2020 Second Annual Report of the Disability Advisory Committee

Table of Contents

- Introduction

- The Client Experience

- Preface

- Part 1: Review of Recommendations

- Part 2: Other Issues

- Appendices

- Appendix A – Terms of Reference

- Appendix B – Description of Federal Measures for Persons with Disabilities

- Appendix C – List of Committee Members

- Appendix D – Disability Measures Linked to DTC Eligibility

- Appendix E – Form T2201, Disability Tax Credit Certificate

- Appendix F – Disability Tax Credit Client Experience Survey Results

- Appendix G – Information Sheets

- Appendix H – Updated Tables for the DTC Statistical Publication

- Appendix I – Jordan’s Principle

- Appendix J – New Recommendations

- Appendix K – First Annual Report Recommendations

Introduction

In November 2017, the Minister of National Revenue, the Honourable Diane Lebouthillier, announced the creation of the Disability Advisory Committee to provide advice to the Canada Revenue Agency (CRA) on interpreting and administering tax measures for persons with disabilities in a fair, transparent and accessible manner. The committee’s full mandate is attached as Appendix A. Key disability tax measures are described in Appendix B.

Members of the Disability Advisory Committee very much appreciate the opportunity to advise the Minister of National Revenue and to work with CRA officials on improving disability tax measures. The full list of committee members is attached as Appendix C.

Our first annual report, Enabling access to disability tax measures, was published in May 2019. Since that time, we believe there has been important progress with respect to the administration of and communications about the disability tax credit (DTC). Our second annual report describes in detail the many improvements that the CRA has introduced over the past year in response to the recommendations in our 2019 report. These changes are summarized in “The Client Experience” on the following pages.

Section 1 of this second annual report presents a review of the 42 recommendations made in our first annual report. Each recommendation summarizes the relevant context and associated follow-up actions.

Section 2 covers the new areas of conversation during the second year of our mandate. Selected topics focus, for example, on DTC data, concerns of Indigenous peoples and eligibility for a registered disability savings plan.

Section 3 includes the appendices, which provide details not covered in the text.

As in the first year of our mandate, the DTC has continued to be the primary focus of our work. The committee recognizes the challenges involved in the fair and consistent assessment of DTC eligibility. We know that this determination is no easy task.

The key eligibility criterion is not the presence of a severe and prolonged disability, but rather the effect of this condition on day-to-day functioning. Eligible applicants must be markedly restricted in at least one of the basic activities of daily living as specifically defined in legislation and administered by the CRA.

Moreover, the DTC story is especially complex because this particular tax measure fulfils two distinct purposes.

First, the DTC reduces the income tax payable of applicants who qualify because they have a severe and prolonged impairment in physical and/or mental functions that impedes their ability to carry out the basic activities of daily living. Canadians with severe disabilities are likely to incur additional costs not experienced by persons without disabilities. These extra expenses are often not readily itemizable, like the costs that may be claimed under the medical expense tax credit or the disability supports deduction (DSD).

Second, the DTC plays a vital role in the landscape of disability-related measures. The DTC has become the gateway to establishing eligibility for a number of federal disability benefits and programs. These are listed in Appendix D.

While access to the DTC has been a long-standing concern, access challenges have become all the more pressing as many Canadians apply not only, or even necessarily, for the financial assistance component of the DTC. They are applying instead for the various benefits and programs linked to DTC eligibility.

As a result of its expanded role, the DTC has effectively become a centrepiece of federal disability policy. Many Canadians with disabilities may not be aware of this dual role. The recent federal announcement of a COVID-19 benefit for persons with disabilities is a prime example of the DTC gateway function and its associated challenges.

In June 2020, the federal government announced a one-time, tax-free, non-reportable payment of up to $600 to DTC-eligible individuals in order to assist with additional expenses incurred during the pandemic. These expenses include, for example, higher costs for personal protective equipment, hiring personal support workers or accessing other disability supports.

When the COVID-19 payment was first announced, the disability community was concerned that many Canadians with disabilities would not receive this financial assistance because they are not eligible for the DTC. While the new measure was positive in its intent, it would have been limited in its impact, as most persons with disabilities would not have qualified for this pandemic-related assistance.

The federal government subsequently expanded the eligibility criteria in July 2020 to include:

- Canadians who are eligible for the DTC

- persons who may be eligible for the DTC (they have up to 60 days to apply after the bill receives royal assent)

- recipients of the Canada Pension Plan or Quebec Pension Plan disability benefit

- recipients of disability supports provided by Veterans Affairs Canada

The expanded criteria will help an estimated 1.7 million Canadians with disabilities benefit from the new financial assistance. The original announcement actually had served to highlight the problems in using the DTC as the sole gateway to other benefits. It was too narrow an entry point. The committee discussed this concern in our first annual report and identified it once again in the recommendations review section of this second annual report.

While there have been many significant improvements in CRA administrative processes and communications, we acknowledge that significant challenges remain around the DTC and other disability tax measures, such as the DSD. We recognize the difficulties experienced by certain groups, including Indigenous Canadians with disabilities, individuals with impairment in mental functions and persons who live with severe, but episodic, conditions.

Our report also considers DTC refundability. We note that the ability to pay up front for many disability-related goods and services is a major challenge facing persons with disabilities, a problem linked to their disproportionately higher rates of poverty.

The committee will continue to focus on these wide-ranging issues, bearing in mind our mandate is based explicitly on disability tax measures. In the meantime, we hope that our work to date has helped to make these measures more understandable, accessible and fair for the hundreds of thousands of Canadians who rely on this assistance to improve the quality of their lives.

The Client Experience

Over the past year, the Canada Revenue Agency (CRA) has introduced many important changes to its administrative procedures regarding the disability tax credit (DTC) and to its communications and outreach activities. Many of these measures were introduced in response to the Disability Advisory Committee’s previous recommendations.

The changes are intended to help applicants access the DTC, as well as reduce the potential for problems that may lead to delays in eligibility decisions and the need for appeals. Ideally, the entire DTC process will be more transparent, expeditious and fair.

These improved procedures are described in the second annual report. The highlights are presented below.

Information

- The CRA is improving the quality of information provided to applicants and the organizations and individuals who support them at both the preapplication and the application stages of DTC eligibility

- All materials are being reviewed for plain language and accessibility

- DTC-related web pages are being reviewed as part of a web optimization project

- The CRA has increased its investment in its Community Volunteer Income Tax Program. The investment will help expand its reach, particularly among organizations serving Indigenous peoples and organizations representing persons with impairment in mental functions

Designated call line

- The regular CRA phone line will continue to respond to basic questions, such as where to obtain and how to complete the DTC application, Form T2201, Disability Tax Credit Certificate

- More complex questions are being directed to a designated call line with specially trained staff. These questions generally relate to DTC eligibility criteria, impairment in mental functions, applications on behalf of children and DTC appeals

Navigator

The CRA is introducing a navigator function to help individuals with complex circumstances work their way through the DTC application process.

Form T2201, Disability Tax Credit Certificate

- The CRA is developing a digital application of Form T2201. This interactive application for health providers (and others) will:

- streamline the application process by ensuring the CRA gets the information it needs so applicants can get access to related financial supports

- provide greater certainty to the application process and reduce the need for clarification letters

- clarify the DTC eligibility criteria for persons with disabilities and health providers

- The CRA has redesigned the paper version of Form T2201, which is being tested with health providers, individuals and DTC assessors

- The CRA is currently exploring selected federal and provincial/territorial programs for how they handle the treatment of certain conditions for the purpose of expedited processing

Procedural changes

- The CRA is working to provide more information, guidelines and examples earlier in the application process in order to reduce and, ideally, eliminate the need for clarification letters

- The CRA currently:

- informs the health provider that all communication to a health provider about an applicant will be copied to the applicant and that any communication the health provider sends to the CRA will also be made available to the applicant

- encourages the health provider to contact and consult the applicant as necessary when providing any clarification to the CRA

- gives the health provider 60 days to respond to a clarification letter. The letter indicates that while the health provider has 45 days to respond, the case is not closed until 60 days have passed. This practice is intended to reduce processing times and associated delays

- Better and more consistent training is being provided to current and new assessors of DTC cases that involve impairment in mental functions

DTC-linked benefits

The requirement to close a Registered Disability Savings Plan (RDSP) when a beneficiary no longer qualifies for the DTC has been eliminated.

Preface

The Disability Advisory Committee has benefited from a collaborative relationship with the leadership and staff of the Canada Revenue Agency (CRA). We believe that they share the committee’s goal of improving the administration of disability tax measures for all Canadians.

The opinions and recommendations presented in our report have been informed by the concerns we have heard from Canadians with disabilities and their families, as well as health providers who complete the disability tax credit (DTC) application: Form T2201, Disability Tax Credit Certificate.

In some cases, we have highlighted the challenges that a single individual has brought to our attention in a submission to the committee. We acknowledge that we are unable to determine whether the issue being raised is unique to that person or whether it may apply to tens or even hundreds of Canadians.

When the report describes difficulties experienced by Canadians, it is possible that the difficulties we are describing may have been, or are in the process of being, resolved by the CRA. The policy or practice in question may have been corrected. Moreover, the problems a given individual faces may be based on limitations in their understanding of the complex DTC eligibility criteria and associated procedures, which in itself may flag the need for more legislative, administrative or communications clarity.

The committee recognizes that CRA officials have no opportunity to respond to or explain the particulars of a specific case, especially in light of confidentiality requirements. At the same time, we know that many DTC applicants have serious concerns that need to be heard. We believe that it is our role to help give people a voice.

If a case or matter has already been resolved, then that is an excellent outcome for all parties. If, however, a single story affects many others, then we have fulfilled our obligation to turn private troubles into public issues which, ideally, can be addressed and constructively resolved.

Part 1: Review of Recommendations

This section of the second annual report reviews the status of the 42 recommendations the Disability Advisory Committee made in our first annual report. These recommendations were developed within the context of a distinct narrative of the objectives that the committee is seeking to achieve.

The first cluster (recommendations #1–16) focuses on changes to the eligibility criteria that would better reflect the intent, and improve the clarity and interpretation of the disability tax credit (DTC).

The second group (recommendations #17–24) explores various administrative improvements. While the administration of the DTC would be far improved if certain legislative changes were made, the committee recognized that administrative modifications even on their own would be helpful to ensure the more effective and efficient delivery of that tax measure.

After considering both legislative improvements to the eligibility criteria and administrative enhancements, the next category (recommendations #25–31) discusses how best to communicate with persons with disabilities and the public about the DTC and disability-related tax measures, more generally.

Our recommendations (#32–35) subsequently shift to the broader role of the DTC as an entry point to other disability-related benefits and programs. Eligibility for the DTC has assumed an increasingly important role in the landscape of disability measures because of this gateway function.

The final cluster (recommendations #36–42) highlights the costs of disability. Our recommendations begin with a narrow focus on fees linked to the DTC application process and end with a broader discussion of disability-related costs and the disproportionately high rates of poverty among persons with disabilities.

Review of Recommendations

Recommendation #1

That in the determination of disability tax credit (DTC) eligibility, the Canada Revenue Agency (CRA) ensures that the principle of parity guides its actions with respect to physical and mental functions including, but not limited to, the removal of multiple screens of eligibility for persons with impairment in mental functions.

Background

In our first annual report, the Disability Advisory Committee (DAC) noted that there are several aspects of the DTC application process in which impairment in physical functions and mental functions is treated differently.

The DTC application, Form T2201, Disability Tax Credit Certificate, requires that three distinct mental functions, problem-solving, goal-setting and judgment, must be “taken together.” This wording implies that a person must have a severe and prolonged impairment in all three mental functions in order to be eligible for the DTC.

We pointed out that it is unfair to require these functions to be present in combination in order to qualify for the DTC. A person may have severe and prolonged depression, for example, that compromises goal-setting and judgment but not problem-solving.

We also noted that there is no similar conjunctive rule regarding severe and prolonged impairment in physical functions. All the physical functions are treated as entirely distinct entities and entries on Form T2201.

The committee wondered throughout our discussions whether this disproportionately high bar may be a key factor in explaining the high rates of DTC rejection among persons with impairment in mental functions. While we knew intuitively that this rejection rate was a problem, the extent of it subsequently was confirmed by the data provided to us by the CRA. We examine this concern in “DTC Data” in Part 2 of this report.

In Recommendation #10, committee members proposed a possible route to ensure more consistency between the treatment of impairment in physical and mental functions. The proposal refers to the way in which physical functions on Form T2201 are described.

Actions

Both legislative and administrative changes are required to effect this recommendation. Legislative responsibility rests with the Department of Finance Canada rather than the CRA. There has been limited progress on this recommendation from a legislative perspective. While the committee assumes that all of our legislative recommendations regarding eligibility criteria are being assessed as a package, we hope that the modest, but important, change represented by this proposal can proceed on its own.

However, there has been progress on this recommendation from an administrative perspective. The CRA is actually interpreting this clause disjunctively through its administrative practice. Form T2201 appears to acknowledge, via the following note on the form itself, that problem-solving, goal-setting and judgment may be interpreted separately: “A restriction in problem-solving, goal-setting or judgment that markedly restricts adaptive functioning, all or substantially all of the time, would qualify.”

Moreover, the work underway on a redesigned Form T2201, procedural updates and the implementation of a new navigator role, described below, will advance the intent of this recommendation. These actions are discussed throughout this section of the report.

Recommendation #2

That the CRA amend the list of mental functions on Form T2201 as follows:

- attention

- concentration

- memory

- judgment

- perception of reality

- problem-solving

- goal-setting

- regulation of behaviour and emotions

- (for example, mood disturbance or behavioural disorder)

- verbal and non-verbal comprehension

- learning

Background

The list of mental functions used to determine eligibility for the DTC is outlined on Form T2201 (Appendix E). The committee’s first annual report described the many concerns that have been identified with respect to that list. The three major problems with the current criteria are as follows:

First, the current list of mental functions is not considered to be clinically meaningful in many situations. It includes only select mental functions and requires that some impairments occur together when, in fact, they may not (for example, problem-solving, goal-setting and judgment). Because Form T2201 requires that a physician, nurse practitioner or psychologist attests to the nature and impact of an applicant’s impairment, the criteria should reflect actual impairments in mental functions as traditionally and routinely assessed by those providers.

Second, health providers informed us about the challenges they face related to mental functions, in particular, when completing Form T2201. The form does a better job of assessing impairment in physical functions, perhaps because their impacts are easier to observe, quantify and convey (for example, a person who has a complete paraplegia cannot walk) than impairment in psychological or neuropsychological functions. There appears to be an implicit bias against the latter.

Third, there is lack of clarity with respect to the eligibility of persons impaired as a result of some mental disorders. Health providers identified the following conditions as especially problematic: autism, attention deficit and hyperactivity disorder, and post-traumatic stress disorder, due to any of the following:

- the conditions can vary considerably in their expression

- there continues to be an erroneous belief among health providers that some conditions are categorically ineligible

- the form falls short in capturing the breadth and depth of impairment that can result from a mental condition

Actions

The committee discussed this recommendation with officials of the CRA and of the Department of Finance Canada. The committee was asked to provide an internationally recognized list of mental functions in support of this proposed reform.

Because there is no single universally accepted list of mental functions, the DAC provided the lists employed by the World Health Organization (WHO) and the U.S.-based National Institute of Mental Health. In formulating our recommendation, the committee had combined the functions identified on both lists with feedback from the more than 1,000 health providers who had completed our health provider survey in 2019 regarding their experience with Form T2201.

The proposed new list of mental functions represents a blend of international criteria and practitioner feedback and, as such, is an evidence-based taxonomy of mental functions. The committee acknowledges the need to test this revised list with the health providers who complete Form T2201 in the area of mental functions.

The CRA and the committee have endeavoured to do this in 2020 and, in part because of the impact of COVID-19 and the fact that health providers are otherwise occupied, this effort is ongoing. Outstanding issues for health providers working in the area of mental functions include:

- whether each of the functions stands on its own or whether some are composites of others. For example, learning can depend on attention and memory, and attention and concentration may be redundant

- the misunderstandings that exist even among knowledgeable health providers that some conditions don’t qualify or that those people who work despite their conditions are ineligible

- that the breadth and depth of impairments in mental functions are not adequately assessed by the current eligibility criteria on Form T2201 (see Recommendation #4)

Recommendation #3

That the CRA replace on page 5 of Form T2201 the term “effects of the impairment” with the following:

“The effects of the individual’s impairment must restrict their activity (that is, walking, seeing, dressing, feeding, mental functions, eliminating, hearing, speaking or some combination thereof) all or substantially all of the time, even with therapy and the use of appropriate devices and medication.”

Background

Reformulating the definition of mental functions as we proposed in Recommendation #2 is clearly important. However, the committee learned during the course of our work that administrative clarifications would also ease the DTC eligibility application process.

More specifically, the text box on page 5 of Form T2201 asks health providers to describe the effects of the applicant’s impairment. In a survey that the committee conducted last year, health providers informed us that they are confused as to whether they are being asked to assess the actual impairment or to determine its impact on the applicant’s functional capacity. Our recommendation is intended to clarify the information that the CRA is requesting on Form T2201.

Actions

The CRA has incorporated this recommendation into a redesigned paper version of Form T2201, which had been scheduled for release in the spring 2020. The first round of user testing with health providers, individuals and DTC assessors has been completed.

The second iteration of the redesign of Form T2201 was tested in February 2020. Due to COVID-19, however, the process was disrupted and the CRA has not received feedback on the latest testing. The work on the paper version of Form T2201 will resume as soon as possible.

Recommendation #4

That the CRA delete the reference to “social activities” on page 5 of Form T2201 due to the contradiction on page 3 of the form. Page 5 states that one is ineligible on the basis of social and recreational activity, while page 3 states that the inability to initiate and respond to social interactions makes one eligible, as does the inability to engage in common simple transactions.

Background

Form T2201 is confusing to many health providers in that it appears to present contradictory information. One page of the form indicates that a certain set of conditions makes an applicant potentially eligible for the DTC, while another page states that these same activities would make that same person ineligible. Health providers have underscored that social dysfunction is an extremely important feature of some mental disorders (for example, autism), that it can be a profound impairment and that it is not clearly captured in the eligibility criteria for the DTC.

Actions

The CRA has incorporated this recommendation into a redesigned paper version of Form T2201, which was scheduled for release in the spring 2020. The first round of user testing with health providers, individuals and DTC assessors has been completed.

The second iteration of the redesign of Form T2201 was tested in February 2020. As noted in Recommendation #3, the process was disrupted due to COVID-19 and the CRA has not received feedback on the latest testing. The work on the paper version of Form T2201 will resume as soon as possible.

Recommendation #5

That the CRA change the question on page 5 of Form T2201 about the likelihood of improvement to ask health providers whether the individual’s illness or condition that is responsible for the impairment in function, such as walking or cognitive functions, is likely to improve, as in the following example:

“In thinking about the individual’s impairment, please consider whether the condition that causes the impairment (for example, blindness, paraplegia, schizophrenia or bipolar disorder) can be expected to last for a continuous period of at least 12 months.”

Background

In addition to the problems identified in Recommendations #3 and #4, health providers raised a third area of confusion regarding the wording of Form T2201. There is a question on page 5 of the form that asks health providers about the applicant’s likelihood of improvement.

Our proposal builds on the concern raised in Recommendation #4. In response to our survey, health providers told us it is not clear whether the CRA is asking if the applicant’s underlying condition or functional capacity is expected to improve. The committee requested that the CRA clarify the text or reword it entirely in order to explain its meaning.

Actions

The CRA has incorporated this recommendation into a redesigned paper version of Form T2201, which had been scheduled for release in the spring 2020. The first round of user testing with health providers, individuals and DTC assessors has been completed.

The second iteration of the redesign of Form T2201 was tested in February 2020. As mentioned in recommendations #3 and #4, the process was disrupted due to COVID-19 and the CRA has not received feedback on the latest testing. The work on the paper version of Form T2201 will resume as soon as possible.

It should be noted that, in order to reduce the number of clarification letters sent, the CRA has removed the “Effects of impairment” box and replaced it with two questions asking health providers if their patients are either unable to perform the activity or if it takes them an inordinate amount of time to do so. This recommendation was identified during usability testing.

Recommendation #6

That the CRA no longer interpret all or substantially all as 90% of the time and no longer interpret an inordinate amount of time as three times the amount of time it takes a person without the impairment.

Background

In order to qualify for the DTC, the presence of impairment is not sufficient. Rather, the effect of the impairment must be severe and prolonged. In fact, the restriction must be present all or substantially all the time, which has been interpreted by the CRA to mean at least 90% of the time.

During the first year of our mandate, discussions around this recommendation were held with Department of Finance Canada officials who raised two key issues. First, they noted that the Income Tax Act does not specify a minimum percentage of time that impacts must occur in order to qualify for the DTC. They acknowledged that in determining whether the legislated criterion of “all or substantially all of the time” is met, the CRA generally uses a 90% of the time threshold, but that there are other situations in which the legislated criteria may also be met. Second, they noted the policy precedent for this percentage. The 90% guideline is employed in several other contexts, including business and charitable accounts.

Our first annual report documented, however, the many problems with this guideline when applied to the DTC. It acts as a major barrier to DTC eligibility, particularly for persons with impairment in mental functions or other serious conditions which have many symptoms, some or all of which may be episodic.

A person whose memory or perception of reality is impaired even half the time, for example, is seriously and significantly impaired, requiring any combination of supports, remedial treatments and devices, or medication. Moreover, there is no basis in law for the 90% guideline; it is simply administrative practice. In fact, several judgments in Tax Court of Canada cases involving impairment in mental functions as well as the goods and services tax have challenged the use of the 90% guideline.

Actions

As in the case of a number of recommendations that require legislative amendment and that are considered to be particularly complex, the committee seek further consultation on this proposal. We want to identify possible ways in which the current guideline could be replaced by instructions that are both rigorous and able to be assessed by health providers who are not with the applicant 90% of the time.

Recommendation #7

That in the DTC assessment process, the CRA employ the following definition to determine marked restriction in mental functions:

“The individual is considered markedly restricted in mental functions if, even with appropriate therapy, medication and devices (for example, memory and adaptive aids):

- all or substantially all the time, one of the following mental functions is impaired, meaning that there is an absence of a particular function or that the function takes an inordinate amount of time:

- attention

- concentration

- memory

- judgment

- perception of reality

- problem-solving

- goal-setting

- regulation of behaviour and emotions (for example, mood disturbance or behavioural disorder)

- verbal and non-verbal comprehension

- learning

or

- they have an impairment in two or more of the functions listed above, none of which would be considered a marked restriction all or substantially all the time individually but which, when taken together, create a marked restriction in mental functions all or substantially all the time

or

- they have one or more impairments in mental functions which are:

- intermittent and/or

- unpredictable; and

- when present, constitute a marked restriction all or substantially all the time.”

Background

Form T2201 asks health providers whether the applicant is markedly restricted in performing designated activities related to mental functions. The committee made this recommendation in response to concerns raised by many health providers who had identified challenges in interpreting the “marked restriction” criterion. Our proposed new wording is intended to provide some clarification and guidance to health providers as they complete Form T2201.

Actions

The CRA is working to establish a framework that will include the responsibilities of a newly proposed navigator role (see Recommendation #20). The navigators will be answering questions according to the current legislation. If the committee’s Recommendation #7 is implemented as presented, the navigators may be able to use these examples. The CRA will continue to work on this initiative.

The CRA and the committee noted that some physical disorders have intermittent and unpredictable symptoms and that any revision to the treatment of conditions with intermittent symptoms, should apply to both mental and physical disorders.

Recommendation #8

That the CRA remove specific references to activities in the Form T2201 section on mental functions and include examples of activities in Guide RC4064, Disability-Related Information, to help health providers detail all the effects of the markedly restricted mental function(s), as in the following illustration:

“The individual is considered markedly restricted in mental functions if they have an impairment in one or more of the functions all or substantially all of the time or takes an inordinate amount of time to perform the functions, even with appropriate therapy, medication, and devices. The effects of the marked restriction in mental function(s) can include, but are not limited to, the following (this list is illustrative and not exhaustive):

- with impaired memory function, the individual cannot remember basic information or instructions such as address and phone number or recall material of importance and interest

- with impaired perception, the individual cannot accurately interpret or react to their environment

- with impaired learning or problem-solving, the individual cannot follow directions to get from one place to another or cannot manage basic transactions like making change or getting money from a bank

- with impaired comprehension, the individual cannot understand or follow simple requests

- with impaired concentration, the individual cannot accomplish a range of activities necessary to living independently like paying bills or preparing meals

- with impaired ability to regulate mood (for example, depression, anxiety) or behaviour, the individual cannot avoid the risk of harm to self and others or cannot initiate and respond to basic social interactions necessary to carrying out basic activities of everyday life

- with impaired judgment, the individual cannot live independently without support or supervision from others or take medication as prescribed

Background

In our first annual report, the committee noted that Form T2201 asks whether the applicant is markedly restricted in performing designated activities related to mental functions. We believed that it would be helpful for the CRA to include concrete examples of marked restriction in mental functions as guidance for health providers. Rather than make a general recommendation, the committee developed a set of examples to convey our intent.

Actions

The CRA is introducing a digital application of Form T2201 (Recommendation #28) that will include multiple examples for each function currently listed on the form. The content will be tested with selected health providers to ensure both its accuracy and clarity. Fortunately, digital application lends itself to the modification or expansion of materials as required.

Ideally, there would be an avenue at the early stages of this process for health providers to send feedback on the helpfulness of the examples. These comments would allow for clarifications that may be required or the correction of errors or omissions.

The digital application of Form T2201 is being tested in stages. Selected health providers who can certify specific functions are being asked for feedback on how well the digital form identifies the requirements for that function.

Committee members also participated in a demonstration of selected parts of the digital application. The digital format was well received, with committee members noting that it responds to many of the concerns raised in the health provider survey we conducted last year. It will be simpler and faster to complete. The digital application allows for tick boxes rather than long descriptions. It can provide examples and guidance to health providers around specific questions that may have been confusing or open to interpretation.

There are a few technical aspects to work out including, for example, the use of electronic signatures and the ability for health providers to retain a copy of the completed digital form in the individual’s electronic medical record. When the digital application is fully in use, the CRA anticipates that its clarity will reduce the need for clarification letters, which will be of great benefit to applicants (Recommendation #21).

Recommendation #9

That the CRA consider a child and an adult version of Form T2201, with eligibility criteria tailored as necessary.

Background

Several respondents to the health provider survey identified another serious weakness in the DTC eligibility process. The current Form T2201 does not readily apply to children because they typically require assistance with most of the activities of daily living. Respondents to the survey suggested that examples would help health providers distinguish between a disability-related limitation and a developmentally related limitation due solely to age and maturation.

The committee recognized that it would take time to develop a new form for children and that legislative underpinnings would need to be introduced for this reform. In the meantime, we urged the CRA to expand the list of guidelines for health providers to include examples that apply to children. This action would at least respond to the concern we heard that “Clearer guidelines for parents with children with disabilities are a must.” The examples should include behaviours related to autism and developmental disabilities, in particular.

Actions

The CRA indicated that testing of the redesigned Form T2201 will help determine the need for a child-specific version.

In the development of the digital application of Form T2201, the CRA is exploring the possibility of directing respondents to a different set of questions if they indicate upfront that they are completing the form on behalf of a child. The CRA is considering including selected examples of behaviours that would apply to children.

This approach may be preferable to the introduction of an entirely separate form. Several health providers noted that, if there were different forms for children and adults, some applicants might be lost to the system when they are required, upon turning age 18, to transition from one form to another.

Recommendation #10

That the CRA revise the list of functions on Form T2201 to the following:

- vision

- speaking

- hearing

- lower-extremity function (for example, walking)

- upper-extremity function (for example, arm and hand movement)

- eliminating

- eating/feeding

- mental functions

Background

Recommendation #1 noted that the eligibility DTC requirements on Form T2201 set the bar higher for mental functions than they do for physical functions. We called for parity in the treatment of mental and physical functions. In order to respect this parity principle, the committee felt it was necessary to revise the current list of functions on Form T2201 as proposed.

Actions

The CRA has seriously considered this recommendation and identified a few concerns, notably whether the proposed changes might inadvertently give some applicants the understanding that they were no longer eligible. For example, they queried whether some conditions, such as severe cardiopulmonary disorders, would not qualify for the DTC if “extremity function” served to replace dressing.

The committee agreed that this problem can be avoided, provided that “upper and lower extremities” are well defined. For example, a restriction in upper-extremity function can result from a number of underlying conditions, including cardiopulmonary ones. The digital application of Form T2201 discussed in Recommendation #8 may help clarify potential confusion around this concern.

Recommendation #11

That the CRA, in respect of the parity principle, create a list of examples of activities for each impaired function for inclusion in Guide RC4064 to help health providers detail all the effects of markedly restricted function(s), as in the following proposed guidelines (this list is illustrative and not exhaustive):

- with impaired lower-extremity function, the individual cannot walk

- with impaired upper-extremity function, the individual cannot feed or dress themselves, or cannot attend to basic personal hygiene

- with impaired eating/feeding, the individual cannot swallow or eat food

Background

If the CRA follows up on Recommendation #10 and proceeds to modify the list of physical functions, the committee felt that it would be helpful to include a few examples as guidelines for health providers completing Form T2201.

Actions

Should Recommendation #10 proceed, the CRA will follow up on this action, which proposes a change to the list of physical functions on Form T2201. As noted in the discussion on that recommendation, several challenges must be addressed before the CRA can act on its implementation.

It will be essential, for example, to identify any conditions that may no longer qualify for the DTC if the proposed changes in eligibility criteria are adopted. Any clarifications or improvements to these criteria should not jeopardize current or potential DTC eligibility.

Recommendation #12

That the CRA review the current eligibility criteria for hearing, which are out of date.

Background

This issue was brought to the attention of the committee through the health providers survey that we carried out during the first year of our mandate. Respondents who identified this problem gave no details, however, about the specific shortcomings in the current criteria. In making this recommendation, we knew that follow-up work would be required to determine precisely where changes in the eligibility criteria should be made.

Actions

The CRA has made initial contact with the Canadian Hearing Society and the Canadian Society of Audiologists. The work on revised eligibility criteria will continue.

Recommendation #13

That the CRA work in collaboration with the Department of Finance Canada to consult with relevant health providers and stakeholders before introducing any legislative changes to the Income Tax Act with respect to the definition of mental or physical functions.

Background

The Disability Advisory Committee was preceded by the Technical Advisory Committee (TAC) on Tax Measures for Persons with Disabilities, which was appointed in 2004 by the Minister of Finance and the Minister of National Revenue. The TAC’s report, Disability Tax Fairness, proposed that mental functions for DTC eligibility be defined as follows:

- changing “thinking, perceiving and remembering” in the Income Tax Act to “mental functions necessary for everyday life”

- providing for the cumulative effects of restrictions in more than one basic activity of daily living, where the effects are equivalent to a marked restriction in a single basic activity of daily living

The TAC also recommended that the list of mental functions be expanded as it was deemed to be too narrowly defined. Mental functions include memory, problem-solving, judgment, perception, learning, attention, concentration, verbal and non-verbal comprehension and expression, and the regulation of behaviour and emotions. These functions are necessary for activities of everyday life that are required for self-care, health and safety, social skills and simple transactions.

The Income Tax Act subsequently was amended in 2005. Mental functions necessary for everyday life as set out in Form T2201 were changed to all of the following:

- adaptive functioning (for example, abilities related to self-care, health and safety, abilities to initiate and respond to social interactions, and common, simple transactions)

- memory (for example, the ability to remember simple instructions, basic personal information such as name and address, or material of importance and interest)

- problem-solving, goal-setting, and judgment, taken together (for example, the ability to solve problems, set and keep goals, and make the appropriate decisions and judgments)

The committee was unclear as to how the federal government arrived at this interpretation of the TAC recommendations regarding mental functions. The changes that were introduced did not accurately capture the intent of the TAC proposals. We included Recommendation #13 in our first annual report in order to avoid a similar misinterpretation of our proposals.

Actions

The CRA has requested additional information and clarification around these proposed changes. The committee will continue to work on advancing the implementation of this recommendation.

Recommendation #14

That the CRA replace the current eligibility criteria for life-sustaining therapies as set out in Form T2201 with the following:

- Individuals who require life-sustaining therapies (LSTs) are eligible for the DTC because of the time required to administer these therapies. These are therapies that are life-long and continuous, requiring close medical supervision. Without them, the individual could not survive or would face serious life-threatening challenges. Close medical supervision is defined as monitoring or visits, at least several times annually, with a health provider. These therapies include but are not necessarily limited to: intensive insulin therapy for type 1 diabetes; chest therapy for cystic fibrosis; renal dialysis for chronic and permanent renal failure; and medically prescribed formulas and foods for phenylketonuria (PKU).

Background

Applicants are potentially eligible for the DTC if they require life-sustaining therapy. A medical doctor or nurse practitioner must certify that several conditions are met.

An individual must require this therapy in order to support a vital function. This condition applies even if the therapy has eased the symptoms. The applicant must require this life-sustaining therapy at least three times a week and for an average of at least 14 hours per week.

Over the course of our mandate, several concerns regarding the eligibility criteria for life-sustaining therapy were brought to our attention and are documented in our first annual report. Perhaps most important, there are serious questions about the empirical basis for the 14-hour minimum weekly time requirement, in particular.

The 14-hour requirement includes only the time related to the actual therapy. The requirement assumes that people must take time away from their normal everyday activities in order to receive it. The time may also be spent administering life-sustaining therapy to a child.

Actions

This is a complex recommendation that will require significant work over time. The committee will continue to work on its implementation.

It should be noted that after our first annual report was completed, we received a submission from a parent whose child had been diagnosed with a rare disorder known as maple syrup urine disorder (MSUD). The parent requested that this condition be included in a modified Recommendation #14 because of the similarity of this condition to PKU. We agreed with this proposal and have modified the recommendation accordingly. We discuss this proposal in “Selected Conditions and Other Concerns” in Part 2 of this report.

Recommendation #15

That the CRA do the following:

- consider whether some conditions, such as a complete paraplegia or tetraplegia, schizophrenia or a permanent cognitive disorder with a MOCA below 16, should automatically qualify for the DTC in the way that blindness does. (MOCA is a mental status examination of cognitive functions used commonly to assess impairment that results from conditions such as dementia, brain injury or stroke)

- examine the eligibility criteria employed in other federal and provincial/territorial programs, such as the Ontario Disability Support Program and the programs for Canada Pension Plan disability benefits and veterans’ disability pensions to identify the conditions/diagnoses that establish automatic eligibility for those programs

Background

In trying to ease DTC access through improved eligibility criteria, the committee discussed whether it would be helpful to include a statement of condition or diagnosis on Form T2201. While diagnosis alone would not necessarily qualify someone for the DTC, awareness of the presenting condition might assist CRA assessors in making DTC eligibility determinations. There is, of course, the precedent that some conditions, such as blindness and paraplegia, are already categorically eligible on the basis of diagnosis alone.

Our first annual report noted that there is precedent for the inclusion of diagnosis on the eligibility forms of selected programs. The Ontario Disability Support Program (ODSP), for example, identifies a set of prescribed classes in its eligibility criteria. These classes refer to specific categories of people who do not have to go through the disability adjudication process in order to qualify for the ODSP.

At the same time, we acknowledged the challenges with this approach. A certain diagnosis does not necessarily mean serious impairment in function. In many cases, it is neither appropriate nor factually correct to equate the two. But there may be some conditions, such as paraplegia or dementia, whose effects are more clearly evident and predictably stable.

Finally, we acknowledged that a designated list in any area of public policy invariably raises questions of fairness about the groups, items or conditions that have been left out. On balance, however, committee members believe that the merits of this recommendation outweigh its potential weaknesses.

Actions

This is a complex recommendation that will require significant work over time. The committee will continue to work on its implementation.

In the meantime, the CRA is researching federal and provincial/territorial programs for automatic eligibility and expedited processing. Obvious conditions will be included in the digital application and the ongoing testing process will provide important guidance. The CRA has also added an area under each functional category, such as vision and walking, to capture a diagnosis on the new paper version of Form T2201.

Recommendation #16

That the CRA examine the new eligibility form being used for Canada Pension Plan disability benefits to identify areas in which there might be synergies regarding eligibility for the DTC, such as including the presenting condition or diagnosis as supplementary information identifying functional limitations.

Background

The committee made this proposal in order to provide additional relevant information when CRA officials assess for DTC eligibility. We recognize, however, that the presence of a certain diagnosis does not automatically equate with impairment.

Actions

CRA officials are in the process of examining the application form currently being used for Canada Pension Plan disability benefits. The CRA is proceeding cautiously on this proposal because DTC eligibility is based on impairment in function rather than presence of a specific condition (other than blindness). A single diagnosis does not always result in severe or prolonged impairment in physical or mental function.

It should be noted that the CRA may decide to use diagnoses in the two areas around which the committee has made specific proposals, notably Recommendation #14 on life-sustaining therapies and Recommendation #15 on the recognition of designated conditions. The digital application of Form T2201 also adds a question about diagnosis.

Recommendation #17

That the CRA test or pilot various approaches that would remove the gatekeeper role from health providers. One such approach would be for community tax clinics to take on a screening or advisory function. Another would be to establish a CRA call centre explicitly for this function.

Background

Health providers made clear to the committee in both their responses to the health provider survey and in committee submissions their concern that they have effectively become the gatekeepers to the DTC.

In addition to the cost and time burden associated with this role, it can inadvertently jeopardize the client/health provider relationship if the provider has an incomplete understanding of who is and isn’t eligible, and completes a form for someone who is not eligible or fails to complete a form for someone who is.

Further, the effects of the impairment upon which they are asked for their judgment may not be the ones they can observe directly. For example, health providers do not spend all or substantially all of the time with their patients to witness the functional impacts of their medical conditions.

Actions

The CRA has introduced several measures to implement this recommendation. The CRA is working to establish a framework that will include the responsibilities of a newly proposed navigator role (see Recommendation #20).

The CRA continues to support its Community Volunteer Income Tax Program, discussed in Recommendation #31. In fact, the investment in this program has increased in order to expand its reach, particularly among organizations serving Indigenous peoples and organizations representing persons with impairment in mental functions. The CRA recognizes that these two populations would benefit greatly from additional tax assistance.

An enhanced phone line has been introduced for call centre agents to consult directly with a DTC unit assessor for answers to more complex questions related to the DTC that they are unable to resolve. These complex questions typically relate to DTC eligibility criteria, impairment in mental functions, applications on behalf of a dependant, and DTC appeals. Generally, the call centre agent is able to obtain and relay an immediate answer to the taxpayer’s query. However, if the taxpayer’s query is not resolved by the call centre agent, an assessor in the DTC unit will either speak to the taxpayer at the time or the taxpayer will receive a callback within two business days.

Recommendation #18

That the client experience survey on the DTC and other disability tax measures to be carried out by the CRA include a question as to whether the individual or recipient had any difficulty accessing a health provider for the purposes of completing Form T2201 and, if so, for which activity. Clients should also be invited to provide any additional comments on this question. Special attention should be paid in this survey to the needs and concerns of Indigenous Canadians.

Background

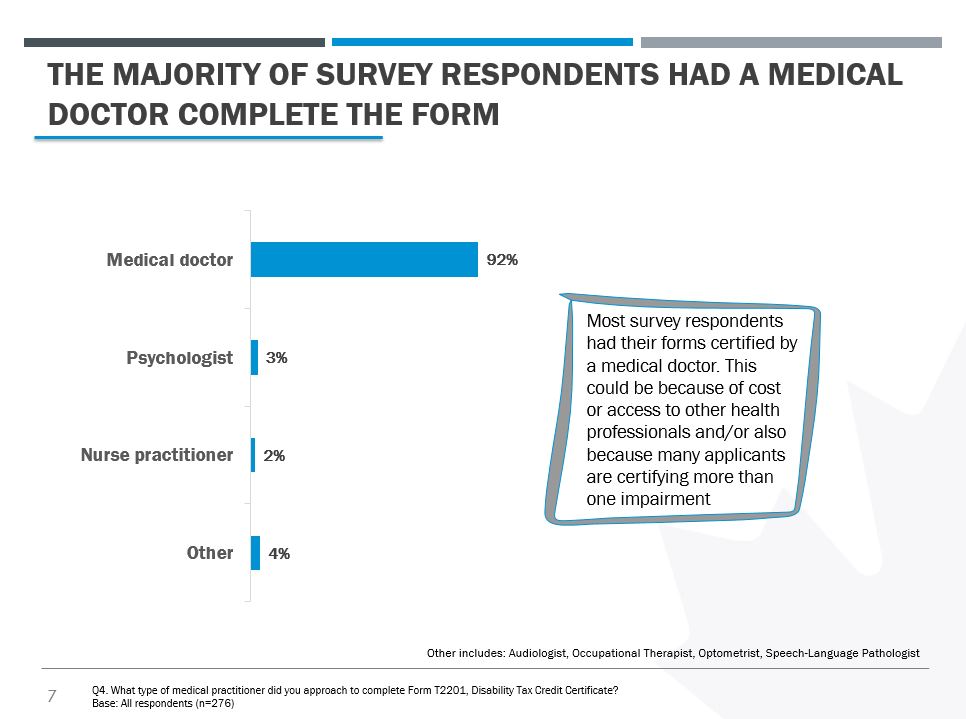

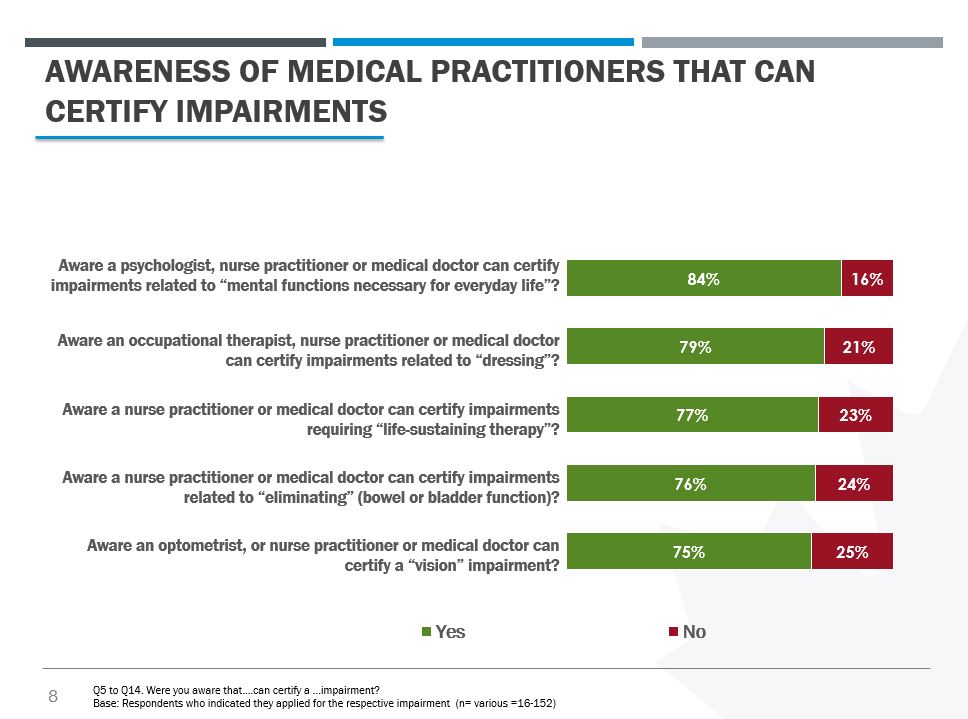

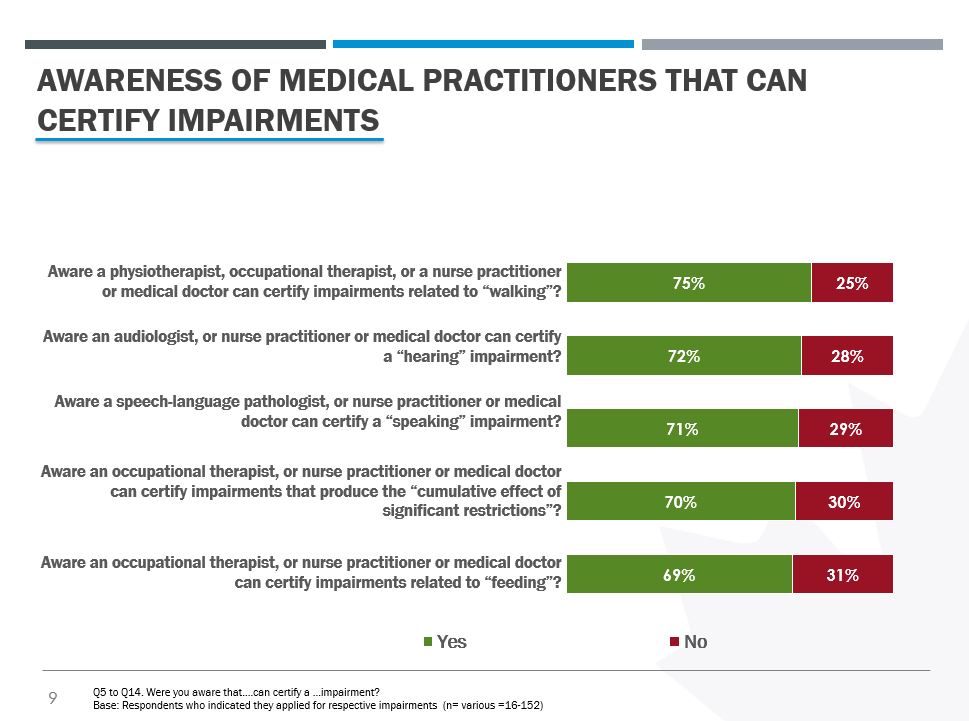

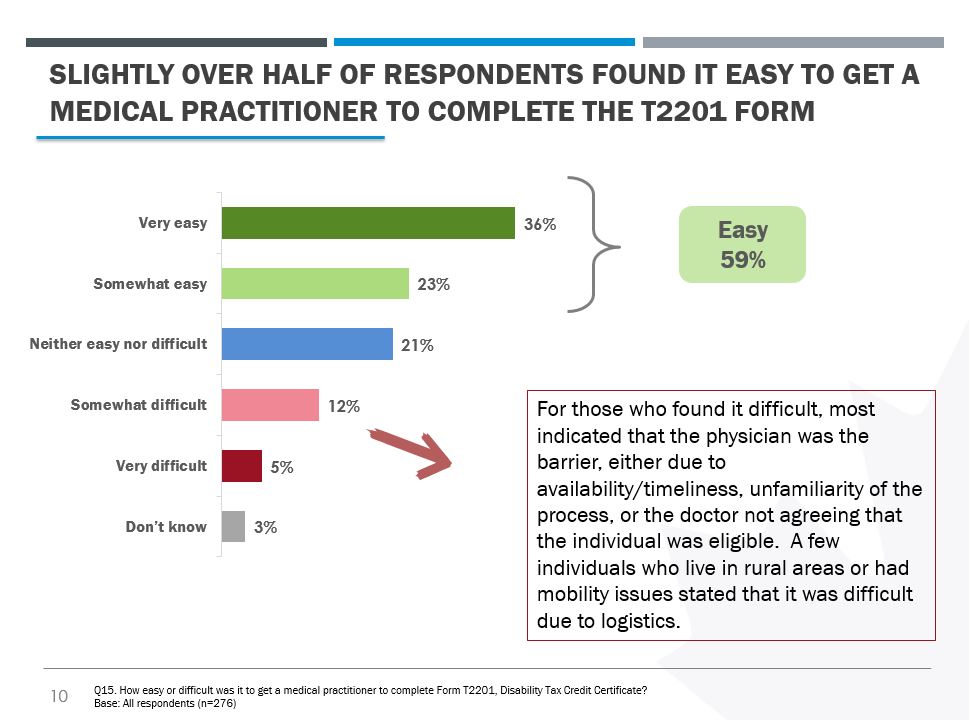

In the first year of our mandate, the committee heard from several organizations that proposed expanding the list of health providers approved to complete Form T2201.

While the committee appreciates the need to ensure access to health providers, we felt that we did not have sufficient information about the nature and extent of the problem. We also questioned whether access to specialized health providers, such as chiropractors or ostomy nurses, was a serious concern for Canadians and whether DTC recipients would have requested some of the proposed changes.

Actions

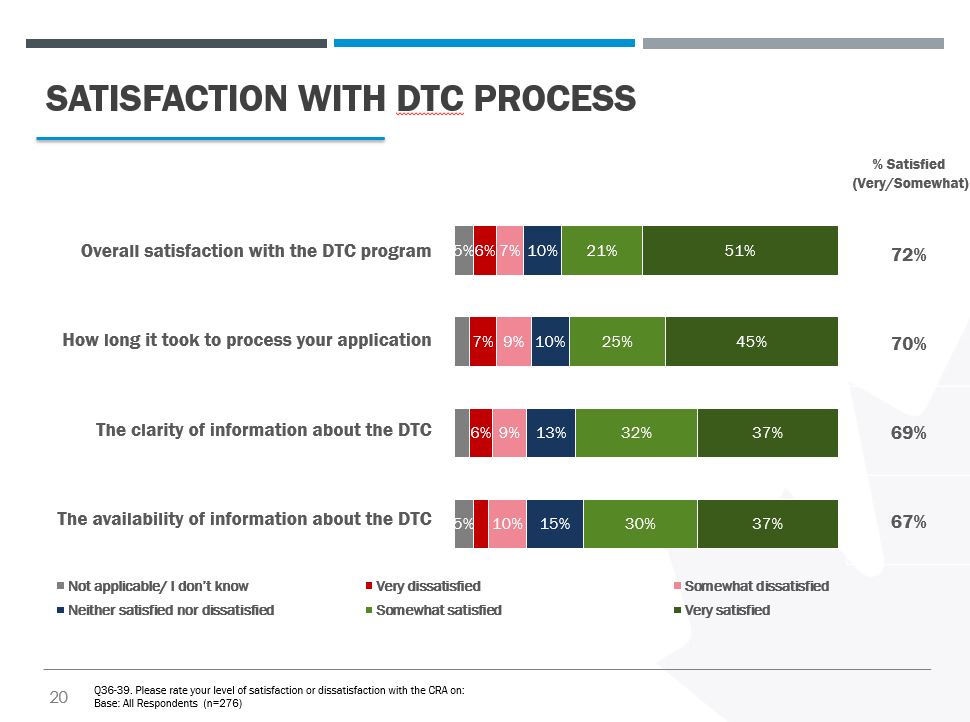

In order to determine whether DTC recipients themselves felt a need for an expanded list as proposed, the committee asked the CRA to include a question in its client experience survey about access to health providers. We wanted to know more about the access problems that DTC recipients actually face.

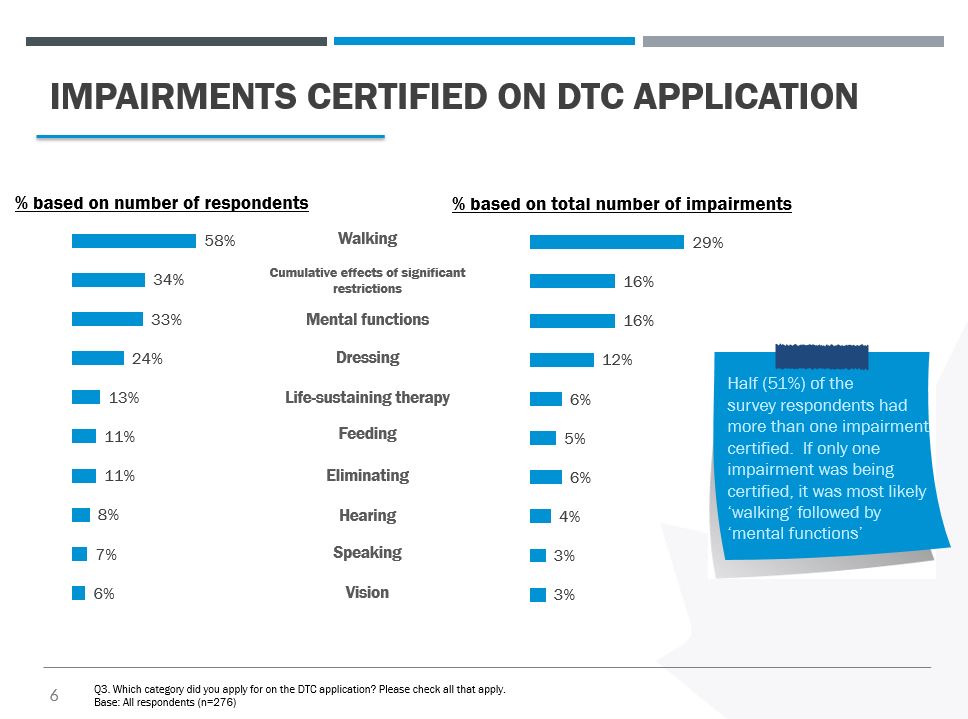

The CRA modified the questions in the client experience survey, based on input from committee members. The survey went live in April 2020. The results of the survey are attached as Appendix F.

Recommendation #19

That the CRA develop a process for expanding the list of health providers with the appropriate expertise who can assess eligibility for the DTC.

Background

Committee members recognized that the CRA likely would receive requests on an ongoing basis to update and expand the list of health providers who can assess for DTC eligibility. We had therefore proposed that data be gathered in order to substantiate the need for an expanded list, as the committee was not clear as to whether clients faced challenges in getting access to qualified health providers. We also suggested the development of principles to guide any expansion in future.

Actions

The CRA is currently considering possible actions with respect to this recommendation. Its first step is to gather information from DTC recipients, as proposed in Recommendation #18, to determine the extent of the problem. The committee agreed that potential expansion of the list would be explored if results from the client experience survey, discussed in Recommendation #18, indicated a need to do so.

Committee members also had a preliminary discussion about key principles that should guide any additions to the health provider list of assessors. For example, the profession must be governed by a recognized regulatory body.

Another possible principle would be that the designated health provider can assess only for the specific function or functions related to their training. For instance, if ostomy nurses are added to the list as requested (Recommendation #18), they would be permitted to certify only for eliminating (bowel or bladder functions) and not for any other impairment in physical or mental functions.

Recommendation #20

That in the case of determining DTC eligibility for persons with impairment in mental functions, the CRA include relevant specialized health providers, including, but not limited to, psychiatrists and psychologists, in the review process when applications are disallowed.

Background

Most of the problems related to DTC eligibility have arisen around impairment in mental functions. Challenges regarding the definition of mental functions were discussed in Recommendations #1 to #16 and are documented at length in our first annual report.

As a result of these wide-ranging concerns, the committee proposed that the CRA carry out a second-level internal review on all rejected DTC applications when a duly-completed Form T2201 and all associated supporting documentation have been submitted.

Committee members made this recommendation in recognition of the fact that CRA assessors typically face complex conditions. We believe that this proposal to include qualified mental health providers as advisors would both enable access to the DTC where appropriate and reduce the need for objecting to and even appealing decisions to disallow eligibility. Formal appeals through the Tax Court of Canada can be a long, costly and stressful process that should be avoided if possible.

Actions

The CRA has acted on this recommendation though not in the precise way the committee proposed. All applications denied the DTC involving impairment in mental functions are sent for secondary review by a CRA team not involved in the initial decision. The CRA will also provide better and more consistent training to current and new assessors of DTC cases that involve an impairment in mental functions.

The CRA has committed to consulting with mental health professionals around selected cases.

In addition, DTC assessors now have access to the guidelines in the document “Mental functions necessary for everyday life.” The guidelines permit greater flexibility in the interpretation of “all or substantially all of the time” by noting that the effects of the impairment must be present and challenging “most of the time” rather than the arbitrary 90% rule.

Different components of Recommendation #20 can be found under various CRA initiatives, such as implementing a new navigator role and strengthening the tools and procedures available to DTC assessors. The navigator role was the result of discussions from the committee’s June 2019 meeting.

While navigators will help streamline the application process and provide co-ordination between the CRA and applicants, their role does not yet include consulting with outside sources on denial of applications from persons with impairment in mental functions. Based on committee feedback, the CRA is currently revising the framework, roles and responsibilities of this new position.

Recommendation #21

That the CRA:

- copy to the applicant all clarification letters sent to the health provider

- let the health provider know that all communication to a health provider about an applicant will be copied to the applicant and that any communication the health provider submits to CRA will also be made available to the applicant

- encourage the health provider to contact and consult the applicant, as necessary, when providing any clarification to the CRA

- extend the time for a health provider to file a clarification letter with the CRA from 45 to 60 days, and note this timeline on the first page of the questionnaire

Background

The committee’s first annual report identified a number of problems with the clarification letters used by the CRA to request additional information regarding Form T2201 completed on behalf of an applicant. Health providers flagged their concern about the apparent increase in recent years in the frequency of clarification letters.

The CRA often asks health providers for additional information about a particular applicant even after they send substantial documentation in the initial application. Some health providers noted that Form T2201, which originally had been rejected, subsequently was approved after precisely the same information was submitted to the CRA a second time.

Others pointed out the difficulty in responding to these clarification letters. The questions on the letters generally are considered too broad and not always relevant to a specific disability.

Actions

As part of its quality review, the CRA is in the process of implementing all the components of this recommendation. It is working to provide more information, guidelines and examples earlier in the application process in order to reduce the need for clarification letters.

The discussion on the development of the digital Form T2201 noted that the application process itself will be made easier. Tick boxes will replace the need to provide long descriptions. Multiple examples will be included at several points in the form as guidance for health providers. The CRA has indicated that it currently:

- informs the health provider that all communication to a health provider about an applicant will be copied to the applicant and that any communication the health provider submits to the CRA will also be made available to the applicant

- encourages the health provider to contact and consult the applicant as necessary when providing any clarification to the CRA

- gives the health provider 60 days to respond to a clarification letter. The letter indicates that while the health provider has 45 days to respond, the case is not closed until 60 days have passed. This practice is intended to reduce processing times and associated delays

The CRA will not be copying the applicant on clarification letters sent to health providers as has been done in the past. However, in order to capture the essence of the recommendation, the CRA has added information to the delay letter sent to the applicant, indicating that their health provider has 45 days to reply to the CRA’s clarification letter.

Recommendation #22

That the CRA:

- provide in notice of determination letters a relevant reason as to why a DTC application was denied

- include in notice of determination letters a copy of the clarification letter and the health provider’s clarification response. This information is vital in case of an appeal

- move the consumer survey request to the bottom of the notice of determination letters

Background

In our first annual report, the committee identified problems with respect to the clarification letters that the CRA sends to health providers to complete on behalf of identified applicants (Recommendation #21). We also noted several problems related to the notice of determination letters that the CRA issues to communicate its decision regarding a given application.

A notice of determination letter does not always provide a reason for not allowing the DTC. Rather, it relies on pre-written clauses it calls “verses” that may have limited relevance to the application. The committee has questioned whether these verses are appropriate guidelines and whether they need to be modified and updated.

The current practice creates difficulties as well for applicants who may want to appeal a decision because they often receive no information regarding the rejection of their application. Disability Advisory Committee members also felt that it was inappropriate to include a consumer experience survey immediately following the statement turning down a DTC application.

Actions

The CRA is drafting verses and accompanying procedures to improve the denial letters. The CRA Appeals Branch has provided proposed wording for the CRA Assessment, Benefit, and Service Branch to include in DTC denial letters to ensure that applicants are informed of their recourse options. This issue is discussed in “Review of DTC Decisions” in Part 2 of this report.

The new client experience survey went live in April 2020. The request to complete the survey will appear at the bottom of the notice of determination. The results of the survey are attached as Appendix F.

Recommendation #23

That the Minister of National Revenue review the current appeals process with a view to creating a straightforward, transparent and informed process where the applicant has access to all relevant information (including the precise reason their application was denied) and documents (including copies of all information submitted by health providers that pertain to their application).

Background

Applicants deemed ineligible for the DTC can challenge that determination through case review, a notice of objection and a notice of appeal. These steps are described in “Review of DTC Decisions” in Part 2 of this report.

Actions

The CRA is taking steps to improve the quality of information provided at both the pre-application and the application stages of eligibility. The CRA is in the process of introducing a navigator function to help individuals presenting complex circumstances work their way through the eligibility process (see Recommendation #20). The digital application of Form T2201 currently in development will respond to many of the problems that health providers identified in the original Form T2201.

The CRA Appeals Branch has taken a number of steps to ensure that DTC determinations are consistent with CRA policy. For example, it has centralized the DTC objections workload for both eligibility and entitlement to four centres of expertise (COEs), with a recent updating of branch procedures to ensure that all DTC objections are forwarded to a COE. It has formed a working group within the COEs to ensure that the objections program has the required support to process increasingly complex DTC files with a consistent approach. Additional improvements are summarized in “Review of DTC Decisions” in Part 2 of this report.

Recommendation #24

That the CRA include a document (one- page, two-sided information sheet) entitled “Your Rights When a Notice of Determination Denies a Claim for the DTC” that would:

- explain the requirements, timelines and details for filing the following:

- review

- notice of objection with the Appeals Branch

- notice of appeal with the Tax Court of Canada

- inform taxpayers that other persons (that is, family members, friends or professional advisors) can act on their behalf by submitting Form T1013, Authorizing or Cancelling a Representative, or writing a letter

- inform taxpayers that they have access to all documents in their files, including a copy of the follow-up questionnaire and any clarification letter completed by the health provider

- inform taxpayers that they can contact the CRA for a copy of Pamphlet P148, Resolving your dispute: Objection and appeal rights under the Income Tax Act, if they do not have access to the Internet

- provide the correct contact information and mailing addresses for the submission of any required materials

Actions

The CRA is taking steps to ensure that DTC applicants know they can submit, at any time, additional material or clarifications with respect to their case. As discussed in Recommendation #22, it will also include in notice of determination letters any relevant information that DTC applicants may require if they choose to object to or appeal a CRA determination.

In response to our recommendation, the Appeals Branch has prepared suggested wording for the notice of determination. The Appeals Branch has also prepared a decision tree to help applicants understand the process of challenging a DTC determination as well as three videos that explain the process involved in launching a challenge. Details and links are provided in “Review of DTC Decisions” in Part 2 of this report.

Recommendation #25

That the CRA consult on a regular basis with selected community organizations to:

- ensure that all its communications and materials (including letters of correspondence with individuals) are easily accessible by persons with disabilities and are available in plain language. Organizations such as People First can assist with ensuring plain language

- determine whether its communications and materials are keeping pace with technological change and with the technologies in common use by communities of persons with disabilities

Background

The committee pointed out in our first annual report that most Canadians are unaware of the various tax provisions from which they can benefit. Moreover, many tax measures are hard to understand. The DTC, in particular, is especially complex because of its complicated eligibility criteria and onerous application process.

We also wanted to ensure that the CRA is using the most up-to-date, disability-related communications technology. At the same time, we recognize that some individuals still use older technologies because they do not have the financial means to upgrade or replace existing communications equipment or they live in rural or remote areas where these upgrades may not be available.

Actions

The CRA has consulted with communications advisors in the Public Affairs Branch and CRA field agents on this recommendation. The Outreach Program and Community Volunteer Income Tax Program continue to work with communications advisors in the Public Affairs Branch to ensure that all materials are reviewed for plain language and are accessible. Outreach field agents are working with individuals claiming the DTC and disability community organizations to solicit feedback on DTC-related material. Comments on CRA products and services are welcome during all outreach events.

It should be noted that the committee received a letter from an individual who had encountered challenges associated with hearing technologies when trying to communicate with the CRA. The committee hopes that the CRA will increase the technological options available to individuals with significant auditory impairments who face unreasonable barriers in accessing the current tools, such as teletypewriter and My Business Account. The CRA has indicated its interest in addressing this issue.

Recommendation #26

That CRA web content, which outlines disability tax measures, link to relevant provincial and territorial websites that identify disability-related provisions in those jurisdictions, as well as the range of federal and provincial/territorial disability measures that require DTC eligibility in order to qualify.

Background

In the first year of our mandate, the committee heard from organizations representing persons with disabilities about possible ways of enabling navigation through the complex webs of disability-related programs and services throughout the country. La Confédération des organismes de personnes handicapées (COPHAN) du Québec had suggested, for example, that the CRA web content follow Quebec’s lead in making links to related disability programs and supports in other provinces and the territories.

Actions

The DTC-related web pages were to be reviewed in spring/summer 2020 as part of the web optimization project, led by the CRA’s Public Affairs Branch. Unfortunately, the DTC content optimization project was temporarily put on hold due to COVID-19.

The purpose of the project was to improve user experience. It was intended to ensure that Canadians spend less time looking for DTC answers on the Canada.ca website and be better able to complete DTC tasks on that site. By making it easier for individuals to find and understand answers to their most frequent DTC questions, the project would:

- improve Canadians’ understanding of whether or not they are eligible for DTC and how to apply

- increase the number of correctly completed and submitted applications

- reduce low-complexity DTC-related enquiries to the call centre, allowing CRA staff to deal more with high-complexity calls

- bring the needs and expectations of Canadians into the design of the optimized web pages

The optimization project is in its early stages and the DAC secretariat has notified the project team of the related committee about Recommendations #25 and #26. The DAC secretariat will be involved in the progress of the project and has suggested that the committee also be engaged, where appropriate.

Recommendation #27

That the CRA provide and make publicly available relevant data on the DTC, including number of applications, approvals, rejections, and appeals; durations of eligibility by function; and a demographic profile of current beneficiaries by age and gender.

Background

For the better part of a year, the committee had requested that the CRA provide data on disability tax measures and the DTC, in particular. We felt that it was essential, at the very least, to have basic information on the actual and potential DTC caseload. We believed that it would be important to know more about DTC applicants in terms of their age, gender and geographic region as well as the impairment in functions(s) for which they were applying.

The purpose of requesting this detailed data was to understand the ratio of successful cases (the actual caseload) to all applications (the potential caseload). The data would be informative for comparative purposes.

We would find out, for example, if there is an imbalance with respect to applications for certain functions, which would then raise questions for further exploration. For example, we know through feedback from disability organizations and health providers that applicants with impairment in mental functions face serious challenges. Empirical data would help determine the extent of this problem.

A serious underrepresentation of applications for certain conditions could point to weaknesses in the approval process. It could also reflect the challenges that health providers face in trying to complete certain sections of Form T2201.

Actions

In May 2019, the CRA publicly released a set of DTC statistics. It subsequently prepared a November 2019 update based on committee comments. We were very pleased to receive this information and to note that it has also been made available to the public. In fact, we examined the data in some depth in order to identify any concerns or determine any policy directions that might derive from this information. Our findings are presented in “DTC Data” in Part 2 of this report.

Recommendation #28

That the CRA provide an option for the electronic submission of Form T2201 and related materials that:

- is convenient and accessible for both taxpayers and tax preparers

- permits submission of those materials at the same time as, or after, the filing of an income tax and benefit return

Background

Tax preparers and other organizations had proposed to the committee and to the CRA that DTC applicants be permitted to file online their Form T2201 and associated materials. This process would make it easier for many individuals to apply for the DTC. In fact, most government transactions are now being carried out through electronic submission.

Actions

The CRA fully supports this proposal and, as noted in Recommendation #8, is in the process of developing a digital application of Form T2201. It will be able to address many of the concerns that health providers raised with respect to the current form.

The digital application will allow for health providers to mark tick boxes rather than provide descriptive responses. The application process will be clearer and more consistent for health providers. A digital application will enable the inclusion of detailed examples, as the committee proposed in Recommendation #8.

A digital form also makes it easier for the CRA to update content as required. For instance, the committee or the CRA may learn that the wording of a certain example appears to be confusing or that an example pertaining to a specific condition should be added.