Learn about your taxes

Completing a basic tax return

An introduction to a basic income tax and benefit return. What you need to report, how to claim deductions and tax credits, and finding out whether you will get a refund or owe tax.

Basics of a tax return – lesson completed

The 6 steps for all tax returns, and how to file electronically.

Time to complete: about 8 minutes

This lesson includes

-

4 sections

- 1 question to test yourself

- 1 video (2 minutes:35 seconds)

Basics of a tax return (part 1 of 4)

Filling out your tax return

There are 6 steps to completing your income tax and benefit return. These steps are the same for simple tax situations and complex ones. Knowing the basic steps and seeing how they connect will help you do your taxes, whether you use a paper return or file electronically using certified tax software.

Income tax and benefit return

- Income tax and benefit return

If you do your taxes electronically, please note that the certified tax software you use may not show all the individual steps. The software calculates continuously as you enter more information.

Video series

The one about doing your taxes

Learn all about the basics of a tax return

Providing your personal information – lesson completed

What kind of personal information do you need to provide, and why it's important for the information with the CRA to be accurate and up-to-date.

Time to complete: about 9 minutes

This lesson includes

-

8 sections

- Why provide information about yourself: Start this lesson

- Providing your name, address and social insurance number

- Providing your date of birth, language of correspondence and email address

- Providing your province or territory of residence

- Providing your marital status

- Registering with Elections Canada

- Other questions you may need to answer

- Entering personal information on your tax return

- 1 question to test yourself

Providing your personal information (part 8 of 8)

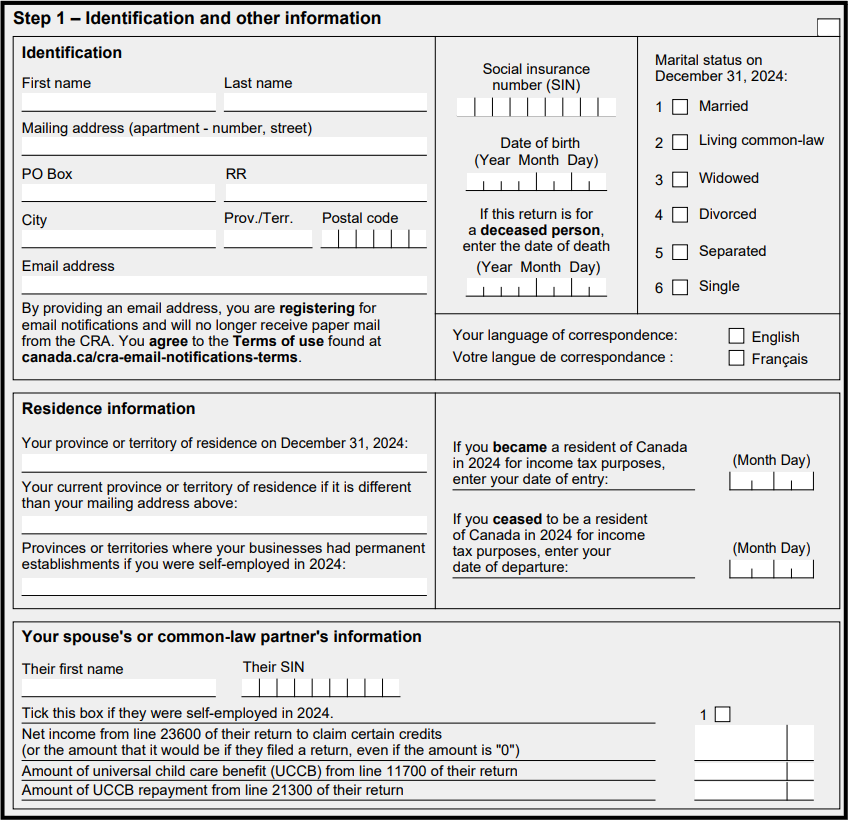

Entering personal information on your tax return

If you are using certified tax software, you enter your personal information at the start of the process. Based on the responses you provide, the software determines if more information is required before moving to the next step. The software may also use the information you provide in this section to determine if you are eligible for certain tax credits or if other forms need to be completed.

Example: How your personal information can determine eligibility

While doing her taxes using certified tax software, Ruman indicated she is married and a resident of Ontario. Her marital status prompted the software to ask her for her spouse’s SIN and net income. Her province of residence prompted the software to ask additional questions related to Form ON-BEN, Application for the Ontario Trillium Benefit, and Ontario Senior Homeowners’ Property Tax Grant, because this form applies only to residents of Ontario.

Below is an example of what the identification and other information page looks like on the tax return:

Example

Is this form hard to read? Don't worry, we will provide you with a link to the PDF (hi-res) version after this lesson.

Resources are available

After you finish this lesson, this resource link will be available:

- Get a T1 income tax package

Reporting your income

What income and information slips are, and how to report your income on your tax return.

Time to complete: about 14 minutes

This lesson includes

Reporting your income (part 7 of 8)

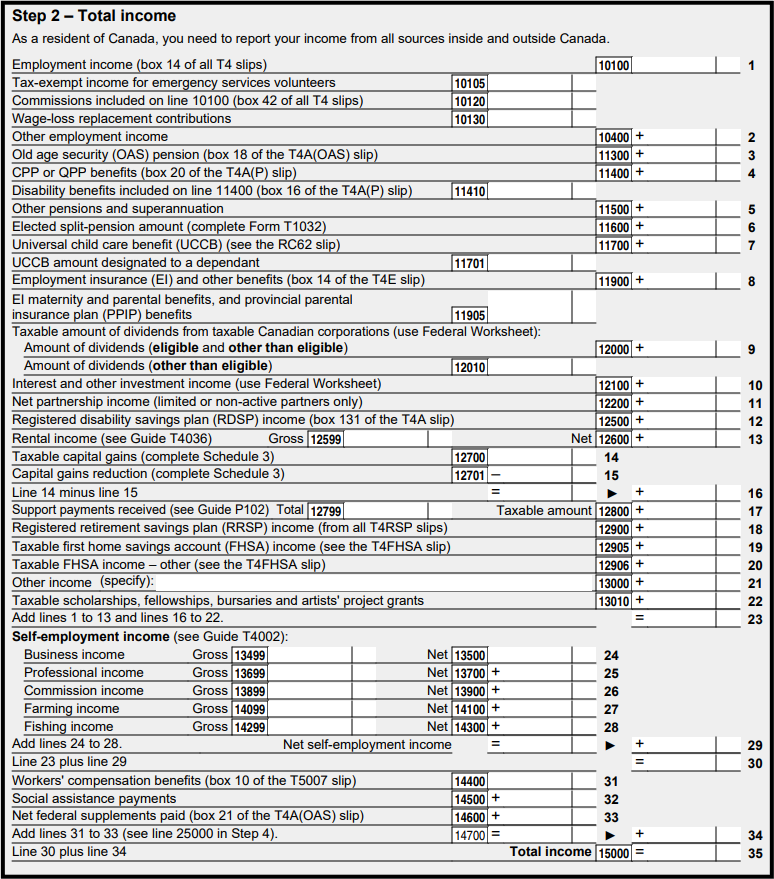

Entering income on your tax return

Before doing your taxes, you must gather all available information about your income. This includes all of your information slips, as well as details about any income not reported on a slip, such as occasional earnings.

If you did not receive a slip in time to do your taxes, talk to the issuer before contacting the CRA. You can also access your slips in My Account. If you cannot get a copy of your slip, you can estimate your income using your paystubs or other financial statements.

Example: Income earned as cash

Paola worked at a restaurant as a server and received a T4 slip showing $8,000 of employment income in box 14. Paola’s employer did not track cash tips, so these were not reported on Paola’s paystubs or T4 slip. However, Paola kept a record of what tips she received and knows the total amount was $1,000 for the year. When Paola did her taxes, she entered the amounts in the boxes on her T4 slip and the information about her tips into the certified tax software.

Certain boxes are for reference purposes only and the amounts they contain do not need to be reported on the tax return, as these amounts are already included in another amount. As in the example of a T4 slip, box 14 already includes amounts shown in other boxes, such as box 30, 32, 34 and 40. You can view the back of a T4 slip to see all the income that you do not report on your tax return.

Test yourself

Below is an example of the total income calculation page of the tax return:

Example

Is this form hard to read? Don't worry, we will provide you with a link to the PDF (hi-res) version after this lesson.

Resources are available

After you finish this lesson, these resource links will be available:

- T4, Statement of Remuneration Paid (slip)

- Get a T1 income tax package

- Contact the Canada Revenue Agency (CRA)

- Infographic - Income sources

Claiming your deductions

What deductions are, where they come from, and how to enter them on your tax return.

Time to complete: about 10 minutes

This lesson includes

-

4 sections

- 3 questions to test yourself

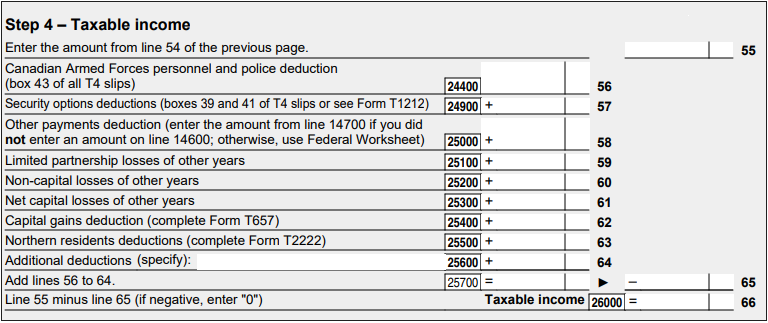

Claiming your deductions (part 4 of 4)

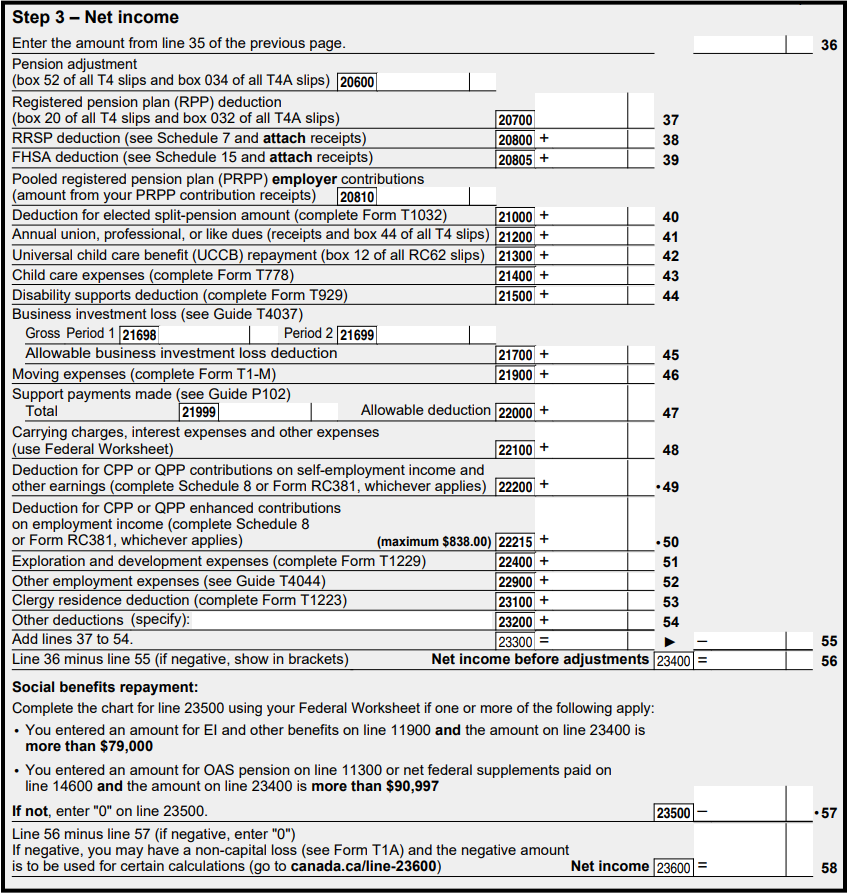

Entering deductions on your tax return

If you are using certified tax software, the software may use information you entered earlier and ask you questions to determine which deductions you may be able to claim. For example, if you indicated that you have a child, the software may ask you questions about your child care expenses.

Once you have entered all information applicable to your tax situation, the certified tax software will calculate all the deductions applicable to you. It will automatically calculate your net income and your taxable income by subtracting your deductions from your total income.

It is your responsibility to make sure that you review the information you have entered into the certified tax software before you submit your tax return to the CRA. For example, if you claimed child care expenses, check that this deduction is displayed on the appropriate line number.

Below is an example the net income and taxable income calculation pages of the tax return:

Example

Is this form hard to read? Don't worry, we will provide you with a link to the PDF (hi-res) version after this lesson.

Is this form hard to read? Don't worry, we will provide you with a link to the PDF (hi-res) version after this lesson.

Resources are available

After you finish this lesson, this resource link will be available:

- Get a T1 income tax package

Claiming your non-refundable tax credits

What non-refundable tax credits are, and how they can help lower the amount of taxes you may owe.

Time to complete: about 13 minutes

This lesson includes

-

6 sections

- 3 questions to test yourself

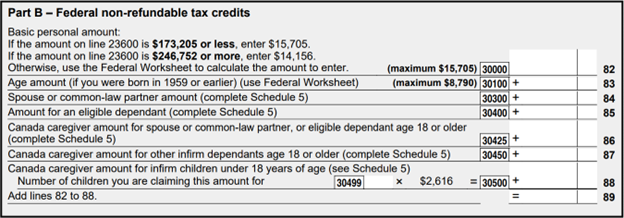

Claiming your non-refundable tax credits (part 6 of 6)

Claiming non-refundable tax credits on your tax return

If you are using certified tax software, the software may use information you entered earlier in the process and ask you questions to determine which non-refundable tax credits you may be able to claim.

The software will do all the calculations for you on the tax return and on any necessary forms.

It is your responsibility to make sure that you review the information you have entered into the certified tax software before you submit your tax return to the CRA.

Below is an example of what the calculation of your federal non‑refundable tax credits looks like on the tax return:

Example

Is this form hard to read? Don't worry, we will provide you with a link to the PDF (hi-res) version after this lesson.

Is this form hard to read? Don't worry, we will provide you with a link to the PDF (hi-res) version after this lesson.

Resources are available

After you finish this lesson, this resource link will be available:

- Get a T1 income tax package

Calculating your taxes

Calculating the federal and provincial or territorial taxes you might owe.

Time to complete: about 12 minutes

This lesson includes

-

7 sections

- How tax is calculated: Start this lesson

- Determining the amount of federal tax on your taxable income

- Example of calculating tax in the first tax bracket

- Example of calculating tax in the third tax bracket

- Calculating your net federal tax

- Calculating your provincial or territorial tax

- Entering tax calculations on your tax return

- 3 questions to test yourself

- 1 video (3 minutes:15 seconds)

Calculating your taxes (part 2 of 7)

Determining the amount of federal tax on your taxable income

Canada has a progressive income tax system, which means you pay more tax as your income increases.

The taxes you pay are determined by which of the 5 tax brackets your income falls into. A different tax rate applies to each tax bracket but only to the income within that bracket. The higher tax rate does not apply to all your taxable income. The same tax brackets are used for all types of income, such as employment income or occasional earnings.

Tax brackets

- Tax brackets

Video series

The one about tax rates

Learn all about tax rates and tax brackets.

Test yourself

The federal income tax rates apply to all provinces and territories.

Current federal tax rates and income tax brackets

Calculating your taxes (part 3 of 7)

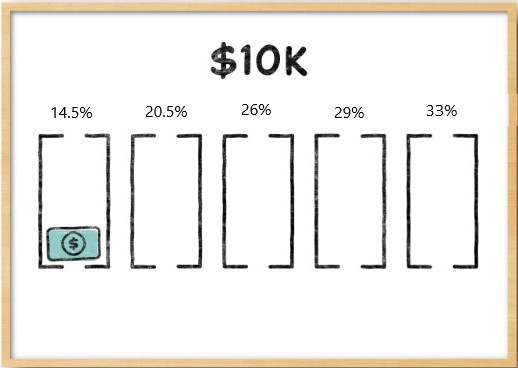

Example of calculating tax in the first tax bracket

This example uses the federal tax rates for 2025.

- 14.5% on the first $57,375 of taxable income, plus

- 20.5% on the next $57,375 of taxable income (on the portion of taxable income over $57,375 up to $114,750), plus

- 26% on the next $63,132 of taxable income (on the portion of taxable income over $114,750 up to $177,882), plus

- 29% on the next $75,532 of taxable income (on the portion of taxable income over $177,882, up to $253,414), plus

- 33% of taxable income over $253,414

Giovanni’s taxable income was $10,000. Because he made less than $57,375, his income falls into the first tax bracket. The 2025 tax rate for this bracket is 14.5%.

Note: The tax brackets are not to scale. The tax rates are updated every year.

When Giovanni does his taxes, the federal taxes he owes on his income are calculated like this:

- Giovanni is taxed at 14.5% rate on his income of $10,000

- 14.5% ltmuiplied by $10,000 =equals $1,450

Calculating taxes on your taxable income is only the first step. Don't worry, you will apply your non-refundable tax credits and refundable tax credits later in the process, which will reduce this amount.

Refundable tax credits

- Refundable tax credits

Calculating your taxes (part 4 of 7)

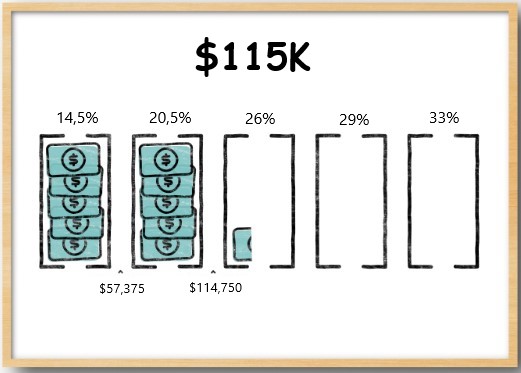

Example of calculating tax in the third tax bracket

This example uses the federal tax rates for 2025.

- 14.5% on the first $57,375 of taxable income, plus

- 20.5% on the next $57,375 of taxable income (on the portion of taxable income over $57,375 up to $114,750), plus

- 26% on the next $63,132 of taxable income (on the portion of taxable income over $114,750 up to $177,882), plus

- 29% on the next $75,382 of taxable income (on the portion of taxable income over $177,882 up to $253,414), plus

- 33% of taxable income over $253,414

Maria’s taxable income was $115,000. Because she made between $114,750 to $177,882, her income falls into the third tax bracket. The 2025 tax rate for this bracket is 26%. Maria will not pay taxes at the 26% rate on the whole $115,000 but will pay a different tax rate for each level of her income based on the federal income tax brackets.

Note: The tax brackets are not to scale. The tax rates are updated every year.

When Maria does her taxes, the federal taxes she owes on her income are calculated like this:

- Maria is taxed at 14.5% rate on the first $57,375.

- 14.5% ×multiplied by $57,375 =equals $8,319

- Maria is taxed at 20.5% rate for the income between $57,375 and $114,750.

- 20.5% ×multiplied by ($114,750 −minus $57,375) =equals $11,762

- Maria is taxed at 26% rate for the income between $114,750 and $115,000.

- 26% ×multiplied by ($115,000 −minus $114,750) =equals $65

- Maria calculates the total federal taxes on her $115,000 taxable income by adding the

results from calculations 1 to 3.

- $8,319 +plus $11,762 +plus $65 =equals $20,146

Both Giovanni and Maria have calculated only the first part of the net federal tax calculation. The amounts calculated here will be reduced as the process continues.

Calculating your taxes (part 7 of 7)

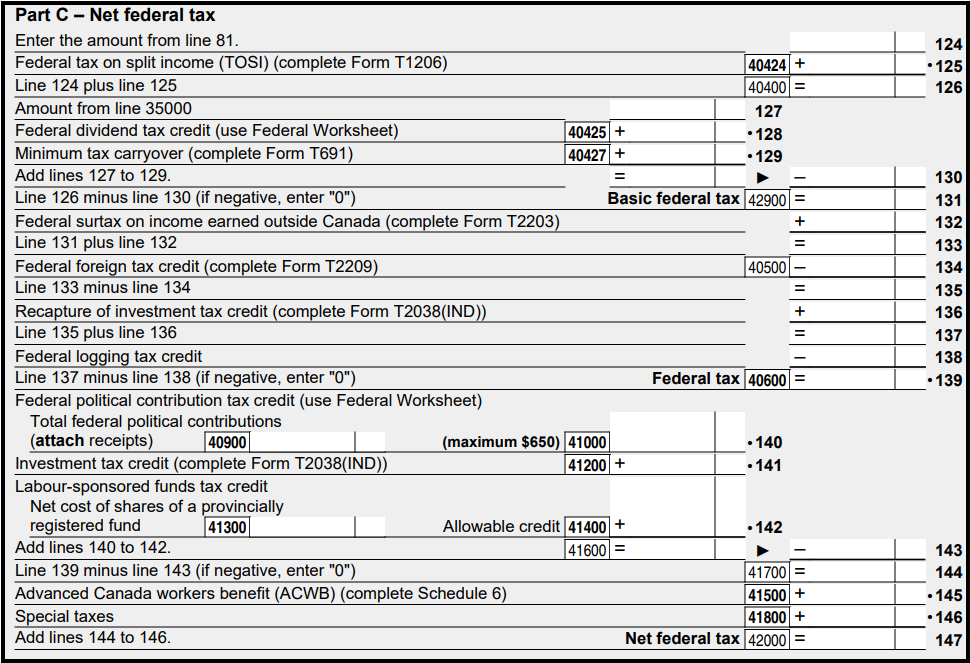

Entering tax calculations on your tax return

If you are using certified tax software, the software may use information you previously entered and ask you additional questions to calculate your net federal and your net provincial or territorial tax. The software will fill out the correct federal and provincial or territorial forms (the tax return itself and any schedules).

Schedule

- Schedule

Test yourself

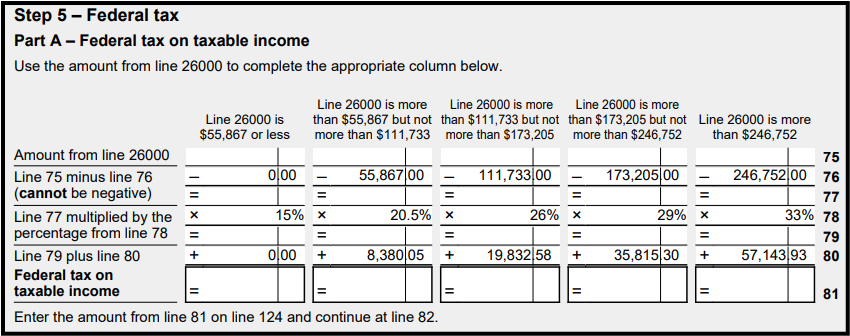

Below is an example of what the federal tax calculation looks like on the tax return:

Example

Is this form hard to read? Don't worry, we will provide you with a link to the PDF (hi-res) version after this lesson.

Is this form hard to read? Don't worry, we will provide you with a link to the PDF (hi-res) version after this lesson.

Resources are available

After you finish this lesson, this resource link will be available:

- Get a T1 income tax package

Finding out if you get a refund or owe tax

After calculating your taxes, you will find out if you get a refund or have a balance owing.

Time to complete: about 10 minutes

This lesson includes

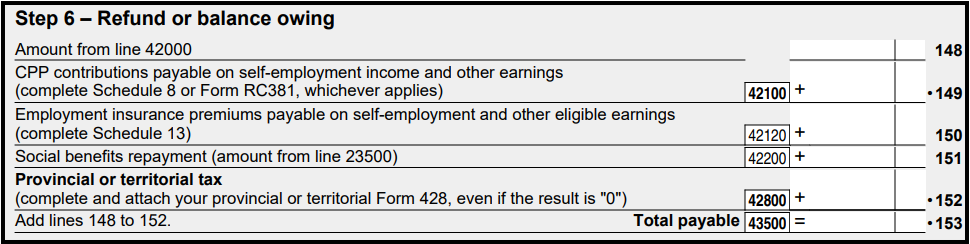

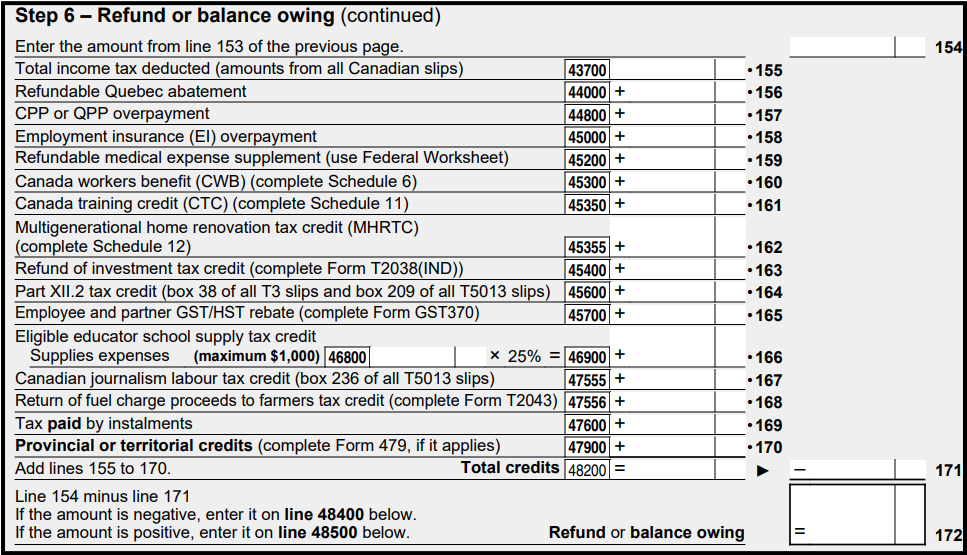

Finding out if you get a refund or owe tax (part 5 of 5)

Calculating a refund or balance owing on your tax return

If you are using certified tax software, it may use information you previously entered to calculate your total payable and your total credits. For example, it calculated the taxes you owe in previous steps based on your taxable income and the non-refundable tax credits you claimed.

Taxable income

- Taxable income

If the certified tax software needs any extra information to complete a calculation or another form, it may ask you more questions based on the required form.

Once the certified tax software has finalized the amounts, it subtracts your total credits from your total payable:

- If the result is negative (below zero), you are entitled to a refund for the difference.

- If the result is positive (above zero), you have a balance owing for the difference.

Test yourself

It is your responsibility to make sure that you review the information you have entered into the certified tax software before you submit your tax return to the CRA. For example, if you worked for 2 employers during the year, you want to check that the income tax deducted found on both T4 slips is shown on the correct line.

Below is an example of what the calculation of a refund or balance owing looks like on the tax return:

Example

Is this form hard to read? Don't worry, we will provide you with a link to the PDF (hi-res) version after this lesson.

Is this form hard to read? Don't worry, we will provide you with a link to the PDF (hi-res) version after this lesson.

Resources are available

After you finish this lesson, this resource link will be available:

- Get a T1 income tax package

Quiz: Completing a basic tax return

Take the quiz after you’ve finished all the lessons for: Completing a basic tax return.

Show the quiz: Completing a basic tax return Hide the quiz: Completing a basic tax return

Your quiz results:

- You answered 0 out of 11 questions correctly

Exercises

There are exercises available to test yourself on completing a basic tax return.