizations.

Ms. Kobernick holds a B.C.L. and LL.B. from McGill University and is a member of the bar of Ontario. In 2012 she obtained a Certificate in Adjudication for Administrative Agencies, Boards and Tribunals from the Osgoode Hall Law School and the Society of Ontario Adjudicators and Regulators.

Dr. Ingrid Sketris,

BSc (Pharm), PharmD, MPA(HSA), Clinical Toxicology Residency

Dr. Ingrid Sketris was appointed Member of the Board on June 29, 2018.

Dr. Sketris is a licensed pharmacist and a professor at the College of Pharmacy, Dalhousie University, with cross appointments to Medicine and Health Administration.

Dr. Sketris received her Doctor of Pharmacy in 1979 from the University of Minnesota, followed by her residency in Clinical Toxicology at the University of Tennessee Centre for the Health Sciences. She also received a Master of Public Administration/Health Services Administration from Dalhousie University.

She is a leader in pharmacy, and has served as President of the Association of Faculties of Pharmacy of Canada and as a board member of the Canadian Council for Accreditation of Pharmacy Programs.

Dr. Sketris is a Fellow of the Canadian Society of Hospital Pharmacists, the American College of Clinical Pharmacy and the Canadian Academy of Health Sciences. She was previously elected to the US National Academies of Practice.

Matthew Herder,

B.Sc. (hons), LL.B., LL.M., J.S.M.

Matthew Herder was appointed Member of the Board on June 29, 2018.

Mr. Herder is the Director of the Health Law Institute at Dalhousie University, as well as an Associate Professor in the Department of Pharmacology in the Faculty of Medicine, with a cross-appointment to the Schulich School of Law.

Mr. Herder’s research focuses on biomedical innovation policy, with a particular emphasis on intellectual property rights and the regulation of biopharmaceutical interventions. His work is often interdisciplinary and policy-oriented, and he has received grants from the Canadian Institutes of Health Research and the Royal Society of Canada, in addition to appearing as an expert witness before several Parliamentary committees on pharmaceutical regulation and policy.

Prior to arriving at Dalhousie, Mr. Herder was the Ewing Marion Kauffman Foundation Legal Research Fellow at New York University’s School of Law. He was a Law Clerk at the Federal Court of Canada and was admitted to the Law Society of Upper Canada. Mr. Herder holds a Master of the Science of Law degree from Stanford Law School as well as two law degrees from Dalhousie University.

Organizational Structure and Staff

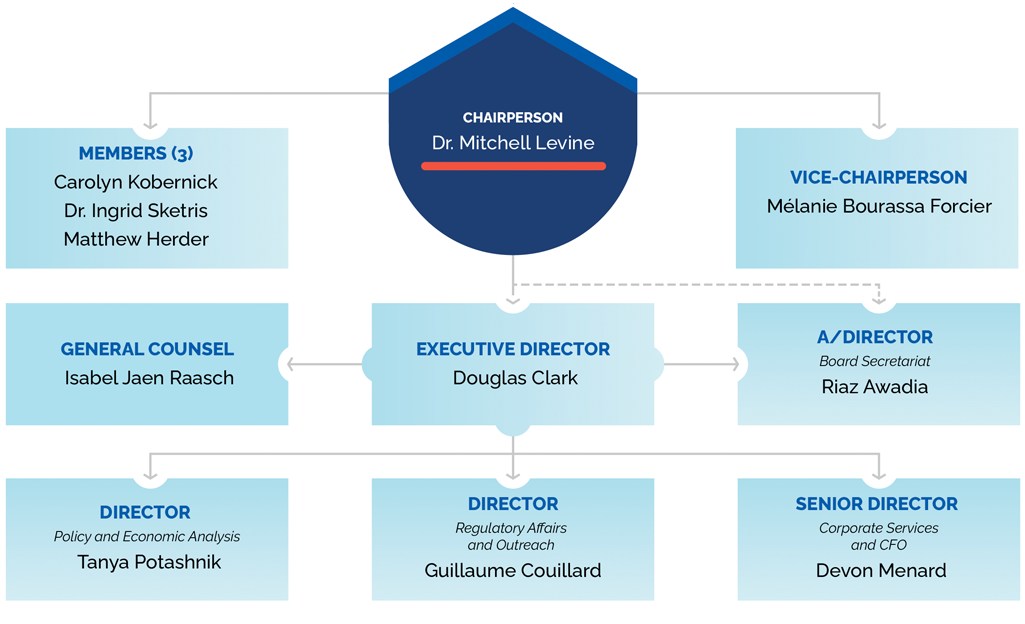

PMPRB Organizational Chart

Figure description

This organizational chart illustrates the high-level reporting structure within the PMPRB and lists the current Board and Senior Staff members. Board: Chairperson— Dr. Mitchell Levine; Vice-Chairperson— Mélanie Bourassa Forcier; Members— Carolyn Kobernick, Dr. Ingrid Sketris, Matthew Herder. Senior Staff: Executive Director— Douglas Clark; General Counsel— Isabel Jaen Raasch; A/Director Board Secretariat— Riaz Awadia; Director Policy and Economic Analysis— Tanya Potashnik; Director Regulatory Affairs and Outreach— Guillaume Couillard; Senior Director Corporate Services and CFO— Devon Menard.

Executive Director

The Executive Director is responsible for advising the Board and for the leadership and management of Staff.

Regulatory Affairs and Outreach

The Regulatory Affairs and Outreach Branch reviews the prices of patented medicines sold in Canada to ensure they are not excessive; ensures that patentees are fulfilling their filing obligations; encourages patentees to comply voluntarily with the PMPRB’s Guidelines; implements related compliance policies; and investigates complaints into the prices of patented medicines.

Policy and Economic Analysis

The Policy and Economic Analysis Branch develops policy and strategic advice; leads stakeholder consultations and makes recommendations on possible amendments to the PMPRB’s Guidelines; conducts research and analysis on the prices of medicines, pharmaceutical market developments, and R&D trends; and publishes studies aimed at providing F/P/T governments and other interested stakeholders with centralized, objective, and credible information in support of evidence-based policy.

Corporate Services

The Corporate Services Branch provides advice and services in relation to human resources management; facilities; procurement; health, safety and security; information technology; and information management. It coordinates activities pursuant to the Access to Information Act and the Privacy Act, and is responsible for strategic planning and reporting. It is also responsible for financial planning and reporting, accounting operations, audit and evaluation, and liaising with federal central agencies on these topics.

Board Secretariat

The Board Secretariat manages the Board’s meeting and hearing processes, including the official record of proceedings.

General Counsel

The General Counsel advises the PMPRB on legal matters and leads the legal team representing Staff in proceedings before the Board.

Budget

In 2020–21, the PMPRB had a budget of $17.8 million and an approved staff level of 87 full-time equivalent employees.

Table 1. Budget and Staffing

| 2019-20 | 2020-21 | 2021-22 | |

|---|---|---|---|

| Budget* | $16,612,511 |

$17,804,400 |

$18,892,322 |

| Salaries and employee benefits | $9,636,550 |

$10,054,721 |

$10,175,540 |

| Operating | $2,699,395 |

$2,491,893 |

$2,510,296 |

| Special Purpose Allotment** | $4,276,566 |

$5,257,786 |

$6,206,486 |

| Full Time Employees (FTEs) | 82 |

87 |

85 |

* Budget amounts are based on the Main Estimates

** The Special Purpose Allotment is reserved strictly for external costs of public hearings (legal counsel, expert witnesses, etc.). Unspent funds are returned to the Consolidated Revenue Fund.

Regulating Prices of Patented Medicines: Informing on PMPRB Regulatory Activities

Medical advancements have introduced many innovative new medicines to the Canadian marketplace to improve existing treatments and to treat conditions that previously had no pharmaceutical therapy. However, many of these new medicines come at a very high cost. Since 1987, pharmaceutical costs in Canada have grown at an average annual rate of 7.2%,Footnote 1 outpacing all other health care costs and growing at well over three times the pace of inflation. At 15.7% of total health care spending, pharmaceuticals now rank ahead of spending on physicians.Footnote 2 About 1 in 5 Canadians reports having no prescription medicine coverage and many more are under-insured or face high deductibles or co-pays. Almost 1 in 10 Canadians have had to forego filling a prescription medicine in the past year for reasons related to cost.Footnote 3

The PMPRB protects the interests of Canadian consumers by ensuring that the prices of patented medicines sold in Canada are not excessive. It does this by reviewing the prices that patentees charge for each individual patented medicine and by ensuring that patentees reduce their prices and pay back excess revenues, where appropriate.

Reporting Requirements

By law, patentees must file information about the sale of their medicines in Canada. The Act and the Patented Medicines Regulations (Regulations) set out the information required and Staff reviews pricing information on an ongoing basis until all relevant patents have expired.

The Compendium of Policies, Guidelines and Procedures (Guidelines) details price tests and triage mechanisms used by Staff when it reviews and investigates the prices of patented medicines. The Guidelines are not binding and were developed in consultation with stakeholders, including the provincial and territorial Ministers of Health, consumer groups, and the pharmaceutical industry. When an investigation suggests that the price of a patented medicine is excessive, the patentee may volunteer to lower its price and/or refund its potential excess revenues through a Voluntary Compliance Undertaking (VCU). If the patentee chooses not to submit a VCU, the Chairperson may consider whether a hearing on the matter is in the public interest. If such a hearing is held before a panel composed of Board members (“Hearing Panel”) and that Hearing Panel concludes, after hearing all of the evidence in light of the factors set out in section 85 of the Act, that the patented medicine was priced excessively in any market, an order may be issued to the patentee requiring that (1) the price be reduced; and/or (2) that measures be taken to offset any excess revenues that may have been earned through sales of the patented medicine at an excessive price. Copies of the Act, the Regulations, and the Guidelines are available on the PMPRB’s website.

Failure to Report

Access to timely and accurate information regarding the sale of patented medicines is necessary for the PMPRB to fulfil its regulatory mandate. Therefore, patentees and former patentees are required to submit this information to the PMPRB. The information that must be submitted is set out in section 82 of the Act and in the Regulations. In 2020, 4 medicines were reported to the PMPRB for the first time despite being patented and sold prior to 2020 (see Table 2, Failure to Report the Sale of Patented Medicines).

Failure to File Price and Sales Data (Form 2)

Failure to file refers to the complete or partial failure of a patentee to file the information required by the Act and the Regulations to the PMPRB. There were no Board Orders issued for failure to file in 2020.

Table 2. Failure to Report the Sale of Patented Medicines

| Patentee | Brand name | Medicinal ingredient | Year medicine reported to the PMPRB as under PMPRB’s jurisdiction | Year medicine reported to the PMPRB with subsequent patent |

|---|---|---|---|---|

Takeda Canada Inc. |

Adynovate |

Antihemophilic factor (recombinant), PEGylated |

2018 |

- |

Swedish Orphan Biovitrum, SOBI |

Orfadin |

Nitisinone |

2019 |

- |

Recordati Rare Diseases |

Ledaga |

Chlormethine hydrochloride |

2019 |

- |

Takeda Canada Inc. |

Ondissolve |

Ondansetron |

2015 |

- |

* Drug Identification Number(s) (DIN) (DINs)

Correction: Xultophy (insulin degludec/liraglutide) should not have been included in Table 2, Failure to Report the Sale of Patented Medicines in 2019.

Data source: PMPRB

Our Motto

Protect, Empower, Adapt.

Scientific Review

Human Drug Advisory Panel

A scientific evaluation is done on all new patented medicines as part of the price review process. The PMPRB established the Human Drug Advisory Panel (HDAP) to provide advice to Staff. The HDAP conducts an evaluation to provide clinical context pertaining to the scientific information that is being considered by Staff. The HDAP members review and evaluate the appropriate scientific information available, including any submission by a patentee about the proposed level of therapeutic improvement, the selection of comparator medicines, and comparable dosage regimens.

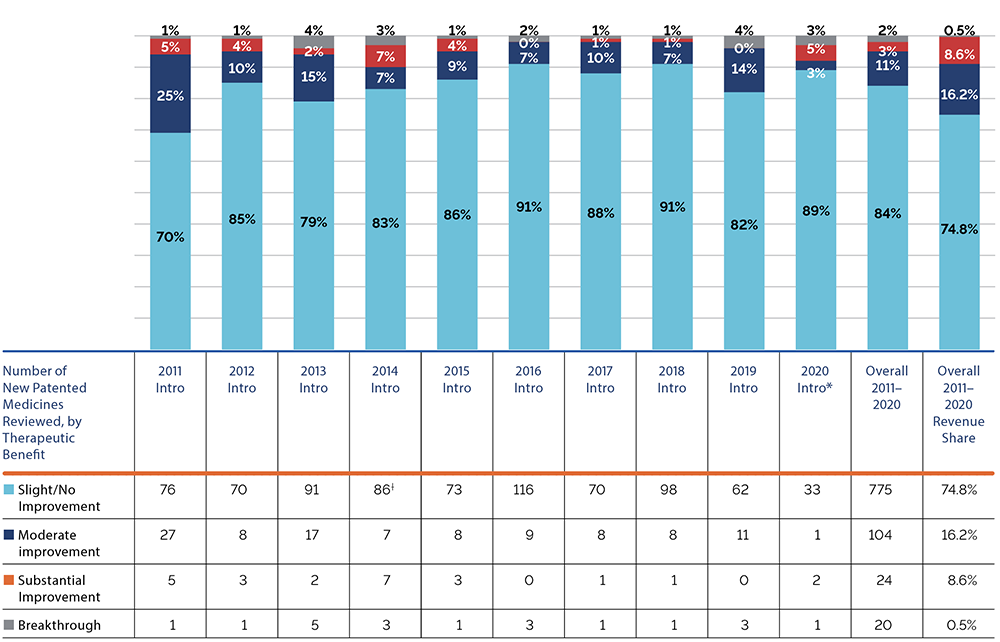

The HDAP evaluates the therapeutic benefit of new patented medicines according to the following definitions:

- Breakthrough: A medicine that is the first one sold in Canada to effectively treat a particular illness or effectively address a particular indication.

- Substantial Improvement: A medicine that, relative to other medicines sold in Canada, provides substantial improvement in therapeutic effects.

- Moderate Improvement: A medicine that, relative to other medicines sold in Canada, provides moderate improvement in therapeutic effects.

- Slight or No Improvement: A medicine that, relative to other medicines sold in Canada, provides slight or no improvement in therapeutic effects.

* Assessment as of March 31, 2021

† This number was revised to remove a medicine that was a failure to report.

Data source: PMPRB

Figure description

This bar graph depicts the breakdown in percentages of new patented medicines by therapeutic benefit over existing medicines in the year of introduction for the period 2011 to 2020. An overall revenue share for the period depicts the percentage of sales related to each level of therapeutic benefit.

|

Slight/No improvement |

Moderate improvement |

Substantial improvement |

Breakthrough |

Intro 2011 |

70% |

25% |

5% |

1% |

Intro 2012 |

85% |

10% |

4% |

1% |

Intro 2013 |

79% |

15% |

2% |

4% |

Intro 2014 |

84% |

7% |

7% |

3% |

Intro 2015 |

86% |

9% |

4% |

1% |

Intro 2016 |

91% |

7% |

0% |

2% |

Intro 2017 |

88% |

10% |

1% |

1% |

Intro 2018 |

91% |

7% |

1% |

1% |

Intro 2019 |

82% |

14% |

0% |

4% |

Intro 2020 |

89% |

3% |

5% |

3% |

Overall 2011-2020 |

84% |

12% |

3% |

2% |

Overall 2011-2020 |

74.8% |

16.2% |

8.6% |

0.5% |

A table below the graph gives the number of new patented medicines reviewed in each level of therapeutic improvement.

|

Slight/No improvement |

Moderate improvement |

Substantial improvement |

Breakthrough |

Intro 2011 |

76 |

27 |

5 |

1 |

Intro 2012 |

70 |

8 |

3 |

1 |

Intro 2013 |

91 |

17 |

2 |

5 |

Intro 2014 |

86 |

7 |

7 |

3 |

Intro 2015 |

73 |

8 |

3 |

1 |

Intro 2016 |

116 |

9 |

0 |

3 |

Intro 2017 |

70 |

8 |

1 |

1 |

Intro 2018 |

98 |

8 |

1 |

1 |

Intro 2019 |

62 |

11 |

0 |

3 |

Intro 2020* |

33 |

1 |

2 |

1 |

Overall 2011-2020 |

775 |

104 |

24 |

20 |

Overall 2011-2020 |

74.8% |

16.2% |

8.6% |

0.5% |

Figure 1 illustrates the percentage breakdown of new patented medicines in the year of introduction by therapeutic benefit for 2011 to 2020. The largest percentage of patented medicines (84%) introduced since 2011 were categorized as “Slight or No Improvement” in therapeutic benefit over existing therapies.Footnote 4

The “Overall 2011–2020” bar represents the therapeutic benefit breakdown for all new patented medicines introduced from 2011 to 2020. The “Overall 2011–2020 Revenue Share” bar illustrates the revenue share by therapeutic benefit for all new patented medicines introduced from 2011 to 2020.

Price Review

The PMPRB reviews the average price of each strength of each individual dosage form of each patented medicine. In most cases, this unit is consistent with the Drug Identification Number(s) (DIN), (DINs) assigned by Health Canada at the time the medicine is approved for sale in Canada.

New Patented Medicines Reported to the PMPRB in 2020

For the purpose of this report, a new patented medicine in 2020 is defined as any patented medicine or new dosage form or strength of a patented medicine first sold in Canada, or previously sold but first patented, between December 1, 2019, and December 1, 2020.

There were 79 new patented medicines for human use reported as sold in 2020. Some are one or more strengths of a new active substance and others are new presentations of existing medicines. Of these 79 new patented medicines, 2 (2.5%) were being sold in Canada prior to the issuance of the Canadian patent that brought them under the PMPRB’s jurisdiction. Table 3 shows the year of first sale for these medicines.

Table 3. Number of New Patented Medicines for Human Use in 2020 by Year First Sold

| Year First Sold | Number of Medicines |

|---|---|

| 2019 | 2 |

| 2020 | 77 |

| Total | 79 |

Data source: PMPRB

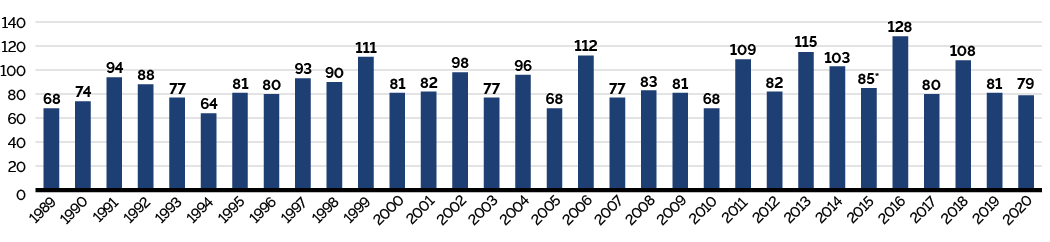

The list of New Patented Medicines Reported to PMPRB is available on the PMPRB’s website under “Regulating Prices”. This list is updated yearly upon the release of the Annual Report and includes information on the status of the review (i.e., whether the medicine is under review, within the Guidelines, under investigation, or subject to a VCU or Notice of Hearing). Figure 2 illustrates the number of new patented medicines for human use reported to the PMPRB from 1989 to 2020.

Data source: PMPRB

Figure description

This bar graph depicts the number of new patented medicines for human use reported to the Patented Medicine Prices Review Board by year. In 1989, 68 patented medicines for human use were reported to the PMPRB.

In 1990: 74; 1991: 94; 1992: 88; 1993: 77; 1994: 64; 1995: 81; 1996: 80; 1997: 93; 1998: 90; 1999: 111; 2000: 81; 2001: 82; 2002: 98; 2003: 77; 2004: 96; 2005: 68; 2006: 112; 2007: 77; 2008: 83; 2009: 81; 2010: 68; 2011: 109; 2012: 82; 2013: 115; 2014: 103; 2015: 86; 2016: 128; 2017: 80; 2018: 108; 2019: 81; 2020: 79.

Of the 79 new patented medicines, the prices of 37 had been reviewed as of March 31, 2021:

- 27 were found to be within the thresholds set out in the Guidelines and, as such, did not trigger the investigation criteria;Footnote 5

- 4 were at a level that appeared to exceed the thresholds set out in the Guidelines by an amount that did not trigger the investigation criteria; and

- 6 were at levels that appeared to exceed the thresholds set out in the Guidelines and resulted in investigations being commenced.

For a complete list of the 79 new patented medicines and their status, see Appendix 2.

Price Review of Existing Patented Medicines for Human Use in 2020

For the purpose of this report, existing patented medicines include all patented medicines first sold and reported to the PMPRB prior to December 1, 2019.

At the time of this report, there were 1,210 existing patented medicines:

- 865 were priced within the thresholds set out in the Guidelines and, as such, did not trigger the investigation criteria;

- 165 had prices that appeared to exceed the thresholds set out in the Guidelines by an amount that did not trigger the investigation criteria;

- 160 were the subject of investigations;

- 12 were under review;

- 5 were the subject of a Voluntary Compliance Undertaking;

- 2 were the subject of a hearing; and

- 1 was subject to a Stay Order.

Table 4 provides a summary of the status of the price review of the new and existing patented medicines for human use in 2020.

Table 4. Patented Medicines for Human Use Sold in 2020—Status of Price Review as of March 31, 2021

| New medicines introduced in 2020 | Existing medicines | Total | |

|---|---|---|---|

| Total | 79 | 1,210 | 1,289 |

| Within Guidelines Thresholds | 27 | 865 | 892 |

| Under Review | 42 | 12 | 54 |

| Does Not Trigger Investigation | 4 | 165 | 169 |

| Under Investigation | 6 | 160 | 166 |

| Subject to Voluntary Compliance Undertaking | – | 5 | 5* |

| Price Hearing | – | 2 | 2 |

| Subject to Price Reduction Order (Stayed) | – | 1 | 1 |

*The terms and conditions of previous years VCUs that have carried over into 2020 are not captured in this count.

Data source: PMPRB

Update From the 2019 Annual Report

- There are 6 reviews of patented medicines for human use that were reported as Under Review in the 2019 Annual Report that remain Under Review.

- 41 of the 128 investigations reported in the 2019 Annual Report resulted in one of the following:

- the closure of the investigation where it was concluded the price was within the thresholds set out in the Guidelines;

- a VCU by the patentee to reduce the price and offset excess revenues through a payment and/or a reduction in the price of another patented medicine (“Voluntary Compliance Undertakings”); or

- a public hearing to determine whether the price was excessive, including any remedial Order determined by the Board (“Hearings”).

Patented Over-the-Counter Medicines, Patented Generic Medicines and Patented Medicines For Veterinary Use

Staff only reviews the prices of patented over-the-counter medicines, patented generic medicines, and patented veterinary medicines when a complaint of excessive pricing has been received. No such complaints were received in 2020.

Voluntary Compliance Undertakings and Hearings

Voluntary Compliance Undertakings

A VCU is a promise by a patentee to reduce its price(s) and/or offset any potential excess revenues from the sale of a patented medicine that is subject to an investigation. The Guidelines set out procedures for patentees to submit a VCU. The consideration of a VCU is an administrative procedure and does not constitute an admission or determination by the PMPRB that the price submitted by the patentee, or used to calculate a revenue offset, is not excessive. However, the acceptance of a VCU by the Chairperson will result in the closure of an investigation.

In 2020, the Chairperson approved the closure of investigations based on the receipt of four VCUs. In addition to price reductions for certain medicines, potential excess revenues totaling $304,354.70Footnote 6 were offset by way of payments to the Government of Canada.

As of May 31, 2021, the Chairperson approved the closure of an investigation after the receipt of an additional VCU, which resulted in a price reduction.

Table 5. Voluntary Compliance Undertakings in 2020 up to May 31, 2021

| Patented medicine brand name | Therapeutic use | Patentee | Date of approval | Offset of excessive revenues | |

|---|---|---|---|---|---|

| Price reduction | Payment to the government | ||||

VCUs in 2020 |

|||||

Ixekizumab (sold under trade name Taltz) |

For the treatment of adult patients with moderate-to-severe plaque psoriasis who are candidates for systemic therapy or phototherapy, and for the treatment of adult patients with active psoriasis who have responded inadequately to, or are intolerant to one or more disease-modifying antirheumatic drugs. |

Eli Lilly Canada Inc. |

January |

|

$75,844.49 |

Patisiran (sold under trade name Onpattro) |

For the treatment of polyneuropathy in adult patients with hereditary transthyretin-mediated amyloidosis (hATTR amyloidosis). |

Alnylam Pharmaceuticals Inc. |

August |

✓ |

|

Inotersen (sold under trade name Tegsedi) |

For the treatment of stage 1 or stage 2 polyneuropathy in adult patients with hereditary transthyretin amyloidosis (hATTR). |

Akcea Therapeutics Canada |

August |

✓ |

|

Erenumab (sold under trade name Aimovig) |

For the prevention of migraine in adults who have at least four migraine days per month. |

Novartis Pharmaceuticals Canada Inc. |

October |

✓ |

|

Total as of December 31, 2020 |

$75,844.49 |

||||

VCUs in 2021 as of May 31, 2021 |

|||||

Neratinib (sold under trade name Nerlynx) |

An oral protein kinase inhibitor approved for the extended adjuvant treatment of women with early-stage hormone receptor positive, HER2 overexpressed/amplified breast cancer within one year after completion of trastuzumab-based adjuvant therapy |

Knight Therapeutics Inc. |

March |

✓ |

|

Total as of May 31, 2021 |

$75,844.49 |

||||

Hearings

The PMPRB holds hearings into two types of matters:

- excessive pricing; and

- failure to file–jurisdiction.

Excessive Pricing

When an investigation into the price of a patented medicine is completed, and the matter is not resolved, the Executive Director may submit a report to the Chairperson. The Chairperson may decide to issue a Notice of Hearing if he or she is of the opinion that it is in the public interest. During a hearing, submissions and evidence from the parties are heard by a Hearing Panel consisting of at least two Board members. The Hearing Panel determines whether a patented medicine is being, or has been, sold at an excessive price in any market in Canada by taking into consideration the available information relating to the factors set out in section 85 of the Act. If the Hearing Panel finds the price is excessive, it can issue an order to reduce the price of the patented medicine in question (or of another patented medicine of the patentee) and/or to offset revenues received as a result of the excessive price. Judicial review of Board decisions can be sought in the Federal Court of Canada.

In January 2019, the PMPRB announced it would hold a public hearing in the matter of the price of the patented medicine cysteamine bitartrate sold under the trade name Procysbi by Horizon Therapeutics Canada. The purpose of this hearing was to determine whether the medicine has been, or is being, sold in any market in Canada at a price that, in the Board’s opinion, is or was excessive: and, if so, what order, if any, should be made to remedy the excessive pricing. The hearing was held over several weeks in late 2020-early 2021 and a decision on the matter is pending.

Failure to File–Jurisdiction

When it is the opinion of Staff that a patentee has failed or refused to provide the PMPRB with the pricing, sales, or revenues and like information required by law, the Executive Director may submit a report to the Chairperson. The Chairperson may decide to issue a Notice of Hearing if he or she is of the opinion that it is in the public interest to hold a hearing to determine whether the patentee has, in fact, breached the reporting requirements of the Act and Regulations. If the Hearing Panel finds, as the result of a public hearing, that the patentee has failed to report the required information, the Hearing Panel can order the patentee to file the required pricing and sales information.

There were no new failure to file hearings as of March 31, 2021.

On May 7, 2020, the Board issued its decision on re-determination on its decision dated December 19, 2016, whereby the Board originally found that Canadian Patent No. 2,478,237 pertains to the patented medicine adapalene sold under the trade name Differin and ordered Galderma to file the required information for the period between January 1, 2010, and March 14, 2016. The Board’s decision on redetermination again ordered Galderma to file the required information for the period between January 1, 2010, and March 14, 2016. On August 11, 2020, Galderma Canada Inc. filed an application for judicial review of the Board’s May 7, 2020 decision on redetermination (T-906-20).

Summary

Excess revenues totaling $75,844.49, were offset by payments to the Government of Canada through VCUs and Board Orders in 2020 and up to May 31, 2021. As a result of a condition in the terms of a VCU accepted in 2019 to make a further payment to the Government of Canada for any remaining cumulative excess revenues as of December 31, 2019, the PMPRB received a payment in the amount of $228,510.21Footnote 7 making the total funds received up to May 31, 2021, $304,354.70.

Since 1993, 158 VCUs have been accepted. In addition, 7 public hearings related to allegations of failure to file and 10 public hearings related to allegations of excessive pricing have been held. These measures resulted in price reductions and the offset of excess revenues by additional price reductions and/or payments to the Government of Canada. Over $210 million has been collected through VCUs, settlements, and Board Orders through payments to the Government of Canada.

Matters Before the Federal Court, Federal Court of Appeal, and Supreme Court of Canada or Other Courts

A-237-19: on October 20, 2017, Alexion Pharmaceuticals Inc. filed an application for judicial review of the Board’s decision dated September 20, 2017 in respect of its finding that the patented medicine eculizumab sold under the trade name Soliris was being sold at an excessive price in Canada and ordering Alexion to lower its price (currently stayed) and make an excess revenue payment of $4,245,329.60. The Board’s decision was found to be reasonable by the Federal Court via a decision dated May 23, 2019. Alexion has appealed the Federal Court’s decision in the Federal Court of Appeal. The Federal Court of Appeal heard the appeal of the Board Panel’s decision in October 2020. The Federal Court of Appeal granted Alexion's appeal on July 29, 2021 and remitted the matter to the Board for redetermination.

T-906-20: on January 18, 2017, Galderma Canada Inc. filed an application for judicial review of the Board’s decision dated December 19, 2016. In that decision the Board found that Canadian Patent No. 2,478,237 pertains to the patented medicine adapalene sold under the trade name Differin and ordered Galderma to file the required information for the period between January 1, 2010, and March 14, 2016. The Federal Court granted Galderma’s judicial review application on November 9, 2017 and quashed the Board’s decision. On November 21, 2017, the Attorney General appealed the Federal Court’s grant of the judicial review application. On June 28, 2019, the Federal Court of Appeal granted the appeal and issued its decision sending the matter back to the Board for redetermination. The Board’s decision on redetermination, issued on May 7, 2020, again ordered Galderma to file the required information for the period between January 1, 2010 and March 14, 2016. On August 11, 2020, Galderma Canada Inc. filed an application for judicial review of the Board’s May 7, 2020 decision on redetermination (T-906-20). The Board Panel’s redetermination in this matter is under judicial review by the Federal Court.

T-1419-20: on November 23, 2020, Innovative Medicines Canada and nineteen individual pharmaceutical companies brought an application in Federal Court for judicial review of the PMPRB’s decision to issue new Guidelines on October 23, 2020 (then slated to come into effect in July 1, 2021). The application seeks a declaration that the new Guidelines are ultra vires the Patent Act and an order quashing and setting aside the decision of the PMPRB to issue the new Guidelines. This matter is currently pending.

There are no PMPRB related matters before the Supreme Court of Canada.

Two challenges related to PMPRB legislation were commenced in 2019 and are ongoing:

T-1465-19: on September 6, 2019, Innovative Medicines Canada (I.M.C.) and sixteen individual pharmaceutical companies brought an application in Federal Court to judicially review s. 4 (new factors), s. 6 and Schedule (new basket of countries) and ss. 3(4) (new net price calculation) of the 2019 Amendments to the Patented Medicines Regulations (coming into force in January 2022) on the basis that they are ultra vires the regulation-making power contained in the Patent Act. The FederPal Court issued its decision on June 29, 2020, and held that the amendments in s 4, s. 6 and the Schedule are intra vires the Patent Act, but that the amendment in ss. 3(4) is not. On September 10, 2020, I.M.C. and the individual pharmaceutical companies filed a Notice of Appeal with respect to the Federal Court decision. The Attorney General of Canada has also filed a cross-appeal in respect of the invalidated amendments. This appeal is currently pending.

No. 500-17-109270-192. Merck et al. v Canada (Attorney General): on August 22, 2019, six individual pharmaceutical companies brought an application for judicial review in Quebec Superior Court challenging the constitutionality of ss. 79-103 of the Patent Act. In its decision issued on December 18, 2020, the Quebec Superior Court found the amendments to subsections 4(4)a) and 4(4)b) that would update the net price calculation to require patentees to include discounts and rebates provided to third parties unconstitutional and of no force or effect. The Court found the rest of the Regulations, including the other amendments, and the relevant sections of the Patent Act constitutionally valid. The pharmaceutical company applicants filed a Notice of Appeal with respect to the Superior Court of Quebec’s decision on January 25, 2021. The Attorney General of Canada has also filed a cross-appeal in respect of the invalidated amendments. The appeal remains pending.

Table 6. Status of Board Proceedings in 2020 up to May 31, 2021

| Medicine | Indication/use | Patentee | Issuance of notice of hearing | Status |

|---|---|---|---|---|

| Eculizumab (sold under trade name Soliris) | Paroxysmal nocturnal hemoglobinuria Atypical hemolytic uremic syndrome |

Alexion Pharmaceuticals Inc. | January 20, 2015 | Board Order: September 27, 2017. |

| Cysteamine bitartrate (sold under trade name Procysbi) |

Nephropathic cystinosis | Horizon Thearpeutics Canada | January 14, 2019 | Hearing held in 2020–2021 and decision is pending. |

| Medicine | Indication/use | Patentee | Issuance of Notice of Hearing | Status |

|---|---|---|---|---|

| Adapalene (sold under trade names Differin and Differin XP) | Acne | Galderma Canada Inc. | (redetermination) | Board Order: May 7, 2020. Galderma to file the required information for the requested period. * Application for Judicial Review and prior litigation: see below. |

| Medicine | Indication/use | Applicant | Issue | Date of notice of hearing/status |

|---|---|---|---|---|

Eculizumab (sold under trade name Soliris) |

Paroxysmal nocturnal hemoglobinuria |

Alexion Pharmaceuticals Inc. |

Allegations of excessive pricing |

Application for Judicial Review. Court File T-1596-17 (Re. Board Panel’s decision of September 20, 2017): Decision issued May 23, 2019. Notice of Appeal (Federal Court of Appeal) filed on June 21, 2019. Court File A-237-19: Matter pending |

Adapalene (sold under trade names Differin and Differin XP) |

Acne |

Galderma Canada Inc. |

Failure to file (jurisdiction) |

Application for Judicial Review. Court File T-83-17 (Re. Board Panel’s decision of December 19, 2016): Decision issued November 9, 2017 quashing in part the Board Panel’s decision. Notice of Appeal (Federal Court of Appeal) filed on November 21, 2017. Court File A-385-17. Decision issued on June 28, 2019. Matter sent for redetermination by the Board. Redetermination decision issued on May 7, 2020. Application for Judicial Review. Court File T-906-20 (Re. Board Panel’s Decision of May 7, 2020) filed on August 11, 2020. Matter pending. |

– |

– |

Innovative Medicines Canada et al |

Vires of new Guidelines issued by the PMPRB in October, 2020. |

Application for Judicial Review. Court File T-1419-20. |

Key pharmaceutical trends: more expensive medicines continue to influence sales

Overall spending on pharmaceuticals is influenced by many factors, including price, utilization, the entry of newer, more expensive medicines, and the loss of market exclusivity for older patented medicines. In 2020, there was a moderate rise in the sales of higher-cost medicines, resulting in an overall increase in total spending of 1.6%. Canadian list prices of patented medicines remained among the highest in the Organisation for Economic Co-operation and Development (OECD), ranking fourth, well behind the US and just marginally lower than Switzerland and Germany.

The PMPRB is responsible for reporting on trends in pharmaceutical sales and pricing for all medicines and for reporting research and development spending by patentees.

Under the Regulations, patentees are required to submit detailed information on their sales of patented medicines, including quantities sold, gross and net prices, and net revenues. The PMPRB uses this information to analyze trends in the sales, prices,Footnote 8 and use of patented medicines.Footnote 9 This section provides key trends, including analyses of Canadian national, public, and private payer markets for all medicines. Note that any reference to sales in this section should be interpreted as sales revenues unless otherwise noted.

An additional $4.9 billion was spent on medicines that previously reported to the PMPRB.

Disclaimers

- Although select statistics reported in the KEY PHARMACEUTICAL TRENDS section are based in part on data obtained under license from the MIDAS® database and the Private Pay Direct Drug Plan database proprietary to IQVIA Solutions Canada Inc. and/or its affiliates (“IQVIA”), the statements, findings, conclusions, views, and opinions expressed in this Annual Report are exclusively those of the PMPRB and are not attributable to IQVIA.

- To provide a broader perspective on pharmaceutical trends in Canada, summaries of the results of NPDUIS analyses have been included as additional “Brief Insights” throughout the Pharmaceutical Trends section of the Annual Report. A variety of public and licensed data sources are used for NPDUIS analytical studies. Many of these sources do not differentiate between patented and non-patented generic medicines; in these instances, the general term “generic” is used to include both. NPDUIS is a research initiative that operates independently of the regulatory activities of the PMPRB.

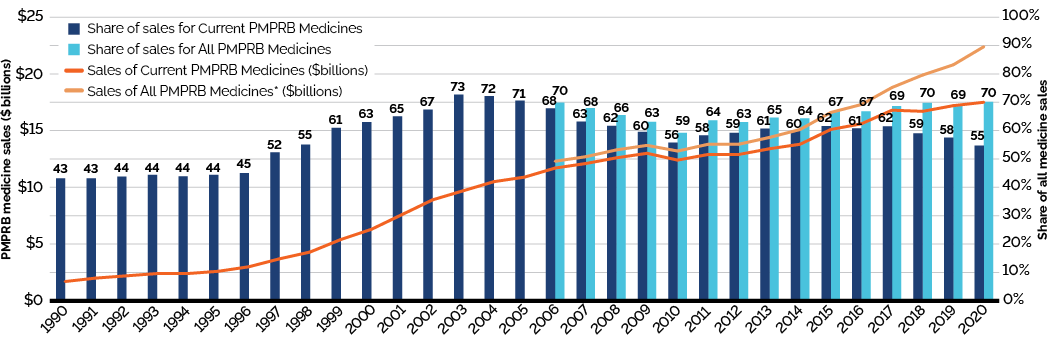

Trends in Sales of Patented Medicines

Canadians spend much more on patented medicines today than they did a decade ago. Over the last five years, sales of these medicines have grown by an average of 3.0% per year, reaching $17.5 billion in 2020. This section looks at the most important factors driving the change in sales revenues from 2019 to 2020 and compares them to trends from previous years.

Trends in Sales Revenues

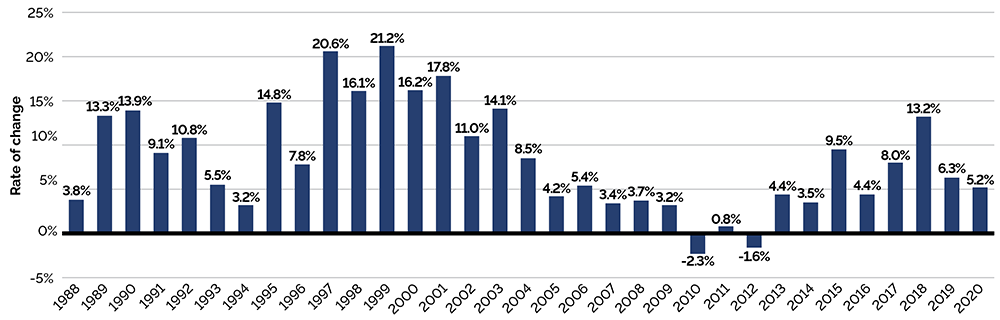

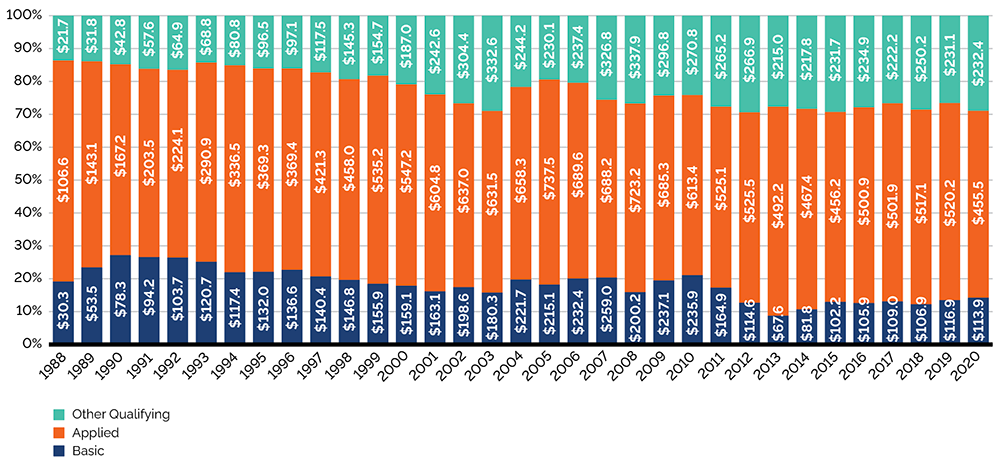

Between 2019 and 2020, there was a modest 1.6% increase in the sales of patented medicines. Figure 3 reports on trends in the sales of patented medicines from 1990 to 2020. While there has been a 10-fold increase in annual sales over the last 30 years, the year-over-year rate of change within that period has varied. This trend is highlighted by the five-year compound annual growth rate given in Figure 3(b).

Figure 3(a) gives the sales of patented medicines as a share of overall medicine sales. This share reached a peak of 72.7% in 2003. In 2020, patented medicines accounted for 54.7% of the sales of all medicines in Canada.

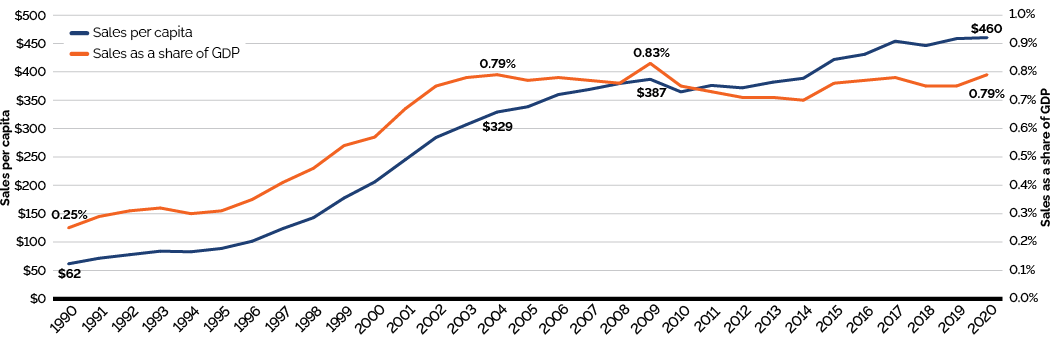

The trends in sales per capita and sales as a percentage of the gross domestic product (GDP) show the increasing importance of patented medicines in the Canadian economy. Overall, per capita sales of patented medicines rose from $61.60 in 1990 to $460.37 in 2020, while sales as a percentage of GDP rose from 0.25% in 1990 to 0.79% in 2020 [Figure 3(c)].

To highlight the continuing impact of patented medicines, Figures 3(a) and 3(b) also provide results for “All PMPRB Medicines”. This broader category includes all medicines, current and historic, that ever reported sales to the PMPRB.

Sales for All PMPRB Medicines rose by 7.7% in 2020. Medicines that previously reported to the PMPRB accounted for estimated sales of $4.9 billion, or 15.4% of all sales. This is considerably more than a decade ago when medicines that formerly reported to the PMPRB accounted for $0.8 billion, or 3.4% of all sales.

A complete table of the data presented in Figure 3 for patented medicines currently reporting to the PMPRB is included in Appendix 3.

Figure 3. Trends in Patented Medicine Sales, 1990 to 2020

* Includes sales of currently patented medicines and medicines that once reported to the PMPRB but are no longer reporting a patent.

Data source: PMPRB; MIDAS® database, 1990–2020, IQVIA (all rights reserved)

Figure description

Figure 3 (a) – Patented medicine share of all medicine sales: Current PMPRB Medicines and All PMPRB Medicines*s

This line and bar graphic depicts the annual sales of patented medicines currently reporting to the PMPRB and patented medicines that once reported to the PMPRB but are no longer reporting a patent and the patented medicine share of sales for current PMPRB medicines and sales for all PMPRB medicines, for the period from 1990 to 2020.

In 1990, the sales of current PMPRB patented medicines was $1.7 billion and the current PMPRB patented medicine share of all medicine sales was 43.2%;

1991: $2.0 billion, 43.2%;

1992: $2.2 billion, 43.8%;

1993: $2.4 billion, 44.4%;

1994: $2.4 billion, 43.9%;

1995: $2.6 billion, 44.4%;

1996: $3.0 billion, 45.0%;

1997: $3.7 billion, 52.3%;

1998: $4.3 billion, 55.1%;

1999: $5.4 billion, 61.0%;

2000: $6.3 billion, 63.0%;

2001: $7.6 billion, 65.0%;

2002: $8.9 billion, 67.4%;

2003: $9.7 billion, 72.7%;

2004: $10.5 billion, 72.2%;

2005: $10.9 billion, 70.6%.

In 2006, the sales of current PMPRB medicines was $11.7 billion, current PMPRB medicines share of all medicine sales was 67.8%, the sales of all PMPRB medicines was $12.3 billion, and the share of sales for all PMPRB medicines was 69.9%;

2007: $12.1 billion, 63.2%, $12.7 billion, 67.9%;

2008: $12.6 billion, 61.7%, $13.3 billion, 65.5%;

2009: $13.0 billion, 59.6%, $13.7 billion, 63.1%;

2010: $12.4 billion, 55.8%, $13.2 billion, 59.2%;

2011: $12.9 billion, 58.3%, $13.8 billion, 63.6%;

2012: $12.9 billion, 59.2%, $13.8 billion 63.0%;

2013: $13.4 billion, 60.7% $14.4 billion, 64.6%;

2014: $13.8 billion, 59.9%, $15.1 billion, 64.3%;

2015: $15.1 billion, 61.6%, $16.6 billion, 66.9%;

2016: $15.6 billion, 60.8%, $17.3 billion, 66.8%;

2017: $16.8 billion, 61.5%, $18.8 billion, 68.6%;

2018: $16.7 billion, 59.0%, $19.9 billion, 69.8%;

2019: $17.2 billion, 57.5%, $20.8 billion, 69.3%;

2020: $17.5 billion, 54.7%, $22.4 billion, 70.1%.

Note: As data is updated each year, historical results may not exactly match those reported in previous editions.

* Includes sales of currently patented medicines and medicines that once reported to the PMPRB but are no longer reporting a patent.

Data source: PMPRB; MIDAS® database, 1990–2020, IQVIA (all rights reserved)

Figure description

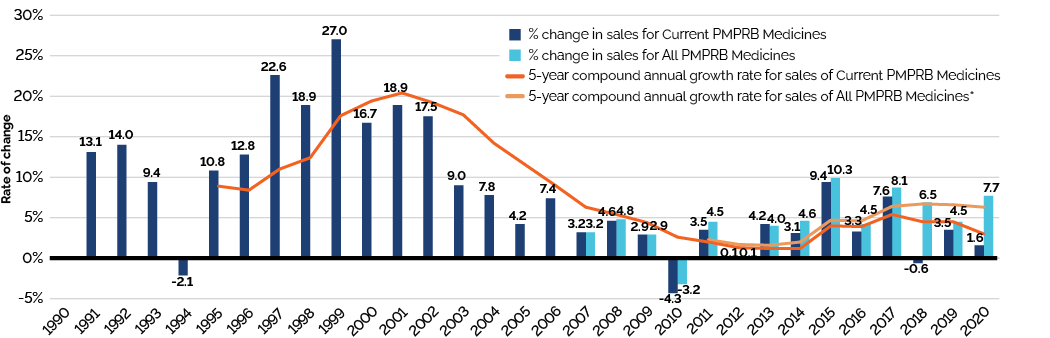

Figure 3 (b) – Rate of change in patented medicine sales: Current PMPRB Medicines and All PMPRB Medicines*

This line and bar graphic depicts the annual rate of change in patented medicine sales and the 5-year compound annual growth rate from 1990 to 2020 for patented medicines currently reporting to the PMPRB and patented medicines that once reported to the PMPRB but are no longer reporting a patent.

In 1991, the rate of change in sales for Current PMPRB medicines was 13.1%;

1992: 14.0%;

1993: 9.4%;

1994: -2.1%.

In 1995, the rate of change in sales for Current PMPB medicines was 10.8% and the 5-year compound annual growth rate for sales of Current PMPRB medicines was 8.9%;

1996: 12.8%, 8.4%;

1997: 22.6%, 11.0%;

1998: 18.9%, 12.4%;

1999: 27.0%, 17.6%;

2000: 16.7%, 19.4%;

2001: 18.9%, 20.4%;

2002: 17.5%, 19.2%;

2003: 9.0%, 17.7%;

2004: 7.8%, 14.2%;

2005: 4.2%, 11.6%;

2006: 7.4%, 9.0%.

In 2007, the rate of change in sales for Current PMPRB medicines was 3.2%, the 5-year compound annual growth rate for sales of Current PMPRB medicines was 6.3% and the rate of change in sales for All PMPRB medicines was 3.2%;

2008: 4.6%, 5.4%, 4.8%;

2009: 2.9%, 4.4%, 2.9%;

2010: -4.3%, 2.6%, -3.2%;

In 2011, the rate of change in sales for Current PMPRB medicines was 3.5%, the 5-year compound annual growth rate for sales of Current PMPRB medicines was 2.0%, the rate of change in sales for All PMPRB medicines was 4.5%, and the 5-year compound annual growth rate for sales of All PMPRB medicines was 2.3%;

2012: 0.1%, 1.3%, 0.1%, 1.7%;

2013: 4.2%, 1.2%, 4.6%, 2.0%;

2014: 3.1%, 1.2%, 4.6%, 2.0%;

2015: 9.4%, 4.0%, 9.9%, 4.7%;

2016: 3.3%, 3.9%, 4.2%, 4.6%;

2017: 7.6%, 5.4%, 8.7%, 6.4%;

2018: -0.6%, 4.5%, 6.9%, 6.7%;

2019: 3.5%, 4.5%, 4.5%, 6.6%;

2020: 1.6%, 3.0%, 7.7%, 6.3%.

Data source: PMPRB; Statistics Canada; OECD

Figure description

Figure 3 (c) – Patented medicine sales per capita and as a share of GDP: Current PMPRB Medicines

This line graphic depicts Current PMPRB medicine sales per capita and as a share of GDP from 1990 to 2020. In 1990, Current PMPRB medicine sales per capita was $61.60 and as a share of GDP 0.25%;

In 1991: $71.40, 0.29%;

1992: $77.70, 0.31%;

1993: $83.90, 0.32%;

1994: $82.80, 0.30%;

1995: $88.70, 0.31%;

1996: $101.40, 0.35%;

1997: $123.70, 0.41%;

1998: $142.90, 0.46%;

1999: $177.60, 0.54%;

2000: $205.90, 0.57%;

2001: $245.20, 0.67%;

2002: $284.30, 0.75%;

2003: $307.00, 0.78%;

2004: $329.20, 0.79%;

2005: $338.50, 0.77%;

2006: $360.00, 0.78%;

2007: $368.90, 0.77%;

2008: $379.50, 0.76%;

2009: $386.90, 0.83%;

2010: $364.70, 0.75%;

2011: $376.10, 0.73%;

2012: $371.80, 0.71%;

2013: $381.80, 0.71%;

2014: $388.70, 0.70%;

2015: $421.80, 0.76%;

2016: $430.94, 0.77%;

2017: $454.09, 0.78%;

2018: $446.30, 0.75%;

2019: $458.60, 0.75%;

2020: $460.37, 0.79%.

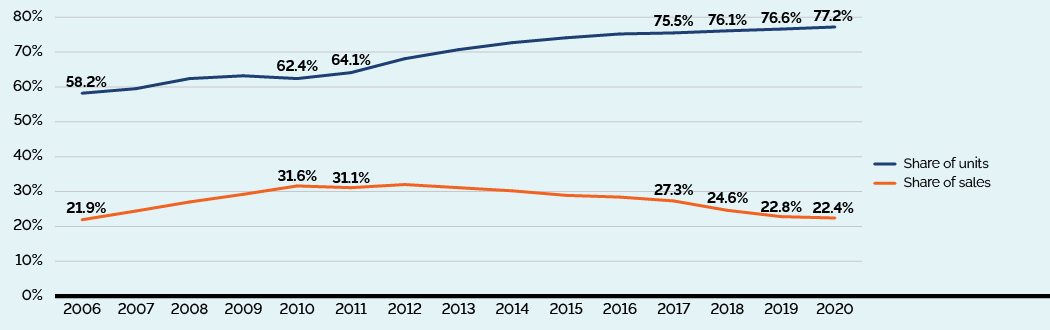

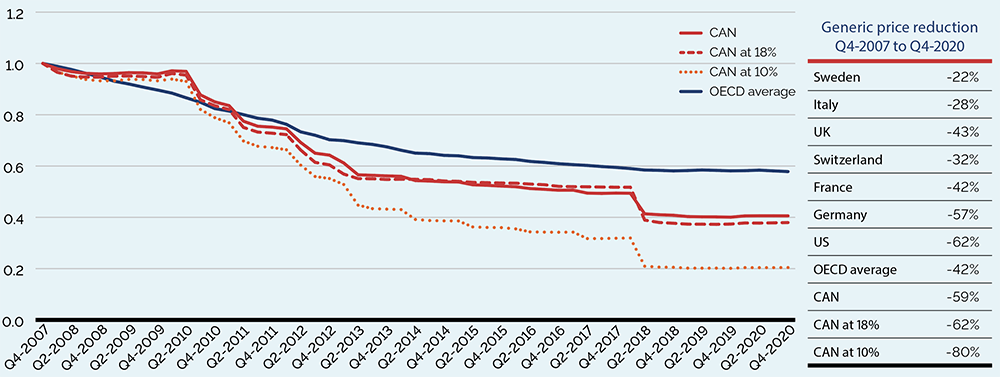

Brief Insights: Trends in the Sales of Generic Medicines

While sales of patented medicines increased by 1.6% in 2020, retail sales of generic medicines rose by 5.5%. This is a notable increase over the generally low or negative rates of change observed since 2010, which were due in large part to the introduction of price-setting policies initiated by individual provincial governments and through the pan-Canadian Pharmaceutical Alliance (pCPA).

In 2018, the introduction of a five-year joint agreement between the pCPA and the Canadian Generic Pharmaceutical Association (CGPA) reduced the prices of 67 generic medicines to 10% or 18% of their reference brand price, driving expenditures down to virtually the same level as in 2010, even as generics continued to grow as a share of units sold in the retail pharmaceutical market (Figure 4).

As the prices of generic medicines begin to stabilize, the return to higher rates of sales growth in 2020 reflects a sustained increase in the use of generics over the previous year.

Note: The results reflect prescription sales in the national retail market based on manufacturer ex-factory list prices.

Data source: MIDAS® database, 2006–2020, IQVIA (all rights reserved)

[NPDUIS Report: Generics360, 2018 – graph updated for 2019 and 2020]

Figure description

This line graph gives the generic share of the retail pharmaceutical market in Canada from 2006 to 2020 in terms of spending (sales) and units sold.

| 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

Share of units |

58.2% |

59.5% |

62.4% |

63.2% |

62.4% |

64.1% |

68.1% |

70.7% |

72.7% |

74.1% |

75.2% |

75.5% |

76.1% |

76.6% |

77.2% |

Share of sales |

21.9% |

24.4% |

27.0% |

29.2% |

31.6% |

31.1% |

32.0% |

31.1% |

30.2% |

28.9% |

28.4% |

27.3% |

24.6% |

22.8% |

22.4% |

Drivers of the Growth in Sales Revenues

The growth in the sales revenues of patented medicines is influenced by changes in several key factors:

- Volume effect: changes in the quantity or amount of patented medicines sold.

This effect focuses on established medicines that were on the market for the period analyzed. Increases in the population, changes in demographic composition (e.g., shifts in the age distribution), increases in the incidence of disease, and changes in prescribing practices are among the factors that may contribute to this effect. - Mix effect: shifts in use between lower- and higher-cost patented medicines.

This effect applies to both new medicines and those that were already on the market. The switch to new higher-priced medicines, the use of new medicines that treat conditions for which no effective treatment previously existed, and changes in prescribing practices are among the factors that may contribute to this change. - Exiting effect: previously patented medicines that have stopped reporting sales revenues to the PMPRB or are no longer sold in Canada.

- Loss-of-exclusivity effect: medicines that have lost market exclusivity and are open to some level of generic competition but are still patented.

- Price effect: changes in the prices of existing patented medicines.

This effect applies to both increases and decreases in the prices of patented medicines over the time period analyzed.

Some factors, such as the mix effect, will generally put an upward pressure on sales, while others, such as the loss-of-exclusivity effect, have the opposite effect.

Figure 5 focuses on the major factors that drove the year-by-year growth in patented medicine salesFootnote 10 between 2015 and 2020 (a) in absolute dollar amounts, and (b) as proportions of the overall annual change in sales. In addition to the standard sales drivers, the emergence of new “blockbuster” medicines that have a significant influence on sales may be monitored as a separate effect. For example, direct-acting antiviral (DAA) treatments for hepatitis C are presented separately to show their continuing impact on expenditures.

Figure 5. Key Drivers of Change in the Sales of Patented Medicines, 2015 to 2020

Note: When multiple factors change simultaneously, they create a residual or cross effect, which is not reported separately in this analysis, but is accounted for in the total cost change.

Values may not add to the net change due to rounding and the cross effect.

Results for 2018 and 2019 have been updated and may not match those reported in previous editions.

* As this model uses various measures to isolate the factors contributing to growth, the net change reported here may differ slightly from the change in sales for the patented medicines market reported in Figure 3(b).

Data source: PMPRB

Figure description

These two bar graphs describe the factors that impacted the annual rates of change in the sales of patented medicines from 2015 to 2020. The first graph gives the rate of change in absolute dollar amounts and the second gives the corresponding percent rate of growth for each contributing factor along with the total push up (positive) and pull down (negative) effects. Direct-acting antiviral (DAA) medicines for hepatitis C are presented separately from the rest of the drug-mix effect because of their high impact.

(a) Absolute change in millions of dollars

| Exiting | Loss-of-Exclusivity | Mix, Other Drugs | Mix, DAAs for hepatitis C | Volume | Price | |

|---|---|---|---|---|---|---|

2015 |

-$531 |

-$372 |

$714 |

$690 |

$485 |

$91 |

2016 |

-$509 |

-$226 |

$1,240 |

-$130 |

$192 |

-$77 |

2017 |

-$271 |

-$150 |

$1,001 |

$80 |

$517 |

-$26 |

2018 |

-$1,833 |

-$299 |

$964 |

$86 |

$1,107 |

-$35 |

2019 |

-$711 |

-$313 |

$1,859 |

-$177 |

-$267 |

$76 |

2020 |

-$795 |

-$191 |

$1,016 |

-$297 |

$468 |

$38 |

| Absolute change (millions of dollars) | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 |

|---|---|---|---|---|---|---|

Total Pull Effects |

-$903 |

-$943 |

-$446 |

-$2,167 |

-$1,428 |

$1,283 |

Total Push Effects |

$1,980 |

$1,432 |

$1,597 |

$2,157 |

$1,876 |

$1,523 |

Net Change |

$1,077 |

$490 |

$1,151 |

-$10 |

$448 |

$263 |

Note: When multiple factors change simultaneously, they create a residual or cross effect, which is not reported separately in this analysis, but is accounted for in the total cost change.

Values may not add to the net change due to rounding and the cross effect.

* As this model uses various measures to isolate the factors contributing to growth, the net change reported here may differ slightly from the change in sales for the patented medicines market reported in Figure 3(b).

Data source: PMPRB

Figure description

(b) Relative change in percent

| Exiting | Loss-of-Exclusivity | Mix, Other Drugs | Mix, DAAs for hepatitis C | Volume | Price | |

|---|---|---|---|---|---|---|

2015 |

-3.7% |

-2.6% |

5.0% |

4.9% |

3.4% |

0.6% |

2016 |

-3.3% |

-1.5% |

8.1% |

-0.9% |

1.3% |

-0.5% |

2017 |

-1.7% |

-0.9% |

6.3% |

0.5% |

3.3% |

-0.2% |

2018 |

-10.9% |

-1.8% |

5.7% |

0.5% |

6.6% |

-0.2% |

2019 |

-3.9% |

-1.9% |

10.7% |

-1.0% |

-1.6% |

0.5% |

2020 |

-4.6% |

-1.1% |

5.9% |

-1.7% |

2.7% |

0.2% |

| Relative change (in percent) | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 |

|---|---|---|---|---|---|---|

Total Pull Effects |

-6.4% |

-6.2% |

-2.8% |

-12.9% |

-8.5% |

-7.4% |

Total Push Effects |

13.9% |

9.4% |

10.1% |

12.8% |

11.2% |

8.8% |

Net Change |

7.6% |

3.2% |

7.3% |

-0.1% |

2.7% |

1.5% |

Changes in the prices of patented medicines have played a very minor role in the growth in patented medicine sales over the last several years, suggesting that, on average, the prices of existing patented medicines are fairly stable. However, this does not reflect the overall increases in treatment costs due to the entry of newer, higher-priced patented medicines, the impact of which is captured by the mix effect.

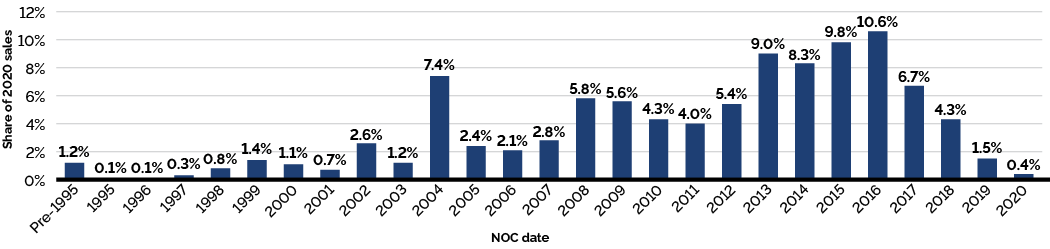

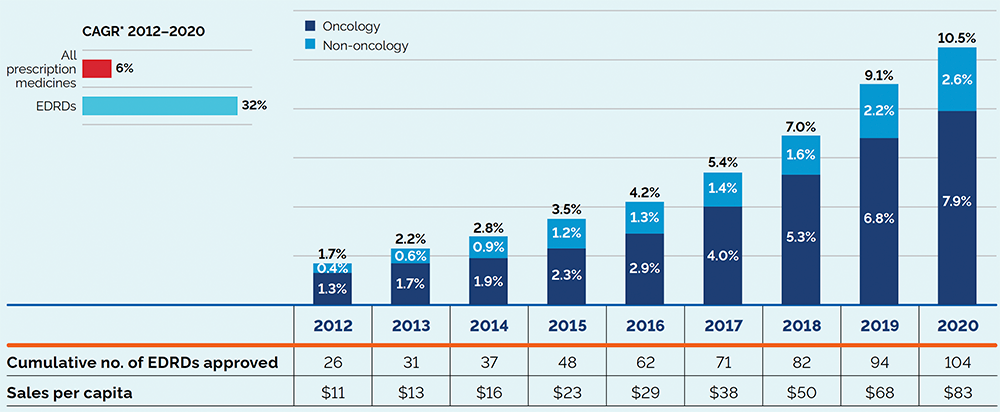

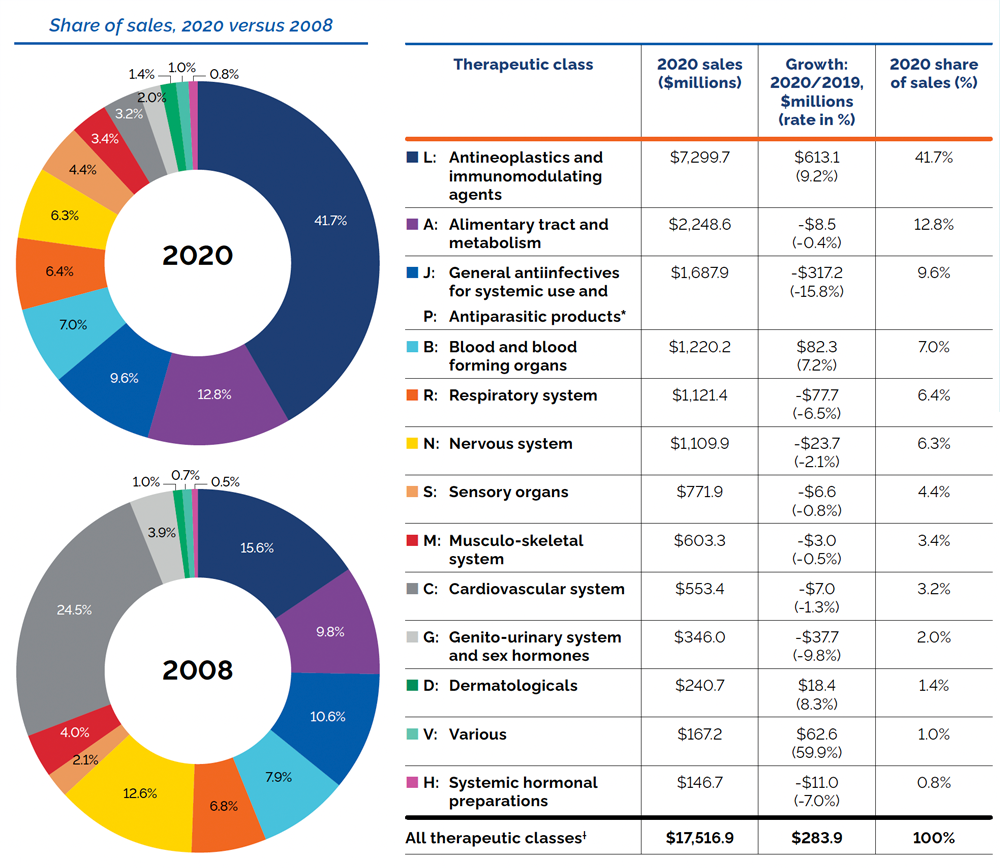

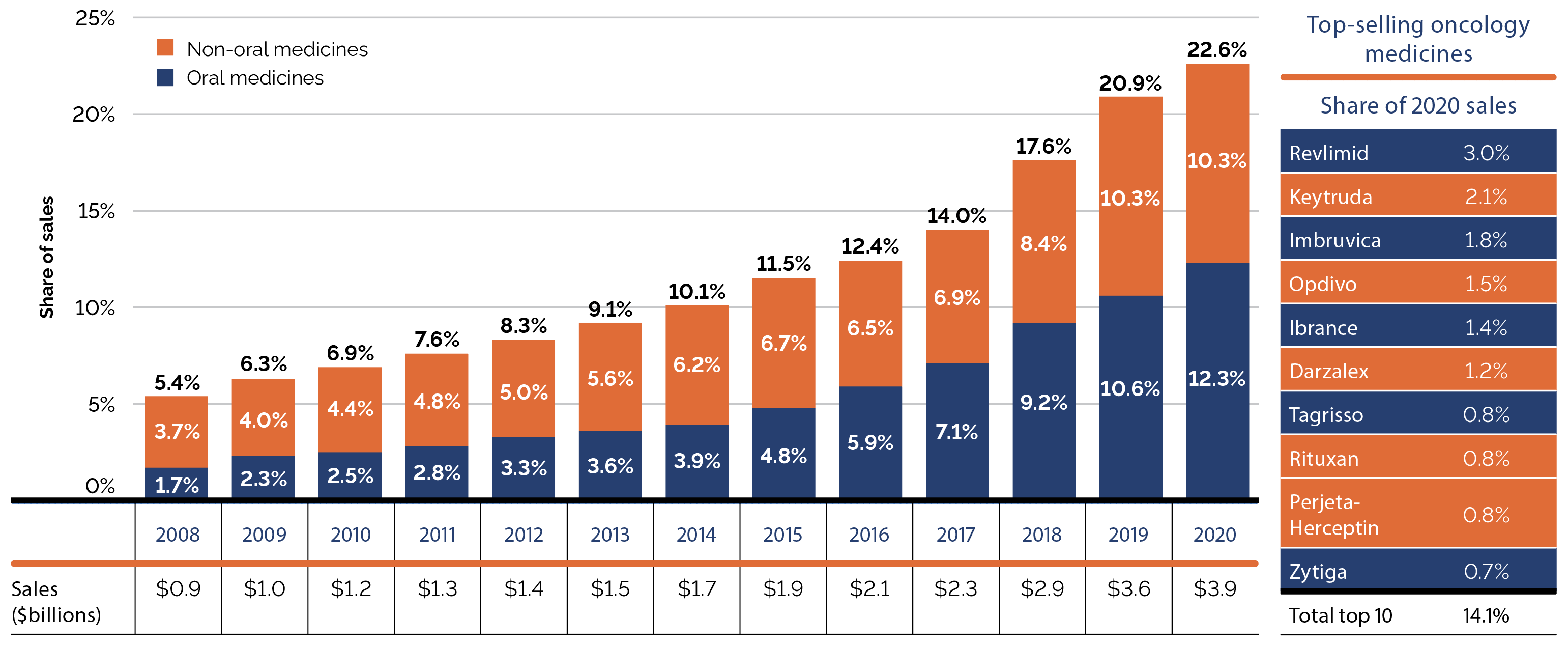

The shift to new higher-cost patented medicines has been a major driver of sales growth in recent years. In 2020, the use of higher-cost patented medicines other than DAAs put an upward pressure on expenditures of $1.0 billion (5.9%). While growth was observed in many therapeutic areas, the increase in sales of “antineoplastic and immunomodulating agents” exceeded that of any other class. These medicines, which include oncology treatments, accounted for more than 40% of all patented medicine sales in 2020. Results by therapeutic class are discussed in further detail in the upcoming sections.

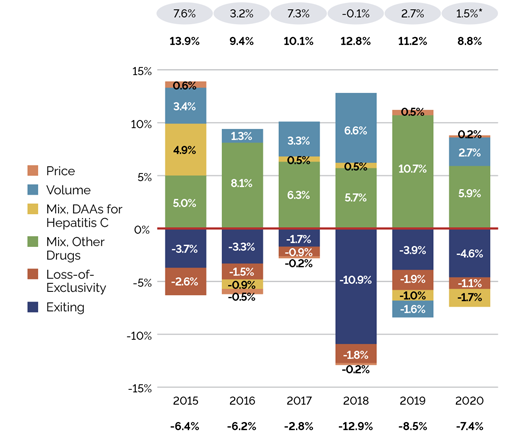

Counterbalancing the upward sales pressures from the mix effect, there was a moderate market segment shift as some high-selling medicines stopped reporting their sales to the PMPRB. The exiting effect accounted for a loss of $795 million (-4.6%) in sales in 2020. Figure 6 illustrates the change in the impact of the exiting effect since 2015 and identifies the 10 top-selling medicines that stopped reporting to the PMPRB in 2020.

Figure 6. Loss in Patented Medicine Sales from the Exiting Effect, 2015 to 2020

Note: If a medicine stops reporting a patent mid-way through the year, its impact may be reflected in the exiting effect in more than one reporting year.

The amounts reported in any given year may not reflect an entire year’s worth of sales for these medicines.

Data source: PMPRB

Figure description

This bar graph describes the change in patented medicine sales caused by patented medicines no longer reporting patents from 2015 to 2020. An accompanying table gives the change in sales for the top-selling medicines that stopped reporting patents in 2020.

| Year | Change in sales (millions of dollars) |

|---|---|

2015 |

-$531 |

2016 |

-$509 |

2017 |

-$271 |

2018 |

-$1,833 |

2019 |

-$653 |

2020 |

-$795 |

| Top-selling medicines that stopped reporting to the PMPRB in 2019 | Change in sales (millions of dollars) |

|---|---|

Lupron Depot |

- $72M |

Victoza |

- $55M |

Biphentin |

- $55M |

Nexium |

- $54M |

Zenhale |

- $33M |

Tiazac XC |

- $25M |

Saxenda |

- $23M |

Norvasc |

- $20M |

Prevacid |

- $18M |

NiaStase |

-$17M |

Brief Insights: Cost Drivers of Public and Private Drug Plans

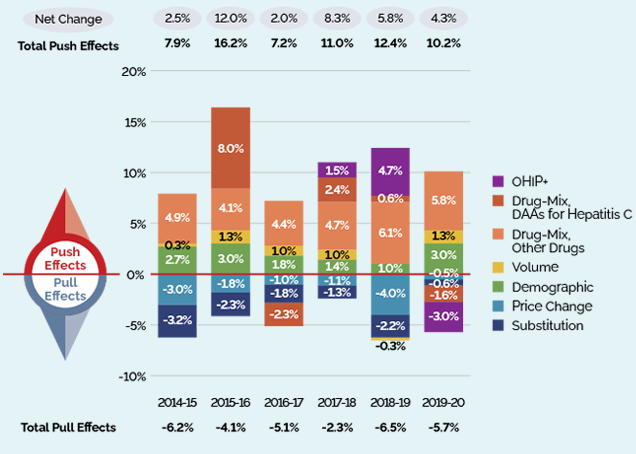

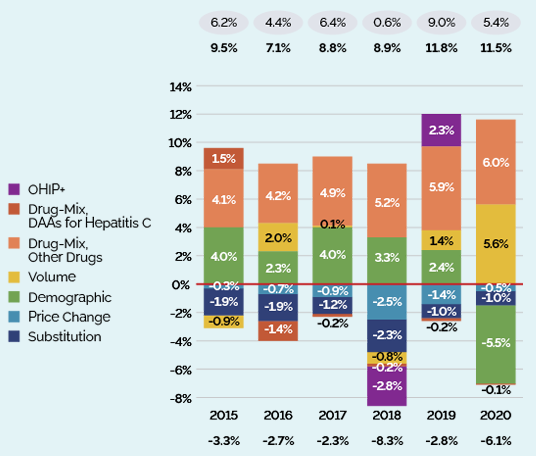

The increasing use of higher-cost medicines is the primary cost driver for Canadian public and private drug plans. Over the past several years, higher-cost medicines (other than DAAs for hepatitis C) have exerted a consistent upward pressure on expenditures, accounting for a significant 5.8% contribution toward drug costs in public plans in 2019–20 and 6.0% toward private plan costs in 2020.

Growth in fiscal year 2019–20 (public plans) and calendar year 2020 (private plans) was marked most distinctly by changes in plan designs and eligible beneficiary populations. The OHIP+ program in Ontario adjusted its eligibility requirements in 2019 to only cover those 24 and under without private insurance, resulting in a notable 3.0% offset to growth for public plans. This pull was counterweighted by a 3.0% push in the demographic effect, primarily due to expanded eligibility of the beneficiary population in British Columbia.

For private payers, a decline in the number of claimants in working age groups in 2020, likely in relation to the COVID-19 pandemic, resulted in a pull effect of -5.5% on drug plan expenditures, while a sizable increase in the number of claims per patient pushed spending upward by 5.6%. This rise, as captured in the volume effect, was mainly driven by a more frequent use of medicines that treat chronic conditions such as heart disease and diabetes.

The significant downward force exerted by generic pricing policies under the price change effect in 2018–19 did not have the same impact on public or private drug plan costs in 2019–20. However, savings are expected to be realized in the substitution effect in coming years as a result of recent biosimilar policy changes in many public drug plans, as well as initiatives introduced by some private payers, aimed at promoting switching from biologic originators to available biosimilars. With a strong market for biologics in Canada, these efforts may act as a means of offsetting the mounting pressure from higher-cost medicines.